Surge Protection Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

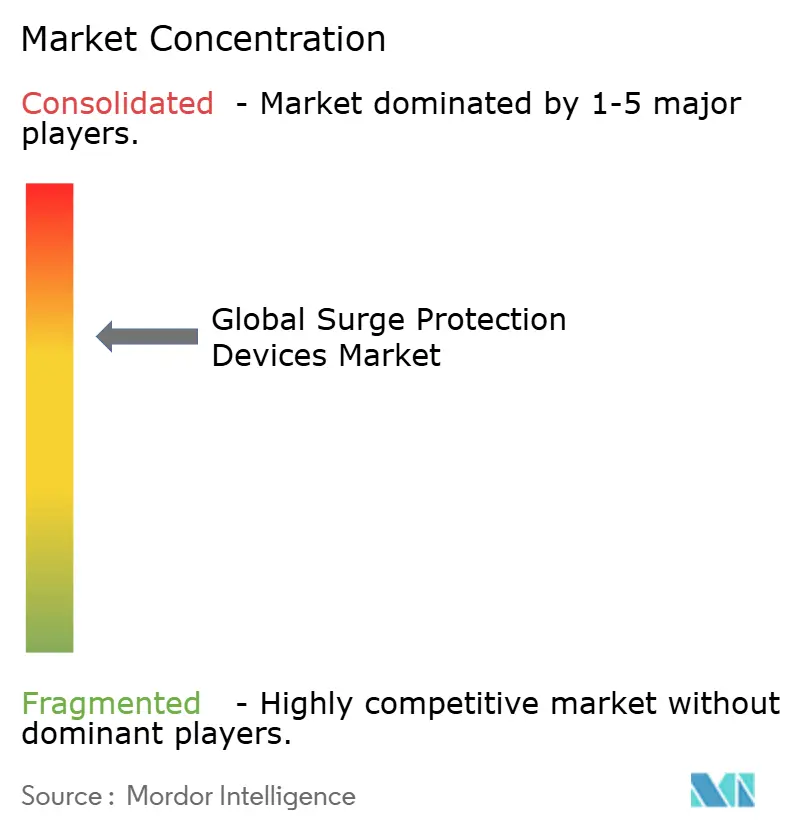

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surge Protection Devices Market Analysis by Mordor Intelligence

The surge protection devices market size in 2026 is estimated at USD 3.01 billion, growing from 2025 value of USD 2.86 billion with 2031 projections showing USD 3.87 billion, growing at 5.18% CAGR over 2026-2031. Solid growth reflects the rising importance of safeguarding sensitive electronics as global power-quality issues intensify. Adoption is accelerating across industrial plants, commercial buildings, and homes as managers weigh the high cost of downtime, repair, and data loss against modest preventive investments. North America’s leadership stems from stringent electrical-safety codes and the region’s extensive data-center footprint, while Asia-Pacific is gaining momentum on the back of rapid industrialization, large-scale infrastructure projects, and expanding renewable-energy capacity. Medium-voltage devices dominate because most industrial power-distribution networks fall into the 1-35 kV band, and industrial users remain the largest buyers as unplanned outages translate directly into production losses. Technology upgrades are reshaping the surge protection devices market, with connected hardware, analytics-powered predictive maintenance, and higher-capacity designs addressing rising loads in AI data centers and EV-charging hubs.

Key Report Takeaways

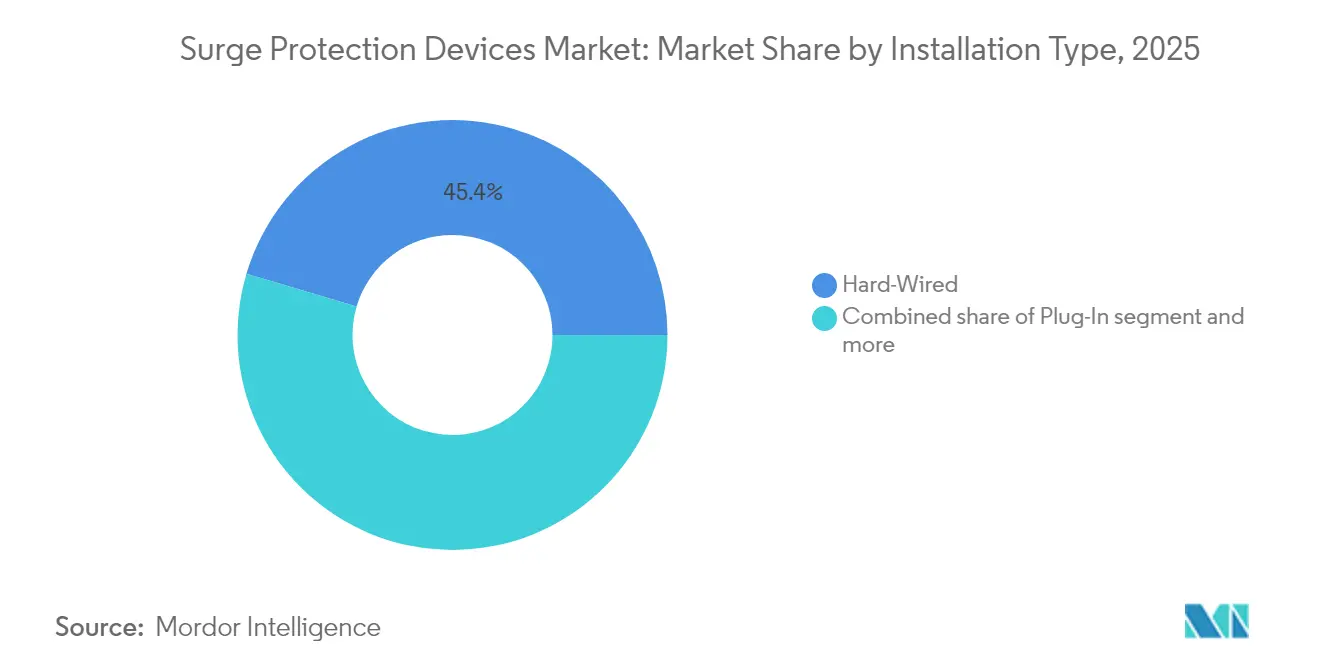

- By installation type, hard-wired devices led with 45.40% of the surge protection devices market share in 2025; the plug-in segment is projected to advance at a 6.05% CAGR through 2031.

- By discharge-current rating, the 10 kA-25 kA class held 51.30% of the surge protection devices market size in 2025, while above-25 kA units are set to grow fastest at 6.32% CAGR between 2026-2031.

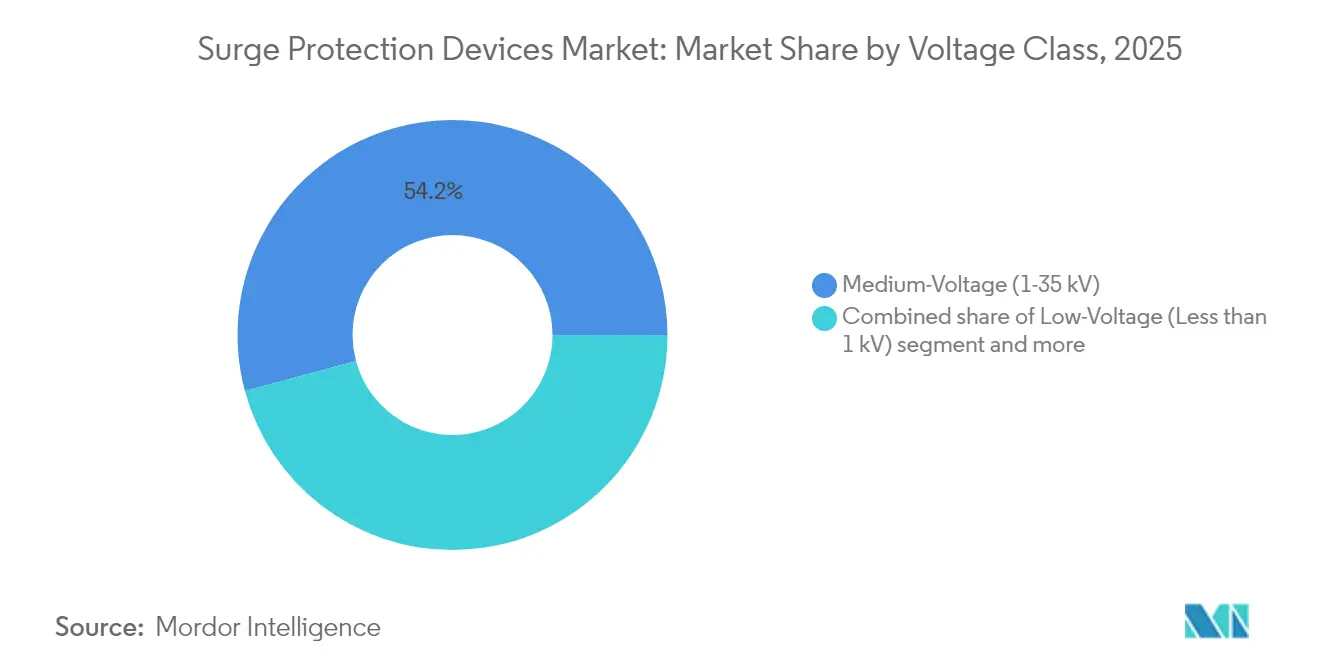

- By voltage class, medium-voltage (1-35 kV) products accounted for 54.20% of 2025 revenue; high-voltage devices are forecast to expand at a 5.62% CAGR to 2031.

- By end-user, industrial facilities captured 64.10% of revenue in 2025; the commercial segment is poised for the quickest rise with a 6.12% CAGR to 2031.

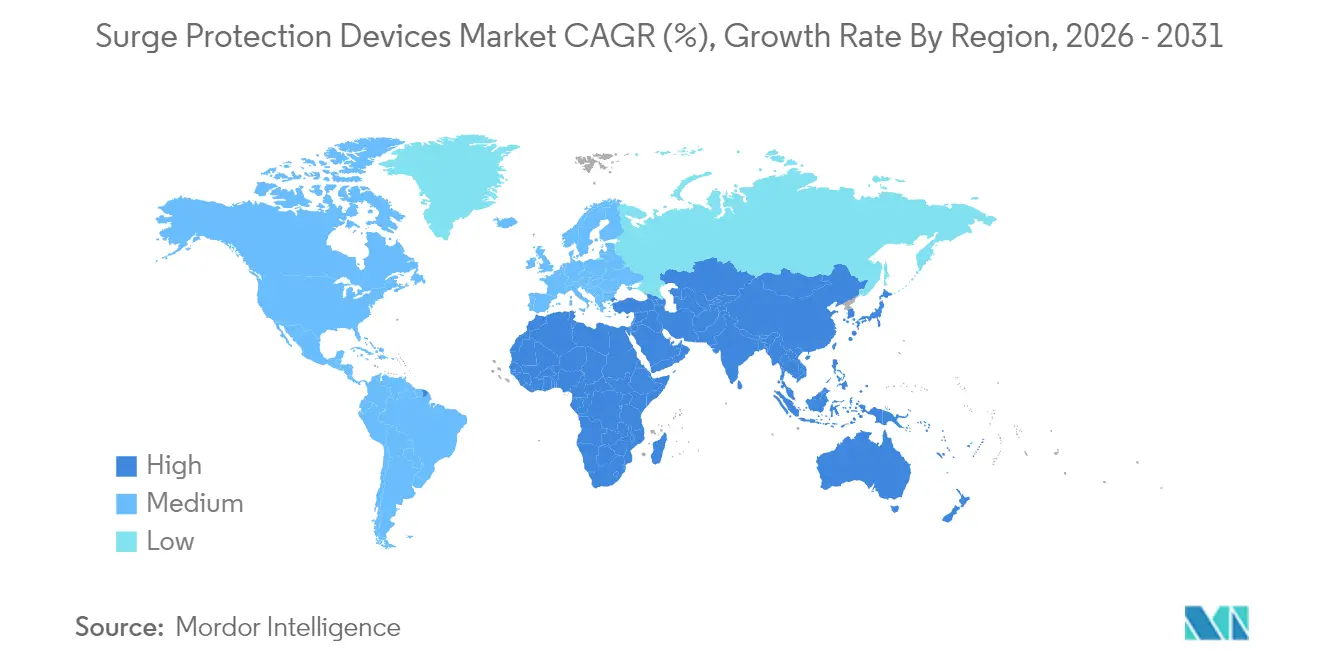

- By region, North America generated 39.60% of 2025 turnover; Asia-Pacific is the fastest-growing geography with a 5.98% CAGR expected for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surge Protection Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-home and IoT adoption | +1.3% | North America, Europe; growing globally | Medium term (2-4 years) |

| Grid instability from renewables | +0.9% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Surging data-center and telecom power density | +1.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| EV-charging mandates for service-entrance SPD | +0.8% | North America, Europe, China | Medium term (2-4 years) |

| Insurance incentives for SPD installation | +1.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of smart-home and IoT devices

Smart-home ecosystems now often hold electronics worth more than USD 15,000, exposing households to material financial risk when surges occur. Microprocessors in connected lighting, appliances, and security systems are highly sensitive to voltage transients, and a surge harming one node can propagate through the network. Whole-house[1]DTE Energy, “Whole Home Surge Protection Program,” dteenergy.com surge protection therefore is replacing point-of-use strips, and manufacturers are bundling power-line and data-line protection in a single enclosure to simplify installation. Insurance carriers reinforce this trend by lowering premiums for protected homes, boosting demand in the residential segment. Growing familiarity with home-automation platforms further widens the audience for feature-rich but easy-to-install plug-in SPDs that sync with mobile apps for status alerts.

Growing grid-instability from renewables integration

Wind and solar are projected to supply over 40% of global generation by 2030, yet inverter-based resources lack the high fault currents required by traditional protective relays. As utilities cycle generation to match variable output, switching-induced transients become more frequent, challenging legacy protection schemes. Digital relays and data-driven arc-flash controls are gaining favor, creating demand for surge devices that perform reliably across wider voltage envelopes and fluctuating waveforms. Innovation now centers on devices capable of handling both lightning-induced and switching-induced events, with thermal-disconnect technology protecting MOV elements from accelerated aging.

Expansion of data-center and telecom power density

AI workloads are pushing U.S. data-center demand from 25 GW in 2024 toward 80 GW by 2030[2]U.S. Department of Energy, “Data Center Energy Usage Report,” energy.gov. Operators are migrating to 400 V DC or even 800 V HVDC distribution, which trims conversion losses but raises continuous operating voltages well above standard SPD ratings. Designers, therefore, specify higher surge-current capacities and lower clamping voltages to protect deep-learning servers worth millions. Remote-monitoring capabilities embedded in rack-mounted SPDs now feed real-time health data to facility management software, enabling predictive replacement before MOV depletion threatens uptime. Telecom edge sites follow a similar trajectory as densification brings power electronics to street-level cabinets that face harsh environmental conditions.

EV-charging infrastructure mandates service-entrance SPDs

The U.S. NEVI program enforces a 97% uptime requirement, pushing owners to harden charging stations against surges. Type 2 SPDs with up to 1 kV are becoming standard at both service entrance and charger cabinet, safeguarding equipment that costs well above USD 100,000 per DC fast charger. Outdoor exposure coupled with Ethernet-based payment systems means combined power-line and data-line protection is a must. European Code IEC 60364-7-722 aligns with these requirements, creating a harmonized market for standardized SPD modules. Manufacturers are responding with compact, IP65-rated units featuring status LEDs and remote signal contacts for integration into site-management dashboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit cost in legacy facilities | -0.7% | Developed markets worldwide | Medium term (2-4 years) |

| Low awareness of hidden SPD failure rates | -0.6% | Emerging markets; global residential segment | Short term (≤ 2 years) |

| Evolving certification-scheme complexity | -0.5% | Global | Medium term (2-4 years) |

| Geopolitical shortages of MOV components | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High retrofit installation cost in legacy facilities

Installing whole-building surge protection in plants built decades ago often necessitates panelboard upgrades, conduit rerouting, or even brief shutdowns. Material costs for a commercial-grade unit run USD 300-700, and professional labor adds USD 100-200 per board, but production downtime can dwarf hardware expense. Many facilities operate on tight margins and defer upgrades until mandated by code revisions or insurance renewals. Vendors are countering with bus-mounted retrofit kits and split-core current-sensing designs that shorten installation windows, yet the perceived payback period still slows adoption, especially in mature industrial economies with aging infrastructure.

Low end-user awareness of hidden SPD failure rates

Most SPDs rely on MOVs that gradually degrade as they absorb transient energy. Once protective clamping capacity falls below a safe threshold, devices may appear operational yet deliver little defense. Typical residential surge strips last only 2-3 years, but consumers often expect a decade of service. Lack of standardized end-of-life indicators leaves users unaware of risk until equipment damage occurs. Premium products now embed thermal fuses, status relays, and app-based alerts, yet low-cost units dominate installed base volumes. Education campaigns by utilities and code bodies aim to raise awareness, but uneven global enforcement continues to slow progress.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Hard-Wired Dominates Critical Infrastructure

The hard-wired category accounted for 45.40% of 2025 revenue as facility engineers prefer devices permanently integrated into switchboards and distribution panels. This configuration offers the lowest let-through voltage, making it a default choice for production lines, cleanrooms, and data halls where uptime is paramount. Smart variants now include field-replaceable modules and web-based dashboards that simplify maintenance schedules.

Plug-in SPDs trail in share but will register the fastest CAGR at 6.05% between 2026-2031 as the smart-home boom continues. Insurance premium incentives and app-enabled power-quality analytics coax homeowners to upgrade from basic strips to networked models. The line-cord niche secures critical servers and audiovisual gear, leveraging slim enclosures and integrated RJ45 ports for combined power-and-signal defense. As code bodies widen protection mandates, hybrid devices that merge hard-wired surge modules with downstream receptacle strips are appearing in commercial buildings seeking whole-system coordination.

By Discharge-Current Rating: Medium-Capacity Devices Lead Market

Medium-capacity (10 kA-25 kA) products captured 51.30% of turnover in 2025 by balancing price and performance for office towers, retail chains, and light-industrial workshops. Manufacturers optimize component counts to keep footprints compact while meeting IEC 61643-11 Type 2 limits. This segment anchors coordinated-level approaches where service-entrance units handle high-energy events and downstream boards rely on 10 kA-25 kA modules for fine clamping.

Above-25 kA units will rise at a 6.32% CAGR through 2031, propelled by data-center rack densities that exceed 15 kW per cabinet and renewable-energy substations integrating battery storage. Continuous-operating-voltage ratings climb to 1,500 V DC in battery systems, so surge designs add wider MOV stacks and spark-gap elements. At the other end, up-to-10 kA strips protect home electronics and SOHO gear. Demand here expands steadily as consumers connect televisions, gaming consoles, and smart appliances into unified entertainment hubs that require affordable yet reliable protection.

By Voltage Class: Medium-Voltage Segment Drives Growth

Medium-voltage (1-35 kV) SPDs held a 54.20% stake in 2025, underpinning distribution transformers, switchgear, and ring-main units. Utilities employ metal-oxide arresters at feeder circuits to limit lightning impulses, while industrial plants deploy panel-mounted units to guard motor drives and control electronics. Digital substations now seek condition monitoring within surge arresters so asset managers can spot moisture ingress or resistive leakage early.

High-voltage devices (More than 35 kV) will outpace the average with a 5.62% CAGR as grid operators expand 138 kV and 230 kV corridors to connect offshore wind and solar farms. Hitachi Energy’s fluoronitrile-based gas mixtures lower greenhouse impact without sacrificing dielectric strength, signaling a sustainability shift in the surge protection devices market. Low-voltage products safeguard everything from HVAC controllers to LED lighting, and adoption rises in emerging economies where urban electrification programs prioritize appliance protection to reduce warranty claims.

By End-User Vertical: Industrial Applications Maintain Dominance

Industrial facilities generated 64.10% of 2025 sales, mirroring their exposure to costly downtime and sensitive programmable logic controllers. Process industries outfit every motor-control center with Type 2 SPDs to preserve drives and sensors that coordinate batch quality. Predictive-maintenance systems pull surge-counter data from these units, enabling reliability engineers to correlate transient events with equipment life.

Commercial buildings will grow fastest at 6.12% CAGR as data-processing loads swell in retail, banking, and healthcare. Hyperscale cloud providers lease floors in converted warehouses, all of which require coordinated surge plans. In parallel, the residential segment gains volume from premium single-family construction and smart-condominium projects that pre-install panel-board SPDs and network-connected receptacle strips. This convergence draws industrial-grade features into consumer form factors, lifting baseline quality expectations across all buyer groups.

Geography Analysis

North America contributed 39.60% of global revenue in 2025, anchored by the United States, where the National Electrical Code now mandates Type 1 or Type 2 protection for all dwelling services. Data-center expansion amplifies demand for high-capacity, service-entrance SPDs. The surge protection devices market size in Canada mirrors the U.S. trajectory as provinces adopt similar code language and utilities promote whole-home programs offering coverage up to USD 5,000 per appliance.

Asia-Pacific will post the fastest 5.98% CAGR to 2031 as manufacturing investment shifts toward India and Southeast Asia. China and Japan drive a thriving plug-in commercial segment, equipping convenience stores and micro-data centers with compact, DIN-rail SPDs. Government plans to lift renewable-energy penetration also accentuate grid-stability challenges, spurring demand for 25 kA-plus products at inverter stations. Regional OEMs partner with multinational brands to localize production, reducing lead times as construction cycles tighten.

Europe maintains a solid share thanks to tight equipment standards and aggressive decarbonization targets that remake grid topology. Germany’s Energiewende and Denmark’s offshore wind arrays entail new 66 kV export cables, each requiring line-surge arresters for voltage stabilization. Corporate sustainability goals further encourage the adoption of eco-friendly arresters that eschew SF6. Meanwhile, South America, the Middle East, and Africa represent emerging pockets where urban electrification and telecom modernization seed incremental volumes. Public-private partnerships building solar-plus-storage microgrids increasingly specify coordinated surge solutions to maximize asset uptime.

Competitive Landscape

The surge protection devices market displays moderate concentration. ABB, Eaton, Schneider Electric, and Siemens collectively hold about 70% of global revenue, leveraging expansive product portfolios, channel reach, and standards-development influence. Each firm funnels research and development into smart, connected modules that stream operational metrics to cloud dashboards. Schneider’s EcoStruxure and Eaton’s Brightlayer exemplify platforms integrating surge health within broader power-quality analytics, giving customers unified visibility over energy and protective devices.

Regional specialists fill white-space niches. Transtector focuses on harsh-environment solutions for 5G base stations, while DEHN targets renewable-energy and battery-storage applications. Delta is scaling 800 V HVDC power architectures for AI data centers that embed coordinated SPDs capable of handling elevated continuous voltages. Component innovation emphasizes low-leakage MOV chemistry and arc-quenching spark gaps to extend lifespan under frequent switching surges.

Strategic moves include technology partnerships and capacity expansions. Hitachi Energy rolled out EconiQ fluoronitrile-based high-voltage arresters, aligning sustainability positioning with utility decarbonization roadmaps. Midsize firms pursue geographic growth by aligning with local panel-board assemblers, bundling SPDs into turnkey gearsets. Price competition remains limited in high-criticality segments as buyers prioritize reliability, but commoditization is visible in residential strips, where branding and retail presence trump advanced specifications.

Surge Protection Devices Industry Leaders

ABB Ltd

Eaton Corporation, Plc.

Emersen Electric Co.

Schneider Electric Se

Littelfuse, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Delta unveiled an 800 V HVDC architecture for AI data centers that boosts efficiency by more than 4% and integrates high-capacity SPDs for rack-level protection.

- April 2025: Hitachi Energy introduced the EconiQ high-voltage portfolio using fluoronitrile gas mixtures with less than 1% of SF6’s global-warming impact, incorporating surge arresters for transmission applications.

- January 2025: Jones Lang LaSalle’s 2025 Global Data Center Outlook highlighted rising power-density constraints, fueling demand for advanced surge protection solutions in new nuclear-powered or SMR-equipped sites.

- January 2025: DEHN launched DEHNcharge T1 BATT 1500 FM for battery-storage systems and DEHNguard EZ50-S, a Type 1 NEMA 4X SPD for AC installations.

- February 2024: ABB released 273ESA-10 medium-voltage surge arresters for underground distribution, featuring fully shielded EPDM rubber housings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global surge protection device (SPD) market as the sale of purpose-built low, medium, and selected high-voltage units that restrict transient over-voltages on AC circuits in residential, commercial, and industrial premises. The devices covered are hard-wired, plug-in, and line-cord formats that carry IEC 61643 or UL 1449 conformity, and the values are recorded at original equipment manufacturer gate prices.

Scope Exclusion: Transmission-line arresters rated above 35 kV and surge-protected consumer power strips sold only as accessories do not fall within this scope.

Segmentation Overview

- By Installation Type

- Hard-Wired

- Plug-In

- Line Cord

- By Discharge-Current Rating

- Up to 10 kA

- 10 kA-25 kA

- Above 25 kA

- By Voltage Class

- Low-Voltage (Less than 1 kV)

- Medium-Voltage (1-35 kV)

- High-Voltage (More than 35 kV)

- By End-User Vertical

- Industrial

- Commercial

- Residential

- By Geography

- North America

- United States

- Canada

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with SPD manufacturers, panel builders, electrical contractors, and safety inspectors across North America, Europe, and Asia-Pacific. These conversations validate penetration ratios, discount structures, and emerging use cases, letting us reconcile secondary estimates and close information gaps quickly.

Desk Research

We begin with data from tier-one public sources, such as the International Energy Agency, the U.S. Energy Information Administration, UN Comtrade, and lightning incidence atlases, to size addressable demand and average selling prices. Regulatory updates from NFPA, IEC committees, and national electrical authorities clarify safety-code driven replacement cycles. Company 10-Ks, earnings calls, and tender portals enrich shipment and pricing patterns, while D & B Hoovers and Dow Jones Factiva give our analysts revenue splits that anchor the industrial segments. The sources cited are illustrative; many more open datasets are reviewed to cross-verify trends.

Market-Sizing & Forecasting

Top-down modeling links new housing completions, data-center megawatt additions, EV-charging point roll-outs, lightning-day statistics, and regional construction GDP with device penetration rates. Then, a selective bottom-up roll-up of supplier revenues checks totals and flags anomalies. Multivariate regression, vetted through scenario analysis, projects values to 2030, and missing inputs are bridged by nearest-neighbor benchmarks with similar grid reliability profiles.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance filters against trade code data, and a peer audit before sign-off. Our team refreshes every twelve months, with interim updates when major code revisions, material price swings, or large capacity announcements emerge.

Why Mordor's Surge Protection Devices Baseline Earns Investor Trust

Published estimates frequently diverge because firms mix differing product classes, price references, and refresh cadences. By locking scope to true SPDs and updating models each year, we deliver numbers that mirror on-ground dynamics.

Key gap drivers observed elsewhere include inclusion of smart strips or very high-voltage arresters, reliance on list prices without channel discounts, and straight-line CAGR extensions that ignore post-pandemic housing resets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.86 B (2025) | Mordor Intelligence | - |

| USD 2.98 B (2025) | Global Consultancy A | Uses distributor resale values and folds Type 4 power strips |

| USD 3.60 B (2024) | Industry Journal B | Counts transmission-line arresters and holds ASPs constant at 2023 levels |

The comparison shows our figure sits between expansive and optimistic counts, giving decision-makers a balanced, transparent baseline that flows from clearly stated devices, data series, and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the surge protection devices market by 2031?

The market is expected to reach USD 3.87 billion by 2031, expanding at a 5.18% CAGR from 2026.

Which installation type is growing fastest?

Plug-in surge protectors are forecast to post a 6.05% CAGR through 2031 as smart-home uptake and insurance incentives fuel residential demand.

Why are high-voltage SPDs gaining attention?

Utility transmission upgrades for large-scale renewables require devices above 35 kV, and eco-friendly gas alternatives such as fluoronitrile are driving new product launches.

How do data centers influence surge protection demand?

AI workloads push power density dramatically higher, prompting facilities to adopt 25 kA-plus SPDs and shift toward 400 V DC or 800 V HVDC architectures with specialized protection.

What role do insurance programs play?

Utilities and insurers offer premium discounts or coverage guarantees—up to USD 5,000 for appliances in some U.S. programs—encouraging homeowners and small businesses to install whole-home SPDs.

How often should surge protection devices be replaced?

Residential strips typically last 2–3 years under normal conditions; industrial units include surge counters and status relays so maintenance teams can replace modules once MOV energy-absorption capacity is exhausted.

Page last updated on: