Online Lottery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

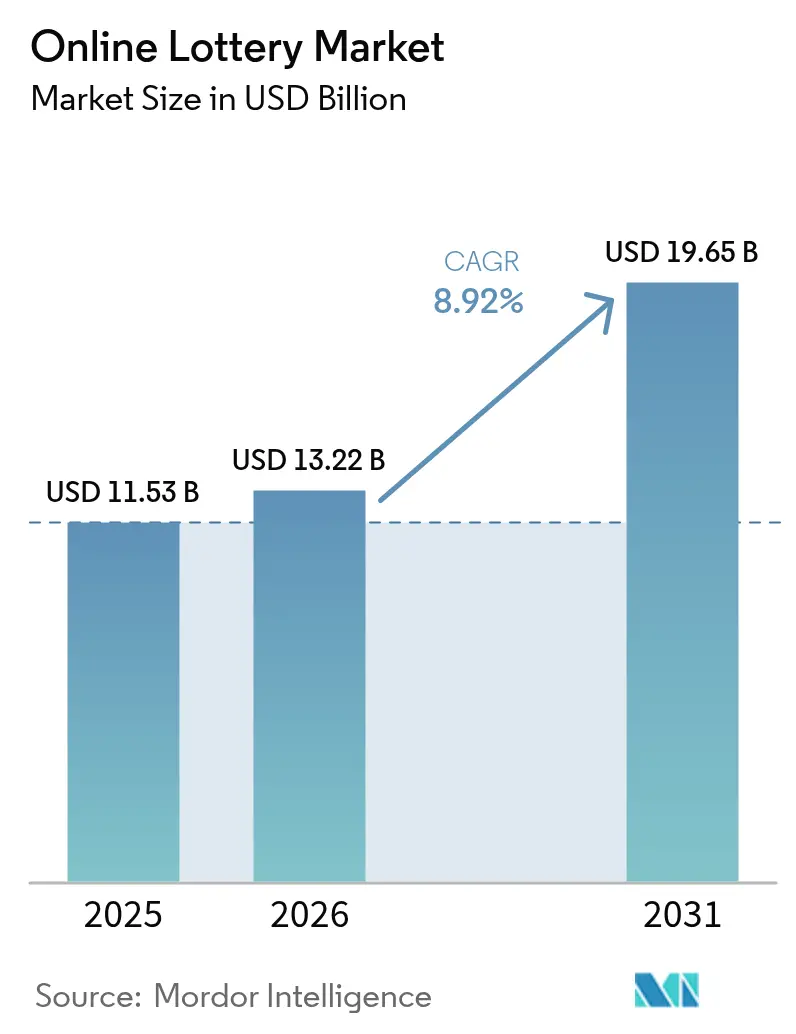

| Market Size (2026) | USD 13.22 Billion |

| Market Size (2031) | USD 19.65 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Lottery Market Analysis by Mordor Intelligence

The online lottery market size is projected to expand from USD 11.53 billion in 2025 and USD 13.22 billion in 2026 to USD 19.65 billion by 2031, registering a CAGR of 8.92% between 2026 and 2031. Mobile access, friction-free digital wallets, and permissive legislation in North America are amplifying player acquisition, while cross-border jackpot pooling sustains headline prizes that exceed USD 1 billion and drive infrequent, value-seeking users back to the platform. Instant-win formats mimic casual mobile gaming and shorten the time from deposit to outcome, a dynamic that resonates with younger cohorts who favor micro-stakes and rapid feedback loops. Mature European frameworks keep revenue steady, yet incremental growth shifts to liberalizing U.S. states and Canadian provinces, where omnichannel cloud stacks streamline licensing compliance and marketing localization. Competitive intensity remains modest because state monopolies, private concessionaires, and cloud-based white-label vendors occupy distinct niches without dominating global share.

Key Report Takeaways

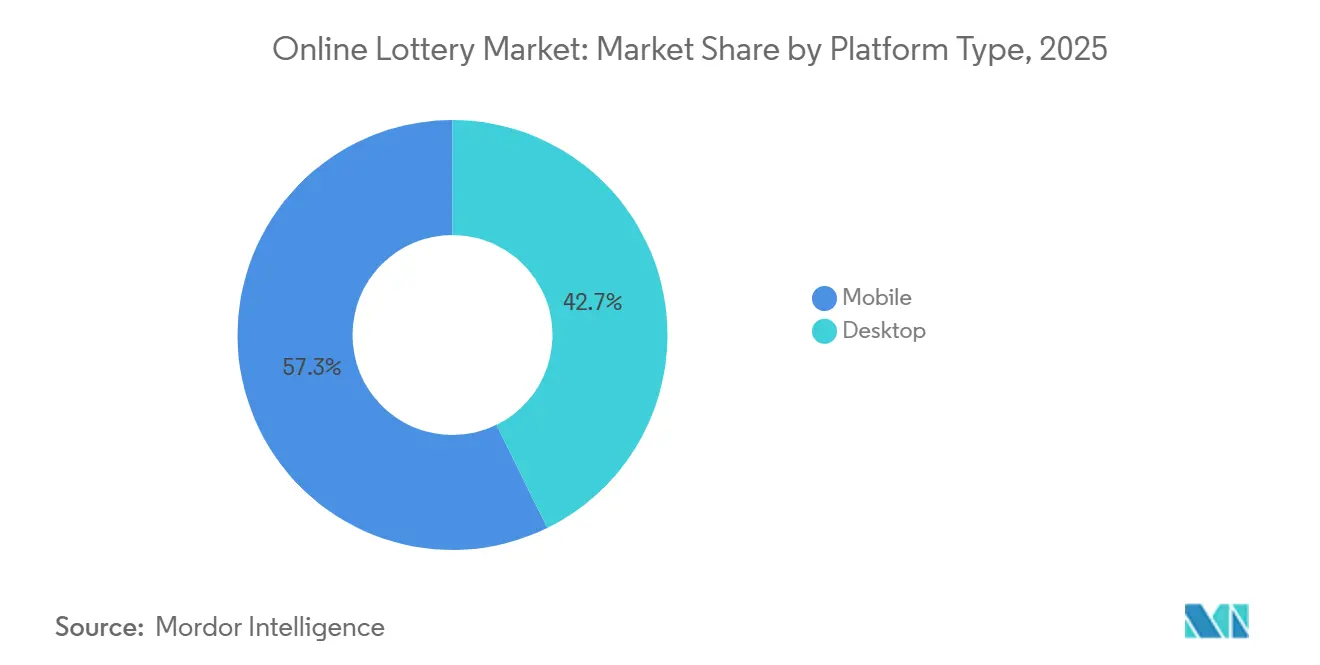

- By platform, mobile platforms captured 57.26% of the online lottery market share in 2025; they are on track for an 10.52% CAGR through 2031.

- By game type, draw-based games accounted for 34.21% of the online lottery market size in 2025, while instant games posted the fastest 10.11% CAGR to 2031.

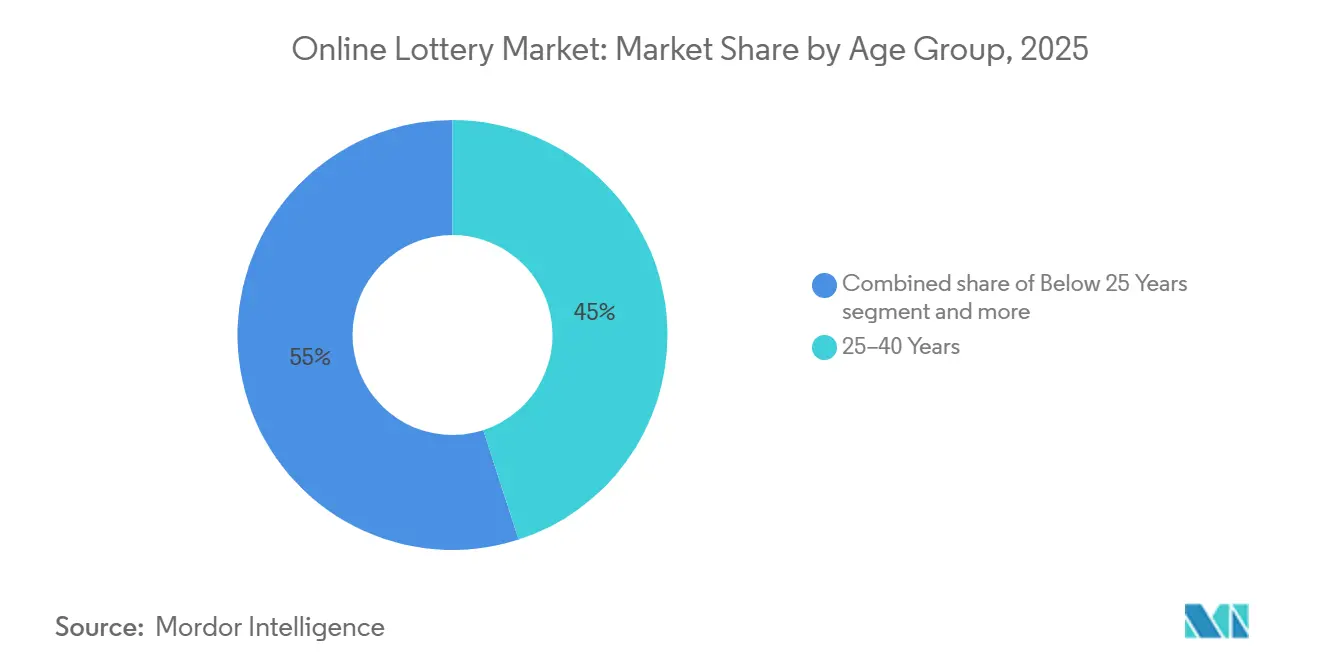

- By age, the 25-40 years bracket held 45.02% share in 2025; the below-25 cohort records the highest 9.78% CAGR.

- By end user, male participants represented 65.12% of 2025 revenue, whereas female engagement expanded at a 9.89% CAGR to 2031.

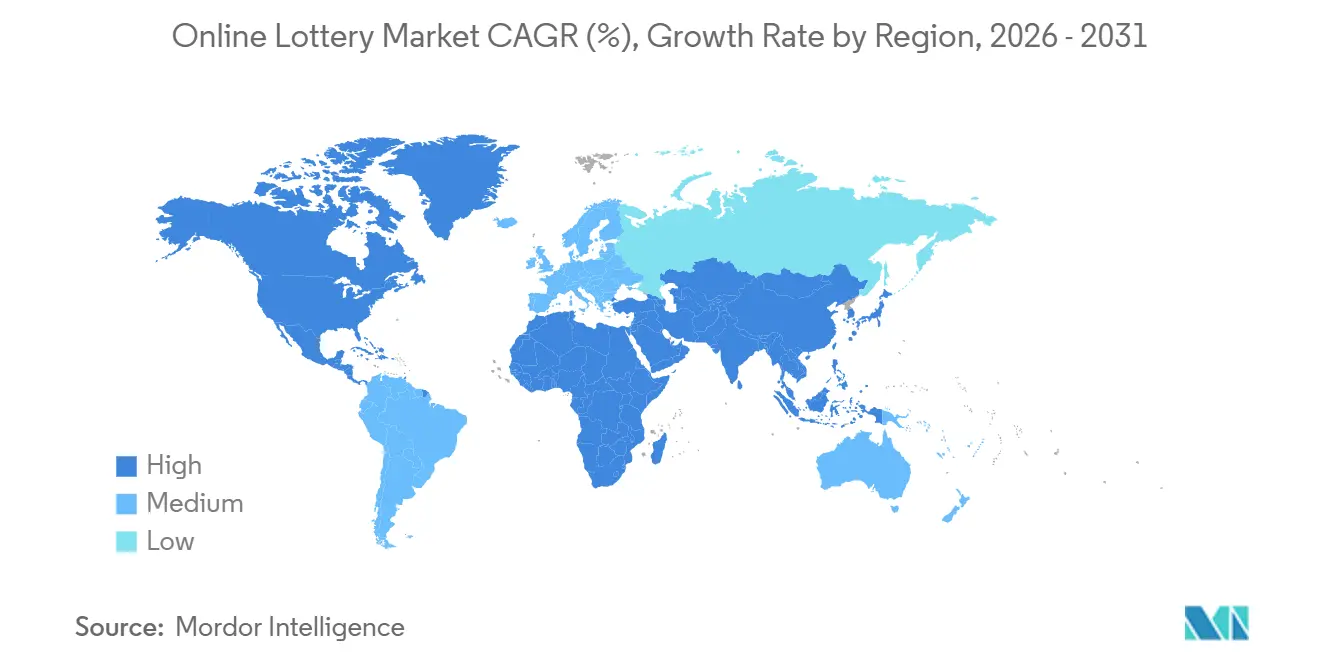

- By Geography, Europe led with a 46.72% share in 2025; North America shows the quickest 10.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Lottery Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Penetration of Digital Wallets and Mobile Payments Integration | +2.1% | Global, with accelerated adoption in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Legalization and Regulatory Liberalization | +2.5% | North America (U.S. state-by-state), Latin America, select Asia-Pacific markets | Short term (≤ 2 years) |

| Increasing Global Internet Penetration | +1.4% | Global, concentrated in emerging markets (India, Indonesia, Nigeria) | Long term (≥ 4 years) |

| Cross-Border Jackpot Pooling Boosting Prize Sizes | +1.8% | Europe (EuroMillions), North America (Powerball, Mega Millions), emerging multi-jurisdiction consortia | Medium term (2-4 years) |

| Micro-Influencer Affiliate Marketing Lowering Acquisition Costs | +1.2% | Global, particularly effective in Europe and North America | Short term (≤ 2 years) |

| Advancement of digital technologies | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Digital Wallets and Mobile Payments Integration

Digital wallets and mobile payment systems now dominate online lottery transactions, reducing checkout abandonment and enabling instant deposits for impulse purchases. In 2025, the International Telecommunication Union reported over 1.6 billion mobile money accounts globally, with transaction values exceeding USD 1.2 trillion, easing access for lottery operators in regions with limited banking infrastructure[1]Source: International Telecommunication Union, “ITU Facts and Figures 2025,” itu.int. IGT's platform integrates Apple Pay, Google Pay, and regional wallets like M-Pesa in Kenya and Paytm in India, allowing quick account funding without card details and speeding up betting. In 2024, Allwyn Entertainment added PayPal and Klarna to its UK National Lottery app, boosting mobile conversion rates by 23% among users aged 18-34. Latin America is leading in embedded finance, with Banco Central do Brasil's PIX system processing 42 billion transactions in 2025, and Caixa Econômica Federal piloting PIX-enabled ticket purchases. In the European Union, the revised Payment Services Directive (PSD2) enforces strong customer authentication while enabling open banking APIs, allowing lottery platforms to initiate payments directly from bank accounts, bypassing card networks and reducing fees.

Legalization and Regulatory Liberalization

Jurisdictional expansion of legal online lottery frameworks serves as a significant near-term growth driver, opening previously restricted markets and transitioning informal lottery activities into regulated systems. In the U.S., Michigan's iLottery platform achieved USD 1 billion in annual sales in 2025, highlighting the compatibility of digital channels with retail operations without eroding brick-and-mortar revenue. The National Council of Legislators from Gaming States (NCLGS) introduced a Model iLottery Act in 2024, providing a legislative framework for states exploring authorization while addressing issues like age verification, geolocation, and responsible gaming[2]Source: National Council of Legislators from Gaming States, “Model iLottery Act 2024,” nclgs.org. In Europe, Germany's Interstate Treaty on Gambling allows online lottery sales under strict advertising and player-protection regulations. In 2025, the Gemeinsame Glücksspielbehörde der Länder (GGL) issued 12 new licenses, intensifying competition among established players such as Lotto24 and ZEAL Network. Similarly, Latin America is experiencing liberalization, with Argentina's Buenos Aires province legalizing online lotteries in 2024 and Brazil's federal government finalizing igaming regulations set to take effect in 2026, creating a combined addressable market of over 250 million adults.

Increasing Global Internet Penetration

Emerging markets are witnessing a surge in internet access, broadening the player base for lotteries. This is especially significant in areas where geographic isolation and limited retail outlets have historically hampered lottery participation. India's internet user count hit 900 million in 2025, buoyed by budget-friendly 4G data plans averaging just USD 2 monthly. Additionally, government initiatives like BharatNet are pivotal, extending fiber connectivity to rural locales, as highlighted by the Telecom Regulatory Authority of India[3]Source: Telecom Regulatory Authority of India, “Internet Penetration Statistics 2025,” trai.gov.in. In a notable shift, state-run lotteries in Kerala and Punjab introduced mobile apps facilitating UPI payments. This move effectively taps into a demand previously met by informal lottery agents. Meanwhile, in Sub-Saharan Africa, mobile broadband subscriptions surged by 18% year-over-year in 2025. Notably, the Uganda National Lotteries Board forged partnerships with telecom giants MTN and Airtel, rolling out USSD-based lottery services. These services are accessible on feature phones, eliminating the need for smartphones, as reported by GSMA's Mobile Economy Sub-Saharan Africa 2025. In Indonesia, while 77% of the populace was online in 2025, the Ministry of Communication and Informatics underscored a critical point: the country's gambling laws still prohibit online lotteries. This highlights a crucial reality: mere connectivity doesn't guarantee participation without the backing of regulatory frameworks.

Cross-Border Jackpot Pooling Boosting Prize Sizes

Multi-jurisdiction lottery consortia pool players across borders, creating jackpots exceeding USD 1 billion and attracting casual participants seeking high returns. In December 2024, EuroMillions, operated by nine European national lotteries, hit a record EUR 240 million (USD 260 million) jackpot, boosting ticket sales by 34% during the rollover period. In the U.S., Powerball and Mega Millions expanded to 48 and 47 jurisdictions, respectively, by 2025. Powerball set a global record in November 2024 with a USD 2.04 billion jackpot, generating USD 120 million in California ticket sales during the final draw week. Emerging markets are adopting this model. The Caribbean Lottery Consortium launched a regional draw in 2025, spanning Jamaica, Trinidad and Tobago, and Barbados, with a starting jackpot of USD 5 million and shared marketing budgets to compete globally. However, cross-border pooling introduces challenges like currency conversion, tax withholding differences, and resolving disputes when winners face conflicting prize-claim regulations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and Legal Challenges | -1.6% | Global, acute in Asia-Pacific (China, India, Indonesia) and Middle East | Long term (≥ 4 years) |

| App-Store Policy Tightening on Real-Money Gambling | -1.3% | Global, particularly impactful in North America and Europe | Short term (≤ 2 years) |

| Cybersecurity Threats and Fraud Risks | -1.1% | Global, with elevated exposure in emerging markets lacking robust KYC infrastructure | Medium term (2-4 years) |

| Negative Public Perception and Stigma | -0.8% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory and Legal Challenges

Fragmented and contradictory regulatory regimes across jurisdictions increase compliance costs, delay market entry, and create legal uncertainties that hinder product innovation. In the U.S., as of 2025, only 11 states allow iLottery sales, while 39 states either prohibit or lack legislation, requiring operators to manage separate technology and marketing efforts for each state. In Asia-Pacific, China's Ministry of Public Security classifies online lotteries as illegal gambling, prosecuting operators and payment processors, effectively closing the market to legitimate providers. In India, the 1867 Public Gambling Act delegates lottery regulation to states, resulting in 13 states running lotteries, with only Sikkim permitting online sales. Additionally, the Goods and Services Tax Council imposes a 28% tax on lottery tickets, the highest for any consumer product. In the European Union, the principle of subsidiarity allows member states to restrict gambling services for public-policy reasons. Countries like Poland and the Netherlands require local licenses, even for operators authorized elsewhere in the EU, further fragmenting the single market.

App-Store Policy Tightening on Real-Money Gambling

Apple and Google have increasingly enforced stricter policies on real-money gambling apps, limiting distribution channels and pushing operators to adopt progressive web apps (PWAs). While PWAs bypass app stores, they compromise on discoverability and push-notification capabilities. Apple's App Store Review Guidelines, revised in June 2024, prohibit lottery apps in regions where online lotteries are not explicitly authorized by law. Additionally, developers must provide proof of licensing for app approval, a process that takes 8 to 12 weeks and often delays product launches. Similarly, Google's Play Developer Policy, updated in September 2024, requires gambling apps to implement age verification at download and restrict in-app advertising to users aged 21 and above. This added friction is estimated to reduce conversion rates by 15%. In response, operators like Lottoland and theLotter have shifted focus to PWAs. These platforms utilize HTML5 and service workers to deliver app-like experiences via mobile browsers, enabling offline functionality and home-screen installation without app-store approval. However, PWAs face limitations, such as the inability to access iOS push notifications and Android's full range of device APIs, which restricts engagement tools essential for driving repeat usage. Moreover, while app-store platforms offer advanced attribution and cohort analysis, PWAs must rely on third-party tools like Google Analytics and Adjust to replicate these analytics capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Mobile Dominance Accelerates

Mobile captured 57.26% of the online lottery market share in 2025 and is expanding at a 10.52% CAGR, while desktop erodes as smartphone penetration deepens. The online lottery market size for mobile transactions is predicted to grow in parallel to rising 5G coverage that supports richer media such as live draws and AR scratch cards. IGT’s biometric-enabled Missouri app lifted monthly active users by 38% within six months, illustrating that single-tap authentication sparks repeat play. Desktop remains relevant for high-value syndicates that require multi-ticket management and larger screens, but cedes share each year. Emerging markets, including India, exhibit virtually mobile-only usage patterns because 89% of users never touch a desktop browser, pushing operators toward Android-first builds.

Mobile provides geofencing, push alerts, and gamification loops that accelerate engagement, yet operators grapple with app-store restrictions, rising acquisition costs, and limited screen real estate for complex bets. Progressive Web Apps bypass store rules but sacrifice native notifications, forcing heavier CRM reliance through SMS and email. As 5G reduces latency and elevates graphics, operators expect to roll out immersive lobbies and livestreamed prize reveals that differentiate mobile from legacy web channels.

By Game Type: Instant Formats Gain Share

Draw-based games retained 34.21% of 2025 revenue, anchored by brands such as Powerball and EuroMillions that deliver ritualized weekly play and viral jackpots. However, instant-win titles record the fastest 10.11% CAGR, shifting the online lottery market size toward on-demand entertainment that mirrors casual mobile gaming. Licensed IP, such as Monopoly, lifts repeat purchase rates and average spending because recognizable themes reduce perceived risk. Instant products demand aggressive content pipelines; NeoGames released 120 unique eInstant titles in 2025 to sustain novelty.

Sports lottery and ancillary games like keno or raffles fill niche appetites and diversify risk but struggle to capture mainstream attention unless jackpots swell well beyond local averages. Draw games still boast lower cost per ticket and bigger average order values, yet limited draw frequency caps engagement versus always-on instant catalogs. Operators now hedge by cross-selling draw subscriptions to instant-first users and vice versa, lowering churn across both verticals.

By Age Group: Youth Adoption Drives Growth

Individuals aged 25-40 provided 45.02% of 2025 participation, blending discretionary income with digital fluency. The online lottery market size attributable to players under 25 is projected to rise fastest at 9.78% CAGR, spurred by mobile-only apps that fuse social chat, micro-stakes, and push-notification reminders. Operators embed subscription auto-buy features that reduce decision fatigue and emulate fintech habits.

The 40-55 band contributes roughly 30% of revenue due to larger baskets and long-term loyalty, though growth flattens as this cohort ages. The 55+ group is digitizing gradually; Allwyn’s large-text mode lifted over-60 registrations by 19%. Younger players demand transparency: 68% of 18-34-year-olds say prize-fund breakdowns and responsible-gaming tools influence brand choice. Operators now publish real-time payout percentages and integrate self-exclusion toggles in dashboards to satisfy that expectation.

By End User: Female Participation Rises

In 2025, male users accounted for 65.12% of the total user base. On the other hand, female participation is witnessing significant growth, expanding at a compound annual growth rate (CAGR) of 9.89%. This increase is primarily driven by the growing appeal of lifestyle-themed events, charitable initiatives, and social playgroups, which resonate more strongly with women. Europe is leading the way in narrowing the gender gap, with the female share rising to 42%. This progress is supported by inclusive marketing campaigns and stringent advertising regulations that actively discourage gender stereotypes.

Women generally place smaller bets but exhibit higher engagement levels, particularly with responsible gaming measures. They are 2.3 times more likely to set deposit limits and 1.8 times more likely to opt for self-exclusion during cooling-off periods. Acquisition strategies also vary significantly, as women respond more positively to social media discoveries and influencer recommendations compared to paid search campaigns. This trend has prompted a reallocation of marketing budgets toward platforms such as Instagram and TikTok to better target female users. Additionally, loyalty programs are undergoing a transformation. Instead of focusing solely on cash-based rewards, these programs now emphasize community badges that recognize consistent, low-stakes participation. This shift aligns more closely with the risk preferences observed among female users.

Geography Analysis

In 2025, Europe contributed 46.72% of global lottery revenues, supported by over 90% internet penetration and the seamless online transition of established national lotteries, which successfully avoided cannibalizing retail sales. The UK's National Lottery reported GBP 1.8 billion (USD 2.3 billion) in digital revenues for the fiscal year ending March 2025. In Germany, a new licensing wave intensified competition between Lotto24 and ZEAL Network. France's FDJ leveraged mobile optimizations and branded instant releases to generate EUR 3.2 billion (USD 3.5 billion) online. In Italy, a nine-year Lotto concession was awarded in 2025 to a consortium comprising Allwyn, Sisal, and IGT, highlighting the preference for omnichannel joint ventures in high-value Southern European markets.

North America recorded the highest growth, with a 10.11% CAGR, driven by the expansion of iLottery legalization across U.S. states and the integration of retail and online play in Canadian provinces. Michigan surpassed USD 1 billion in digital sales in 2025 while maintaining retail revenue. New York's iLottery launch in November 2024 exceeded expectations, generating USD 180 million in its first six months, 22% above forecasts. Ontario's open gaming framework resulted in total igaming revenues of CAD 1 billion (USD 740 million) by 2025, with the lottery segment accounting for 15%. In Mexico, a newly introduced mobile app targeting 92 million internet users aimed to achieve USD 50 million in its first year.

The Asia-Pacific region experienced steady digital growth, though it was constrained by restrictions in China, several Indian states, and Indonesia. Australia's Lottery Corporation reported a 9% year-over-year increase, achieving AUD 3.9 billion (USD 2.6 billion) in online revenues for FY 2025. In New Zealand, Lotto NZ generated NZD 680 million (USD 420 million) in 2024, with mobile accounting for 72% of the total. Brazil finalized its federal igaming regulations in 2025, with implementation planned for 2026, potentially unlocking a market of over 150 million players. However, in the Philippines and across the Middle East and Africa, regulators are proceeding cautiously, weighing social costs against fiscal revenues, which has slowed the adoption of digital lotteries.

Competitive Landscape

The online lottery market is moderately fragmented. Established technology providers secure multi-year contracts by leveraging their expertise in regulatory compliance and operational scale, thereby gaining competitive advantages. International Game Technology has strengthened its position by signing a 10-year contract extension with the North Carolina Education Lottery. This extension, effective from 2027 to 2037, includes upgrades to the Aurora central system and retail technology, supporting over USD 1 billion in annual education funding. Similarly, NeoPollard Interactive has reinforced its strategic presence by renewing contracts with the Virginia Lottery and entering Alberta's draw games market, seamlessly integrating its technology with existing lottery systems.

Emerging players are adopting artificial intelligence and blockchain technologies to differentiate their offerings and enhance operational efficiency. AI improves player experiences through data analysis and predictive modeling, while blockchain ensures transparent transaction records and automates smart contracts, reducing operational costs and minimizing fraud risks. Major market players include Allwyn Entertainment, Francaise des Jeux, Lotto Agent, ZEAL Network SE, and Lottoland. These companies focus on product innovation to expand their global reach and diversify their brand portfolios to meet varied consumer preferences.

Mobile-first lottery platforms offer significant opportunities, particularly in emerging markets with limited traditional retail infrastructure. This is especially relevant in regions experiencing rapid smartphone adoption and digital payment integration. Regulatory compliance requirements present challenges for new entrants but provide advantages to established players with proven track records and strong governmental relationships. The sector's technology-driven transformation benefits companies investing in digital capabilities, responsible gambling tools, and cross-platform integration to meet evolving consumer expectations and regulatory demands.

Online Lottery Industry Leaders

Francaise des Jeux

Allwyn Entertainment

ZEAL Network SE

Lottoland

Lotto Agent

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FOMO7, a well-established name in online entertainment, has introduced a major update to its gaming platform by adding 46 new Indian lottery games. This enhancement provides players with more opportunities to win guaranteed prizes alongside their regular winnings.

- December 2024: Pollard Banknote collaborated with Premier Lotteries Ireland to introduce a mobile app and an eInstant games portfolio, featuring 11 integrated games for a seamless digital lottery experience on Android and iOS platforms.

- November 2024: Goa has become one of the first Indian states to introduce a fully tech-enabled online lottery. This platform, developed through a partnership between Rhiti Sports and Dusane Infotech, aims to redefine the lottery industry by prioritizing transparency and accessibility, with prize money exceeding Rs 50 crore.

- October 2024: IGT Global Solutions Corporation has signed a 10-year contract extension with the North Carolina Education Lottery. According to the agreement, IGT will implement its high-performing Aurora™ central system, a key component of IGT's integrated lottery solution, OMNIA™.

Global Online Lottery Market Report Scope

An online lottery is a system where one can bet an amount online and gain returns. These games are linked to a central computer, further connected through a telecommunication network, allowing players to play and win tickets by chance and luck. The online lottery market is segmented by end-user type and geography. The market is segmented into desktop and mobile users based on end users. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Desktop |

| Mobile |

| Draw-based Lottery |

| Instant Lottery |

| Spots Lottery |

| Others |

| Below 25 Years |

| 25–40 Years |

| 40–55 Years |

| 55+ Years |

| Male |

| Female |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Sweden | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | Oceanic Countries |

| Rest of Asia-Pacific | |

| Rest of the Wolrd | South America |

| Middle East and Africa |

| By Platform Type | Desktop | |

| Mobile | ||

| By Game Type | Draw-based Lottery | |

| Instant Lottery | ||

| Spots Lottery | ||

| Others | ||

| By Age Group | Below 25 Years | |

| 25–40 Years | ||

| 40–55 Years | ||

| 55+ Years | ||

| By End User | Male | |

| Female | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Sweden | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | Oceanic Countries | |

| Rest of Asia-Pacific | ||

| Rest of the Wolrd | South America | |

| Middle East and Africa | ||

Key Questions Answered in the Report

How large will the online lottery market be by 2031?

The online lottery market size is forecast to reach USD 19.65 billion by 2031, growing at an 8.92% CAGR over 2026-2031.

Which platform grows fastest in global online lottery sales?

Mobile is advancing at a 10.52% CAGR as smartphone adoption deepens and digital wallets trim payment friction.

Which region currently delivers the quickest revenue expansion?

North America leads with a 10.11% CAGR because additional U.S. states and Canadian provinces are legalizing iLottery.

What game format is gaining share most rapidly?

Instant-win digital scratch cards are outpacing draw games at a 10.11% CAGR owing to on-demand, mobile-friendly play.

Page last updated on: