Men's Personal Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

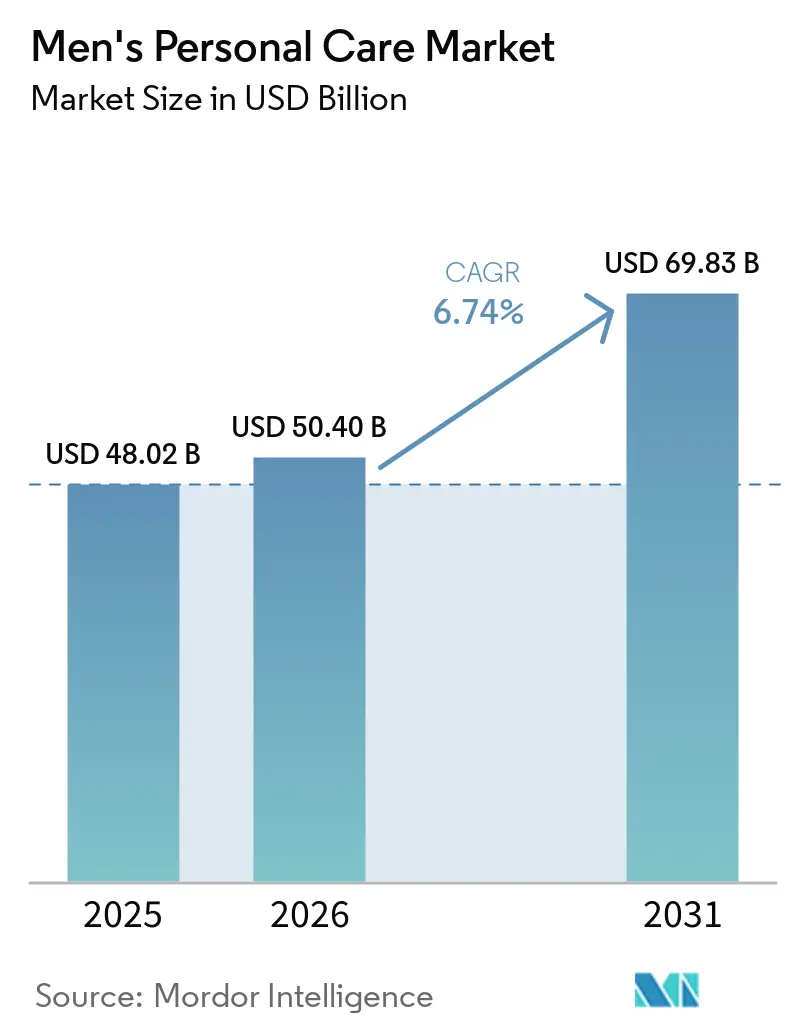

| Market Size (2026) | USD 50.40 Billion |

| Market Size (2031) | USD 69.83 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Men's Personal Care Market Analysis by Mordor Intelligence

The men's personal care market size is projected to expand from USD 48.02 billion in 2025 and USD 50.40 billion in 2026 to USD 69.83 billion by 2031, registering a 6.74% CAGR between 2026 and 2031. Accelerating workplace return-to-office programs have revived demand for premium deodorants and facial care, while e-commerce lowers adoption barriers in price-sensitive regions and broadens access to niche brands that once relied on specialty retail. Rapid innovation in multifunctional, natural-ingredient formulations is simplifying grooming routines for time-pressed consumers and widening the men’s personal care market opportunity across income tiers. However, tighter regulation of endocrine-disrupting fragrance chemicals and the growth of refill models are compressing launch timelines and forcing legacy brands to overhaul packaging lines, thereby reshaping cost structures throughout the men's personal care industry.

Key Report Takeaways

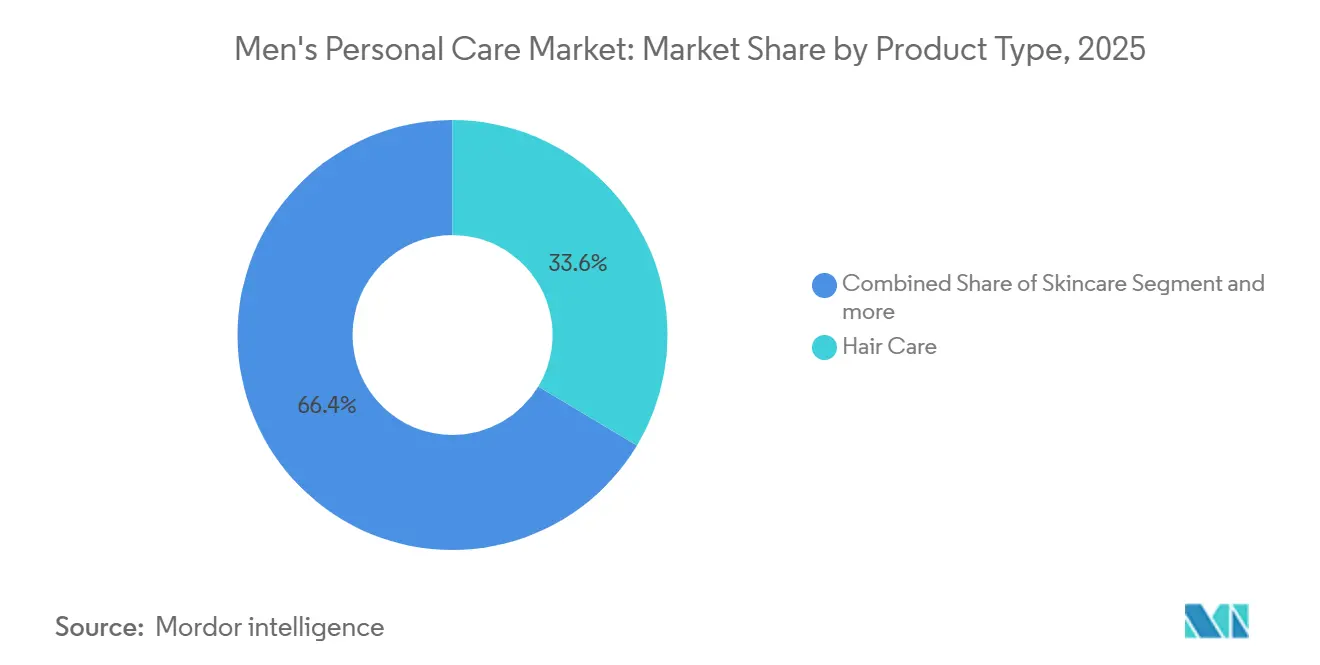

- By product type, Hair Care Products held 33.59% of the men’s personal care market share in 2025, while Deodorants and Fragrances are projected to expand at a 7.08% CAGR through 2031.

- By ingredient type, Conventional/Synthetic formulations accounted for 56.69% of the men’s personal care market share in 2025, whereas Natural and Organic products are forecast to grow at a 7.67% CAGR during the same period.

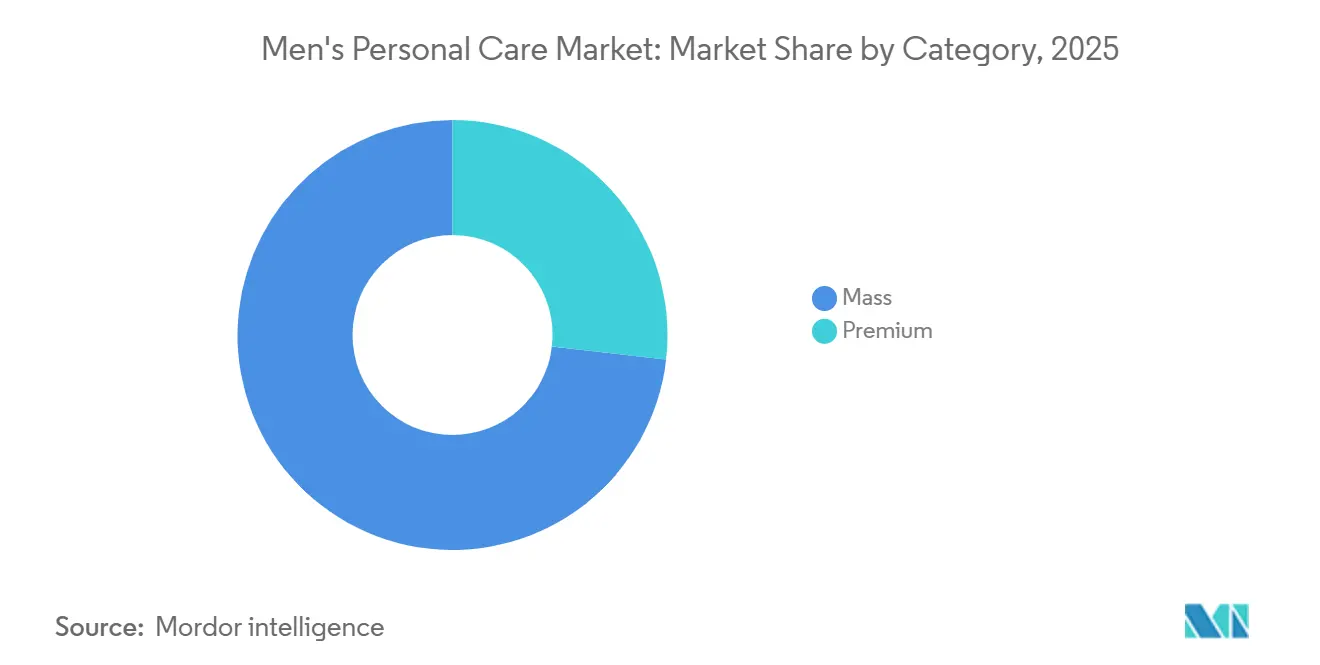

- By category, Mass products captured 73.18% of the men’s personal care market share in 2025, while the Premium segment is expected to advance at a 7.07% CAGR to 2031.

- By distribution channel, Supermarkets and Hypermarkets led with 35.72% of the men’s personal care market size in 2025, whereas Online Retail Stores are set to rise at a 7.81% CAGR through 2031.

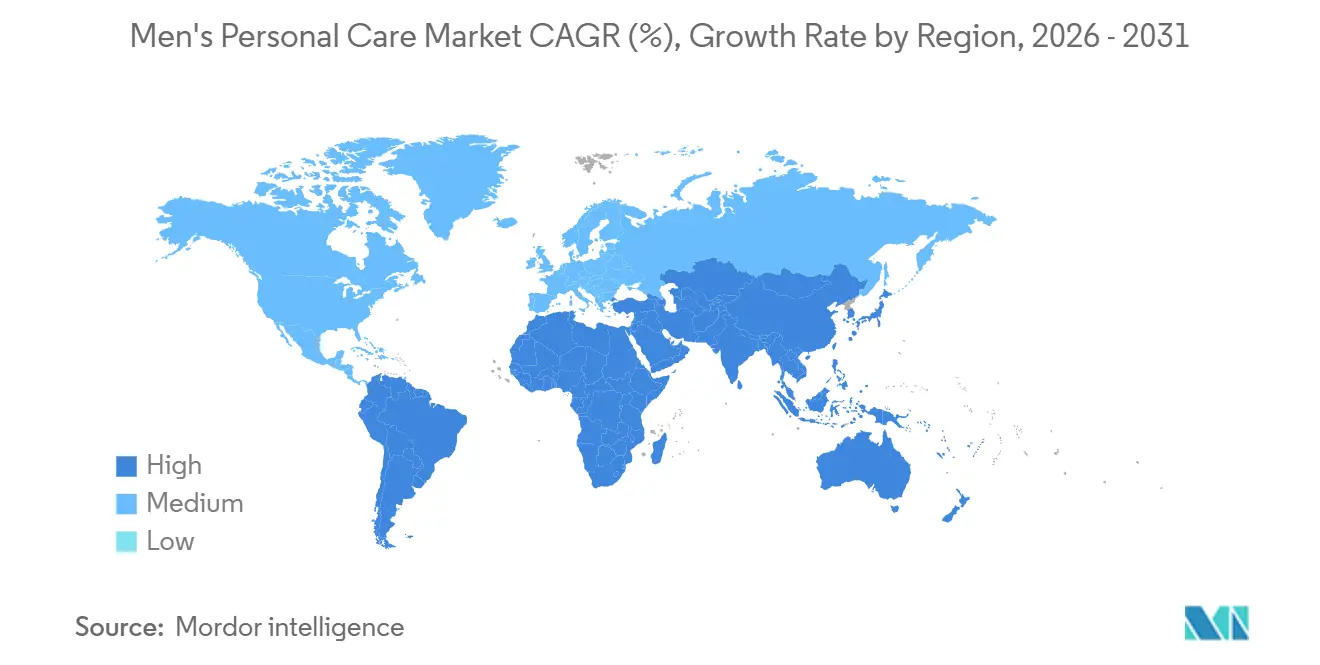

- By geography, Europe commanded 35.40% of the men’s personal care market share in 2025, yet the Middle East and Africa region will post the fastest growth at an 8.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Men's Personal Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising per-capita spending on male grooming in emerging markets | +1.2% | Asia-Pacific (India, Indonesia, Thailand), South America (Brazil, Colombia), Middle East and Africa (Nigeria, Egypt) | Medium term (2-4 years) |

| Marketing shifts toward male influencers and social media | +0.9% | Global, with the highest ROI in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Product innovation in multifunctional and natural-ingredient lines | +1.4% | Global, led by North America and Europe; rapid adoption in Asia-Pacific premium segments | Medium term (2-4 years) |

| Expansion of online retail and e-commerce penetration | +1.3% | Global, with accelerated growth in Asia-Pacific, the Middle East and Africa, and South America | Short term (≤ 2 years) |

| Growth of male-focused subscription boxes and DTC refill models | +0.8% | North America, Europe, urban Asia-Pacific (China, India, Singapore) | Medium term (2-4 years) |

| Workplace return policies are driving demand for premium products | +1.1% | North America, Europe, and Asia-Pacific corporate hubs (Singapore, Hong Kong, Tokyo) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Marketing Shifts Toward Male Influencers and Social Media

Male influencers are outpacing traditional celebrity endorsements in engagement and conversion rates. Vietnamese influencer Bách Buquen, for instance, pocketed USD 500,000 in 2025 from grooming and lifestyle partnerships, underscoring the lucrative potential of niche audiences. While TV and print combined account for just 31% of grooming-product discovery among Gen Z males, TikTok and Instagram Reels dominate with a 62% share. This shift has led brands to divert 40-50% of their marketing budgets towards creator partnerships and short-form video content. Collaborations like Gillette's with ex-NFL star Marshawn Lynch and Dove Men+Care's February 2025 limited-edition merchandise kits highlight how athlete-influencer partnerships can destigmatize body-care discussions and achieve viral reach. However, there's a cautionary tale: brands that overly rely on paid partnerships risk losing authenticity. In contrast, brands that foster organic advocacy, where influencers seamlessly weave products into their daily routines without overt sponsorship, enjoy a 3-4× boost in purchase intent compared to scripted endorsements.

Product Innovation in Multifunctional and Natural-Ingredient Lines

Time-starved consumers are increasingly opting for all-in-one formulations, consolidating multi-step routines into single products. This trend is evident in offerings like Nivea Men's Age Defense line, which combines hyaluronic acid, thiamidol, and pro-retinol in one moisturizer, and Gillette's GilletteLabs Body razor, featuring a built-in exfoliating bar. Certifications like USDA Organic, Ecocert, and COSMOS, once considered niche, now resonate with Gen Z and Millennial consumers. These certifications, signaling transparency and safety, are scrutinized by buyers using apps like Yuka and Think Dirty. In 2025, aluminum-free deodorants, leveraging coconut oil, shea butter, and baking soda alternatives, accounted for 22% of U.S. men's deodorant sales, a significant rise from 11% in 2023. This surge aligns with Google Trends data highlighting sustained interest in "natural deodorant men" searches. Incumbent brands face challenges with reformulation costs and achieving performance parity. Natural actives often necessitate higher concentrations to rival synthetic efficacy, potentially compressing gross margins by 3-5 percentage points unless brands can secure premium pricing.

Expansion of Online Retail and E-Commerce Penetration

In 2026, e-commerce accounted for 22% of men's grooming sales in France and 27% in the U.S. This surge was fueled by the allure of subscription convenience, discreet deliveries for sensitive items (like intimate grooming and anti-aging products), and personalized algorithms highlighting niche brands. Take Harry's, for instance: boasting 2.5 million subscribers each paying USD 77 annually, the brand underscores the financial edge of recurring revenue. Their customer lifetime value stands at over USD 300, a stark contrast to the USD 120 typical for one-time retail buyers. Meanwhile, Dollar Shave Club, buoyed by Unilever's backing, made waves in 2024 by expanding into 30,000-35,000 retail outlets just after its acquisition. This move underscores a vital lesson: while direct-to-consumer (DTC) brands must establish a physical footprint to harness impulse buys and product trials, traditional brick-and-mortar stores need to facilitate smooth online reordering to retain customers. However, the landscape isn't without its challenges. Data privacy regulations, notably GDPR and California's CPRA, introduce consent mandates. For brands heavily leaning on third-party cookies and retargeting, this translates to a 15-20% uptick in customer-acquisition costs.

Growth of Male-Focused Subscription Boxes and DTC Refill Models

Subscription boxes, priced between USD 15-35 monthly, offer a mix of trial sizes, full-size products, and grooming accessories, alleviating decision fatigue and ensuring repeat purchases. Harry's, with its annual plan priced at USD 77, provides razors, shave gel, and skincare products every eight weeks. Meanwhile, India's Bombay Shaving Company presents tiered subscriptions ranging from INR 499 to INR 1,499, complete with free shipping and early access to new launches. The financials tilt in favor of brands: subscription services boast gross margins of 55-60%, outpacing the 40-45% margins seen in wholesale distribution. This advantage arises as direct-to-consumer (DTC) models sidestep retailer markups and harness dynamic pricing informed by usage data. Refill models are gaining traction, not just as a nod to sustainability but also as a means to boost margins. Unilever, for instance, is eyeing 2026 to roll out refillable formats for 10% of its personal-care lineup. They're banking on in-store refill stations, which promise a 30-40% reduction in packaging costs and cater to the eco-conscious demographic. However, a significant hurdle remains: consumer inertia. A survey revealed that 55% of shoppers lean towards convenience over sustainability. This insight nudges brands to position refill stations at bustling grocery and drugstore checkouts, rather than in isolated boutiques.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny over endocrine-disrupting fragrance chemicals | -0.6% | Europe (EU REACH, ECHA), North America (FDA, California Prop 65), Asia-Pacific (select markets) | Medium term (2-4 years) |

| Refill/zero-waste retail models cannibalizing packaged product sales | -0.4% | Europe, North America, urban Asia-Pacific | Long term (≥ 4 years) |

| Cultural stigma in certain regions is limiting adoption | -0.5% | Middle East (conservative segments), South Asia (rural areas), parts of South America | Long term (≥ 4 years) |

| Price sensitivity amid economic slowdowns | -0.7% | Global, with acute impact in South America, the Middle East & Africa, and price-sensitive Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny Over Endocrine-Disrupting Fragrance Chemicals

EU Regulations 2025/877 and 2026/78 target CMR (carcinogenic, mutagenic, reprotoxic) substances and PFAS in cosmetics[1]Source: European Union, “Packaging and Packaging Waste Regulation Proposal,” eur-lex.europa.eu . As a result, brands are reformulating products like fragrances, deodorants, and aftershaves, moving away from synthetic musks, phthalates, and parabens, which were previously used as fixatives and preservatives. Limits on formaldehyde have been tightened to 0.05% for leave-on products. Additionally, 26 fragrance allergens now mandate explicit labeling. These changes extend product-development cycles by 6-12 months and elevate compliance costs by 8-12% for mid-tier brands that don't have in-house toxicology teams. California's Prop 65, alongside the FDA's voluntary guidance on phthalates in personal care, creates a fragmented regulatory environment. This landscape pressures global brands to either tailor formulations to specific regions or adopt the EU's stringent standards as their global benchmark. In response, brands are opting for transparent ingredient disclosures and third-party certifications, such as Ecocert, COSMOS, and USDA Organic. While these measures help mitigate regulatory risks, they come at an added cost of USD 0.15-0.30 per unit, covering both certification fees and reformulation expenses.

Refill/Zero-Waste Retail Models Cannibalizing Packaged Product Sales

California's Extended Producer Responsibility (EPR) mandates a rise in refillable packaging: starting at 2% by 2027 and scaling up to 10% by 2032. Meanwhile, the EU's Packaging and Packaging Waste Regulation echoes these targets, pushing brands to experiment with refill stations and concentrated formats. Unilever's pledge to make 10% of its personal-care range refillable by 2030, with a 2026 milestone, underscores a significant industry shift. However, consumer uptake remains tepid. A survey reveals 55% of shoppers lean towards convenience over sustainability. For refill stations to gain traction, they must be strategically placed at bustling grocery checkouts. Yet, there's a looming challenge: each refill transaction nets 30-40% less revenue than a fresh package. If 15-20% of consumers opt for refills, this could stifle top-line growth by 0.3-0.5 percentage points annually. Brands can counteract this by pricing refills at 70-75% of their packaged counterparts, capitalizing on packaging cost savings. Additionally, positioning refill programs as loyalty incentives could boost purchase frequency and open doors for cross-selling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Haircare Dominance Faces Fragrance Acceleration

In 2025, haircare holds a 33.59% share of the men's personal care market, driven by the need to cleanse, condition, and style hair across age groups and lifestyles. The market offers a wide range of SKUs, from value shampoos to salon-grade pomades and gels. Rising professional appearance standards fuel demand for styling products with all-day hold, while urban men increasingly seek innovations like anti-pollution serums and caffeine-infused thickening sprays. Brands leverage scientific insights, particularly in scalp microbiome health, to create research-driven solutions for results-focused consumers. Social media tutorials further highlight the benefits of styling clays and fiber pastes, emphasizing experiential storytelling to maintain a competitive edge.

Fragrance-infused deodorants lead the men's personal care segment, with a 7.08% compound annual growth rate (CAGR) projected through 2031. This growth is tied to the work-from-anywhere culture blending fitness, work, and social activities. Consumers value these deodorants for their fresh scent profiles and the confidence they provide, enabling brands to charge a 15–20% premium over standard antiperspirants. Rising disposable incomes drive purchases of complementary products like body sprays and colognes, expanding grooming routines and boosting basket sizes. Collaborations with fashion labels enhance the appeal of these deodorants, while innovations in scent and packaging position them as both essentials and lifestyle statements, shaping the future of men's grooming.

By Ingredient Type: Natural Revolution Challenges Synthetic Dominance

In 2025, synthetic formulations dominate the men's personal care market, accounting for 56.69% of revenue. Their stability, cost-effectiveness, and scalability make them the preferred choice for manufacturers and consumers. These formulations meet diverse consumer expectations and allow brands to offer competitive pricing, maintaining their mass-market appeal. While natural alternatives are gaining traction, synthetic formulations remain a key component of many brands' portfolios.

The natural and organic segment is the fastest-growing category in men's personal care, with a projected CAGR of 7.67% from 2026 to 2031. Rising consumer awareness about ingredient safety and social responsibility, along with regulatory measures like PFAS bans, is driving demand for plant-based products. Brands are reformulating products with botanicals such as aloe and tea tree oil, often obtaining certifications like COSMOS and USDA Organic. However, climate change threatens the supply of key botanicals, prompting investments in vertical farming and synthetic biology. Male consumers prioritize efficacy, pushing R&D to balance clean-label standards with performance. Despite higher costs for biodegradable preservatives and sustainable packaging, the premium segment absorbs these expenses. Regulatory momentum and consumer activism are reshaping industry benchmarks, narrowing the gap between niche eco-brands and mainstream offerings in the men's personal care market.

By Category: Mass-Market Scale Versus Premium Growth Velocity

In 2025, the mass-market segment dominated the men's personal care market, accounting for 73.18% of the total revenue. This dominance stems from its affordability, widespread availability, and backing by well-known brands. Multipacks, larger bottles, and promotional bundles cater to price-sensitive consumers and families. The accessibility and familiarity of these products ensure steady sales across demographics. Trust in established brands enhances loyalty, solidifying the segment's position. Despite competition, its value-driven approach and extensive distribution channels maintain consistent revenue.

The premium segment is the fastest-growing in men's personal care, with a 7.07% CAGR. Growth is driven by innovative packaging, curated ingredients, and gift-worthy products appealing to urban professionals and grooming enthusiasts. Premium products symbolize self-care and social standing. Subscription services featuring exclusive balms and fragrances encourage repeat purchases. With profit margins often exceeding 60%, private equity firms are investing, as seen in Unilever's USD 1.5 billion acquisition of Dr. Squatch in June 2025. Mid-tier brands are launching prestige sub-lines and collaborations, blending luxury aesthetics with affordability. The men's personal care market is set to split between premium, experience-driven products and mass-market staples prioritizing volume and value.

By Distribution Channel: Digital Disruption Challenges Traditional Retail

In 2025, supermarkets and hypermarkets commanded a notable 35.72% share of the men's personal care market. These retail giants capitalized on their strengths: offering one-stop convenience, ensuring immediate product availability, and prominently displaying promotions, such as end-caps. For first-time buyers, especially those new to grooming, these venues play a crucial role. Shoppers often make in-aisle decisions, and the physical presence of multiple brands in one location fosters trust and encourages impulse buys. With a vast geographic reach and diverse product assortments, these retailers cater to a wide consumer base in both urban and suburban settings. Additionally, strategic merchandising and price promotions bolster shopper loyalty. Even with rising competition from alternative channels, supermarkets and hypermarkets remain foundational to the men's personal care retail scene.

Online retail has emerged as the fastest-growing channel in the men's personal care market, boasting a robust 7.81% CAGR. This surge is largely attributed to consumers gravitating towards the convenience and speed of digital shopping. Mobile applications now offer features like loyalty rewards, same-day delivery, and AI-driven chatbots, expediting the journey from product discovery to purchase. Subscription services, especially for staples like body wash, not only boost customer lifetime value but also expand wallet share. E-commerce platforms are pushing boundaries with innovations like shoppable social livestreams, where influencers showcase products in real-time, amplifying both engagement and conversion rates. On another front, new omnichannel models are emerging, offering click-and-collect options that merge the immediacy of brick-and-mortar shopping with online convenience. This swift transformation compels brands to reevaluate their investment strategies, striking a balance between traditional shelf space, online marketplace fees, and digital advertising to uphold visibility and market presence.

Geography Analysis

In 2025, Europe commands a 35.40% share of the revenue pie, a testament to its deep-rooted grooming traditions. With its mature market, Europe leans towards premiumization over sheer volume growth. Here, brands vie for attention through masterful fragrance artistry, eco-friendly packaging, and exclusive limited-edition collaborations. Regulatory shifts play a pivotal role, highlighted by Directive 2024/825, which bans baseless green claims, pushing for greater transparency and innovative eco-designs[2]Source: European Union, " DIRECTIVE (EU) 2024/825 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL", eur-lex.europa.eu. Retailers are quick to act, enforcing chemical blacklists that hasten product reformulations.

In contrast, the Middle East and Africa region is on an upswing, boasting an impressive 8.02% CAGR projected through 2031. This growth is fueled by urbanization, the ambitious agendas of the UAE and Saudi Vision, and a burgeoning mall culture. Gulf megamalls are witnessing a surge in grooming kiosks, while local entrepreneurs harness social media's power to promote products like beard oils and Oud-infused shower gels.

North America continues to be at the forefront of innovation, buoyed by venture-backed start-ups and the FDA's enforcement of the Modernization of Cosmetics Regulation Act (MoCRA)[3]Source: United States Food and Drug Administration," Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", www.fda.gov. The region also sees a robust appetite for multifunctional grooming products. On the other hand, South America grapples with economic challenges; while inflation curtails the appetite for premium products, the region's barbershop culture ensures a steady demand for budget-friendly hair gels and colognes. This geographical landscape underscores the need for tailored strategies, harmonizing local nuances with the overarching consistency of global brands in the men's personal care arena.

Competitive Landscape

Major companies dominate the men's personal care market is moderately fragmented. This dominance is bolstered by Procter & Gamble's robust research and development, proprietary blade-coating technology, and a significant shelf presence. Unilever's acquisition of Dr. Squatch for USD 1.5 billion in June 2025 underscores its strategic move into the premium-natural segment, pushing its premium portfolio share closer to 50%. Meanwhile, companies like Edgewell, L’Oréal, Beiersdorf, and Johnson & Johnson’s Kenvue division are expanding their portfolios through a mix of serial acquisitions, digital innovation labs, and regional standout products.

Direct-to-consumer (DTC) brands like Harry’s, Dollar Shave Club, and Hims are reshaping the landscape by harnessing subscription models, fostering direct customer engagement, and rapidly iterating their products. Their nimble fulfillment networks resonate with younger consumers who value convenience and transparent pricing. Private labels are also gaining traction, with retailers such as Target and Boots launching house brands that marry competitive pricing with clean labels. Technology collaborations are on the rise: L’Oréal’s Perso device offers on-demand customised moisturisers, and Beiersdorf is testing AI skin cameras in Nivea Men displays. Marketing budgets are shifting towards short-form video platforms, where algorithmic reach far outpaces traditional TV. Additionally, apparel giants are venturing into grooming, creating cross-industry synergies and broadening their lifestyle ecosystems.

Under the MoCRA regulations, which require facility registration and product listing by July 2024, compliance is becoming a key differentiator. Early adopters are using their compliance readiness as a badge of trust. Sustainability commitments are also setting players apart; for instance, Edgewell's 2024 report pledges 100% recyclable packaging by 2030, a move that could sway retailer shelf placements. In this dynamic landscape, established players are balancing acquisitions with organic innovations to maintain their relevance, while newer entrants are capitalizing on cultural shifts and channel diversifications to challenge the status quo in the men's personal care market.

Men's Personal Care Industry Leaders

-

Procter & Gamble

-

Unilever PLC

-

L’Oréal S.A.

-

Beiersdorf AG

-

Colgate-Palmolive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Gillette (Procter & Gamble) launched the GilletteLabs Body razor, engineered specifically for men's body and intimate grooming with a Triple Protection System (anti-irritation bar, anti-ingrown bar, lubrication strip) and body-optimized handle design (shorter length, enhanced wet grip, magnetic shower mount), addressing the 70% of men who repurpose facial razors for body use and experience nicks, cuts, and ingrown hairs.

- May 2025: Manscaped unveiled its new skincare line, Skin Ultra, tailored for men, featuring products like face wash and moisturizers. This launch marked the brand's expansion into the men's skincare segment, aiming to cater to the growing demand for male grooming products.

- February 2025: Suave Brands rolled out a fresh lineup of men's personal care items, encompassing shampoos, conditioners, and more. The new range was introduced to strengthen the company's presence in the men's personal care market and to provide affordable yet high-quality grooming solutions.

Global Men's Personal Care Market Report Scope

Men's personal care products are specialized, non-medicinal grooming items, including skincare, hair care, beard maintenance, and shaving products, designed specifically for male skin biology and grooming routines. The Men's personal care products are segmented by product type, ingredient type, category, distribution channel, and geography. By product type, the market is segmented into skin care products, hair care products, deodorants and fragrances, and bath and shower products. The skin care products segment is further sub-segmented into face wash, moisturizers, face masks, and other skin care products. Similarly, the hair care products segment is further sub-segmented into shampoo and conditioners, styling products, hair colorants, and other hair care products. By ingredient type, the market is segmented into natural/organic and conventional/synthetic. By category, the market is segmented into mass and premium. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Skin Care Products | Face Wash |

| Moisturizers | |

| Face Mask | |

| Other Skin Care | |

| Hair Care Products | Shampoo and Conditioners |

| Styling Products | |

| Hair Colorants | |

| Other Hair Care Products | |

| Deodorants and Fragrances | |

| Bath and Shower |

| Natural/Organic |

| Conventional/Synthetic |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Skin Care Products | Face Wash |

| Moisturizers | ||

| Face Mask | ||

| Other Skin Care | ||

| Hair Care Products | Shampoo and Conditioners | |

| Styling Products | ||

| Hair Colorants | ||

| Other Hair Care Products | ||

| Deodorants and Fragrances | ||

| Bath and Shower | ||

| Ingredient Type | Natural/Organic | |

| Conventional/Synthetic | ||

| Category | Mass | |

| Premium | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the men's personal care market in 2026?

The men's personal care market size stands at USD 50.40 billion in 2026, on track to reach USD 69.83 billion by 2031.

What is the expected growth rate for men’s personal care through 2031?

The market will advance at a 6.74% CAGR from 2026 to 2031 thanks to premiumization, e-commerce penetration, and product innovation.

Which product segment is growing fastest?

Deodorants and fragrances will record the highest CAGR at 7.08% between 2026 and 2031 as whole-body formats attract new users.

Why are natural and organic formulations gaining share?

Gen Z and Millennials value transparency and safety, driving a 7.67% CAGR for certified natural products that already account for 22% of U.S. deodorant sales.

Page last updated on: