Market Overview

| Study Period | 2021 - 2031 |

|---|---|

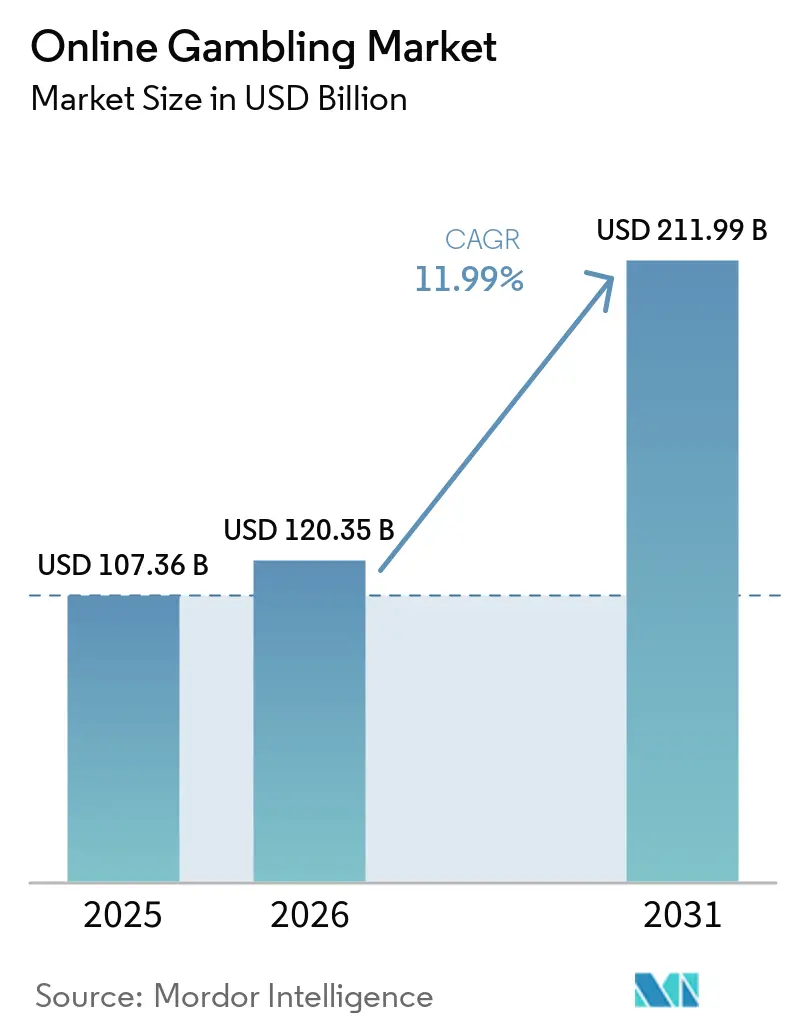

| Market Size (2026) | USD 120.35 Billion |

| Market Size (2031) | USD 211.99 Billion |

| Growth Rate (2026 - 2031) | 11.99% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Online Gambling Market Analysis by Mordor Intelligence

Online gambling market size in 2026 is estimated at USD 121.93 billion, growing from 2025 value of USD 107.36 billion with 2031 projections showing USD 211.99 billion, growing at 11.99% CAGR over 2026-2031. Factors such as the rising penetration of smartphones, the widespread rollout of 5G, and increasingly harmonized regulations across major jurisdictions are driving a swift migration to digital channels. As of 2024, the GSM Association (GSMA) reports North America leading globally in 5G adoption, boasting a rate of 55%, trailed closely by Greater China[1]Source: GSM Association (GSMA), "The Mobile Economy", www.gsma.com. Operators are harnessing live streaming, AI-driven odds engines, and cloud-native architectures, often eclipsing the immersive experiences of traditional land-based venues. With real-time data feeds, operators can manage hundreds of micro-markets for each sporting event, boosting both the frequency of bets and the average ticket size. On the regulatory front, governments are embracing the new tax revenues, viewing regulated iGaming not just as a fiscal tool in the post-pandemic landscape but also as a manageable alternative to gray-market activities, driving the market's growth.

Key Report Takeaways

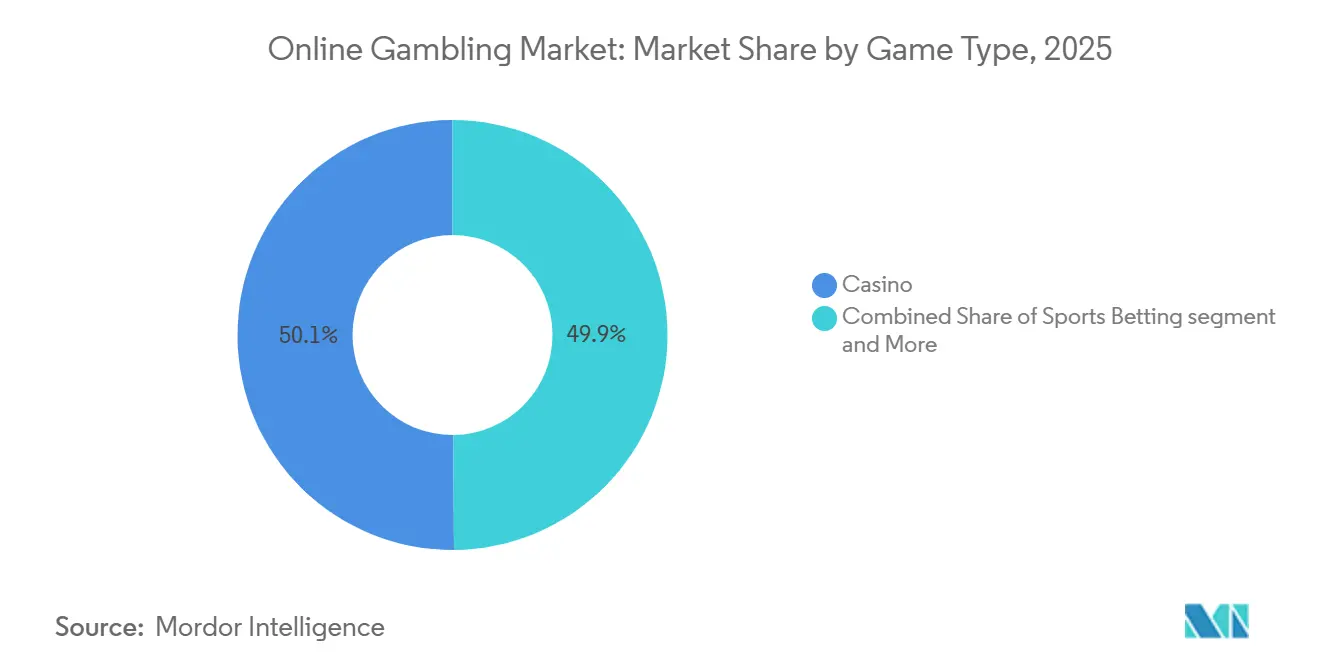

- By game type, casino led with 50.12% of the online gambling market share in 2025 and is forecast to grow at a 12.61% CAGR through 2031, the highest among all game segments.

- By platform, mobile and tablet captured 57.14% revenue share in 2025, and are projected to post the fastest 14.65% CAGR between 2026-2031.

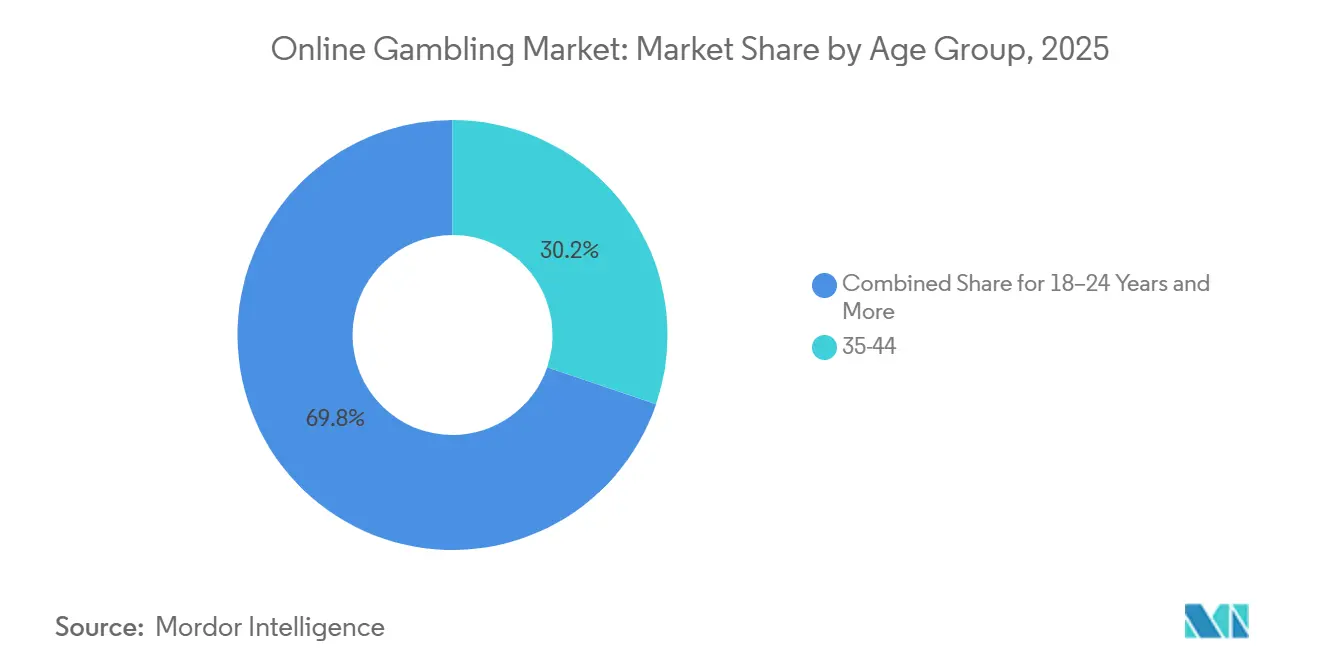

- By age group, users aged 35-44 years accounted for 30.22% of the global customer base in 2025, while users aged 25-34 Years are projected to post the fastest 14.59% CAGR between 2026-2031.

- By betting type, pre-match/fixed odds wagering represented 56.29% of betting activity in 2025 and live/in-play segment is advancing at a 13.79% CAGR through 2031.

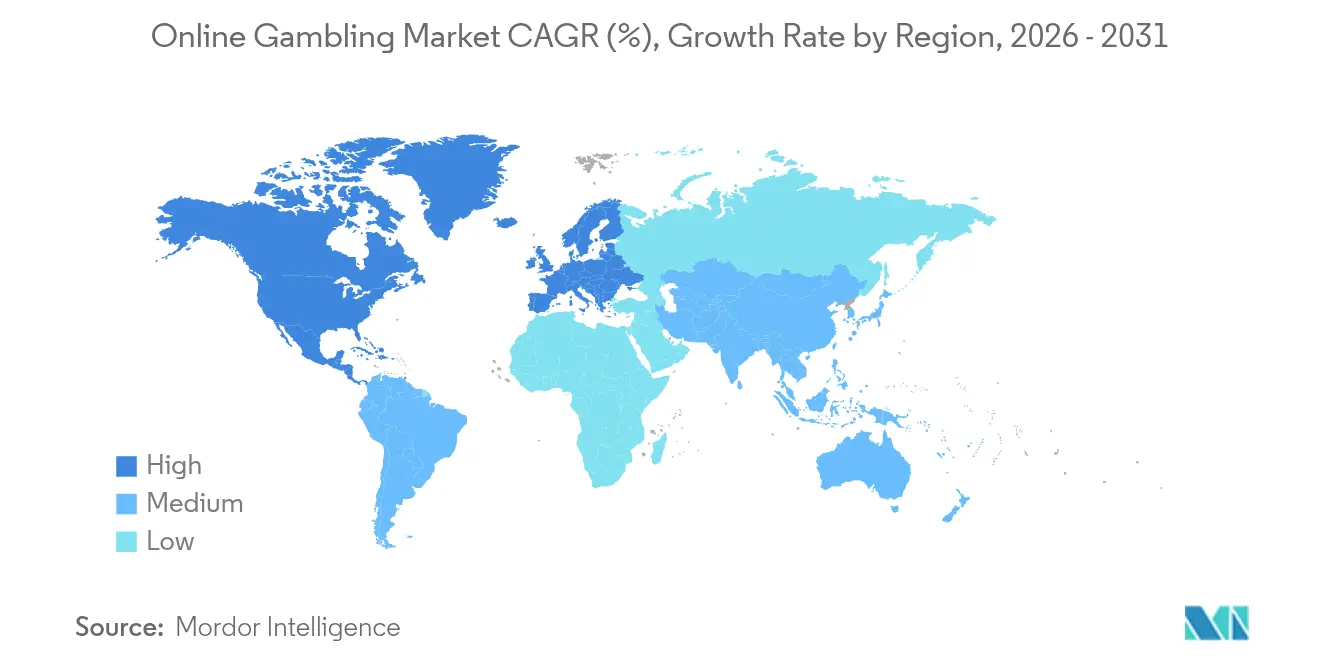

- By geography, Europe commanded 49.25% revenue share in 2025, while North America is accelerating at a 16.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Gambling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancement of Digital Technologies | + 2.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Legalization and Regulatory Liberalization | + 3.2% | North America, Latin America, the Middle East | Long term (≥ 4 years) |

| Live Betting and Real-Time Streaming | + 2.1% | Global, strongest in Europe and North America | Short term (≤ 2 years) |

| Improved Payment Solutions | + 1.7% | Global, with emphasis on emerging markets | Medium term (2-4 years) |

| Blockchain Technology | + 0.9% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Personalized User Experience | + 1.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancement of Digital Technologies

Advancements in digital technology are reshaping online gambling, evolving it from static web platforms to dynamic, AI-driven ecosystems that tailor experiences to individual users in real-time. By harnessing artificial intelligence and machine learning, operators can now analyze betting patterns, forecast user behavior, and fine-tune offerings with unmatched accuracy, gaining a competitive edge that's elusive for traditional operators. Today's platform development is dominated by mobile-first strategies, with operators pouring resources into progressive web applications and native mobile experiences, bringing console-quality gaming to smartphones. The synergy of 5G networks and edge computing slashes latency to almost nothing, facilitating live dealer experiences and real-time sports betting that can compete with being there in person. With the adoption of cloud infrastructure, operators can swiftly expand across various jurisdictions, all while adhering to local data residency mandates. This compliance is paramount as regulatory bodies place increasing importance on data sovereignty and safeguarding consumer rights.

Legalization and Regulatory Liberalization

Regulatory liberalization stands as the foremost structural force reshaping the global online gambling arena. Governments are increasingly acknowledging digital platforms as legitimate revenue streams, crafting frameworks that harmonize economic gains with consumer safeguards. The U.S. spearheads this evolution, legalizing gambling state by state. The National Council of Legislators from Gaming States is at the forefront, crafting model legislation that standardizes tax rates between 15% and 25% on adjusted gross revenue, ensuring operators face predictable environments. Brazil's Law 14.790/2023, cited by Brazil’s Secretariat of Prizes and Betting, showcases the regulatory maturity of emerging markets, mandating operators to set up headquarters in Brazil and adopt thorough responsible gaming protocols, all while raking in an estimated USD 4.5 billion in annual tax revenue[2]Source: Brazil’s Secretariat of Prizes and Betting, "www.gov.br. The UAE's launch of the General Commercial Gaming Regulatory Authority signifies a major shift in the Middle East, potentially turning the region into a magnet for licensed operators eyeing affluent demographics and tourism-centric markets. Meanwhile, France's ambition to legalize online casinos by 2025 hints at a broader European market expansion, moving past the confines of traditional sports betting. The Ministry of Economy and Finance in France projects revenues from these newly regulated activities could soar between EUR 748 million and EUR 1.5 billion.

Live Betting and Real-Time Streaming

The integration of live betting with real-time streaming technology enhances user engagement by converting passive viewing into interactive wagering opportunities. This integration allows operators to provide micro-betting options on specific game events, such as predicting the next pitch in baseball or the next possession in basketball. These features create multiple betting opportunities within individual sporting events, surpassing the limitations of traditional pre-match betting. Through streaming partnerships with major sports leagues, operators gain access to exclusive content and data feeds, which support their in-play pricing models. This access creates significant barriers to entry for new competitors. The combination of real-time statistics and augmented reality features in streaming platforms makes betting a natural part of sports viewing, particularly appealing to younger users. Advanced technology infrastructure, including edge computing and content delivery networks, maintains synchronization between streaming and betting interfaces, protecting operator profitability and ensuring platform reliability.

Improved Payment Solutions

The online gambling industry benefits from advanced payment solutions that address key operational challenges. Digital wallets, cryptocurrency integration, and instant settlement systems reduce transaction processing times from days to seconds while making services accessible to more users. Blockchain-based payment systems enable cross-border transactions without traditional banking intermediaries, particularly in markets where conventional financial institutions limit gambling-related transactions. Account-to-account transfers through open banking initiatives in Europe and the UK eliminate the need for card networks, lowering transaction costs and providing immediate deposit confirmation. In jurisdictions with restricted traditional payment methods, cryptocurrencies like Bitcoin and Ethereum offer alternative transaction options while maintaining compliance through blockchain traceability. Buy-now-pay-later services and digital credit solutions increase market accessibility, though operators must manage these offerings within responsible gambling frameworks and regulatory requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Taxation and Licensing Costs | -1.8% | Global, particularly acute in newly regulated markets | Medium term (2-4 years) |

| Cybersecurity and Fraud Risks | -1.2% | Global, with a higher impact in emerging markets | Short term (≤ 2 years) |

| Payment Processing Limitations | -0.9% | Emerging markets, regions with banking restrictions | Medium term (2-4 years) |

| Negative Public Perception and Social Stigma | -0.7% | Conservative markets, religious jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Taxation and Licensing Costs

High taxation and licensing costs create significant barriers to market entry while compelling established operators to improve operational efficiency and pursue economies of scale through consolidation or geographic expansion. Brazil's regulatory framework demonstrates this challenge, with operators facing a 12% tax on gross gaming revenue and licensing fees up to USD 6 million from January 2025 under Law No. 14,790/2023, as reported by Brazil's Secretariat of Prizes and Betting (SPA). These requirements create substantial capital barriers that benefit large multinational operators over local companies. Illinois's tiered tax structure, which increases rates based on operator revenue levels, shows how taxation can inhibit market growth by imposing higher effective tax rates on successful operators, limiting their ability to reinvest. In some jurisdictions, the combined federal, state, and local taxes reach up to 40% of gross gaming revenue, requiring operators to reduce marketing expenses, restrict bonus offerings, or increase house edges to maintain profit margins. The varying licensing costs across jurisdictions influence operator strategy, with companies prioritizing markets that provide favorable tax conditions and efficient regulatory processes instead of broad geographic expansion.

Cybersecurity and Fraud Risks

Cybersecurity threats and fraud risks not only inflate operational costs but also challenge regulatory compliance, risking license suspensions or revocations. This underscores the importance of security infrastructure investments, elevating them from mere compliance necessities to vital competitive differentiators. The online gambling sector grapples with sophisticated threats: from account takeovers and payment frauds to bonus abuses, often executed through coordinated bot networks and identity theft. Advanced persistent threats zero in on customer databases and financial systems. When breaches occur, they lead to regulatory fines, costs for customer compensation, and reputational harm, jeopardizing market standing and customer acquisition efforts. Implementing robust fraud prevention measures like multi-factor authentication, behavioral biometrics, and real-time transaction monitoring demands hefty technology investments and ongoing operational costs. These burdens weigh heavier on smaller operators, who often lack the advantages of economies of scale. As regulatory mandates for data protection and incident reporting evolve, the European Union's General Data Protection Regulation (GDPR) stands out as a global benchmark, shaping compliance frameworks worldwide. This evolution adds layers of operational complexity for operators catering to diverse markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Sports Betting Drives Market Leadership

In 2025, casinos held a dominant 50.12% market share by leveraging the widespread appeal of mainstream sports and benefiting from regulatory advantages over traditional casino games in several jurisdictions. Casino games have thrived due to innovations such as live dealers and mobile-optimized slots, which enhance user engagement and accessibility. Meanwhile, the lottery segment continues to perform strongly, supported by robust government partnerships and a dedicated consumer base. Although bingo remains a niche segment, it maintains steady popularity in regions like the UK and parts of Europe, driven by cultural familiarity.

Sports betting's advantage stems from its perceived skill element and societal acceptance, smoothing its journey to regulatory approval and consumer adoption. This is especially evident in markets where traditional casino games encounter challenges. Football betting leads the pack, followed closely by horse racing, which boasts a robust infrastructure, and tennis, with its consistent year-round tournaments. Data from the Gambling Commission reveals that on-course horse race betting in Great Britain achieved an annual turnover exceeding GBP 238 million from April 2022 to March 2023, a notable increase from GBP 151.86 million the previous year. Furthermore, the fusion of fantasy sports with social betting features is crafting hybrid experiences, enabling operators to diversify their offerings and appeal to a broader audience with varied preferences and risk appetites.

By Platform: Mobile Dominance Reshapes User Behavior

In 2025, mobile and tablet platforms accounted for 57.14% of the global online gambling market, underscoring the growing popularity of smartphone-based gaming and betting. This segment is expected to grow at a CAGR of 14.65% through 2031, driven by increasing smartphone usage, improved mobile internet connectivity, and the rising adoption of mobile-first gambling apps. To meet user demands, operators are enhancing mobile platforms with features such as biometric login, push notifications, and easy payment options, making gambling more convenient and engaging.

Desktop platforms, however, still hold a significant role in the online gambling market, especially for users who prefer detailed betting analysis and longer gaming sessions. Many players favor desktops for their larger screens, the ability to use multiple windows, and a more stable experience during complex betting activities. Despite this, the market's growth is increasingly driven by the convenience of mobile and tablet platforms, which allow users to gamble anytime, anywhere through dedicated apps or browser-based platforms, making them a preferred choice for many.

By Age Group: Millennial Preferences Shape Market Evolution

In 2025, the 35-44 age group commands a 30.22% share of the market, underscoring their digital fluency and disposable income. Meanwhile, the 15-34 segment is projected to grow at a 14.59% CAGR through 2031, signaling a shift towards more interactive and socially-driven gambling experiences. Older age groups, while loyal to traditional brands and game formats, are increasingly embracing mobile platforms as these become more user-friendly. This generational gap shapes product development, with younger users pushing for gamification, social features, and cryptocurrency payments elements that older users might view as superfluous or perplexing.

Regulatory bodies are honing in on age verification and responsible gambling, often targeting younger players with measures like spending caps, session time limits, and enforced breaks to curb potential gambling issues. The growth of the 18-24 demographic isn't just about numbers; it's also about a rising legal gambling age as jurisdictions warm up to online gambling, presenting operators with a ripe opportunity for tailored marketing and age-suitable products. However, with many regions imposing marketing and advertising constraints, operators find themselves walking a tightrope, appealing to the youth while adhering to regulations. This has birthed advanced targeting methods, leaning more on behavioral insights than mere age demographics.

By Betting Type: Live Wagering Transforms Engagement Models

In 2025, pre-match/fixed odds betting captured a 56.29% market share, underscoring its triumph in turning passive sports viewers into active participants. Live/In-play is projected to have a 13.79% CAGR through 2031, this growth is largely attributed to advancements in real-time data processing and the optimization of mobile platforms. Meanwhile, pre-match/fixed-odds betting retains a robust market presence, bolstered by traditional customer preferences and a familiarity with regulations. This is especially evident in regions where live betting encounters technical or legal hurdles, limiting what operators can offer. The edge of live betting lies in its ability to boost engagement frequency and elevate average bet amounts, as users capitalize on evolving game situations and multiple wagering chances during events.

Establishing a technological backbone for live betting presents competitive hurdles, favoring seasoned operators equipped with advanced risk management and real-time data collaborations with sports leagues and data sources. As operators juggle thousands of concurrent bets, ensuring accurate odds and thwarting arbitrage opportunities is paramount to safeguarding profitability. The fusion of live streaming with in-play betting amplifies user engagement, extending session durations and enhancing lifetime value. This synergy underscores the hefty tech investments needed to provide smooth real-time experiences across diverse sports and betting markets.

Geography Analysis

In 2025, Europe accounted for a dominant 49.25% of global revenues, amounting to a substantial USD 52.15 billion. However, the region's CAGR is stalling as mature markets tighten their grip on advertising codes and impose bonus caps. Germany's lenient approach and the Netherlands' merit-based licensing are channeling grey operations into regulated platforms. This move not only safeguards tax revenues but also moderates headline growth. Meanwhile, Nordic leaders are pioneering harm-prevention measures, leveraging tools like AI-driven risk scoring and enforced loss limits.

North America's regulatory shift is yielding a robust 16.56% CAGR, the fastest among regions. The U.S. gross handle surged from USD 93 billion in 2024 to USD 110 billion in 2025, spurred by twelve states approving mobile sports wagering, as reported by the National Council of Legislators from Gaming States. Ontario's liberalized market approach is evident, with first-year receipts surpassing CAD 1.4 billion (USD 1.1 billion). The continent's online gambling landscape is heating up, underscored by cross-border merger and acquisition activities like DraftKings' acquisition of Jackpocket, highlighting the race for user bases and advanced technology.

Asia-Pacific, while brimming with potential, grapples with policy fragmentation. PAGCOR's withdrawal from offshore licensing has curtailed the region's hub capacity. In India, state-specific regulations swing between leniency and strictness. Yet, with high mobile engagement and an increasing acceptance of e-wallets, there's a promising upside once regulatory harmonization is achieved.

Latin America's fortunes hinge on Brazil's anticipated January 2025 launch. While Brazil's stipulations like mandatory local headquarters and a 12% GGR tax pose challenges, the nation's vast consumer market is too enticing to ignore. Both Argentina and Colombia exemplify the benefits of stable returns when there's clarity at either provincial or federal levels.

The Middle East and Africa's spotlight is on the UAE, marking its debut with a casino license. Wynn's ambitious USD 5.1 billion complex in Ras Al Khaimah, unveiled in October 2024, hints at a grander vision for entertainment-led economic diversification, potentially inspiring neighboring GCC states. While South Africa enjoys steady growth under the watchful eye of its National Gambling Board, Nigeria and Kenya are championing mobile sports betting, leveraging airtime-credit systems.

Competitive Landscape

The global online gambling market is moderatly fragmented and tech-savvy multinationals and nimble regional players dominate the online gambling landscape. In May 2025, Flutter Entertainment bolstered its presence in South America, acquiring a 56% stake in NSX Group for USD 350 million. This move seamlessly integrated its FanDuel tech stack with Brazil’s Betnacional brand. Meanwhile, Entain, pouring over USD 100 million each year into AI-driven risk controls, fortifies itself against tightening AML audits.

In 2025, DraftKings' merger with Jackpocket not only integrated digital lottery services into a unified wallet but also enhanced cross-selling efficiency, broadening potential spending beyond traditional sportsbook offerings. Kindred Group, leveraging a proprietary churn-prediction model, boasts a 13% retention advantage over cohort benchmarks, underscoring the rising significance of data science in the sector.

Localized independent operators, attuned to cultural nuances like payment preferences, language, and local leagues, are strategically positioning themselves, often before acquisition offers materialize. Compliance capabilities are becoming pivotal in determining the pace of market entry; operators equipped with ISO-27001 data protocols and multi-jurisdictional audit logs find themselves securing licenses more swiftly than newcomers. Consequently, the top five brands now hold approximately 45% of the market share, painting a picture of moderate concentration, yet leaving ample space for innovation-driven newcomers.

Online Gambling Industry Leaders

-

Flutter Entertainment PLC

-

Entain PLC

-

Bet365 Group Ltd

-

DraftKings Inc.

-

Betsson AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Evolution secured an exclusive deal with Hasbro to develop and distribute online casino games based on iconic Hasbro brands such as Monopoly, Clue, and Battleship. This partnership expanded Evolution’s branded content offerings and strengthened its leadership in live casino experiences.

- April 2025: Caesars expanded its partnership with AGS to bring the Triple Coin Treasures slot family online for the first time, making Caesars’ online casino platforms the exclusive home for these fan-favorite games in multiple states of the United States, including New Jersey and Pennsylvania.

- December 2024: DraftKings completed a major acquisition of 888 Holdings, combining its strong presence in the United States with 888’s extensive portfolio in Europe and Latin America. This merger significantly expands DraftKings’ reach in online casino and sports betting markets globally.

- June 2024: Riot Games expanded its partnership with Cisco, enhancing connectivity and security for League of Legends esports events worldwide. Cisco continues as Riot’s official enterprise networking and security partner, boosting esports event reliability.

Global Online Gambling Market Report Scope

Online gambling is typically betting on casino or sports-type games over the internet. The online gambling market is segmented by game type, end user, and geography. Based on game type, the online gaming market share is segmented into sports betting, casino, lottery, and bingo. Sports betting is further segmented into football, horse racing, tennis, and other sports. Casinos are further segmented into live casinos, baccarat, blackjack, poker, slots, and other casino games. Based on end users, the market is segmented into desktop and mobile. The market is segmented based on geography into North America, Europe, Asia-Pacific, and the Rest of the World. The online gambling market size has been done in value terms in USD for all the above-mentioned segments.

By Game Type

| Sports Betting | Football |

| Horse Racing | |

| Tennis | |

| Other Sports | |

| Casino | Live Casino |

| Baccarat | |

| Blackjack | |

| Poker | |

| Slots | |

| Other Casino Games | |

| Lottery | |

| Bingo |

By Platform

| Desktop |

| Mobile and Tablets |

By Age Group

| 18–24 Years |

| 25–34 Years |

| 35–44 Years |

| 45–54 Years |

| 55+ Years |

By Betting Type

| Pre-Match/Fixed-Odds |

| Live/In-Play |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | Oceanic Countries |

| Rest of Asia-Pacific | |

| Rest Of The World | South America |

| Middle East and Africa |

| By Game Type | Sports Betting | Football |

| Horse Racing | ||

| Tennis | ||

| Other Sports | ||

| Casino | Live Casino | |

| Baccarat | ||

| Blackjack | ||

| Poker | ||

| Slots | ||

| Other Casino Games | ||

| Lottery | ||

| Bingo | ||

| By Platform | Desktop | |

| Mobile and Tablets | ||

| By Age Group | 18–24 Years | |

| 25–34 Years | ||

| 35–44 Years | ||

| 45–54 Years | ||

| 55+ Years | ||

| By Betting Type | Pre-Match/Fixed-Odds | |

| Live/In-Play | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | Oceanic Countries | |

| Rest of Asia-Pacific | ||

| Rest Of The World | South America | |

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the online gambling market in 2026?

The online gambling market size is USD 101.45 billion in 2026.

What CAGR is projected for global online wagering through 2031?

The compound annual growth rate is forecast at 10.72% between 2026 and 2031.

Which segment holds the largest revenue share?

Sports betting leads with 52.05% of 2025 revenue.

Which platform is growing fastest?

Mobile and tablet stakes are expanding at a 13.65% CAGR.

Which region posts the highest growth?

North America leads regional growth at a 15.40% CAGR through 2031.

How are regulators impacting industry expansion?

Standardized tax bands, mandatory safer-gambling tools, and clearer licensing rules are encouraging legal market entry while protecting consumers.

Page last updated on: