Mexico Online Gambling Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

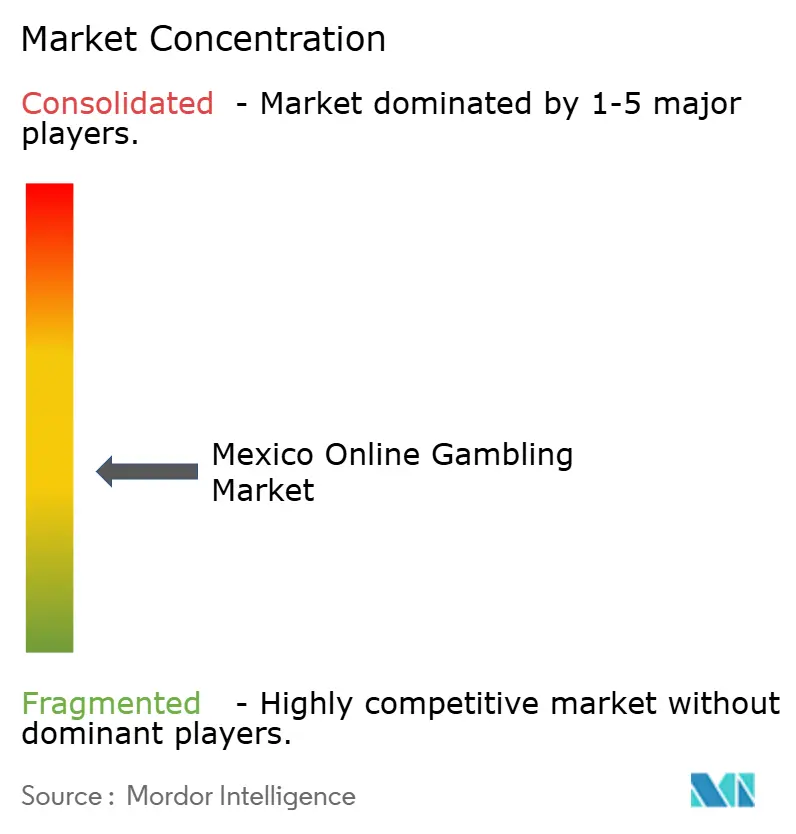

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Online Gambling Market Analysis by Mordor Intelligence

The Mexico Online Gambling Market size is projected to expand from USD 0.79 billion in 2025 and USD 0.97 billion in 2026 to USD 1.09 billion by 2031, registering a CAGR of 8.60% between 2026 to 2031. Rapid smartphone adoption, expanding payments infrastructure, and a pending overhaul of the 1947 Gaming and Raffles Law are positioning the Mexico online gambling market for sustained double-digit expansion. Licensed and grey-market operators are racing to capture a digitally native customer base that spends more leisure time on mobile screens than in physical betting shops. Momentum is amplified by the looming FIFA 2026 World Cup, which will direct unprecedented international attention toward Mexico’s regulated sports-betting channels. Meanwhile, a fragmented regulatory regime creates both opportunity and uncertainty as compliant operators face higher tax outlays while unlicensed sites retain cost advantages.

Key Report Takeaways

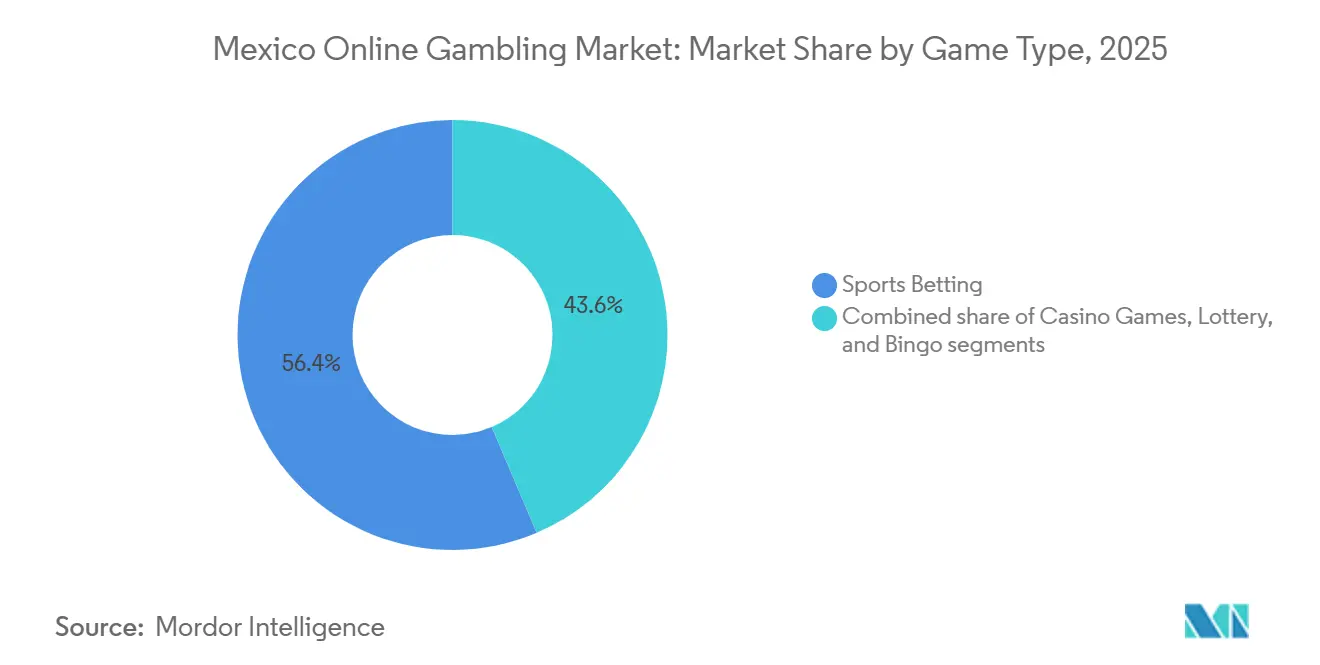

- By game type, sports betting led with 56.41% revenue share of the Mexico online gambling market in 2025, and it is projected to register the fastest 17.82% CAGR through 2031.

- By platform, mobile/tablet accounted for 63.92% of user activity across the Mexico online gambling market in 2025 and is growing at an 18.15% CAGR; desktop/laptop remains profitable but trails in growth prospects.

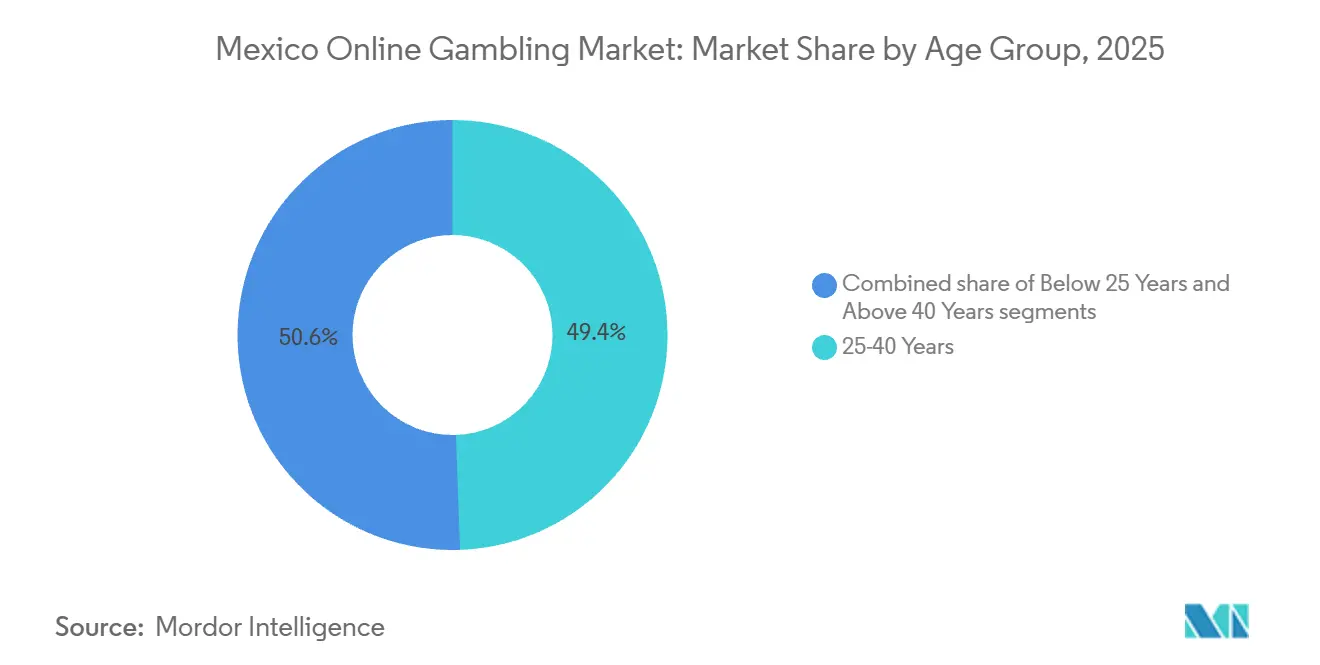

- By age group, consumers aged 25-40 commanded 49.44% of the Mexico online gambling market share in 2025, whereas the under-25 cohort is expanding at a 16.73% CAGR to 2031.

- By region, Central Mexico captured 41.27% of the Mexico online gambling market size in 2025, while North Central Mexico is pacing ahead at a 16.19% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Online Gambling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of gambling | +2.8% | National, urban centers | Medium term (2-4 years) |

| Enhanced internet connectivity and technology | +2.1% | National, rural acceleration | Long term (≥ 4 years) |

| Rising esports viewership drives betting adoption | +1.9% | National, metropolitan focus | Short term (≤ 2 years) |

| Spanish content and soccer themes drive millennial audiences | +2.3% | National, heightened by FIFA 2026 | Medium term (2-4 years) |

| Increasing popularity of sports betting | +3.1% | National, peaks during major tournaments | Short term (≤ 2 years) |

| Strong investment and revenue trajectory boosting market growth | +1.8% | Central & North Central regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of gambling

Cultural acceptance of wagering has broadened as Mexico’s 129 million residents gain access to digital entertainment and as roughly 78.6% of the population now uses the internet[1]Source: International Trade Administration, "Mexico - Internet and Digital Economy", trade.gov. With smartphones becoming widely used in major cities, more people are moving from physical casinos to online gambling platforms. According to the National Council of the Entertainment Industry, gambling in Mexico supports 150,000 direct jobs, showing its importance in the domestic gaming ecosystem. Mexico's online gambling market is growing by attracting its young population and tapping into the country's love for football. Regulatory authorities are recognizing the industry's role in generating tax revenue and creating jobs. As a result, they are helping shift the sector from unregulated markets to legal platforms, ensuring long-term growth.

Enhanced internet connectivity and technology

Mexico's "Internet para Todos" initiative is actively expanding broadband access across the country to increase household connectivity beyond the current 81.6% urban baseline. This strategic expansion is expected to create significant opportunities for growth in Mexico's online gambling market by enabling greater digital participation. In 2023, the fintech sector witnessed a substantial investment of USD 828 million, which has driven advancements in mobile wallet functionalities and accelerated the implementation of open-banking APIs under Mexico's groundbreaking Fintech Law[2]Source: Finnosummit, "Fintech in Latin America and the Caribbean", finnosummit.com. Furthermore, the establishment of rural banking-agent outlets has introduced physical cash-in points, which serve as a critical complement to digital deposit systems. These developments are effectively integrating previously underserved populations into the digital financial ecosystem, fostering greater financial inclusion and digital adoption.

Rising esports viewership drives betting adoption

Young consumers under 25 are increasingly interested in esports, with more of them starting to bet on competitive gaming. The rise in esports viewership is a key factor driving this trend, as a larger audience creates more awareness and curiosity about esports betting. This growing audience not only increases the visibility of esports betting platforms but also pushes operators to create customized betting options that suit their preferences. To attract this group, operators are designing esports betting markets similar to traditional sports betting. The fast-paced and live nature of esports fits well with the mobile-focused lifestyles of these consumers. As Mexico prepares for FIFA 2026, esports are becoming a major attraction, which could further boost interest in all types of sports betting.

Spanish content and soccer themes drive millennial audience

Football is the most popular sport in Mexico and a key part of its culture. Platforms aiming to attract millennials have found that using Spanish-language interfaces gives them an advantage. By including soccer-related themes and offering content in Spanish, these platforms connect better with millennials and make their services more relevant. Soccer-focused promotions, such as special offers on match days and localized commentary, strongly appeal to this group, creating a more engaging and personalized experience. Spanish-language content also makes these platforms more accessible and inclusive, which helps build trust and loyalty among millennial users. Licensed bookmakers are focusing on strategies like investing in local commentary, match-day promotions, and culturally relevant messages about responsible gambling. With Spanish-language consumer-protection materials now matching the quality of English ones, operators can expand their marketing efforts without regulatory issues, boosting the growth of Mexico's online gambling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty and cybersecurity threats | -1.7% | National, acute in border zones | Short term (≤ 2 years) |

| Tax regulations impact Mexican gaming market profitability | -2.4% | National | Medium term (2-4 years) |

| Persistent grey/off-shore competition | -1.9% | National, urban concentration | Long term (≥ 4 years) |

| Limited Spanish responsible-gambling programs | -1.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory uncertainty and cybersecurity threats

Operators are struggling with the outdated 1947 statute, while the 2025 reforms are still being finalized. Mexico's gambling industry is facing major security and compliance challenges as companies try to manage old regulations while preparing for upcoming changes. The country also faces serious money laundering risks, mainly caused by drug trafficking and organized crime, which funnel billions through the financial system every year. Cybersecurity weaknesses make these issues worse. Inconsistent regulations make it harder for operators to create strong compliance systems. To address these problems, companies need better monitoring tools and stricter internal controls, which add more pressure on their resources. These challenges are especially difficult for smaller operators and discourage international companies, slowing the short-term growth of Mexico's online gambling market.

Tax regulations compress profitability for compliant firms

In Mexico, operators face a 30% corporate income tax and a charge on Gross Gaming Revenue, both set by the Ministry of the Interior, though states can apply their own rules. For instance, Jalisco's Treasury Commission has added a 7% tax on Gross Gaming Revenue under its State Revenue Law, specifically targeting gambling activities. These taxes, along with other excise duties and withholding requirements, raise compliance costs for licensed operators. On the other hand, grey-market competitors avoid these taxes and regulations, creating an unfair competitive environment. In its 2024 filings, Codere Online highlighted the heavy tax burden in Mexico, explaining that these challenges reduce profit margins. This is in sharp contrast to offshore operators, who face fewer restrictions and lower costs. While many operators are pushing for unified tax rates to create fair competition, ongoing differences in taxation and compliance rules continue to hold back the growth of Mexico's online gambling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Sports Betting Extends Lead on Event-Driven Momentum

In 2025, sports betting accounted for 56.41% of the market and is projected to grow at a 17.82% CAGR through 2031. This growth reflects Mexico's strong connection to soccer and its role as a co-host for the FIFA 2026 World Cup. Traditional table games and live-dealer formats continue to attract players by offering a realistic gaming experience online. In Central Mexico, more land-based players are moving to hybrid options that combine live video with on-screen betting, driving the growth of casino games.

Lottery products, deeply rooted in Mexican culture, are growing steadily but at a slower pace, as players focus on winning large jackpots. Bingo, the smallest segment, is seeing renewed interest due to social-play features and charity-focused initiatives that appeal to older audiences. Together, these segments create a balanced revenue mix, helping to stabilize the Mexican online gambling market during times when sports betting activity slows down.

By Platform: Mobile Dominance Mirrors Smartphone Economy

Mobile/tablet accounted for 63.92% of all stakes in Mexico's online gambling market and is projected to grow at an 18.15% CAGR through 2031. This underscores the pivotal role of handheld screens in user acquisition strategies. Progressive web apps and native Android downloads now provide seamless access to both betting and casino content through a single wallet. While desktops still cater to multi-screen users seeking broader odds grids and data visualization tools, their market share is poised to decline. This is largely due to the advent of 5G networks and more affordable devices, which are diminishing latency issues on mobile.

In Mexico's online gambling landscape, banking agents play a crucial role, facilitating the transition from cash to digital. This is especially vital for rural populations that still lean towards physical currency. However, security remains a paramount concern. Platforms that invest in two-factor authentication and tokenized payment flows are witnessing improved conversion and retention rates. This trend underscores a vital insight: in the mobile realm, trust translates directly to lifetime value.

By Age Group: Millennials Anchor Volume While Gen Z Drives Velocity

Millennials aged 25-40 make up 49.44% of the Mexican online gambling market. They often use their disposable income to bet on soccer leagues and international tournaments. Their betting habits developed during Mexico’s early mobile internet growth, making them loyal app users and ideal customers for casino content. To engage this group, operators focus their marketing efforts on customer lifetime value. They also use soccer-themed jackpots to maintain interest among millennial players.

At the same time, the under-25 age group is growing quickly, with a projected CAGR of 16.73% through 2031. This younger demographic, heavily reliant on smartphones, is showing more interest in gambling and is becoming an important part of the market. For instance, data from the National Institute of Statistics and Geography (INEGI) reveals that in 2024, those aged 18 to 24 spent an average of 5.7 hours daily on their devices, closely trailed by the 25 to 34 age bracket at 5.6 hours [3]Source: National Institute of Statistics and Geography (INEGI), "National Survey on the availability and use of information in households", inegi.org.mx. Such increased screen time has amplified exposure to online gambling platforms, which frequently tailor advertisements and promotions to target these age groups.

Geography Analysis

In 2025, Central Mexico held a 41.27% share of the country's online gambling market, supported by its large population, higher income levels, and strong LTE network. This leadership is further reinforced by widespread internet access, many banking outlets, and partnerships with club operators. These factors help lower customer acquisition costs and improve loyalty programs, such as free-bet credits for Liga MX matches. However, as the market becomes more saturated, marketing costs are increasing, leading companies to focus on CRM segmentation instead of broad advertising strategies.

North Central Mexico is growing rapidly, with a 16.19% CAGR, making it an important area for expansion. Platforms are offering customized odds for popular MLB and NFL games in the region. Industrial towns with reliable 4G networks and higher wages are boosting ticket values. Tax revenues from this region are becoming essential for state budgets, prompting stricter regulation of unlicensed sites. While northern regions benefit from dual-currency income and a strong digital presence, southern areas, which rely on cash deposits through OXXO stores, are expected to grow significantly, making the shift from traditional to online gambling easier.

Northern states are seeing strong growth, driven by high remittance flows and the influence of U.S. media, which has increased user engagement. In the south, although the market is smaller, it is expanding. Programs like “Internet para Todos” are improving rural internet access, unlocking new opportunities in areas that previously had only a few physical betting locations.

Competitive Landscape

Mexico's online gambling market is moderately fragmented, with operators using strategic marketing efforts to expand their product range. Many companies are forming partnerships and offering both casino and sports betting options to attract more customers and strengthen their market presence.

Key players like Grupo Caliente, Codere Online Luxembourg S.A., Bet365 Group Ltd, Novibet USA Inc., and Super Group Ltd. are customizing their services to match local entertainment preferences. These companies provide Spanish-language services and include culturally relevant features, such as traditional casino themes, to connect better with their audience. They are also working with specialized service providers to create easy-to-use platforms, improving user experience and operational performance.

Operators are focusing on factors like responsible gambling, Spanish-language customer support, and improving mobile apps to stand out in the market. Offshore operators face challenges as SEGOB, the regulatory authority, plans to introduce a nationwide registry to address fiscal non-compliance. To prepare, licensed operators are launching Spanish-language self-exclusion tools and simplifying Know Your Customer (KYC) processes. These efforts aim to build customer loyalty and secure their position in the market. With upcoming regulatory changes expected to reshape the industry, these strategies are crucial for staying competitive in Mexico's online gambling sector.

Mexico Online Gambling Industry Leaders

-

Grupo Caliente

-

Codere Online Luxembourg S.A.

-

Bet365 Group Ltd

-

Novibet USA Inc.

-

Super Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Betway signed Andrés Guardado as Betway’s brand ambassador across Mexico and Latin America. Known affectionately as ”El Principito” among fans, for his leadership qualities on the pitch, Guardado represented Mexico at five FIFA World Cups between 2006 and 2022, to attract more players.

- April 2026: 7777 Gaming entered into a partnership with Playdoit Mexico, an established operator with a strong presence in the Mexican market. Through this partnership, Playdoit integrated the complete 7777 Gaming portfolio, expanding its content offering with a diverse selection of titles. Through this collaboration, Playdoit provided players with seamless access to more than 200 online games.

- March 2026: RubyPlay entered into a strategic partnership with Codere Online to strengthen its expansion across the Latin American iGaming market, particularly in Mexico. Through the collaboration, RubyPlay integrated its portfolio of slot games into Codere Online’s platform, enabling broader access to localized and market-focused gaming content for players across Codere’s Spanish-speaking markets.

- February 2026: Logrand Entertainment Group announced a partnership with global business-to-business (B2B) gaming technology provider Bragg Gaming Group through its subsidiary ORYX Gaming to expand its presence in the Mexican market. Through this agreement, ORYX content will be made available to players through Logrand’s online brand in Mexico, Strendus Casino.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Mexico's online gambling market as all licensed, real-money wagering activity, sportsbooks, casino games, poker, bingo, and lotteries offered through internet-connected desktop, mobile, or tablet interfaces to players physically located in Mexico and measured on gross gaming revenue. According to Mordor Intelligence, this digital pool was valued at about USD 0.97 billion in 2025 and is projected to reach nearly USD 1.96 billion by 2030.

Scope exclusion: Land-based casino turnover and revenue generated by offshore operators that do not hold a Mexican license are excluded.

Segmentation Overview

-

By Game Type

- Sports Betting

- Casino Games

- Lottery

- Bingo

-

By Platform

- Desktop/Laptop

- Mobile/Tablet

-

By Age Group

- Below 25 Years

- 25-40 Years

- Above 40 Years

-

By Region (Mexico)

- North

- North Central

- Central

- South

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed regulators, payment processors, sportsbook managers, and marketing affiliates across Mexico City, Monterrey, Guadalajara, and Tijuana. These discussions validated consumer funnel metrics, bonus-related churn, and average hold percentages and helped fine-tune assumptions where public data were silent.

Desk Research

We began with publicly available data from Secretaría de Gobernación (licensing registry), INEGI household ICT surveys, Banco de México currency bulletins, Telcel and América Móvil subscriber statistics, and peer-reviewed journals that track online wagering behavior. Company 10-Ks, operator investor decks, and trade association white papers (e.g., AIEJA, IBIA) supplemented usage metrics, ARPU trends, and tax flows. Paid databases such as D&B Hoovers and Dow Jones Factiva filled financial gaps and historical news. This list is illustrative; dozens of additional sources were tapped for cross-checks and clarification.

Market-Sizing & Forecasting

We anchor the 2025 baseline with a top-down rebuild of licensed operator GGR reported to SEGOB, reconciled to net receipts disclosed in financial filings, and then corroborated through targeted bottom-up channel checks on monthly active users and sampled average spend. Key variables like smartphone penetration, mobile data cost, debit card issuance, major sports calendar effects, and federal GGR tax take feed a multivariate regression that drives the 2026-2030 forecast. Scenario runs flag sensitivity to regulatory reform timing, FX swings, and sports mega-events. Where operator roll-ups lacked detail, gaps were bridged by applying validated hold rates to verified betting volumes.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance screens versus historical SEGOB tax receipts, and peer comparison. Models refresh annually; any mid-year legal or fiscal shock triggers an interim update, and a final sense-check is completed before each client delivery.

Why Our Mexico Online Gambling Baseline Commands Trust

Published estimates often differ because firms choose dissimilar product mixes, data vintages, and currency treatments.

Key gap drivers here include whether social gaming is bundled, how offshore traffic is handled, and if headline numbers reflect GGR or turnover. Mordor's figures stick to licensed real-money GGR, convert monthly pesos at average yearly FX, and are refreshed every twelve months, which often narrows inflation-driven distortion seen elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.97 B (2025) | Mordor Intelligence | - |

| USD 1.62 B (2024) | Global Consultancy A | Includes land-based and offshore sites; relies on single top-down estimate without operator checks |

| USD 0.91 B (2023) | Industry Data Provider B | Omits in-play sports and uses constant 2023 FX; limited platform coverage |

These comparisons show that once scope, metric, and FX choices are aligned, Mordor's disciplined, annually refreshed approach offers decision-makers a balanced, transparent baseline that can be replicated and stress-tested with publicly traceable inputs.

Key Questions Answered in the Report

What is the current size of the Mexico online gambling market?

The Mexico online gambling market stands at USD 0.97 billion in 2026 and is projected to reach USD 1.09 billion by 2031.

Which game type generates the most revenue in Mexico’s online space?

Sports betting leads with 56.41% share and is expected to grow at a 17.82% CAGR through 2031.

How important are mobile platforms in Mexico’s online gambling landscape?

Mobile accounts for 63.92% of all user engagement and is on track for an 18.15% CAGR, reflecting Mexico’s smartphone-first economy.

How will the 2026 FIFA World Cup affect Mexico’s online gambling market?

The World Cup is expected to boost user acquisition and betting volume, especially for operators with sports-centric content and scalable mobile infrastructure.

Page last updated on: