Men's Underwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.31 Billion |

| Market Size (2031) | USD 13.10 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

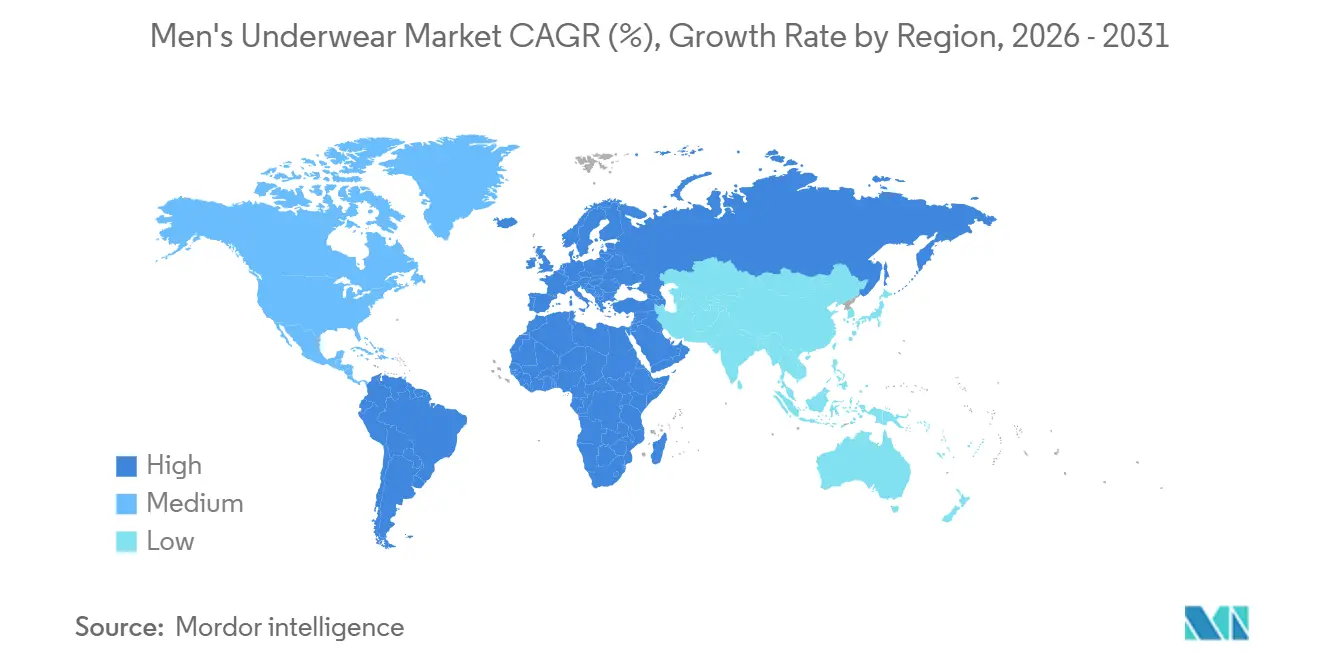

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

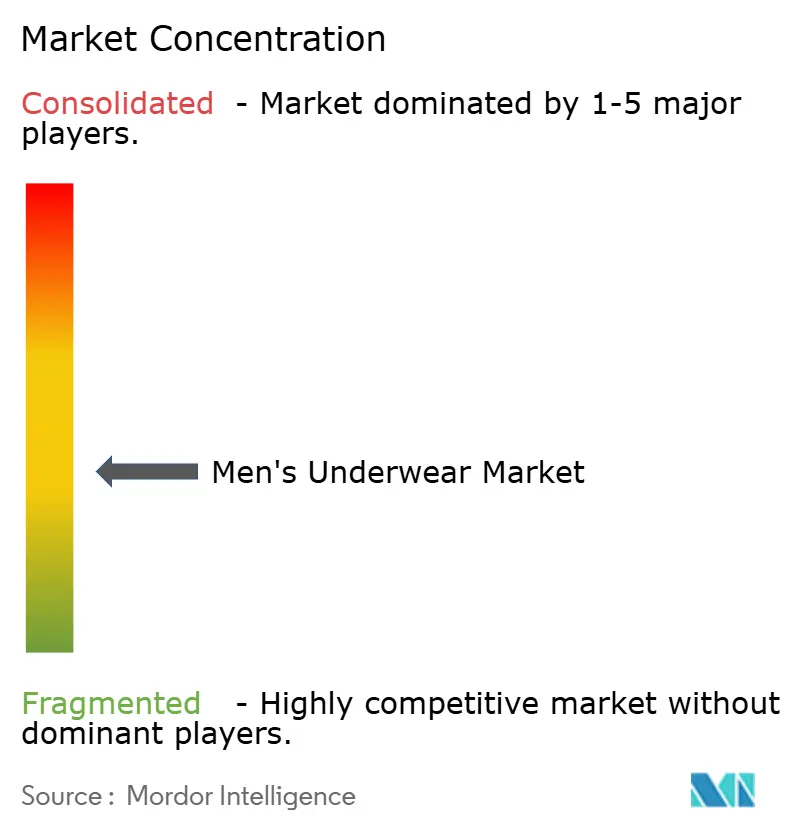

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Men's Underwear Market Analysis by Mordor Intelligence

The men's underwear market size is projected to expand from USD 9.82 billion in 2025 and USD 10.31 billion in 2026 to USD 13.10 billion by 2031, registering a CAGR of 4.92% between 2026 and 2031. This growth trajectory reflects evolving consumer preferences, advancements in fabric technologies, and the increasing adoption of premium and sustainable products. On the demand side, factors such as the rising influence of athleisure trends, growing awareness of personal hygiene, and the shift toward comfort-focused apparel are significantly shaping the market. Gen Z and millennial consumers, in particular, are driving demand for hybrid designs that combine athletic support with everyday comfort. On the supply side, the market faces challenges such as fluctuating raw material costs, tightening microfiber regulations, and stringent sustainability mandates. Key regulations, including the European Union's Ecodesign for Sustainable Products Regulation and the 2026 ban on destroying unsold textiles, are pushing manufacturers to adopt eco-friendly practices and to innovate with sustainable materials [1]Source: European Commission, "New EU Rules to Stop Destruction of Unsold Clothes and Shoes," environment.ec.europa.eu. Consumers are increasingly prioritizing features such as antimicrobial properties, moisture-wicking fabrics, and durability, which are becoming critical differentiators in the market.

Key Report Takeaways

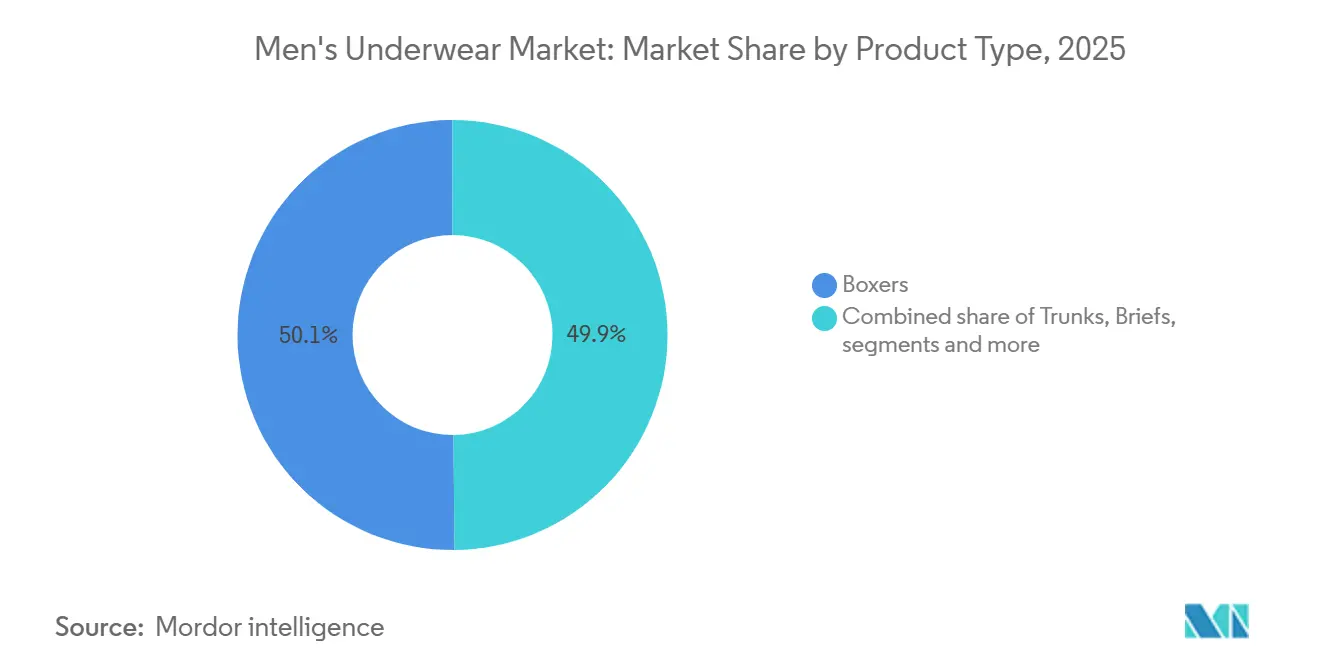

- By product type, boxers led with 50.15% of the men's underwear market share in 2025, while trunks are forecast to expand at a 5.02% CAGR through 2031.

- By fabric type, cotton accounted for 63.78% of the men's underwear market size in 2025, whereas synthetic blends are projected to grow at a 5.43% CAGR through 2031.

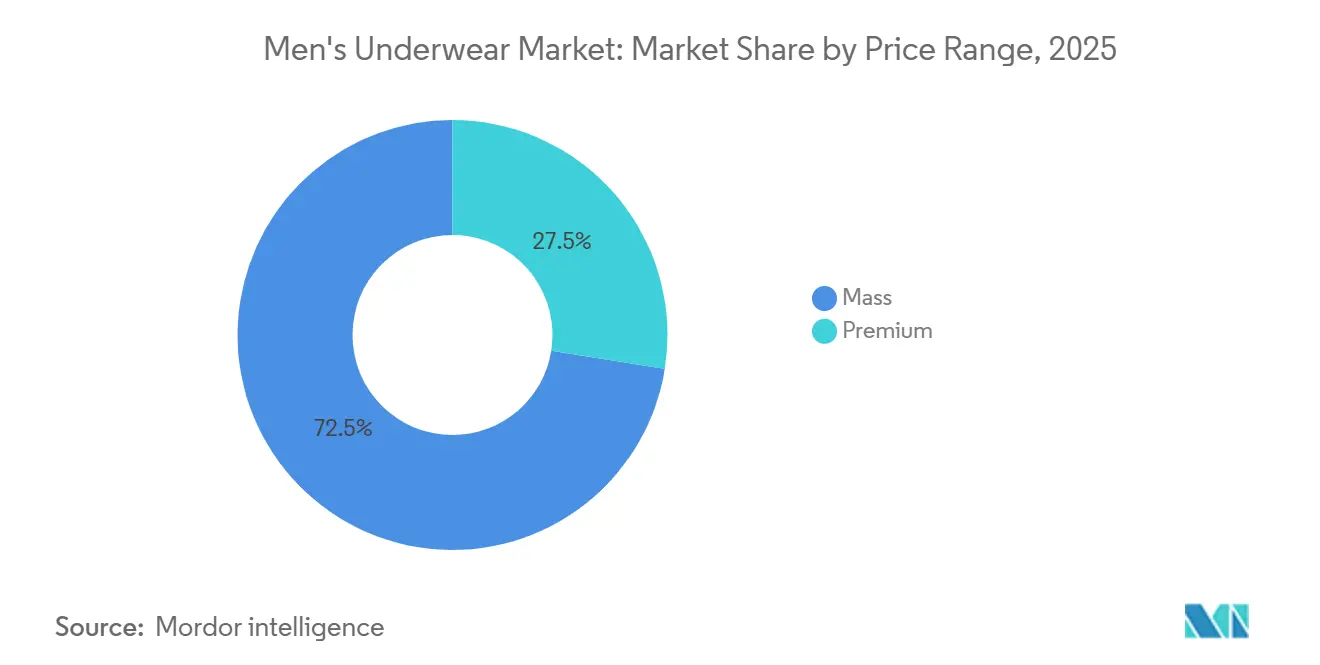

- By price range, mass-market lines held 72.49% share of the men's underwear market in 2025, yet the premium tier is advancing at a 6.34% CAGR from 2026 to 2031.

- By distribution channel, specialty stores commanded 52.67% revenue share in 2025, but online retail is advancing at a 5.95% CAGR through 2031.

- By geography, Asia-Pacific captured 53.85% of global sales in 2025, while Europe is slated to post the fastest regional CAGR at 5.18% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Men's Underwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and functional performance demand | +0.8% | Global, with premium concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Acceleration of e-commerce and D2C channel expansion | +0.9% | Global, led by North America and Europe; rapid adoption in Asia-Pacific tier-1 cities | Short term (≤ 2 years) |

| Rising adoption of athleisure-inspired innerwear | +0.6% | North America, Europe, Australia; emerging in urban India and China | Medium term (2-4 years) |

| Brand-led differentiation through celebrity endorsements and influencer marketing | +0.5% | North America and Europe core; spillover to Latin America and Asia-Pacific youth segments | Short term (≤ 2 years) |

| Innovation in antimicrobial and sustainable fabrics | +0.7% | Europe (regulatory push), North America (consumer preference), Asia-Pacific (manufacturing innovation) | Long term (≥ 4 years) |

| Emergence of subscription-based replenishment models | +0.4% | North America and Europe; pilot expansions in Australia and select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and functional performance demand

Consumers are increasingly shifting toward engineered fabrics that offer moisture management, odor control, and enhanced durability, driving higher average selling prices and improved margin profiles for manufacturers. Materials such as Tactel, Micro Modal, and bamboo-derived viscose have become standard in the premium segment, reflecting the growing demand for performance-oriented products, while SAXX’s BallPark Pouch illustrates ergonomic innovation. Academic trials confirm that advanced technologies, including silver-decorated boron nitride nanoparticles and plant-based antimicrobial agents like eucalyptus oil and hop extract, effectively inhibit bacterial growth on textile surfaces. These innovations not only extend wear cycles but also reduce the frequency of laundry, aligning with consumer preferences for convenience and sustainability. This trend is particularly prominent in North America and Western Europe, where consumers are willing to pay premiums for enhanced performance features. Additionally, urban markets in the Asia-Pacific region are witnessing similar growth as rising middle-class incomes and expanding brand awareness drive demand for premium and functional fabrics.

Acceleration of e-commerce and D2C channel expansion

Digital channels are reshaping distribution economics in the men's underwear market by eliminating intermediary markups and enabling hyper-targeted customer acquisition. Direct-to-consumer platforms such as Mack Weldon and MeUndies have gained significant traction by offering subscription models that ensure recurring revenue and customer loyalty. The growing preference for premium and performance-based underwear, featuring moisture-wicking, odor control, and enhanced comfort, is further driving demand in this segment. Social commerce, fueled by platforms like Instagram and TikTok, is accelerating e-commerce conversions by seamlessly integrating product discovery and purchase. Investors are increasingly favoring omnichannel strategies, highlighting confidence in brands that combine digital-first marketing with selective physical retail presence. Meanwhile, the rapid growth in smartphone penetration in markets such as India, where 85.5% of households owned at least one smartphone in 2025, has significantly enhanced access to digital commerce, according to the Ministry of Statistics & Programme Implementation [2]Source: Press Information Bureau of India, "Results of Comprehensive Modular Survey: Telecom, 2025," pib.gov.in. This advancement enables premium men’s underwear brands to target urban consumers in tier-1 cities like Shanghai, Mumbai, and Seoul. Furthermore, the development of mature mobile payment systems and improved last-mile logistics has streamlined the purchasing process for higher-value innerwear, thereby driving premiumization trends. These structural factors are propelling the global men’s underwear market toward branded, high-quality segments, with the Asia-Pacific region emerging as a critical growth driver.

Rising adoption of athleisure-inspired innerwear

The growing emphasis on versatility and technical innovation is transforming the landscape of performance sportswear and everyday innerwear. Consumers are increasingly seeking fabrics that combine functionality with style, blurring the lines between activewear and casual attire. For instance, Bike Athletic focuses on athleisure-inspired men's innerwear by integrating performance fabrics, such as moisture-wicking modal and stretch blends, with functionality that caters to both gym use and everyday wear. The company positions products like active briefs and jock styles as practical sports gear and versatile daily essentials. Polyamide-elastane blends stand out for offering 10 times the abrasion resistance of cotton, along with superior moisture-wicking, stretch, and shape-retention properties. These features make them ideal for hybrid use cases, seamlessly transitioning from gym sessions to office environments. Additionally, seamless construction and ergonomic paneling reduce chafing during high-intensity activities, enhancing comfort and performance. Millennials and Gen Z consumers, who prioritize both functionality and aesthetics, are driving this trend. While North America, Europe, and Australia remain at the forefront of adoption, urban markets in India and China are rapidly emerging as growth hubs, driven by rising fitness culture, higher disposable incomes, and greater awareness of the benefits of technical fabrics.

Innovation in antimicrobial and sustainable fabrics

The global shift towards sustainability is reshaping material innovation, driven by regulatory mandates and evolving consumer preferences. The European Union's Ecodesign for Sustainable Products Regulation, which requires Digital Product Passports, is pushing brands to adopt traceable and recyclable inputs [3]Source: European Union, "EU's Digital Product Passport: Advancing Transparency and Sustainability," data.europa.eu. Bamboo-derived viscose and lyocell, processed through closed-loop systems, offer biodegradability and a lower water footprint compared to conventional cotton. While consumer preferences guide North America, Asia-Pacific manufacturers are innovating to meet export demand. However, compliance costs and supply chain complexities remain significant challenges for smaller players. Companies pioneering silver-treated fabrics, recycled materials, and biodegradable options are strategically positioning themselves to address tightening regulations and evolving consumer preferences for environmental sustainability. The increasing focus on sustainability and functionality is driving investments in advanced manufacturing processes and material science research, further accelerating the adoption of antimicrobial fabrics. Although consumers often prefer natural fibers, this trend benefits the growth of synthetic fabrics, which can more readily incorporate antimicrobial properties compared to traditional cotton.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive price competition impacting profitability | -0.6% | Global, most acute in mass-market segments across Asia-Pacific | Short term (≤ 2 years) |

| Volatility in raw material costs | -0.5% | Global, with polyester-dependent regions (Asia-Pacific manufacturing hubs) most exposed | Short term (≤ 2 years) |

| Regulatory pressure on microfiber and textile sustainability | -0.3% | Europe (strictest enforcement), North America, spillover to export-oriented Asia-Pacific | Medium term (2-4 years) |

| Persistent cultural sensitivity toward body-fit styles in certain regions | -0.2% | Middle East, South Asia, select Southeast Asian markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive price competition impacting profitability

The mass-market segment is facing significant challenges amid mounting margin pressures from retailers' private-label products, which are increasingly undercutting branded alternatives. This trend is particularly evident in North America and Europe, where heightened consumer price sensitivity forces established players to adopt aggressive pricing strategies to maintain market share. In Asia-Pacific and Latin America, the situation is further aggravated by the proliferation of low-cost offerings from local manufacturers, which dilute brand premiums and push incumbents toward steep discounting. The rapid expansion of e-commerce, including ultra-low-cost platforms (e.g., Temu, Shein), is disrupting traditional pricing models globally, forcing local manufacturers to rely on heavy discounting and enabling smaller players to gain traction. As a result, companies are exploring cost optimization strategies, product differentiation, and value-added offerings to sustain profitability in this highly competitive landscape.

Volatility in raw material costs

The global textile industry continues to face significant challenges due to fluctuating raw material prices and supply chain disruptions. Polyester and elastane prices, closely tied to crude oil prices, have surged as Brent crude prices have risen. This has driven up the costs of purified terephthalic acid and monoethylene glycol feedstocks, compressing margins for vertically integrated manufacturers. In contrast, the cotton market has experienced opposing dynamics. The Cotton Association of India in 2025 highlighted that India's cotton acreage has declined by 30% over the past three years [4]Source: Cotton Association of India, "North India Cotton 2025: A Season of Hopes Withering Without Water and Concerns of Worms", caionline.in. Global yarn prices have softened amid reduced demand from China. This divergence has created cross-fiber arbitrage opportunities, complicating manufacturers' procurement strategies. Asia-Pacific manufacturing hubs, including Bangladesh, Vietnam, and Indonesia, are particularly exposed to these challenges. These regions rely heavily on imported feedstocks and operate on thin margins, amplifying the impact of fluctuations in input costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Trunks Capture Younger Demographics

Boxers commanded 50.15% of global revenue in 2025, reflecting entrenched consumer habits among older cohorts who prioritize loose fits and breathable cotton construction. Despite the emergence of new trends, boxers continue to anchor the men’s underwear category, catering to a diverse range of consumer preferences. Trunks, however, are expanding at a 5.02% CAGR through 2031, driven by millennials and Gen Z consumers who prefer hybrid designs that offer athletic support and everyday versatility. Products such as SAXX’s BallPark Pouch and Under Armour’s Boxerjock Ballbag typify comfort-plus-performance propositions. Features like seamless construction and ergonomic paneling, which minimize chafing, are particularly popular in regions such as North America, Europe, and Australia, where fitness culture is prominent.

Briefs continue to maintain a loyal customer base, especially in professional and formal-wear settings where slim-fit trousers require low-profile waistbands. However, their market share is gradually declining as the rise of athleisure blurs traditional dress codes. The "Others" category, which includes boxer briefs, jockstraps, and specialty designs, caters to niche segments such as athletic and medical applications. Growth in this category is fueled by performance innovations and inclusive sizing initiatives that address the needs of previously underserved body types.

By Fabric Type: Synthetics Gain on Durability

Cotton maintained its dominance in the men’s underwear market, capturing 63.78% of market share in 2025, anchored by its breathability, hypoallergenic properties, and cultural familiarity. This enduring leadership stems from cotton's heritage appeal. Cotton's soft touch and breathability have anchored its popularity, especially in warmer climates where moisture-wicking is less crucial. Additionally, the availability of organic and sustainably sourced cotton has further strengthened its position, appealing to environmentally conscious consumers. Cotton remains the go-to fabric for comfort enthusiasts, solidifying its foundational role in the men's underwear sector. Furthermore, the affordability and widespread availability of cotton products have made them accessible to a broad consumer base, ensuring their continued relevance in both developed and emerging markets.

Synthetic fabrics are set for significant growth, with projections of a 5.43% CAGR through 2031, driven by performance attributes and cost advantages. Polyamide-elastane composites deliver 10-fold abrasion resistance compared to cotton, alongside superior moisture-wicking and shape retention, making them ideal for hybrid athletic-casual use cases. Common blends such as 90% polyamide, 10% elastane balance stretch and recovery, while antimicrobial finishes extend wear cycles and reduce laundry frequency. The "Others" category encompasses bamboo-derived viscose, modal, and lyocell, which offer biodegradability and lower water footprints than conventional cotton, yet remain premium-priced due to limited production scale. Brands are hedging by diversifying fiber portfolios and investing in closed-loop recycling infrastructure to mitigate input volatility.

By Price Range: Premium Tier Expands on Celebrity Collaborations

Mass-market offerings accounted for 72.49% of the 2025 market, reflecting price sensitivity across Asia-Pacific, Latin America, and value-conscious North American and European consumers. The rise of social media-driven "dupe" culture, which promotes affordable alternatives to premium products, has further accelerated the adoption of mass-market options. Younger generations, particularly Gen Z, are increasingly drawn to these affordable yet trendy offerings, driven by their focus on value and accessibility.

The premium segment, however, is surging at 6.34% CAGR through 2031, fueled by celebrity endorsements that generate outsized media value and accelerate brand recall. Premium brands command price premiums by integrating proprietary technologies, including SAXX's BallPark Pouch, Under Armour's anti-odor treatments, and sustainable materials such as Under Armour's UNLESS regenerative cotton to reduce soil degradation and water use. The tier is concentrated in North America, Western Europe, and urban Asia-Pacific, where rising disposable incomes and brand consciousness support higher price points, yet mass-market players face relentless margin compression due to private-label offerings.

By Distribution Channel: Online Retail Accelerates

Specialty stores held 52.67% of the distribution share in 2025, leveraging tactile trial and personalized service to retain customers who value fit assurance and immediate gratification. These stores play a critical role in the underwear market, particularly for premium and niche products, as they allow consumers to experience the quality, fit, and comfort of the products firsthand. Online retail stores are expanding at a 5.95% CAGR through 2031, driven by the growing influence of social commerce channels and direct-to-consumer platforms that eliminate intermediary markups. The convenience of online shopping, coupled with the availability of detailed product descriptions, size guides, and customer reviews, has significantly boosted the adoption of e-commerce in the underwear market. The shift is most advanced in North America and Europe, yet Asia-Pacific tier-1 cities are witnessing rapid adoption as mobile payment infrastructure matures and logistics networks densify.

Supermarkets and hypermarkets cater to price-sensitive consumers seeking convenience and bundled promotions. However, their share is gradually declining as e-commerce platforms offer broader assortments, competitive pricing, and personalized recommendations. In the underwear market, these retail channels primarily focus on mass-market products, often featuring private-label offerings that appeal to budget-conscious shoppers. The "Other Channels," comprising department stores, airport retail, and pop-up shops, cater to impulse purchases and gift-giving occasions. While these channels are shrinking due to the rationalization of physical retail space, they remain relevant for premium and luxury underwear brands that rely on curated displays and exclusive shopping experiences to attract high-end consumers.

Geography Analysis

Asia-Pacific accounted for 53.85% of global revenue in 2025, driven by its large population, rising disposable incomes, and the expanding middle class in countries like India, China, and Southeast Asia. Despite a decline in India's cotton output in 2024-2025 due to erratic monsoons, global yarn prices trended lower as Chinese demand softened. This created cross-fiber arbitrage opportunities, complicating procurement strategies. Urban centers in Asia-Pacific are becoming key markets for premium and athleisure-inspired innerwear, fueled by the growing fitness culture and consumer preference for functional benefits over traditional loose-fit boxers. Indonesia, Thailand, and Singapore are witnessing similar trends, with Gen Z and millennial consumers driving demand for moisture-wicking synthetics and seamless construction. Meanwhile, Japan and Australia, as mature markets, exhibit strong brand loyalty, but sustainability-focused messaging is creating opportunities for eco-certified brands.

Europe is projected to grow at a CAGR of 5.18% through 2031, the fastest among all regions, driven by stringent sustainability regulations and the ban on destroying unsold textiles. Germany, the United Kingdom, France, and Italy are leading the premiumization trend, with consumers willing to pay a premium for performance fabrics and traceable supply chains. For instance, PVH Corp transitioned Calvin Klein men's underwear packaging from plastic to paper globally. Countries like Spain, the Netherlands, Poland, Belgium, and Sweden are following similar trends, with specialty stores and online retail channels gaining market share from hypermarkets. However, compliance costs are disproportionately impacting smaller players, accelerating market consolidation.

North America, comprising the United States, Canada, and Mexico, remains a high-value market where celebrity endorsements and direct-to-consumer models are thriving. In South America, led by Brazil, Argentina, Colombia, Chile, and Peru, premiumization is in its early stages as urban middle classes expand. However, intense price competition and cultural preferences for looser fits remain challenges. In the Middle East and Africa, including South Africa, Saudi Arabia, the United Arab Emirates, Nigeria, Egypt, Morocco, and Turkey, cultural sensitivities toward body-fit styles limit the penetration of athleisure-inspired trunks and performance briefs. Nevertheless, urban Gen Z consumers in these regions are showing greater openness to unisex and inclusive designs.

Competitive Landscape

The men's underwear market is moderately fragmented, with established apparel conglomerates such as PVH Corp, Gildan, and Fruit of the Loom competing against digitally native players such as SAXX, Mack Weldon, and MeUndies. Gildan's acquisition of HanesBrands in December 2025 for USD 2.2 billion highlights the consolidation pressure within the mass-market segment. While incumbents leverage vertical integration and scale economies to maintain market share, agile entrants capitalize on direct-to-consumer channels and subscription models to bypass intermediaries and secure recurring revenue streams.

Strategic shifts and innovation are shaping the competitive landscape. SAXX's Spring 2026 partnership with actor Antoni Porowski and its December 2025 collaboration with creative agency WITHIN reflect a move toward lifestyle branding. Similarly, Under Armour's December 2025 launch of the Boxerjock Ballbag integrates anti-odor treatments and contoured front panels, catering to both athletic and casual wear needs. Growth opportunities are emerging in areas such as sustainable materials and inclusive sizing. Under Armour's UNLESS regenerative cotton collaborations, introduced in September and December 2025, aim to address soil degradation and water usage concerns, aligning with regulatory and consumer demands for traceable and recyclable inputs.

Technological advancements are reshaping the market, with innovations such as 3D body scanning for custom fits, antimicrobial finishes to extend wear cycles, and blockchain-enabled Digital Product Passports to meet Ecodesign for Sustainable Products Regulation requirements. Emerging disruptors like ALPHX and Bolas differentiate themselves through fit-focused positioning and sustainable direct-to-consumer models. However, these players often lack the capital to scale manufacturing or compete on price with vertically integrated incumbents, resulting in a bifurcated market landscape where scale and agility coexist with challenges.

Men's Underwear Industry Leaders

-

PVH Corp (Calvin Klein, Tommy Hilfiger)

-

Jockey International

-

Gildan Activewear Inc.

-

H&M Group

-

Berkshire Hathaway (Fruit of the Loom)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Patrick Mouratoglou launched his first underwear collection in 2026, featuring a set of three boxers in classic colors: black, white, and grey. Designed for all-day wear, these boxers offered an optimal combination of softness, support, and breathability.

- December 2025: Gildan Activewear completed its USD 2.2 billion acquisition of HanesBrands, raising the annual synergy target from USD 200 million to USD 250 million through procurement consolidation and manufacturing footprint rationalization.

- December 2025: Under Armour launched the Boxerjock Ballbag, integrating anti-odor treatment with a contoured front panel designed for athletic and casual wear. The product exemplifies the athleisure crossover trend, blending performance fabrics with everyday versatility to capture younger demographics.

- October 2025: Pump Club, India's first premium men's underwear brand, recognized for its bold, colorful, and sporty designs, announced its official launch. The brand targeted the modern man, with a particular focus on youth and Gen Z consumers. Pump Club products became available for purchase on the brand's official website, www.pumpclub.in, as well as on leading e-commerce platforms such as Myntra and Amazon.

Global Men's Underwear Market Report Scope

The men's underwear market is segmented by product type, fabric type, price range, distribution channel, and geography. Based on product type, the market is segmented into boxers, briefs, trunks, and other product types. By fabric type, the market is segmented into cotton, synthetic, and other fabric type. By price range, the market is segmented into mass and premium. By distribution channels, the market has been segmented into supermarket/hypermarket, specialty stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Boxers |

| Briefs |

| Trunks |

| Others |

| Cotton |

| Synthetic |

| Others |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Boxers | |

| Briefs | ||

| Trunks | ||

| Others | ||

| By Fabric Type | Cotton | |

| Synthetic | ||

| Others | ||

| By Price Range | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global revenue be for men’s underwear by 2031?

It is projected to reach USD 13.10 billion, reflecting a 4.92% CAGR over 2026-2031.

Which region is expected to post the fastest growth rate?

Europe is forecast to grow at 5.18% CAGR as strict sustainability policies drive premium spending.

Which product format is gaining traction among Gen Z buyers?

Trunks, favored for hybrid athletic-casual appeal, are forecast to expand at a 5.02% CAGR.

How big is online retail within the market?

Online channels are expanding at 5.95% CAGR, making them the quickest-rising distribution route.

Page last updated on: