AI Cybersecurity Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

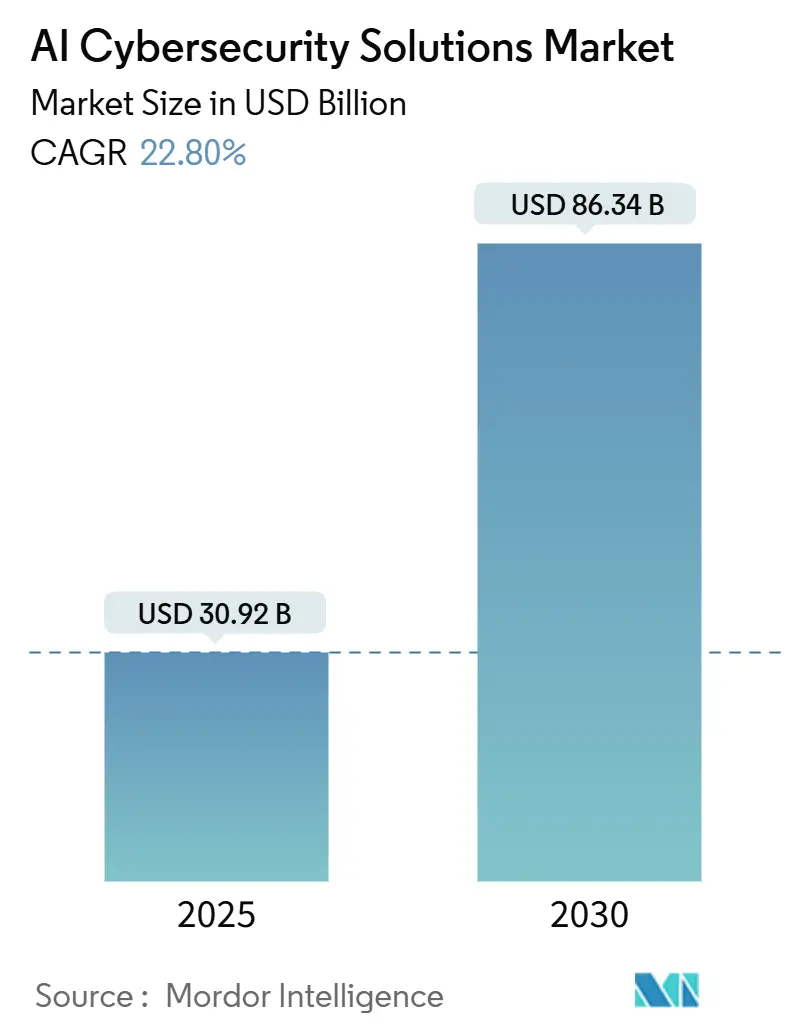

| Market Size (2025) | USD 30.92 Billion |

| Market Size (2030) | USD 86.34 Billion |

| Growth Rate (2025 - 2030) | 22.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Cybersecurity Solutions Market Analysis by Mordor Intelligence

The AI Cybersecurity Solutions market size reached USD 30.92 billion in 2025 and is projected to hit USD 86.34 billion by 2030, reflecting a robust 22.8% CAGR. Accelerated cloud adoption, regulatory mandates that favor autonomous defenses, and a chronic shortage of qualified security personnel keep demand high. Enterprises now face AI-enabled attacks that morph in real time, making automated detection and response essential. Zero-trust architectures, mandated across multiple jurisdictions, further stimulate investment in behavioral analytics and continuous authentication. Vendors differentiate by embedding self-healing capabilities that lower the total cost of ownership while shrinking mean-time-to-respond. Simultaneously, service providers see rising demand for managed model training, threat-hunting, and compliance automation, underscoring the industry’s pivot toward outcome-based security consumption.

Key Report Takeaways

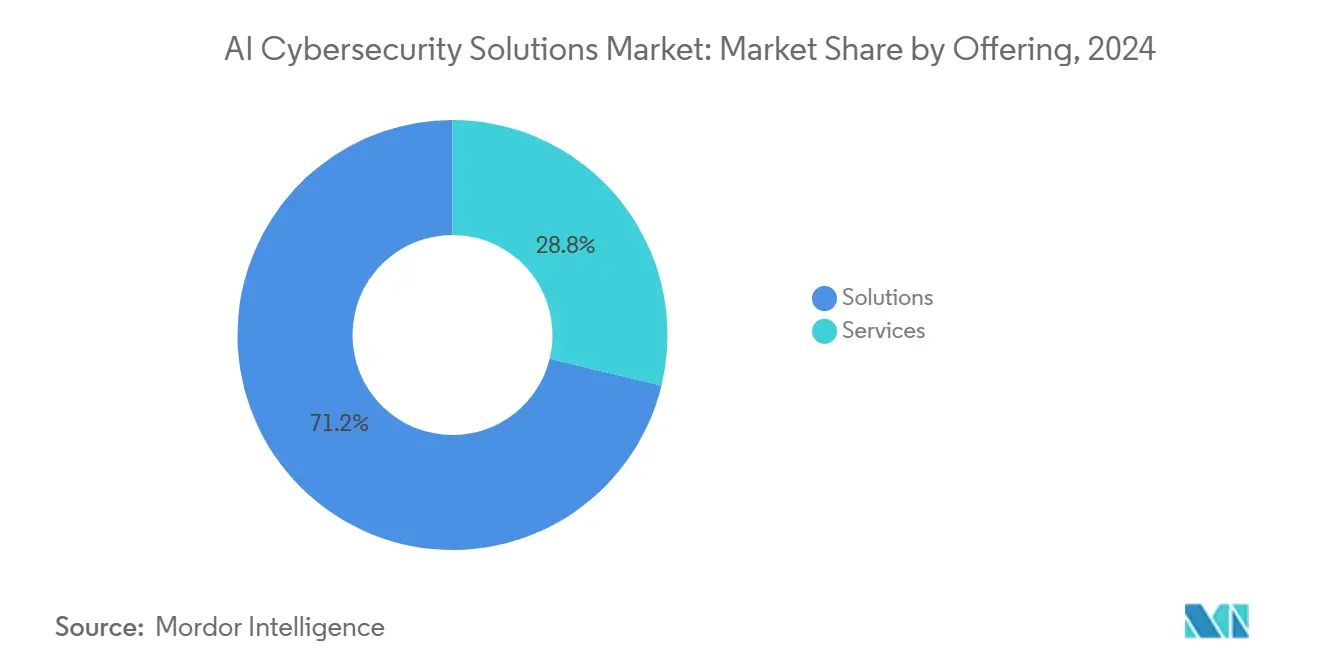

- By offering, solutions captured 71.2% of the AI Cybersecurity Solutions market share in 2024, while services are forecast to advance at a 23.6% CAGR through 2030.

- By deployment mode, cloud platforms commanded 58.8% of the AI Cybersecurity Solutions market size in 2024 and are set to expand at a 23.2% CAGR.

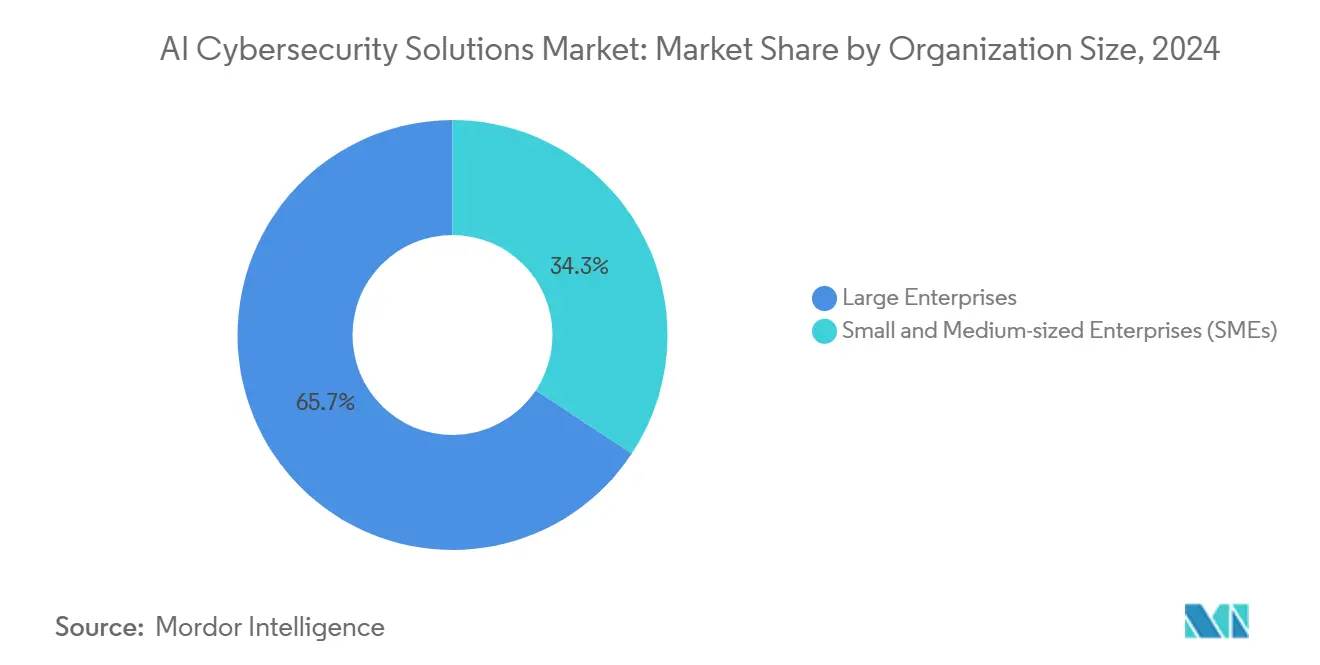

- By organization size, large enterprises held 65.7% revenue of the AI Cybersecurity Solutions market in 2024; small and medium enterprises are poised for 23.5% CAGR growth to 2030.

- By end-user industry, banking and financial services led with 28.4% revenue of the AI Cybersecurity Solutions market in 2024; IT and telecom are positioned for the quickest climb at 24.3% CAGR.

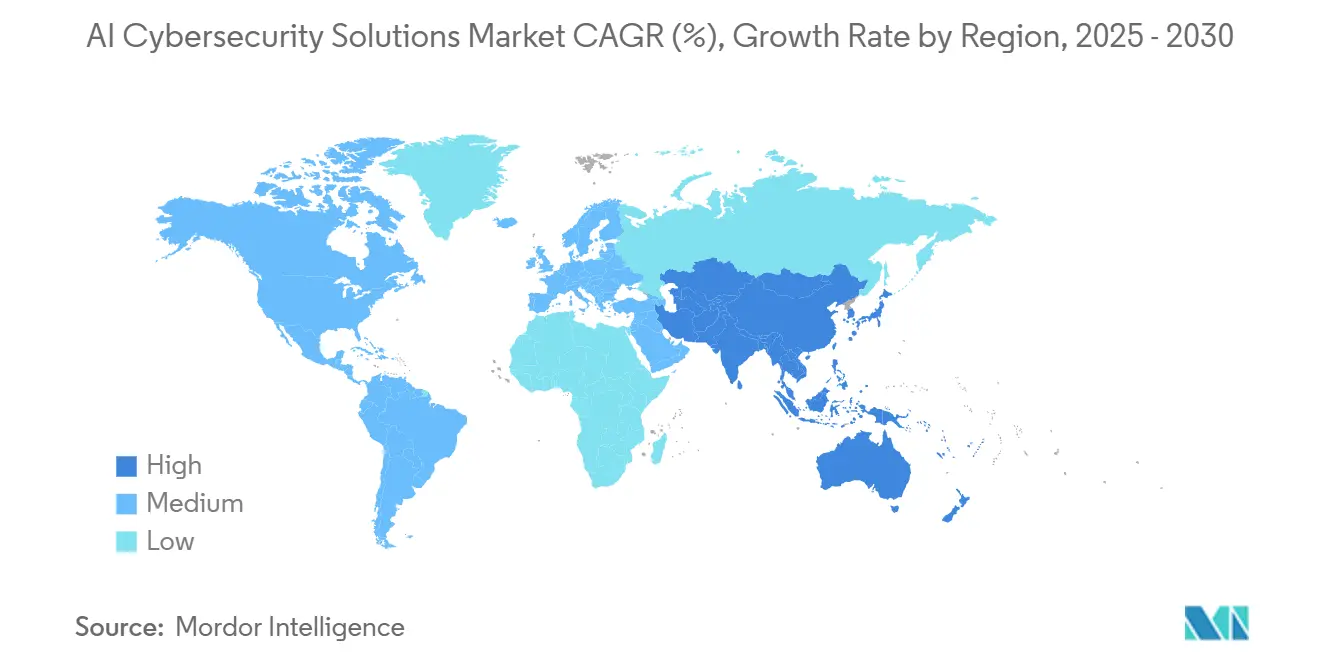

- By geography, North America maintained a 37.8% share of the AI Cybersecurity Solutions market in 2024, while Asia-Pacific is projected to rise at a 24.1% CAGR through 2030.

Global AI Cybersecurity Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating volume and sophistication of cyber-attacks | +6.2% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rapid cloud adoption expanding the attack surface | +5.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Proliferation of IoT and OT devices demanding zero-trust AI security | +4.9% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Stringent data-protection regulations (GDPR, CCPA, NIS2, etc.) | +3.7% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI into DevSecOps pipelines for continuous protection | +2.4% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Emergence of autonomous security operations and self-healing networks | +1.8% | North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Volume and Sophistication of Cyber-Attacks

AI-enabled adversaries now automate vulnerability discovery, exploit development, and deepfake-driven social engineering schemes. The FBI recorded a 10% year-over-year rise in cybercrime complaints for 2024, with monetary losses topping USD 12.5 billion.[1]Federal Bureau of Investigation, “Internet Crime Complaint Center 2024 Annual Report,” FBI, fbi.gov Real-time adaptive malware bypasses signature-based tools, prompting enterprises to deploy continuous AI threat modeling. The spread of AI-as-a-Service makes advanced attack kits available to less-skilled actors, widening the threat pool. Financial services and healthcare remain priority targets because of high-value data. Standards bodies, including NIST, updated frameworks in 2024 to emphasize machine-learning-aware defenses, further institutionalizing AI adoption.

Rapid Cloud Adoption Expanding the Attack Surface

Enterprises now manage thousands of cloud assets across multi-provider environments, generating visibility gaps that manual processes cannot close. The shared-responsibility model often blurs ownership, especially in serverless and containerized workloads. Massive authentication logs demand machine learning for anomaly detection at scale. Multi-cloud strategies intensify complexity, pushing demand for orchestration engines that normalize policies across providers. Zero-trust network access produces continuous authorization data, which AI pipelines convert into actionable insights. Cloud-native security offerings that integrate threat hunting and auto-remediation reduce administrative overhead and speed deployment cycles.

Proliferation of IoT and OT Devices Demanding Zero-Trust AI Security

Industrial IoT deployments hit 17.7 billion connected endpoints in 2024, exposing operational networks that traditionally lacked authentication safeguards. Seventy-eight percent of surveyed utilities reported rising cyber-physical threats. Legacy protocols complicate patch cycles, making behavior-based detection indispensable. AI-driven asset discovery engines map devices in real time and enforce micro-segmentation without disrupting processes. Industry 4.0 accelerates this trend, especially in manufacturing and energy, where every minute of downtime can cost USD 50,000. Regulators enforce protective baselines such as the EU’s NIS2 Directive, prompting critical-infrastructure operators to invest in scalable AI analytics.[2]European Union, “Directive (EU) 2022/2555,” EUR-Lex, europa.eu

Stringent Data-Protection Regulations Driving Compliance Automation

The EU’s expanded NIS2 framework, effective October 2024, now covers 18 critical sectors and obligates incident reporting within 24 hours, leveraging fines of up to EUR 10 million (USD 10.9 million) or 2% of annual turnover. Parallel U.S. state laws broaden the compliance burden, making manual audit trails untenable. AI platforms now automate data classification, privacy-impact assessments, and breach notification workflows, reducing compliance overhead by up to 40%. Differential privacy and federated learning techniques allow multinational firms to honor localization rules while still sharing threat intelligence. Regulatory scrutiny elevates demand for explainable AI to demonstrate alignment with due-care requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled AI-cybersecurity professionals | -3.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| High upfront cost and integration complexity | -2.9% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Model bias and susceptibility to adversarial AI attacks | -2.1% | Global, critical in regulated industries | Medium term (2-4 years) |

| Data-privacy restrictions limiting training-data availability | -1.7% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled AI-Cybersecurity Professionals

The global workforce gap reached 4 million in 2024, with specialized AI roles in particularly short supply. Universities graduate fewer than 15,000 qualified candidates annually, but industry demand tops 200,000. Scarcity drives salary inflation that many mid-tier firms cannot absorb, slowing adoption timelines. Managed service providers attempt to bridge the gap, yet capacity constraints persist. Certification bodies race to update curricula, while vendors integrate no-code interfaces to minimize setup complexity. Without talent infusion, implementation backlogs will continue to restrain short-term growth.

High Upfront Cost and Integration Complexity

Comprehensive AI security rollouts cost between USD 2.5 million and USD 5 million, covering data infrastructure modernization, model training, and API integration. Legacy SIEM platforms often lack compatible data schemas, requiring custom connectors that add months to go-live dates. Small and medium enterprises face particular financial hurdles, even as consumption-based pricing gains traction. Business cases hinge on avoided breach costs, which are difficult to quantify until an incident occurs. Vendors that simplify deployment through pre-trained models and turnkey connectors are seeing accelerated procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Integrated Platforms Drive Adoption

Solutions accounted for 71.2% of 2024 revenue, illustrating the enterprise preference for consolidated control planes that span endpoint, network, and identity vectors. The AI Cybersecurity Solutions market size for services is forecast to expand at a 23.6% CAGR as organizations outsource model tuning and 24/7 threat hunting. Application security dominates because API-centric development introduces vulnerabilities that static firewalls miss. Data-centric defenses also gain traction, safeguarding SaaS and multi-cloud workloads with machine-learning-based anomaly detection.

Services growth stems from a persistent talent gap; companies increasingly lean on managed detection and response providers to operationalize complex toolsets. Consulting practices bundle transformation roadmaps with compliance automation, while fully managed SOC offerings supply outcome-based SLAs. Vendors that bundle training, red-teaming, and post-deployment optimization enjoy higher renewal rates, signaling a shift from product to lifecycle partnerships within the AI Cybersecurity Solutions market.

By Deployment Mode: Cloud-Native Architecture Scales Defenses

Cloud deployments held a 58.8% share in 2024 and are projected to keep a 23.2% CAGR, reflecting the scalability needed for compute-intensive model inference. This share translates into a significant portion of the overall AI Cybersecurity Solutions market size, reinforcing the cloud’s role as the default environment for analytics pipelines. Elastic resources allow rapid ingestion of high-velocity telemetry, enabling sub-second anomaly scoring.

On-premise installations persist for data sovereignty and latency-sensitive use cases, especially in defense and critical infrastructure. Hybrid models combine local preprocessing with cloud-hosted control consoles, balancing performance and compliance. Edge deployments bring AI closer to IoT sensors, delivering immediate response in operational environments. The proliferation of cloud governance frameworks FedRAMP, ISO 27017 further legitimizes cloud adoption, smoothing procurement cycles for public-sector customers.

By Organization Size: SME Momentum Redefines Economics

Large enterprises retained 65.7% revenue in 2024, leveraging sizable budgets to deploy multi-layered defenses. Yet SMEs deliver the fastest growth at 23.5% CAGR, propelled by SaaS platforms that remove infrastructure barriers. Consumption-based billing lets smaller firms tap enterprise-grade analytics without capital expenditure.

Automated orchestration levels the playing field by translating complex indicators into plain-language alerts. Insurance carriers increasingly require AI-empowered controls as a condition for cyber-policy underwriting, nudging SMEs toward adoption. Conversely, large organizations prioritize custom model development and advanced hunting capabilities, which augment their existing SOC workflows. The democratization of capabilities is reshaping vendor go-to-market strategies within the AI Cybersecurity Solutions market.

By End-User Industry: BFSI Leads While Technology Sectors Accelerate

Banking and financial services commanded 28.4% of sectoral demand in 2024, driven by regulatory scrutiny and high-value data. AI-driven behavioral analytics detect insider threats, synthetic identity fraud, and account takeover attempts in milliseconds. The IT and telecom vertical is set for the steepest ascent at 24.3% CAGR, fueled by 5G rollouts and edge computing that expand attack surfaces.

Healthcare organizations integrate device telemetry with electronic health record protections to thwart ransomware targeting patient safety. Retail leverages AI for real-time payment fraud detection, tying security to customer-experience metrics. In manufacturing, predictive maintenance data intersects with security analytics to safeguard smart-factory assets. Each vertical seeks turnkey compliance mappings, for example, PCI DSS for retail and HIPAA for healthcare, embedding governance directly into defense workflows.

Geography Analysis

North America retained a 37.8% share in 2024 due to mature regulatory frameworks, abundant venture capital, and an extensive vendor ecosystem. Federal mandates, including the Cybersecurity Executive Order, obligate zero-trust adoption across agencies, feeding enterprise spillover. High digital maturity in financial services and tech sectors ensures sustained investment in behavioral analytics and autonomous response platforms. Public-private threat-intelligence sharing through programs such as CISA’s Continuous Diagnostics and Mitigation further catalyzes uptake.[3]Cybersecurity and Infrastructure Security Agency, “Continuous Diagnostics and Mitigation Program,” CISA, cisa.gov

Asia-Pacific will record a 24.1% CAGR to 2030, propelled by rapid urbanization, 5G expansion, and Industry 4.0 manufacturing hubs. China, Japan, and Australia represent the largest spenders, while India showcases high velocity among cloud-native SMEs. Governmental cybersecurity blueprints such as APEC’s regional framework support cross-border information exchange, encouraging multinational deployments. Smart-city projects in Southeast Asia embed AI security controls from inception, elevating baseline capability across municipal networks.

Europe posts steady growth anchored by the NIS2 Directive, which formalizes cybersecurity obligations across 27 members. Organizations seek AI platforms with data-localization options to satisfy sovereignty concerns. Germany, the United Kingdom, and France dominate enterprise adoption, while Nordic countries achieve near-parity between SMEs and large corporations. The forthcoming EU AI Act prompts vendors to certify transparency and auditability, reshaping product roadmaps. Brexit‐related realignments create dual-regime complexities, where cross-border operators demand flexible compliance tooling. Across these regions, the AI Cybersecurity Solutions market continues to evolve through localized product adaptations and multilateral cooperation.

Competitive Landscape

The AI cybersecurity arena remains moderately fragmented, with no single provider exceeding 15% revenue. Established vendors such as Palo-Alto Networks, Fortinet, and CrowdStrike extend existing portfolios via AI acquisitions and in-house innovation. AI-native challengers like Darktrace and SentinelOne prioritize autonomous response, disrupting incumbent refresh cycles. Cloud hyperscalers embed security analytics into their platforms, blurring lines between infrastructure and protection.

Strategic moves revolve around three archetypes: platform consolidation as seen in Palo-Alto’s acquisition of Talon Cyber Security in May 2025, vertical specialization, exemplified by Vectra’s pivot to operational technology security, and partner ecosystems typified by CrowdStrike’s integrations with Google Cloud, HPE, and Cloudflare in July 2025.[4]Palo Alto Networks, “Palo Alto Networks Acquires Talon Cyber Security,” paloaltonetworks.com Vendors emphasizing measurable outcomes gain traction amid budget scrutiny, leveraging MITRE ATT&CK mappings and time-to-contain metrics as proof points.

White-space opportunities include privacy-preserving analytics for regulated sectors and domain-specific solutions for industrial control systems. Start-ups that couple consumptive pricing with quick-start deployments find resonance among SMEs, driving an undercurrent of disruptive competition. Overall, the AI Cybersecurity Solutions market rewards vendors capable of combining technical depth with operational simplicity.

AI Cybersecurity Solutions Industry Leaders

Darktrace plc

Vectra AI, Inc.

SentinelOne, Inc.

CrowdStrike Holdings, Inc.

Palo Alto Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Thoma Bravo completed a USD 5.3 billion acquisition of Darktrace, enabling accelerated product investment and geographic expansion.

- July 2025: CrowdStrike forged partnerships with Google Cloud, HPE, and Cloudflare, embedding Falcon endpoint protection within multiple cloud ecosystems.

- July 2025: Sophos unveiled its Adaptive Cybersecurity Ecosystem, unifying endpoint, network, and cloud protections.

- June 2025: Check Point launched Infinity AI, consolidating prevention, detection, and response under one roof.

Global AI Cybersecurity Solutions Market Report Scope

AI for security solutions involves integrating endpoint data and analytics to gain threat intelligence, which aids in detecting and exposing an attack in a particular environment. With the growth in online transactions and a surge in NEFT, RTGS, and mobile commerce, the demand for security solutions is increasing. The banking sector noticed a significant rise in adopting artificial intelligence-based security solutions, which helped improve banking services.

The market is segmented by security type (network security, application security, and cloud security), service (professional and managed), deployment (on-premises and cloud), end-user industry (government and defense, retail, BFSI, manufacturing, healthcare, automotive and transportation, and other end-user industries), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

| On-premise |

| Cloud |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Industrial and Defense |

| Energy and Utilities |

| Manufacturing |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Solutions | Application Security | |

| Cloud Security | |||

| Data Security | |||

| Identity and Access Management | |||

| Infrastructure Protection | |||

| Integrated Risk Management | |||

| Network Security | |||

| End-point Security | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Industrial and Defense | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the AI Cybersecurity Solutions market in 2025?

The AI Cybersecurity Solutions market size stands at USD 30.92 billion in 2025, and it is set to grow rapidly through 2030.

What CAGR is projected for AI-based cyber defense spending to 2030?

Aggregate spending is forecast to post a 22.8% CAGR between 2025 and 2030, underscoring strong demand for autonomous security controls.

Which region is expected to grow fastest for AI-driven security?

Asia-Pacific is projected to achieve a 24.1% CAGR through 2030 as digital-transformation initiatives multiply attack surfaces.

Why are small and medium enterprises adopting AI security now?

Cloud-native SaaS delivery lowers infrastructure barriers, while insurance requirements increasingly mandate automated threat detection.

What segment leads current adoption by industry vertical?

Banking and financial services hold the largest share, accounting for 28.4% of 2024 revenue due to strict compliance mandates and valuable data stores.

How are vendors addressing the cybersecurity talent gap?

Platforms now incorporate AI-powered triage, no-code automation, and managed service bundles, allowing organizations to operate with leaner security teams.

Page last updated on: