Market Overview

| Study Period | 2021 - 2031 |

|---|---|

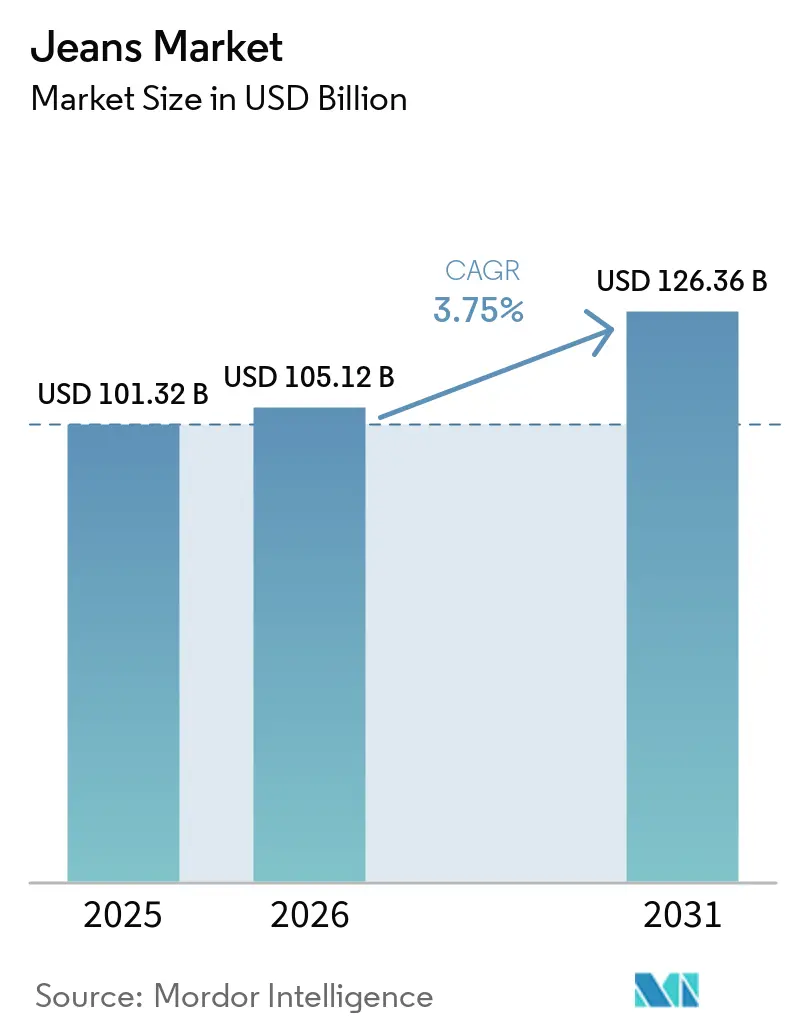

| Market Size (2026) | USD 105.12 Billion |

| Market Size (2031) | USD 126.36 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

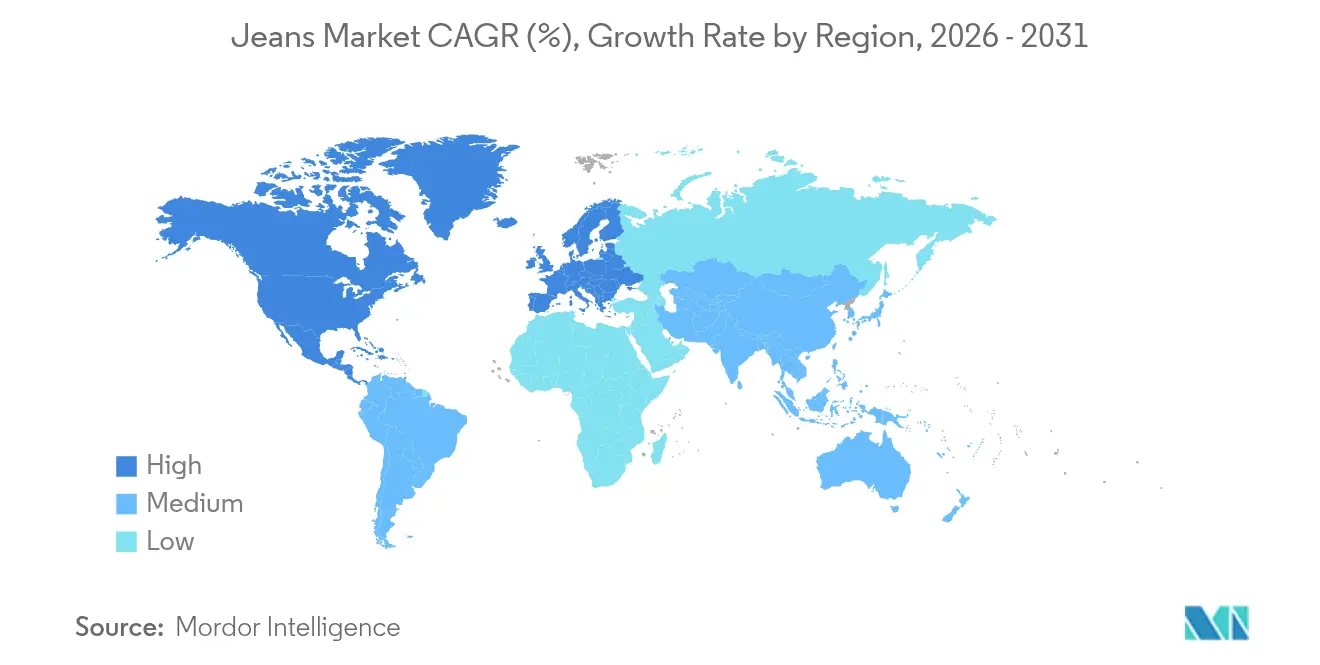

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

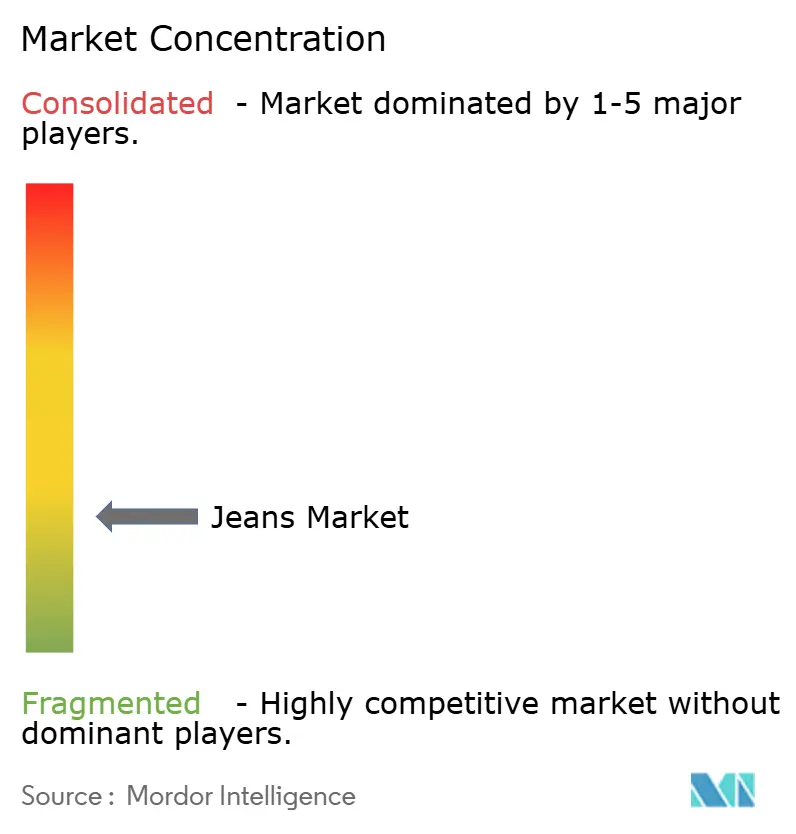

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Jeans Market Analysis by Mordor Intelligence

The global jeans market size was valued at USD 101.32 billion in 2025 and estimated to grow from USD 105.12 billion in 2026 to reach USD 126.36 billion by 2031, at a CAGR of 3.75% during the forecast period (2026-2031). As premium denim and innovative fabrics gain traction, coupled with direct-to-consumer (DTC) strategies, consumers enjoy a broader selection. This not only bolsters brand margins but also extends product life cycles. In 2024, Levi Strauss & Co., the American giant synonymous with its Levi's denim brand, reported net sales of approximately USD 6.35 billion, a rise from USD 6.17 billion in 2023[1]Source: Levi Strauss & Co., "Levi Strauss & Co. - 10-K Report 2024", www.levistrauss.com. Denim's enduring cultural significance cements its place in casual wardrobes. Yet, with sustainability in focus, brands are increasingly turning to low-impact dyeing, recycled fibers, and take-back initiatives. The rise of digital commerce is undeniable, with virtual fit tools playing a pivotal role in reducing return rates and expanding market reach. In response to a hefty 120% U.S. tariff on Chinese jeans, manufacturers are diversifying their supply chains, shifting production to Mexico, Turkey, and Egypt, and ramping up investments in automation for nimble inventory management.

Key Report Takeaways

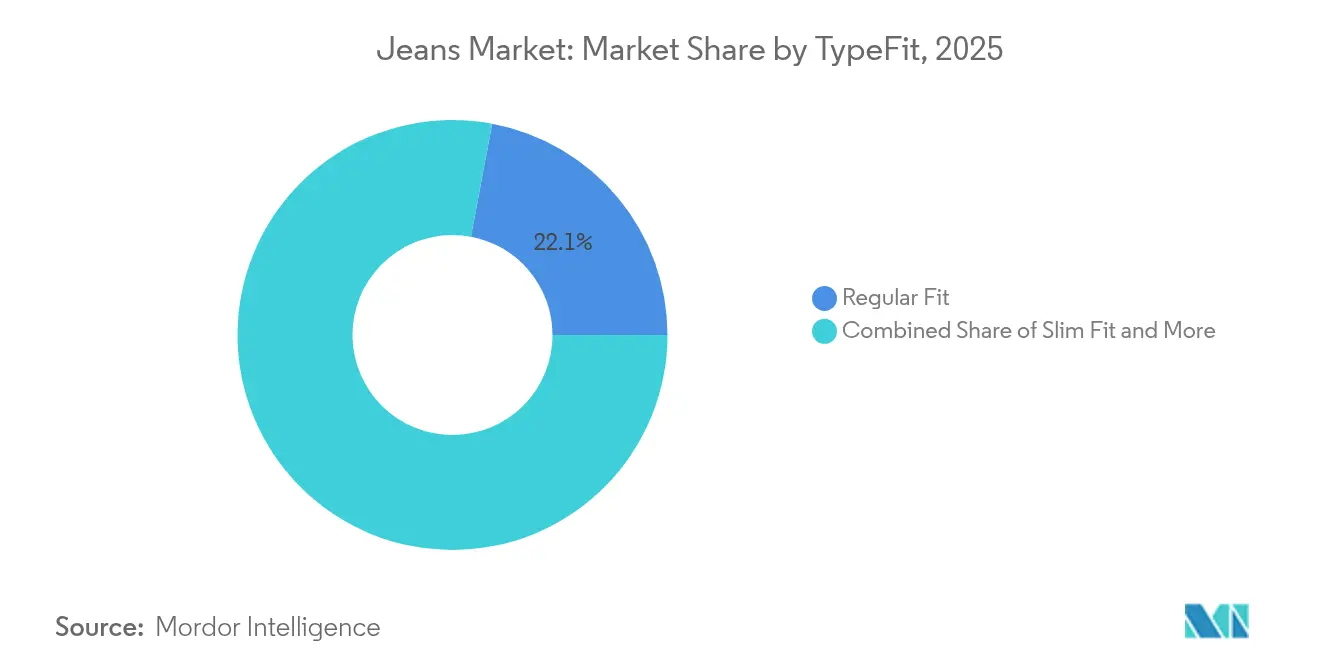

- By product fit, regular fit led with 22.05% of the jeans market share in 2025, and slim fit is projected to advance at a 4.55% CAGR through 2031.

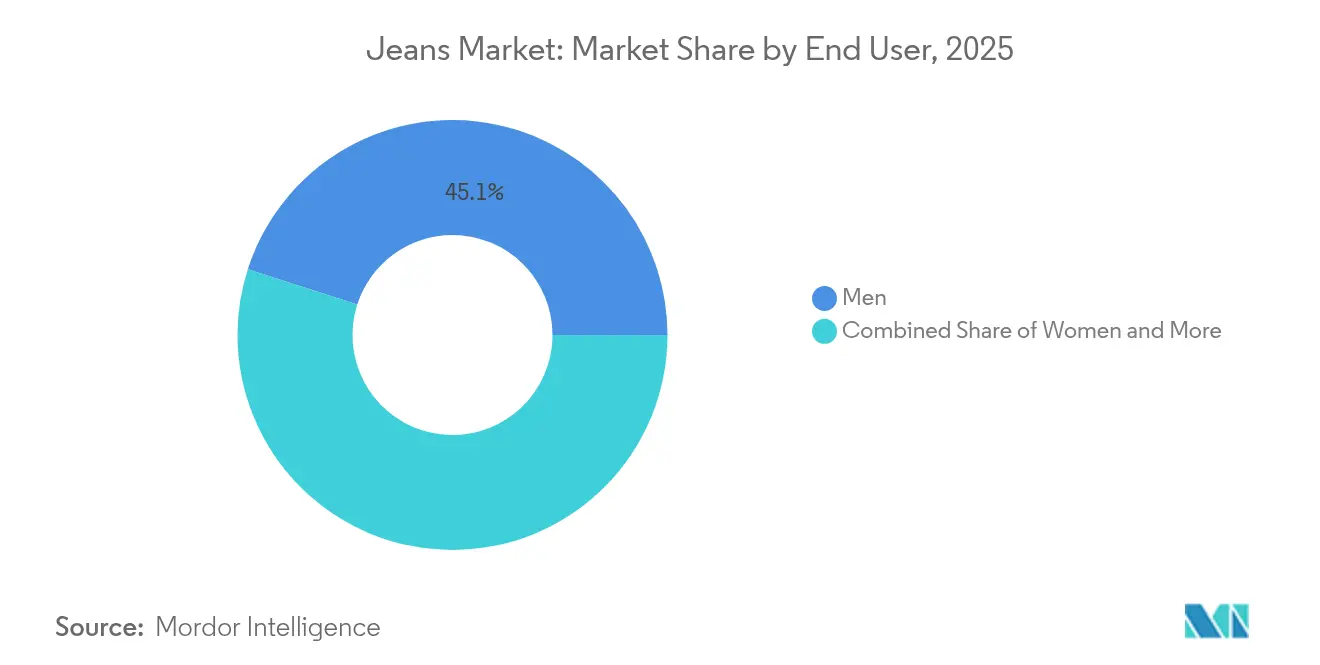

- By end user, men commanded a 45.05% share of the global jeans market in 2025, while women’s lines are forecast to expand at an 5.92% CAGR through 2031.

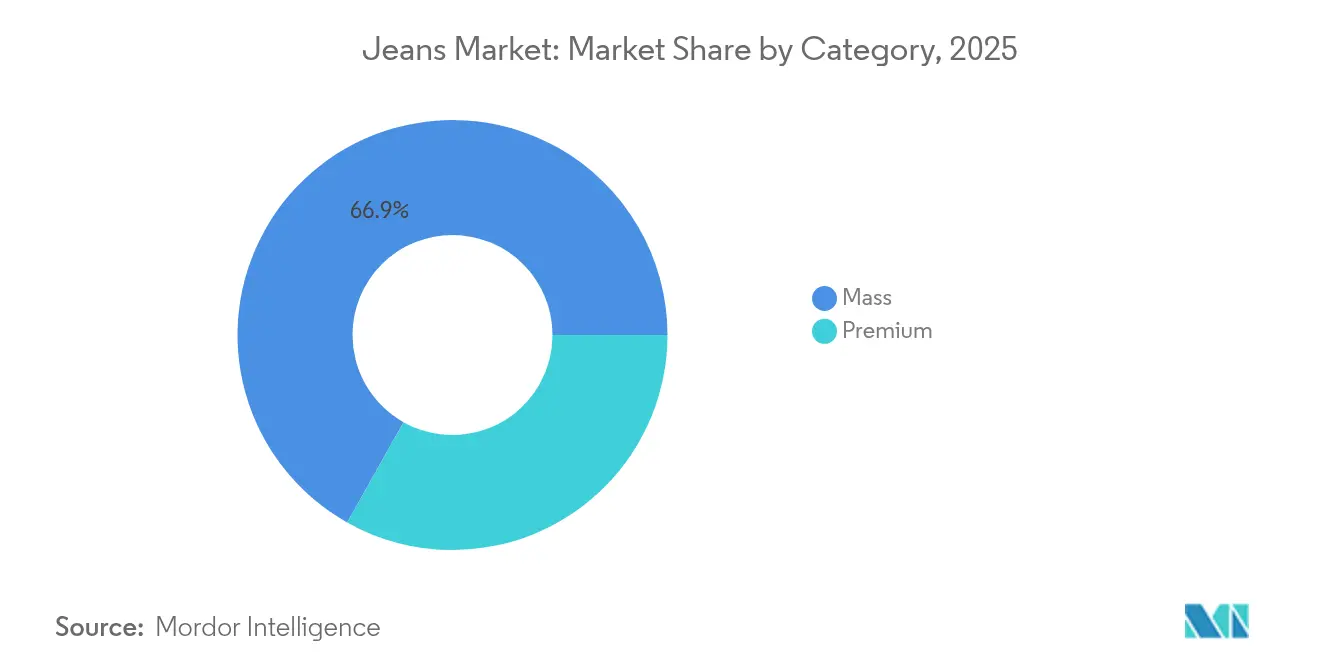

- By category, mass-market offerings accounted for a 66.85% share of the jeans market size in 2025, and premium denim is projected to grow at a 4.92% CAGR between 2026 and 2031.

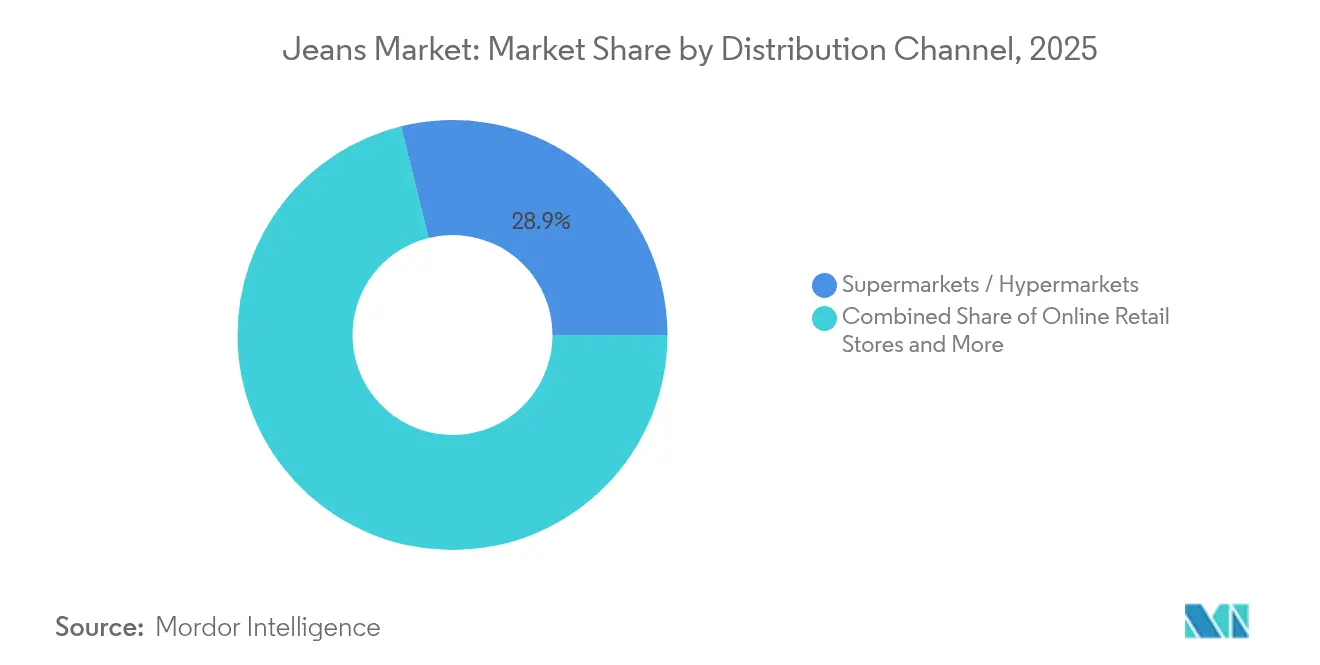

- By distribution channel, supermarkets and hypermarkets held 28.85% revenue share in 2025, whereas online retail is on track for a 6.55% CAGR to 2031.

- By geography, North America retained a 32.35% share in 2025, and Asia-Pacific carries the fastest trajectory with a 5.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Jeans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fashion Trends and Consumer Preferences | +1.5% | Global, with stronger influence in North America and Europe | Medium term (2-4 years) |

| Increasing Preference for Premium and Branded Denim | +0.8% | North America, Europe, Asia Pacific urban centers | Long term (≥ 4 years) |

| Technological Advancements in Fabric and Finishes | +0.6% | Global, led by manufacturing hubs in the Asia-Pacific | Medium term (2-4 years) |

| Sustainability and Eco-Friendly Innovations | +0.4% | Europe, North America, with spillover to the Asia-Pacific | Long term (≥ 4 years) |

| Customization and Personalization | +0.3% | North America, Europe, Asia-Pacific premium segments | Medium term (2-4 years) |

| Celebrity and Influencer Collaborations | +0.2% | Global, concentrated in fashion-forward markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fashion Trends and Consumer Preferences

As consumer preferences evolve, denim pieces are increasingly favored for their versatility, effortlessly transitioning from casual to semi-formal settings. This shift is propelling the denim market's expansion, moving beyond its traditional workwear roots. In the wake of the pandemic, workplaces have embraced an "elevated casual" dress code, fueling a demand for premium denim that strikes a balance between comfort and professionalism. Generational preferences in denim consumption reveal stark contrasts: Gen Z places a premium on fit innovation and sustainability, often sidelining brand legacy, whereas millennials seek a harmonious blend of quality and value. The color palette of denim has expanded, moving beyond the classic indigo to embrace earthy tones and technical washes, resonating with the style-savvy. The rapid pace of trend cycles, amplified by social media, has pushed brands to shorten their design-to-market timelines from 18 months to a swift 6-8 months, ensuring they don't miss out on viral fashion moments. These dynamics underscore the surging global demand for denim and jeans, a demand increasingly met by rising imports. Highlighting this trend, data from UN Comtrade reveals Vietnam's dominance as the world's top denim importer, with a staggering import value exceeding USD 320 million[2]Source: UN Comtrade, "Denim Fabric Imports", www.comtradeplus.un.org.

Increasing Preference for Premium and Branded Denim

Even in tough economic times, consumers are willing to invest in premium denim, valuing its longevity and the status it conveys. The USD 200-400 price segment is thriving, as buyers justify the splurge with cost-per-wear logic and sustainability narratives. Heritage brands, with their emphasis on craftsmanship and storytelling, use limited edition releases to validate their premium pricing. In contrast, newer brands are carving their niche with innovative materials and ethical production. By selling directly to consumers, premium brands not only boost their margins but also offer a personalized shopping experience that's hard to find in traditional retail. Collaborations with luxury fashion houses have transformed denim from a mere utility to a coveted fashion statement, broadening its market appeal. Cotton-based denim, celebrated for its timelessness and versatility from casual outings to semi-formal events, is witnessing a surge in global demand. This is driven by a growing appetite for durable, comfortable, and sustainable clothing. Data from UN Comtrade highlights this trend: in 2023, Mexico exported nearly USD 56 million worth of denim fabric, predominantly cotton (at least 85% cotton content), to the U.S. Nicaragua trailed with imports valued at USD 8.7 million[3]Source: UN Comtrade, "Leading importers of denim made from at least 85 percent cotton to the United States", www.comtradeplus.un.org.

Technological Advancements in Fabric and Finishes

Advanced materials, such as graphene and anti-microbial treatments, are revolutionizing denim's performance characteristics. For example, Candiani Denim's GRAPHITO technology uses graphene fibers to boost durability and introduce antibacterial properties. This innovation not only cuts down on washing frequency but also prolongs the garment's lifespan. In another instance, LYCRA's Anti-Slip fiber tackles seam slippage in stretch denim, enhancing garment quality and helping manufacturers reduce return rates. Meanwhile, laser finishing technologies are taking the place of traditional chemical methods, slashing water consumption by up to 96% and still achieving precise fade patterns and distressing effects. Furthermore, digital printing is paving the way for mass customization without the risk of excess inventory, empowering brands to roll out personalized designs on a larger scale.

Sustainability and Eco-Friendly Innovations

Brands are reshaping their production methodologies in response to regulatory pressures and a growing consumer demand for transparent supply chains. A 2024 survey by the UK government revealed that nearly 80% of UK residents expressed concerns about climate change. Traditional denim processing, known for its high water consumption, is under scrutiny. This has led to the adoption of closed-loop systems and alternative dyeing technologies, which boast a 70-80% reduction in environmental impact. Principles of the circular economy are gaining momentum, with brands implementing take-back programs and integrating recycled fibers. Many are setting ambitious targets, aiming for 100% sustainable material sourcing by 2030. In the EU, regulations now enforce Extended Producer Responsibility for managing textile waste. This pushes brands to rethink their designs, emphasizing recyclability and durability. Furthermore, blockchain certification systems are bolstering supply chain transparency, allowing consumers to easily verify sustainability claims and ethical production practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Alternative Apparel | -0.7% | Global, particularly in casual wear segments | Short term (≤ 2 years) |

| Counterfeit and Low-Quality Products | -0.5% | Global, concentrated in online marketplaces | Medium term (2-4 years) |

| High Production Costs | -0.4% | Global, acute in developed manufacturing regions | Medium term (2-4 years) |

| Tariff and Trade Policy Uncertainties | -0.3% | Global trade routes, US-China corridor most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Alternative Apparel

As consumers shift towards comfort and versatility in their post-pandemic lifestyles, athletic wear's rise in casual fashion is encroaching on denim's market share. Athleisure brands are harnessing technical fabrics and performance features, outpacing traditional denim, especially in areas like moisture management and stretch recovery. With the normalization of the "work from home" culture, there's been a marked reduction in occasions for structured denim, leading to a pronounced shift in preference towards joggers and leggings. Fast fashion retailers, by offering denim alternatives at competitive price points, are accelerating trend cycles, putting established brands under pressure to innovate and provide value. As fashion trends lean towards minimalist wardrobes, there's a growing preference for multi-functional garments, sidelining category-specific pieces like jeans.

High Production Costs

Manufacturers grapple with margin pressures and reduced pricing flexibility due to volatile costs of raw materials, especially cotton and synthetic fibers. The Office of Economic Adviser, India, reported that in the financial year 2024, India's Wholesale Price Index for cotton yarn hovered around INR 149.4. Rising labor costs in traditional manufacturing hubs, notably Bangladesh and Vietnam, compel brands to reconsider strategies, leaning towards nearshoring or automation, both of which demand hefty capital investments. Compliance with sustainability mandates, encompassing eco-friendly materials, water treatment, and certification, inflates production costs by 15-20%. This surge poses a challenge, especially for smaller manufacturers. European manufacturers, in particular, feel the pinch of rising energy prices, which heavily impact dyeing and finishing operations reliant on thermal processing. Additionally, as brands bolster inventory buffers to counter disruption risks, the intricacies of the supply chain amplify working capital demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type/Fit: Slim Fit Drives Style Evolution

In 2025, the regular fit segment leads the market with a 22.05% share, underscoring a consumer preference for versatile silhouettes that cater to various body types and style inclinations. Meanwhile, slim fit variants are on the rise, boasting a 4.55% CAGR through 2031, fueled by younger consumers drawn to modern aesthetics and refined tailoring. As fashion trends pivot towards relaxed silhouettes, skinny fit options see a downturn. Conversely, bootcut and flared styles make a comeback, appealing to trendsetters with a penchant for Y2K-inspired looks. The "others" category highlights emerging fits like tapered, straight-leg, and wide-leg variants, reflecting the industry's response to shifting style preferences and the body positivity movement.

Brands leverage advanced manufacturing techniques to broaden size ranges and fit variations, all without a proportional spike in inventory, bolstering their market segmentation strategies. By integrating fit technologies such as 3D body scanning and virtual try-ons, brands not only enhance customer satisfaction across diverse body types but also curtail return rates. The fusion of comfort and style has birthed hybrid fits, merging relaxed waistlines with tapered legs, catering to consumers who prioritize both fashion and functionality. While regulatory compliance for fit variations is largely minimal, industry associations are pushing for sizing standardization to mitigate consumer confusion and reduce return rates.

By End User: Women's Segment Accelerates Growth

In 2025, men's denim holds a 45.05% share of the market, a testament to its historical development and robust per-capita consumption globally. Women's denim, however, is on a rapid ascent, boasting an 5.92% CAGR through 2031. This surge is fueled by fashion innovations, a premium market stance, and a broadened application of occasion-wear, moving beyond just casual settings. Meanwhile, children's denim, though stable, grows at a more measured pace, shaped by swift market dynamics and parents' awareness of their kids' rapid growth.

Women's denim thrives on the fast-paced fashion cycle, with seasonal collections prompting more frequent purchases. In contrast, men's denim sales are largely driven by replacements. Premium women's denim, with its trendy fits and sustainable materials, often backed by celebrity endorsements, commands higher price points and wider margins. The rise of gender-neutral designs is resonating with younger consumers, opening doors to markets that defy traditional segmentation. Growth in the children's denim segment is closely tied to birth rates and disposable income, with eco-conscious parents increasingly favoring organic cotton and sustainable production methods.

By Category: Premium Growth Outpaces Mass Market

In 2025, mass market products command a dominant 66.85% share, catering to price-sensitive consumers worldwide through strategic value positioning and extensive distribution networks. Meanwhile, premium segments are on a growth trajectory, boasting a 4.92% CAGR through 2031. This growth underscores a notable consumer trend: even amidst economic challenges, there's a pronounced willingness to invest in quality, sustainability, and brand heritage. Such dynamics hint at a market polarization, where mid-tier offerings are gradually ceding ground to both value-driven and luxury positioning strategies.

Premium brands are harnessing direct-to-consumer channels, not just for margin control but also to curate personalized experiences that validate their elevated price points. On the other hand, mass market players are honing in on operational efficiency and supply chain optimization. By adopting fast fashion principles, they're able to roll out trend-relevant products at prices that resonate with the average consumer. Sustainability is becoming a pivotal factor in category positioning. Premium brands are spotlighting their commitment to ethical production, while mass market counterparts are pivoting towards offering affordable yet eco-friendly alternatives. However, it's worth noting that regulatory compliance costs weigh heavily on mass market margins. In contrast, premium brands, buoyed by their ability to command higher selling prices, find it easier to shoulder the costs associated with sustainability and safety mandates.

By Distribution Channel: Digital Transformation Accelerates

In 2025, traditional supermarkets and hypermarkets capture a 28.85% market share, leveraging convenience, competitive pricing, and opportunities for impulse purchases that resonate with grocery shopping habits. Online retail stores, buoyed by advancements like sizing technology, virtual try-ons, and direct-to-consumer strategies, emerge as the fastest-growing channel, boasting a 6.55% CAGR projected through 2031. Meanwhile, specialist stores, offering curated experiences and expert fitting services, assert their relevance in the face of digital competition.

E-commerce's ascent is bolstered by enhanced logistics, adaptable return policies, and personalized algorithms that boost product discovery and conversion rates. The COVID-19 pandemic catalyzed a lasting shift, making consumers more at ease with online apparel purchases and diminishing previous hesitations. With social commerce on the rise, brands harness the power of influencer marketing and user-generated content, significantly influencing purchase decisions. As cross-border e-commerce broadens the horizons for premium brands, it simultaneously introduces challenges, navigating the intricate web of customs, duties, and varying consumer protection standards across jurisdictions.

Geography Analysis

In 2025, North America captured 32.35% of global revenue, driven by mature consumption and aggressive direct-to-consumer (DTC) strategies from established brands. Factors like high disposable incomes, prevalent casual dress codes, and an early embrace of personalization technology bolster the regional jeans market. In response to rising sustainability concerns, brands are initiating take-back events and highlighting recycled cotton blends on their hangtags. However, tariff disputes with China are inflating landed costs, prompting a shift in sourcing towards Mexico, Guatemala, and the Caribbean.

Asia-Pacific emerges as the dominant growth engine, targeting a 5.45% CAGR through 2031. Urbanization in China, India, and Indonesia is broadening the middle-class demographic, increasingly attracted to Western fashion. Platforms like Tmall in China and Myntra in India are enhancing last-mile delivery, boosting market penetration in tier-2 cities. Government initiatives bolster textile growth: India’s Production-Linked Incentive scheme offers modernization subsidies, while Vietnam enjoys duty-free access to the EU. Rising wages in coastal China are pushing factory clusters either inland or overseas, creating intricate supply networks across Asia.

Europe, while anchoring a premium stance in the jeans market, grapples with stringent regulations promoting eco-innovation. The EU’s Extended Producer Responsibility mandates designs that facilitate disassembly, leading to the creation of modular jeans with detachable components. Heightened consumer awareness is elevating the importance of B-Corp and Fairtrade certifications. In a bid to meet circularity goals, brands are testing rental and resale initiatives. Yet, challenges arise from currency volatility and fluctuating energy prices, pushing Italian and Spanish brands towards greater automation.

South America, along with the Middle East and Africa, holds potential for the long haul, buoyed by youthful demographics and burgeoning e-commerce. Yet, political instability and currency fluctuations hinder swift expansion. To navigate these challenges, brands are piloting micro-fulfillment centers in Brazil and setting up omnichannel kiosks in Saudi malls, aiming to enhance local service and mitigate import duties.

Competitive Landscape

The jeans market remains moderately fragmented, with no single player commanding a double-digit global share, creating ample opportunities for niche entrants. Levi Strauss, Kontoor Brands (the parent of Wrangler, Lee), and PVH, with its Tommy Hilfiger and Calvin Klein brands, boast strong brand equity. However, fast fashion giants Inditex and H&M lead in trend responsiveness, data analytics, and an expansive store network. Direct-to-consumer (DTC) brands like Re/Done and Mott & Bow attract premium shoppers through online-first sizing algorithms and exclusive limited drops.

Competitive strategies can be categorized into three main themes. Heritage brands are increasingly focusing on DTC channels, leveraging data-driven inventory management, and emphasizing storytelling around craftsmanship and sustainability. In contrast, fast fashion entities prioritize agile, vertically integrated supply chains, enabling them to produce small batches in just three weeks. Newer, pure-play brands are carving a niche through eco-credibility, offering features like plant-based dyes, repair services, and blockchain certificates for provenance.

Investment trends highlight a focus on automation, 3D design software, and laser finishing techniques, all aimed at reducing unit costs and minimizing environmental impact. In light of a hefty 120% duty imposed by the U.S., there's a noticeable shift in strategic sourcing from China to countries like Mexico, Turkey, Egypt, and Bangladesh. Furthermore, supply chain digitization, harnessing tools like RFID and predictive analytics, is enhancing real-time stock visibility and curbing markdown expenses. On the regulatory front, compliance measures, ranging from carbon disclosures and water-use reporting to labor audits are becoming stringent, creating higher entry barriers and favoring well-capitalized industry incumbents.

Jeans Industry Leaders

-

Kontoor Brands Inc

-

Levi Strauss & Co.

-

Gap Inc

-

Hennes & Mauritz AB

-

PVH Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Guess Jeans was launched in India in partnership with Tata CLiQ. As part of this partnership, Tata CLiQ will be the official retailer for Guess Jeans in India, expanding its retail presence through brick-and-mortar stores along with digital storefronts in Bengaluru. As the next step in the global growth initiative for Guess Jeans, the company has been expecting a rapidly expanding and prosperous partnership with Tata CLiQ.

- November 2024: Denim wear brand, Wrangler, launched six new stores across Ujjain, Goa, Indore, Bilaspur, Katihar, and Bareilly. The new stores, located in shopping malls and high-street areas, each span over 1,000 sq. ft and offer customers a curated range of denim products and accessories. With the addition of these stores, Wrangler’s retail footprint in India grew to 58 exclusive brand outlets (EBOs), with over 80% retail stores located outside of tier-1 cities.

- September 2024: Levi’s expanded its retail footprint in Kerala with the launch of its largest store in the state. Located on MG Road in Kochi, the store spans 4,000 sq. ft. of retail space and offers a range of clothing, accessories, and footwear, featuring a classic Levi’s denim collection tailored for both men and women.

- June 2024: Levi Strauss & Co. opened its new store in New Delhi, India. Located within the Pacific Mall in Tagore Garden and spanning an impressive 9,150 square feet, the newest store in the fleet was both the largest Levi’s store in Asia to date as well as the brand’s largest mall store globally. It is the fifth-largest Levi’s store in the world.

Global Jeans Market Report Scope

Jeans are trousers or pants that are made from denim or dungaree cloth. The report's scope includes the different types of jeans offered in the market for men, women, and kids. The scope of the jeans market includes segmentation of the market into end-user, category, distribution channels, and geography. By end users, the market is segmented into men, women, and children. The market is also divided according to the category, which includes mass and premium. The market is segmented based on the distribution channel, including specialty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. Moreover, the study involves the global analysis of the main regions, such as North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts are based on value (in USD million).

By Type/Fit

| Regular Fit |

| Slim Fit |

| Skinny Fit |

| Bootcut |

| Flared |

| Others |

By End User

| Men |

| Women |

| Children |

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Specialist Stores |

| Online Retail Stores |

| Other Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type/Fit | Regular Fit | |

| Slim Fit | ||

| Skinny Fit | ||

| Bootcut | ||

| Flared | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Specialist Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global jeans market in 2026?

The jeans market size reaches USD 105.12 billion in 2026 with a 3.75% CAGR outlook to 2031.

Which region will add the most new denim sales by 2031?

Asia Pacific, propelled by a 5.45% CAGR, is forecast to contribute the biggest absolute growth through rising urban income and Western fashion adoption.

What is driving the shift toward premium denim?

Consumers rationalize higher price tags through durability, sustainability narratives, and status signaling, while DTC channels maintain margins and deliver personalized fits.

How will U.S. tariffs influence sourcing strategies?

The 120% duty on Chinese jeans is moving production toward Mexico, Turkey, Egypt, and other competitive hubs as brands pursue tariff-neutral supply chains.

Which distribution channel shows the fastest expansion?

Online retail is projected to post a 6.55% CAGR as virtual try-on, AI sizing, and flexible logistics reduce purchase friction.

What technology trends will shape denim innovation?

Graphene fibers for durability, laser finishing to cut water use, and AR-based virtual fitting rooms are set to redefine product performance and shopping experiences.

Page last updated on: