Microbiology Testing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 6.7 Billion |

| Market Size (2031) | USD 10.35 Billion |

| Growth Rate (2026 - 2031) | 9.09% CAGR |

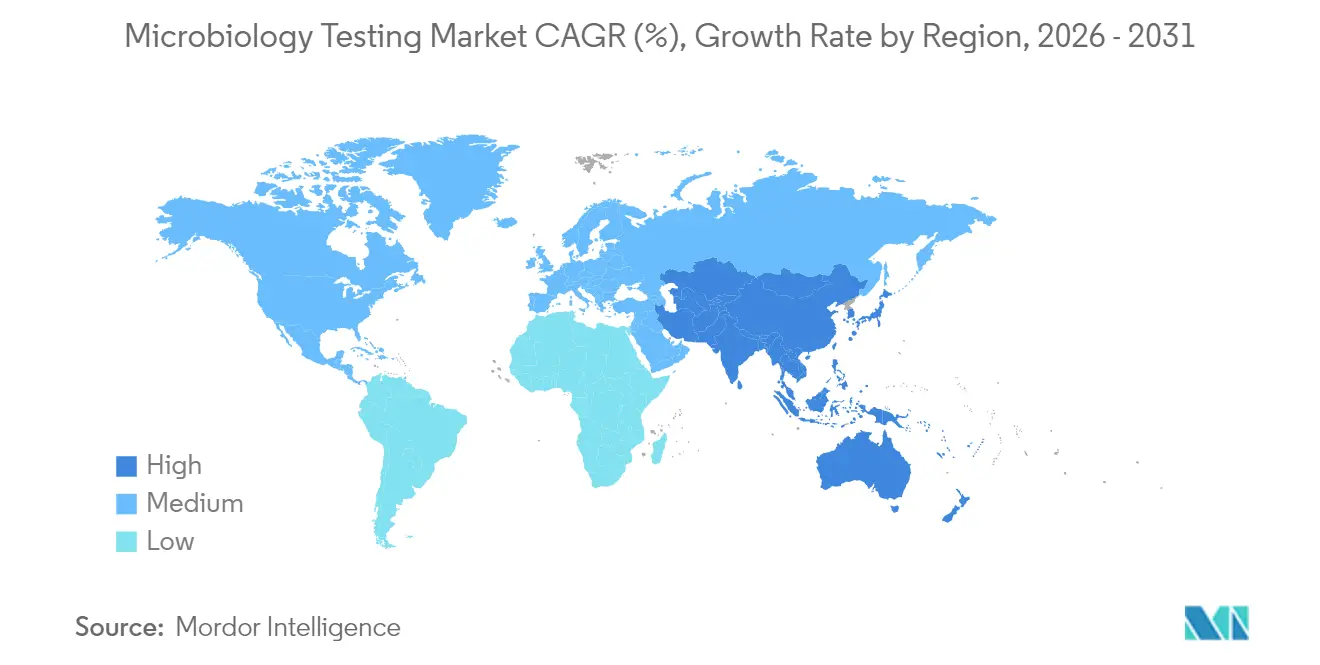

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microbiology Testing Market Analysis by Mordor Intelligence

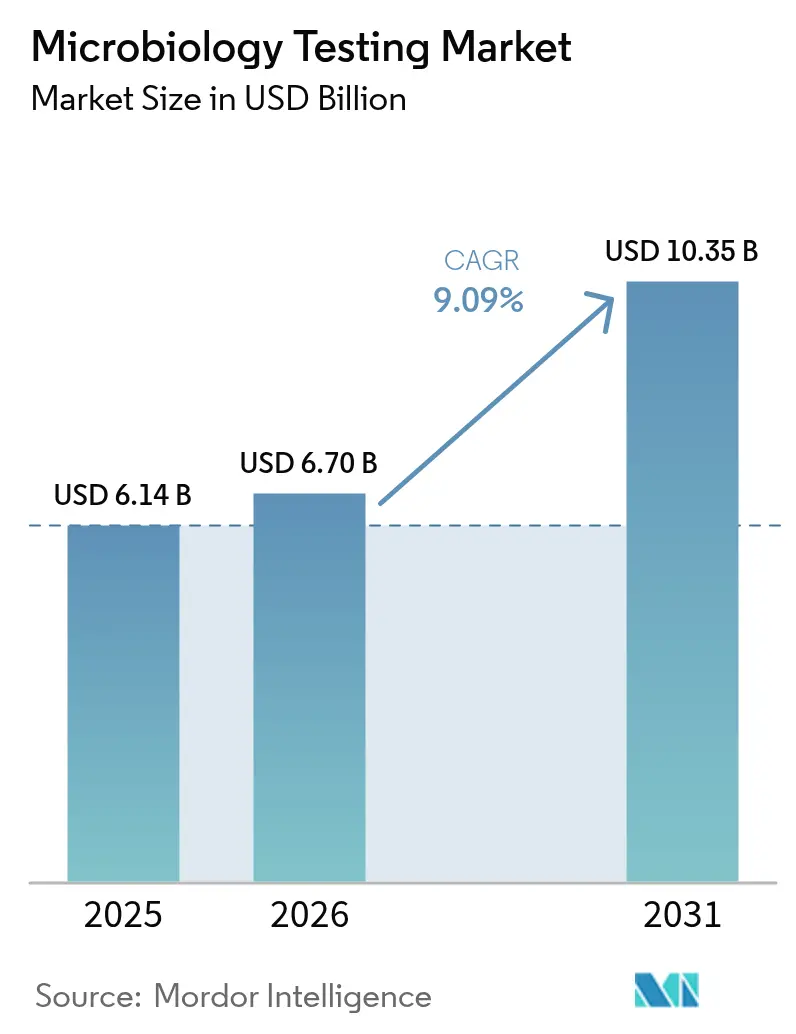

The microbiology testing market size was valued at USD 6.14 billion in 2025 and estimated to grow from USD 6.7 billion in 2026 to reach USD 10.35 billion by 2031, at a CAGR of 9.09% during the forecast period (2026-2031). Clinical demand for faster pathogen identification, the spread of antimicrobial resistance, and accelerating laboratory automation are the strongest growth catalysts. Governments have tightened regulatory oversight of pharmaceutical, food, and personal-care supply chains, which raises the frequency and scope of routine microbial quality control. At the same time, AI-enabled mass-spectrometry and molecular platforms shorten turnaround times, allowing hospitals to start targeted therapy within hours instead of days. Laboratories facing double-digit vacancy rates view total laboratory automation as the most practical remedy for chronic staffing shortages. Manufacturers that can combine rapid diagnostics with connectivity, analytics, and remote-support features will capture a disproportionate share of future tenders in the microbiology testing market.

Key Report Takeaways

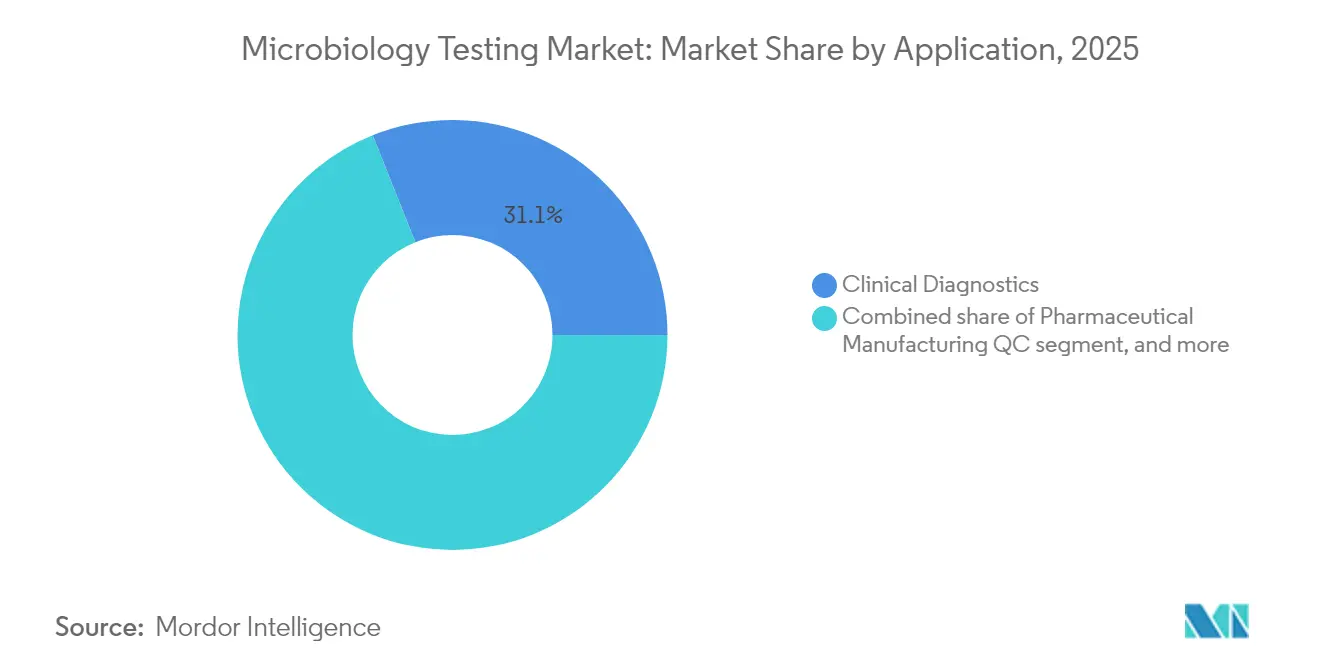

- By application, clinical diagnostics held 31.05% of microbiology testing market share in 2025; cosmetic testing is projected to expand at an 11.23% CAGR through 2031.

- By product, reagents and consumables accounted for 72.98% of the microbiology testing market size in 2025, while instruments and equipment are advancing at an 11.65% CAGR to 2031.

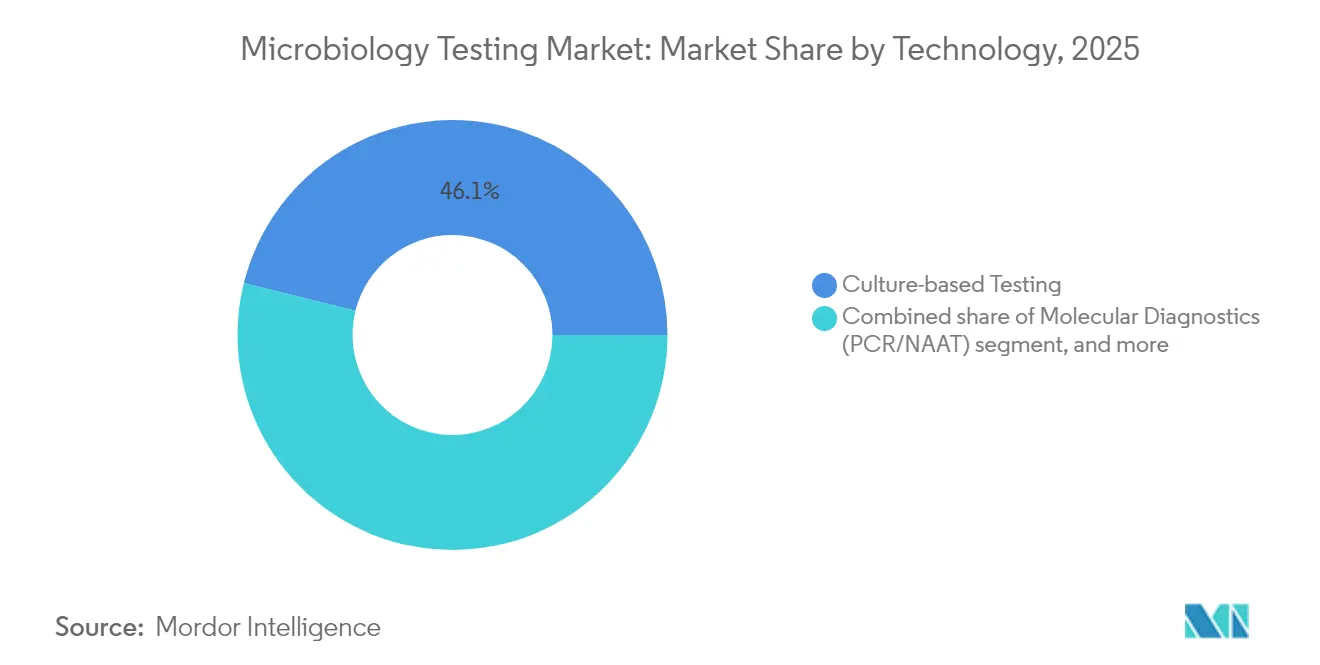

- By technology, culture-based methods retained 46.12% revenue share in 2025; molecular diagnostics are forecast to grow at a 12.18% CAGR between 2026 and 2031.

- By end user, hospitals and diagnostic laboratories commanded 52.20% of the microbiology testing market in 2025, whereas academic and research institutes show the fastest CAGR of 12.46% through 2031.

- By geography, North America led with 42.10% revenue share in 2025; Asia-Pacific is poised for a 10.37% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microbiology Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in diagnostic technologies and automation | +2.1% | Global; early uptake in North America and EU | Medium term (2-4 years) |

| Growing incidence of infectious diseases and antimicrobial resistance | +1.8% | Global; particularly acute in APAC and other emerging markets | Long term (≥ 4 years) |

| Expansion of public and private healthcare funding | +1.4% | APAC core; spill-over to MEA and Latin America | Medium term (2-4 years) |

| Rising demand for rapid and point-of-care testing solutions | +1.6% | Global; strong demand in North America and EU | Short term (≤ 2 years) |

| Stringent regulatory standards for product safety and quality | +1.2% | North America and EU; expanding to APAC | Long term (≥ 4 years) |

| Diversifying applications in pharmaceutical, food, and environmental testing | +1.1% | Global; concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in Diagnostic Technologies and Automation

Laboratory automation reshapes microbiology workflows by pairing robotics with AI-guided imaging systems that cut plating and reading times by around 40%, a clear benefit when vacancy rates in clinical labs hover near 25%. Mass-spectrometry platforms such as MALDI-TOF now integrate machine-learning models capable of species-level identification in minutes, replacing manual techniques that once required up to two days[1]Nature Scientific Data, “Machine Learning-Assisted MALDI-TOF for Bacterial Identification,” nature.com. Fully automated “dark labs” operate lights-out shifts to keep essential testing running during staffing shortages or crises like COVID-19. Interoperability with hospital information systems enables seamless data flow that supports infection-control dashboards and antimicrobial-stewardship alerts. Vendors that bundle hardware, reagents, and cloud-based analytics under service contracts improve uptime while lowering ownership costs, enhancing the attractiveness of their offers in the microbiology testing market.

Growing Incidence of Infectious Diseases and Antimicrobial Resistance

Rising drug-resistant pathogens push clinicians to adopt culture-independent tests that can deliver identification and resistance markers inside the first critical hours of patient admission. Healthcare-associated infections in the United States alone cost more than USD 20 billion annually, intensifying pressure on hospitals to deploy rapid diagnostics that prevent broad-spectrum antibiotic overuse. Climate-driven expansion of mosquito-borne diseases increases the baseline demand for molecular panels that can differentiate co-circulating arboviruses. Evidence that targeted therapy lowers mortality and length of stay amplifies interest in one-hour multiplex PCR assays. Policy makers channel funding toward surveillance networks that rely on timely microbiology data, which in turn enlarges the installed base of advanced systems across the microbiology testing market.

Expansion of Public and Private Healthcare Funding

National preparedness plans created after COVID-19 include dedicated budgets for laboratory modernization, sharply raising capital spending in Asia-Pacific. Public-private partnerships subsidize installation of total laboratory automation in secondary and tertiary hospitals, while global aid programs finance training for molecular technicians. Private insurers increasingly reimburse point-of-care microbiology tests because early pathogen confirmation curbs unnecessary hospital admissions. Pharmaceutical manufacturers allocate a larger portion of plant expansion budgets to environmental monitoring suites that comply with evolving Good Manufacturing Practice guidelines. Collectively, these financial flows expand the addressable pool of end users for the microbiology testing market.

Rising Demand for Rapid and Point-of-Care Testing Solutions

Clinicians value assays that shrink result times from 48 hours to less than 30 minutes, enabling immediate triage decisions in emergency units. Microfluidic cartridges integrate extraction, amplification, and detection in palm-sized devices powered through smartphones, supporting telemedicine follow-up for rural patients[2]Frontiers in Bioengineering and Biotechnology, “Smartphone-Linked Microfluidic Diagnostics,” frontiersin.org. Success of decentralized COVID-19 testing validated the economic case for portable diagnostics and has accelerated product pipelines aimed at respiratory, enteric, and sepsis pathogens. AI-driven readers now guide non-specialist staff through test interpretation, minimizing errors. As a result, hospitals, urgent-care chains, and even retail clinics represent fresh customer segments within the microbiology testing market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment and operational costs | -1.7% | Global; particularly acute in emerging markets | Medium term (2-4 years) |

| Reimbursement and pricing challenges for novel tests | -0.9% | North America and EU; expanding elsewhere | Long term (≥ 4 years) |

| Shortage of skilled laboratory personnel | -1.2% | Global; most severe in developed markets | Short term (≤ 2 years) |

| Supply-chain disruptions for critical reagents and consumables | -0.8% | Global; with regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Operational Costs

Total laboratory automation systems require upfront outlays of USD 2-5 million per site, a hurdle that smaller community hospitals and independent labs struggle to clear. MALDI-TOF instruments cut per-test costs but still demand more than USD 500,000 for hardware plus annual database licensing fees. Molecular reagent packs priced at USD 100-200 per panel dwarf the USD 10-20 consumable spend of culture methods, limiting routine use in low-volume settings. Facilities must also budget for controlled-environment rooms, redundant power, and specialized IT infrastructure. Without volume-based discounts, many emerging-market labs remain locked out of next-generation platforms, constraining the reachable segment of the microbiology testing market.

Shortage of Skilled Laboratory Personnel

Vacancy rates exceeding 25% in critical roles mean remaining technologists handle higher workloads, a situation that 95% of professionals say jeopardizes diagnostic accuracy. Molecular tests demand expertise in nucleic-acid extraction, thermal-cycling protocols, and post-analytic bioinformatics, skills not widely taught in standard clinical-lab curricula. Retirement of senior microbiologists outpaces new graduate output, especially in Europe and the United States. Competitive pay in biotech and pharma diverts talent away from routine diagnostics. Even high-automation sites still need trained staff to validate instrument flags and manage quality systems, making workforce limitations a persistent drag on growth for the microbiology testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Clinical Diagnostics Dominates Amid Cosmetic Testing Surge

Clinical diagnostics delivered 31.05% of 2025 revenue, reflecting hospitals’ priority to curtail healthcare-associated infections with same-day pathogen confirmation. Pharmaceutical-quality control ranked second in value because cGMP rules obligate batch release only after sterile assurance testing. Food and beverage processors adopted Hazard Analysis and Critical Control Point standards that mandate pathogen screening at multiple checkpoints. Environmental monitoring tract steadily due to stricter wastewater and remediation rules.

Cosmetic testing posts the quickest expansion at an 11.23% CAGR as EU Regulation 1223/2009 compels safety dossiers, and the shift toward preservative-light “clean label” formulas raises contamination risk. As brands promote plant-based ingredients, microbial hurdles climb, driving demand for challenge testing and preservative-efficacy studies. Contract labs specializing in personal-care microbiology capture new outsourcing contracts, enlarging their footprint within the microbiology testing market size.

By Product: Reagents Lead While Instruments Accelerate

Reagents and consumables controlled 72.98% of 2025 spending because every culture or molecular run consumes media, panels, discs, or cartridges, ensuring steady replenishment cycles. Stock-out scares during the COVID-19 crisis convinced procurement teams to diversify suppliers and build inventory buffers. Multi-plex respiratory panels, chromogenic media, and AST cards remain staple revenue generators, anchoring the cash-flow base for manufacturers in the microbiology testing market.

Instrumentation revenue rises at an 11.65% CAGR as laboratories upgrade to high-throughput streakers, incubators, and mass-spectrometry analyzers that compress workflow times. More than 550 VITEK MS PRIME systems were installed in 2024 alone, reflecting demand for faster identification without sacrificing accuracy. Automated susceptibility platforms that pair with LIS middleware unlock real-time reporting and antimicrobial-stewardship notifications. Service contracts and software licenses add an annuity layer to hardware sales, enhancing lifetime customer value.

By Technology: Molecular Diagnostics Disrupt Culture-Based Dominance

Culture methods still accounted for 46.12% of 2025 revenue because regulators insist on phenotypic antimicrobial-susceptibility results before approving therapy changes in complex infections. Automated broth micro-dilution and imaging shorten incubation cycles, yet two-day turnaround remains common. Some pathogens, notably anaerobes and slow-growing mycobacteria, cannot yet be fully resolved by molecular shortcuts, preserving the role of culture in the microbiology testing market.

Molecular diagnostics grow at a 12.18% CAGR, propelled by hospital stewardship protocols that demand pathogen identification inside stewardship-critical windows. PCR and isothermal amplification panels detect multiple targets in one cartridge, easing sample-handling burden. Syndromic panels adopted in emergency departments cut empirical broad-spectrum antibiotic use, aligning practice with resistance-mitigation goals. As a result, molecular platforms absorb incremental budget share without fully displacing traditional culture, enlarging total microbiology testing market size.

By End User: Hospitals Dominate as Academic Institutes Accelerate

Hospitals and diagnostic laboratories collected 52.20% of global revenue in 2025 because acute-care physicians rely on near-real-time microbiology to guide therapy decisions. Centralized networks route samples from multiple collection sites to automated hubs that operate 24/7, maximizing asset utilization. Volumes are large enough to justify capital investment in mass-spectrometry and total laboratory automation, reinforcing hospital dominance in the microbiology testing market.

Academic and research institutes expand at a 12.46% CAGR, buoyed by national bio-preparedness programs funneling grants toward pathogen-discovery and vaccine-development projects. Funding covers specialized instruments such as high-resolution sequencing and metagenomic classifiers. Pharmaceutical and biotech firms retain steady demand for in-process control and release testing, while food and contract labs broaden service menus to win multi-year outsourcing contracts.

Geography Analysis

North America generated 42.10% of 2025 revenue, underpinned by advanced hospital infrastructure, mandatory infection-control guidelines, and a clear regulatory pathway for novel diagnostics. The Food Safety Modernization Act obliges extensive pathogen monitoring, stimulating demand from food processors and reference labs. Federal programs that reimburse rapid diagnostics strengthen the business case for premium molecular panels, reinforcing leadership of the microbiology testing market in the region.

Europe ranks second and upholds stringent standards under Regulation 2073/2005 for foodstuffs and the well-enforced cGMP framework for pharmaceuticals. Germany, France, and the Nordics account for the bulk of installed automation lines, and Regulation 1223/2009 keeps cosmetic-testing laboratories busy across the bloc. Collaborative surveillance through the European Centre for Disease Prevention and Control harmonizes outbreak response, indirectly encouraging pan-regional adoption of advanced testing systems.

Asia-Pacific is the fastest-growing territory with a 10.37% CAGR as China, India, and Southeast Asian countries pour capital into laboratory networks that underpin public-health resilience. Massive expansions in biologics and vaccine manufacturing create steady need for environmental monitoring and sterility testing. Japanese hospitals, early adopters of point-of-care molecular devices, showcase the operational gains of rapid diagnostics, prompting regional peer institutions to follow suit. As infrastructure improves, previously underserved rural markets open, enlarging the total addressable microbiology testing market size across the region.

Regulatory Landscape

Regulatory oversight for microbiology testing is anchored in medical-device quality and sterility/bioburden expectations that affect both clinical IVD workflows and industrial microbial quality control. In the United States, the FDA released the second edition of the Pyrogen and Endotoxins Testing (PET) Q&A guidance in March 2026, clarifying sampling practices, handling of out-of-specification results, and explicit support for recombinant reagents as alternatives to animal-derived lysates. The FDA also finalized Quality System Regulation amendments in February 2024, reinforcing lifecycle quality controls that flow through assay design controls, software validation, and manufacturing change management.

In Europe, Regulation (EU) 2017/745 (EU MDR) continues to shape compliance for microbiology-relevant devices, while CE-IVDR requirements increasingly influence menu expansion and claims for multiplex molecular panels. DIN EN ISO 11737-1:2026-04, published April 2026, updates methods for determining microbial populations on products and supports harmonized validation approaches for manufacturers operating across regions.

Value Chain Analysis

The microbiology testing value chain spans specialty inputs (enzymes, antibodies, growth media, plastics, optical and fluidic components), assay and instrument manufacturing, software and middleware integration, distribution and service, and execution at hospitals, diagnostic laboratories, and industrial quality-control sites. Regulatory and standards compliance (for example, FDA quality system requirements and ISO microbiological method standards such as ISO 11737-1) acts as a structural barrier to switching critical materials because formulation or supplier changes frequently trigger re-validation and documentation updates. Supply continuity and component complexity are recurring constraints along the chain.

A single diagnostic device can require assembly of over 1,000 individual components, which can raise exposure to disruptions in plastics, reagents, and subassemblies. This risk was evident in July 2024 when supply constraints tied to plastic bottle availability contributed to disruptions affecting BD blood culture media, prompting U.S. FDA safety communications and forcing laboratories to use contingency workflows. Incidents like this tend to reinforce dual-sourcing, inventory buffering, and longer-term supply agreements for high-throughput microbiology consumables.

Competitive Landscape

The microbiology testing industry is moderately fragmented, yet scale advantages favor corporations that supply integrated platforms spanning clinical, industrial, and environmental applications. bioMérieux led 2024 growth with 8.7% sales expansion, underpinned by the rollout of VITEK MS PRIME and the acquisition of SpinChip Diagnostics, which adds 10-minute immunoassay capability. Thermo Fisher Scientific reinforced vertical-integration synergy by launching contract development and manufacturing offerings that tie test kits to bioprocess equipment. Abbott leveraged epidemiological research to tailor rapid panels toward mosquito-borne pathogens that clinicians expect to rise under climate-change scenarios.

Strategic acquisitions accelerate footprint broadening. Mérieux NutriSciences paid USD 393.4 million to absorb Bureau Veritas’ food-testing arm, instantly adding 34 laboratories and doubling exposure in Canada and Asia-Pacific. BD introduced MiniDraw, a capillary collection system that eliminates phlebotomy in many point-of-care workflows, expanding its reach beyond core laboratory instrumentation [BD.COM]. Emerging firms such as BugSeq, backed by BARDA, marry cloud-based AI with metagenomic sequencing to deliver pathogen-agnostic reports suitable for hard-to-diagnose infections.

Partnerships catalyze technology diffusion. bioMérieux and Illumina co-develop next-generation sequencing kits standardized on MiSeq instruments, combining 80,000-strain reference libraries with routine lab workflows. Equipment makers collaborate with LIS vendors to embed rule-based reporting that automates antimicrobial-stewardship alerts. Service-level agreements now include remote monitoring, predictive maintenance, and reagent auto-replenishment, enhancing customer retention within the microbiology testing market.

Microbiology Testing Industry Leaders

Bio-Rad Laboratories Inc.

Abbott Laboratories

Bruker Corporation

Becton Dickinson and Company

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Demand is building for rapid and automated workflows that connect syndromic molecular detection, antimicrobial-resistance (AMR) markers, and downstream culture confirmation, especially for high-acuity infections where time-to-result is operationally critical. QIAGEN expanded its CE-IVDR-certified QIAstat-Dx bloodstream infection menu in Europe with the BCID GN Plus AMR panel in July 2026, adding gram-negative targets and AMR markers. That menu expansion supports sepsis pathways in regulated markets and aligns with stewardship-driven buying.

Platform-level automation is also an active investment focus as laboratories address staffing constraints and look for sample-to-answer solutions that reduce hands-on steps. A second opportunity area is advanced identification and outbreak management, where MALDI-TOF and related software ecosystems are being broadened through workflow and library enhancements. Bruker highlighted expanded MALDI Biotyper and IR Biotyper workflows in April 2026 and initiated U.S. clinical studies to support additional identification claims, including mycobacteria and filamentous fungi, indicating continued productization of faster organism ID and outbreak analytics that can be integrated into routine microbiology operations. Outside acute-care diagnostics, validated rapid methods for food and consumer safety testing create pull for standardized kits and certifications (AOAC and MicroVal validations), supporting broader adoption by contract labs and manufacturers that need audit-ready microbial results.

Recent Industry Developments

- July 2026: QIAGEN expanded its CE-IVDR-certified QIAstat-Dx bloodstream infection menu in Europe with the BCID GN Plus AMR panel, adding gram-negative targets and AMR markers. The expansion broadens hospital sepsis pathways and supports stewardship-driven purchasing in regulated markets.

- April 2026: Bruker highlighted expanded MALDI Biotyper and IR Biotyper workflows and initiated U.S. clinical studies to support additional identification claims. These steps strengthen Bruker's presence in rapid microbial identification and outbreak analytics programs.

- March 2025: Becton Dickinson launched BD MiniDraw capillary blood-collection technology designed to deliver laboratory-equivalent accuracy from fingertip samples. The product supports decentralized and point-of-care pathways and could influence downstream microbiology and molecular test volumes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the microbiology testing market is counted as revenues generated from equipment and reagents used to detect, identify, and quantify microorganisms in clinical, pharmaceutical quality control, food and beverage, environmental, and related testing workflows across major regions.

Scope exclusions: We exclude non-microbiology analytical tests and general laboratory consumables that are not directly used for microbial detection, identification, or enumeration.

Segmentation Overview

- By Application

- Clinical Diagnostics

- Pharmaceutical Manufacturing QC

- Food & Beverage Testing

- Environmental Monitoring

- Cosmetic Testing

- Industrial Quality Control

- By Product

- Instruments & Equipment

- Reagents & Consumables

- Software & Services

- By Technology

- Culture-based Testing

- Molecular Diagnostics (PCR/NAAT)

- Mass Spectrometry (MALDI-TOF)

- Rapid/Automated Methods

- Biosensors & Nano-based Assays

- By End User

- Hospitals & Diagnostic Laboratories

- Pharmaceutical & Biotech Companies

- Food & Beverage Companies

- CROs & CMOs

- Academic & Research Institutes

- Environmental Testing Labs

- Cosmetics & Personal-Care Labs

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping what drives routine microbiology testing demand and what gets purchased to meet it, and then we collect reference data that can be checked without paywalls. Public sources such as the US FDA, the CDC, the European Commission and ECDC publications, and WHO laboratory guidance help us understand testing standards, surveillance priorities, and where method shifts (for example, rapid and molecular tests) are being encouraged.

Next, we align these signals with measurable activity indicators using sources such as OECD health statistics, UN Comtrade trade flows for relevant lab items, and peer reviewed journals covering clinical microbiology and quality control practices. Company annual reports, investor decks, and credible press releases are also used to anchor product mix shifts and pricing discussions. A paid subscription for company financials and news intelligence is used selectively to cross-check revenue splits and corporate actions. This list is illustrative only, and many other public and paid sources were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

To close gaps left by public data, we conduct expert interviews and surveys with stakeholders across clinical labs, pharma and biotech quality teams, food safety labs, and contract testing providers, followed by discussions with distribution and channel participants where needed. Because this is a global market, views are balanced across APAC, EMEA, and the Americas so assumptions around testing volumes, method adoption, and price progression can be sanity checked and adjusted where local conditions differ.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 38% |

| Mid tier: 59% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 15% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing begins with a top-down demand pool build, where healthcare testing loads, regulated production and batch release activity, and food safety monitoring are translated into expected microbiology test runs, then converted into spend using typical equipment placement and reagent pull-through patterns. Because datasets are never perfect, we corroborate the totals using selective bottom-up approximations, including sampled supplier revenue checks, channel feedback on reagent consumption per site, and spot comparisons of average selling prices against observed procurement behavior.

Inputs that influence the model include hospital and diagnostic activity indicators, infectious disease testing intensity trends, pharma and biologics manufacturing scale, food and beverage compliance testing cadence, and the pace of adoption for rapid and molecular methods versus culture-based workflows. Forecasts are developed using scenario analysis supported by interview-based consensus, where key variables (like regulatory scrutiny, lab automation uptake, and price inflation for consumables) are flexed to reflect realistic paths. Where bottom-up views have gaps by country or application, proxying is done using comparable markets on lab density and regulated production presence, before the result is normalized back to regional totals.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number is not driven by one assumption. We compare implied spending per lab and per testing site against what interviews describe, and we also test whether regional splits align with observable signals such as healthcare activity, regulated manufacturing footprint, and trade movement for relevant lab inputs.

Before sign-off, anomalies are reviewed, assumptions are rechecked, and follow-up calls are triggered when a variance cannot be explained by scope or timing. The report is refreshed annually, and interim updates are made when material events occur that can shift demand or pricing. Right before delivery, a final review pass is completed to ensure the latest public developments are reflected in both the narrative and the model.

Mordor Intelligence's Microbiology Testing Market Size Compared Against Other Published Estimates

Published market sizes for microbiology testing can look far apart even when they sound like they are measuring the same thing, since the year, boundaries, and pricing logic are often not aligned. Differences usually come from what is counted as testing revenue, how equipment versus reagents are treated, and whether estimates are calibrated to real testing activity signals.

A second driver is timing and assumptions, where some publishers lean on aggressive method-shift narratives, while others use conservative price progression or different currency conversion points. When these choices are not clearly tied back to test volumes, installed base behavior, and regulated use cases, the final market value can drift upward or downward by a meaningful amount.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.7 B (2026) | |

| Trade Publisher A | USD 5.9 B (2024) | Uses an earlier base year and its scope is more centered on instrument and reagent revenues without clearly aligning to regulated QC testing intensity across pharma and food applications, which can understate later-year expansion. |

| Global Consultancy B | USD 6.21 B (2024) | Blends microbiology testing with a clinical microbiology framing in places, and the application-led sizing can miss non-clinical demand signals that show up in routine QC and compliance testing. |

The table shows a spread that is largely explained by base-year choice and what parts of demand are counted beyond clinical settings. In Mordor Intelligence's model, the 2026 value is tied to equipment and reagent spending only when it maps to microbiology test workflows across pharma QC, food safety, environmental, and diagnostics. Once the year is aligned and the included testing use cases are made explicit, the remaining differences mostly come from how price progression and method adoption are carried through the forecast, which is why a clear, repeatable set of inputs matters.

Key Questions Answered in the Report

What is the current size of the microbiology testing market?

The microbiology testing market size stood at USD 6.7 billion in 2026 and is projected to reach USD 10.35 billion by 2031.

Which application segment generates the highest revenue?

Clinical diagnostics leads with 31.05% of revenue in 2025, primarily due to hospital demand for rapid pathogen identification.

What technology is growing fastest in microbiology testing?

Molecular diagnostics, including PCR and nucleic-acid amplification, are advancing at a 12.18% CAGR through 2031.

Why is Asia-Pacific considered the most attractive growth region?

Healthcare infrastructure upgrades, pharmaceutical manufacturing expansion, and rising food-safety awareness underpin a 10.37% CAGR in Asia-Pacific.

How are staffing shortages influencing laboratory investment decisions?

Vacancy rates near 25% push laboratories to invest in total automation systems that cut manual workload and maintain turnaround times.

Which companies are strengthening their competitive position through acquisitions?

BioMérieux, Mérieux NutriSciences, and Thermo Fisher Scientific have all closed strategic deals to broaden technology portfolios and geographic reach.

Page last updated on: