MEA AI, Cybersecurity and Big Data Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

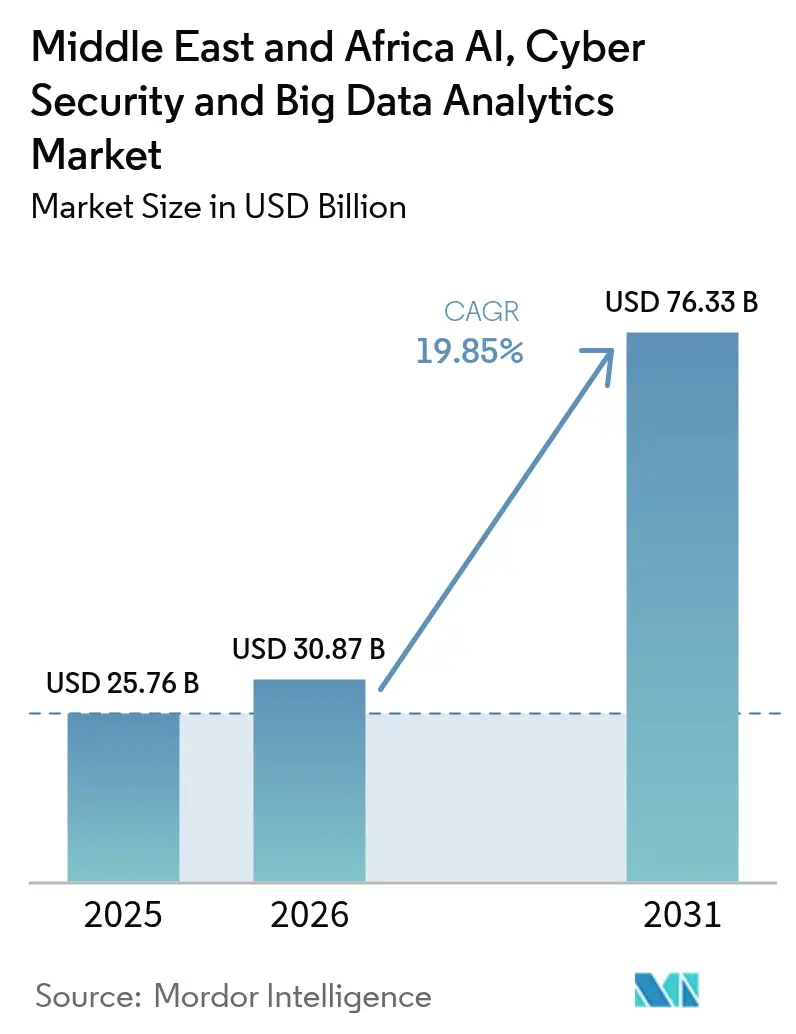

| Base Year Market Size (2025) | USD 25.76 Billion |

| Market Size (2026) | USD 30.87 Billion |

| Market Size (2031) | USD 76.33 Billion |

| Growth Rate (2026 - 2031) | 19.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEA AI, Cybersecurity and Big Data Analytics Market Analysis by Mordor Intelligence

The Middle East and Africa AI, Cybersecurity, and Big Data Analytics market size was valued at USD 25.76 billion in 2025 and estimated to grow from USD 30.87 billion in 2026 to reach USD 76.33 billion by 2031, at a CAGR of 19.85% during the forecast period (2026-2031). Intensifying sovereign AI funds, mandatory data-localization laws, and rapid public-sector cloud adoption jointly expand addressable demand while heightening the need for integrated threat-intelligence and analytics capabilities. Established vendors deepen footprints through hyperscale facilities and GPU-as-a-Service partnerships, whereas local specialists focus on Arabic language models that remedy historical content under-representation and ensure data sovereignty compliance. The Middle East and Africa AI, Cybersecurity, and Big Data Analytics market, therefore, benefits from synchronized technology upgrades and policy mandates, even as talent shortages and silicon supply constraints temper near-term deployment velocity.

Key Report Takeaways

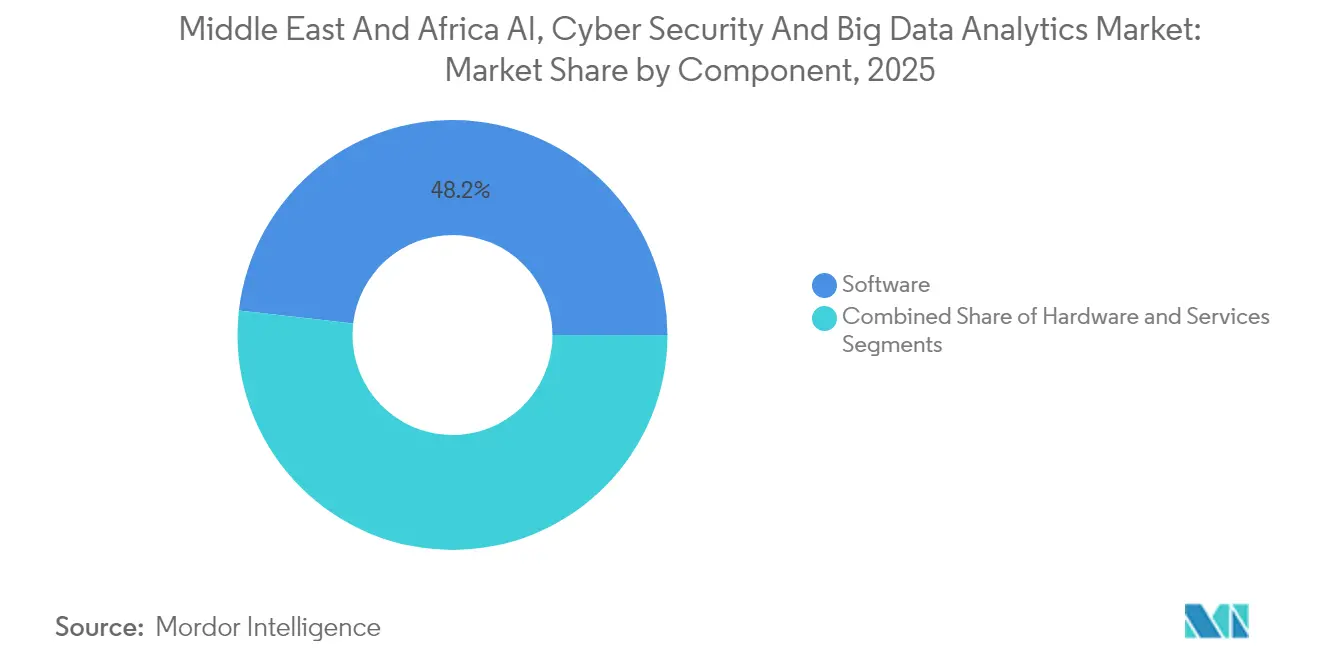

- By component, software captured 48.18% of 2025 revenue, while services are forecast to expand at a 21.78% CAGR to 2031, the strongest acceleration within the component mix.

- By security type, network security led with a 28.55% share of the Middle East and Africa AI, Cybersecurity, and Big Data Analytics market size in 2025; cloud security is poised to grow at a 20.92% CAGR through 2031.

- By analytics type, advanced/predictive analytics commanded a 51.95% share of the Middle East and Africa AI, Cybersecurity, and Big Data Analytics market size in 2025, whereas real-time streaming analytics will progress at a 23.05% CAGR.

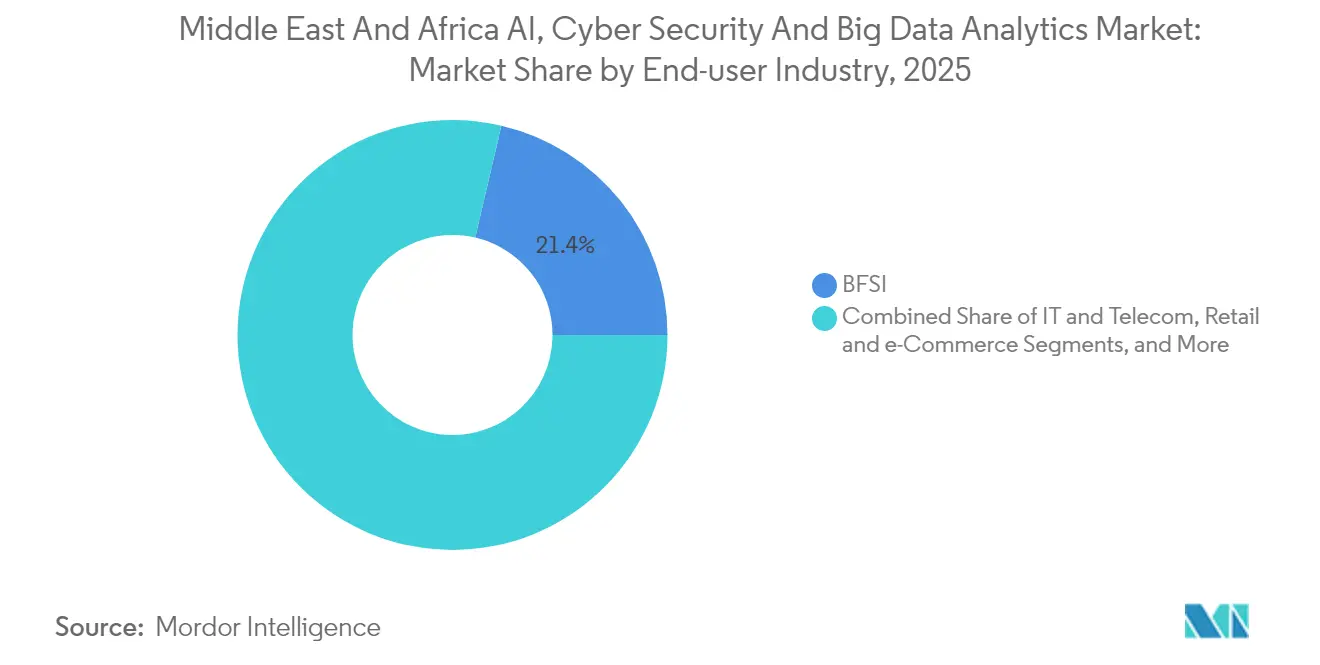

- By end-user industry, BFSI held 21.35% of 2025 revenue, but healthcare and life sciences are projected to log the fastest 23.62% CAGR to 2031.

- By end-user enterprise size, large enterprises accounted for 67.90% of 2025 spending, yet SMEs are forecast to advance at a 22.05% CAGR as cloud-native platforms lower entry barriers.

- By geography, Saudi Arabia led with a 25.90% share of 2025 spending, while the UAE is set to record a 22.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MEA AI, Cybersecurity and Big Data Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding sovereign AI funds across the GCC | +4.2% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Accelerated cloud-first mandates in the public sector | +3.8% | Global, with early gains in the UAE, Saudi Arabia | Short term (≤ 2 years) |

| Retail and BFSI race for hyper-personalized CX | +3.1% | Global | Medium term (2-4 years) |

| 5G-IoT proliferation fueling edge analytics demand | +2.9% | GCC core, spill-over to MEA | Long term (≥ 4 years) |

| Mandatory data-localization and cyber-resilience regulations | +2.7% | MENA core, expanding to Africa | Short term (≤ 2 years) |

| Rise of GenAI-powered Arabic large language models | +2.4% | Arabic-speaking regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding sovereign AI funds across the GCC transforms regional innovation

GCC sovereign wealth vehicles quintupled AI allocations during 2024-25, exemplified by Abu Dhabi’s MGX targeting USD 100 billion for AI infrastructure and Saudi Arabia’s Public Investment Fund earmarking USD 40 billion for venture partnerships [1]Bloomberg News, “Abu Dhabi Targets $100 Billion AUM for AI Investment Firm MGX,” bloomberg.com. Investment prioritizes domestic model training, data-center capacity, and Arabic-centric language research, creating local vendor ecosystems able to serve 350 million Arabic speakers with culturally relevant solutions. Sovereign capital also crowds in foreign partners through joint ventures that accelerate technology transfer while ensuring data residency compliance.

Accelerated cloud-first mandates drive public-sector digital transformation

Saudi Arabia’s DEEM program consolidated 175 data centers across 237 entities and saved USD 1.33 billion, showcasing the fiscal and operational gains of mandatory cloud adoption. Parallel initiatives in the UAE and Qatar mandate migration of government workloads to local hyperscale regions, prompting a surge in procurement for zero-trust controls, cloud access security brokers, and automated compliance management.

Retail and BFSI race for hyper-personalized CX

Banks account for a majority of regional security outlays as open-banking APIs multiply attack surfaces and boost demand for AI-driven fraud analytics. Retailers adopt autonomous shopping agents that complete complex purchase journeys, compelling firms to restructure product data into machine-readable formats to sustain share-of-voice amid AI-mediated commerce shifts.

5G-IoT proliferation fuels edge analytics demand

Operators pledge USD 97 billion for 5G rollouts through 2030, with private 5G networks such as ADNOC-e& delivering projected USD 1.5 billion economic value from latency-sensitive AI workloads[2]Telecom Lead, “Strategies for Operators to Boost 5G,” telecomlead.com. Edge platforms ingest sensor streams and trigger millisecond decisions that mitigate downtime, optimize energy, and improve worker safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Arabic AI talent and data-labeling expertise | -2.8% | Arabic-speaking regions | Long term (≥ 4 years) |

| Fragmented legacy OT networks hindering zero-trust rollouts | -2.1% | Industrial hubs in Saudi Arabia, UAE | Medium term (2-4 years) |

| High TCO for silicon-heavy GPU infrastructure | -1.9% | Global | Short term (≤ 2 years) |

| Escalating geopolitical cyber-risk raising insurance premiums | -1.6% | MENA core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Arabic AI talent and data-labeling expertise limits deployment speed

Only 12% of enterprises surveyed feel fully prepared for AI adoption, reflecting shortages of native Arabic data scientists and annotators able to curate high-quality corpora for model fine-tuning. This bottleneck prolongs proof-of-concept phases and elevates the dependence on managed services.

Fragmented legacy OT networks hinder zero-trust rollouts

Industrial sites across energy and utilities operate heterogeneous control systems with minimal segmentation, complicating identity-centric security overlays and delaying broad zero-trust adoption. Retrofit costs and downtime risk discourage immediate upgrades, pushing some operators to perimeter-centric defenses that cannot address converged threat vectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services growth outpaces product sales

Software retained 48.18% of 2025 revenue due to entrenched SIEM, XDR, and visualization deployments that anchor enterprise security architectures. Yet services will generate the bulk of incremental value at a 21.78% CAGR as organizations procure consulting, integration, and 24/7 managed detection in response to region-wide talent gaps. The Middle East and Africa AI, Cybersecurity, and Big Data Analytics market share for services is projected to widen once hyperscalers complete new availability zones and activate GPU-as-a-Service clusters.

Hardware growth tempers because of high capital intensity, with enterprises favoring consumption-based models that shift GPU depreciation to service providers. Consequently, managed security and AIOps subscriptions become core delivery mechanisms across BFSI and healthcare cohorts confronting 24/7 uptime mandates.

By Security Type: Cloud security races ahead

Network protection tools held a 28.55% stake in 2025 as telecom operators hardened 5G infrastructure against signaling storms and DDoS attacks. Cloud security will log a 20.92% CAGR because public-sector cloud-first edicts and enterprise hybrid strategies require continuous posture management across multi-cloud estates. The Middle East and Africa AI, Cybersecurity, and Big Data Analytics market size for cloud security is further amplified by mandatory breach-notification laws carrying fines up to AED 2 million, pushing boards to prioritize centralized controls.

Convergence of API, OT, and identity layers drives unified policy engines, while specialized model-integrity scanners emerge to detect hallucination or prompt-injection risks in generative AI applications.

By Analytics Type: Real-time streaming gains prominence

Advanced/predictive analytics owned 51.95% of 2025 expenditure, underpinned by machine-learning pipelines that forecast risk and customer churn. Real-time streaming analytics will outstrip all other categories with a 23.05% CAGR, reflecting edge architectures that localize millisecond decisions in oil fields, ports, and smart-city command centers.

The Middle East and Africa AI, Cybersecurity, and Big Data Analytics market size allocated to streaming analytics will bridge on-premises industrial data and cloud AI fabrics, enabling autonomous field interventions. Sophisticated visualization layers remain essential as business users demand context-rich narratives rather than raw anomaly alerts, thereby ensuring adoption beyond data science teams.

By End-user Industry: Healthcare adoption inflects upward

BFSI contributed 21.35% of 2025 revenue thanks to persistent regulatory pressures and fraud analytics. In contrast, healthcare and life sciences will compound at 23.62% per year to 2031 as telemedicine platforms, diagnostic imaging AI, and smart hospitals proliferate under national e-health strategies. The Middle East and Africa AI, Cybersecurity, and Big Data Analytics market share for healthcare is catalyzed by cross-border data standards that open secure exchanges between hospitals and insurers.

Energy and utilities sustain double-digit investments as ADNOC, Aramco, and grid operators digitize asset-intensive operations, deploying predictive models that shrink unplanned downtime and carbon intensity simultaneously.

By End-user Enterprise Size: SMEs close the gap

Large enterprises captured 67.90% of 2025 spend; however, SMEs are registering a rapid 22.05% CAGR as subscription-based AI accelerators and managed SOC services sidestep capital and staffing constraints. GPU-as-a-Service facilities introduced by NVIDIA and Ooredoo democratize access to massive compute, reshaping competitive dynamics by lowering the technical threshold for advanced analytics projects.

Standardized compliance frameworks from national cybersecurity agencies provide pre-packaged control mappings that help smaller firms pass audits without bespoke consulting, further leveling the playing field.

Geography Analysis

Saudi Arabia secured a 25.90% share of 2025 spending as Vision 2030 earmarked USD 20 billion for 300 startups and funded an 18,000-GPU supercomputer to host HUMAIN’s ALLaM model. The Kingdom’s Essential Cybersecurity Controls and sector-specific cloud mandates spur continuous upgrade cycles across financial, energy, and government domains. New COE collaborations with NVIDIA reinforce domestic chip availability and high-density compute clusters that accelerate model training.

The UAE, expanding at a 22.20% CAGR, benefits from Microsoft’s USD 1.5 billion G42 injection and MGX’s USD 100 billion global AI infrastructure consortium participation. National AI Strategy 2031 targets a USD 96 billion GDP contribution, directing ministries to implement AI-first service delivery, which in turn stimulates demand for cloud security and analytics layers. Qatar, Turkey, and Egypt form a second tier of fast followers. Ooredoo’s GPU service spans six MENA markets, enabling cross-border AI startups, while Turkey’s digitalization plan modernizes banking APIs, and Egypt leads African regulatory harmonization on data privacy. South Africa anchors sub-Saharan momentum through established colocation campuses and skill-development programs backed by Google’s USD 5.8 million training grant. Cassava Technologies and NVIDIA will construct Africa’s first AI factory, initially serving Southern and East African digital-health, fintech, and agritech workloads . The rest of MEA, comprising Kenya, Nigeria, Morocco, and others, exhibits untapped upside but faces bandwidth and power-grid constraints. Regional development banks finance fiber rollouts and renewable energy projects that will underpin future data-center expansion, enabling wider adoption of the Middle East and Africa AI, Cybersecurity, and Big Data Analytics market solutions.

Competitive Landscape

Global hyperscalers and chipmakers dominate foundation layers but rely on local partnerships to navigate language, regulation, and procurement preferences. Microsoft anchors platform share through new Saudi, UAE, and South African regions and reports 157% YoY regional Azure AI consumption growth. NVIDIA links GPU supply chains to sovereign programs via Khazna AI factories and Ooredoo connectivity, reinforcing an ecosystem approach spanning silicon, software, and managed services.

Regional specialists differentiate by cultural alignment. HUMAIN’s ALLaM 34B and Watad’s Mulhem focus on colloquial dialects and regulatory-compliant datasets, carving niches in government chatbots, fintech KYC, and media localization. G42 blends model research with cloud infrastructure, acquiring cybersecurity integrator CPX to secure GenAI pipelines end-to-end [4]AIbase, “G42 Acquires Cybersecurity Company CPX,” aibase.com.

Vendor rivalry intensifies around AI security. Palo Alto Networks’ USD 700 million Protect AI bid and Mastercard’s USD 2.65 billion Recorded Future acquisition signal convergence between threat-intelligence and model-integrity domains. Managed security providers roll out “AI SOC” offerings that ingest telemetry into LLMs for analyst co-pilots, targeting SME accounts that lack in-house expertise.

MEA AI, Cybersecurity and Big Data Analytics Industry Leaders

Microsoft Corporation

NVIDIA Corporation

Amazon Web Services, Inc.

Cisco Systems, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: HUMAIN schedules the public release of ALLaM 34B, the first Saudi-trained 34-billion-parameter Arabic LLM, to coincide with the Riyadh AI Summit.

- June 2025: Khazna partners with NVIDIA to deploy regional AI factories, each housing 4,000 Hopper GPUs, beginning in Abu Dhabi and Cairo.

- May 2025: Virtual InfoSec Africa opens an AI-driven cyber-forensics center in Accra in collaboration with Exabeam.

- May 2025: HUMAIN and NVIDIA commence installation of an 18,000-GPU supercomputer to support Vision 2030 targets.

MEA AI, Cybersecurity and Big Data Analytics Market Report Scope

The study analyzes the current market scenario and growth trends related to the AI, Cyber Security, and Data Analytics industries in the Middle East & Africa region, with a focus on the developments in the GCC region, which has emerged as one of the major hotspots for investments, aided by substantial investment activity and supportive governmental policies.

The study tracks the country-level market dynamics and the primary implementation use cases for AI and data analytics. The study analyzes the impact of COVID-19 on the region's I and digital transformation-related technologies.

The Market is Segmented by Component (Hardware, Software, Services), End-user Industry (IT & Telecom, Retail, Public & Government Institutions, BFSI, Manufacturing, and Construction, Healthcare), Cyber Security Type (Network, Cloud, Application, End-point, Wireless Network), Big Data Analytics Type (Data Discovery & Visualization, Advanced Analytics), and Country (UAE, Saudi Arabia, Qatar, Kuwait). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Hardware | AI Accelerators (GPU/ASIC) |

| Edge Devices and Sensors | |

| Software | Security Platforms (SIEM/XDR/SASE) |

| Analytics and Visualization Suites | |

| Services | Professional (Consulting, Integration) |

| Managed (MSSP, AIOps, DAaaS) |

| Network |

| Cloud |

| Application |

| End-point |

| Wireless / IoT |

| Other Emerging (API, OT) |

| Data Discovery and Visualization |

| Advanced / Predictive Analytics |

| Real-time Streaming Analytics |

| IT and Telecom |

| Retail and e-Commerce |

| Public Sector and Smart Cities |

| BFSI |

| Manufacturing and Construction |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Transport and Logistics |

| Other Industries (Education, Media) |

| Large Enterprises |

| SMEs |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Turkey |

| Egypt |

| South Africa |

| By Component | Hardware | AI Accelerators (GPU/ASIC) |

| Edge Devices and Sensors | ||

| Software | Security Platforms (SIEM/XDR/SASE) | |

| Analytics and Visualization Suites | ||

| Services | Professional (Consulting, Integration) | |

| Managed (MSSP, AIOps, DAaaS) | ||

| By Security Type | Network | |

| Cloud | ||

| Application | ||

| End-point | ||

| Wireless / IoT | ||

| Other Emerging (API, OT) | ||

| By Analytics Type | Data Discovery and Visualization | |

| Advanced / Predictive Analytics | ||

| Real-time Streaming Analytics | ||

| By End-user Industry | IT and Telecom | |

| Retail and e-Commerce | ||

| Public Sector and Smart Cities | ||

| BFSI | ||

| Manufacturing and Construction | ||

| Healthcare and Life Sciences | ||

| Energy and Utilities | ||

| Transport and Logistics | ||

| Other Industries (Education, Media) | ||

| By End-user Enterprise Size | Large Enterprises | |

| SMEs | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

Key Questions Answered in the Report

What revenue is expected from MEA AI, cybersecurity, and big-data solutions by 2031?

Spending is projected to reach USD 76.33 billion by 2031, reflecting a 19.85% CAGR during 2026-2031.

Which segment grows fastest through 2031?

Services will advance at a 21.78% CAGR as firms outsource AI integration and managed detection.

Why is cloud security surging in MEA?

Government cloud-first mandates and multi-cloud expansion accelerate demand, driving a 20.92% CAGR.

How are sovereign funds shaping adoption?

GCC wealth funds channel over USD 140 billion toward local AI infrastructure, speeding commercialization.

Page last updated on: