Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

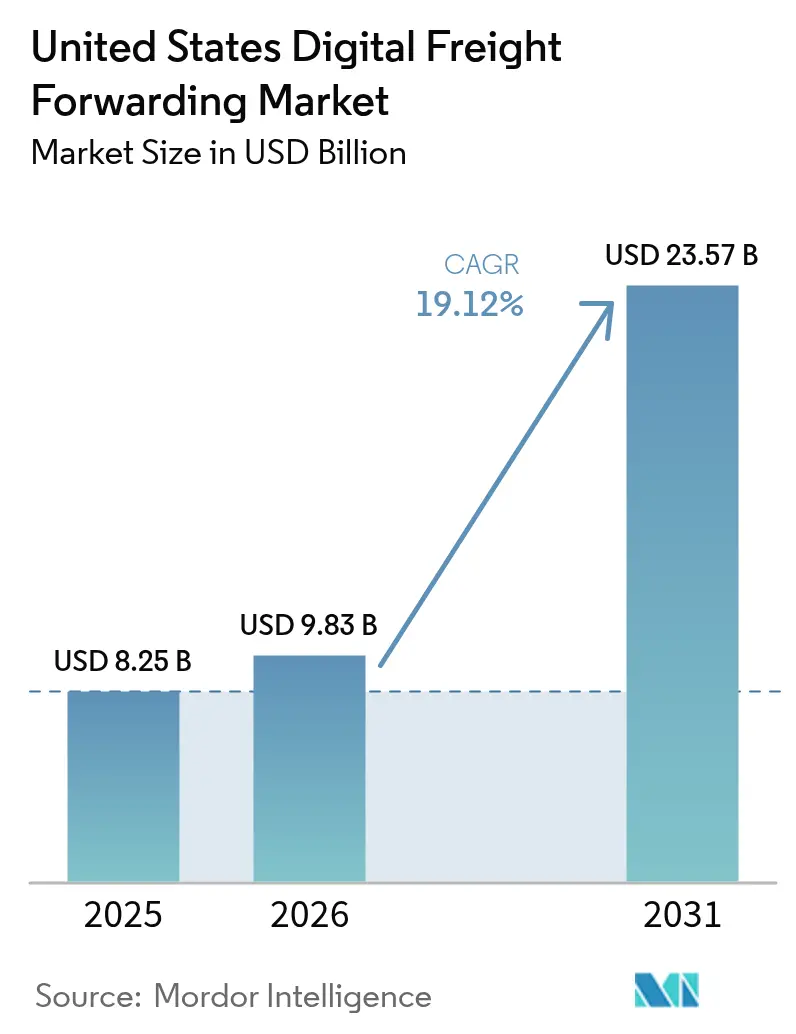

| Base Year Market Size (2025) | USD 8.25 Billion |

| Market Size (2026) | USD 9.83 Billion |

| Market Size (2031) | USD 23.57 Billion |

| Growth Rate (2026 - 2031) | 19.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Digital Freight Forwarding Market Analysis by Mordor Intelligence

The United States Digital Freight Forwarding Market size was valued at USD 8.25 billion in 2025 and estimated to grow from USD 9.83 billion in 2026 to reach USD 23.57 billion by 2031, at a CAGR of 19.12% during the forecast period (2026-2031).

Escalating e-commerce parcel volumes, rapid near-shoring to Mexico, and the rollout of the Automated Commercial Environment (ACE) have placed real-time visibility, automated customs clearance, and API-driven collaboration at the heart of the United States digital freight forwarding market. Platforms that align with new SEC cyber-incident rules by maintaining SOC-2 compliance are attracting large shippers seeking resilient data infrastructures. Meanwhile, AI-powered pricing engines are mitigating volatile ocean spot rates, and near-shoring initiatives are refashioning cross-border trade corridors, which now exceed 320,000 annual freight movements. These forces collectively unlock fresh opportunities for agile providers to streamline costs, improve shipment reliability, and deepen customer loyalty.

Key Report Takeaways

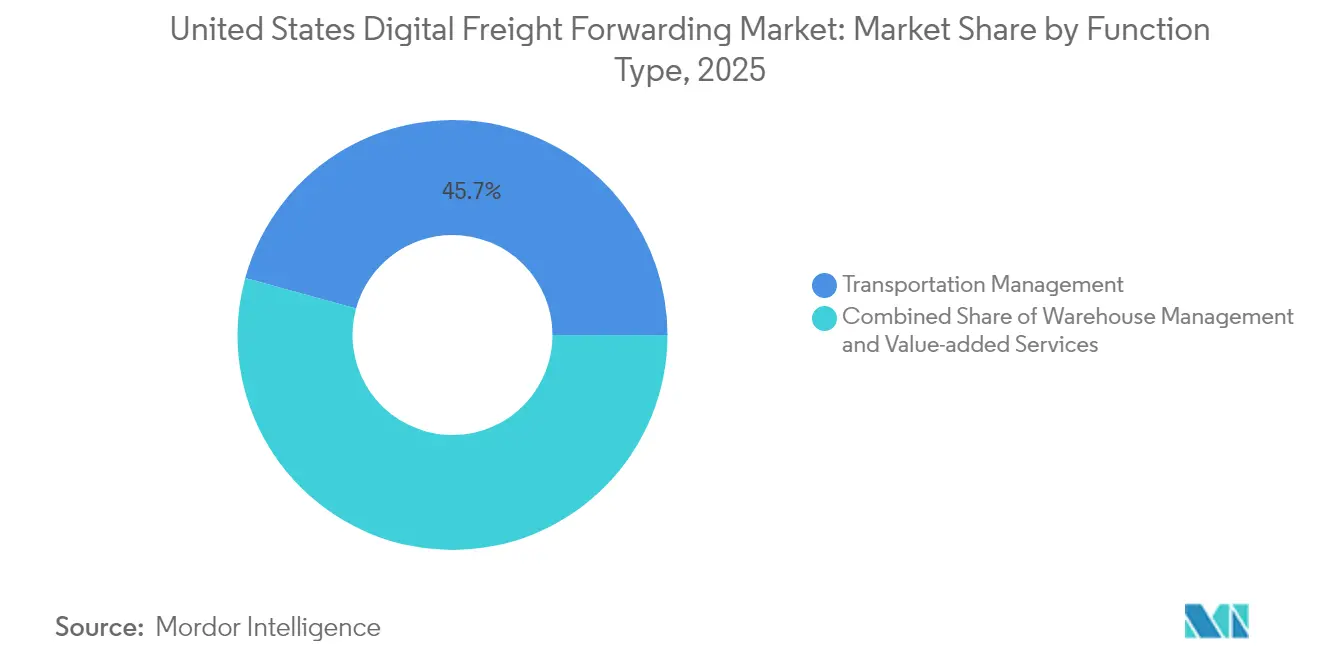

- By function, Transportation Management captured 45.72% of the United States digital freight forwarding market share in 2025, whereas Value-added Services is advancing at an 10.94% CAGR through 2031.

- By end-user, Retail & E-commerce held 36.48% of the United States digital freight forwarding market size in 2025, while Healthcare & Pharma posts the highest growth at 11.86% CAGR to 2031.

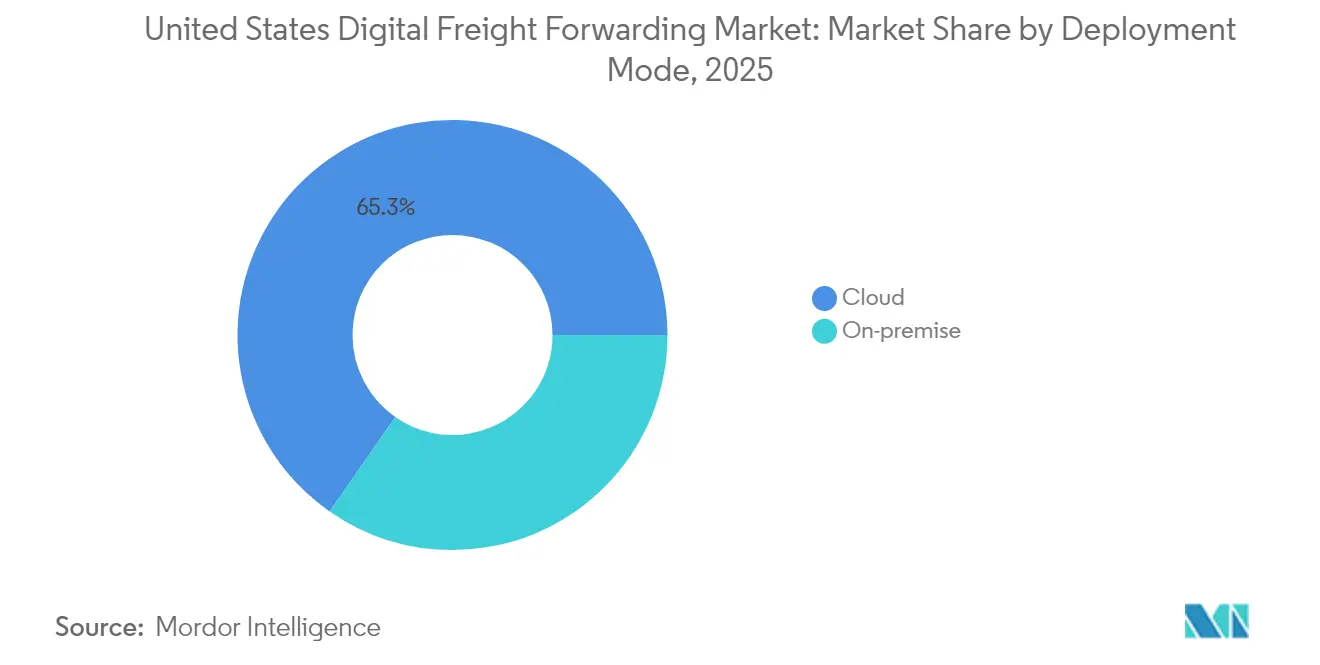

- By deployment mode, Cloud solutions dominated with 65.32% share in 2025 and are also expanding fastest at 9.98% CAGR through 2031.

- By firm type, Large Enterprises accounted for 53.22% share in 2025, whereas the SME segment is rising at 9.05% CAGR to 2031.

- By U.S. region, the West led with 28.64% share in 2025; the South registers the fastest growth at 15.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Digital Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom driving small-parcel import volumes | +3.2% | National; West & Northeast focus | Medium term (2-4 years) |

| Demand for end-to-end shipment visibility & real-time analytics | +2.8% | National; early in West & South | Short term (≤ 2 years) |

| Digitized customs clearance via ACE & USMCA reduces dwell time | +2.1% | Border states; expanding nationwide | Long term (≥ 4 years) |

| SEC cyber-incident rules push SOC-2-compliant platforms | +1.9% | National; large enterprises | Medium term (2-4 years) |

| Near-shoring to Mexico spurs cross-border digital corridors | +3.4% | South & West | Long term (≥ 4 years) |

| Softening cyber-insurance rates unlock mid-market adoption | +1.8% | National; SME focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom Driving Small-Parcel Import Volumes

U.S. e-commerce reached USD 833.8 billion in 2024, representing 15.5% of total retail, and cross-border parcels already account for 5% of that value. Parcel volumes are projected to hit 29 billion by 2029 at a 5% CAGR, flooding last-mile networks and forcing a shift toward high-velocity, low-value shipment orchestration. Digital freight forwarders are embedding automated customs algorithms and AI route optimization to manage thousands of daily entries under Entry Type 86. Real-time retail expectations compel carriers to deliver low-cost two-day shipping, intensifying pressure on traditional forwarders to digitize. Companies lacking these capabilities risk losing share in the United States digital freight forwarding market to technology-native rivals capable of processing small-parcel data at scale[1]“ACE and Automated Systems,” U.S. Customs and Border Protection, cbp.gov.

Demand for End-to-End Shipment Visibility and Real-Time Analytics

Only 20% of forwarders had comprehensive visibility in place by 2024, yet shippers increasingly rank reliability above pure speed. IoT sensors, cloud dashboards, and predictive analytics are replacing manual status emails, enabling proactive exception management. McKinsey notes 90% of U.S. consumers still prioritize cost, but on-time delivery remains mandatory. Uber Freight’s generative-AI platform illustrates the payoff: 24 million loads processed annually with dynamic ETA predictions and alternative routing suggestions. This capability increasingly differentiates providers as shippers demand data-rich service.

Digitized Customs Clearance via ACE and USMCA Reduces Dwell Time

CBP’s ACE modernization now automates cargo detention notices and prompts mandatory ACE IDs, cutting paperwork and port dwell time. USMCA provisions, including the Entry Type 86 de-minimis threshold, allow goods valued under USD 800 to clear faster, further lifting the United States digital freight forwarding market. Digital forwarders integrate ACE APIs with routing engines to supply real-time compliance checks, minimizing human error. As processing bottlenecks shrink, border throughput climbs, drawing more shippers toward API-ready platforms[2]“2024 WMS Software Report,” STIQ, stiqreport.com.

Near-shoring to Mexico Spurs Cross-Border Digital Corridors

Mexico overtook China as the United States’ top trading partner in 2024, posting USD 475.6 billion in bilateral trade. Foreign direct investment into Mexico is forecast to exceed USD 60 billion by 2027, underpinning 450 new factories along the border. Container flows from China to Mexico jumped 59.7% in January 2024 and another 26.2% by July, underscoring the pivot. Digital freight forwarders are embedding Carta Porte invoice modules, multi-modal tracking, and AI-powered ETA engines to orchestrate cross-border moves in near real time. These capabilities shorten clearance windows, enhance compliance, and strengthen shipper confidence in the United States digital freight forwarding market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented carrier base slows API onboarding | -2.1% | National; fragmented regions | Medium term (2-4 years) |

| Volatile ocean spot rates hamper instant quoting accuracy | -1.8% | Coastal, import-heavy | Short term (≤ 2 years) |

| Ransomware incidents disrupt logistics tech platforms | -1.4% | National; tech-centric regions | Short term (≤ 2 years) |

| Rising trucking insurance premiums inflate brokerage costs | -2.3% | National; high-risk lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Carrier Base Slows API Onboarding

The United States hosts more than 80,000 trucking carriers, many of which lack modern IT stacks, complicating platform integrations. Digital forwarders spend disproportionate resources on hybrid manual-digital workflows, delaying network scale-up. Although simplified onboarding kits and low-code API bridges help, regional disparities persist, and onboarding timelines lengthen, reducing the attainable growth rate for the United States digital freight forwarding market.

Volatile Ocean Spot Rates Hamper Instant Quoting Accuracy

Global ocean pricing swung sharply in 2024-2025 as capacity imbalances and geopolitical tensions altered sailing schedules. Digital pricing engines struggle to keep quotes aligned with real-time market swings, risking margin erosion. Incumbent forwarders with long-term contracts can undercut tech-native spot quotes, dulling competitive positioning. AI-based predictive models improve accuracy but cannot fully neutralize volatility, imposing a drag on service perception.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Transportation Management Extends Digital Lead

Transportation Management accounted for a 45.72% United States digital freight forwarding market share in 2025, underscoring shippers’ priority to optimize lane selection, carrier performance, and route planning. AI algorithms now balance freight mix across land, sea, and air to reduce empty miles and cut dwell time. Real-time APIs align drivers, warehouses, and customs brokers, enabling platforms to automate tendering across more than 400,000 U.S. truck drivers. This efficiency lets forwarders process high-velocity retail imports while sustaining service quality.

Value-added Services record the fastest 10.94% CAGR as shippers demand consolidated dashboards that blend customs brokerage, insurance, and trade-compliance analytics. Machine-learning models read commercial invoices, identify duty-savings opportunities, and suggest alternative Incoterms. The converging feature set encourages shippers to favor unified platforms, deepening revenue per account and amplifying scale within the United States digital freight forwarding market.

By End-users: Retail and E-commerce Remain Anchor Vertical

Retail & E-commerce captured 36.48% of the United States digital freight forwarding market size in 2025, fueled by 15.5% online retail penetration and the surge of low-value parcel imports. Omnichannel retailers integrate order-management systems with digital forwarder APIs to orchestrate store replenishment and consumer deliveries through a single interface. Reverse-logistics workflows also gain traction as return rates average 16% in apparel.

Healthcare & Pharma exhibit the highest 11.86% CAGR through 2031, reflecting strict temperature-control and traceability needs. FedEx’s sustainable aviation-fuel rollout and AI-enabled cold-chain insights illustrate demand for specialized lanes. Digital forwarders leverage sensor-laden packaging and regulatory-compliant data vaults to win contracts for time-sensitive biologics shipments.

By Deployment Mode: Cloud Platforms Drive Scalability

Cloud deployments claimed 65.32% share and continue to outpace on-premise systems at 9.98% CAGR DHL.COM. Multitenant architectures slash IT overhead and grant SMEs access to enterprise-grade modules through subscription models. Continuous integration pipelines ship new features weekly, such as AI fraud-detection and automated detention-fee tracking, bolstering stickiness.

On-premise remains a niche for heavily regulated shippers and government entities requiring air-gapped environments. Even here, hybrid solutions pipe sanitized data to the cloud for analytics while preserving local control, reinforcing the United States digital freight forwarding market’s migration toward flexible architectures.

By Firm Type: Large Enterprises Anchor Revenue, SMEs Accelerate Adoption

Large Enterprises provide 53.22% of platform revenue, leveraging complex global supply chains and higher freight spend that justify enterprise licenses. Their multi-modal tendering needs push vendors to integrate air, ocean, rail, and parcel modules into one pane of glass, while SOC-2 and ISO 27001 certifications remain non-negotiable.

SMEs grow at 9.05% CAGR as falling cyber-insurance premiums and low-code onboarding tools lower barriers. Vendors package best-practice workflows and embedded compliance checks to offset limited in-house expertise. These network effects attract more carriers, enriching rate options and fueling virtuous-cycle growth for the United States digital freight forwarding market.

Geography Analysis

The West accounts for 28.64% of the United States digital freight forwarding market, anchored by ports of Los Angeles and Long Beach, which move roughly 40% of U.S. container imports. Technology companies headquartered in California co-create APIs and beta-test machine-learning modules, accelerating commercial adoption. Persistent cybersecurity risks 40 million monthly attacks at the Port of Los Angeles make robust encryption and zero-trust frameworks table stakes for providers.

The South records the fastest 15.21% CAGR as Mexico became America’s top trading partner, driving 20,900 monthly truck crossings through Texas alone. Near-shored automotive and electronics plants rely on Carta Porte-compliant document flows and multi-modal coordination. Florida’s emergence as a hub for Latin American trade further widens regional demand for bilingual brokerage services and tariff-classification engines.

Northeast and Midwest corridors maintain steady growth. The Northeast benefits from pharmaceutical imports through Port NY/NJ and heightened e-commerce activity, while the Midwest’s automotive belt digitizes logistics to support EV battery supply chains. Investments such as Norfolk Southern’s USD 1 billion systemwide upgrades including five digital train-inspection portals enhance rail-based freight visibility. Together, these advances reinforce nationwide momentum in the United States digital freight forwarding market.

Competitive Landscape

The competitive field remains moderately fragmented even as consolidation accelerates. DSV’s EUR 14.3 billion (USD 15.78 billion) acquisition of Schenker closed in April 2025, birthing a 160,000-employee powerhouse forecasting DKK 9.0 billion (USD 1.33 billion) in annual synergies by 2028 DSV.COM. Traditional incumbents simultaneously revamp internal tech stacks; C.H. Robinson’s ACE-integrated platform now pushes real-time compliance alerts. Pure-play digital entrants such as Flexport deploy micro-services to interface seamlessly with shipper ERPs, while Uber Freight’s generative-AI tools automate tendering and lane forecasting across USD 20 billion in managed freight.

Strategic playbooks cluster into three groups. Legacy giants acquire assets to achieve end-to-end digital depth; tech-natives double-down on vertical specializations like cold chain; and orchestrator platforms aggregate niche providers via open APIs, offering modular value. White-space persists in healthcare logistics, where FDA compliance deters smaller entrants, and in cross-border e-commerce, where customs variability rewards algorithmic classification engines. As AI-driven pricing matures and cyber resilience becomes table stakes, competitive advantage hinges on data science talent, carrier network density, and the breadth of embedded value-added modules in the United States digital freight forwarding market.

United States Digital Freight Forwarding Industry Leaders

Flexport

Uber Freight

Convoy

C.H. Robinson (Navisphere)

Loadsmart

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Flexport divested the Convoy technology platform to DAT Freight & Analytics for USD 250 million, expanding DAT’s digital toolkit at zero upfront cost to users.

- May 2025: Uber Freight upgraded its AI suite, now managing USD 20 billion in freight volume and 24 million loads yearly.

- April 2025: DSV completed its acquisition of DB Schenker for roughly DKK 106.7 billion (USD 15.79 billion), targeting DKK 9.0 billion (USD 1.33 billion) in annual synergies and reshaping global market rankings.

- February 2025: Flexport relaunched the Convoy platform, connecting 400,000 drivers and 80,000 carriers through a unified digital network.

United States Digital Freight Forwarding Market Report Scope

Digital freight forwarders use digital tools that help smooth communication flow and quickly get status updates regarding any shipment. Digital freight forwarder employs a completely transparent system that compares various shippers to offer the best deal to the customers.

A complete background analysis of the US digital freight forwarding market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report. The US digital freight forwarding market is segmented by mode of transportation (ocean, air, and land) and by firm type (SMEs and large enterprises and governments). The report offers market size and forecasts for the US digital freight forwarding market in value (USD billion) for all the above segments.

By Function

| Transportation Management | Land |

| Sea | |

| Air | |

| Warehouse Management | |

| Value-added Services |

By End-users

| Retail and E-commerce |

| Manufacturing |

| Healthcare and Pharma |

| Automotive |

| Others |

By Deployment Mode

| Cloud |

| On-premise |

By Firm Type

| SMEs |

| Large Enterprises and Government Entities |

By US Region

| Northeast |

| Midwest |

| South |

| West |

| By Function | Transportation Management | Land |

| Sea | ||

| Air | ||

| Warehouse Management | ||

| Value-added Services | ||

| By End-users | Retail and E-commerce | |

| Manufacturing | ||

| Healthcare and Pharma | ||

| Automotive | ||

| Others | ||

| By Deployment Mode | Cloud | |

| On-premise | ||

| By Firm Type | SMEs | |

| Large Enterprises and Government Entities | ||

| By US Region | Northeast | |

| Midwest | ||

| South | ||

| West |

Key Questions Answered in the Report

How large is the United States digital freight forwarding market in 2026?

The United States digital freight forwarding market size stands at USD 9.83 billion in 2026 and is set to grow rapidly at a 19.12% CAGR to 2031.

Which segment holds the largest market share by function?

Transportation Management leads with a 45.72% share, reflecting shipper focus on optimized routing and carrier coordination.

Why is the South region growing faster than other U.S. regions?

Near-shoring to Mexico and increased cross-border trade are propelling the South to a 15.21% CAGR through 2031.

What role does cloud deployment play in digital freight forwarding?

Cloud solutions account for 65.32% of deployments, offering scalable, subscription-based access to advanced analytics and real-time visibility.

How are AI tools reshaping freight forwarding operations?

AI supports predictive pricing, real-time ETA forecasting, and automated exception handling, enabling platforms such as Uber Freight to process 24 million loads annually.

Which end-user vertical is expanding fastest?

Healthcare & Pharma is the fastest‐growing end-user segment with a 11.86% CAGR, driven by stringent compliance and cold-chain needs.

Page last updated on: