Cigarette Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 770.89 Billion |

| Market Size (2031) | USD 821.21 Billion |

| Growth Rate (2026 - 2031) | 2.25% CAGR |

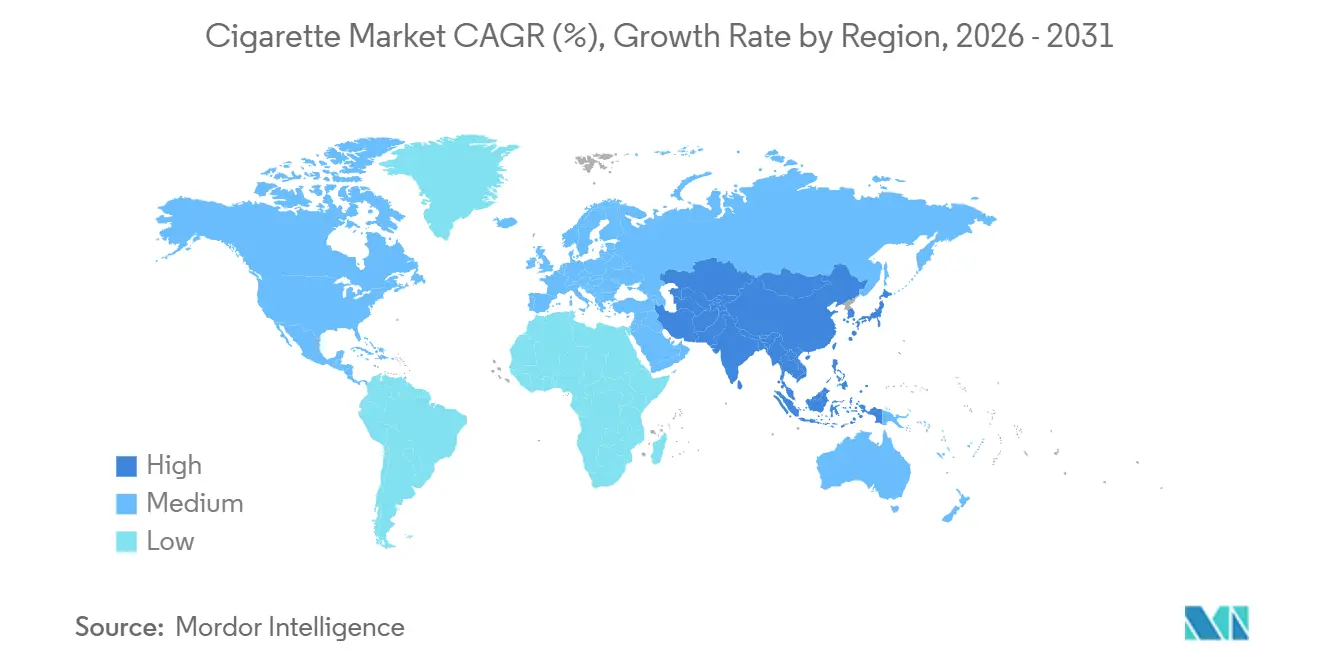

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

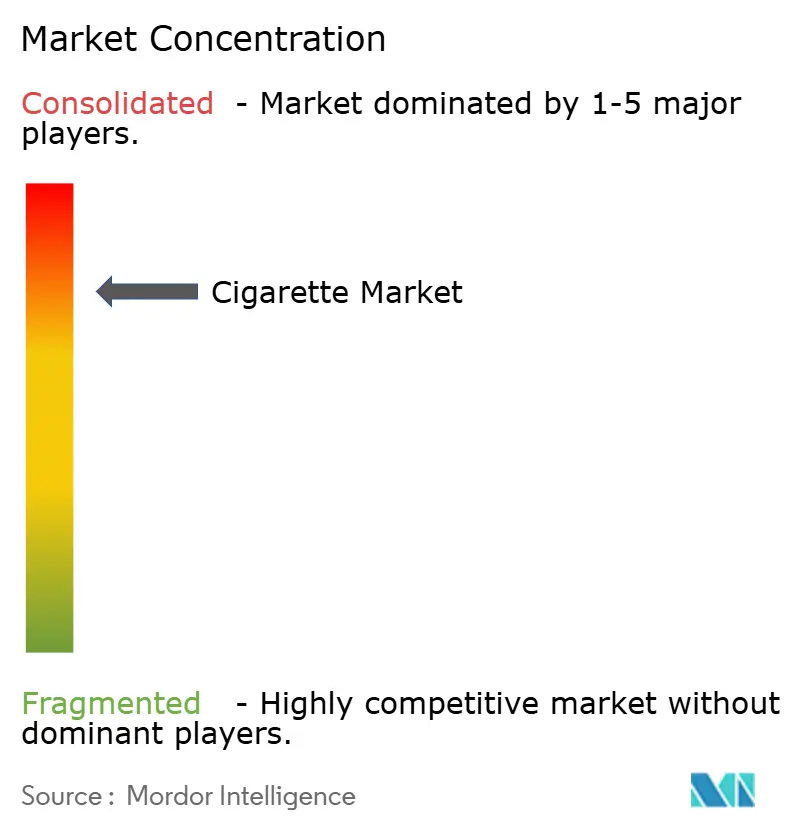

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cigarette Market Analysis by Mordor Intelligence

The cigarette market size is valued at USD 770.89 billion in 2026, growing from the 2025 value of USD 762.34 billion, and is forecast to climb to USD 821.21 billion by 2031, advancing at a 2.25% CAGR during the forecast period. Demand resiliency stems from entrenched nicotine dependence and a solid consumer base in emerging economies, even as regulation tightens in high-income nations. Asia-Pacific remains the growth engine, buoyed by rising disposable incomes, while high excise taxes and plain-packaging mandates pressure margins in Europe, North America, and Australia. Premiumization is accelerating value growth in China, Japan, and Western Europe, offsetting declining volumes in mature markets. Meanwhile, automation, track-and-trace technologies, and supply-chain integration are helping incumbents contain costs and maintain competitive advantage.

Key Report Takeaways

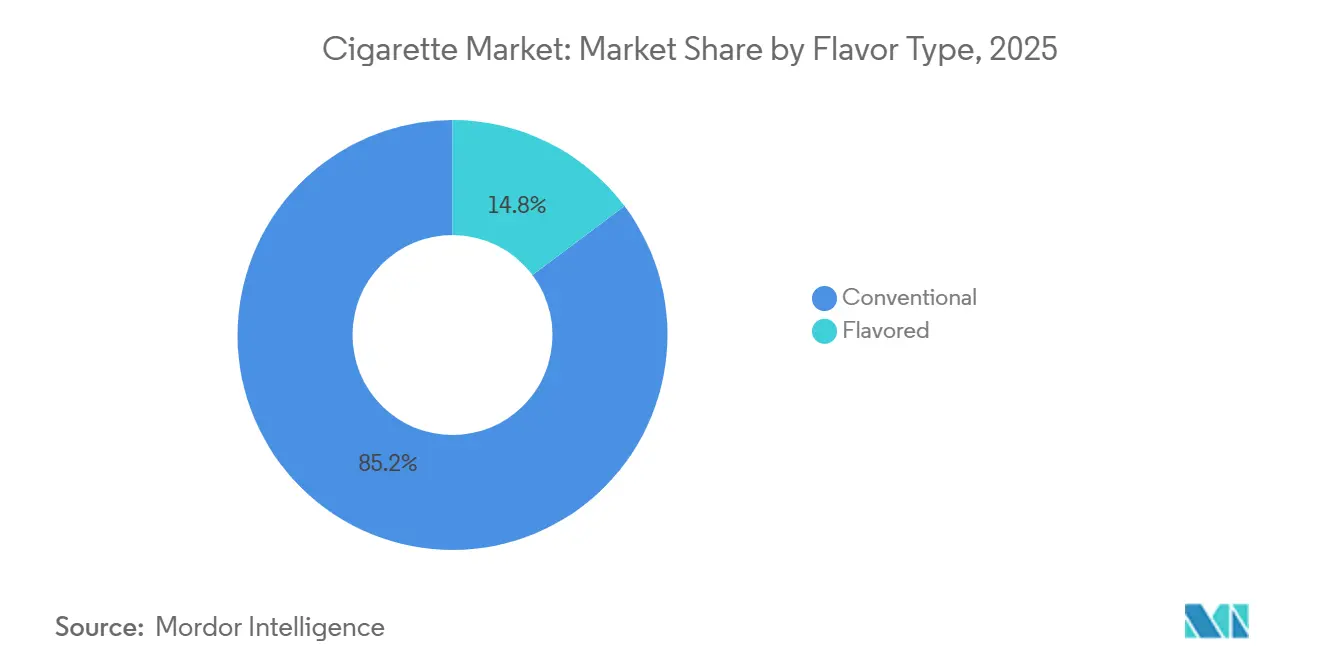

- By flavor type, conventional unflavored cigarettes led with 85.24% of 2025 volume, whereas flavored variants are forecast to expand at a 3.45% CAGR through 2031.

- By format, king-size commanded 52.38% of 2025 volume, while super-slim formats are advancing at 3.32% CAGR.

- By category, mass-market lines held 90.28% of 2025 revenue; the premium segment is set to grow at 4.02% CAGR.

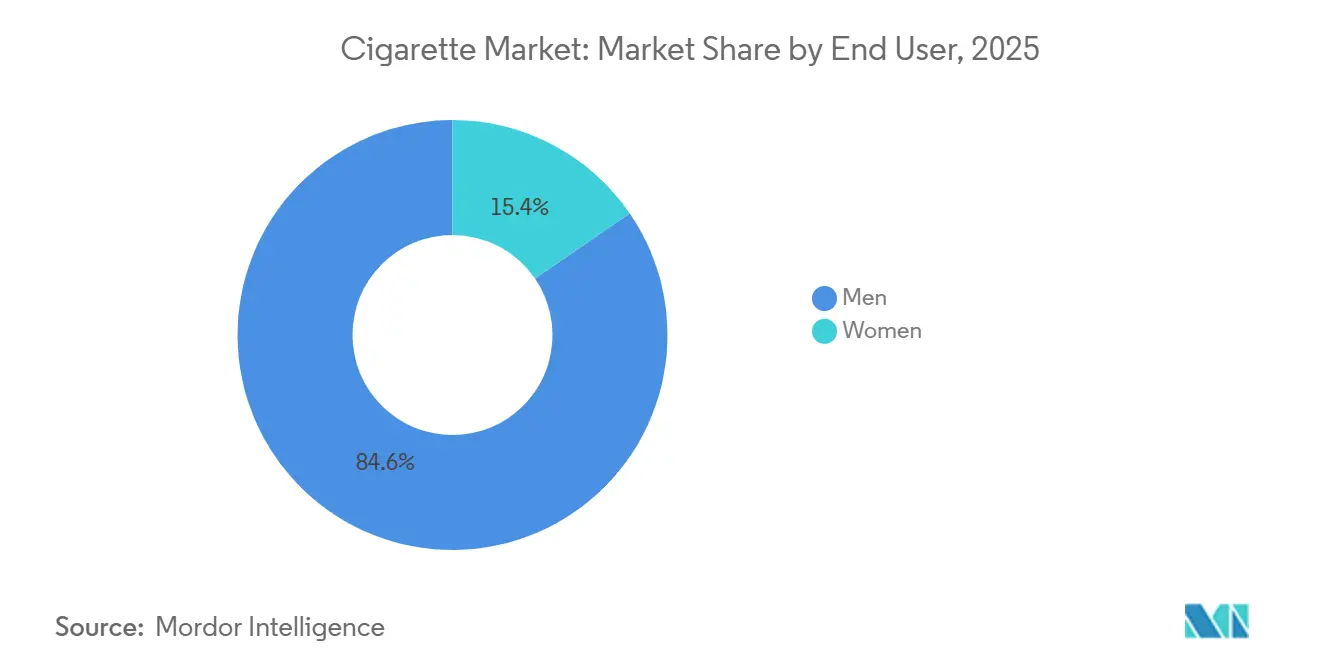

- By end user, men accounted for 84.56% of 2025 consumption; women constitute the fastest-growing cohort at 3.38% CAGR.

- By distribution channel, convenience and grocery stores dominated with 45.57% share in 2025, yet online retail is rising at 3.22% CAGR.

- By geography, Asia-Pacific captured 48.26% of 2025 cigarettes market share and is expanding at 3.47% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cigarette Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nicotine Addiction Ensuring Resilient Consumer Loyalty | +0.6% | Global, with highest retention in Asia-Pacific and Eastern Europe | Long term (≥ 4 years) |

| Rising Premiumization Trend | +0.4% | North America, Western Europe, China, Japan | Medium term (2-4 years) |

| Rising Disposable Incomes in Emerging Markets | +0.5% | Asia-Pacific (India, Indonesia, Vietnam), Middle East and Africa, South America | Long term (≥ 4 years) |

| Technological Advancements in Production | +0.2% | Global, concentrated in automated facilities in China, United States, Germany | Medium term (2-4 years) |

| Effective Marketing and Peer Influence Sustain Demand Among Millennials | +0.3% | Southeast Asia, Latin America, Middle East | Short term (≤ 2 years) |

| Introduction of Herbal and Nicotine-Free Flavors | +0.2% | North America, Europe, urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nicotine Addiction Ensuring Resilient Consumer Loyalty

Longitudinal studies indicate that 70% to 80% of daily smokers sustain their consumption levels despite a 20% to 30% increase in excise taxes. This persistence, driven by nicotine's addictive properties, is particularly prominent in the Asia-Pacific region. In this area, cultural acceptance of smoking and limited cessation support contribute to relapse rates exceeding 85% within a year of quit attempts. In the European Union, the Tobacco Products Directive requires health warnings to cover 65% of cigarette pack surfaces[1]Source: European Commission, “Tobacco Products Directive – Overview,” ec.europa.eu. However, between 2020 and 2025, EU cigarette sales declined by only 1.8% annually, demonstrating the minimal impact of visual deterrents on habitual smokers. Similarly, the China National Tobacco Corporation's 2025 report revealed that, despite a 15% increase in retail prices since 2022, male smokers aged 35 to 54 consistently consumed 14.2 cigarettes daily. This indicates that price elasticity is nearly zero for core users. Such steadfast loyalty ensures stable cash flows for tobacco companies, enabling them to invest in reduced-risk products while maintaining traditional portfolios as key profit generators.

Rising Premiumization Trend

Affluent consumers in China, Japan, and Western Europe are increasingly choosing premium cigarette brands priced above USD 8 per pack, associating them with status and perceived quality. Consequently, the premium cigarette segment is growing at an annual rate of 4.02%, nearly twice the overall market rate. In 2025, Philip Morris International's Marlboro Gold and Parliament lines recorded a 6.3% volume growth in the Asia-Pacific. This growth was primarily driven by urban professionals in cities such as Shanghai, Tokyo, and Seoul, who perceive these premium formats as offering reduced tar delivery and superior flavor profiles. Similarly, British American Tobacco's Dunhill and Rothmans brands expanded their share of Europe's premium segment from 18% in 2023 to 22% in 2025. This increase was achieved by emphasizing their heritage and introducing limited-edition packaging, which commands a 40% to 50% price premium over mass-market alternatives. Excise tax structures further support this trend by applying flat per-unit duties instead of ad-valorem rates, making premium cigarettes relatively more affordable on a percentage basis. In 2025, Japan Tobacco's Mevius brand, priced at JPY 600 (USD 4.20) per pack, experienced a 4.1% rise in domestic volume. This growth occurred as smokers consolidated their purchases into fewer, higher-quality sticks, avoiding discount alternatives.

Rising Disposable Incomes in Emerging Markets

In India, Indonesia, Vietnam, and sub-Saharan Africa, increasing disposable incomes are adding 15 to 20 million new smokers to the market annually, offsetting declines in OECD nations. The World Bank reported that India's median household income grew by 6.8% in real terms in 2024. This growth enabled lower-middle-class consumers to shift from unbranded beedis or loose tobacco to branded cigarettes, priced at INR 350 to 400 (USD 4.20 to 4.80) per pack[2]Source: World Bank, “GDP Per Capita Data,” data.worldbank.org. ITC Limited, India's largest cigarette manufacturer, stated in its 2025 annual report that its Gold Flake Kings brand gained 2.3 million new users in tier-2 and tier-3 cities, driven by increased formal employment and improved credit access. In 2025, Indonesia's GDP per capita reached USD 5,240, a level historically associated with rising cigarette consumption. Supporting this trend, Gudang Garam and Djarum reported a combined volume growth of 3.9%, with kretek clove cigarettes expanding into rural Java and Sumatra. In Nigeria, the urban population surpassed 120 million in 2025, creating a significant young adult demographic with discretionary income. However, regulatory uncertainties and the prevalence of counterfeit products continue to hinder the growth of the formal market.

Technological Advancements in Production

Leading cigarette manufacturers are utilizing machine-vision systems and robotic handling to achieve sub-millimeter accuracy in rod diameter and filter attachment. This approach reduces waste and ensures compliance with ISO 3402 standards. Cognex Corporation's vision systems, widely implemented in major factories across China, Germany, and the U.S., enable real-time defect detection at line speeds exceeding 20,000 cigarettes per minute. This innovation has reduced rejection rates from 1.2% to 0.4%, resulting in annual savings of approximately USD 2 million to 3 million per facility. In 2024, Japan Tobacco International's Bucharest facility adopted automated guided vehicles for material handling, achieving a 12% reduction in labor costs and a 9% increase in output per shift. These efficiency improvements are crucial as plain packaging mandates erode brand-driven pricing power, pushing manufacturers to focus on cost optimization. Additionally, the European Union's Tobacco Excise Directive, proposed in July 2025, plans to extend track-and-trace requirements to all member states by 2027. This development highlights the need for serialization and data-matrix printing capabilities, which can only be cost-effectively achieved through automated lines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulations Like Nicotine Caps and Plain Packaging | -0.5% | Global, most severe in United Kingdom, Australia, Canada, European Union, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Health Awareness of Tobacco Risks | -0.3% | North America, Europe, Australia, urban Asia-Pacific | Long term (≥ 4 years) |

| Shift to Smokeless Alternatives Like E-Cigarettes | -0.4% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Aggressive Public Health Campaigns | -0.2% | Australia, United Kingdom, Scandinavia, with emerging impact in Brazil, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations Like Nicotine Caps and Plain Packaging

Plain packaging mandates and nicotine content ceilings are diminishing brand equity, which has traditionally supported premium pricing. In April 2024, Australia finalized its Tobacco Plain Packaging Act, requiring all tobacco packs to feature a standardized olive-brown color and uniform typography. Only small brand names are now allowed to differentiate products, as mandated by the Australian Government. Canada's regulations, fully implemented in 2025, go further by requiring health warnings to be displayed on individual cigarettes in addition to the packaging. If the FDA's proposed nicotine cap of 0.7 milligrams per gram is approved, manufacturers will need to reformulate their blends, potentially reducing the sensory satisfaction that underpins brand loyalty. Philip Morris International's 2025 investor presentation noted that plain packaging in the UK and Australia resulted in a 15% to 20% decline in premium-brand volume within 18 months, as consumers shifted to cheaper alternatives when visual branding elements were removed. These regulatory changes favor larger players with cost-efficient production and extensive distribution networks, while smaller brands that rely on packaging aesthetics face significant challenges.

Health awareness of tobacco risks

Government-funded anti-smoking initiatives in high-income countries are showing significant results. Annual smoking prevalence has declined by 1.5% to 2.5%, driven by graphic health warnings and cessation support programs. Australia's National Tobacco Campaign, with an investment of AUD 50 million (USD 33 million) for 2024-2025, combined television advertisements with subsidized nicotine replacement therapy, resulting in a 2.1 percentage-point drop in adult smoking rates to 9.8% in 2025, according to the Australian Government Department of Health[3]Source: Australian Government, “Tobacco Plain Packaging Act,” legislation.gov.au. Similarly, the UK's National Health Service reported success with its Stoptober initiative, which encourages smokers to quit for 28 days each October. In 2025, the program engaged 1.2 million participants, achieving a 6-month abstinence rate of 18%, up from 14% in 2022. These campaigns have been particularly effective among younger age groups. In the EU, smoking initiation rates among 15-to-18-year-olds fell to 4.2% in 2025, compared to 7.8% in 2020. However, in low- and middle-income countries, the impact of such campaigns remains limited due to constrained public health budgets and the influence of tobacco industry lobbying.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor Type: Conventional Dominates, Flavored Accelerates

In 2025, Conventional products accounted for 85.24% of the cigarette market share, maintaining their dominant position. Flavored variants, however, are projected to grow at a CAGR of 3.45%, primarily due to the adoption of capsule technology, which effectively bypasses direct menthol bans. Following the EU's 2020 menthol prohibition, capsule cigarettes, led by popular brands such as Marlboro Ice Blast and Lucky Strike Click, managed to recover 60% of the flavored segment's lost volume. Meanwhile, regulators in the Asia-Pacific region are deliberating broader flavor bans, with Hong Kong already implementing a total ban set to take effect in 2027. In anticipation of these regulatory changes, manufacturers are diversifying their portfolios by investing in nicotine pouches and heated-tobacco sticks, which deliver flavor without violating restrictions on combustible products.

The growth trajectory of flavored products remains uneven across regions. Europe and North America are driving innovation in this segment, introducing new and diverse flavor options to attract consumers. In contrast, markets such as China and India continue to favor the traditional taste of straight tobacco. In the United States, regulatory pressures are intensifying, with potential restrictions on menthol and capsule products posing a significant threat to the flavored segment. These measures could result in the loss of up to 20% of flavored sales. Despite these challenges, the diversification of flavors continues to resonate with younger adult smokers, ensuring the segment's sustained outperformance and reinforcing its appeal in an evolving market landscape.

By Format: King Cigarettes Reign Supreme, Slim Cigarettes Gain Momentum

In 2025, king-size cigarettes accounted for 52.38% of the market volume. However, super-slim cigarette lines are witnessing significant growth, expanding at a 3.32% CAGR. This growth reflects a deliberate strategy to target women and younger adults, who are increasingly drawn to these formats. British American Tobacco’s Vogue and Philip Morris’s Virginia Slims recorded a notable 5.7% increase in volume across Europe and North America in 2025. Additionally, Japan Tobacco’s Pianissimo achieved a 9.2% share in the domestic market, further solidifying its position. Slim cigarette formats command a price premium of 20%–30%, attributed to their specialized production processes.

Despite their popularity, public health organizations emphasize that slimmer diameters do not mitigate toxicant exposure. In line with this, the WHO has recommended banning descriptors that imply a lower health risk to consumers. Regular cigarette formats continue to dominate in price-sensitive markets such as India and Indonesia, where affordability plays a critical role in consumer preferences. On the other hand, super-slim cigarette sticks remain a niche product outside of South Korea and Japan but are instrumental in reinforcing premium brand positioning. Innovations in filter design and paper porosity have been pivotal in maintaining optimal draw resistance and flavor delivery, even with reduced tobacco content, ensuring that consumer satisfaction is not compromised.

By Category: Premium Growth Accelerates Despite Economic Pressures

In 2025, mass-market brands dominated the revenue share, contributing 90.28% of the total. However, premium sales are expected to grow steadily, with a CAGR projected at 4.02%. In China, premium brands such as Chunghwa and Panda are priced between CNY 100–150 (equivalent to USD 14–21) per pack, reflecting their high-end positioning. Meanwhile, Marlboro Gold, a leading premium brand in Western Europe, commands a price exceeding USD 10 per pack and is projected to achieve a significant 6.3% increase in volume sales in 2025. The implementation of flat excise duties has further reduced the price gap between premium and mass-market segments. Consequently, premium product lines generate higher profitability, which helps offset the costs associated with mass-market channels.

The middle-tier segment is gradually shrinking as consumers either upgrade to premium offerings or quit smoking altogether. In India, premium brand penetration remains below 5%, but evolving demographics and increasing urbanization indicate a potential rise in demand for premium products. Additionally, excise reforms across Europe, which aim to raise minimum tax rates, are expected to exert pressure on low-margin segments. This regulatory shift is likely to accelerate the market's inclination toward premium offerings, reinforcing their growing prominence.

By End User: Women Segment Drives Demographic Transformation

In 2025, men accounted for 84.56% of total consumption; however, women are emerging as the fastest-growing consumer group, with a CAGR of 3.38%. By 2025, the prevalence of female consumers reached 6.8% in Indonesia and doubled to 3.2% in Vietnam. To appeal to this growing demographic, brand owners are adopting strategies such as introducing slim product formats, utilizing pastel-colored packaging, and incorporating lifestyle-oriented messaging—where regulations permit. In South Korea, female consumer rates increased to 7.1%, while male rates declined, effectively reducing the gender disparity in consumption patterns.

Marketing strategies increasingly target female consumers through product design innovations, including slim formats, lighter tobacco blends, and sophisticated packaging that appeals to feminine aesthetics and lifestyle aspirations. However, health awareness campaigns specifically targeting women's health risks, including pregnancy-related concerns and cosmetic impacts, create countervailing pressures that may constrain long-term growth in this segment. The women's segment's growth trajectory depends on balancing social acceptance trends with intensifying health education efforts that highlight gender-specific smoking risks and consequences.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

In 2025, convenience and grocery outlets maintained a significant 45.57% market share, driven by their extensive availability and the appeal of impulse purchasing. These outlets continue to dominate due to their accessibility and ability to cater to immediate consumer needs. Meanwhile, online retail, though still a smaller segment, is experiencing a CAGR of 3.22%, fueled by the exploitation of weak age verification protocols in several markets. Despite regulatory restrictions, online sales in urban China accounted for nearly 10% of total sales in 2025, showcasing the resilience and adaptability of e-commerce in the region. In the European Union, cross-border e-commerce is effectively bypassing excise parity regulations, creating pricing disparities. Conversely, Australia took a stringent approach by completely banning internet sales in 2024, reflecting a stark contrast in regulatory strategies.

Digital transformation and changing consumer behaviors, influenced by the pandemic, drive this growth. E-commerce simplifies online cigarette purchases, offering convenience, variety, and competitive pricing. Increased smartphone use, better internet connectivity, and improved logistics further boost online retail in the cigarette sector. Specialty stores cater to niche markets with premium products and personalized services, focusing on customer experience and exclusivity to maintain loyalty despite competition.

Geography Analysis

Asia-Pacific, which accounted for 48.26% of the 2025 market share, is expected to lead all regions with an annual growth rate of 3.47% through 2031. This growth is attributed to a large population, increasing incomes, and relatively relaxed regulatory environments. China, contributing 40% to 45% of global cigarette consumption, sees its China National Tobacco Corporation producing over 2.3 trillion sticks annually. However, per-capita consumption has stabilized at 14.2 cigarettes daily for male smokers as urbanization and growing health awareness limit growth. In India, the cigarette market expanded by 4.1% in 2025, driven by growth in formal-sector employment and a shift from beedis and loose tobacco. Brands like Gudang Garam and Djarum leveraged cultural preferences for spiced tobacco and faced minimal regulatory challenges. Japan's market, while contracting with a 2.1% volume decline in 2025, maintained value growth through premiumization. Brands such as Japan Tobacco's Mevius and Seven Stars commanded prices exceeding JPY 600 (USD 4.20) per pack.

Europe, which held 22% to 24% of the 2025 market share, is experiencing annual volume declines of 1.2% to 1.8%. Factors such as plain packaging, high excise taxes, and widespread smoking bans are reducing consumption. The UK's Tobacco and Vapes Bill, passed in November 2024, aims to phase out the legal market over 15 to 20 years by banning sales to individuals born after January 1, 2009. In Germany, Europe's largest market, cigarette sales fell by 2.3% in 2025. However, premium brands like Marlboro and Dunhill gained market share as consumers shifted towards fewer, higher-quality sticks. The European Commission's proposed excise duty increase, which will raise minimum rates to EUR 3.60 per pack by 2027, is expected to further suppress demand. This impact will be particularly pronounced in Eastern European countries like Poland and Romania, where prices currently remain 50% to 60% lower than in Western Europe.

North America, which accounted for 15% to 17% of 2025 sales, is witnessing volume declines exceeding 2.5% annually in both the U.S. and Canada as smoking prevalence falls below 12% of adults. The FDA's January 2025 proposal to cap nicotine levels at 0.7 milligrams per gram represents a historic regulatory intervention. It aims to reduce the appeal of cigarettes and accelerate the transition to e-cigarettes or cessation. Mexico, however, shows resilience with a 1.2% volume increase in 2025. This growth is supported by a younger demographic and weaker enforcement of smoke-free regulations. South America, led by Brazil, Argentina, and Colombia, contributed 6% to 8% of 2025 sales and is growing at an annual rate of 2.8%. This growth is driven by rising incomes and stable smoking prevalence, which remains between 18% and 22%. While Brazil's National Health Surveillance Agency tightened advertising restrictions in 2024, enforcement remains inconsistent outside major cities. The Middle East and Africa, collectively accounting for 8% to 10% of 2025 sales, are growing at an annual rate of 3.1%. Egypt, Turkey, and South Africa are leading this volume growth, although political instability and currency fluctuations pose challenges. In Nigeria, urban cigarette consumption is growing at a rate of 5% to 6% annually. However, counterfeit products, which account for an estimated 30% to 40% of the market, are hindering formal market expansion.

Competitive Landscape

The cigarette market is highly consolidated, dominated by multinational tobacco companies that balance defending traditional cigarette revenues with investing in next-generation products. Companies like Philip Morris International and British American Tobacco are heavily investing in reduced-risk products such as heated tobacco and e-cigarettes to address shifting consumer preferences. This trend is particularly evident in developed markets, where health concerns and regulatory pressures are driving demand for alternatives to traditional cigarettes.

Competition in the cigarette market involves global conglomerates and regional specialists. While multinationals benefit from extensive distribution networks and strong brand portfolios, regional players leverage their understanding of local consumer preferences and distributor relationships. For example, Gudang Garam and Djarum dominate the Indonesian market with clove-based cigarettes, while local manufacturers in Africa cater to regional demands and price sensitivities. These dynamics make regional firms attractive acquisition targets for global companies seeking to expand their reach and overcome market entry barriers.

The cigarette industry is witnessing a surge in mergers and acquisitions as companies pursue economies of scale and geographical expansion. Global giants are targeting local manufacturers in emerging markets for quick market entry and established distribution channels. For instance, Japan Tobacco's acquisition of Akij Group's tobacco business in Bangladesh strengthened its presence in a high-growth market, while British American Tobacco's acquisition of Reynolds American consolidated its position in the U.S. Additionally, strategic alliances like the collaboration between Altria and Philip Morris International to market IQOS in the U.S. highlight how partnerships enhance competitive positioning in key markets.

Cigarette Industry Leaders

British American Tobacco PLC

Altria Group Inc.

Japan Tobacco International

ITC Limited

Philip Morris International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BAT Rothmans, the South Korean arm of British American Tobacco, announced the global launch of Dunhill’s first sub-brand, Global Editions, starting with South Korea as the inaugural market.

- November 2024: Imperial Brands has introduced Paramount, a new cigarette brand tailored for adult smokers seeking strong value without compromising on quality. Made with premium, full-flavour Virginia sun-ripened tobacco, Paramount caters to the preferences of the UK market and is available through UK wholesale and independent retail channels.

- September 2024: TABATERRA has announced the launch of Premier, a premium cigarette brand developed for discerning consumers who prioritize quality and sophistication. Featuring four distinct SKUs, Premier sets a new benchmark in the category, combining meticulously crafted tobacco with a sleek, modern design that underscores its premium positioning.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cigarette market as the value generated by factory-made combustible tobacco sticks that are duty-paid and legally distributed worldwide. Pricing is tracked at the weighted average retail level, then restated in constant 2025 USD for comparability.

Scope exclusion: All forms of illicit trade, roll-your-own products, cigars, heated tobacco, e-cigarettes, filters, and packaging materials fall outside this sizing.

Segmentation Overview

- Flavor Type

- Flavored

- Unflavored

- Format

- Slim

- Super Slim

- King Size

- Regular

- Category

- Mass

- Premium

- End User

- Men

- Women

- Distribution Channels

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with distributors, tax officers, packaging converters, and cessation program leads across Asia-Pacific, Europe, the Americas, and Africa enabled us to verify stick volume shifts, typical net-to-retail margins, and likely policy moves that are not yet published.

Desk Research

We started with headline datasets from WHO tobacco statistics, UN Comtrade codes 2402.xx, national excise collections, and IMF retail price indices. Supplementary evidence came from trade associations such as the US Tobacco Merchants Association, Eurostat retail scanner panels, and health ministry prevalence surveys. Our team next consulted company 10-Ks, investor decks, and customs filings, and then tapped D&B Hoovers for brand level splits. Patent analytics from Questel indicated premiumization momentum, while Dow Jones Factiva newsfeeds flagged sudden tax or regulatory shocks. These examples illustrate, not exhaust, the wider secondary stack employed.

Market-Sizing & Forecasting

A top-down build reconstructed 2025 value by multiplying duty-paid stick volumes with country specific weighted prices, followed by selective bottom-up checks from supplier roll-ups and sampled channel audits to align totals. Key drivers, adult smoking prevalence, excise burden, disposable income, premium share, and price elasticity, feed a multivariate regression with an ARIMA overlay that projects 2026-2030, while scenario analysis captures abrupt tax hikes or flavor bans.

Data Validation & Update Cycle

Outputs undergo peer review, automated variance scans, and senior analyst sign-off. Mordor analysts refresh every twelve months and trigger mid-cycle updates whenever material fiscal or regulatory events reshape core variables.

Why Our Cigarette Market Baseline Earns Trust

Published estimates rarely agree because some firms blend heated products, others apply retail mark-ups, and many freeze exchange rates that move every quarter.

Key gap drivers observed include scope creep into next-generation nicotine, inclusion of illicit sticks, or use of unverified pack prices, whereas Mordor Intelligence fixes its lens on duty-paid factory sticks, quarterly currency resets, and documented tax pass-throughs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 769.52 bn (2025) | Mordor Intelligence | - |

| USD 840.70 bn (2024) | Regional Consultancy A | Includes illicit and roll-your-own; uses shelf prices without tax breakout |

| USD 815.74 bn (2024) | Global Consultancy B | Bundles heated tobacco; keeps 2020 FX rates constant |

The comparison shows that modest tweaks in scope or pricing can widen values by tens of billions. By anchoring inputs in transparent public data, validated interviews, and an annual refresh cadence, we believe our baseline offers the most dependable starting point for strategic decision-making.

Key Questions Answered in the Report

How large is the global cigarettes market today?

The global cigarettes market size is USD 770.89 billion in 2026 and is forecast to reach USD 821.21 billion by 2031 at a 2.25% CAGR.

Which region contributes the most to cigarette sales?

Asia-Pacific leads with 48.26% of 2025 global volume and is projected to expand at a 3.47% CAGR through 2031.

What segment is growing fastest within cigarette formats?

Super-slim formats are advancing at a 3.32% CAGR, outpacing king-size and regular sticks.

How are premium cigarettes performing compared with mass-market lines?

Premium products, though under 10% of sales, are projected to grow at 4.02% CAGR, nearly twice the overall market.

Page last updated on: