Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

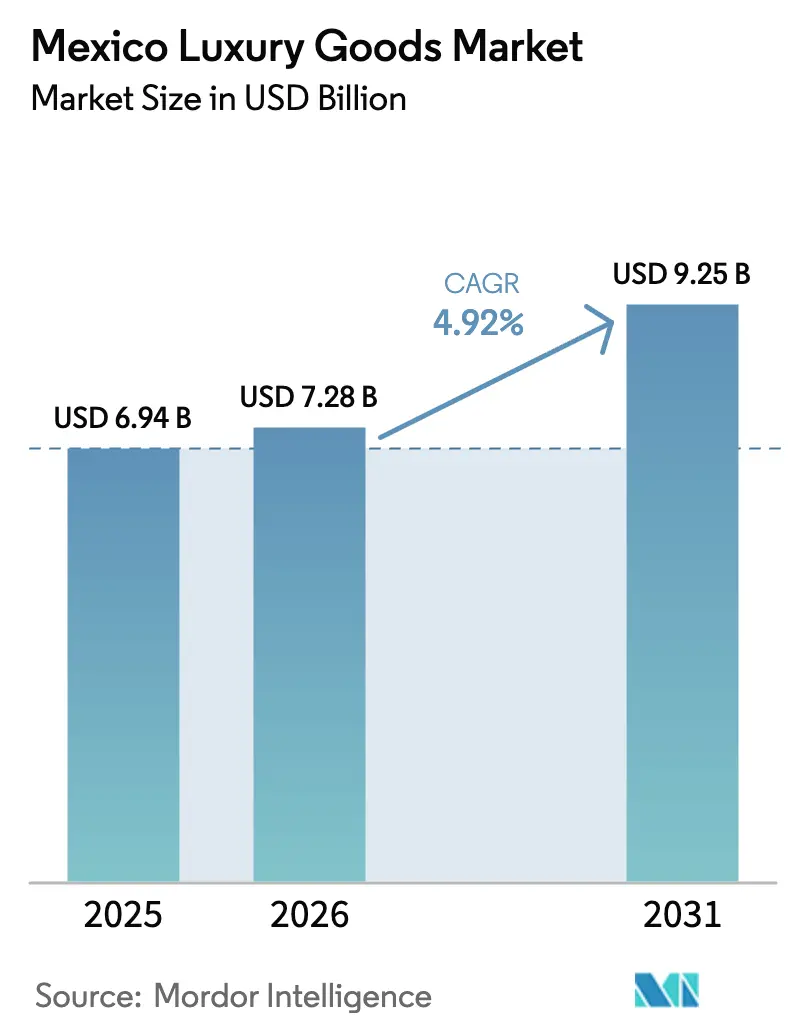

| Base Year Market Size (2025) | USD 6.94 Billion |

| Market Size (2026) | USD 7.28 Billion |

| Market Size (2031) | USD 9.25 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Luxury Goods Market Analysis by Mordor Intelligence

The Mexico luxury goods market size is expected to grow from USD 6.94 billion in 2025 to USD 7.28 billion in 2026 and is forecast to reach USD 9.25 billion by 2031 at 4.92% CAGR over 2026-2031. This growth trajectory is buoyed by a swelling affluent demographic, a robust 8.6% contribution of tourism to the national GDP, and a discernible shift towards valuing experiences over mere ownership. Data from Mexico's Ministry of Tourism highlights that in 2024, the nation rolled out the red carpet for over 45 million international tourists, a commendable 7.4% uptick from the previous year[1]Source: Mexico's Ministry of Tourism, "Number of international tourists in Mexico", www.datatur.sectur.gob.mx. A steady influx of high-net-worth visitors further amplifies the demand, and a notable 50% spike in luxury hotel investments in 2024 underscores the unwavering confidence of global brands. Digital innovations, including augmented reality product trials and AI-driven concierge services, are bridging the divide between the ease of online shopping and the personalized touch of boutique services. The younger demographic is steering this growth, favoring brands that seamlessly meld authentic Mexican craftsmanship with transparent sustainability practices.

Key Report Takeaways

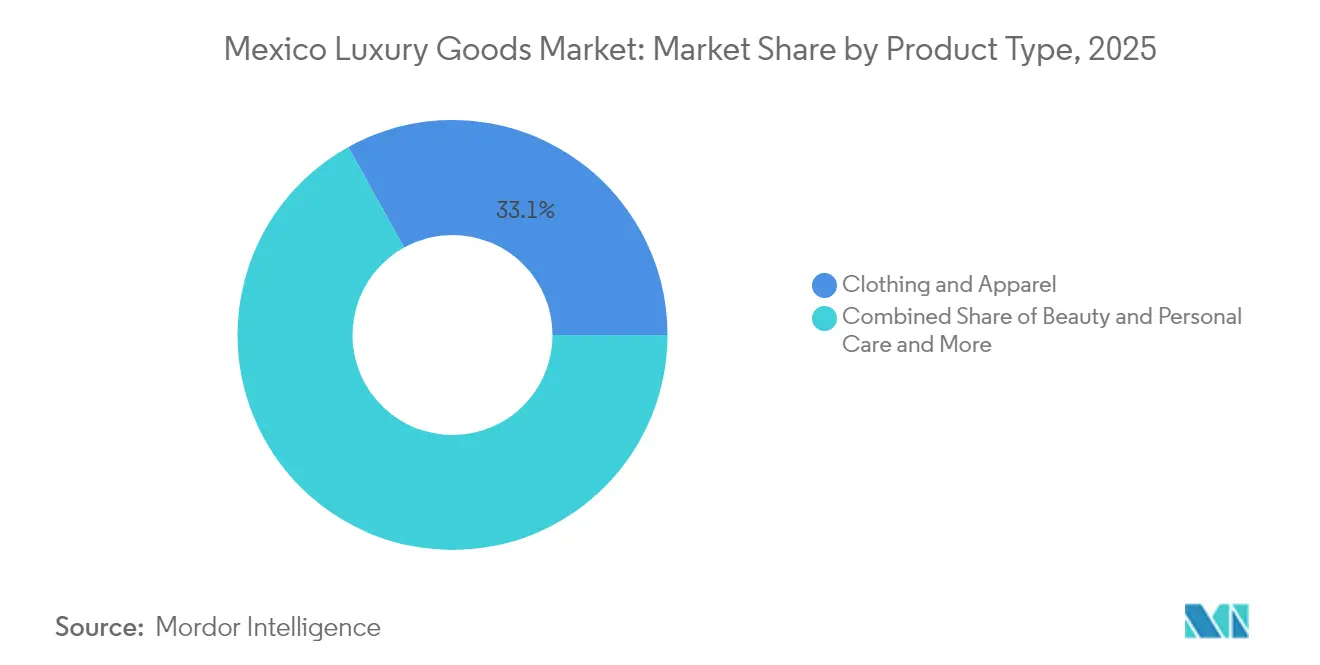

- By product type, Clothing and Apparel held 33.05% of the Mexico luxury goods market share in 2025; Beauty and Personal Care is projected to climb at a 7.54% CAGR through 2031.

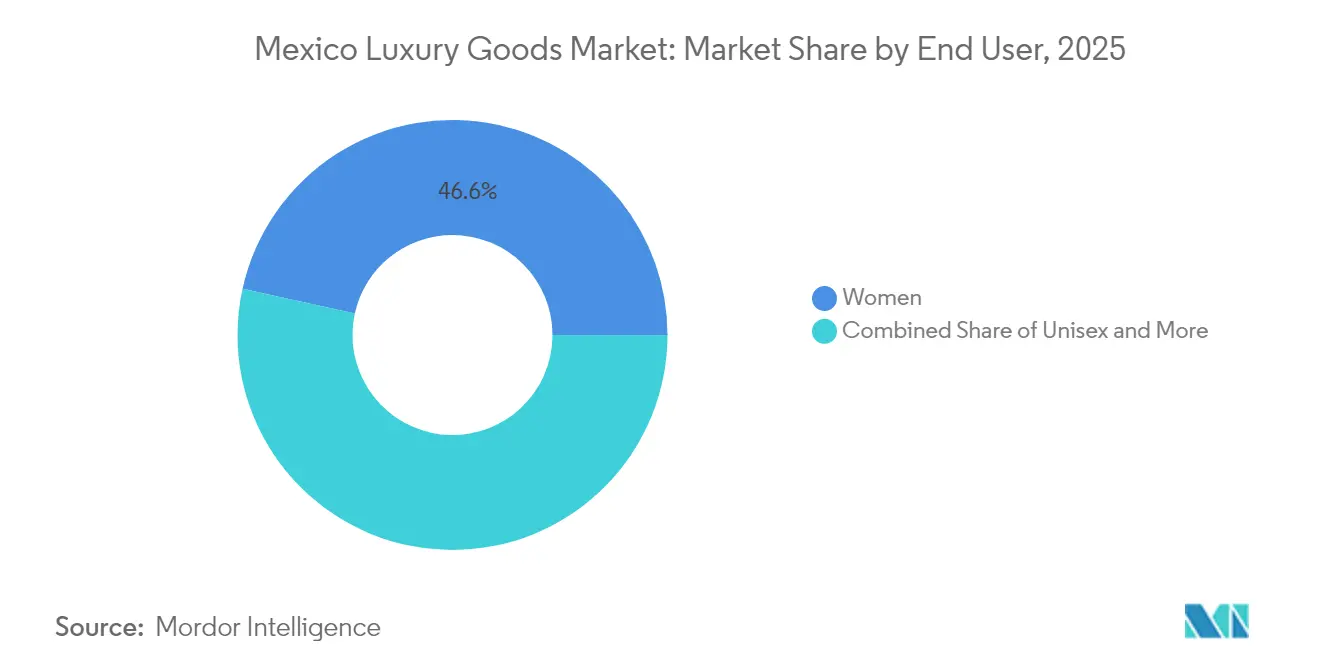

- By end user, Women accounted for 46.55% consumption in 2025, while Unisex products are slated to advance at an 7.78% CAGR to 2031.

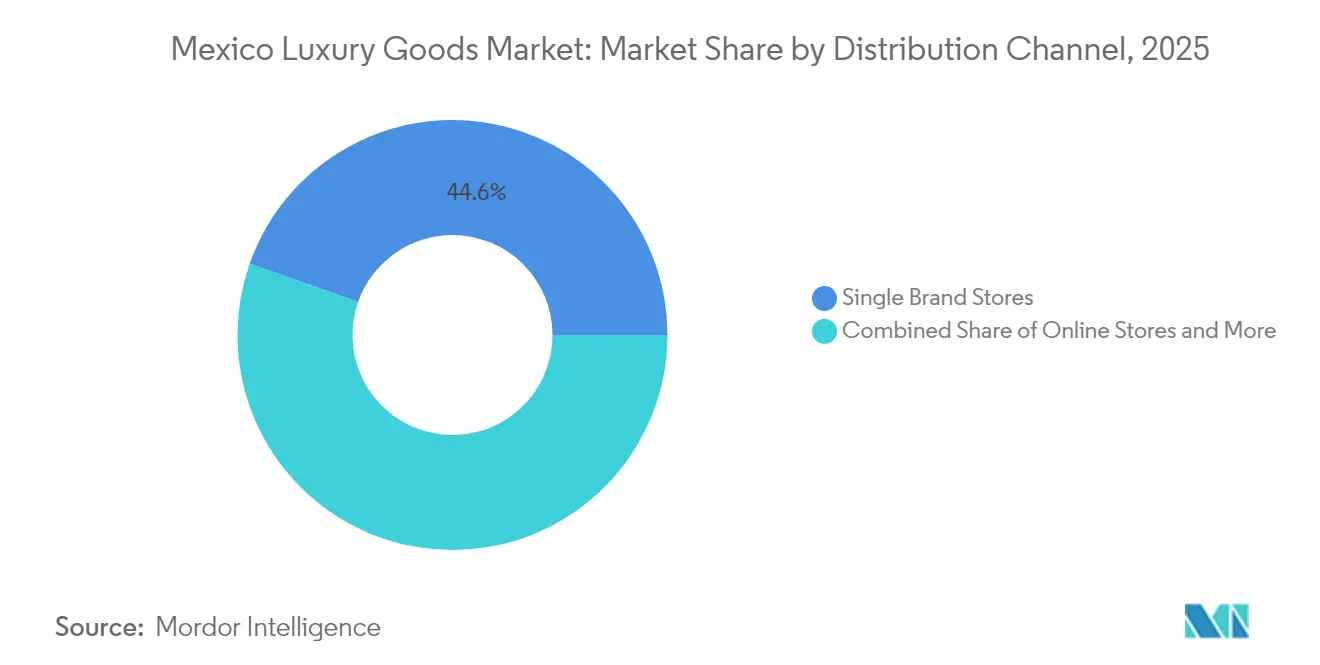

- By distribution channel, Single Brand Stores controlled 44.62% of sales in 2025, yet Online Stores are expected to post a 9.45% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Growth and Spending | +1.2% | National, with concentration in Cancun, Puerto Vallarta, and Los Cabos | Medium term (2-4 years) |

| Localized Brand Storytelling and Heritage Integration | +0.8% | National, particularly in Mexico City and cultural centers | Long term (≥ 4 years) |

| Sophistication in Personalization and Customization | +0.7% | Global, with Mexico City leading adoption | Medium term (2-4 years) |

| Integration of Augmented Reality and Artificial Intelligence | +0.6% | National, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Luxury Wellness and Self-Care Trend | +0.9% | National, with coastal resort areas showing the highest growth | Medium term (2-4 years) |

| Cross-Industry Collaborations and Limited Editions | +0.5% | National, with emphasis on cultural heritage regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Growth and Spending

In 2024, Mexico welcomed 27 million international tourists. Leading the charge in Latin America, the country boasts 248 luxury hotel projects currently under construction, predominantly in the upscale segment. As international visitors indulge during their stays, many transition into repeat customers, often engaging through digital platforms long after their visit. A notable 50% surge in investments within the luxury hotel market this year underscores institutional confidence in Mexico's allure as a premium destination. Notably, properties in Cabo and Puerto Vallarta are now eclipsing performance metrics of established markets like Maui. High-net-worth travelers are increasingly drawn to Mexico, lured by its blend of cultural immersion and top-tier service. The Ritz-Carlton's strategic move to re-enter Cancun in 2027, featuring 131 keys and 126 branded residences, highlights the deepening commitment of luxury brands to Mexico. Resort markets continue to captivate luxury brands eyeing expansion, with tourism not only driving immediate sales but also amplifying brand recognition across borders.

Localized Brand Storytelling and Heritage Integration

Mexican luxury brands are harnessing cultural authenticity as a key differentiator. For instance, Carla Fernández collaborates with indigenous artisans throughout Mexico, aiming to both preserve traditional textile techniques and craft contemporary luxury designs. This strategy deeply resonates with consumers who value meaningful connections to their purchases, transcending mere status signaling. Premium tequila brands, such as Clase Azul, underscore the potency of heritage integration. By emphasizing Mexican cultural traditions and earning the Butterfly Mark for sustainability, they've not only commanded premium pricing but also bolstered global brand recognition. Furthermore, international luxury brands are increasingly collaborating with Mexican artisans. A notable example is Someone Somewhere, whose viral success paved the way for an Adidas contract, spotlighting hand-embroidered jerseys and benefiting over 3,000 artisans. Meanwhile, the Mexican government's crackdown on fast fashion brands misappropriating indigenous designs underscores a regulatory endorsement for genuine cultural collaboration over exploitation. Strategies that authentically integrate heritage and involve local communities in value creation are proving to be both sustainable and lucrative, outpacing superficial cultural nods.

Integration of Augmented Reality and Artificial Intelligence

Luxury brands have poured investments into AI technologies globally in the last three years, primarily targeting personalization features to boost revenues. In Mexico, luxury retailers are harnessing these technologies to meld the ease of digital shopping with the hands-on experience synonymous with luxury. With AI-enhanced customer service and predictive analytics for inventory, brands are not only personalizing experiences but also streamlining operations. To combat the pervasive issue of counterfeit goods, especially in textiles and footwear, Mexican brands are turning to blockchain technology for verifying product authenticity. Meanwhile, virtual reality is revolutionizing luxury retail, offering customers deep dives into brand heritage and craftsmanship, a boon for those prioritizing cultural authenticity. While Mexico's luxury sector adopts technology at a pace akin to global counterparts, there's a distinct focus on solutions that augment human interaction, ensuring the cherished personal touch remains intact.

Luxury Wellness and Self-Care Trend

In Mexico, wellness tourism is on the rise, highlighted by the opening of SHA Wellness Clinic's inaugural international branch in Costa Mujeres. This luxury facility boasts 100 treatment rooms, offering personalized health programs priced at USD 8,250 for a week. The blend of luxury and wellness is not just limited to hospitality; it's making waves in product categories too. Notably, the beauty and personal care segment is leading the charge with a robust 7.80% CAGR growth projected through 2030. Institutional confidence in the wellness-luxury nexus is evident with Banyan Tree Group's foray, unveiling two new Veya wellness resorts, one of which is a USD 28 million investment in Bacalar. Mexican consumers are shifting their perspective, viewing luxury wellness not as a mere indulgence but as a proactive investment in health. This shift is fueling demand for offerings that meld traditional Mexican healing with contemporary luxury. Brands that forge genuine partnerships with traditional healers and wellness experts stand to gain, especially as the market leans towards holistic experiences rooted in indigenous knowledge. Furthermore, sustainability is no longer a luxury add-on; it's a must-have. A striking 50% of travelers express willingness to pay a premium for eco-friendly luxury stays.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Duties and Regulatory Barriers | -1.10% | National, with particular impact on border regions | Short term (≤ 2 years) |

| Prevalence of Counterfeit Goods | -0.80% | National, concentrated in major urban markets | Medium term (2-4 years) |

| Competition from Accessible Luxury | -0.60% | National, with strongest impact in metropolitan areas | Medium term (2-4 years) |

| Environmental and Ethical Concerns | -0.50% | National, with higher impact among younger demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Duties and Regulatory Barriers

Mexico imposes a 16% value-added tax on most luxury goods, leading to cumulative tax burdens exceeding 30% on certain items[3]Source: United States Council for International Business, "Value Added Tax Rates (VAT) By Country", www.uscib.org. Starting August 2025, import taxes on low-value packages surged to 33.5%, hitting e-commerce luxury sales hard. For instance, a USD 500 shipment from non-USMCA countries now faces a tax of USD 167.50, up from the previous USD 95. Beyond taxes, the National Customs Agency has tightened oversight, mandating companies to retain value-added tax and register with federal taxpayer registries. The USTR's 2025 National Trade Estimate report points out challenges for luxury goods importers, such as inconsistent regulatory interpretations at border crossings and short notice for new customs requirements. These hurdles disadvantage international luxury brands on pricing, while potentially giving an edge to domestic producers who sidestep import costs. Smaller luxury brands, lacking customs expertise, find compliance daunting, which could lead to a market consolidation favoring larger players with established import operations.

Prevalence of Counterfeit Goods

Mexico's Federal Law for the Protection of Industrial Property has bolstered the country's intellectual property enforcement framework. Yet, counterfeit luxury goods continue to thrive. The OECD has spotlighted Mexico as a key player in the global trade of counterfeit textiles and footwear. In the heart of Mexico City, the Tepito market stands out as a major hub for these counterfeit luxury goods, jeopardizing brand integrity and eroding consumer trust in genuine products. Enforcement remains a challenge, partly due to Mexico's bustling informal economy. Luxury brands face an added hurdle: they must register with Mexican authorities under the "first-to-file" principle. This requirement opens the door for opportunistic actors to engage in trademark poaching. Furthermore, the National Customs Agency, lacking ex officio powers, can't act against suspected counterfeits without orders from competent authorities. This limitation often results in delays. For effective enforcement, especially in high-traffic ports with limited detection capabilities, collaboration between trademark owners and customs officials is crucial. The digital realm complicates matters further with the surge of online counterfeiting. However, the introduction of notice and takedown mechanisms by the LFPPI offers some relief to rights holders grappling with digital infringements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beauty Drives Digital Transformation

Projected to grow at a 7.54% CAGR through 2031, the Beauty and Personal Care segment is outpacing others, while Clothing and Apparel commands the largest market share at 33.05% in 2025. The beauty segment's surge is a testament to the merging of wellness trends with luxury consumption. This is underscored by Ulta Beauty's strategic move, eyeing a 2025 entry into Mexico's USD 9.46 billion beauty market, collaborating with local partner Axo. Further highlighting the segment's digital evolution, Dior inaugurated an exclusive e-commerce platform in January 2024, catering to the Mexican market. This platform not only showcases makeup, fragrances, and skincare but also offers premium services like hand-wrapping and complimentary shipping on orders exceeding MXN 2,000. In response to the burgeoning demand, Mexico's cosmetic, perfume, and toiletry production surpassed 140 billion Mexican pesos in 2023, as reported by the National Institute of Statistics and Geography (INEGI).

Tourism-driven impulse purchases bolster the Footwear and Eyewear segments, especially in resort locales where global travelers hunt for genuine Mexican luxury. While Leather Goods enjoy consistent growth, buoyed by Mexico's rich craftsmanship legacy, Jewelry grapples with volatility stemming from gold price swings and a shift in consumer focus towards experiential luxury. The rise of smartwatches poses challenges for traditional watches, yet mechanical timepieces continue to captivate classic luxury aficionados. Brands are increasingly blending online and offline strategies, evident from Dior's upcoming men's fashion shop-in-shop at El Palacio de Hierro Polanco, signaling a shift towards digital-first customer engagement.

By End User: Unisex Luxury Gains Momentum

In 2025, women make up 46.55% of luxury consumption, highlighting longstanding gender trends in luxury buying. However, unisex products are outpacing the competition, boasting a robust 7.78% CAGR growth rate projected through 2031. This pivot towards gender-neutral luxury not only mirrors societal shifts but also resonates with younger consumers who favor brands championing inclusivity. Meanwhile, men are carving out a larger slice of the luxury pie, reshaping the narrative of masculine luxury, especially in grooming, wellness, and experiential domains.

The swift rise of the unisex segment underscores luxury brands' strategic shift towards marketing and product designs that transcend traditional gender confines. This movement is especially evident in fragrances, accessories, and wellness products, where benefits are universal, not gendered. The trajectory indicates that luxury brands adeptly catering to unisex markets can siphon off shares from conventional gendered segments, all while resonating with a younger, more varied audience. In Mexico, consumer protection regulations play a pivotal role, ensuring that luxury product marketing claims are credible, a crucial consideration as brands navigate the waters of inclusive positioning.

By Distribution Channel: Digital Acceleration Reshapes Retail

In 2025, Single Brand Stores dominate with a 44.62% market share, curating brand experiences that resonate with luxury consumers. Meanwhile, Online Stores are on a rapid ascent, boasting a 9.45% CAGR projected through 2031. This digital surge underscores a shift in consumer habits and significant brand investments in e-commerce. A case in point: Hermès broadened its online sales reach to Mexico in September 2024. Multi-brand stores, caught between the rise of single-brand retailers and the online boom, must carve out a niche through curated offerings and top-notch service.

Other Distribution Channels, such as duty-free shops and airport retail, are riding the wave of Mexico's tourism surge. Yet, they're grappling with evolving travel habits and a rise in online pre-purchases. This shift underscores luxury consumers' quest for a seamless omnichannel journey, blending digital ease with tangible experiences. Tiffany & Co. is leading the charge, unveiling a flagship in Mexico City that melds luxury retail with an integrated café, signaling a shift towards experiential destinations over mere transactional hubs. As the distribution landscape evolves, luxury brands face the challenge of maintaining exclusive brand control while ensuring market reach, especially as online platforms broaden luxury access, risking a dilution of exclusivity perceptions.

Geography Analysis

In Mexico, luxury spending is heavily concentrated in Mexico City, particularly in the Polanco district, which has seen a surge in boutique openings. While Guadalajara and Monterrey have fewer stores, they boast higher conversion rates, likely due to a lesser emphasis on tourist browsing. Seasonal peaks in luxury spending are evident in resort areas like Cancun, Los Cabos, and Puerto Vallarta, bolstered by hospitality groups showcasing luxury galleries on-site. Meanwhile, the Maya Train project is set to channel affluent tourists further into the Yucatán Peninsula, intensifying competition among beachfront and archaeological sites.

Historically, border states have thrived on cross-border purchases. However, with import duties set to rise in August 2025, some of that demand may shift to domestic boutiques. Cities like Puebla and Mérida are becoming hotspots for accessible luxury, attracting aspirational households eyeing entry-level price points. Notably, Cancun's real estate prices in 2025 suggest a continued wealth effect, influencing discretionary spending. Enhancements in supply-chain infrastructure, such as a last-mile cold-chain for luxury cosmetics and expanded bonded warehouse capacity in Querétaro, are streamlining omnichannel fulfillment across the nation. As a result, the luxury goods market in Mexico is decentralizing, prompting brands to adjust inventories based on regional preferences and climate differences.

Competitive Landscape

The market remains moderately concentrated: the top five global luxury groups together command an estimated 45-50% revenue share. In 2024, LVMH reported a turnover of EUR 84.7 billion and broadened its Fendi and Sephora presence in Mexico City. Kering's revenue dipped by 11%, highlighting execution risks, especially after Gucci's notable 20% sales drop; in response, they've introduced capsule collections co-designed with local Mexican artisans. Meanwhile, Swiss watchmakers, facing competition from smartwatches, are ramping up boutique openings. They're also emphasizing heritage-themed exhibitions to underscore their artisanal expertise.

Domestic luxury brands are moving upscale. Jeweler TANE, for instance, is winning over eco-conscious consumers by pairing three-hour deliveries in Mexico City with a commitment to recycled-silver sourcing. Newer brands are strategically pricing their limited-run pieces: positioned just above accessible ranges but below European price points, they cater to a "new formal" aesthetic, appealing especially to tech professionals. Technology is a key differentiator; one major fashion house, leveraging AI-driven demand forecasting, successfully reduced stock-outs by 15%. Additionally, strategic maneuvers like early trademark registrations, in line with Mexico's first-to-file rules, and adapting to stricter IP enforcement, are crucial in the battle against counterfeits.

Sustainability is emerging as a pivotal focus. Luxury labels that embrace verified carbon-neutral leather or upcycled gemstones are resonating with the values of Generation Z shoppers. Furthermore, corporate initiatives aimed at preserving community crafts not only bolster brand value but also act as a safeguard against potential cultural appropriation criticisms in Mexico's luxury market.

Mexico Luxury Goods Industry Leaders

-

LVMH Moet Hennessey Louis Vuitton

-

Hermès International S.A.

-

Kering S.A.

-

Compagnie Financière Richemont SA

-

Prada S.p.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Louis Vuitton launched a temporary pop-up store inside El Palacio de Hierro, an upscale department store in Mexico City. This pop-up featured a curated selection of luxury accessories, including handbags, shoes, and ready-to-wear pieces from Louis Vuitton’s latest runway collections. This launch allowed Mexican luxury shoppers exclusive access to the brand’s newest offerings in an immersive boutique environment, enhancing Louis Vuitton’s footprint in the country.

- May 2024: Zadig & Voltaire further consolidated its presence in Mexico as it opened in southern Mexico City, building on its 2023 entry. Meanwhile, Alo Yoga, a luxury athleisure brand, operated three stores in Mexico, two in Mexico City and one in Monterrey, catering to Mexico’s affluent consumers seeking premium activewear that blends performance with stylish design.

- July 2024: Retail Fashion Group expanded its luxury fashion presence in Jalisco by launching five distinct high-end brands, Maje, Sandro, Alo Yoga, AllSaints, and Zadig & Voltaire, in standalone stores at the affluent Andares shopping complex in Guadalajara. These brands collectively offer upscale women’s and men’s apparel, footwear, and accessories characterized by contemporary fashion, quality craftsmanship, and trendsetting designs, targeting Mexico’s sophisticated luxury shoppers.

- January 2024: Bottega Veneta debuted its first Mexican store in Cancun, which featured a luxurious 349-square-meter boutique designed by creative director Matthieu Blazy. The store’s Mediterranean-inspired architecture, blending Venetian plaster and teak wood, offers an elevated experience for luxury shoppers. It launched with the Summer 2024 collection, including exclusive handcrafted Sardine bags, marking a significant expansion of upscale fashion retail outside Mexico City.

Mexico Luxury Goods Market Report Scope

Luxury goods refer to high-priced personal accessories which are often handcrafted with painstaking detail and discipline, featuring extraordinary craftsmanship, and are built with the highest quality materials. The Mexico luxury goods market is segmented by type and distribution channel. By type, the market is segmented into clothing and apparel, footwear, bags, jewelry, watches, and other accessories. By distribution channel, the market is segmented into single-brand stores, multi-brand stores, online stores, and other distribution channels. The report offers market size and forecasts for the luxury goods market in value (USD million) for all the above segments.

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Beauty and Personal Care |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Single Brand Stores |

| Multi Brand Stores |

| Online Stores |

| Other Distribution Channels |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Beauty and Personal Care | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Single Brand Stores |

| Multi Brand Stores | |

| Online Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Mexico luxury goods market in 2026?

The Mexico luxury goods market size is USD 7.28 billion in 2026, with a projected 4.92% CAGR over 2026-2031.

Which product category is expanding fastest?

Beauty and Personal Care leads growth at a 7.54% CAGR, propelled by wellness convergence and digital retail.

What share do Single Brand Stores hold?

Single-brand stores account for 44.62% of sales, underscoring the importance of controlled brand environments.

Why are Unisex products gaining traction?

Inclusive design and gender-neutral marketing align with younger consumer values, driving an 7.78% CAGR through 2031.

How do high import duties affect pricing?

Combined VAT and excise taxes can push landed costs above 30%, challenging smaller foreign labels on price competitiveness.

What is the main strategy against counterfeits?

Brands implement blockchain authentication and collaborate closely with customs to protect intellectual property.

Page last updated on: