Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

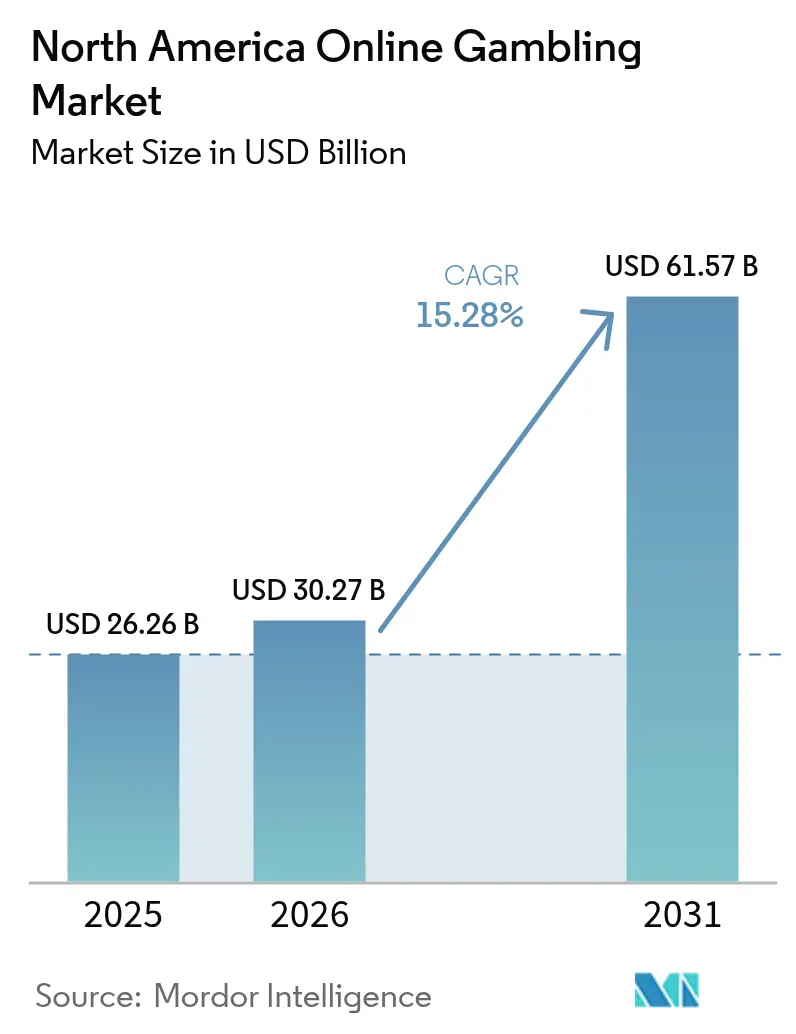

| Base Year Market Size (2025) | USD 26.26 Billion |

| Market Size (2026) | USD 30.27 Billion |

| Market Size (2031) | USD 61.57 Billion |

| Growth Rate (2026 - 2031) | 15.28% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Online Gambling Market Analysis by Mordor Intelligence

North America online gambling market size in 2026 is estimated at USD 30.27 billion, growing from 2025 value of USD 26.26 billion with 2031 projections showing USD 61.57 billion, growing at 15.28% CAGR over 2026-2031. Swift digital transitions are reshaping the landscape of online gambling, with waves of state-level legalizations and the rise of AI-driven commercial tools. These advancements are revolutionizing how bettors engage with sports, casinos, lotteries, and bingo. Operators are turning to blockchain-enabled payments, slashing both transaction costs and settlement durations. Furthermore, tighter bonds between streaming media and betting platforms are expediting the journey from content viewing to placing a bet. While there's a pronounced shift towards mobile, innovative cross-platform designs ensure desktops remain relevant. A younger median age among bettors fuels a sustained surge in revenues. Although increased regulatory scrutiny on responsible gambling and player protection has led to heightened compliance costs, it simultaneously fosters public trust, bolstering mainstream acceptance.

Key Report Takeaways

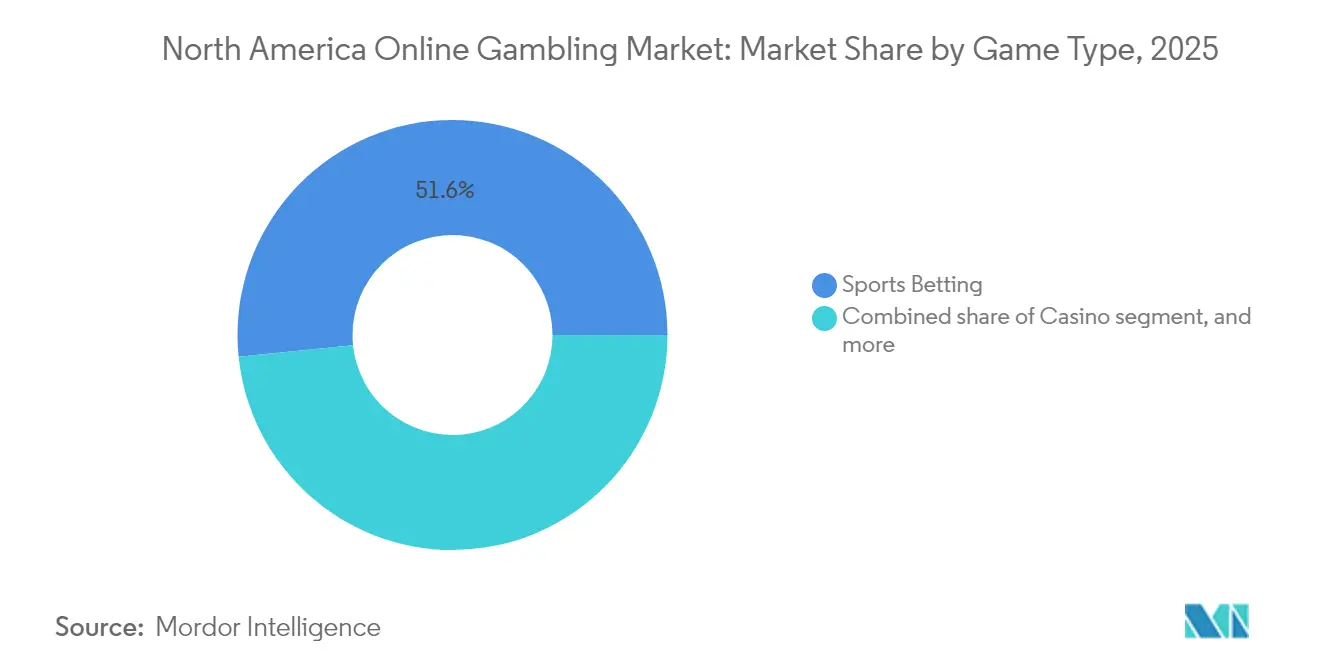

- By game type, sports betting accounted for 51.62% of regional revenue in 2025, whereas casino gaming is forecast to compound at an 17.92% CAGR through 2031.

- By platform, mobile and tablets delivered 72.10% of total user activity in 2025, while desktop applications are expanding at a 16.03% CAGR as multi-screen analytics tools gain favor.

- By age group, the 25–34 cohort held 34.30% of active bettor accounts in 2025; the 18–24 bracket is on track for 16.74% CAGR, highlighting Gen Z adoption tailwinds.

- By betting type, pre-match wagering retained a 59.55% share in 2025, but live/in-play stakes will accelerate at 18.05% CAGR on the back of real-time data feeds and micro-markets.

- By geography, the United States contributed 79.05% share in 2025, while Canada registered the fastest climb at 15.82% CAGR, thanks to province-level regulatory harmonization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Online Gambling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legalization expanding across states | +4.2% | United States, with spillover to Canada | Medium term (2-4 years) |

| AI and data-driven personalization | +3.1% | North America, concentrated in tech-forward states | Short term (≤ 2 years) |

| Esports and fantasy betting integration | +2.8% | United States and Canada, urban markets | Medium term (2-4 years) |

| Cross-media partnerships integrating live sports and betting feeds | +2.3% | United States, expanding to Canada | Short term (≤ 2 years) |

| Advanced payment solutions (Digital wallets, cryptocurrency, blockchain) | +1.9% | North America, regulatory approval dependent | Long term (≥ 4 years) |

| Personalized user experience | +1.3% | Global, with North America early adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legalization expanding across states

Vermont kicked off operations in January 2024, and North Carolina is set to follow suit in Q1 2024, underscoring a growing trend of state-by-state legalization. In Wyoming, the House Bill HB0120 lays down a comprehensive framework for interactive gaming, mandating an initial operator permit fee of USD 100,000 and imposing a 10% tax on monthly revenues[1]Source: Wyoming Legislature, “House Bill HB0120, framework for interactive gaming,” wyoleg.gov. This move, as noted by the Wyoming Legislature, reflects a push towards standardization across different jurisdictions. Meanwhile, in Missouri, the Secretary of State's rejection of emergency rulemaking has led to regulatory delays, with potential market launches now pushed back by 6-12 months. Such a fragmented landscape offers a dual-edged sword: operators can gain first-mover advantages by securing early market access, but they also grapple with heightened compliance costs due to varying jurisdictional demands. In Alberta, the unveiling of the iGaming Alberta Act hints at provincial efforts to harmonize regulations, potentially paving the way for broader cross-border operator expansions and collaborative liquidity pooling.

AI and data-driven personalization

Artificial intelligence is reshaping how businesses attract and retain customers, leveraging tools like predictive analytics and behavioral targeting. However, the absence of clear regulations poses ethical dilemmas. The Ethical AI Standards Committee of the International Gaming Standards Association is crafting best-practice frameworks. Their focus is on ensuring AI systems don't exploit vulnerable players for profit, as highlighted by the University of Florida[2]Source: Alisha Katz, “AI is Transforming Gambling, Ethical AI Standards Committee of the International Gaming Standards Association,” Phys.org, phys.org. While the U.S. Blueprint for an AI Bill of Rights sets a foundation, it falls short on industry-specific directives, leaving operators in the lurch as they invest in machine learning. Proposed measures advocate for independent audits of AI systems, clarity in game recommendations, and openness about data collection. The current lack of thorough AI regulations fosters swift innovation but also invites potential consumer protection challenges, which could lead to stricter laws. By adopting ethical AI practices now, operators not only prepare for impending regulations but also cultivate trust with consumers through clear and fair algorithmic choices.

Esports and fantasy betting integration

Esports wagering gains momentum with regulatory nods and platform integrations, yet legal hurdles cast a shadow of uncertainty. In 2016, the Nevada Gaming Control Board set a pivotal precedent for esports betting in Las Vegas, approving League of Legends tournament wagering at William Hill Sports Book, as reported by ESPN. However, a July 2025 opinion from California Attorney General Rob Bonta, labeling daily fantasy sports as illegal betting under Penal Code section 337a, sends ripples through the market, as highlighted by Esports Insider[3]Source: Kerman Garrett, “California Attorney General Declares DFS Illegal,” esportsinsider.com. This ruling not only disrupts California's hefty stake in the national DFS market but also hints at potential legislative shifts in other states. Adding to the intrigue, Governor Gavin Newsom publicly contests the Attorney General's stance, signaling a possible political compromise, even as fantasy operators gear up for legal battles. Meanwhile, the melding of esports tournaments with traditional sportsbooks opens doors for cross-selling and lures in younger audiences. Yet, the patchwork of regulatory standards across states poses challenges for nationwide platform rollouts.

Cross-media partnerships integrating live sports and betting feeds

Strategic media alliances are boosting user engagement by integrating real-time content and offering promotional opportunities across platforms. In a notable move, X has partnered with BetMGM to showcase betting statistics directly on its platform, complete with links to wagering interfaces. This is particularly striking given X's usual stance against promoting gambling. Meanwhile, ESPN BET, leveraging its account linking feature, allows users to monitor their bets within ESPN's ecosystem. Customers also benefit from tailored promotions based on their preferred teams and fantasy rosters, a feature highlighted by PENN Entertainment. In another significant partnership, Churchill Downs has inked a multi-year deal with FanDuel. This agreement not only secures exclusive television rights for racing content but also grants sponsorship rights for the prestigious Kentucky Derby, underscoring Churchill Downs Incorporated's savvy content monetization strategies. These collaborations not only fortify competitive advantages through exclusive content access but also open up new revenue avenues for media entities. Yet, as these partnerships flourish, they face mounting regulatory scrutiny. A notable 37 states have rolled out restrictions, particularly targeting promotions aimed at youth and those related to addiction messaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory landscape | -2.8% | United States, federal coordination gaps | Long term (≥4 years) |

| Cybersecurity and fraud risks | -1.9% | High-volume betting states across North America | Short term (≤2 years) |

| Responsible gambling and social concerns | -1.4% | United States and Canada | Medium term (2-4 years) |

| High taxation and licensing costs | -1.2% | State-specific, led by New York and Pennsylvania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented regulatory landscape

Across 38 states, inconsistent jurisdictions complicate operations and inflate compliance costs, hitting smaller operators harder while giving an edge to seasoned players with regulatory know-how. For instance, New York's hefty 51% gross gaming revenue tax starkly contrasts with Nevada's more lenient 6.75%, swaying operators' market entry choices, as highlighted by the National Conference of State Legislatures[4]Source: Lesley Kennedy, “Exploring Legalized Sports Betting,” ncsl.org. In Manitoba, a civil injunction against offshore operator Bodog underscores the patchy enforcement across provinces. Meanwhile, Ontario's market, with its competitive frameworks, lures in private operators. In Pennsylvania, the interactive gaming license process demands enterprise disclosures and thorough background checks, a move that, as per the Pennsylvania Gaming Control Board, burdens smaller entities while favoring those with deeper pockets. The lack of federal oversight not only opens doors to regulatory arbitrage but also heightens the risk of market fragmentation. Furthermore, while interstate compacts exist for liquidity pooling, their limited nature curtails the growth of poker and tournament betting across state lines.

Cybersecurity and fraud risks

Operational risks stemming from digital payment vulnerabilities and stringent data protection mandates necessitate hefty technology investments and continuous compliance oversight. The Department of Homeland Security highlights money laundering, cybercrime, and consumer scams as predominant threats in digital asset transactions[5]Source: Department of Homeland Security, “Combatting Illicit Activity,” dhs.gov. Furthermore, tools such as mixers, privacy coins, and decentralized finance platforms amplify these obfuscation risks. While cryptocurrency adoption in gambling platforms is on the rise, it grapples with anti-money laundering compliance hurdles. Casinos, under the Bank Secrecy Act, are tasked with upholding risk-based AML programs, all the while navigating the complexities of pseudo-anonymous transaction traceability. Cross-jurisdictional enforcement collaboration remains sparse, allowing illicit actors to maneuver deftly. Stricter mandates like enhanced KYC requirements, travel rule reporting, and multi-factor authentication, while bolstering security, also inflate operational costs and introduce friction in user experience. Despite the pressing need, cross-jurisdiction enforcement collaboration remains sparse, allowing illicit actors to deftly maneuver through regulatory voids, often leveraging offshore exchanges and privacy-centric payment methods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Sports Betting Dominance Faces Casino Innovation

In 2025, sports betting claims a dominant 51.62% market share, underscoring a clear consumer tilt towards skill-based wagering and real-time event participation. Meanwhile, casino gaming is on an upswing, projected to grow at an 17.92% CAGR through 2031. This surge is largely attributed to operators embracing immersive live dealer experiences and forging partnerships with branded content. The American Gaming Association forecasts a whopping USD 35 billion in legal wagers for the 2024 NFL season, marking a 30% leap from last season's USD 26.7 billion. This boost is largely fueled by fresh state launches in Maine, North Carolina, and Vermont. Football continues to dominate the sports betting arena, trailed by horse racing and tennis. Yet, the horizon is broadening with budding prospects in esports and fantasy integrations, paving the way for operators to cross-sell.

Casino gaming is reaping the rewards of technological advancements. A prime example is MGM Resorts' collaboration with Playtech, which streams exclusive live content from the iconic Bellagio and MGM Grand casino floors. This initiative is strategically aimed at regulated markets beyond U.S. borders. Different games cater to varied demographics: while slots draw in the casual crowd, poker is a magnet for the skill-centric. Established customer bases and straightforward regulatory landscapes ensure steady performances for lottery and bingo segments. In a bid to bolster platform loyalty and attract new users, FanDuel has rolled out Light & Wonder's Huff N' More Puff slot, underscoring the importance of content differentiation. This exclusive launch spans states like New Jersey, Pennsylvania, Michigan, West Virginia, Connecticut, and even reaches Ontario.

By Platform: Mobile Supremacy Drives Desktop Innovation

In 2025, mobile and tablet platforms dominate user engagement, accounting for 72.10%. Meanwhile, desktop experiences are witnessing a robust growth at a 16.03% CAGR. This growth is driven by operators enhancing betting complexity and analytical capabilities through complementary multi-screen functionalities. A report from the University of Nevada, Las Vegas, highlights a generational shift: Millennials and Gen Z users favor mobile-first designs, valuing convenience and real-time access over traditional desktop interfaces. Mobile platforms boast features like location-based services, push notifications, and biometric authentication, outpacing desktops in these capabilities.

Despite the mobile surge, desktop platforms hold a strategic edge for professional bettors and high-volume users. These users rely on advanced charting tools, multiple market displays, and sophisticated analytical interfaces. Meanwhile, platforms like smart TVs and other emerging devices present new opportunities. Operators are delving into voice-activated betting and augmented reality experiences. As users demand seamless transitions between devices, cross-platform synchronization becomes paramount. This ensures continuity in betting histories, account balances, and personalized settings. Operators that invest in unified platform architectures not only enhance user experience consistency but also leverage data analytics for informed product development and marketing strategies, securing a competitive edge.

By Age Group: Millennials Lead While Gen Z Accelerates

In 2025, users aged 25-34 account for 34.30% of the active gambling demographic, showcasing their established spending power and familiarity with the activity. Meanwhile, the 18-24 age group, as digital natives, is propelling market growth at a 16.74% CAGR through 2031, particularly favoring mobile-first betting experiences. According to the University of Nevada, Las Vegas, millennials lean towards table games over slots, appreciate social gaming elements, and value non-gaming amenities that enhance their gambling experience, highlighting a trend of integrating gambling into broader lifestyle choices. These evolving preferences are reshaping product development, marketing strategies, and the design of responsible gambling programs.

While the 35-44, 45-54, and 55+ age groups continue to hold a notable market share, driven by higher average spending and loyalty program engagement, their growth rates are stabilizing as digital adoption nears its peak. Gen Z stands out with unique behaviors, favoring esports betting, cryptocurrency transactions, and a strong tie to social media – areas where traditional operators find challenges. Highlighting the concerns, the International Association of Gaming Regulators points to the gambling risks for young adults, leading to a heightened regulatory emphasis on age verification, spending caps, and measures to prevent addiction. Operators face the dual challenge of attracting younger audiences while upholding responsible gambling standards and navigating the diverse regulatory landscape across jurisdictions.

By Betting Type: Pre-Match Stability Meets Live Innovation

In 2025, pre-match/fixed-odds betting commands a 59.55% market share, thanks to its predictable odds calculations and user-friendly interfaces. Meanwhile, live/in-play wagering is on the rise, boasting an 18.05% CAGR. This surge is fueled by operators' investments in real-time data feeds and micro-betting features, which boost user engagement during events. While traditional pre-match betting enjoys the advantages of customer familiarity and clear regulations, allowing operators to hone in on odds optimization and risk management, live leaps in data processing, mobile connectivity, and user interface design drive betting's evolution. These advancements empower real-time decision-making during events.

Operators harness advanced algorithms to swiftly adjust odds, responding to game dynamics, player performances, and betting volume trends. By weaving in live streaming, social elements, and same-game parlays, they craft engaging experiences that not only extend session durations but also amplify betting frequency. Yet, diving into live betting isn't without challenges. It demands hefty investments in tech infrastructure and navigation through regulatory approvals, which differ by jurisdiction. This creates hurdles for smaller operators, while established platforms, with their robust tech and regulatory ties, stand to gain significantly.

Geography Analysis

In 2025, the United States commands a dominant 79.05% market share, buoyed by state-by-state legalization and a robust operator infrastructure. However, disparities in profitability arise due to varying regulatory complexities and taxation across jurisdictions. For instance, New York, despite imposing a hefty 51% gross gaming revenue tax rate, one of the highest in the nation, raked in a whopping USD 188.53 million in sports betting tax revenue during Q3 2023. This figure accounted for over 37% of the nation's total sports betting tax collections, as highlighted by the US Census Bureau. Meanwhile, Pennsylvania showcased its market maturation with a record gaming revenue of USD 554.6 million in March 2024. Of this, iGaming contributed USD 191.1 million, and the state garnered a total tax revenue of USD 229.6 million, according to the Pennsylvania Gaming Control Board. In Illinois, the state-level revenue optimization strategies are evident as they implement a progressive taxation structure: starting at 15% on adjusted gross receipts for amounts up to USD 25 million, escalating to a steep 50% on revenues surpassing USD 200 million for non-table games, as per the Illinois Gaming Board.

Canada is on a rapid ascent, boasting the highest growth trajectory in North America at a projected 15.82% CAGR through 2031. This surge is largely attributed to provincial regulatory harmonization and a swift influx of operators, a momentum gained post the passage of Bill C-218 in June 2021. Ontario's iGaming market, which went live in April 2022, stands as a testament to this success. With private operators seamlessly integrated, iGaming Ontario proudly reports a GDP contribution exceeding CAD 2.7 billion and the creation of around 15,000 full-time jobs. Alberta, not to be left behind, has rolled out the iGaming Alberta Act, establishing the Alberta iGaming Corporation as a Crown agent. This move, aimed at managing online gambling partnerships with private entities, underscores the province's coordinated efforts, potentially paving the way for cross-border liquidity arrangements. Meanwhile, British Columbia Lottery Corporation's initiatives, like the GameSense program and Game Break self-exclusion system, are setting regulatory benchmarks. These frameworks, now being adopted by other provinces, present standardization opportunities for operators eyeing multi-provincial expansions.

Mexico is carving out a niche within the Rest of North America segment, navigating its gaming landscape under the Federal Gaming and Raffles Law. Currently, 36 permit holders, in partnership with land-based casinos, are authorized for online activities, as detailed in the Chambers Global Practice Guides. However, recent regulatory tweaks in November 2023 like the removal of sub-licensor structures and a cap on new casino permits pose hurdles for market entry. While these amendments aim to shield existing operators from heightened competition, they also stir constitutional litigation, casting a shadow of regulatory uncertainty. This ambiguity has led to a slowdown in international operators' expansion endeavors. Furthermore, stringent anti-money laundering mandates classify gambling as a "vulnerable activity." This designation necessitates client identification and transaction reporting for amounts exceeding USD 2,500. Such compliance costs, while burdensome for newcomers, play to the advantage of established operators with pre-existing AML frameworks.

Regulatory Landscape

Online gambling regulation in North America remains jurisdiction-led, with the United States largely governed at the state level and bounded federally by the Unlawful Internet Gambling Enforcement Act (UIGEA) of 2006, which restricts payment processing tied to unlawful internet gambling. Key operating rulebooks include New Jersey Division of Gaming Enforcement regulations (Chapter 69O), Michigan's Lawful Internet Gaming Act, and Nevada Gaming Control Board Regulation 5A, each setting requirements spanning licensure, game integrity, geolocation, and controls around wagering operations.

In Canada, Ontario continues to anchor the regulated private-operator model through iGaming Ontario and the Alcohol and Gaming Commission of Ontario (AGCO), where the Registrar's Standards for Internet Gaming define expectations for player protection, game integrity, and AML controls. The iGaming Ontario Act, 2024 establishes an updated legal framework for online lottery schemes effective April 1, 2026, while Indigenous and provincial oversight also shapes cross-border operations, such as the Kahnawake Gaming Commission amendments to its Regulations concerning Interactive Gaming dated January 14, 2026. Operators still face a compliance-first entry model, typically requiring parallel registrations, technical certifications, and responsible gambling programs tailored to each state or province.

Value Chain Analysis

The North America online gambling value chain begins with B2B technology and content inputs: platform and account management systems, sportsbook engines, casino game studios, and real-time sports data/API providers that support pre-match and live/in-play markets. This is complemented by trust and compliance services, including KYC/identity verification, AML screening, geolocation, fraud/risk tooling, and independent testing and certification, which are then translated into operator-facing layers such as CRM, personalization, and responsible gambling controls.

Distribution and monetization flow through licensed operators (digital-first brands and casino/sportsbook groups) that acquire customers via media and league partnerships, affiliates, and app ecosystems, then convert and retain players through payments, loyalty, and product differentiation. Payment processing rails (cards, ACH, digital wallets, and other approved methods) and cloud/infrastructure uptime underpin service continuity, while switching costs and vendor lock-in around proprietary sportsbook engines, RNG implementations, and integrations can slow expansion into new jurisdictions. Enforcement actions against unlicensed offshore or sweepstakes-style models and state/provincial rule changes also create recurring reconfiguration work across the value chain, raising the need for modular, multi-jurisdiction platform architectures.

Competitive Landscape

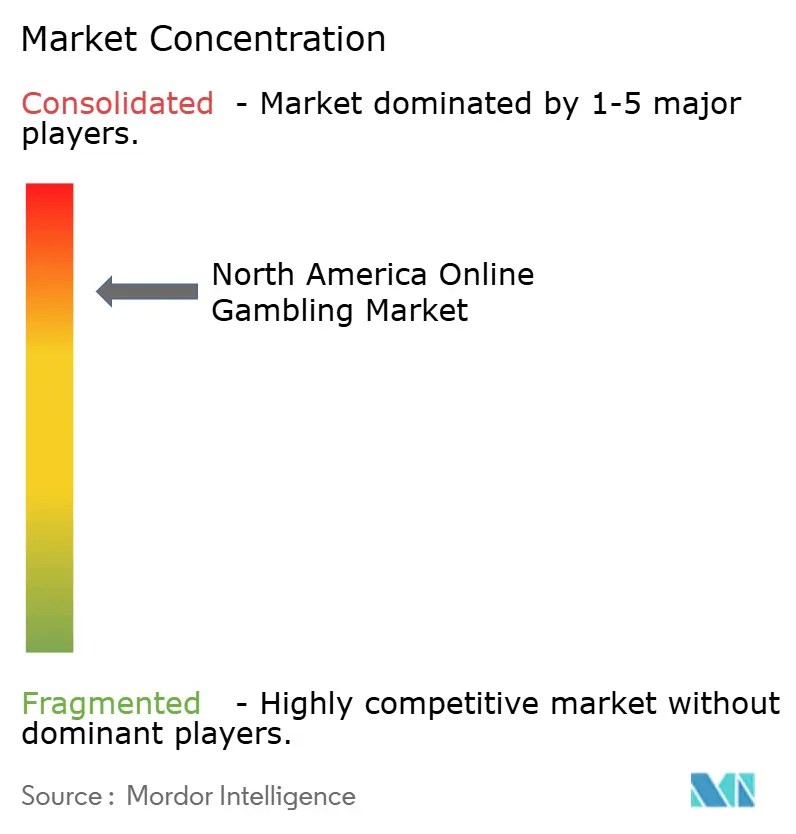

The market is concentrated with Flutter Entertainment, DraftKings, and BetMGM leveraging strategic partnerships, technological edge, and regulatory know-how to dominate the market. This creates formidable barriers for smaller players. The competitive landscape resembles a tight oligopoly, where major players exploit economies of scale, brand clout, and regulatory ties, while smaller entities grapple with high compliance and customer acquisition costs.

Flutter Entertainment's FanDuel boasts a commanding 43.2% share in states where online sports betting is operational and captures 25.7% of active iGaming markets. These figures underscore the benefits of being an early entrant and the impact of consistent marketing, as highlighted by Flutter Entertainment plc. Their strategy revolves around tech integration, content collaborations, and seamless user experiences across platforms, all aimed at boosting customer loyalty and lifetime value.

Playtech's strategic partnerships with industry giants like DraftKings, Rush Street, BetMGM, Bet365, and Penn Entertainment showcase a trend of B2B supplier consolidation. This not only accelerates market entry for these operators but also fosters a dependency on Playtech plc. While there's potential in emerging demographics, cryptocurrency payments, and esports, regulatory challenges and compliance hurdles restrict access. In a notable move, Caesars Entertainment sold the World Series of Poker's intellectual property rights to NSUS Group for USD 500 million. However, Caesars retained operational licenses, highlighting a strategy of asset optimization to boost valuation while ensuring a foothold in the market, as per insights from Caesars Entertainment, Inc.

North America Online Gambling Industry Leaders

Flutter Entertainment / FanDuel

DraftKings Inc.

BetMGM (MGM Resorts + Entain)

Caesars Digital

Bet365

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity is concentrated in newly opened or reforming regulated frameworks, and in the ability to operationalize compliant launches quickly. Alberta's move to a multi-license regulated online gambling model in July 2026, with an initial set of 22 platforms that include DraftKings, FanDuel, and BetMGM, creates a second large Canadian anchor alongside Ontario and widens routes for suppliers and operators to scale within Canada. Content and platform providers are using this opening to expand distribution, including Play'n GO launching its casino portfolio with more than 10 licensed operators in Alberta following the market opening.

In the United States, opportunity increasingly reflects consumer-protection and enforcement-driven market structure as much as new-state sports betting launches. Legislative initiatives such as Pennsylvania's Online Consumer Protection Act introduced in June 2026 (deposit limits and credit card funding bans) and the 2025-2026 wave of explicit bans on sweepstakes-style online casino models across several states shift demand toward compliant product design, payments configuration, and responsible gambling tooling that can be reused across jurisdictions. Multi-jurisdiction standardization also shows up in platform stack choices, such as Playtech confirming in June 2026 that its iPoker platform powers the PokerStars on FanDuel product across Ontario, Michigan, New Jersey, and Pennsylvania, supporting a repeatable operating model for regulated poker and casino expansions where licensing permits.

Recent Industry Developments

- July 2026: DraftKings launched its online sportsbook and casino in Alberta on July 13, aligning with the province-wide regulated market opening. The launch extends DraftKings into a second major Canadian province beyond Ontario, strengthening cross-border operating scale and supplier relationships under a regulated framework.

- June 2026: BetMGM renewed its multi-year partnership with Major League Baseball as an Official Gaming and Sports Betting Partner. The renewal sustains league-linked acquisition channels and content adjacency during peak sports calendars, supporting continuity for branded integrations and promotions in regulated US markets.

- May 2025: BetMGM announced an exclusive partnership with the Las Vegas Aces and the WNBA through 2027, including arena signage, VIP experiences, and development of a WNBA-branded online slot. The tie-up expands operator marketing into womens sports audiences and connects team assets to iGaming content, reinforcing cross-sell between sports betting and casino products.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers money wagered on sports-style betting and casino-style games that are placed and played through the internet using operator websites and apps across North America. The market value is measured as the USD value generated from online gambling activity.

Scope exclusions: offline casino gaming and in-person sports betting at retail locations are excluded, and illegal or unlicensed activity is not counted.

Segmentation Overview

- By Game Type

- Sports Betting

- Football

- Horse Racing

- Tennis

- Other Sports

- Casino

- Live Casino

- Baccarat

- Blackjack

- Poker

- Slots

- Other Casino Games

- Lottery

- Bingo

- Sports Betting

- By Platform

- Desktop

- Mobile and Tablets

- Other Platforms

- By Age Group

- 18–24 Years

- 25–34 Years

- 35–44 Years

- 45–54 Years

- 55+ Years

- By Betting Type

- Pre-Match/Fixed-Odds

- Live/In-Play

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model on market signals that can be checked year after year. We reviewed public regulatory and statistical sources, including state and provincial gaming regulator releases, American Gaming Association dashboards and annual summaries, Statistics Canada tables, and the U.S. Bureau of Economic Analysis and Census Bureau series for income and digital spending context. To keep definitions consistent, we also used public legal and policy trackers that summarize which states and provinces allow iGaming or online sports betting.

We then incorporated supplier and operator disclosure materials, including annual reports, investor presentations, and earnings call notes, to understand shifts in revenue mix and changes in promotional intensity, especially the channel migration toward mobile. Where needed, paid subscriptions for company financials and a paid news and financials service were used to speed up cross-checks of timelines, M&A, and reported KPIs. The sources listed here are illustrative only, and other public documents were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate how reported gaming revenue lines up with observed market behavior across the United States, Canada, Mexico, and the rest of North America. We spoke with a mix of online operators and platform enablers, along with payment, compliance, and marketing-focused stakeholders. This input helped pressure-test assumptions around conversion, promo credits, and the mobile share of play. When a metric looked inconsistent by jurisdiction, follow-up questions were used to clarify whether the difference was driven by timing, reporting definitions, or a one-off event tied to a launch or regulatory change.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 46% | Functional/Unit leaders: 35% | |

| Smaller Players: 20% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs online gambling value using jurisdiction-level reporting and legalization coverage, then translates into a regional total in USD. In practice, we map where online sports betting and online casino are legal, align it with reported gross gaming revenue series where available, and adjust for timing effects such as seasonality around major sports calendars.

To keep the totals realistic, selective bottom-up approximations were used as cross-checks, including sampled operator revenue disclosures, implied active player and ARPU ranges from interviews, and a simple volume and ASP logic for bet activity where regulators publish handle and hold. Key inputs tracked and refreshed include the count of legalized states and provinces, movements in sports betting hold rate, promotional credit intensity (which affects net revenue), the split of mobile versus desktop play, and the pace of iGaming adoption in new jurisdictions. For forecasting, scenario analysis was used around legalization pathways and tax or rule changes, and then a smoothing step was applied so short-term spikes do not distort the longer trend. When a jurisdiction lacked clean reporting, we used proxy ratios from comparable markets and reconciled the implied totals against regional benchmarks from interviews.

Data Validation & Update Cycle

Outputs are checked through triangulation across multiple independent signals, followed by an outlier review before finalization. We compare the implied growth path against legalization timelines, regulator-reported revenue series, and changes in mobile share to ensure the narrative fits the observed numbers. If a state or province shows a sudden jump, the drivers are reviewed, and experts are re-contacted when the variance cannot be explained by known events such as new launches or policy shifts.

Before sign-off, a second analyst reviews key assumptions, unit logic, and currency conversions, which helps reduce avoidable errors. The report is refreshed annually, and interim updates are added when a material event occurs, such as a major legalization decision or a large tax change. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's North America Online Gambling Market Estimate Compared With Other Published Estimates

Published estimates for online gambling in North America can differ substantially, even when they refer to the same overall segment, because scope and value definitions are not always aligned. Differences often come down to whether the metric is gross gaming revenue versus handle, whether promotions are netted out, and how quickly new legalization is assumed to translate into revenue.

The table shows a spread around the 2025 value because some sources count handle-based activity or include offshore and unregulated play, which changes the total quickly. In Mordor Intelligence's model, the value is tied to regulated online gambling activity across the United States, Canada, Mexico, and the rest of North America. The build separates sports betting from casino-style games before consolidating totals into USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 26.26 B (2025) | |

| Industry Newswire A | USD 33.61 B (2024) | Uses a different base year and often reflects a broader activity view that can blend regulated revenue with wider online gambling participation without consistent netting of promotions. |

| Regional Research Outlet B | USD 13.36 B (2023) | Anchors the series on an earlier year when fewer jurisdictions were live, and may apply a narrower coverage of game types or exclude newer iGaming states, which compresses the total. |

Overall, the gap narrows when definitional choices are made explicit. When the scope is tied to regulated revenue lines, aligned to legalization status, and checked against operator disclosures and the dynamics of hold and promotions, the market size becomes easier to track and repeat over time.

Key Questions Answered in the Report

How large is the North America online gambling market in 2026?

It stands at USD 30.27 billion and is projected to more than double by 2031 at a 15.28% CAGR.

Which game type produces the most revenue?

Sports betting leads with 51.62% of 2025 gross receipts, supported by football and expanding statewide legalization.

Which platform attracts the most users?

Mobile and tablet devices account for 72.10% of wagers, driven by convenience and 5G coverage.

Which age group is growing fastest?

The 18–24 demographic shows 16.74% CAGR through 2031 as Gen Z embraces esports and social betting features.

What is the main regulatory hurdle for operators?

Fragmented state and provincial rules, including tax rates ranging from 6.75% to 51%, add compliance complexity and cost.

Page last updated on: