MENA Retail Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.92 Trillion |

| Market Size (2026) | USD 1 Trillion |

| Market Size (2031) | USD 1.31 Trillion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Retail Market Analysis by Mordor Intelligence

The MENA Retail Market size is projected to expand from USD 0.92 trillion in 2025 and USD 1 trillion in 2026 to USD 1.31 trillion by 2031, registering a CAGR of 5.67% between 2026 to 2031.

The MENA retail market is now entering a higher-volume phase, as 2026 marks the first year in which aggregate regional retail spending exceeds USD 1 trillion. This shift is being supported by the continued build-out of formal retail networks, stronger urban consumption, and deeper digital participation across both GCC economies and North Africa’s major cities. The MENA retail market is also benefiting from a broad consumer base that remains young, more brand aware, and increasingly open to modern formats that combine convenience, assortment, and digital access. Competitive behavior is becoming more scale-driven, with larger operators using acquisitions, store expansion, format innovation, and omnichannel investment to defend traffic and raise operating leverage. The MENA retail market still faces meaningful friction from logistics volatility and uneven channel formalization, but those pressures are also widening the gap between well-capitalized retailers and smaller operators.[1]U.S. Department of Agriculture Foreign Agricultural Service, “Retail Foods Annual, Saudi Arabia, SA2025-0015,” USDA GAIN, apps.fas.usda.gov

Key Report Takeaways

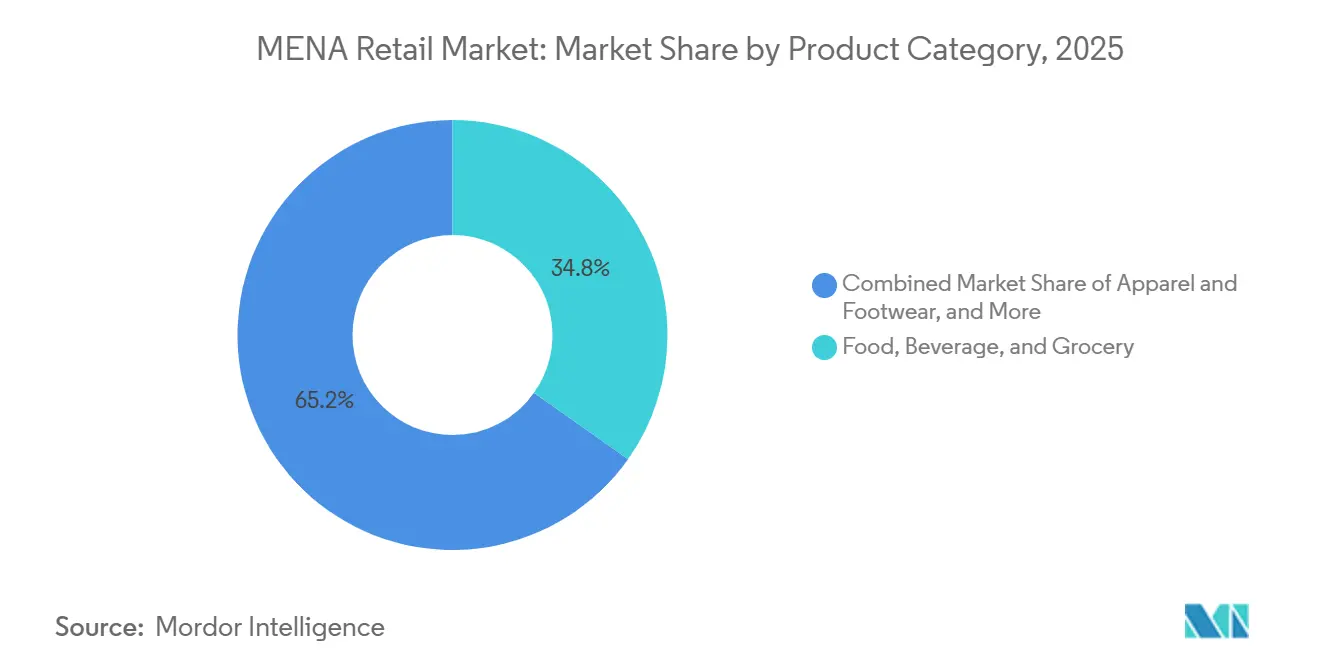

- By product category, Food, Beverage, and Grocery led with 34.81% revenue share in 2025, while Beauty, Personal Care, and Healthcare is forecast to expand at 6.73% CAGR through 2031.

- By store type, Hypermarkets and Supermarkets held 30.94% of revenue in 2025, while E-commerce and Online Retail recorded the highest projected CAGR at 6.92% through 2031.

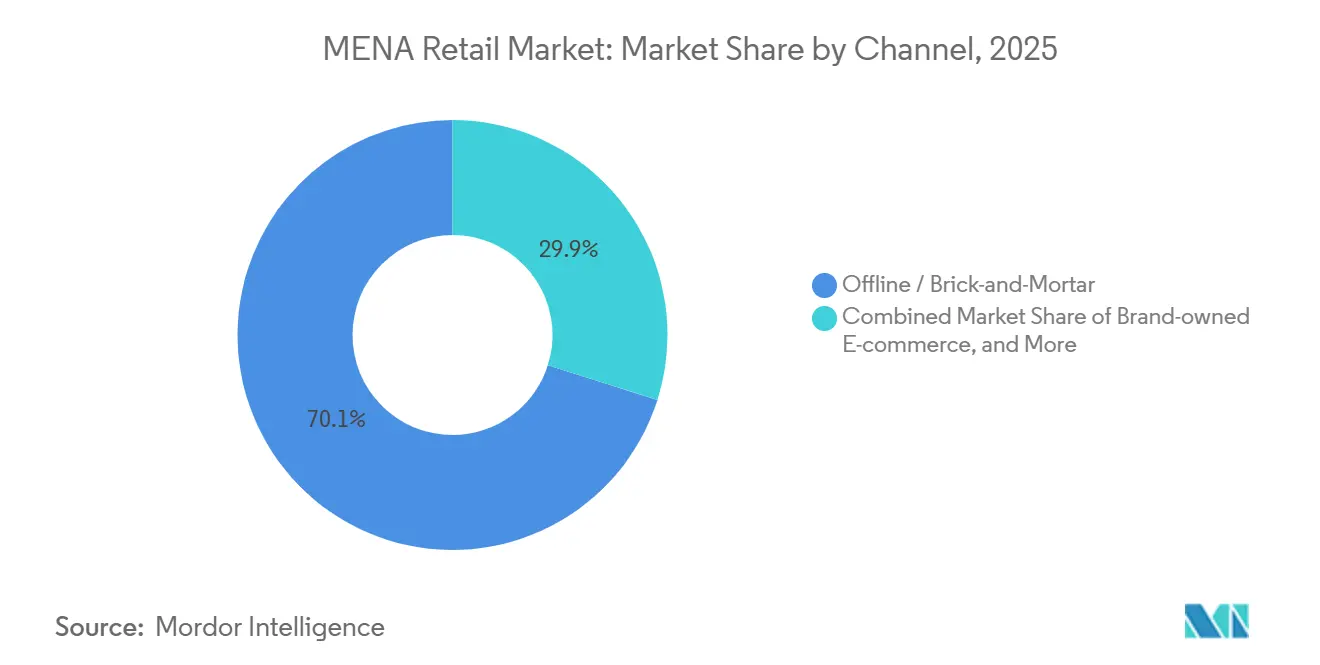

- By channel, Offline and Brick-and-Mortar accounted for 70.12% of revenue in 2025, while Quick Commerce is advancing at a 7.57% CAGR through 2031.

- By geography, the GCC held 62.64% of the MENA retail market in 2025, while North Africa is forecast to grow at the fastest CAGR of 6.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

MENA Retail Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organized Modern Trade Expansion | +1.2% | GCC core, with spill-over to North Africa | Medium term (2-4 years) |

| Omnichannel and E-commerce Acceleration | +1.0% | GCC primary, Egypt and Morocco accelerating | Medium term (2-4 years) |

| Youth-Led Premiumization and Discretionary Spend | +0.8% | GCC-wide, Egypt's urban corridors emerging | Long term (≥ 4 years) |

| Ramadan and Religious-Tourism Demand Spikes | +0.7% | Saudi Arabia, GCC, broader MENA in key seasonal windows | Short term (≤ 2 years) |

| Offline BNPL and Local-Payment Enablement | +0.6% | Saudi Arabia, UAE, Kuwait, Egypt nascent | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rapid Expansion of Quick Commerce Platforms | +0.5% | UAE, Saudi Arabia, Egypt metro areas accelerating | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Organized Modern Trade Expansion

Organized trade expansion remains one of the clearest structural supports for the MENA retail market, because scale operators continue to gain from better sourcing, stronger compliance capacity, and broader format coverage. In Saudi Arabia, the food retail market exceeded USD 50 billion in 2024, and hypermarkets and supermarkets continued to strengthen their position as consumers shifted toward packaged food, larger assortments, and more dependable retail environments. The same report shows that major chains such as Panda, Othaim, Tamimi, BinDawood, LuLu, and Carrefour already operate extensive store networks, which gives them a wider base for expansion than smaller traditional outlets. Across the MENA retail market, this matters because modern trade is not only adding square footage but also raising standards in merchandising, inventory control, and supply consistency. That shift is improving the economics of branded retail, private label development, and fresh-food execution in the more formal parts of the region. It is also pushing the competitive center of gravity toward operators that can manage both store density and operating discipline across multiple urban clusters.

Omnichannel and E-commerce Acceleration

Omnichannel adoption is becoming a core growth lever for the MENA retail market, as digital commerce is no longer a side channel for only a few categories. LuLu Retail reported that its e-commerce sales grew 38.6% in FY2025. At the same time, half of its estate was e-commerce-enabled by year-end, indicating that large regional retailers are embedding online fulfillment within their physical networks rather than treating it as a separate business. Majid Al Futtaim reported 20% growth in e-commerce revenue and 38% growth in quick commerce in FY2025, indicating a similar pattern of digital acceleration within established retail platforms. In the MENA retail market, that combination is important because shoppers increasingly move between mobile discovery, store pickup, home delivery, and app-based replenishment within the same brand relationship. Omnichannel execution is therefore becoming less about adding a website and more about redesigning assortment, pricing, fulfillment, and loyalty around a blended shopping journey. Retailers that get this right are likely to defend their share more effectively as digital traffic keeps rising in the GCC and gradually deepens in North Africa.

Youth-Led Premiumization and Discretionary Spend

Youth-led premiumization is widening the addressable opportunity within the MENA retail market, especially in categories where identity, wellness, and convenience drive repeat spending. Saudi Arabia’s rising female workforce participation is supporting demand for convenient, higher-value packaged food, ready-to-eat products, and personal care items, with the USDA noting that women represented 36% of the workforce in the country’s recent retail context. Nahdi Medical’s 2024 annual report also showed that health, beauty, and care-oriented retail formats are gaining momentum, with online revenue up 40%, private-label sales above SAR 1.2 billion, and digital health services continuing to scale. In the MENA retail market, the result is a consumer mix willing to spend more on selected categories while remaining price-sensitive on everyday staples. That is why premium beauty, healthcare retail, wellness-linked products, and curated specialty assortments are growing in importance faster than headline consumption figures alone would suggest. It also explains why large retailers are trying to hold both ends of the value ladder, using private-label for daily essentials and premium positioning for discretionary items.[2]General Authority for Statistics, “Labor Market Statistics Q4 2024,” Kingdom of Saudi Arabia, gastat.gov.sa

Ramadan and Religious-Tourism Demand Spikes

Seasonal demand remains a major performance driver for the MENA retail market, and Ramadan continues to create one of the strongest annual concentration points for store traffic, basket expansion, and promotional activity. The supplied draft states that Saudi Arabia’s Ramadan 2026 consumer season reached SAR 65 billion in total spending, up 12% from Ramadan 2025, underscoring the region’s biggest consumption center's strong seasonal demand. For retailers, this effect goes well beyond food, because gifting, apparel, beauty, electronics, and foodservice-linked categories also benefit from higher purchase frequency and stronger family-oriented spending during peak periods. Religious tourism reinforces this pattern by generating recurring consumer demand in key Saudi retail corridors, especially where pilgrimage traffic, hospitality flows, and convenience spending overlap. This creates a reliable calendar effect inside the MENA retail market and rewards operators that can prepare inventory, staffing, promotions, and fulfillment windows well ahead of peak demand periods. It also supports format diversity, because supermarkets, malls, pharmacies, specialty stores, and digital channels all participate in the seasonal lift through different shopping missions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Red Sea Logistics Shocks and Import Dependence | -1.0% | MENA-wide, acute in North Africa and GCC import-reliant markets | Short term (≤ 2 years) to Medium term (2-4 years) |

| Informal Trade and Uneven Last-Mile Infrastructure | -0.9% | North Africa primary, spill-over to GCC lower-tier cities | Long term (≥ 4 years) |

| Belief-Driven Boycotts and Localization Costs | -0.7% | GCC, wider MENA in conflict-adjacent periods | Medium term (2-4 years) |

| Retail Margin Pressure from Discounting Trends | -0.5% | GCC organized retail most exposed | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Red Sea Logistics Shocks and Import Dependence

Logistics disruptions in and around Red Sea routes remain a significant restraint on the MENA retail market, as a large part of the region’s retail assortment still depends on imported goods. The supplied draft notes that Asia-to-MENA transit times have been extended by 10 to 15 days during rerouting periods, putting pressure on working capital, replenishment timing, and seasonal merchandise planning. USDA also notes that Saudi Arabia relies on imports for up to 80% of its food consumption, which illustrates how exposed major regional retail systems remain to freight costs, trade frictions, and external supply volatility. In the MENA retail market, that exposure hits time-sensitive and lower-margin categories the hardest, especially fresh food, fashion, and electronics. Retailers with better local sourcing, stronger planning systems, or private label control are therefore in a better position to defend margins when shipping conditions tighten. The restraint is structural rather than temporary, because even short disruption periods can affect landed costs, inventory availability, and promotional timing across several retail categories at once.

Informal Trade and Uneven Last-Mile Infrastructure

Informal trade remains a major constraint on the MENA retail market in North Africa, where organized retail still competes with deeply embedded traditional and semi-formal channels. The supplied draft highlights that informal economic activity remains large in key North African economies, which helps explain why modern trade penetration does not rise as quickly as store-opening plans might suggest. Uneven last-mile logistics, weak cold-chain coverage outside primary cities, and inconsistent delivery economics across second-tier urban areas reinforce this challenge. In the MENA retail market, the result is a slower formalization curve, because retailers must build trust, logistics, and affordability simultaneously rather than relying solely on format rollout. World Bank material in the supplied references also supports the broader point that infrastructure quality and institutional conditions remain uneven across the region. This means the addressable opportunity is large, but scale execution outside the best-served cities is still harder than headline population figures would imply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Staples Lead, Healthcare Reshapes the Revenue Mix

Food, Beverage, and Grocery accounted for 34.81% of the MENA retail market share in 2025, confirming that staples still anchor volume and traffic across the region. This leading position reflects the non-discretionary nature of food demand, the role of seasonal purchasing during Ramadan, and the continued spread of supermarkets and hypermarkets in both GCC and North African cities. In the MENA retail industry, grocery also benefits from repeat purchase frequency, which makes it the base category around which retailers build loyalty, cross-selling, and neighborhood relevance. Consumer Electronics and Household Appliances continue to hold a stable role in the MENA retail market, supported by housing expansion, household formation, and ongoing demand from expatriate populations in the Gulf. Apparel and Footwear also remain important because youth-heavy demographics, occasion-led spending, and mall traffic still support category turnover in major urban centers. Even when digital channels grow faster, grocery remains the category that most often links store visits, delivery demand, and basket-building behavior across the wider MENA retail market.

Beauty, Personal Care, and Healthcare is projected to grow at a 6.73% CAGR through 2031, the fastest pace among the MENA retail market's product categories. This reflects rising demand for wellness-linked spending, stronger female workforce participation, and a broader shift toward health, self-care, and convenience. Nahdi's 2024 annual report showed that private-label sales exceeded SAR 1.2 billion, online revenue grew 40%, and healthcare-related service activity expanded sharply, highlighting how healthcare retail is becoming a more integrated commercial platform rather than a narrow pharmacy format. In the MENA retail industry, that shift matters because it pulls spending into higher-value categories that combine products, advice, digital services, and repeat customer relationships. Home Care, Home Décor, and Furniture continue to benefit from residential development and urban household formation. At the same time, Toys, Hobbies, and Leisure Goods remain smaller but more relevant as family entertainment spending broadens. The less visible category shift is the growing role of retailer-controlled brands, as private label can improve margins and customer stickiness simultaneously.

By Store Type: Hypermarkets Anchor Volume, Digital Channels Accelerate Share Gains

Hypermarkets and Supermarkets accounted for 30.94% of the MENA retail market in 2025, indicating that large-format modern trade still anchors the region’s volume base. These stores remain important because they combine essential shopping, a broad assortment, promotional visibility, and family-oriented shopping missions in a single trip. USDA’s Saudi retail review also noted that hypermarkets and supermarkets are increasingly dominating traditional food retail, with the leading chains already operating at significant scale across the country. In the MENA retail market, large formats also function as fulfillment assets, because retailers increasingly use them to support delivery, click-and-collect, and app-led replenishment. That gives hypermarkets and supermarkets a relevance that goes beyond floor space alone. Their challenge is not demand, but the need to keep experience, assortment, and service standards high enough to defend traffic against faster digital alternatives.

E-commerce and online retail are the fastest-growing store types, with a 6.92% CAGR through 2031, confirming how quickly digital participation is deepening across the MENA retail market. LuLu reported 38.6% e-commerce growth in FY2025. In comparison, Majid Al Futtaim reported 20% growth in e-commerce revenue during the same year, which shows that digital scale is already becoming meaningful for leading operators. Convenience stores are also evolving in the MENA retail industry, as urban consumers increasingly value faster access, proximity, and mission-led assortments rather than just large weekly stock-up trips. Discount stores and cash-and-carry formats look underpenetrated relative to the needs of value-conscious households, while specialty stores continue to benefit from premium beauty, healthcare, and lifestyle spending. Department stores appear more exposed, because they face pressure from both focused specialty chains and digital-first alternatives. The store mix is therefore widening, but the strongest performers are usually those that align with clear shopper missions and deliver better execution.

By Channel: Offline Holds Majority, Quick Commerce Sets the Pace

Offline and Brick-and-Mortar accounted for 70.12% of the MENA retail market by value in 2025, which confirms that physical retail remains the main spending channel across the region. Store-led retail still matters because customers continue to value product inspection, immediate purchase, family shopping routines, and the social role of malls and neighborhood retail. In the MENA retail market, offline retail is not being displaced; rather, more convenience-led formats are reshaping it, along with better app integration and stronger expectations around service and delivery. Brand-owned e-commerce and marketplace-led e-commerce are both expanding as retailers seek to maintain direct customer access while leveraging large platforms for reach and traffic. This balance is important in categories where loyalty, pricing, and delivery speed all influence repeat purchase. It also explains why physical retail continues to hold a majority share even as digital channels expand more quickly.

Quick Commerce is forecast to grow at a 7.57% CAGR through 2031, which makes it the fastest-growing channel in the MENA retail market. The channel’s momentum reflects a shift toward urgent and convenience-led shopping missions, especially for grocery top-ups, health products, and household essentials. Majid Al Futtaim’s FY2025 results, which showed 38% quick commerce growth, support the idea that rapid fulfillment is moving from a niche service to a more established consumer behavior in the region. Social commerce is also gaining attention because product discovery, promotion, and transaction pathways are becoming more tightly linked in mobile-first environments. The channel mix inside the MENA retail market is therefore broadening, but speed, convenience, and digital trust are becoming more central to who captures incremental spend. Over time, this could shift more value toward retailers that control customer data, last-mile delivery, and app engagement, rather than just physical space.

Geography Analysis

The GCC accounted for 62.64% of the MENA retail market share in 2025, keeping it the clear commercial core of the region. Saudi Arabia and the UAE remain the twin engines of that position, as both markets combine deeper formal retail with higher digital adoption and more active investment by leading retail groups. In Saudi Arabia, the USDA estimated the food retail market at more than USD 50 billion in 2024, while major supermarket and hypermarket chains continued to expand their reach, reinforcing the country’s scale advantage in essential retail. USDA FAS. The supplied draft also notes that Ramadan 2026 spending in Saudi Arabia reached SAR 65 billion, underscoring how concentrated peak demand can be in the region’s largest market. The UAE complements Saudi Arabia with a more mature omnichannel structure and a concentration of high-capability operators that are already investing in faster fulfillment, loyalty, and format innovation. Together, these two markets give the broader MENA retail market a strong base in scale, digital execution, and modern trade density.

The UAE remains the region’s most advanced template for integrated retail execution, and Majid Al Futtaim’s FY2025 results help explain why. The company reported AED 35.9 billion in revenue, AED 5.1 billion in EBITDA, 20% e-commerce revenue growth, and 38% quick commerce growth, indicating that digital and physical retail are now operating as a linked system rather than separate channels. LuLu’s FY2025 results point to the same regional pattern, with USD 7.9 billion in revenue, 20 new stores added in 2025, and a 50-store opening pipeline planned for 2026 to 2028 across the GCC. Kuwait, Oman, and Bahrain continue to function as the next layer of organized retail expansion, where network density is improving, and large regional operators still see room for store-led growth. This keeps the GCC at the center of the MENA retail market not only because of current demand, but also because it remains the main testing ground for new formats, digital tools, and loyalty-led customer models. The region’s larger listed and family-owned groups are therefore shaping standards that may later spread into adjacent MENA markets.

North Africa is the fastest-growing regional cluster in the MENA retail market, with a forecast CAGR of 6.12% through 2031. Its opportunity remains heavily volume-led, because population scale, urban growth, and low formal retail penetration still create a long runway for organized formats. At the same time, the MENA retail market does not develop evenly across North Africa, as informal trade, weaker last-mile systems, and lower purchasing power continue to affect the pace of channel formalization. Morocco stands out for stronger, more organized retail momentum and rising consolidation activity, while Egypt remains structurally attractive due to its large population and broad grocery demand base. The path to convergence with GCC-style retail penetration will likely be gradual, as physical infrastructure, logistics quality, and consumer affordability need to improve together. That means North Africa is likely to remain the faster-growing side of the MENA retail market. Still, it will not necessarily align with GCC operating economics over the current forecast horizon.[3]International Trade Administration, “Saudi Arabia - Country Commercial Guide: Retail and E-commerce,” U.S. Department of Commerce, trade.gov

Competitive Landscape

The MENA retail market has a dual-speed competitive structure, with scale-led consolidation in the GCC and a more fragmented setup in North Africa. Large operators are increasingly competing through store density, digital execution, loyalty systems, vertical integration, and portfolio breadth rather than only through headline brand presence. Al-Futtaim’s September 2025 acquisition of a 49.95% stake in Cenomi Retail for SAR 2.52 billion, together with a SAR 1.35 billion shareholder loan facility, is one of the strongest examples of this direction. That transaction matters because it connects capital strength, local retail reach, and future digital capability in one structure. It also shows that the MENA retail market is no longer defined only by organic expansion, because major players are now willing to use strategic transactions to accelerate position. Even where the market stays fragmented, the direction of travel is clearly toward more scale and more formalization.

Majid Al Futtaim remains one of the clearest examples of asset-backed retail competition in the MENA retail market. Its FY2025 results showed AED 35.9 billion in revenue, AED 3.6 billion in net profit, more than 98% mall occupancy, e-commerce revenue growth of 20%, and quick commerce growth of 38% MAJID AL FUTTAIM. The company also launched HyperMax in Oman, Bahrain, and Kuwait, launched SAVA in the UAE, and committed AED 5 billion to the Mall of the Emirates transformation, which shows how leading players are expanding through both new retail formats and higher-quality destination assets. LuLu follows a similar regional logic, with FY2025 revenue of USD 7.9 billion, 20 new stores added in 2025, strong e-commerce growth, and a 50-store GCC pipeline for 2026 to 2028. These examples show that the MENA retail market increasingly rewards operators that can scale physical presence while improving data use, fulfillment speed, and loyalty economics. Retail leadership is therefore being built through integrated operating models rather than through store count alone.

Healthcare and wellness retail are also becoming more competitive in the MENA retail market, and Nahdi offers a clear example of that shift. Nahdi’s 2024 annual report showed 1,181 stores across Saudi Arabia and the UAE, 10 new UAE pharmacies added in 2024, 4 new polyclinics opened, online revenue up 40% to SAR 2 billion, and the launch of its first private label medicine products. In Q1 2026, Nahdi reported revenue growth of 6.1%, healthcare business growth of 34.8%, and regional expansion growth of 31.8%, which confirms that healthcare retail is widening beyond core pharmacy sales. This creates a broader competitive field inside the MENA retail market, where pharmacies, beauty chains, grocery operators, and digital platforms increasingly overlap on wellness-linked spending. The most successful companies are likely to be those that combine trust, recurring demand, data, and service integration in a way that smaller single-format operators cannot match. That is why competition is intensifying even though the market still remains regionally diverse and structurally fragmented.

MENA Retail Industry Leaders

Majid Al Futtaim

LuLu Retail Holdings

Landmark Group

Abdullah Al Othaim Markets

BinDawood Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Dubai South signed a major agreement with retail and lifestyle conglomerate Majid Al Futtaim to develop a mixed-use master community valued at AED 62 billion (USD 16.88 billion). Spanning 22 million square feet, the development will be strategically located near Al Maktoum International Airport. Crucially for the retail sector, the project will be anchored by a massive, state-of-the-art shopping mall designed to serve as a premier entertainment and lifestyle destination for the expanding population of Dubai South.

- May 2026: Alshaya Group signed a major agreement with Kuwaiti real estate developer, Mabanee. Under the contract, Alshaya will open over 20 stores spanning a leasable area of over 10,000 square meters at the upcoming Aventura Mall in Kuwait (slated to open in Q3 2026). The massive footprint will introduce global brands like H&M, Victoria's Secret, and Starbucks, while also facilitating the highly anticipated regional debuts of Ulta Beauty and Primark.

- October 2025: Apparel Group signed a strategic partnership with Arabian Alesaar Group to expand its footprint in the Kingdom of Saudi Arabia. The agreement secures over 9,000 square meters of retail space inside the Al Shubaily Grand Mall in Riyadh to launch 24 international brands simultaneously. The mega-launch brings global heavyweights like Calvin Klein, Tommy Hilfiger, Skechers, and Levi's to the new destination, aligning directly with the Kingdom's Vision 2030 goals to boost the domestic lifestyle and retail economy.

- September 2025: Al-Futtaim completed the acquisition of a 49.95% stake in Cenomi Retail for SAR 2.52 billion (USD 0.67 billion) and also extended a SAR 1.35 billion (USD 0.36 billion) shareholder loan facility to support balance sheet strengthening and future expansion.

MENA Retail Market Report Scope

| Food, Beverage, and Grocery |

| Apparel and Footwear |

| Beauty, Personal Care, and Healthcare |

| Consumer Electronics and Household Appliances |

| Home Care, Home Decor, and Furniture |

| Toys, Hobbies, and Leisure Goods |

| Hypermarkets and Supermarkets |

| Convenience Stores |

| Specialty Stores |

| Department Stores |

| Discount Stores and Cash-and-Carry |

| E-commerce and Online Retail |

| Offline / Brick-and-Mortar |

| Brand-owned E-commerce |

| Marketplace-led E-commerce |

| Social Commerce |

| Quick Commerce |

| GCC | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| North Africa |

| By Product Category | Food, Beverage, and Grocery | |

| Apparel and Footwear | ||

| Beauty, Personal Care, and Healthcare | ||

| Consumer Electronics and Household Appliances | ||

| Home Care, Home Decor, and Furniture | ||

| Toys, Hobbies, and Leisure Goods | ||

| By Store Type | Hypermarkets and Supermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Department Stores | ||

| Discount Stores and Cash-and-Carry | ||

| E-commerce and Online Retail | ||

| By Channel | Offline / Brick-and-Mortar | |

| Brand-owned E-commerce | ||

| Marketplace-led E-commerce | ||

| Social Commerce | ||

| Quick Commerce | ||

| By Geography | GCC | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| North Africa | ||

Key Questions Answered in the Report

What is the current size of the MENA retail space?

The MENA retail market was valued at USD 0.92 billion in 2025 and is estimated at USD 1.00 billion in 2026, with forecast value reaching USD 1.31 billion by 2031.

Which product category leads regional retail demand?

Food, Beverage, and Grocery led with a 34.81% share in 2025, reflecting the role of essential demand, repeat purchase frequency, and broad modern trade distribution.

Which retail format is expanding the fastest in MENA?

By store type, E-commerce and Online Retail is projected to grow fastest at a 6.92% CAGR through 2031, while Quick Commerce leads all channels at a 7.57% CAGR.

Why does the GCC dominate regional retail performance?

The GCC held 62.64% of 2025 regional revenue because Saudi Arabia and the UAE combine stronger formal retail depth, scale operators, and more advanced omnichannel execution.

What are the main constraints on growth across MENA retail?

The main limits remain import dependence and logistics disruption, informal trade in North Africa, localization costs during sentiment-driven shifts, and tighter margins from discount-led competition.

How are leading retailers changing their strategy in MENA?

Large operators are using acquisitions, new store formats, loyalty systems, private label, e-commerce, and service integration to defend share and improve operating leverage across the region.

Page last updated on: