Erotic Lingerie Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.5 Billion |

| Market Size (2031) | USD 7.95 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

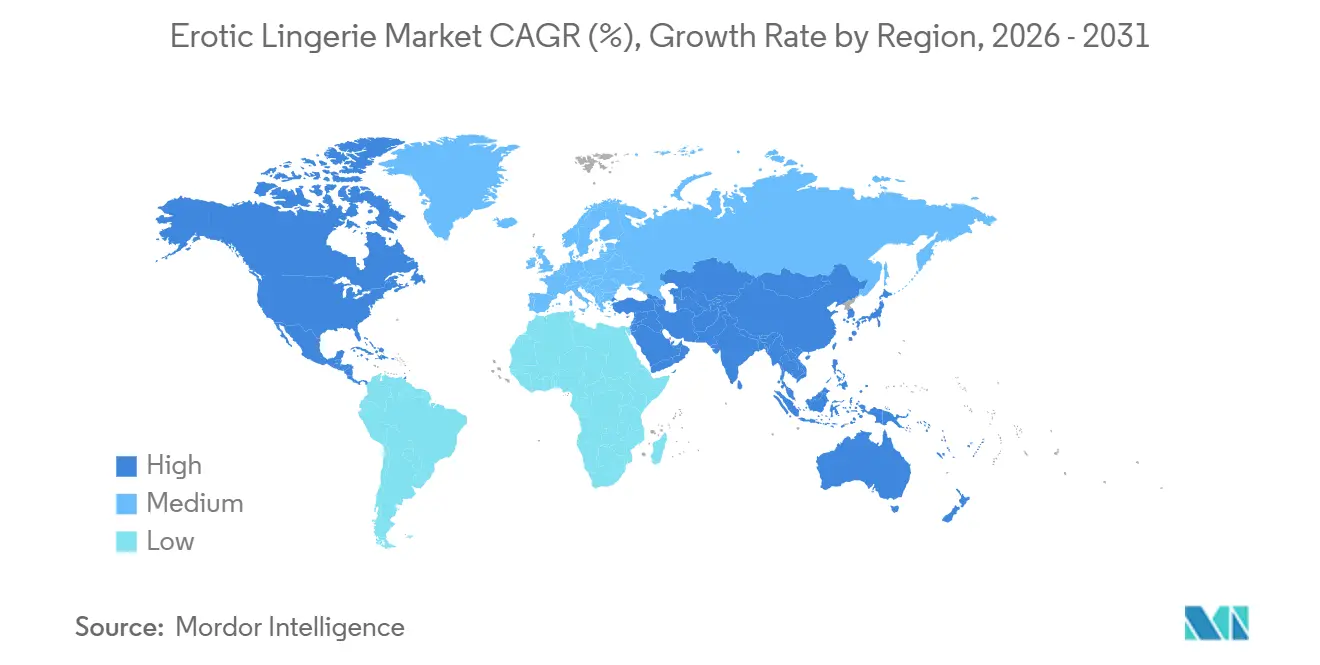

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

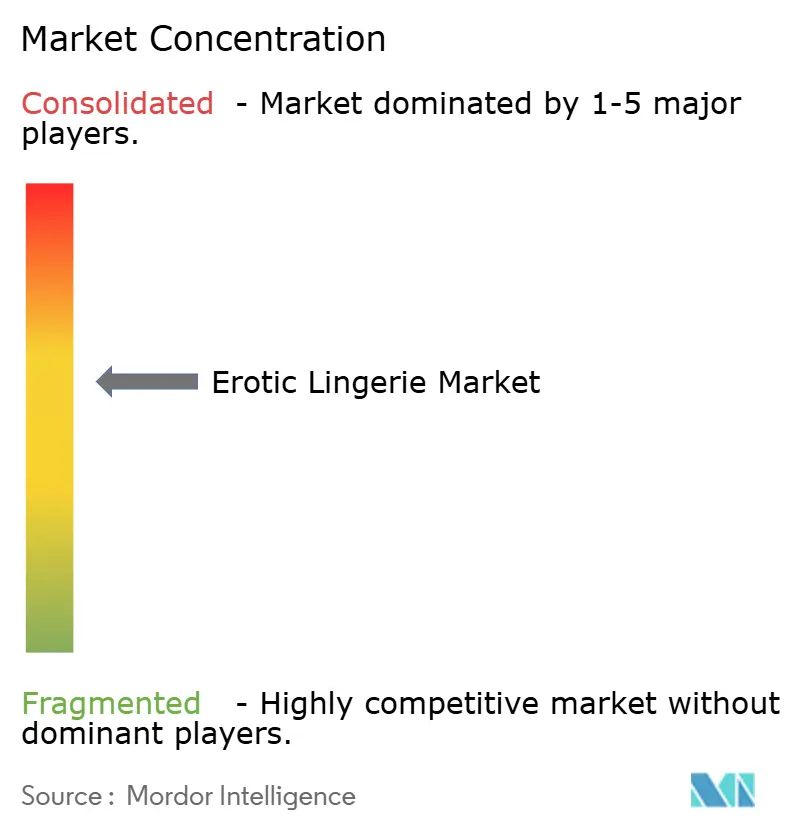

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Erotic Lingerie Market Analysis by Mordor Intelligence

The erotic lingerie market size was valued at USD 6.24 billion in 2025 and estimated to grow from USD 6.5 billion in 2026 to reach USD 7.95 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). This measured trajectory masks a structural realignment as direct-to-consumer insurgents leverage virtual fitting algorithms and influencer networks to capture share from heritage brands constrained by retail footprint and advertising codes. Europe commands 37.21% of 2025 revenue, yet Asia-Pacific will grow fastest at 5.27% annually through 2031, propelled by India's double-digit growth in 2025 and China's rising middle-class spending on premium intimate apparel. Direct-to-consumer insurgents continue to capture shelf space in physical and digital aisles, while celebrity collaborations help brands comply with stricter advertising codes by emphasizing empowerment over objectification. Wireless technology, smart fabrics, and size-inclusive patterns sharpen category differentiation, but counterfeit volumes and intense price competition still suppress margins across the global lingerie market.

Key Report Takeaways

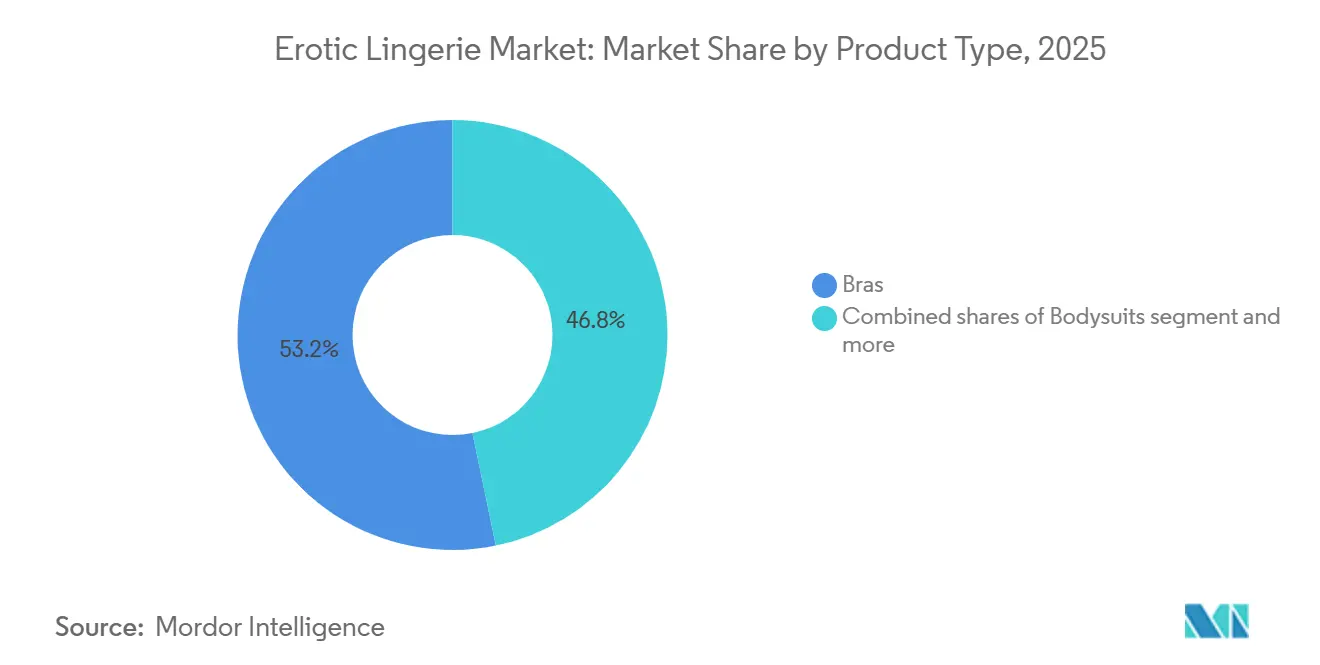

- By product type, bras held 53.22% of the lingerie market share in 2025, and bodysuits are forecast to expand at a 4.34% CAGR through 2031.

- By category, mass offerings captured 76.21% of the lingerie market size in 2025; premium lines are projected to register a 5.25% CAGR between 2026 and 2031.

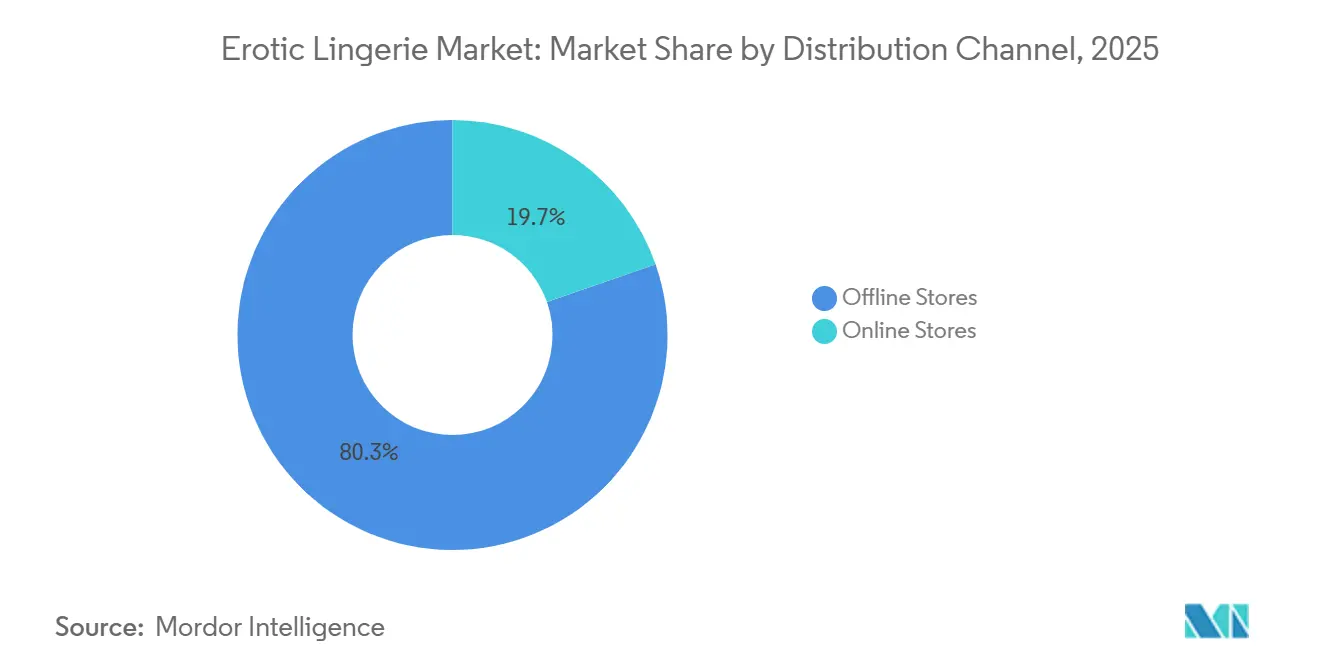

- By distribution channel, offline stores accounted for 80.34% of the lingerie market size in 2025. Online sales will advance at a 6.05% CAGR to 2031.

- By geography, Europe led with 37.21% revenue contribution in 2025, while Asia-Pacific is poised for a 5.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Erotic Lingerie Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Body positivity expanding consumer size inclusivity | +0.8% | Global, with accelerated adoption in Middle East (GCC markets via Ann Summers expansion March 2025) and Asia-Pacific | Medium term (2-4 years) |

| Shifting cultural acceptance of intimate apparel | +1.0% | North America and Europe core, spillover to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Social media and influencer marketing impact | +0.9% | Global, TikTok-led in North America and Europe, Instagram dominance in Asia-Pacific | Short term (≤ 2 years) |

| Virtual fitting tech improving online fit confidence | +0.7% | North America and Europe early adoption, Asia-Pacific rapid scaling post-2026 | Medium term (2-4 years) |

| Celebrity collaborations boosting brand visibility | +0.5% | Global, with highest ROI (Return on Investment) in North America and Europe markets | Short term (≤ 2 years) |

| Growth of online retail and e-commerce | +0.6% | Global, led by Asia-Pacific mobile commerce and North America omnichannel strategies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Body positivity expanding consumer size inclusivity

Size inclusivity has transitioned from a niche differentiator to a baseline expectation. Savage X Fenty's bra range spans 32A to 46DDD, and underwear extends from XS to 4X, a spectrum that legacy players struggled to match until Victoria's Secret expanded its sizing in 2024 following activist investor pressure from Brett Blundy's BBRC. Wacoal's December 2024 acquisition of Lively for USD 85 million plus contingent payments up to USD 55 million reflects incumbents' recognition that organic innovation lags direct-to-consumer agility in serving diverse body types. The shift also extends to adaptive designs for mastectomy patients and gender-affirming styles, segments that command premium pricing and foster brand loyalty. Retailers report that inclusive sizing drives higher average transaction values as customers purchase multiple items once they find a reliable fit.

Social media and influencer marketing impact

Social media and influencer marketing significantly boost the erotic lingerie market by amplifying brand visibility and shaping consumer preferences through visually engaging content on platforms like Instagram, TikTok, and Pinterest. Influencers lend authenticity and social proof, often increasing trust and driving purchase decisions more effectively than traditional ads, with promoted items sometimes seeing notably higher conversion rates. Their partnerships help normalize intimate apparel, connect brands with diverse audiences, and foster communities centered on body positivity and self-expression. Interactive campaigns, user-generated content, and targeted ads also deepen engagement and loyalty, making social channels key drivers of trend adoption and sales growth in this niche.

Virtual fitting tech improving online fit confidence

Virtual fitting algorithms reduce return rates, addressing e-commerce's persistent friction point. Google's virtual try-on tool, launched in 2024, uses generative AI to render garments on diverse body types, enabling shoppers to visualize fit before purchase. Victoria's Secret deployed NetVirta's 3D body-scanning technology in 2024, allowing customers to input measurements via smartphone camera and receive size recommendations with maximum accuracy. Fit:Match's AI engine analyzes purchase history and return patterns to predict optimal sizing, a capability adopted by Adore Me's partnership with Veesual in 2024, which introduced augmented-reality try-ons that overlay bras and briefs onto live video feeds, driving an uplift in conversion rates. These tools also surface demand signals: Brarista's AI detected a 40% surge in requests for wireless bras sized 34DD to 38G in Q1 2025, prompting inventory rebalancing that cut stockouts.

Shifting cultural acceptance of intimate apparel

Intimate apparel has migrated from private necessity to public fashion statement, evidenced by Ann Summers' March 2025 partnership with Liwa Trading Enterprises to enter Gulf Cooperation Council markets, launching its first standalone Middle East store in July 2025, and the knickerbox.ae e-commerce platform. This expansion into regions historically constrained by modesty norms signals that younger cohorts prioritize self-expression over convention. Victoria's Secret revived its fashion show in October 2024 after a six-year hiatus, recalibrating the event to feature diverse body types and age ranges rather than a singular aesthetic. The UK (United Kingdom) Advertising Standards Authority issued updated guidance in 2024, prohibiting sexualized imagery, objectification, and harmful body-image stereotypes, compelling brands to reframe campaigns around empowerment and inclusivity[1]Source: Advertising Standards Authority (ASA), "Updated Guidance in 2024", asa.org.uk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High premium product prices deter some buyers | -0.6% | Global, most acute in price-sensitive Asia-Pacific and Latin America markets | Medium term (2-4 years) |

| Restrictive advertising regulations hinder promotions | -0.4% | Europe (UK ASA codes), North America (platform content policies) | Short term (≤ 2 years) |

| Counterfeit products undermine brand trust | -0.5% | Asia-Pacific manufacturing hubs, Middle East distribution networks | Long term (≥ 4 years) |

| Intense competition reduces differentiation opportunities | -0.7% | Global, concentrated in North America and Europe saturated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High premium product prices deter some buyers

Premium lingerie pricing, often USD 100 to 300 per piece, limits addressable market penetration. La Perla filed for bankruptcy and cycled through ownership by Tennor Holding and Sapinda Asia, struggling to justify luxury price points amid direct-to-consumer alternatives priced lower. Victoria's Secret's premium tier, priced at USD 75 to 150, captured only a small share of its 2025 sales mix, with mass-market offerings at USD 30 to 50 driving volume. Economic headwinds in Europe, where inflation averaged 3.2% in 2025, shifted consumer spending toward essentials, compressing discretionary budgets for intimate apparel, according to the Eurostat[2]Source: Eurostat, "EU Key Indicators", ec.europa.eu . Brands respond by introducing tiered collections: Intimissimi's core line ranges from USD 20 to 60, while its limited-edition collaborations reach USD 120, a strategy that preserves aspirational positioning without alienating price-conscious shoppers.

Restrictive advertising regulations hinder promotions

The UK (United Kingdom) Advertising Standards Authority's 2024 guidance prohibits sexualized imagery, objectification, and body-shaming tropes, banning campaigns that present intimate apparel as tools for male approval or feature models in submissive poses. Brands must now emphasize comfort, functionality, and self-expression, narratives that resonate less with impulse purchases driven by aspiration. Social-media platforms enforce similar content policies: Instagram restricts nudity even in commercial contexts, requiring brands to blur or crop images that show nipples or genitalia, reducing visual impact. These constraints advantage influencer marketing, where peer-to-peer recommendations bypass formal advertising channels, yet smaller brands lack the budgets to activate large influencer networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By product type: bodysuits redefine intimate apparel

Luxury fashion houses embedding bodysuits into ready-to-wear collections propel the segment to 4.34% CAGR through 2031, the fastest pace across all product categories. Bras retain 53.22% of 2025 market share, anchored by wireless innovations that blend comfort with support. MIT's fiber-computer prototypes integrate sensors for breast-cancer monitoring, and Wacoal introduced moisture-wicking, temperature-regulating fabrics in 2024. Sustainable materials gain traction: ECONYL regenerated nylon, organic cotton certified by GOTS (Global Organic Textile Standard) (requiring 70% organic content minimum), and bamboo fibers reduce environmental impact while commanding 15% to 25% price premiums over [3]Source: GOTS (Global Organic Textile Standard), " Sustainable Materials", global-standard.org.

Bodysuits' ascent reflects their versatility, worn alone as tops or layered under blazers, and their flattering silhouette that eliminates tucking and bunching. Brands capitalize by expanding size ranges: Savage X Fenty offers bodysuits from XS to 4X, while Wolford's seamless construction accommodates diverse body types without visible lines. Briefs remain foundational, yet innovation stalls beyond fabric improvements like modal blends and laser-cut edges. Corsets and bustiers, once relegated to special occasions, resurge as outerwear in Gen Z wardrobes, driven by TikTok styling tutorials that amassed 2.3 billion views in 2025. Bras face technical challenges in wireless designs: balancing support for larger cup sizes (DD and above) without underwire requires advanced engineering, a capability that separates premium brands like ThirdLove from mass-market imitators.

By category: premium tier outpaces mass despite smaller base

Premium lingerie will expand at a 5.25% CAGR through 2031, as consumers prioritize quality, sustainability, and size inclusivity over price. Mass-market offerings dominate with 76.21% of 2025 sales, yet direct-to-consumer brands like Savage X Fenty and ThirdLove demonstrate that premium positioning, USD 50 to 150 per item, resonates when paired with extended sizing and ethical production. La Perla's bankruptcy and Agent Provocateur's private-equity struggles illustrate that ultra-luxury pricing, USD 200 to 500, requires brand heritage and retail theater that newer entrants lack. Wacoal's December 2024 acquisition of Lively for USD 85 million plus contingent payments signals incumbents' recognition that premium growth lies in accessible luxury rather than rarefied exclusivity.

Certifications differentiate premium players: GOTS organic cotton, Bluesign chemical management, Fair Trade labor standards, and OEKO-TEX (International Association for Research and Testing in the Field of Textile and Leather Ecology) textile safety add credibility that justifies higher prices. Organic Basics, Pact, Boody, Knickey, Girlfriend Collective, LIVELY, Naja, and Underprotection embed these credentials into brand narratives, converting sustainability-conscious consumers willing to pay premiums. Premium brands also invest in customer experience: virtual fitting consultations, personalized sizing algorithms, and hassle-free returns reduce purchase friction. ThirdLove's Fitting Room Quiz, completed by 15 million users, captures fit preferences and recommends styles, a data asset that informs product development and inventory allocation.

By distribution channel: offline dominance erodes as digital tools mature

Offline stores command 80.34% of 2025 sales, yet online channels will grow at 6.05% CAGR through 2031, driven by virtual fitting technologies that resolve e-commerce's historical fit-confidence gap. Victoria's Secret operates 1,404 stores globally as of November 2025, 792 company-operated, 545 partner-operated, 63 in China via joint venture, and 4 Adore Me locations, yet the brand's Q3 2025 digital sales rose year-over-year, outpacing brick-and-mortar growth of 6%. Savage X Fenty's omnichannel strategy blends direct-to-consumer e-commerce with selective retail partnerships: August 2024 Nordstrom placement across 16 stores and Nordstrom.com, September 2024 Selfridges shop-in-shop on Oxford Street, and December 2024 announcement of 6 new US stores in Chicago, Long Island, Atlanta, Detroit, St. Louis, and Newark.

Mobile commerce dominates in Asia-Pacific, where the majority of lingerie transactions occur via smartphone, facilitated by payment integrations with Alipay and WeChat Pay. Subscription models generate recurring revenue: Adore Me's membership program, offering monthly credits and free shipping, retained most of its subscribers beyond the first year. Offline stores remain critical for initial fit discovery, the majority of first-time lingerie buyers prefer in-person consultations, yet subsequent purchases migrate online once sizing is established. Retailers experiment with hybrid formats: Victoria's Secret's October 2025 NYC pop-up combined physical try-ons with QR-code links to shoppable Instagram Reels, converting foot traffic into digital followers.

Geography Analysis

Europe holds 37.21% of 2025 revenue, reflecting mature markets where per-capita lingerie spending averages USD 85 annually, yet Asia-Pacific will expand at 5.27% CAGR through 2031 as rising incomes and cultural shifts unlock latent demand. The broader Asia-Pacific underwear segment, encompassing lingerie, basics, and shapewear, includes contributions from China, India, Japan, Australia, Indonesia, South Korea, Thailand, and Singapore. Wacoal launched in India in 2024, targeting the premium tier with bras priced at INR 2,000 to 4,000, a range that balances aspiration with affordability.

North America, the United States, Canada, and Mexico benefit from direct-to-consumer innovation and influencer-driven discovery, yet face headwinds from department-store closures that historically anchored lingerie distribution. South America (Brazil, Argentina, Colombia, Chile, Peru) and Middle East and Africa (South Africa, Saudi Arabia, UAE (United Arab Emirates), Nigeria, Egypt, Morocco, Turkey) represent emerging opportunities: Ann Summers' March 2025 GCC (Gulf Cooperation Council) partnership with Liwa Trading Enterprises launched knickerbox.ae and a standalone store in July 2025, testing cultural receptivity in markets where intimate apparel traditionally remained private.

In Asia-Pacific, rapid urbanization, expanding middle-class wealth, changing cultural perceptions, and booming online retail make it the fastest-growing market. Latin America sees increasing demand as social media influence, urbanization, and improved digital access expand fashion consciousness. In the Middle East and Africa, growth is emerging from rising urban incomes, greater internet penetration, and discreet online sales that bypass cultural sensitivity barriers. Collectively, these regional drivers reflect economic development, digital adoption, and evolving cultural norms toward self-expression and personal style.

Regulatory Landscape

Erotic lingerie sold into major markets is governed primarily by apparel safety, chemical, labeling, and advertising-content rules, which affect both product design and go-to-market execution. In the United States, the Consumer Product Safety Commission enforces flammability requirements for clothing textiles under the Flammable Fabrics Act (16 CFR Part 1610), and importers must maintain compliance documentation such as a General Certificate of Conformity for general-use apparel. These requirements shape fabric selection, trims, and quality control processes, particularly for lace, mesh, and synthetic blends common in erotic lingerie.

In Europe, market entry is anchored in product safety and chemical restrictions, with REACH Annex XVII influencing allowable substances in textiles and components, including metal hardware. The region is also moving toward stronger circularity and traceability obligations for textiles: the European Commission published a technical study in May 2026 on Digital Product Passport content for textile apparel under the Ecodesign for Sustainable Products Regulation (ESPR) framework, and an EU-wide ban on the destruction of unsold textiles and footwear for large enterprises is slated to begin in July 2026. Alongside advertising constraints such as the UK Advertising Standards Authoritys updated 2024 guidance limiting sexualized imagery and harmful stereotypes, these shifts push brands toward more rigorous compliance documentation, inventory disposition planning, and empowerment-led creative that remains platform-compliant.

Competitive Landscape

The lingerie sector's concentration index reflects moderate consolidation, where direct-to-consumer insurgents leverage virtual fitting algorithms and influencer networks to capture share from incumbents constrained by retail footprint and advertising codes. Savage X Fenty's January 2024 funding round supported its expansion into Nordstrom's 16 stores by August 2024, blending direct-to-consumer agility with selective retail partnerships. Wacoal's December 2024 acquisition of Lively for USD 85 million plus contingent payments up to USD 55 million exemplifies incumbents buying rather than building innovation.

White-space opportunities emerge in adaptive designs for mastectomy patients, gender-affirming styles, and post-pregnancy recovery wear, segments commanding premiums yet underserved by legacy players focused on aesthetic-driven collections. Technology separates winners from laggards: Google's virtual try-on tool, NetVirta's 3D body scanning, and Bold Metrics' AI-powered sizing reduce return rates, converting browsers into buyers. MIT's fiber-computer prototypes, capable of breast-cancer monitoring, and Wacoal's smart fabrics integrating moisture-wicking and temperature regulation, illustrate how technical innovation extends beyond fit to health and wellness.

Sustainability certifications, GOTS organic cotton (70% minimum), Bluesign chemical management, Fair Trade labor standards, differentiate premium players like Organic Basics, Pact, and Knickey, yet add USD 5 to 15 per unit in production costs, compressing margins in price-sensitive categories. Emerging disruptors bypass traditional retail entirely: ThirdLove's direct-to-consumer model eliminates wholesale markups, enabling USD 68 bras versus department-store equivalents at USD 90 to 120.

Erotic Lingerie Industry Leaders

-

Victoria's Secret

-

Zivame

-

Chantelle Group

-

Adore Me

-

CLO intimo

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digitization across design-to-manufacturing creates whitespace for faster iteration, better fit outcomes, and lower waste in intimate apparel, supporting differentiation in erotic lingerie where fit, comfort, and aesthetics intersect. Evidence of this operational shift shows up in production and product development tooling: a 2026 academic study on intimate-apparel new product development highlights the role of 3D CAD in reducing sample iterations and accelerating fit decisions, while seamless circular knitting is being adopted to reduce cut-and-sew waste by producing near-finished garments directly from yarn. These capabilities align with the categorys momentum in wireless and comfort-led construction, helping brands refresh assortments without relying on restricted ad creatives.

On the supply side, manufacturers are investing in data-led costing and efficiency programs that allow tighter price architecture across mass and accessible-premium lines. In May 2026, PT Globalindo Intimates adopted Coats Digitals GSDCost solution to improve costing accuracy and production efficiency, reinforcing a broader move toward digital production management that supports shorter lead times and more responsive replenishment. On the demand side, online growth is being enabled by algorithm-driven fit recommendations and digital body-scanning to reduce returns, complementing brand initiatives such as Victorias Secret deployment of 3D body-scanning technology and Googles virtual try-on tool introduced in 2024. In parallel, EU sustainability and traceability direction under ESPR and the emerging Digital Product Passport framework elevates opportunities for brands and suppliers that can document materials, component compliance, and product provenance in a scalable way.

Recent Industry Developments

- July 2026: Chantelle marked its 150th anniversary at an event in London and previewed limited-edition anniversary lingerie sets slated for an August launch. The milestone activation reinforces brand heritage and provides a platform to spotlight premium collections in a crowded intimates landscape where newer entrants compete heavily on social-first discovery.

- May 2026: Chantelle introduced the Magique Collection, including the Magique Wireless Support Bra and the Magique Back Smoothing Minimizer. The launch emphasizes functionality-led lingerie design, supporting demand for comfort and versatility that translates across everyday intimates and erotic-adjacent styling.

- April 2026: Victorias Secret rolled out a global The Season of Strapless campaign alongside the Invisible by Victoria Strapless Collection. The collection-and-campaign pairing supports high-volume seasonal merchandising while staying within tighter advertising and platform content policies by leaning into wardrobe utility and fit innovation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from erotic lingerie products sold through online and offline channels, where the main purpose is intimate and sensual wear rather than everyday basics.

Scope exclusions: We exclude general everyday lingerie and innerwear that is not positioned and marketed as erotic.

Segmentation Overview

-

Product Type

- Bras

- Briefs

- Bodysuits

- Other Types

-

Category

- Mass

- Premium

-

Distribution Channel

- Offline Stores

- Online Stores

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a simple fact base on apparel and intimatewear demand, retail sales direction, and cross border trade flows that influence product availability. For this, we used public sources such as U.S. Census Bureau retail data, UN Comtrade trade statistics, Eurostat, OECD consumer and price indicators, and World Bank macro series, which help anchor the demand environment.

After that, we reviewed company annual reports, investor presentations, earnings call transcripts, and brand and retailer press releases to understand category positioning and pricing moves. In parallel, we used paid company financials and intelligence databases for consistent company profiles and historical financial context, and we also checked import export shipment level databases to sanity check sourcing intensity for key manufacturing corridors. This list is illustrative only, and many other public and paid sources were also referenced to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure test what we saw in desk research, especially on how erotic lingerie is defined in catalogs, what pricing bands move fastest, and how online versus specialty retail affects realized revenue. We spoke with executives, category leaders, and managers across key regions so that demand signals, channel mix, and typical discounting behavior could be confirmed and then reflected back into the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 47% |

| Mid tier: 55% | Functional/Unit leaders: 38% | EMEA: 32% |

| Smaller Players: 18% | Managers: 46% | Americas: 21% |

Market-Sizing & Forecasting

Market size was built using a top-down approach where consumer spending signals and apparel and intimatewear category splits were used to reconstruct an addressable revenue pool, which was then adjusted using channel mix evidence. To keep the result grounded, we corroborated totals with selective bottom-up approximations, such as sampled price points multiplied by observed unit movement proxies from retailer activity and supplier and distributor checks.

Key inputs used in the model included online share of intimatewear sales, average selling price ranges by product style (for example bodysuits, babydolls, thongs, and erotic bras), frequency and depth of promotional cycles, regional disposable income and inflation direction, and cross border import intensity for relevant apparel categories. Where direct volume signals were thin in a country, gaps were handled by using a closest-market proxy based on retail structure and income bands, and then recalibrated through interview feedback.

Forecasting relied mainly on scenario analysis supported by a light multivariate regression, so the forward view could flex with macro variables and channel shifts while still staying explainable. Assumptions on ASP progression and online penetration were reviewed with industry respondents, and then applied consistently across the forecast years.

Data Validation & Update Cycle

Outputs were checked against independent signals such as category growth rates, trade movement direction, and major channel performance cues, and then any large variances were traced back to the specific assumption that caused them. When an outlier appeared, we either revisited the desk inputs or re-contacted a relevant respondent group to confirm whether a change was structural or temporary.

Before sign-off, the model and narrative go through multiple analyst reviews so that arithmetic, unit logic, and year alignment are consistent across sections. Reports are refreshed annually, with interim updates triggered by material events that can shift pricing, channel mix, or demand. Right before delivery, a final review pass is done so clients receive the latest updated view.

Mordor Intelligence's Erotic Lingerie Market Size Versus Other Published Estimates

Published market size numbers for erotic lingerie often do not match, and the gap is usually not a math error. Differences typically come from what gets counted as erotic lingerie versus general lingerie, how online discounts and premium pricing are treated in ASP assumptions, and how fast the model is refreshed when consumer sentiment changes.

The other big driver is scope blending, where some estimates roll in broader intimate apparel, adjacent apparel categories, or wider lifestyle products, which pushes totals up quickly. Currency conversion timing and whether figures are reported as manufacturer value or retail value also matter, and they can move the headline number even if unit demand is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.24 B (2025) | |

| Global Consultancy A | USD 22.66 B (2024) | The published scope appears to be much broader, with end-user and channel cuts that can pull in wider intimatewear demand and higher retail-value pricing, which inflates totals versus a narrower erotic-only definition. The base year and forecast window differ, so currency timing and inflation treatment can also shift the stated value. |

| Industry Research Group B | USD 23.03 B (2025) | The estimate is presented with wide segmentation and long-range forecasts, but the summary does not disclose the underlying calculation steps, which makes it hard to see whether everyday lingerie or adjacent categories are included. Limited visibility on ASP build-up and discounting assumptions can lead to a much larger market number. |

The table shows a large spread, and in Mordor Intelligence's model the total is tied to erotic lingerie products as a defined subset rather than being expanded into the full lingerie category or adjacent intimatewear demand. Once scope, pricing logic, and year alignment are kept consistent, the resulting market value becomes easier to trace back to clear demand and channel variables, and it is simpler to update when new signals emerge.

Key Questions Answered in the Report

How large will the lingerie market be by 2031?

The lingerie market is projected to reach USD 7.95 billion by 2031, advancing at a 4.11% CAGR from 2026 to 2031.

Which product segment is growing the fastest?

Bodysuits lead with a forecast 4.34% CAGR through 2031 as luxury houses reposition them as outerwear essentials.

Why is Asia-Pacific considered the key growth region?

Rising incomes, cultural liberalization, and mobile-commerce penetration give Asia-Pacific a 5.27% CAGR, outpacing mature Western markets.

How are brands tackling high return rates in online sales?

Companies deploy virtual fitting solutions such as 3D scanning and AI-generated try-ons, which cut returns by up to 40%.

Page last updated on: