Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

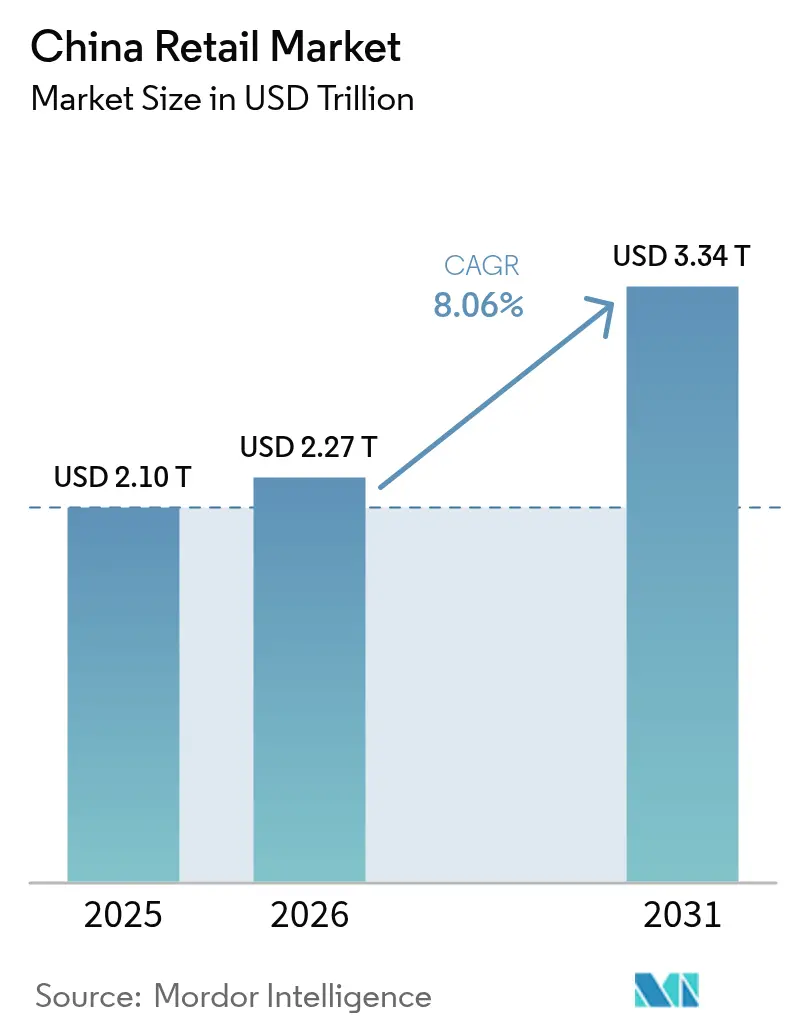

| Base Year Market Size (2025) | USD 2.10 Trillion |

| Market Size (2026) | USD 2.27 Trillion |

| Market Size (2031) | USD 3.34 Trillion |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Retail Market Analysis by Mordor Intelligence

The China retail market size is expected to grow from USD 2.1 trillion in 2025 to USD 2.27 trillion in 2026 and is forecast to reach USD 3.34 trillion by 2031 at 8.06% CAGR over 2026-2031. Momentum reflects the combined effects of omnichannel investments, policy support that boosts consumption, and format innovation that widens choice for value and premium shoppers. The digital yuan has scaled into daily life and is shaping the checkout layer of payments, which is strengthening the quality of retail data and speeding settlement. Social commerce and livestreaming have deepened reach in lower-tier cities, while membership clubs have lifted household basket sizes as consumers trade up on bulk and imported goods. Competitive intensity remains high as price-led plays squeeze margins and raise the bar on unit economics, yet structural upgrades in logistics and data tooling keep long-run growth intact for the China retail market

Key demand signals are visible in payments, channels, and policy. The digital yuan recorded 3.48 billion cumulative transactions totalling CNY 16.7 trillion (USD 2.37 trillion) as of late 2025, a scale that has catalysed merchant acceptance and lowered per-transaction costs[1]Source: State Council Information Office Staff, “Digital Yuan Accumulated 3.48 Billion Transactions by November 2025,” Gov.cn, english.www.gov.cn. Livestreaming commerce reached USD 807 billion in 2024 with a user base of 833 million, and platforms are prioritizing engagement quality in lower-tier markets where the next wave of growth resides. Warehouse clubs surpassed CNY 300 billion (USD 42.6 billion) in annual sales, and Sam’s Club recorded CNY 120 billion GMV in 2025 (USD 17.0 billion), which has validated the premium bulk model for urban families. A national consumer-goods trade-in program delivered CNY 2.6 trillion in sales in 2025 (USD 368.8 billion), and fiscal allocations for 2026 have been guided higher, which keeps appliances and related categories on a firm trajectory in the China retail market.

Key Report Takeaways

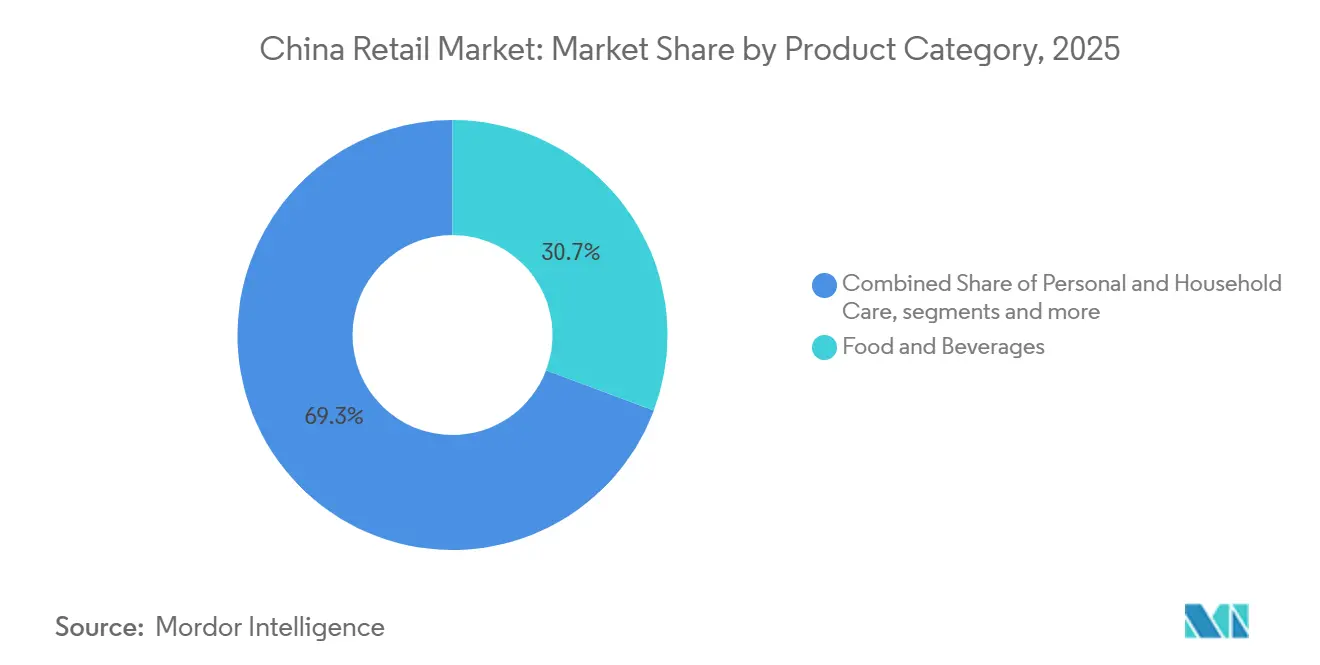

- By product category, food & beverages led with 30.72% revenue share in 2025; consumer electronics & appliances is projected to expand at a 9.23% CAGR to 2031 in the China retail market.

- By distribution channel, e-commerce platforms held a 34.15% share of the China retail market size in 2025, while discount & membership-club stores are forecast to grow at 13.35% CAGR through 2031.

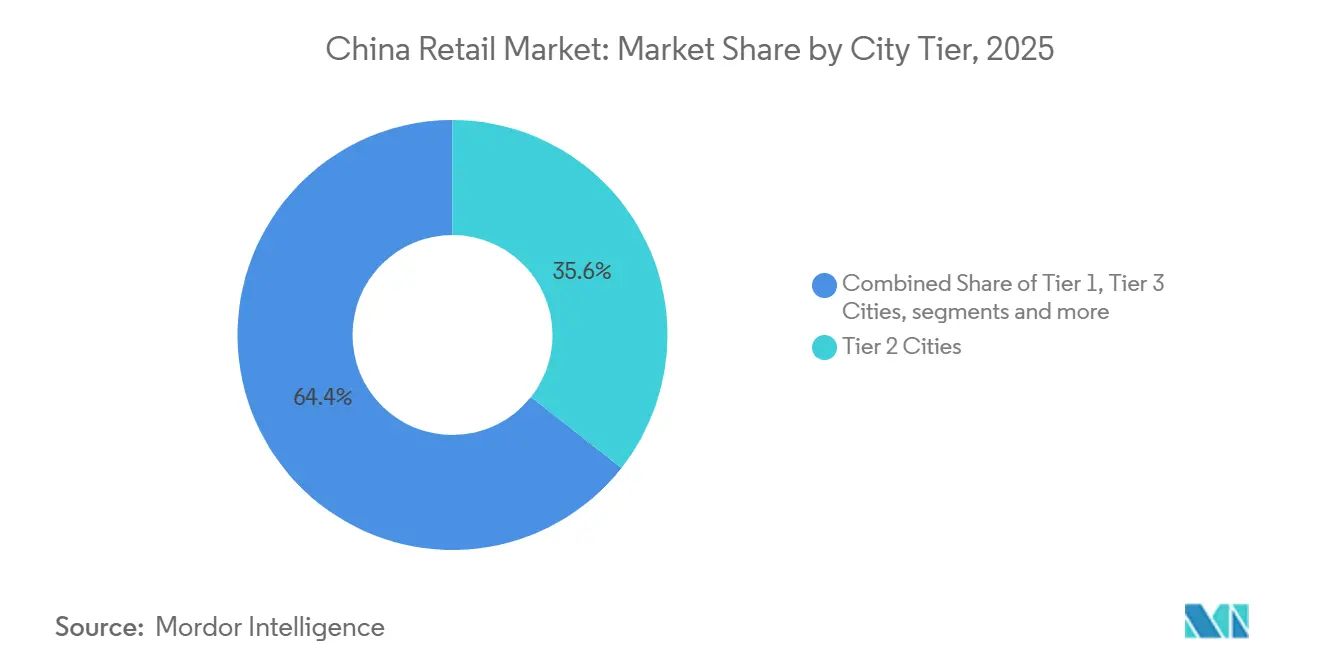

- By city tier, Tier 2 cities accounted for 35.62% of China retail market share in 2025; Tier 3 cities are advancing at an 10.88% CAGR between 2026 and 2031.

- By store format size, small-format outlets captured 81.35% of China retail market share in 2025; warehouse clubs are poised to rise at 13.92% CAGR over the forecast period.

- By geography, East China contributed 31.28% in the China retail market in 2025, and Southwest China is projected to post the fastest regional expansion at a 4.98% CAGR through 2031.

- Alibaba, JD.com, Sun Art, Walmart and Yonghui jointly controlled more than half of sector revenue in 2025, underscoring scale advantages in logistics and technology.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower-tier cities rapidly embrace social and live-stream commerce | +1.8% | Tier 3–5 cities, concentrated in central and western provinces | Medium term (2-4 years) |

| Membership-based warehouse clubs are boosting the average basket size | +1.2% | Tier 1–2 cities, expanding into Tier 2 provincial capitals | Long term (≥ 4 years) |

| Demand from the silver economy is propelling premium health and wellness categories | +1.0% | National, with early gains in East China and major urban centers | Long term (≥ 4 years) |

| 'Smart Retail' initiatives and digital-yuan trials drive omnichannel growth | +0.9% | National rollout, pilot cities include Shenzhen, Suzhou, Xiong’an, Chengdu | Short term (≤ 2 years) |

| Autonomous stores and group-buy models see rising adoption | +0.7% | Urban centers nationwide, especially Beijing, Shanghai, Guangzhou | Medium term (2-4 years) |

| Tourism policies revive experiential retail | +0.6% | Hainan Province and major tourist cities, including Beijing, Shanghai, and Guangzhou | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lower-tier cities rapidly embrace social and live-stream commerce

Livestreaming e-commerce in China reached USD 807 billion in 2024 and drew 833 million users, which underscores how short video and live hosts have become embedded in shopping behavior. Lower-tier markets are driving net-new adoption as platforms tailor content and logistics to local preferences outside the largest metro areas[2]Source: USDA Foreign Agricultural Service, “Selling in China, The Rise of Livestreaming E-commerce,” USDA FAS, apps.fas.usda.gov . Category penetration has moved beyond beauty and apparel to staples and home care as anchors, which broadens the total addressable base for the China retail market. Douyin’s commerce ecosystem has scaled by pairing discovery with instant conversion, and brands are rebalancing media budgets toward creator-led formats to reach new buyers. Municipal programs that back last-mile networks are also enabling faster delivery and more reliable fulfillment in counties and townships that were previously underserved. As a result, the China retail market is seeing an influence shift from pure price competition to engagement quality and authenticity at the point of content.

Membership-based warehouse clubs are boosting the average basket size

Warehouse-club sales crossed USD 42.6 billion (CNY 300 billion) in 2024, and are steadily increasing their share of family grocery trips in top cities. Sam’s Club reported GMV above USD 17.0 billion (CNY 120 billion) in 2025, and it added 10 locations in 2025 with plans for more than 10 openings in 2026 to widen access for urban families[3]FoodTalks, “Marriott International Expands Luxury Portfolio in Asia-Pacific,” FoodTalks, https://www.foodtalks.cn/en/news/60139 . Costco operated seven warehouses in China by late 2025, and a global plan for 35 new locations in fiscal 2026 included a meaningful allocation to China, which signals sustained confidence in premium bulk. Membership fees build switching costs while curated assortments, private labels, and perceived value lift basket size in ways that traditional hypermarkets struggle to match. These retailers are also blending app-based ordering with rapid delivery from club stores, which expands their catchment beyond immediate neighbourhoods. This combination is raising the bar for in-store experience and supply-chain efficiency in the China retail market

Demand from the silver economy is propelling premium health and wellness categories

China counts more than 300 million residents aged 60 and older today, and this cohort is emerging as a decisive force across categories linked to wellness, nutrition, and convenience[4]Source: Xinhua News Agency Staff, “Tourism Services for Elderly Rose in H1 2025,” Xinhua, english.news.cn. The silver-economy policy agenda advanced at the start of 2026 with a package of 14 measures that promote age-friendly products, services, and home upgrades, which encourages retailers to expand targeted assortments. Travel and leisure services designed for seniors recorded strong year-on-year gains in the first half of 2025, and fitness and wellness offers also grew as activity and health priorities rose among retirees. This has redirected merchandising toward low-sodium foods, joint-care supplements, mobility aids, and accessible packaging that lowers friction in the store. Retailers are beginning to translate these needs into store layouts with wider aisles and better seating, along with clearer signage and service desks. Premiumization appears earliest in coastal provinces, while value-focused variants gain traction in central and western regions, which together shape a durable growth pocket for the China retail market.

'Smart Retail' initiatives and digital-yuan trials drive omnichannel growth

The digital yuan surpassed 3.48 billion cumulative transactions and USD 2.37 trillion (CNY 16.7 trillion) in value by November 2025, which reflects fast-rising consumer familiarity and merchant acceptance. Retail pilots in cities such as Shenzhen, Suzhou, Xiong’an, and Chengdu have spurred upgrades to point-of-sale terminals and back-end systems so that stores can accept e-CNY alongside cards and mobile wallets. Lower interchange-like fees and faster settlement are commonly cited benefits, and these have started to tip the cost-of-acceptance in favor of the sovereign digital currency in select stores. The policy backdrop is supportive as authorities refine governance and infrastructure for e-CNY in 2026, which reduces uncertainty for mid-size chains planning payment-stack overhauls. These developments encourage unified commerce platforms that integrate inventory, checkout, and reconciliation across in-store and online journeys. As adoption scales, the China retail market will capture tangible working-capital and data-quality advantages that strengthen omnichannel economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retailers face shrinking margins as e-commerce platforms engage in fierce price wars | -1.5% | National, acute on Alibaba, JD.com, Meituan | Short term (≤ 2 years) |

| A declining working-age population is creating substantial challenges | -0.8% | National, most severe in Northeast China | Long term (≥ 4 years) |

| Stricter enforcement of data privacy and influencer marketing regulations is increasing compliance expenses | -0.6% | National, with enforcement focus in East and South China hubs | Medium term (2-4 years) |

| Rural-urban logistical gaps are constraining the expansion of cold-chain infrastructure for fresh groceries | -0.5% | Rural areas and Tier 4–5 cities in Central, Southwest, Northwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Retailers face shrinking margins as e-commerce platforms engage in fierce price wars

Rising subsidy spend in 2025 pushed platform competition into a loss-making phase that strained marketplace economics across categories. Meituan reported an operating loss of USD 2.8 billion (CNY 19.8 billion) in the third quarter of 2025, which reflected a sharp deterioration in local services margins. Alibaba’s operating profit fell from USD 5.0 billion (CNY 35.2 billion) to USD 0.8 billion (CNY 5.4 billion) in the same quarter, as cost discipline and lower take-rates weighed on earnings. Total subsidies and sales expenses across major platforms exceeded USD 14.2 billion (CNY 100 billion) in the second and third quarters of 2025 and are well above what most brick-and-mortar chains can match. Authorities published guidance in mid-2025 to rein in irrational discounting, though enforcement and platform responses vary across regions and product lines. For physical retailers, the practical response has been to accelerate omnichannel options and lean-format pilots while seeking more resilient price architecture in-store for the China retail market.

A declining working-age population is creating substantial challenges

Population decline and aging continue to reshape the demand base, with the working-age share dropping over the past decade and dependency ratios moving higher. National statistics and multilateral assessments point to pronounced aging in Northeast provinces, where factory closures and youth out-migration depress local consumption. A smaller inflow of young households into peak spending years reduces the long-run lift from categories like baby products and entry-level appliances. The silver economy partly offsets this effect by shifting wallet share toward health and wellness, home adaptation, and travel for retirees. Retailers that adjust assortments and store design for seniors can capture margin-rich categories while steadying volumes in everyday goods. These demographic realities are embedded in the medium-term outlook for the China retail market and call for balanced growth strategies across age cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Electronics Outpace Food and Beverage Maturity

Food and beverages led with a 30.72% revenue share in 2025 as core staples maintained dependable frequency while the faster-moving device cycle lifted home electronics into the top growth slot for the China retail market. Consumer electronics and appliances are projected to expand at a 9.23% CAGR through 2031 as connected devices and energy-saving upgrades stimulate replacement demand in urban households. Appliance retail sales rose strongly through 2025, supported by trade-in incentives and rising smart-home adoption, which strengthened the category’s pull on discretionary budgets. Brands that shift toward efficient motors, AI-enabled features, and streamlined user interfaces have seen better sell-through in mid- to high-end tiers. Food and beverages remain a stable foundation and benefit from digital merchandising that pairs promotions with local tastes and dietary trends. The China retail market is balancing value and premium demand as households manage budgets and still trade up in categories that improve daily routines.

Assortments now reflect a wider health and wellness span that includes lower-sugar beverages, high-fiber cereals, and functional supplements without crowding out core staples. In personal and household care, recovery is underway as consumers rediscover store formats that showcase newness and credible claims with sampling and beauty services. Apparel and footwear show a split between value basics in community retail and performance wear in malls, helped by e-commerce try-on tools that cut returns. Within electronics, white goods and small cooking appliances are benefiting from energy-label upgrades and the trade-in push that accelerates product lifecycles. The China retail industry will continue to see crossovers across home, wellness, and convenience themes as brands reframe benefits for multi-generational households.

By Distribution Channel: E-commerce Dominance Faces Discount-format Disruption

E-commerce platforms held a 34.15% share of the China retail market in 2025 and continue to scale mobile-first shopping journeys with faster checkout and integrated content. Discount and membership-club stores are forecast to grow at a 13.35% CAGR through 2031 as bulk value and private labels pull share from hypermarkets and general supermarkets. The China retail market shows a higher mix of impulse and replenishment orders on apps, while larger planned stock-ups shift to clubs where unit economics favor family baskets. Retailer-owned apps and mini-programs are improving post-purchase service and returns, which strengthens lifetime value in categories like beauty and small appliances. These changes reinforce a more barbelled channel mix and put a premium on logistics, data science, and stock discipline.

Brick-and-mortar channels are stabilizing with remodels, curated assortments, and more foodservice inside supermarkets to improve visit satisfaction. Convenience stores reported year-on-year sales growth through 2025, and top chains kept opening small-footprint sites near residential clusters and transit hubs. Unmanned and autonomous formats are approaching scale, with the unmanned retail segment expected to exceed USD 7.0 billion (CNY 50 billion) in 2025, as software cuts labor and reduces shrinkage. Clubs combine store traffic with on-demand delivery from in-store picking to extend reach, while specialist stores in categories like health supplements use the service to defend niche positioning. Multi-format operators are building synergies around shared supply chains and data, which is key to managing cost-to-serve across frequent and infrequent trip missions in the China retail market.

By City Tier: Lower-tier Volume Offsets Higher-tier Saturation

Tier 2 cities accounted for 35.62% of the China retail market share in 2025, which demonstrates the durable pull of provincial capitals where wage levels and rents support healthy store-level returns. Tier 3 cities are advancing at a 10.88% CAGR between 2026 and 2031 as value-driven consumers in lower tiers fuel the next leg of volume growth for the China retail market. Retailers are tailoring price ladders, pack sizes, and local brands to match preferences in city clusters that have been underserved by premium formats. Livestreaming and community group-buy have widened access and coverage in counties near these cities by pooling demand for fast replenishment. Government programs that finance logistics and rural revitalization continue to alleviate delivery constraints and improve service quality outside Tier 1. Retailers that balance price, freshness, and delivery consistency will sustain loyalty in these fast-growing markets.

Tier 1 cities will continue to serve as test beds for autonomous stores, high-service clubs, and experiential malls, although growth is moderating due to saturation in core categories. Tier 4 and below markets are benefiting from e-commerce enablement that balances last-mile cost and delivery time, which stabilizes fresh grocery fulfillment. Compliance obligations for data privacy and cybersecurity are now part of checklists for store rollouts into new provinces and smaller cities, which raises initial costs but reduces future enforcement risk. Retailers are building secure data pipelines for mobile engagement in these regions to protect customer trust and marketing effectiveness. This balanced approach positions the China retail industry to continue expanding even with uneven demand and more rigorous compliance

By Store Format Size: Small-format Ubiquity Versus Warehouse-club Momentum

Small-format outlets captured 81.35% of the China retail market share in 2025, which reflects the high frequency of top-up trips and the importance of neighbourhood proximity. Warehouse clubs and other large-format sites are set to rise at a 13.92% CAGR during the forecast period as family stock-ups consolidate into trips that seek premium value and imported staples in bulk. Sam’s Club recorded GMV above USD 17.0 billion (CNY 120 billion) in 2025, and its store pipeline for 2026 shows continued confidence in the format’s economics. Convenience stores and small supermarkets are making better use of data and automation to refine assortments and improve on-shelf availability despite tight footprints. These operational gains are essential to defend share as clubs draw larger baskets and increase category authority with private labels in the China retail market.

Mid-sized supermarkets are pivoting into fresh, ready-to-eat, and foodservice-in-store concepts that create reasons to visit beyond weekly top-ups. Unmanned checkout and AI-based replenishment have started to lower labor requirements in small formats while maintaining service windows that match commuter schedules. Discount-led snack and essentials stores continue to add locations in lower-tier markets on the back of simple layouts, quick turns, and a sharp value pitch. Large-format clubs are embedding digital engagement through scan-and-go and next-day delivery to capture more of the total household basket. Operators are using centralized distribution and data science to coordinate across three format bands so that each store type performs a defined trip mission in the China retail market

Geography Analysis

East China led with a 31.28% share of the China retail market in 2025, supported by manufacturing clusters in Jiangsu, Zhejiang, and Shanghai, and higher disposable incomes that lift premium categories. Southwest China posted the fastest regional CAGR at 4.98% through 2031, with urbanization in Chengdu, Chongqing, and Kunming, and better transport connectivity that widens access to modern retail. Appliance upgrade cycles and smart-home adoption remain stronger in coastal provinces, which supports above-average sell-through in white goods and small appliances. Retailers in city clusters across East China keep building delivery density and last-mile quality, which raises service consistency for perishable and bulky goods. The China retail market will continue to see provincial-speed differences as logistics and incomes converge across regions at different paces.

North China contributes steady growth from Beijing and Tianjin as format innovation offsets slower category expansion in a mature urban base. South China, anchored by Guangzhou and Shenzhen, benefits from cross-border flows with Hong Kong and Macau and a deep base of digitally engaged shoppers. Central and Western regions are growing foodservice and experiential retail spend as new housing completions and infrastructure projects raise traffic in provincial capitals. Retailers are aligning inventory and service models to city-level patterns within each region, which improves conversion and returns. These moves keep the China retail market focused on city clusters where density and logistics support economies of scale.

Northeast China is confronting demographic decline and elevated local debt risks that temper store expansion and mall performance. National and multilateral reporting indicates steeper aging and out-migration in Liaoning, Jilin, and Heilongjiang, which shapes flat or shrinking demand for discretionary goods in these provinces. Hainan is a structural outlier because policy changes have accelerated duty-free shopping, with H1 2025 duty-free sales of USD 4.6 billion (CNY 32.396 billion0. The island-wide customs closure launched on December 18, 2025, raised the number of tariff-free items to 6,637 and drove USD 0.7 billion (CNY 4.86 billion) in sales in the first month. A zero-tariff policy effective February 2026 grants each resident an annual quota of USD 1,418 (CNY 10,000), and is expected to redirect more premium spend to domestic stores. Hainan’s tourism reached 106 million visits in 2025 and total spending of USD 32.0 billion (CNY 225.4 billion), which consolidates the island’s position as a duty-free destination that supports the China retail market.

Competitive Landscape

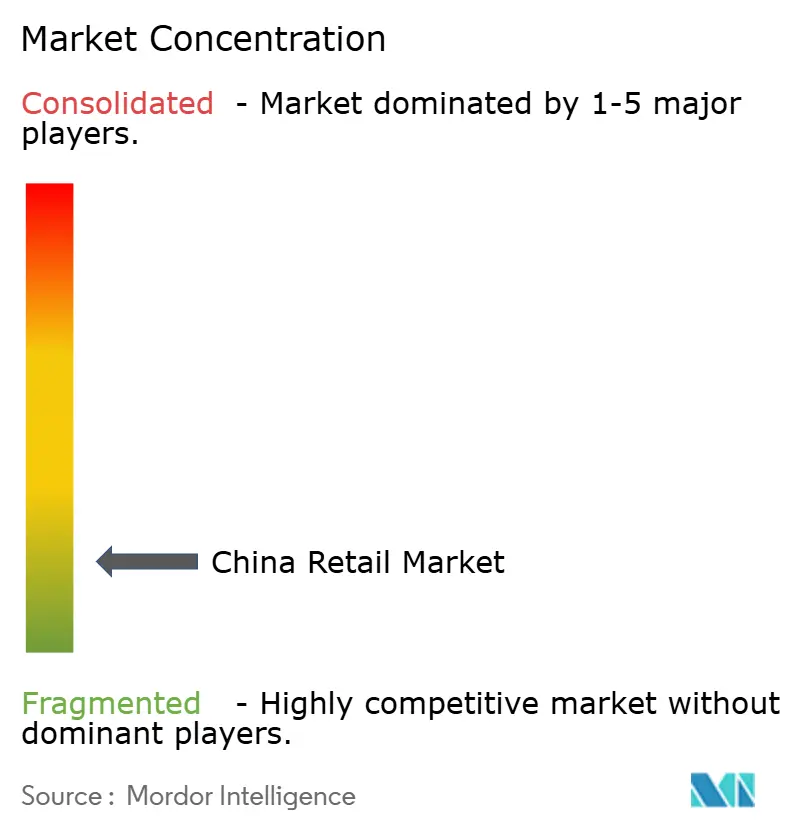

The China retail market remains fragmented even as large platforms and national chains extend their reach through apps and new formats. Company shares remain distributed across a long tail of regional and category specialists, which keeps store-level competition intense. E-commerce led growth in digital channels in 2025, while membership clubs expanded in top cities and moved into more Tier 2 locations. The latest segmentation estimates reinforce this fragmentation and show that national concentration has not spiked despite merger and rollout activity. That structure influences strategy, as many players favor targeted format expansion over broad attempts to win in every category.

Scale players are using capital and data to build durable advantages in logistics, private label, and loyalty economics. Sam’s Club opened 10 stores in 2025, delivered GMV above USD 17.0 billion (CNY 120 billion), and plans more than 10 openings in 2026, which deepens its coverage in the country’s most attractive trade areas. Costco operated seven warehouses in China by late 2025, and a plan for 35 global openings in fiscal 2026 includes a meaningful China allocation, which demonstrates conviction in the bulk retail proposition. On the foodservice side, Restaurant Brands International and CPE Capital formed a joint venture to accelerate Burger King China, with funding earmarked for store expansion over the next decade. These moves highlight how capability-led expansion in real estate and supply chains can outlast short-term subsidy cycles in the China retail market.

Price competition among platforms sharpened in mid-2025 and imposed heavy subsidy costs that weighed on profitability and cash flow. Meituan and Alibaba both reported margin compression linked to higher subsidies and sales expenses, which forced recalibration of growth-at-any-cost tactics. Regulators issued guidance in 2025 to curb irrational discounting, which aims to improve market order and reduce wasteful spending over the near term. Autonomous retail and vending are scaling as operators seek labor-light ways to expand reach, and the unmanned retail segment is expected to exceed USD 7.0 billion. Retailers are also investing in data and cybersecurity management to comply with updated rules that took effect at the start of 2026, which tightens marketing and data-handling practices. These conditions reinforce the need for resilient gross margins, diversified channels, and disciplined capital allocation across the China retail market.

China Retail Industry Leaders

Alibaba Group Holding Ltd.

Walmart Inc.

JD.com Inc.

Sun Art Retail Group Ltd.

Yonghui Superstores Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Hainan Province implemented a zero-tariff policy effective February 2026 that grants each resident a USD 1,418 (CNY 10,000) annual quota, complementing the island-wide customs closure launched in December 2025.

- January 2026: Government advanced a package of measures to support the silver economy and promote age-friendly goods and services that expand senior-oriented retail offerings.

- December 2025: Hainan launched island-wide customs closure on December 18, 2025, expanded tariff-free items from 1,900 to 6,637, and recorded USD 0.7 billion (CNY 4.86 billion) in duty-free sales in the first month.

- November 2025: Burger King China and CPE Capital formed a joint venture with CPE investing USD 350 million to accelerate expansion over the next decade.

China Retail Market Report Scope

Retail is the sale of goods and services to consumers, in contrast to wholesaling, which is a sale to business or institutional customers. The report on the China retail industry provides a comprehensive evaluation of the market, with an analysis of the segments in the market. Moreover, the report provides drivers, restraints, and the competitive profile of the key players.

The China retail market is segmented by products and distribution channels. By products, the market is sub-segmented into food and beverages, personal and household care, apparel, footwear and accessories, furniture, toys and hobbies, electronic and household appliances, and other products. By distribution channels, the market is sub-segmented into supermarkets/hypermarkets, convenience stores, department stores, specialty stores, online, and other distribution channels. The report offers market size and forecasts in value (USD) for all the above segments.

By Product Category

| Food & Beverages | Fresh Food |

| Packaged Food | |

| Beverage - Alcoholic | |

| Beverage - Non-Alcoholic | |

| Personal & Household Care | Beauty & Personal Care |

| Home Care | |

| Apparel, Footwear & Accessories | Apparel |

| Footwear | |

| Accessories & Luxury Goods | |

| Furniture, Toys & Hobby | Furniture & Home Decor |

| Toys & Baby Products | |

| Sports & Leisure Equipment | |

| Consumer Electronics & Appliances | Mobile & IT |

| Home Appliances | |

| Other Electronics | |

| Other Products |

By Distribution Channel

| Supermarkets & Hypermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Discount & Membership Club Stores |

| E-commerce Online Marketplaces |

| Other Channels (Direct selling, vending, community group-buy) |

By City Tier

| Tier 1 Cities |

| Tier 2 Cities |

| Tier 3 Cities |

| Tier 4 & Below |

By Store Format Size

| Large-Format |

| Mid-Sized |

| Small-Format |

By Region (China)

| East China |

| North China |

| Northeast China |

| South China |

| Central China |

| Southwest China |

| Northwest China |

| By Product Category | Food & Beverages | Fresh Food |

| Packaged Food | ||

| Beverage - Alcoholic | ||

| Beverage - Non-Alcoholic | ||

| Personal & Household Care | Beauty & Personal Care | |

| Home Care | ||

| Apparel, Footwear & Accessories | Apparel | |

| Footwear | ||

| Accessories & Luxury Goods | ||

| Furniture, Toys & Hobby | Furniture & Home Decor | |

| Toys & Baby Products | ||

| Sports & Leisure Equipment | ||

| Consumer Electronics & Appliances | Mobile & IT | |

| Home Appliances | ||

| Other Electronics | ||

| Other Products | ||

| By Distribution Channel | Supermarkets & Hypermarkets | |

| Convenience Stores | ||

| Department Stores | ||

| Specialty Stores | ||

| Discount & Membership Club Stores | ||

| E-commerce Online Marketplaces | ||

| Other Channels (Direct selling, vending, community group-buy) | ||

| By City Tier | Tier 1 Cities | |

| Tier 2 Cities | ||

| Tier 3 Cities | ||

| Tier 4 & Below | ||

| By Store Format Size | Large-Format | |

| Mid-Sized | ||

| Small-Format | ||

| By Region (China) | East China | |

| North China | ||

| Northeast China | ||

| South China | ||

| Central China | ||

| Southwest China | ||

| Northwest China | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the China retail market?

The China retail market size is USD 2.27 trillion in 2026 and is projected to reach USD 3.34 trillion by 2031 at an 8.06% CAGR.

Which product and channel segments are leading growth across categories?

Food and beverages led with a 30.72% revenue share in 2025 while consumer electronics and appliances is projected to grow at a 9.23% CAGR; e-commerce held a 34.15% channel share in 2025 and discount and membership-club stores are forecast at a 13.35% CAGR.

How is the digital yuan influencing retail operations?

The e-CNY surpassed 3.48 billion transactions totaling USD 2.37 trillion by late 2025, which is encouraging payment-stack upgrades and lower acceptance costs for merchants.

Which city tiers offer the strongest medium-term momentum?

Tier 2 cities held 35.62% of the China retail market in 2025 and Tier 3 cities are advancing at a 10.88% CAGR between 2026 and 2031 as lower-tier demand scales.

Which formats are set to gain share in 2026 and beyond?

Membership clubs and discount formats are positioned to gain as families consolidate stock-ups into bulk trips and small formats expand with automation and curated assortments in the China retail market.

What policy moves could lift consumption in 2026?

Consumer-goods trade-in allocations increased after 2025 sales reached USD 368.8 billion, and Hainan’s zero-tariff policy added USD 1,418, annual quota per resident, which supports premium retail spend.

Page last updated on: