AI Governance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

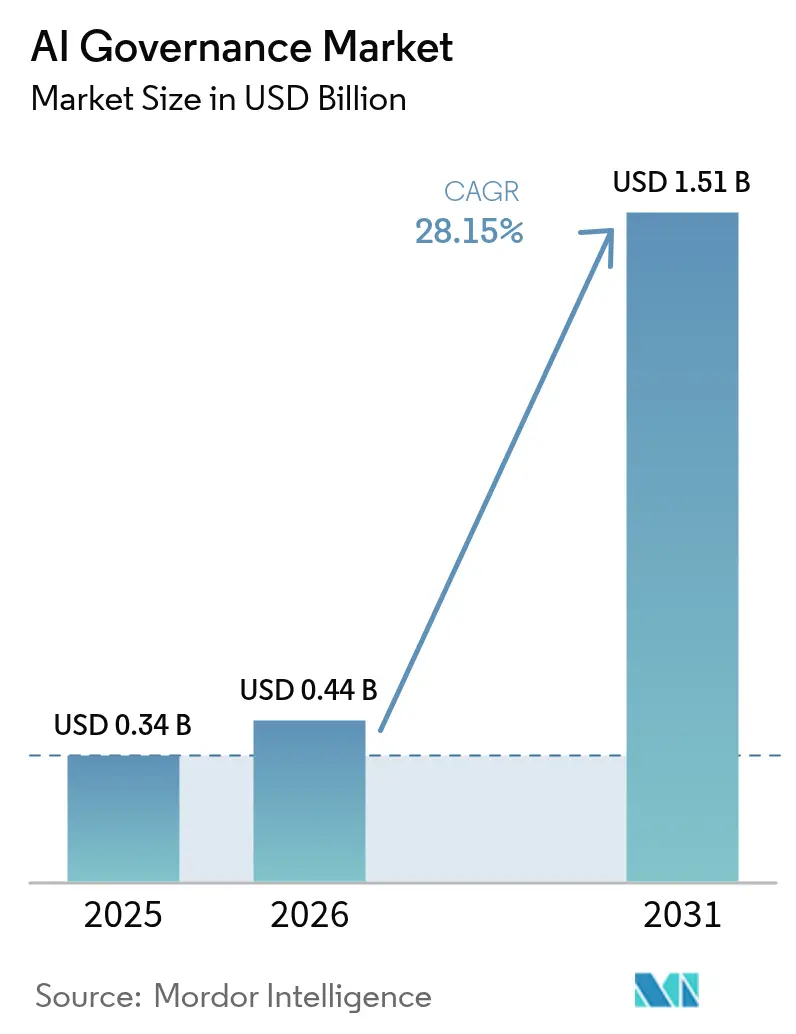

| Market Size (2026) | USD 0.44 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 28.15% CAGR |

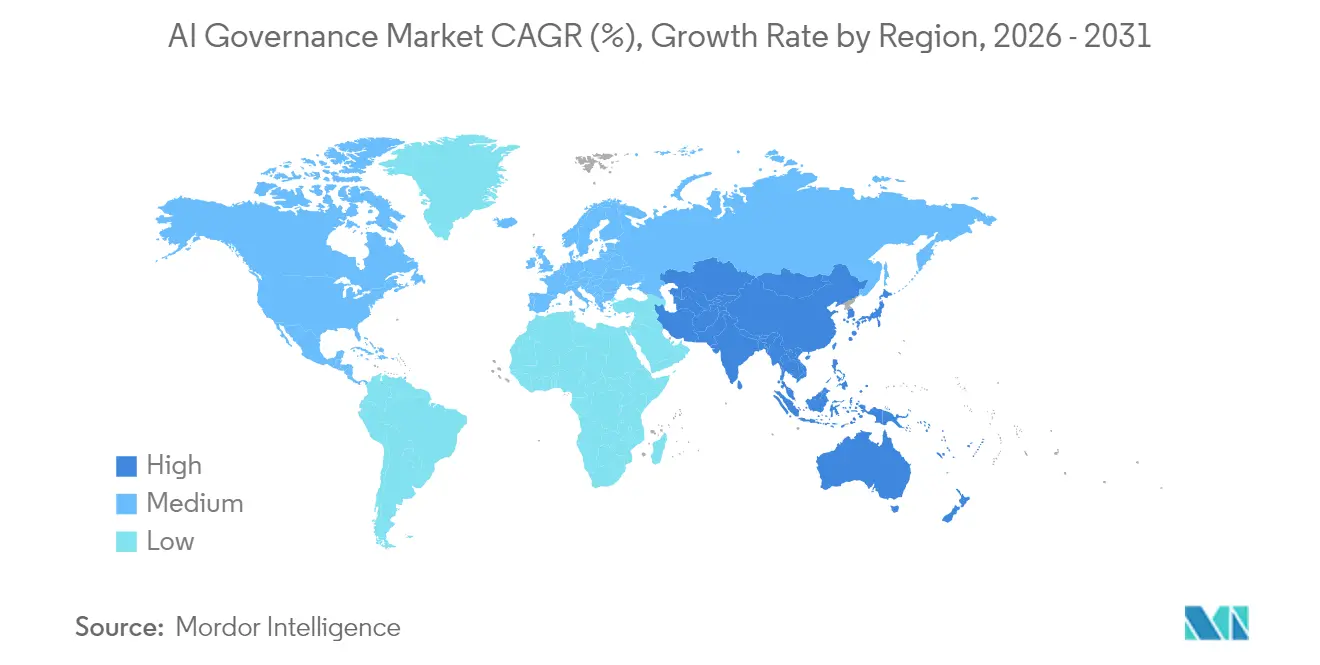

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Governance Market Analysis by Mordor Intelligence

The AI Governance Market size was valued at USD 0.34 billion in 2025 and estimated to grow from USD 0.44 billion in 2026 to reach USD 1.51 billion by 2031, at a CAGR of 28.15% during the forecast period (2026-2031).

Accelerated growth reflects the urgent need for systematic oversight as generative AI adoption continues to outpace legacy risk-management frameworks. Enforcement of the EU AI Act from February 2025 has become a pivotal inflection point, mandating comprehensive governance structures for high-risk systems and threatening fines of up to EUR 35 million or 7% of global turnover for non-compliance[1]Moody’s, “EU AI Act Credit Implications,” moodys.com. Simultaneously, insurance carriers now link premium discounts to certified governance frameworks, pushing enterprises toward rapid adoption. Large enterprises dominate initial spending, yet cloud-native platforms are lowering entry barriers and catalysing small- and mid-size enterprise (SME) demand. Geographically, North America leads today, while Asia Pacific records the fastest future upswing as regional regulators blend innovation agendas with progressively tighter safety rules.

Key Report Takeaways

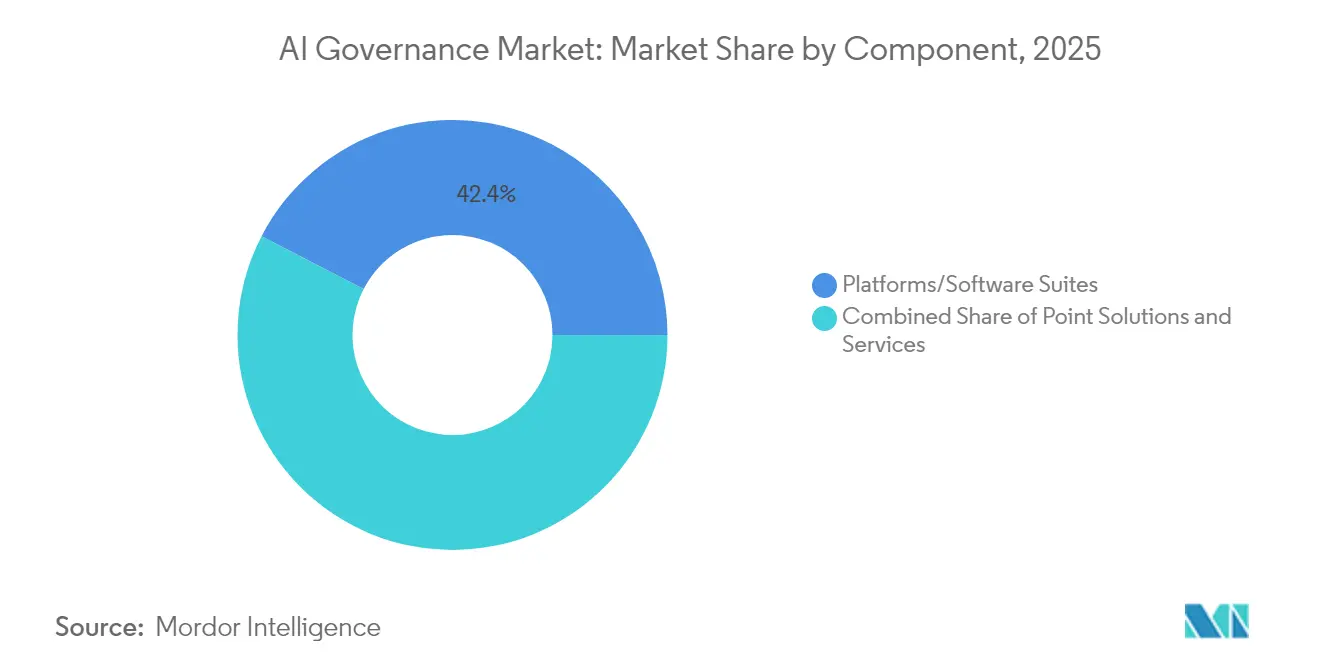

- By component, platforms and software suites held 42.40% of the AI Governance market share in 2025, whereas point solutions for bias detection and explainability are forecast to expand at a 28.6% CAGR through 2031.

- By deployment model, cloud implementations represented 77.20% of the AI Governance market size in 2025 and are projected to widen at a 29.4% CAGR to 2031.

- By end-user industry, financial services led with 25.40% revenue share in 2025; healthcare is advancing at a 28.5% CAGR through 2031.

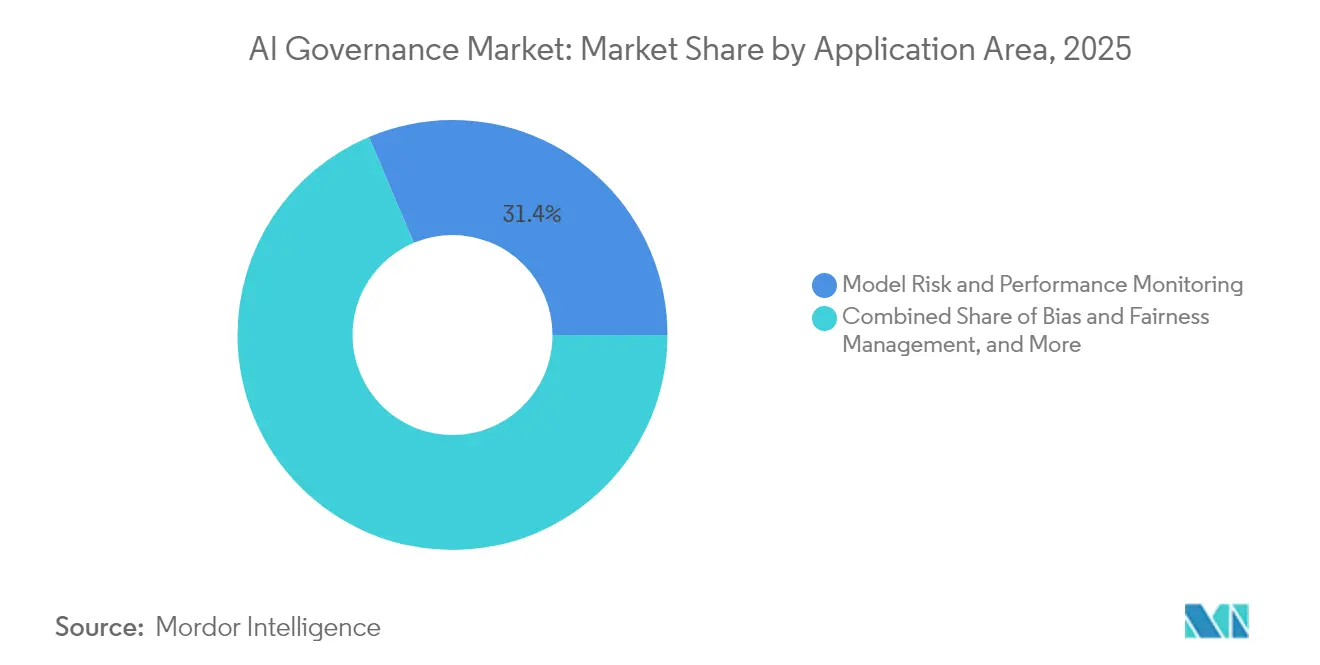

- By application area, model risk and performance monitoring captured a 31.35% share of the AI Governance market size in 2025, while bias and fairness management is growing at a 28.55% CAGR to 2031.

- By organisation size, large companies accounted for 60.20% share of the AI Governance market size in 2025; SMEs are scaling at a 29.05% CAGR to 2031.

- By geography, North America maintained a 32.85% revenue share in 2025, whereas Asia Pacific is accelerating at a 34.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI Governance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for model transparency and explainability | +6.2% | Global, strictest in the EU, and California | Medium term (2-4 years) |

| Rapid proliferation of AI-specific regulations | +8.1% | EU, US states, and leading APAC economies | Short term (≤ 2 years) |

| Rising enterprise reputational risk from biased AI | +4.7% | Global, especially BFSI and healthcare | Medium term (2-4 years) |

| Escalating ESG-driven investor pressure | +3.4% | North America and the EU, extending into APAC | Long term (≥ 4 years) |

| Emergence of AI-for-AI autonomous compliance agents | +3.8% | Global, pilot deployments inside large enterprises | Medium term (2-4 years) |

| Insurance carriers linking premium discounts to certified governance | +2.6% | North America and the EU insurance markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Model Transparency and Explainability

Provisions in the EU AI Act now require high-risk AI systems to generate clear technical documentation, traceable audit logs, and human-readable justification for automated decisions. Financial institutions using AI for credit scoring must supply explanations that satisfy both regulators and affected consumers[2]Bank for International Settlements, “Credit Model Transparency Guidance,” bis.org. Enterprises increasingly view interpretability as a competitive asset that speeds internal approval cycles and bolsters customer trust. Vendors respond with platforms that auto-document model lineage and produce real-time natural-language explanations. As a result, procurement teams prioritize solutions certified for transparency, shifting budget away from opaque “black-box” algorithms toward interpretable architectures.

Rapid Proliferation of AI-Specific Regulations

Between 2024 and 2025, more than 70 new legislative or executive directives governing AI entered force worldwide. The EU AI Act sets a global reference point, while China’s generative-AI filing regime introduces a de facto license model that obliges service providers to register training data and safety controls. Jurisdictional divergences force multinational firms to maintain compliance dashboards that map model inventories to each region’s risk categories. Deadlines as short as six months for high-risk systems in the EU contrast with one-year grace periods common in Asia, rewarding companies that embed flexible governance frameworks at design time rather than retrofitting controls late in the lifecycle.

Rising Enterprise Reputational Risk from Unfair or Biased AI Outcomes

Algorithmic discrimination lawsuits have moved from theoretical to material risk. In 2024, Progressive Insurance acknowledged potential liability from AI-generated pricing discrepancies in its 10-K filing. Boards now demand bias dashboards and scenario testing before models reach production. Media coverage amplifies failures, turning single incidents into global talking points within hours. Insurance underwriters have begun offering performance-guarantee policies contingent on documented bias mitigation, further monetizing governance maturity.

Escalating ESG-Driven Investor Pressure to Disclose Algorithmic Impacts

Institutional investors now incorporate AI fairness and environmental footprint metrics into due diligence checklists. Data-center energy use at 2-3% of global emissions draws scrutiny because AI workloads intensify compute density. Roughly 15% of S&P 500 companies elevated AI oversight to board level in 2024. Adoption of the Taskforce on Nature-related Financial Disclosures framework requires businesses to quantify social and ecological outcomes of automated decisions, spurring demand for governance software that auto-generates ESG-conforming impact statements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of AI ethics and compliance talent | −4.9% | Global, acutest in North America and the EU | Short term (≤ 2 years) |

| High integration complexity with legacy MLOps stacks | −3.2% | Global, large enterprises with entrenched infrastructure | Medium term (2-4 years) |

| Fragmented global regulatory definitions | −2.8% | Multinationals operating in BFSI and healthcare | Medium term (2-4 years) |

| Shadow-AI deployments outside formal oversight | −2.1% | Global; intensified by remote and citizen-developer environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Widespread Shortage of AI Ethics and Compliance Talent

Demand for multidisciplinary professionals who understand data science, law, and risk oversight far exceeds supply. A 2024 workforce survey found that 65% of organizations believe additional regulation is needed to ensure safe use of generative AI, yet few possess enough internal expertise to comply[3]IBM, “Global AI Adoption Index 2024,” ibm.com. European companies urgently recruit AI ethics specialists to satisfy the EU AI Act mandates. High salaries and consulting fees inflate compliance budgets, motivating investment in automation that embeds policy checks into development pipelines.

High Integration Complexity with Legacy MLOps Stacks

Legacy model-ops environments lack built-in control points for versioning, lineage, and audit logging. In a 2024 industry poll, 58% of respondents identified fragmented tooling as the chief governance hurdle. Retrofitting oversight into sprawling data-science workflows can cost millions and extend project timelines by quarters. Vendors that supply pre-built adapters to popular data-science notebooks, experiment trackers, and CI/CD orchestrators, therefore, gain a strategic edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Anchor Enterprise Spend

Platforms and software suites commanded 42.40% revenue in 2025, underlining buyer preference for unified environments that manage policies, monitoring, and documentation together. Vendors such as IBM deliver integrated dashboards that map model inventories to jurisdiction-specific obligations, minimizing audit fatigue. Point tools for bias detection and explainability expand fastest at a 28.6% CAGR because they plug neatly into existing pipelines without a large-scale rip-and-replace. The services sub-segment grows steadily as organizations outsource framework design and regulator liaison amid acute skill shortages.

Enterprise architects favor a single system of record to avoid gaps. Yet in brownfield settings, incremental roll-outs dominate. Teams often start with a bias-scanning API that flags disparate impact, then layer on automated documentation generators. This “modular” journey fuels parallel growth paths where platforms gain share in green-field digital-native firms while point solutions penetrate established corporates. Professional services demand remains resilient, reflecting the heavy lift of mapping data flows, classifying risk tiers, and aligning internal policies to each regulator’s language.

By Deployment: Cloud First, Yet Hybrid Persists

Cloud implementations represented 77.20% of the AI Governance market in 2025 and are slated to compound at 29.4% annually. Providers embed governance hooks directly into platform services, offering automatic upgrades that track evolving rules. A single console can inspect prompts, training runs, and inference logs across multi-region data centers, slicing compliance overhead. SMEs gravitate to these pay-as-you-go options because upfront capital requirements are negligible.

Despite cloud momentum, certain workloads remain on-premises to satisfy data sovereignty or latency constraints. European banks piloting generative-credit scoring often run explainability algorithms on in-house servers to keep sensitive customer data inside national borders. Hybrid designs, therefore, proliferate training may occur in an on-premises sandbox, whereas monitoring dashboards reside in a sovereign cloud enclave. Vendors that deliver parity across deployment modes capture cross-sell opportunities as clients move models through staged environments.

By End-User Industry: Financial Services Still Leads

Financial institutions retained 25.40% of 2025 revenue due to stringent audit regimes such as SR 11-7 in the United States and EBA Guidelines on Model Risk Management in the EU. These rules map cleanly onto AI Governance controls, accelerating spend. Risk and compliance teams leverage governance tooling to automate model approval committees, shortening time-to-market for new scoring or fraud algorithms. Insurers further adopt continuous performance monitoring to update actuarial tables in real time.

Healthcare grows fastest at 28.5% as AI-assisted diagnosis and treatment require transparent reasoning. Regulators now ask hospitals to justify triage decisions made by image classifiers. Governance platforms provide pixel-to-decision traceability that satisfies ethical review boards. Pharmaceutical R&D uses similar features to defend AI-driven target discovery paths during FDA or EMA filings. Government, retail, telecom, and mobility verticals follow, guided by sector-specific standards that increasingly reference the EU AI Act taxonomy.

By Application Area: Monitoring Dominates, Bias Leads Growth

Model risk and performance monitoring owned a 31.35% share in 2025 because every production system demands health checks for drift, latency, and uptime. Dashboards aggregate telemetry and fire alerts when statistical metrics cross warning thresholds. Bias and fairness management, though smaller, escalates at 28.55% CAGR as firms operationalize DEI commitments and shield brands from discrimination claims. Explainability, audit-trail generation, and privacy controls round out the stack, often bundled into single-license packages.

Organizations first deploy monitoring to stabilize operations, then introduce bias scans on sensitive models. Fintech lenders now rerun fairness assessments nightly, recalibrating scorecards when demographic distributions change. Retailers apply similar logic to recommendation engines to avoid reinforcing historical stereotypes. As generative content enters marketing workflows, hallucination detection and toxicity filtering become additional modules stitched into the governance mesh.

By Organisation Size: Enterprises Set Pace, SMEs Catch Up

Large companies captured 60.20% of 2025 spending. They face multi-regulator exposure and possess dedicated risk offices, which use governance tooling to coordinate legal, compliance, and engineering stakeholders. Budgets also extend to premium service tiers that include 24-hour regulatory hotlines and tailored assurance reports.

SMEs, however, record a 29.05% CAGR because cloud pricing has collapsed, and regulators apply rules proportionately rather than exempting smaller players. Low-code policy editors help lean teams codify controls without bespoke scripting. Vendors launch “starter kits” that ship with pre-templated risk taxonomies mapped to the EU AI Act and California’s forthcoming Automated Decision Systems statute. This democratisation means governance becomes an entry ticket for B2B contracts: large buyers increasingly require evidence of oversight from suppliers, regardless of headcount.

Geography Analysis

North America’s 32.85% 2025 share reflects early venture funding, high cloud adoption, and a mosaic of state rules that drive demand for centralised oversight. The White House Executive Order on AI sets broad guardrails but defers specifics to agencies, prompting proactive compliance spending while definitions mature. Canada favors voluntary standards but signals an impending AI & Data Act that mirrors European risk tiers. Mexico adopts cross-border data-flow clauses within USMCA, nudging domestic firms toward governance upgrades compatible with North American partners.

Asia Pacific is projected to post a 34.7% CAGR to 2031, the fastest worldwide. China blends national security imperatives with provincial implementation guidelines, creating multi-layer checkpoints that reward vendors able to cascade policies down organisational hierarchies. Japan’s light-touch approach encourages voluntary codes complemented by sector guidance, offering growth lanes for modular governance suites that snap into diverse toolchains. South Korea’s AI Basic Act, effective January 2026, extends Europe-style transparency requirements, whereas India’s state initiatives inject funding for responsible-AI sandboxes. Collectively, these schemes create a patchwork that necessitates multilingual interface support and flexible policy engines.

Europe shows steady uptake anchored by the EU AI Act. Enforcement authorities can levy penalties equal to 7% of global turnover, compelling swift action. Germany and France lead deployments through established industrial AI hubs and government co-investment in trustworthy AI centres. The United Kingdom pursues an innovation-friendly route centred on existing regulators, yet cross-border businesses still align with EU standards to preserve market access. Nordic countries emphasise public-sector transparency, deploying open-source monitoring scripts to publish algorithm registers, while Eastern European members leverage EU structural funds to adopt turnkey governance platforms.

Competitive Landscape

The AI Governance market remains moderately fragmented. Incumbent tech vendors exploit enterprise footholds to bundle governance features into broader analytics or cloud portfolios. IBM’s watsonx.governance suite exemplifies this approach, offering model-catalogue views, bias scans, and policy workflow orchestration within one license. Microsoft integrates similar controls directly into Azure AI Studio, creating switching costs that lock workflows into its ecosystem. Google Cloud pairs partner services with built-in policy libraries aligned to NIST and ISO standards.

Specialised startups fill niche gaps. Credo AI emphasises policy generation and stakeholder scorecards. Arthur AI delivers model-specific telemetry for drift and outlier detection, while Fairly AI focuses on continuous compliance testing. These firms frequently partner with consulting integrators such as Slalom or Booz Allen to tackle organisational change management. Patent filings underscore innovation intensity: WIPO logged more than 25,000 generative-AI patents in 2023, a notable subset aimed at governance tooling[4]WIPO, “Patent Landscape Report on Generative AI 2023,” wipo.int.

Strategic alliances multiply as ecosystem players race to deliver end-to-end stacks. Anthropic’s three-way collaboration with AWS and Accenture trains over 1,400 engineers to embed Claude models into regulated industries. IBM’s tie-ups with e& and KPMG Japan illustrate how platform vendors leverage telecom and advisory channels to penetrate geographies with tough regulatory deadlines. Funding momentum persists: Monitaur, ValidMind, and ModelOp collectively raised more than USD 24 million during 2024, signalling sustained investor confidence in the category.

AI Governance Industry Leaders

Microsoft Corporation

IBM Corporation

SAP SE

Google LLC (Alphabet Inc.)

FICO Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: OpenAI raised USD 40 billion in a SoftBank-led round to expand compute infrastructure and governance safeguards.

- March 2025: Anthropic, AWS, and Accenture launched a programme to scale responsible AI with 1,400 trained engineers serving regulated sectors.

- January 2025: e& collaborated with IBM to deploy a full-stack AI governance solution built on watsonx.governance, covering automated risk assessment and continuous compliance across telecom networks.

- January 2025: KPMG Japan deepened its partnership with IBM to extend “Trusted AI” services using watsonx.governance for post-EU AI Act mandates.

Global AI Governance Market Report Scope

AI governance is the concept that promotes the establishment of legal frameworks for facilitating the ethical deployment of machine learning (ML) and other AI-based technologies.

The AI governance market is segmented by component (solution and service), deployment (cloud and on-premise), end-user vertical (healthcare, government and defense, automotive, retail, BFSI, and other end-user verticals), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, and the Rest of Europe), Asia-Pacific (China, India, Japan, and the Rest of Asia-Pacific), and the Rest of the World. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Platforms/Software Suites |

| Point Solutions (Bias/Explainability/Monitoring) |

| Services |

| Cloud (SaaS) |

| On-Premise/Private Cloud |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and E-commerce |

| Automotive and Mobility |

| Telecom and Media |

| Other Industries |

| Bias and Fairness Management |

| Explainability and Transparency |

| Model Risk and Performance Monitoring |

| Regulatory Compliance and Audit Trail |

| Data Privacy and Security Controls |

| Large Enterprises |

| Small and Mid-size Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Platforms/Software Suites | |

| Point Solutions (Bias/Explainability/Monitoring) | ||

| Services | ||

| By Deployment | Cloud (SaaS) | |

| On-Premise/Private Cloud | ||

| By End-User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Government and Defense | ||

| Retail and E-commerce | ||

| Automotive and Mobility | ||

| Telecom and Media | ||

| Other Industries | ||

| By Application Area | Bias and Fairness Management | |

| Explainability and Transparency | ||

| Model Risk and Performance Monitoring | ||

| Regulatory Compliance and Audit Trail | ||

| Data Privacy and Security Controls | ||

| By Organisation Size | Large Enterprises | |

| Small and Mid-size Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the AI Governance market today, and how fast will it grow?

The market is USD 0.44 billion in 2026 and is projected to reach USD 1.51 billion by 2031 at a 28.15% CAGR.

Which regions contribute most to AI Governance revenue?

North America holds 32.85% revenue share, while Asia Pacific is the fastest-growing region at a 34.7% CAGR through 2031.

Why are cloud deployments dominating adoption?

Cloud platforms make up 77.20% of implementations because they deliver rapid scalability, automatic regulation-aligned updates, and lower upfront costs.

What is driving the surge in bias and fairness management tools?

A rise in lawsuits and insurer-mandated guarantees has turned bias mitigation into a board-level priority, fuelling a 28.55% CAGR in this application area.

Which industries are the earliest adopters of AI Governance frameworks?

Financial services leads with a 25.40% share due to strict supervisory mandates; healthcare follows with the highest growth rate at 28.5% through 2031.

How severe is the skills bottleneck?

Talent shortages subtract an estimated 4.9 percentage points from forecast growth, forcing organisations to automate compliance checkpoints wherever possible.

Page last updated on: