Snus Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.17 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Snus Market Analysis by Mordor Intelligence

Snus market size in 2026 is estimated at USD 3.35 billion, growing from 2025 value of USD 3.21 billion with 2031 projections showing USD 4.17 billion, growing at 4.43% CAGR over 2026-2031. The market is shaped by harm-reduction policy changes, significant capacity expansions by leading players, and rapid flavor innovations. Public health campaigns and increased consumer awareness are positioning snus as a lower-risk alternative to traditional cigarettes. The growth of e-commerce has expanded market accessibility. Additionally, rising demand for environmentally friendly packaging and sustainably sourced tobacco is enhancing the market's appeal. North America dominates the snus market, driven by a landmark marketing authorization from the U.S. Food and Drug Administration (FDA) in January 2025, which approved 20 ZYN pouch variants, legitimizing the entire snus category. The Asia-Pacific region is experiencing the fastest growth, fueled by increasing awareness in countries such as Japan, Thailand, and India. Meanwhile, Europe's fragmented regulatory environment presents challenges but also offers selective growth opportunities. Favorable regulations in Nordic countries, particularly Sweden, provide a stable foundation for growth. Leading tobacco companies are investing in U.S. manufacturing upgrades to secure pharmaceutical-grade nicotine supplies and accelerate the launch of new products. Innovations such as discreet "all-white" cellulose pouches and AI-driven product personalization are expanding the market's appeal, especially among younger adults and female consumers, supporting sustained demand growth over the coming years.

Key Report Takeaways

- By product type, portion snus led with 90.82% revenue share in 2025; loose snus is forecast to register a 2.98% CAGR through 2031.

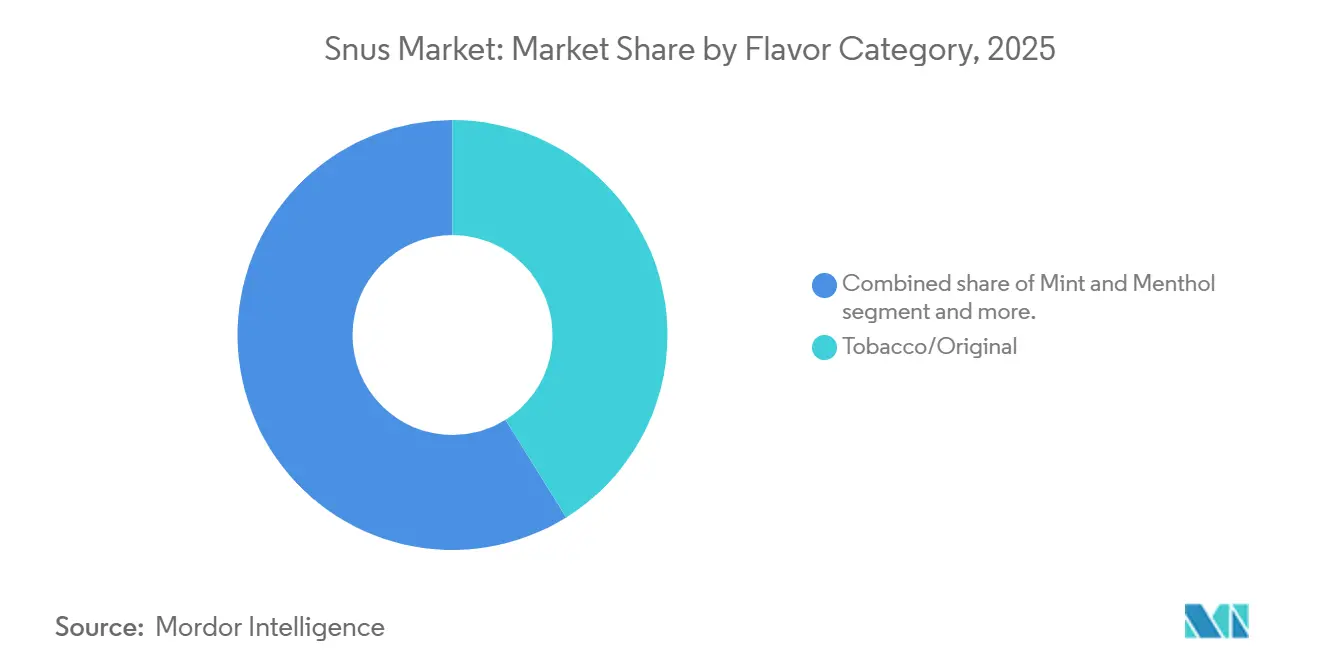

- By flavor category, traditional tobacco held 41.12% of the snus market share in 2025, whereas mint and menthol is projected to expand at a 3.37% CAGR between 2026-2031.

- By end user, men accounted for 76.54% of the snus market size in 2025, while the women’s segment is set to post a 4.58% CAGR to 2031.

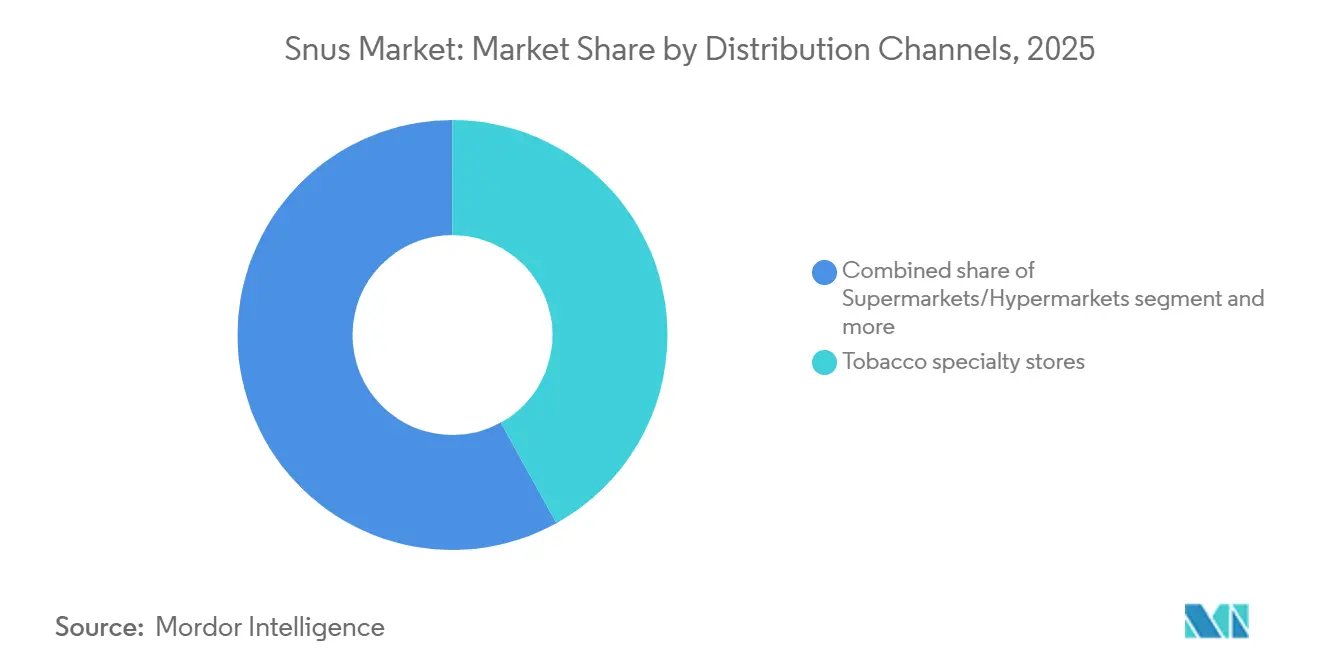

- By distribution channel, tobacco specialty stores maintained 41.97% share of the snus market size in 2025; online retail is advancing at a 4.06% CAGR through 2031.

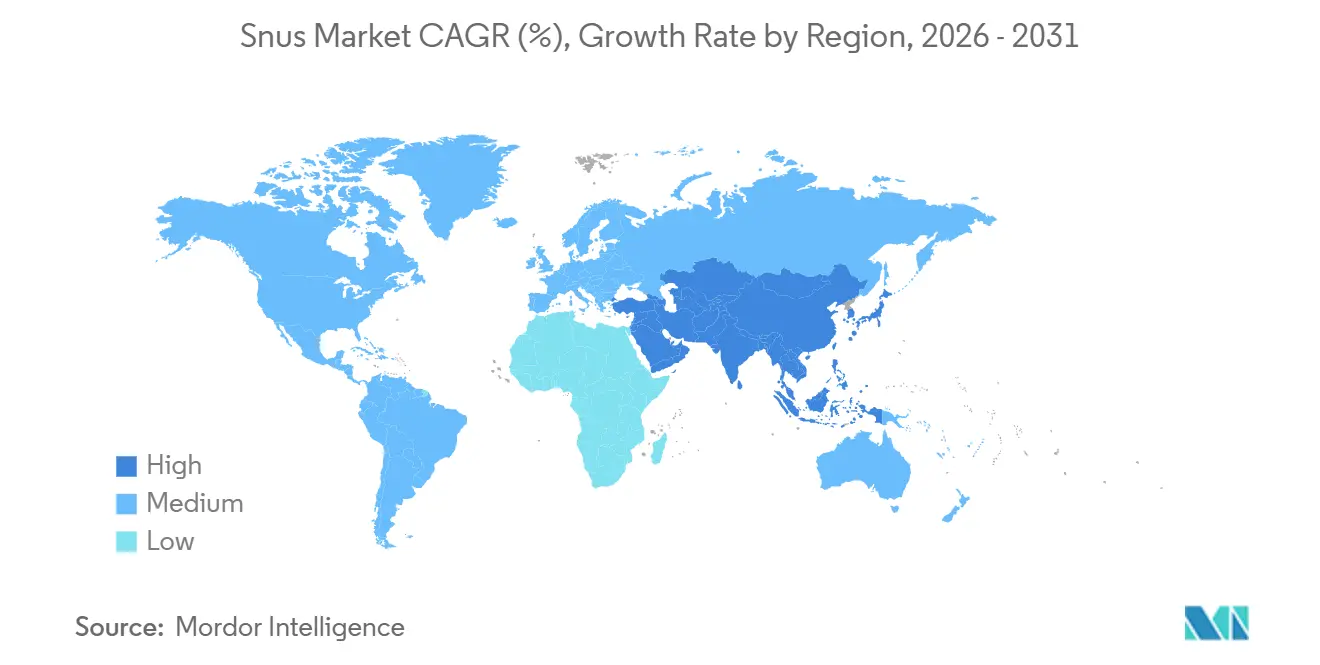

- By geography, North America commanded 60.73% of the snus market in 2025; Asia-Pacific is the fastest-growing region at a 4.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Snus Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased demand for smokeless tobacco alternatives | +1.2% | Global (North America and Europe strongest) | Medium term (2-4 years) |

| Product innovation and flavor variety | +0.8% | North America and Europe core; Asia-Pacific emerging | Short term (≤ 2 years) |

| Convenience and discreet nicotine consumption | +0.7% | Global, especially urban markets | Short term (≤ 2 years) |

| Rise of “all-white” cellulose pouches attracting first-time users | +0.6% | North America and Europe core; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expanding awareness and adoption in new geographies | +0.9% | Asia-Pacific core; spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Ai-driven nicotine customization and marketing | +0.4% | Advanced markets in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased demand for smokeless tobacco alternatives

Regulatory momentum toward harm reduction is creating significant market opportunities as health authorities recognize the varying risk profiles of nicotine delivery systems. The increasing prevalence of smoking-related diseases is driving demand for smokeless tobacco alternatives, such as snus. Cigarette smoking continues to be a major public health issue, with over 16 million Americans living with smoking-related diseases in 2024[1]Source: Centers for Disease Control and Prevention, "Smoking and Tobacco Use", cdc.gov, according to the Centers for Disease Control and Prevention. The FDA's renewal of Modified Risk Tobacco Product (MRTP) orders for 8 General Snus products, effective through November 2032, establishes a regulatory precedent for reduced-risk marketing claims. In December 2024, Sweden's Parliament formally incorporated tobacco harm reduction into its public health policy, illustrating how risk-proportionate taxation and regulation can promote population-level smoking cessation. This regulatory acceptance provides a competitive advantage to companies with established smokeless portfolios and PMTA-ready products, while traditional cigarette manufacturers face declining volumes and increasing margin pressures.

Product innovation and flavor variety

Technological advancements in pouch design and nicotine delivery systems are significantly broadening the category's appeal, reaching beyond its traditional consumer base. In March 2025, Scandinavian Tobacco Group introduced KLAR pouches featuring bioceramic technology, which is designed to enable faster and more efficient nicotine absorption, offering a more satisfying experience for users. Similarly, British American Tobacco has enhanced its VELO Plus product line with hinged lid designs, aimed at improving convenience and overall user experience. In April 2025, XQS UK launched a range of innovative flavors, including Raspberry Blackcurrant, Strawberry Kiwi, and Berrynana Twist, specifically targeting younger adult consumers who are increasingly seeking alternatives to traditional tobacco flavors. Manufacturing advancements are also evident in packaging, with companies adopting fully recyclable materials and incorporating child-resistant designs. These efforts not only ensure compliance with regulatory requirements but also help brands stand out in a competitive market. Furthermore, the innovation cycle within the industry has accelerated, as companies actively utilize consumer feedback loops and rapid prototyping techniques to introduce new product variants on a quarterly basis, rather than adhering to the traditional annual launch schedule.

Convenience and discreet nicotine consumption

As urbanization continues to rise and workplace smoking restrictions become more stringent, the demand for discreet, odorless nicotine delivery solutions that seamlessly integrate into professional environments is increasing. Snus remains a more affordable option for consumers due to its significantly lower excise tax compared to cigarettes, promoting regular use. In 2024, the Swedish Tax Agency stated that the tax on snus in Sweden was SEK 526 per kilogram[2]Source: Swedish Tax Agency," Skattesatser för tobak", skatteverket.se. Modern oral nicotine products effectively address the social stigma associated with traditional smokeless tobacco by offering a controlled nicotine release lasting between 30 to 60 minutes. Consumer behavior analysis reveals a strong purchase intent among adults aged 24 and older, particularly those who smoke and are actively seeking to quit. Conversely, these products exhibit minimal appeal to individuals who have never smoked, aligning with broader public health objectives. The convenience of these products is especially significant in markets with comprehensive smoke-free legislation, where traditional smoking is becoming increasingly impractical. Additionally, the adoption of digital tools, such as age-verification systems and subscription-based delivery models, enhances product accessibility while ensuring compliance with regulatory requirements.

Rise of “all-white” cellulose pouches attracting first-time users

Formulations that are free from tobacco and utilize either synthetic nicotine or nicotine derived from tobacco, embedded in plant-fiber matrices, effectively eliminate a significant number of harmful and potentially harmful constituents (HPHCs) typically found in traditional snus. According to an FDA analysis of ZYN pouches, 36 out of 42 HPHCs were detected at levels too low to quantify, highlighting a substantial reduction in toxicant levels when compared to cigarettes and moist snuff. This improved safety profile is particularly appealing to health-conscious consumers who have historically avoided tobacco products, thereby expanding the potential market to include a broader audience beyond traditional smokeless product users. From a manufacturing perspective, these products offer several advantages, including consistent nicotine content, an extended shelf life, and reduced regulatory challenges in regions where tobacco-free products are subject to less stringent oversight. Additionally, the white pouch format addresses concerns related to staining and residue, issues that have previously discouraged adoption among professional demographics, further enhancing their appeal in the market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory restrictions | –1.1% | European Union and selected emerging markets | Medium term (2-4 years) |

| Health-risk perception and anti-tobacco lobbies | –0.7% | Developed markets worldwide | Long term (≥ 4 years) |

| Supply-chain volatility in pharma nicotine | –0.5% | Global manufacturing hubs | Short term (≤ 2 years) |

| Competition from other nicotine alternatives | –0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory restrictions

Regulatory fragmentation across jurisdictions increases compliance challenges and creates market access barriers, hindering growth potential. The European Union's Tobacco Products Directive limits the sale of tobacco-containing snus to Sweden. However, individual EU member states impose additional restrictions on nicotine pouches, despite their tobacco-free nature. France's proposed ban on nicotine pouches, opposed by Sweden, highlights the fragmented European market and the growing regulatory uncertainty. According to the World Health Organization, in 2024, tobacco causes over 7 million deaths annually, including approximately 1.6 million non-smokers exposed to second-hand smoke[3]Source: World Health organization, "Tobacco Key facts", who.int. This concerning statistic supports the implementation of strict regulatory measures on snus. The FDA's import alert system, aimed at unauthorized products, demonstrates its impact on disrupting established supply chains, as seen with detention orders against The Snus Factory and Another Snus Factory Stockholm AB. Manufacturers face rising compliance costs as they navigate varied regulatory pathways, age-verification requirements, and marketing restrictions across different jurisdictions.

Supply-chain volatility in pharmaceutical-grade nicotine

Manufacturing bottlenecks in the production of pharmaceutical-grade nicotine are creating significant supply constraints, which are hindering market expansion and driving up input costs. The reliance on a limited number of suppliers for nicotine extraction and purification capabilities has made the market highly susceptible to disruptions. This vulnerability was clearly illustrated by the ZYN shortage that began in May 2024. To address these supply challenges, Philip Morris International committed USD 832 million to expand capacity at its facilities in Kentucky and Colorado. The stringent quality requirements for pharmaceutical-grade nicotine, which mandate a purity level exceeding 99%, significantly restrict the number of eligible suppliers and pose substantial barriers to entry for new manufacturers. Furthermore, as the demand for tobacco-free formulations continues to grow, the supply chain is becoming increasingly complex. Scaling up synthetic nicotine production to meet this demand requires advanced chemical synthesis capabilities and compliance with rigorous regulatory approval processes, adding further challenges to the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portion Snus Dominates Through Convenience

Portion snus holds a dominant 90.82% market share in 2025, driven by consumer preference for its pre-portioned, discreet packaging. This format avoids the mess and social stigma associated with loose varieties. With a projected CAGR of 2.98% from 2026 to 2031, its growth is supported by innovations such as moisture optimization, improved pouch materials, and advanced flavor encapsulation. On the other hand, loose snus, though a smaller segment, appeals to traditional users who prefer customizable portion sizes and authentic Scandinavian consumption methods.

Portion snus benefits from manufacturing efficiencies, utilizing automated packaging systems and strict quality controls. This enables mass production at lower unit costs. British American Tobacco's Pécs facility in Hungary, certified with ISO 22000 food safety standards, highlights how food-industry practices enhance product quality and ensure regulatory compliance. Additionally, the portion format supports flavor and nicotine strength innovations while preserving product integrity during storage and distribution.

By Flavor Category: Mint Innovation Challenges Traditional Preferences

Traditional tobacco and original flavors hold a 41.12% market share in 2025, highlighting their strong consumer appeal and widespread regulatory approval. For experienced users, the original flavor represents authenticity, tradition, and quality, reinforcing its leading position. However, mint and menthol variants are experiencing rapid growth, with a 3.37% CAGR projected from 2026 to 2031. Their popularity stems from cooling sensations and breath-freshening qualities, which enhance their social acceptability. At the same time, younger adults are increasingly drawn to fruit and berry flavors as alternatives to traditional tobacco. Specialty flavors, including coffee, citrus, and seasonal options, continue to expand the market's reach.

Flavor development is shifting towards natural extract formulations, driven by health-conscious consumer preferences and potential regulatory restrictions on artificial additives. The FDA's approval of 10 ZYN flavor variants, including non-traditional options like Coffee and Citrus, sets a regulatory precedent for diverse flavor profiles in authorized products. In February 2025, Scandinavian Tobacco Group demonstrated the importance of flavor innovation by rapidly expanding its flavor portfolio in the UK market, introducing Black Cherry and Citrus Cooling variants, which highlight the role of flavor diversity in driving brand differentiation and increasing market share.

By End User: Women's Segment Disrupts Traditional Demographics

Men account for 76.54% of the market in 2025, a trend influenced by historical consumption patterns and cultural associations with traditional snus. Leading snus brands have historically focused their designs and marketing on male consumers, emphasizing themes of strength, tradition, and masculinity. However, the female demographic is now the fastest-growing segment, with a 4.58% CAGR projected for 2026-2031. This growth is driven by discreet product formats, appealing flavor options, and reduced social stigma compared to traditional smokeless products. This demographic shift marks a significant expansion of the market beyond its core smokeless tobacco user base.

Product innovations are increasingly catering to female preferences, offering smaller pouch sizes, subtle flavors, and elegant packaging that contrasts with the traditionally masculine image of tobacco products. The all-white pouch format addresses staining concerns while providing controlled nicotine delivery, appealing to professional women seeking smoking alternatives. Marketing strategies now focus on lifestyle integration and social acceptability, moving away from traditional tobacco messaging and significantly expanding the market's reach.

By Distribution Channels: Digital Transformation Accelerates

Tobacco specialty stores hold a 41.97% market share in 2025, driven by their product expertise and strong connections with adult tobacco consumers. These stores often surpass general retail outlets by providing tobacco users with a superior shopping experience, including better ambiance and product availability. However, online retail channels are experiencing the fastest growth, with a projected 4.06% CAGR from 2026 to 2031. This growth is supported by age-verification technologies and direct-to-consumer models that eliminate traditional distribution markups. While convenience stores and supermarkets offer wide market access, they are increasingly under regulatory scrutiny aimed at preventing youth access.

Digital transformation in the tobacco sector faces challenges. For example, Philip Morris suspended ZYN online sales due to regulatory concerns over flavored product compliance in areas with flavor bans. E-commerce platforms are leveraging advanced age-verification systems and geographic restrictions to comply with regulations while meeting consumer demand for convenient and discreet purchasing. The UK's nicotine pouch market, which has seen a ~79% year-over-year volume increase, highlights the effectiveness of multi-channel distribution strategies in enhancing market penetration.

Geography Analysis

North America holds a leading 60.73% market share on 2025, driven by regulatory approvals and significant investments from major tobacco companies. The FDA's approval in January 2025 of 20 ZYN products marks a turning point, establishing a regulatory pathway for marketing nicotine pouches in the world's largest tobacco market. Philip Morris International's USD 832 million investment in manufacturing facilities in Kentucky and Colorado strengthens the region's dominance through 2030. Additionally, Canada's regulatory framework, which exempts tobacco-free nicotine pouches (≤4 mg/dose) from prescription requirements, creates new growth opportunities. In Mexico, while strict tobacco control laws present challenges, the courts' 2025 decision to uphold these regulations also opens avenues for reduced-risk products that adhere to stringent advertising restrictions.

Europe's regulatory environment remains fragmented. Sweden leads in harm reduction, while other EU member states enforce more restrictive policies. Sweden's formal adoption of a harm reduction policy in December 2024, including preferential taxation for snus over cigarettes, reinforces its status as a global model for risk-proportionate regulation. Following the June 2025 ban on disposable vapes, the UK has emerged as Europe's third-largest nicotine pouch market, capitalizing on substitution opportunities for oral nicotine products. Germany's complex regulatory framework, where tobacco-containing snus is banned under EU TPD but nicotine pouches face only regional restrictions, highlights the diverse national regulations that create both market opportunities and compliance challenges.

Asia-Pacific is poised for the fastest regional growth, with a 4.86% CAGR from 2026 to 2031, driven by increasing awareness and evolving regulatory frameworks in key markets. Japan's classification of synthetic nicotine pouches outside traditional tobacco regulations provides market access opportunities through pharmaceutical approval pathways. Thailand's regulatory ambiguity regarding personal snus imports, coupled with growing acceptance of tobacco-free alternatives, demonstrates how unclear regulations can foster market development. India's emerging manufacturing capabilities, exemplified by companies like Mohan Food Products with a 20-tonne production capacity for nicotine pouches, signal potential for regional supply chain growth. On the other hand, Singapore's comprehensive ban on nicotine pouches, including restrictions on promotion and importation, illustrates how stringent policies can limit market access despite regional growth trends.

Competitive Landscape

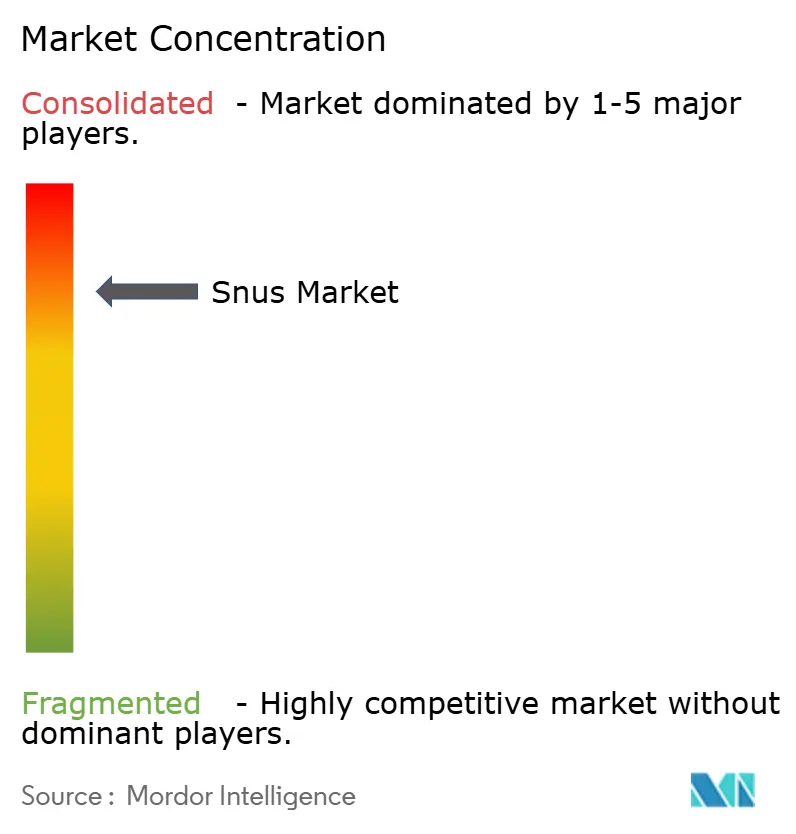

The snus market is consolidated with established tobacco conglomerates leveraging distribution networks, regulatory expertise, and manufacturing scale to maintain competitive advantages. Philip Morris International solidified its leadership in the nicotine pouch segment through its USD 16 billion acquisition of Swedish Match. Similarly, Japan Tobacco's proposed USD 2 billion acquisition of Vector Group highlights the ongoing consolidation trend among top-tier players, as companies aim to strengthen their market positions. Regulatory barriers, which restrict new entrants, contribute to moderate competitive intensity and favor firms with well-established PMTA capabilities and robust compliance infrastructures.

In this market, companies focus on strategic differentiation through product innovation, expedited regulatory approvals, and enhanced manufacturing capacities rather than engaging in price competition. British American Tobacco, under its "Building a Smokeless World" initiative, has set an ambitious target to generate 50% of its revenue from non-combustible products by 2035. Meanwhile, Imperial Brands is actively expanding its Next Generation Products (NGP) portfolio across more than 20 markets, reflecting the broader industry shift toward reduced-risk alternatives. Prominent players in the market include Philip Morris International, British American Tobacco PLC, Altria Group Inc., Imperial Brands PLC, and GN Tobacco Sweden AB. Historically, tobacco companies have relied on innovation and new product development (NPD) to enhance brand performance, retain existing customers, and attract new ones. This approach has driven global firms to diversify steadily into alternative tobacco and nicotine products, including smokeless tobacco, as part of their growth strategies.

Emerging markets with underdeveloped regulatory frameworks and niche product segments, such as caffeine-infused pouches or pharmaceutical-grade formulations, present significant growth opportunities. In response to the highly regulated nature of the tobacco industry, companies are prioritizing technological advancements in areas like manufacturing automation, age-verification systems, and AI-driven consumer insights. These efforts underscore the importance of compliance and operational efficiency over the pursuit of disruptive product innovations, aligning with the industry's regulatory demands and market dynamics.

Snus Industry Leaders

-

Philip Morris International

-

British American Tobacco PLC

-

Altria Group Inc.

-

Imperial Brands PLC

-

GN Tobacco Sweden AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Scandinavian Tobacco Group has introduced three new XQS flavors in the UK: Raspberry Blackcurrant, Strawberry Kiwi, and Berrynana Twist, expanding its portfolio to eight SKUs. These new offerings address the increasing consumer preference for fruity flavors with a long-lasting nicotine experience.

- May 2024: Scandinavian Tobacco Group introduced XQS nicotine pouches in the UK, offering four distinct flavors and varying nicotine strengths. This launch, aimed at Europe's third-largest nicotine pouch market, was bolstered by an expanded field sales team and active consumer engagement initiatives.

- April 2024: Philip Morris International has invested USD 232 million to expand its ZYN manufacturing facility in Owensboro, Kentucky. This expansion facilitates 24/7 production and aims to achieve a capacity of 900 million cans by 2025.

- April 2024: Japan Tobacco aims to strengthen its position in the US market through the acquisition of Vector Group Ltd. This strategic acquisition is expected to increase Japan Tobacco's US market share by 3.2%, bringing its total share close to 8%, aligning it with ITG Brands' market position.

Global Snus Market Report Scope

Snus is a moist, smokeless, finely ground tobacco product marketed as a less harmful alternative to smoking.

The snus is segmented by product type, distribution channel, and geography. Based on product type, the market studied is segmented into loose snus and portion snus. Based on distribution channels, the market studied is segmented into tobacco stores, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Loose Snus |

| Portion Snus |

| Tobacco/Original |

| Mint and Menthol |

| Fruit and Berry |

| Other Flavors |

| Men |

| Women |

| Tobacco Specialty Stores |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Czech Republic |

| Denmark | |

| Norway | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | India |

| Rest of Asia-Pacific | |

| Rest of the World | South Africa |

| Algeria | |

| Other Countries |

| By Product Type | Loose Snus | |

| Portion Snus | ||

| By Flavor Category | Tobacco/Original | |

| Mint and Menthol | ||

| Fruit and Berry | ||

| Other Flavors | ||

| By End User | Men | |

| Women | ||

| Distribution Channels | Tobacco Specialty Stores | |

| Supermarkets/Hypermarkets | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Czech Republic | |

| Denmark | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| Rest of Asia-Pacific | ||

| Rest of the World | South Africa | |

| Algeria | ||

| Other Countries | ||

Key Questions Answered in the Report

What is the current global value of the snus market?

The snus market size reached USD 3.35 billion in 2026 and is projected to grow to USD 4.17 billion by 2031 at a 4.43% CAGR.

Which region generates the highest snus revenue?

North America leads with 60.73% of global revenue, fueled by recent FDA approvals and large-scale capacity investments.

Which product segment dominates sales?

Portion snus holds 90.82% of revenue owing to convenience, automated production and quicker regulatory clearance.

How fast is the women’s user base expanding?

The women’s segment is forecast to grow at a 4.58% CAGR from 2026-2031, outpacing the overall market.

Page last updated on: