Saudi Arabia Big Data And Artificial Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

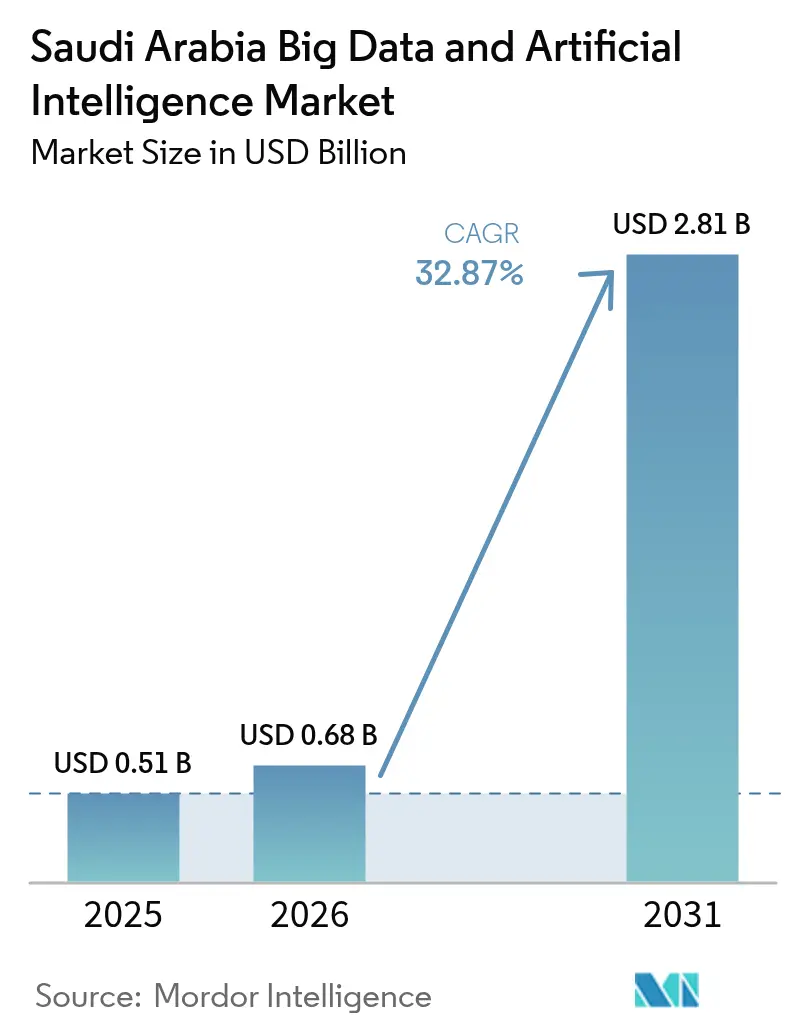

| Base Year Market Size (2025) | USD 0.51 Billion |

| Market Size (2026) | USD 0.68 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 32.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Big Data And Artificial Intelligence Market Analysis by Mordor Intelligence

The Saudi Arabia big data and artificial intelligence market size was valued at USD 0.51 billion in 2025 and estimated to grow from USD 0.68 billion in 2026 to reach USD 2.81 billion by 2031, at a CAGR of 32.87% during the forecast period (2026-2031). The surge is propelled by Vision 2030 investment pledges, a USD 40 billion sovereign AI fund launched in 2024, and NEOM’s sensor network that now streams more than 1 petabyte of data every day.[1]Jensen Huang, “Saudi Arabia and NVIDIA to Build AI Factories,” NVIDIA News, nvidia.com Software commands 45.32% revenue as Arabic-language large models mature, while services post the fastest 36.30% CAGR on rising DataOps and MLOps demand. Enterprises already rely on on-premises and hybrid deployments for 59.47% of workloads, yet public-cloud usage is expanding at 37.90% CAGR thanks to hyperscaler build-outs. The Saudi Arabia big data and artificial intelligence market benefits additionally from mandatory e-invoicing that has digitized 85% of transactions and produced billions of structured invoices ripe for analytics.[2]Saudi Zakat, Tax and Customs Authority, “E-Invoicing Phase 2 Overview,” zatca.gov.sa

Key Report Takeaways

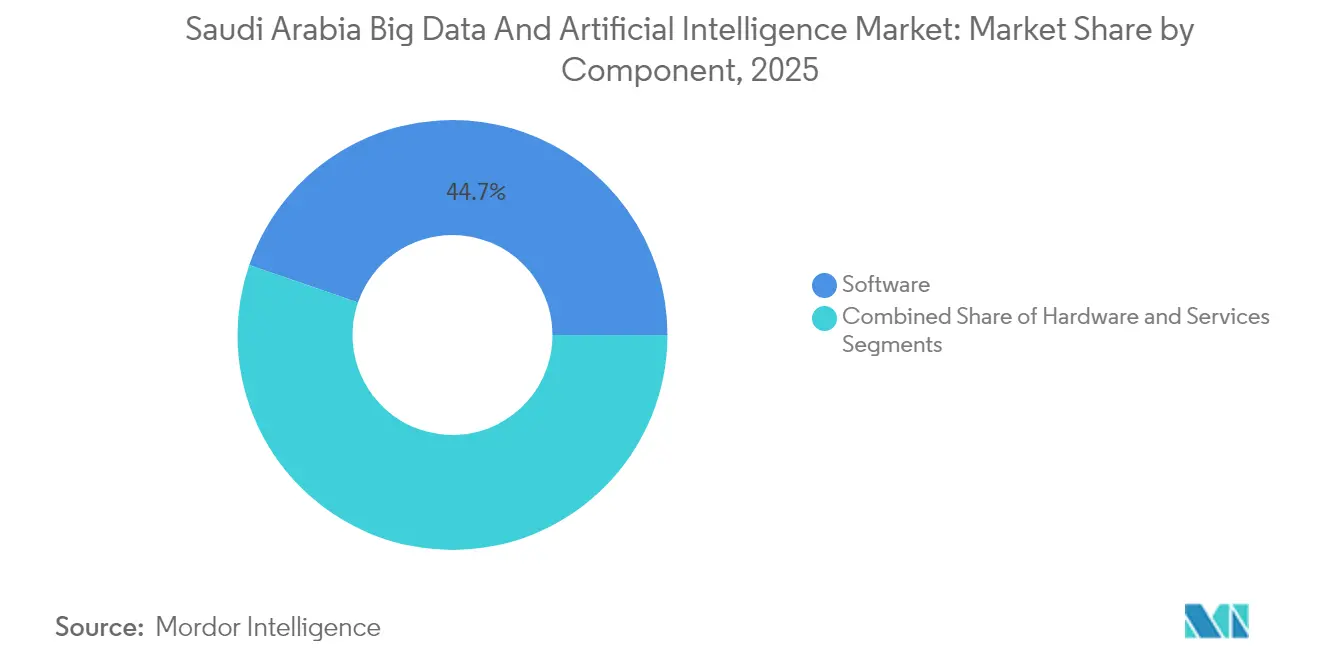

- By component, software held 44.72% of the Saudi Arabia big data and artificial intelligence market share in 2025.

- Services are projected to record the strongest 34.85% CAGR to 2031.

- By organization size, large enterprises accounted for 68.71% share of the Saudi Arabia big data and artificial intelligence market size in 2025, while SMEs are poised to climb at 36.20% CAGR through 2031.

- By end-user vertical, BFSI led with 21.34% revenue share in 2025; healthcare is advancing at a 36.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Big Data And Artificial Intelligence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National AI Strategy funding surge | +8.20% | National, concentrated in Riyadh and Eastern Province | Medium term (2-4 years) |

| NEOM sensor-data explosion | +6.80% | Northern region, spillover to national infrastructure | Long term (≥4 years) |

| Mandatory e-Invoicing roll-out | +5.10% | National, with early gains in Riyadh, Jeddah, Dammam | Short term (≤2 years) |

| Cloud-First workload migration | +4.90% | National, led by government and large enterprises | Medium term (2-4 years) |

| Green-hydrogen analytics demand | +3.70% | Eastern Province and NEOM industrial zones | Long term (≥4 years) |

| Arabic Gen-AI localisation efforts | +2.80% | National, with research hubs in Riyadh and Khobar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National AI Strategy Funding Surge

The USD 100 billion Project Transcendence budget has underwritten 14 hyperscale campuses and bulk GPU purchases that include an 18,000-GPU supercomputer delivered under the HUMAIN-NVIDIA alliance. The Public Investment Fund lifted U.S. tech allocations to USD 26.7 billion in 2024, focusing on AI chips and software. AMD and Microsoft added separate build-outs, giving Saudi developers privileged access to next-generation accelerators. These moves accelerate sovereign model training for Arabic tasks and set cost hurdles that deter late-market entrants. Businesses reap spillover gains through lower-latency domestic inference services and a maturing local talent ecosystem.

NEOM Sensor-Data Explosion

Daily data volumes in the NEOM region now exceed 1 petabyte, captured from autonomous shuttles, air-quality probes, and utility meters. DataVolt’s liquid-cooled centers near Tabuk process streams in real time for traffic routing and carbon-neutral energy balancing. Aramco and Qualcomm have co-deployed edge rigs that trim industrial energy use by 40% through predictive maintenance. The resulting trove of labelled Arabic datasets supports speech formalization, dialect mapping, and context reinforcement, sharpening regional LLM performance and enabling exportable smart-city blueprints.

Mandatory E-Invoicing Roll-Out

Phase 2 of ZATCA’s “Fatoora” mandate has produced more than 2.8 billion XML invoices, instantly accessible through standard APIs. Banks apply graph analytics to those flows to flag tax evasion, while retailers mine item-level tags for demand forecasts. SMEs, newly digitized, tap pay-as-you-go dashboards that replicate enterprise-grade insights without capex. International systems integrate seamlessly because invoices follow a globally accepted UBL schema, positioning exporters for automated reconciliation.

Cloud-First Workload Migration

Saudi cloud spend is forecast to top USD 4.7 billion by 2027 as Alibaba Cloud, Tencent, and Microsoft commission multi-zone regions. STC-Alibaba’s joint venture opened two local facilities that host encrypted multitenant AI training clusters, and Microsoft earmarked USD 1.5 billion for additional capacity. Rapid elasticity lets healthcare apps run imaging inference bursts at peak times while scaling back overnight. Lower entry thresholds entice SMEs to deploy AI services that would be infeasible in self-hosted racks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Senior data-science talent gap | -4.30% | National, most acute in Riyadh and Eastern Province | Medium term (2-4 years) |

| Fragmented data-governance standards | -3.80% | National, affecting cross-sector integration | Short term (≤2 years) |

| Legacy OT systems in oil and gas | -2.90% | Eastern Province industrial complexes | Long term (≥4 years) |

| Data-sovereignty for sensitive workloads | -2.10% | National, particularly government and defense sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Senior Data-Science Talent Gap

The SAMAI scheme aims to train 1 million citizens by 2030, yet demand already triples supply. Competing employers bid salaries 50% above Gulf averages, squeezing startup burn rates. Universities have added joint degrees with MIT and KAUST, but near-term relief depends on imported expertise paired with accelerated upskilling bootcamps.

Fragmented Data-Governance Standards

Sectoral regulators interpret the Personal Data Protection Law inconsistently, forcing firms to juggle divergent consent protocols. BFSI players often over-restrict data pooling, which hampers cross-sell models. SDAIA’s Standard Contractual Clauses promise eventual harmonization, yet until adoption widens, project approvals face costly legal reviews.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Arabic AI Innovation

Software captured 44.72% revenue in 2025, reflecting the early monetization of language models and analytics engines customized for Arabic. The Saudi Arabia big data and artificial intelligence market size for software is projected to outpace hardware because recurring license fees and platform subscriptions accelerate top-line gains. Intensified investment in ALLaM and ArabianGPT keeps localization capabilities ahead of imported products, creating defensible moats. Services, though smaller, post a 34.85% CAGR as enterprises engage integrators for data pipeline orchestration and model retraining.

Vendors bundle software with managed services, blurring segment lines yet elevating gross margins. Hyper-vertical modules now surround ERP cores, automating invoice validation, Arabic voice chatbots, and reservoir optimization. Open-source packages such as Wan2.1, downloaded more than 2.2 million times, seed ecosystems for startups building compliant toolchains. This flywheel ensures the Saudi Arabia big data and artificial intelligence market maintains localized intellectual property that circulates royalty income domestically.

By Organization Size: SME Acceleration Reshapes Market Dynamics

Large enterprises generated 68.71% of 2025 revenue after early pilots in predictive maintenance, robo-advisory, and real-time fraud detection. Their adoption curves reflect multi-year digital-core programs and captive data lakes. Yet SMEs now record a 36.20% CAGR because cloud platforms shrink entry barriers. The Saudi Arabia big data and artificial intelligence market share commanded by SMEs is expected to widen each year as subscription-based AI suites replace upfront licenses.

Government procurement quotas that favour local suppliers encourage small firms to embed AI in niche solutions, from halal-compliance scanning to Arabic sentiment analytics. Further acceleration comes from fintech open-banking rules that expose customer data via secure APIs, letting SME developers craft micro-services atop bank rails. Aggregated, these forces diversify revenue streams and lessen concentration risk in the Saudi Arabia big data and artificial intelligence market.

By End-User Vertical: Healthcare Emerges as Growth Leader

BFSI retained 21.34% revenue in 2025, with banks automating credit scoring and insurers piloting telematics-based pricing. Still, healthcare now races ahead at 36.16% CAGR through 2031, supported by Seha Virtual Hospital’s 1.6 million AI-triaged consultations and AI pathology screening at King Fahad Medical City. The Saudi Arabia big data and artificial intelligence market size allocated to healthcare is primed to jump as reimbursement codes start rewarding AI-assisted diagnostics.

Improved imaging throughput reduces referral backlogs, while symptom-triage chatbots lower primary-care visits. Regulatory sandboxes allow algorithm upgrades without restarting certification, motivating suppliers to iterate quickly. In parallel, wearable device integrations feed personalized treatment models, a trend that spills over to wellness and fitness sub-segments.

By Deployment Model: Cloud Migration Accelerates Despite Sovereignty Concerns

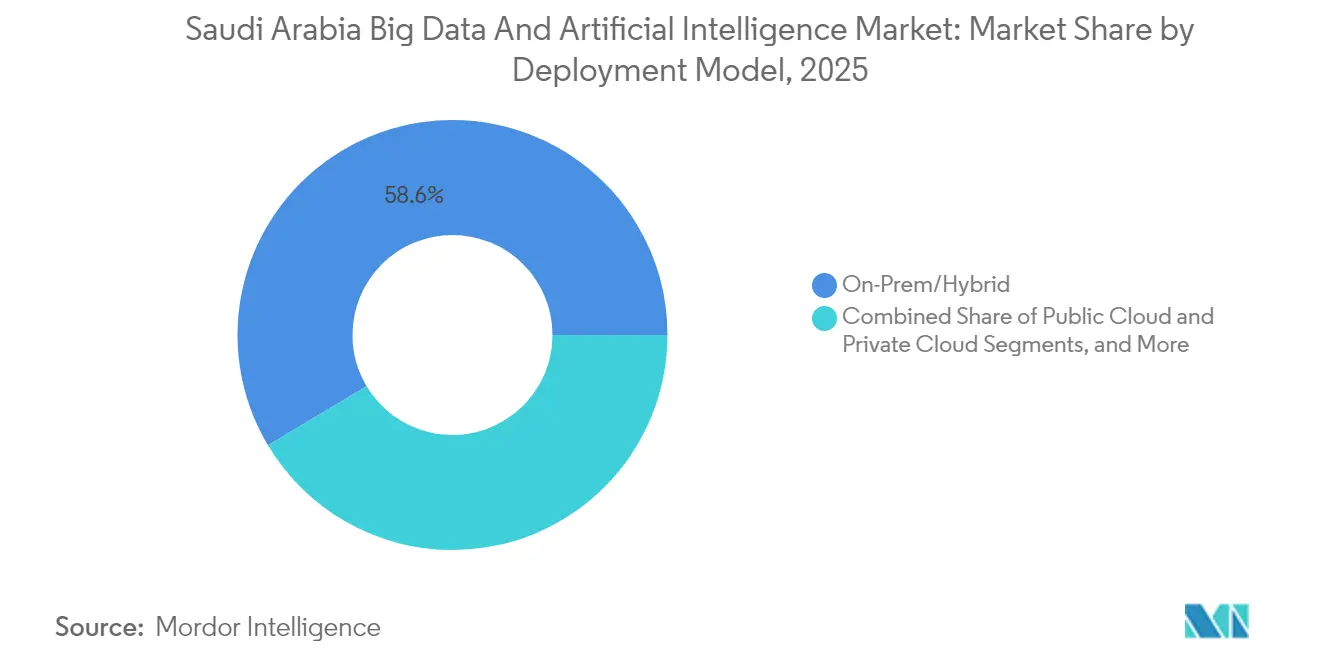

On-premises and hybrid environments secured 58.57% of 2025 spending because ministries demand physical control of sensitive data. The public cloud sub-segment, however, shows a 35.63% CAGR as clarified residency clauses ease compliance fears. Hyperscalers deliver dedicated compute zones with sovereign key management, persuading banks and hospitals to offload training runs.

Hybrid patterns dominate models trained on cloud GPUs and then deployed on local inference gateways. Such schemes exploit elasticity while limiting outbound traffic. Over time, private-cloud offerings from SCCC and Alibaba-STC blur the boundary by placing hyperscale racks in customer-owned cages. This continuum ensures the Saudi Arabia big data and artificial intelligence market continues to diversify deployment choices.

By Technology: Machine Learning Leads Practical Applications

Supervised machine learning remains the workhorse for anomaly detection, churn prediction, and dynamic pricing across retail and telecom. Businesses favour its interpretability and narrower data requirements. Deep-learning adoption accelerates where vision and language tasks dominate, assisted by NVIDIA Grace Blackwell chips now available through HUMAIN clusters. Natural language processing ranks high in strategic priority because 400 million Arabic speakers require culturally aligned interfaces.

Edge-AI applications rise as 5G coverage expands and latency budgets tighten. Aramco shows 40% energy savings via on-site inference, and NEOM’s traffic lights react in under 15 milliseconds to camera feeds. Big-data analytics platforms still supply the feature-engineering backbone, but their prominence gradually recedes as end-to-end AI pipelines merge ETL and model governance. The technology blend assures the Saudi Arabia big data and artificial intelligence market sustains both breadth and depth of use cases.

Geography Analysis

Riyadh anchors the Saudi Arabia big data and artificial intelligence market, hosting SDAIA, HUMAIN, and most venture funding. The capital’s corridor boasts five hyperscale zones that together exceed 500 megawatts of IT load. Eastern Province leverages hydrocarbons and green-hydrogen plants to justify AI optimization clusters that manage refinery throughput and renewables balancing. NEOM stands out for smart-city deployments whose data spillovers nurture nationwide model performance.

Cross-border positioning further fortifies competitiveness. Saudi data centers interconnect to Marseille and Mumbai cables, providing sub-100-millisecond latency to Europe and Asia. This geography allows the Kingdom to attract international AI workloads that seek politically stable yet energy-efficient hosting. Regulatory leadership, particularly the Personal Data Protection Law, grants legal certainty that many neighbouring states still refine, motivating multinational firms to anchor regional headquarters in Riyadh.

Provincial digitization programs extend AI outside megacities. Qassim pilots drone-based crop analytics, Asir deploys wildfire prediction, and Tabuk runs aquaculture feed optimization. These grassroots projects widen data diversity and test AI robustness in varied climates. The cumulative effect raises the floor for national AI maturity and sustains the Saudi Arabia big data and artificial intelligence market growth trajectory.

Competitive Landscape

Market structure is moderately fragmented, yet consolidation accelerates as sovereign alliances crystallize. HUMAIN’s multi-billion-dollar GPU purchases secure privileged capacity, nudging rivals to pool resources or specialize in vertical niches. Microsoft, AWS, Google Cloud, and Alibaba compete vigorously for enterprise workloads, yet must localize through joint ventures or reseller pacts to satisfy residency rules. This duality fosters coopetition: hyperscalers share infrastructure investments but diverge on platform services.

Domestic champions flourish in Arabic-centric tooling. Intelmatix applies decision-intelligence engines to logistics, Tarjama localizes enterprise content, and vminds.ai aggregates consumer apps into a super-app model. Funding rounds above USD 20 million signal maturing investor confidence. International chipmakers push reference-architecture labs in Riyadh to seed demand for their accelerators, creating downstream business for system integrators.

Edge device ecosystems also evolve. STC supplies 5G connected routers that bundle computer vision inferencing, while Aramco’s in-house AI group sells industrial models to external petrochemical firms. Vendors offering turnkey governance modules win contracts as compliance costs climb. Overall, diverse strategies ensure that the Saudi Arabia big data and artificial intelligence market continues to foster both global scale and local specialization.[4]Microsoft Corporation, “Middle East Cloud Region Expansion,” news.microsoft.com

Saudi Arabia Big Data And Artificial Intelligence Industry Leaders

Microsoft Corporation

Nvidia Corporation

Amazon Web Services Inc.

SAP SE

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HUMAIN and NVIDIA revealed plans for AI factories featuring an 18,000 NVIDIA GB300 Grace Blackwell cluster and the first Omniverse Cloud region in the Middle East.

- May 2025: DataVolt signed with Supermicro to introduce rack-scale liquid cooling for NEOM data centers, boosting energy efficiency.

- April 2025: Alibaba released the open-source short-video model Wan2.1-FLF2V-14B, surpassing 2.2 million downloads.

- March 2025: BlackRock, Microsoft, and MGX launched a USD 30 billion Global AI Infrastructure Partnership, earmarking Saudi facilities.

Saudi Arabia Big Data And Artificial Intelligence Market Report Scope

Artificial intelligence is a topic that blends computer science and robust datasets to enable problem-solving abilities. In contrast, big data refers to data sets that are complex or too large to be handled by ordinary data-processing application software.

The study analyses the current market scenario and growth trends related to the Big Data and Artificial Intelligence industries in Saudi Arabia. A view of National AI Strategies across the world is also included. The study tracks the region's country-level market dynamics and the significant implementation use cases for AI and data analytics.

The Saudi Arabia Big Data and Artificial Intelligence market is segmented by solutions (hardware, software, service), organization size (SMEs, large enterprises), and end-user (IT and telecom, retail, public and government institutions, BFSI, healthcare, energy, construction and manufacturing, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| SMEs |

| Large Enterprises |

| IT and Telecom |

| Retail and e-Commerce |

| Public and Government Institutions |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Energy (Oil, Gas and Utilities) |

| Construction and Manufacturing |

| Other End-User Verticals (Tourism, Transport, Education) |

| On-Premises / Hybrid |

| Public Cloud |

| Private Cloud |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Big-Data Analytics Platforms |

| Edge-AI |

| By Component | Hardware |

| Software | |

| Services | |

| By Organisation Size | SMEs |

| Large Enterprises | |

| By End-User Vertical | IT and Telecom |

| Retail and e-Commerce | |

| Public and Government Institutions | |

| Banking, Financial Services and Insurance (BFSI) | |

| Healthcare | |

| Energy (Oil, Gas and Utilities) | |

| Construction and Manufacturing | |

| Other End-User Verticals (Tourism, Transport, Education) | |

| By Deployment Model | On-Premises / Hybrid |

| Public Cloud | |

| Private Cloud | |

| By Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Big-Data Analytics Platforms | |

| Edge-AI |

Key Questions Answered in the Report

What is the forecast revenue for Saudi AI solutions by 2031?

The Saudi Arabia big data and artificial intelligence market is projected to reach USD 2.81 billion by 2031.

Which sector is growing fastest in AI adoption across the Kingdom?

Healthcare leads with a 36.16% CAGR, driven by telemedicine and AI diagnostics programs.

How are SMEs benefiting from Saudi AI initiatives?

Cloud-first policies and mandatory e-invoicing have lowered entry barriers, enabling SMEs to adopt pay-as-you-go AI analytics rapidly.

Why do many firms still favor on-premises deployment?

Data-sovereignty mandates for government and defense workloads keep 58.57% of deployments on-premises or hybrid.

Which geographic zones host the bulk of AI data centers?

Riyadh concentrates most hyperscale campuses, while Eastern Province and NEOM add capacity for industrial and smart-city workloads.

What is the biggest restraint on AI growth?

A senior data-science talent gap persists, with demand outpacing supply by roughly three to one, raising salary costs.

Page last updated on: