Respiratory Disease Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 7.48 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Disease Testing Market Analysis by Mordor Intelligence

The Respiratory Disease Testing Market size is projected to expand from USD 6.04 billion in 2025 and USD 6.24 billion in 2026 to USD 7.48 billion by 2031, registering a CAGR of 3.69% between 2026 to 2031.

An entrenched installed base of multiplex molecular platforms, combined with post-pandemic vigilance for coinfections, continues to anchor routine diagnostic demand. However, procurement normalization is pushing laboratories toward leaner inventory models, pressuring reagent suppliers to adopt just-in-time distribution. Fast-maturing reimbursement pathways for AI-enabled image and spirometry analytics are improving clinical productivity, widening the addressable patient pool, and smoothing pay-for-performance revenue streams. At the same time, escalating workplace air-quality regulations across Asia-Pacific and stricter FDA sensitivity thresholds for rapid antigen tests are recalibrating product pipelines and pricing strategies. Competitive focus is therefore shifting from single-analyte throughput toward integrated ecosystems that fuse hardware, consumables, and cloud analytics into subscription-style offerings.

Key Report Takeaways

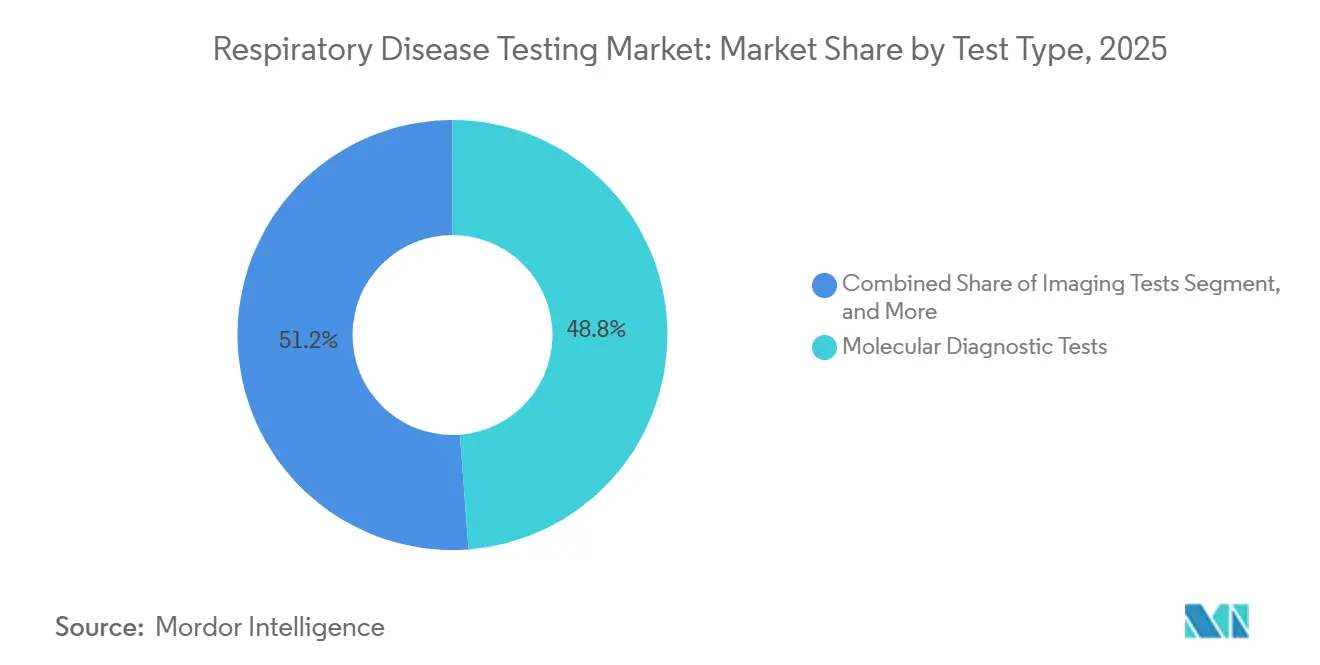

- By test type, molecular diagnostic platforms captured 48.82% of 2025 respiratory disease testing market share, while mechanical tests are advancing at the fastest 4.06% CAGR to 2031.

- By disease, influenza & RSV panels retained 35.27% revenue share in 2025, whereas lung-cancer assays are poised for a leading 6.63% CAGR through 2031.

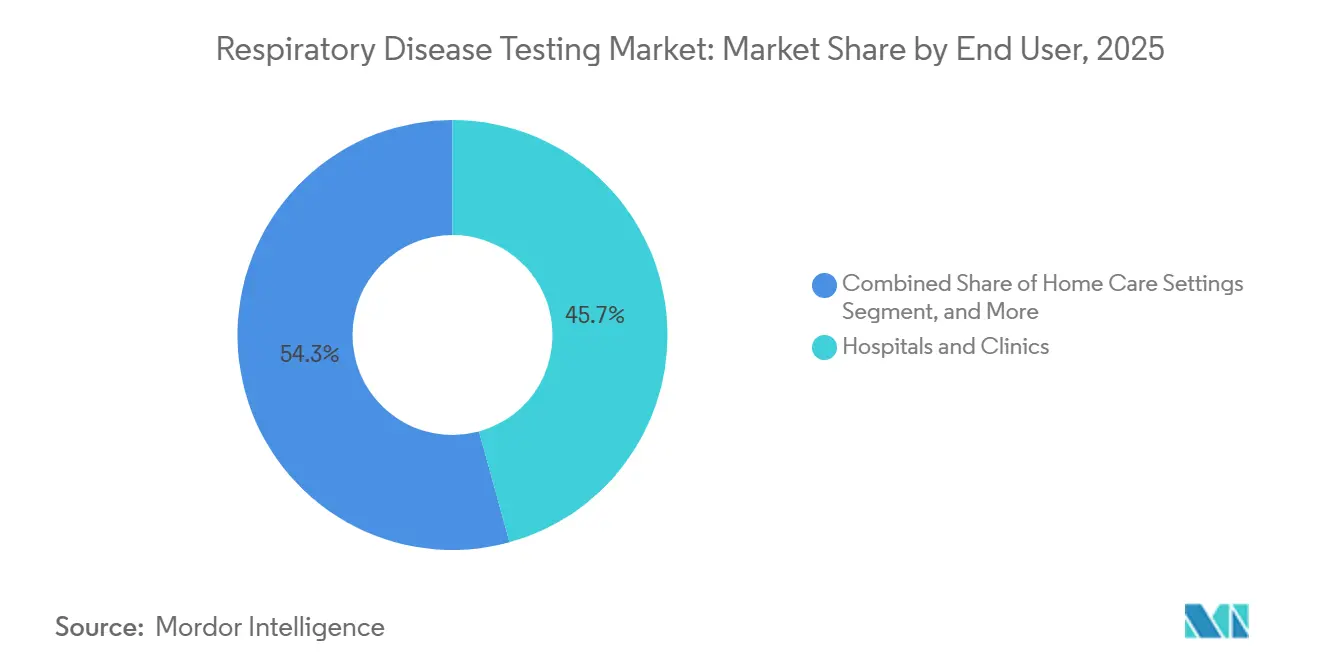

- By end user, hospitals and clinics accounted for 45.72% of the 2025 respiratory disease testing market, but home-care settings are growing at 5.18% through 2031.

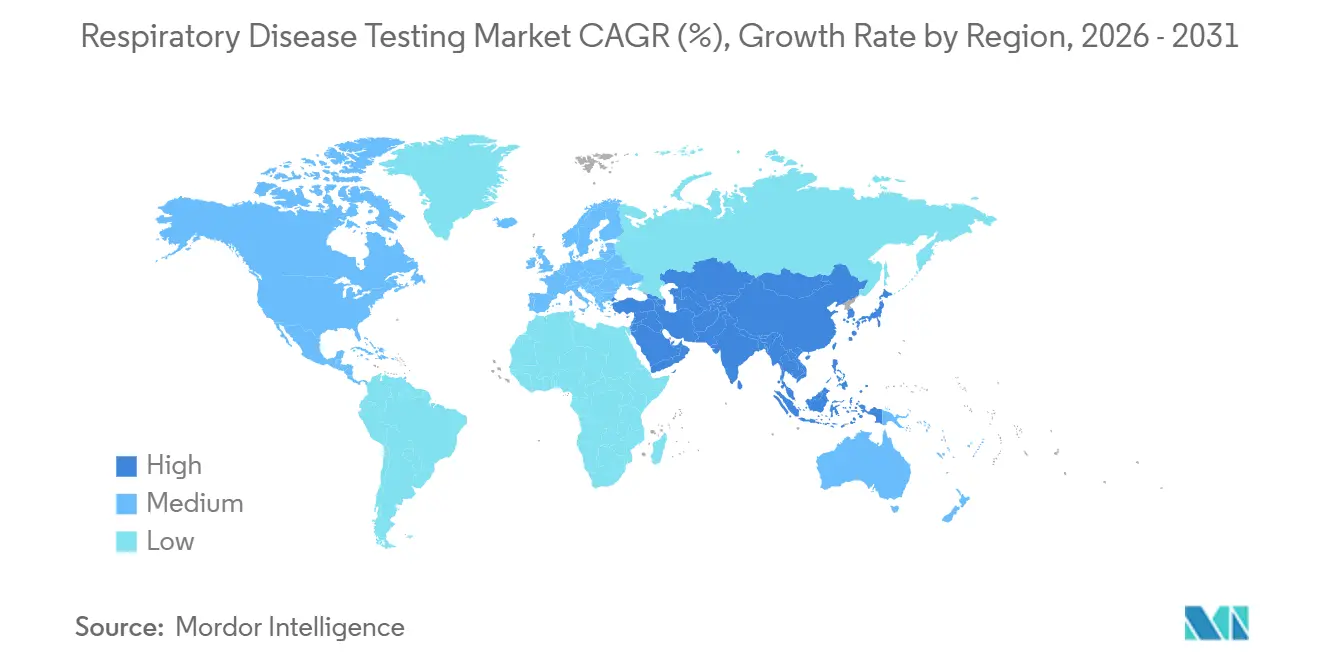

- By geography, North America dominated with a 43.08% share in 2025; Asia-Pacific is set to register the quickest 7.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Respiratory Disease Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Air-Quality Regulation–Fuelled Demand Surge | +0.8% | Asia-Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| Post-COVID Era Stockpiling of Multiplex Panels | +0.5% | North America & Europe | Short term (≤2 years) |

| Hospital Decanting to Home/POC Settings | +0.7% | Global, early gains in North America & Western Europe | Long term (≥4 years) |

| AI-Assisted Image & Spirometry Analytics Adoption | +0.6% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Digital-Diagnostic Data Mandates | +0.4% | Europe, North America | Medium term (2-4 years) |

| Climate-Linked Pathogen Seasonality Shifts | +0.3% | Global, pronounced in temperate zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Air-Quality Regulation–Fuelled Demand Surge

Strengthening particulate-matter limits across China and India requires mandatory spirometry for industrial workers, driving bulk purchases of portable devices and associated disposables.[1]Source: 360Dx, “Labs Find Reimbursement Process Becoming a Herculean Task,” 360dx.com Enterprises are choosing bundled contracts that include hardware, calibration services, and cloud dashboards, enabling vendors to lock in recurring revenue. Real-time AI coaching embedded in modern spirometers reduces dependence on scarce technicians and extends screening into tier-2 cities. This expansion is widening the footprint of the respiratory disease testing market among employer health programs. Device makers that localize manufacturing close to Asian hubs are capturing cost advantages and faster regulatory clearance.

Post-COVID Era Stockpiling of Multiplex Respiratory Panels

Hospital preparedness grants in the United States and bulk buys in Europe lifted molecular-panel shipments by nearly one-fifth during 2024 to early 2025.[2]Source: FDA, “Laboratory Developed Tests Regulatory Impact Analysis,” fda.gov By mid-2025, consumption normalized to roughly two-thirds of installed capacity, triggering an abrupt drawdown of surplus inventory. Laboratories are now pivoting toward modular syndromic panels that combine respiratory, gastrointestinal, and central nervous system targets to retain capital utilization. The swing exposed supply-chain fragilities and prompted reagent makers to roll out auto-refill programs matched to real-time analyzer telemetry, a service model that is becoming table stakes in the respiratory disease testing market.

Hospital Decanting to Home/POC Settings

Parity laws for telehealth reimbursement and Medicare billing codes 99457 and 99458 now compensate providers for reviewing remote lung-function data, encouraging migration of COPD and asthma monitoring into living rooms.[3]Centers for Medicare & Medicaid Services, “2025 Medicare Physician Fee Schedule Final Rule,” cms.gov Integrated ecosystems from ResMed and Philips bundle connected inhalers, spirometers, and coaching portals that feed care-team dashboards. Monthly device-as-a-service fees convert one-off instrument sales into annuity streams, a transformation reshaping end-user economics in the respiratory disease testing market. Private insurers increasingly tie bonuses to avoided readmissions, boosting adoption of at-home diagnostics that provide early exacerbation alerts.

AI-Assisted Image & Spirometry Analytics Adoption

FDA-cleared AI modules for chest CT scans and spirometry quality control are shrinking report turnaround times from days to minutes. Algorithms flag suboptimal patient efforts or suspicious nodules, standardize thresholds, and push structured results into electronic medical records. Early deployments lifted first-attempt spirometry success rates by more than one-fifth and trimmed radiologist workload in high-volume lung-cancer screening centers. Vendors that license algorithms on a per-scan or per-test basis are layering novel revenue lines atop equipment sales, adding defensible differentiation in the congested respiratory disease testing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Headwinds for Advanced Molecular Panels | -0.6% | North America, select Europe | Short term (≤2 years) |

| Shortage of Trained Pulmonary-Lab Personnel | -0.4% | Global, acute in rural North America & emerging Asia-Pacific | Medium term (2-4 years) |

| Consumable-Grade Polysilicone Supply Bottlenecks | -0.3% | Global, pronounced in North America & Europe | Short term (≤2 years) |

| Antigen-Test Sensitivity Scrutiny by Regulators | -0.2% | North America, Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Headwinds for Advanced Molecular Panels

CMS lowered the 2025 national limitation amount for CPT 87631 respiratory panels by 12%, and private payers layered on prior-authorization hurdles, curbing uptake outside inpatient walls. Laboratories are downgrading to 3-to-5-target assays that fit tighter cost ceilings, eroding absolute revenue per sample. The margin squeeze is widening the gap between large hospital networks, which dilute overhead across higher volumes, and stand-alone clinics, which cannot amortize instrument investments as quickly. Tiered pricing tied to medical-necessity documentation is emerging as a short-term mitigation lever.

Shortage of Trained Pulmonary-Lab Personnel

The United States faces a deficit of up to 15,000 certified respiratory therapists, while India counts fewer than 2,000 ISO-compliant spirometry technicians for 1.4 billion people. Staffing gaps limit throughput and extend appointment backlogs, especially in rural geographies. Vendors are embedding AI-guided coaching and remote proctoring features that let a single therapist supervise multiple parallel tests, trimming labor needs. However, slow enrollment in training programs suggests shortages will persist through at least 2029, acting as a structural drag on mechanical-test expansion in the respiratory disease testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Panels Lead, Mechanical Tests Accelerate

Molecular diagnostics accounted for 48.82% of 2025 respiratory disease testing market revenue, underscoring decades of investment in automated PCR and isothermal platforms. Yet, mechanical tests are the fastest-growing slice, climbing 4.06% annually as primary-care providers bundle spirometry with routine checkups and employers meet new compliance rules. This upswing pushes the mechanical slice’s respiratory disease testing market size toward an incremental USD 0.56 billion over the forecast horizon. Vendors capitalizing on integrated Bluetooth spirometers coupled with AI coaching stand to outpace peers on both unit volumes and SaaS margins.

Targeted reimbursement policies bolster the shift. A Grade B USPSTF endorsement for COPD screening mandates insurer coverage of spirometry without patient cost-sharing. In parallel, lower-priced pathogen-specific PCR assays are cannibalizing broad syndromic panels, compressing molecular average selling prices by roughly 4% to 6% each year. Imaging tests continue to benefit from AI-triaged CT workflows, drawing community centers into lung-cancer screening programs and expanding downstream biopsy referrals, but they trail mechanical modalities in absolute growth velocity within the respiratory disease testing market.

By Disease: Influenza & RSV Dominate, Lung Cancer Surges

Influenza and RSV panels accounted for 35.27% of 2025 segmental revenue, cementing their seasonal centrality in the respiratory disease testing market. Lung-cancer assays, however, are on track for a 6.63% CAGR through 2031 thanks to broadened low-dose CT eligibility and FDA-approved liquid-biopsy panels that capture actionable mutations from a single blood draw. These liquid tests, when bundled with imaging follow-up, elevate the respiratory disease testing market share of oncology-oriented kits to heights previously unseen.

Tuberculosis remains program-driven, with India’s 2,400 additional GeneXpert machines lifting daily test capacity by over 30%. Asthma and COPD diagnostics deliver steady mid-single-digit growth, tied closely to chronic-care reimbursement. Price competition in rapid antigen formats continues to shave margins; yet, manufacturers that pivot toward semi-quantitative viral-load reporting are carving premium niches.

By End User: Hospitals Hold Share, Home Care Gains Momentum

Hospitals and clinics represented 45.72% of 2025 respiratory disease testing market size on the strength of high-complexity labs and imaging suites. Nevertheless, home-care settings chart the sharpest rise, with a 5.18% CAGR, driven by device connectivity, payer incentives, and consumer comfort with telehealth. Remote patient monitoring devices plug effortlessly into electronic health records, ensuring compliance with reimbursement requirements and generating subscription revenue streams that outlast hardware depreciation.

Independent diagnostic laboratories remain the second-largest cohort, using automation to reduce per-sample labor costs in the face of reimbursement cuts. Retail clinics and employer health centers, while fragmented, are important gateways for antigen and portable PCR tests, cementing multi-channel distribution models that underpin long-run resilience of the respiratory disease testing market.

Geography Analysis

North America commanded 43.08% of global revenue in 2025, underpinned by high insurance penetration, generous Medicare coding, and an FDA backlog-clearing spree that granted Breakthrough Device status to seven respiratory platforms over two years. While reimbursement reductions temper molecular margins, speed-to-market advantages keep innovation pipelines vibrant. Hospitals increasingly deploy rapid PCR analyzers at emergency-department triage stations, cutting antibiotic overuse and reinforcing demand for syndromic cartridges.

Europe contributes a mature yet innovation-friendly share of the respiratory disease testing market, navigating IVDR compliance turbulence to restore product breadth. Lung-cancer screening pilots in Germany and the United Kingdom are scaling to nationwide programs by 2028, promising steady CT and biomarker volumes. Conversely, national health payors enforce volume caps on high-plex PCR, driving labs toward algorithm-driven test utilization that maximizes clinical utility.

Asia-Pacific posts the quickest 7.27% CAGR, set to overtake Europe on absolute dollars by 2030. India’s Ayushman Bharat scheme now reimburses molecular TB testing and spirometry, bringing diagnostics to tier-3 towns. China’s National Healthcare Security Administration boosted syndromic-panel payment rates by 15% in 2025, unlocking provincial hospital budgets. Parallel air-pollution mandates increase COPD screening volumes, swelling the mechanical-test subset of the respiratory disease testing market.

Middle East & Africa and South America remain smaller but opportunity-rich. Gulf Cooperation Council members are funding flagship tertiary hospitals with on-site molecular labs, while Brazil’s private insurer market fuels retail-clinic expansion stocked with rapid antigen tests. Both regions import the bulk of their kits, presenting scale economies for global OEMs that establish regional assembly nodes.

Competitive Landscape

Market structure is moderately concentrated. Molecular diagnostics are oligopolistic due to high capital hurdles and proprietary cartridge ecosystems, whereas mechanical and point-of-care segments exhibit lower entry barriers, fostering vibrant challenger competition. Vertical integration trends see incumbents acquiring analytics startups to embed AI layers that boost switching costs and recurring returns across the respiratory disease testing market.

Technological differentiation serves as the primary offense. Roche’s 20-minute cobas Liat PCR carved out a premium share in urgent care, while Seegene’s 24-analyte Allplex panel reduced per-pathogen reagent costs by 40%, winning tenders in price-sensitive public hospitals. Emerging disruptors like Visby Medical are pursuing single-use PCR cartridges tailored for telehealth workflows, potentially revolutionizing the economics of at-home molecular testing. Regulatory frameworks also evolve; the FDA's 2025 draft guidance on AI-augmented software expedites clearance paths, compressing development cycles and catalyzing algorithm-feature races that redefine value capture in the respiratory disease testing market.

Strategic moves in 2025-2026 underscore geographic bets and SaaS layering. Abbott’s USD 160 million pickup of Cepheid’s respiratory portfolio expands its TB footprint in high-burden economies, while Siemens’ Atellica VTLi panel bolsters middleware-centric lab consolidation strategies. Thermo Fisher’s USD 120 million Bangalore plant localizes cartridge fabrication, shaving lead times and import duties to attack emerging-market price points. Collectively, these maneuvers indicate an arms race to secure reagent annuities, analytics stickiness, and regional cost leadership.

Respiratory Disease Testing Industry Leaders

Abbott Laboratories

Seimens Healthineers AG

Thermo Fisher Scientific Inc.

Qiagen N.V.

Becton Dickinson & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Roche introduced the cobas Respiratory flex 12-target PCR assay, enhancing comprehensive pathogen coverage in a single workflow.

- May 2024: Vyaire Medical completed the sale of its Respiratory Diagnostics business to Trudell Medical, ensuring product line continuity while Vyaire restructures under Chapter 11.

Global Respiratory Disease Testing Market Report Scope

As per the scope of the report, respiratory disease testing is used to diagnose respiratory conditions in an individual. Some respiratory diseases include chronic obstructive pulmonary disease, asthma, and infections such as bacterial pneumonia and enterovirus respiratory virus.

The Respiratory Disease Testing Market Report is Segmented by Test Type (Imaging Tests, Molecular Diagnostic Tests, Mechanical Tests, Blood-Gas & Electrolyte Tests), Disease (Asthma & COPD, Tuberculosis, Lung Cancer, Influenza & RSV, Other Respiratory Infections), End User (Hospitals & Clinics, Diagnostic Laboratories, Home Care Settings, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Imaging Tests |

| Molecular Diagnostic Tests |

| Mechanical Tests (PFT/Spirometry) |

| Blood-Gas & Electrolyte Tests |

| Asthma & COPD |

| Tuberculosis |

| Lung Cancer |

| Influenza & RSV |

| Other Respiratory Infections |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Home Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Imaging Tests | |

| Molecular Diagnostic Tests | ||

| Mechanical Tests (PFT/Spirometry) | ||

| Blood-Gas & Electrolyte Tests | ||

| By Disease | Asthma & COPD | |

| Tuberculosis | ||

| Lung Cancer | ||

| Influenza & RSV | ||

| Other Respiratory Infections | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Home Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the respiratory disease testing market by 2031?

The respiratory disease testing market is expected to reach USD 7.48 billion by 2031, growing at a 3.69% CAGR over 2026-2031.

Which test type currently generates the highest revenue?

Molecular diagnostic platforms account for 48.82% of 2025 revenue, making them the largest contributor.

Which segment is projected to grow fastest through 2031?

Lung cancer diagnostics are forecast to advance at a 6.63% CAGR, the fastest among disease segments.

Why is Asia-Pacific the most dynamic regional market?

Air-quality regulations, TB control programs, and expanded insurance coverage propel Asia-Pacific toward a 7.27% CAGR through 2031.

How are home-care settings affecting demand?

Remote monitoring reimbursement and connected devices are driving a 5.18% CAGR for home-care diagnostics, steadily shifting share away from hospital labs.

Page last updated on: