Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

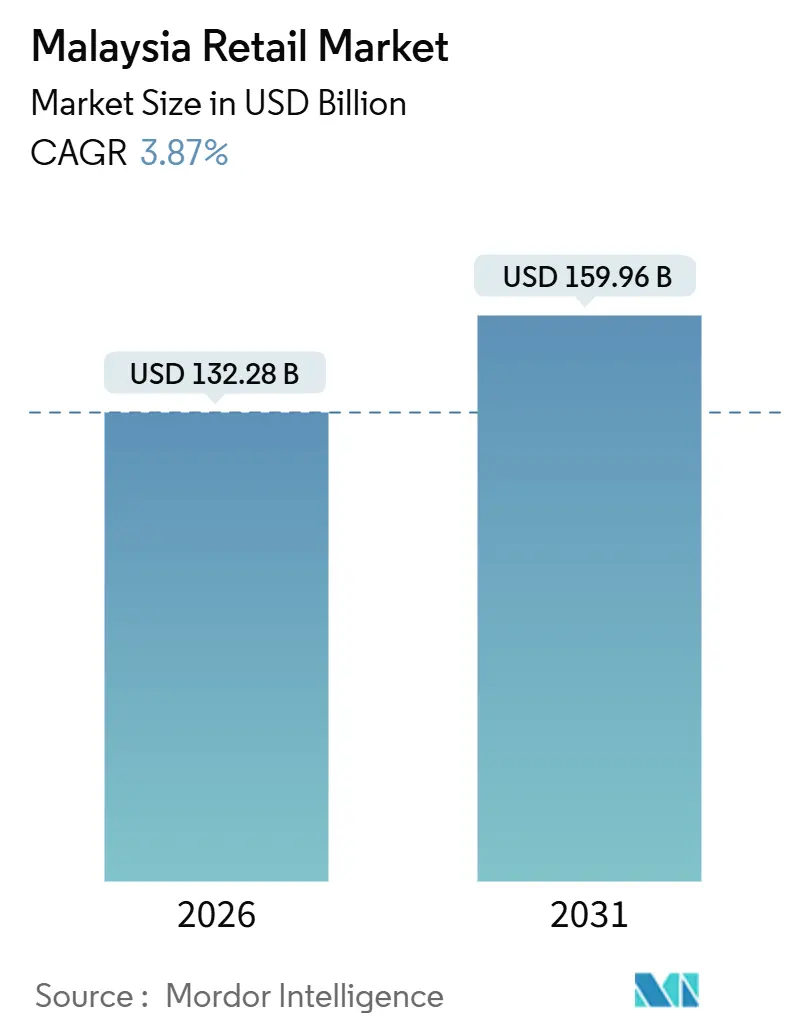

| Market Size (2026) | USD 132.28 Billion |

| Market Size (2031) | USD 159.96 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Retail Market Analysis by Mordor Intelligence

The Malaysia retail market size is USD 132.28 billion in 2026 and is projected to reach USD 159.96 billion by 2031 at a 3.87% CAGR. Growth reflects an active transition toward digital commerce, proximity-led formats, and policy shifts that change how consumers and retailers interact. Consumers continue to rebalance budgets toward essentials, guided by cost-of-living pressures and persistent price sensitivity across categories. Consumer inflation moderated to 1.83% in 2024, down from 2.49% in 2023, but essentials such as food, housing, utilities, and transport still account for over 23% of the Consumer Price Index (CPI) basket, keeping value-seeking behavior elevated. These dynamics have driven retailers to expand private labels, entry-price packs, and promotional intensity, particularly in grocery, personal care, and household segments. Policy adjustments around indirect taxes shape pricing and operating costs, which prompts retailers to expand value ranges and efficiency programs.

Key Report Takeaways

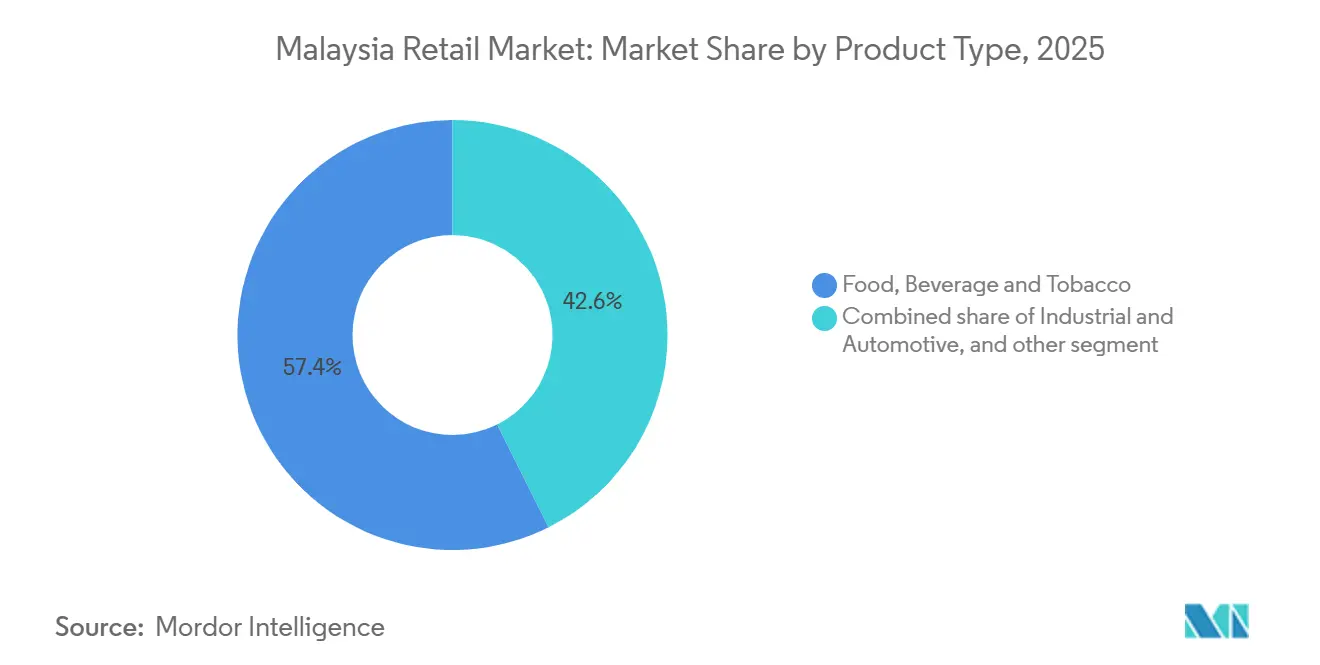

- By product type, food, beverage, and tobacco led with 57.39% of the Malaysia retail market share in 2025; electronic and household appliances are projected to expand at a 4.65% CAGR through 2031.

- By retail channel, traditional mom-and-pop stores held 48.37% of the Malaysia retail market in 2025; e-commerce and others recorded the highest projected CAGR at 5.01% through 2031.

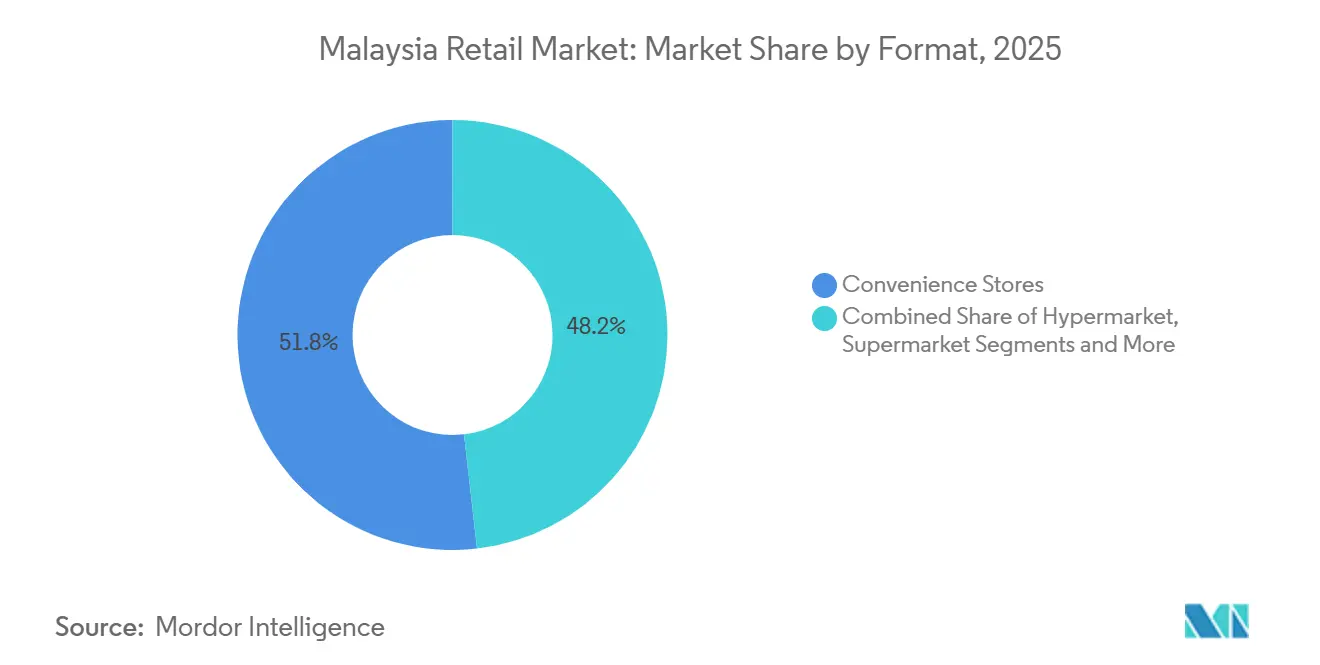

- By format, convenience stores commanded 51.82% of the Malaysian retail market share in 2025 and are advancing at a 5.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & middle-class expansion | +1.0% | National, strongest in Klang Valley, Penang, Johor, and fast-growing secondary cities | Medium to Long term (3–5 years) |

| Government incentives are accelerating e-wallet adoption | +0.8% | National, with stronger urban penetration and gradual rural catch-up | Medium term (2-4 years) |

| Rapid urbanisation is fuelling mini-mart penetration | +0.7% | Asia-Pacific core, with momentum in Northern Peninsular and East Malaysia | Long term (≥ 4 years) |

| EPF Account 3 withdrawals boosting near-term spending | +0.5% | National, with early gains in Klang Valley, Johor Bahru, Penang | Short term (≤ 2 years) |

| E-commerce & omnichannel retail boom | +0.9% | National, concentrated in larger urban markets | Medium term (2-4 years) |

| 99 Speed Mart-led logistics efficiencies are lowering shelf prices | +0.6% | Nationwide dense store network, particularly in suburban and semi-urban Malaysia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Middle-Class Expansion

Private consumption remains a core macro anchor and continues to contribute a large share of GDP, with policy support and labor-market stability underpinning spending in 2026. Wage measures and targeted assistance have helped support household budgets, while unemployment stabilized at low levels through late 2025. These trends support essential categories first, which is consistent with the observed resilience in food and grocery baskets during recent price cycles. Malaysia's private consumption, constituting 61% of GDP, is forecast to expand 5.0% in 2025 and 5.1% in 2026, anchored by civil servant salary adjustments under SSPA Phase 2, a minimum wage hike to USD 380.2 (MYR 1,700), and targeted assistance programs[1] Ministry of Finance Malaysia Economic Outlook 2026 https://www.midf.com.my/sites/corporate/files/2025-10/budget_2026-mbsbr-111025.pdf..

Government Incentives Accelerating E-Wallet Adoption

Interoperable QR payments continue to lower acceptance friction for small merchants, expanding cashless coverage across convenience formats and neighborhood stores. As of 2024–2025, Malaysia’s national DuitNow QR network supports over 2.5 million merchant touchpoints nationwide, making it one of the most widely deployed interoperable QR systems in Southeast Asia. Transaction activity highlights the scale of adoption. During 2024, DuitNow QR transaction volumes expanded at double-digit quarterly growth rates, with cross-border QR usage alone rising about 50% quarter-on-quarter. In the peak December 2024 travel and shopping period, Malaysian merchants using DuitNow QR recorded approximately 6-fold year-on-year revenue growth from participating inbound wallets, reflecting higher ticket sizes and faster checkout throughput[2][Rachel Tan, Airwallex Guide to DuitNow, June 2025] https://www.airwallex.com/my/blog/duitnow.. Government digitalization initiatives have supported merchant onboarding and raised awareness of the benefits of QR acceptance for small businesses. National payment rails now handle scaled transaction volumes, which underscores the resilience and reach of the infrastructure. Providers continue to expand features such as instant payment confirmation devices and merchant dashboards, which support bookkeeping and cash management for micro and small retailers. The combined effect is broader acceptance, better visibility of sales flows, and a higher cashless share among daily-use categories.

Rapid Urbanisation Fuelling Mini-Mart Penetration

Urban population concentration continues to support high-frequency shopping in proximate retail formats focused on fast-moving essentials. In 2024, approximately 77-78% of Malaysia’s population lived in urban areas, rising further to about 79.2% in 2025 in absolute population terms, placing Malaysia among the most urbanized markets in Southeast Asia. This density structurally favors mini-marts and neighborhood convenience stores over large-format retail. Store-level transaction counts and same-store growth have recovered since pandemic-era disruptions, which reflects the draw of convenience and value. Management guidance from leading banners indicates further white space in secondary towns and East Malaysia before format saturation.

E-Commerce & Omnichannel Retail Boom

Malaysia’s online retail continues to expand, led by mobile-first behavior and platform investments that improve service levels. Consumer adoption is supported by platforms and brands that guarantee authenticity, better returns, and tighter service standards in branded Mall environments. Authenticated Mall ecosystems have scaled their revenue share across Southeast Asia and are on track to take a larger slice of digital sales by 2030. Shoppers move fluidly between store visits and online research, which raises the importance of consistent pricing and service across channels. Shopee's introduction of a USD 0.11 (MYR 0.50) Platform Support Fee per order (plus 8% SST) from July 16, 2025, alongside recent commission hikes, disproportionately impacts low-priced SKUs and forces sellers to optimize average order value through bundling and minimum order quantities[3]https://seller.shopee.com.my/edu/article/25269..

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven squeeze on discretionary spend | -0.9% | National, with higher pressure on lower-income segments | Short term (≤ 2 years) |

| Margin pressure from regional e-commerce giants | -0.6% | National, concentrated in larger urban e-commerce markets | Medium term (2-4 years) |

| Labour shortages in brick-and-mortar operations | -0.4% | National, with acute effects in key commercial states | Long term (≥ 4 years) |

| SST hike on non-essentials dampens demand | -0.3% | National, with stronger effects on discretionary categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Squeeze on Discretionary Spend

Inflationary pressure through late-2025 and into 2026 has kept household budgets tight and reinforced trade-down behavior. Malaysia’s headline inflation averaged ~1.4% in 2025 and is projected to remain between 1.3% and 2.0% in 2026, indicating price stability but limited real relief for discretionary categories as essential costs absorb a large share of income. Essential baskets remain resilient, while large-ticket and lifestyle categories face slower sell-through when prices rise faster than income. In 2024, Malaysia’s median monthly household income reached ~USD 1,560, while median monthly disposable income stood at ~USD 1,330, leaving limited headroom for discretionary upgrades after housing, food, utilities, and transport expenses. Company updates show traffic gains can still occur even when average unit value softens, which supports a defense-first approach to category management. Forward guidance from official sources points to stable inflation in 2026, which should support a gradual return of discretionary spending if wage gains hold.

Margin Pressure from Regional E-Commerce Giants

Large platforms continue to shape price expectations through promotions, logistics speed, and category coverage, which compresses room for store-led discounting. Changes in platform fees and commission structures can shift seller strategies and tighten net margins for merchants that rely on marketplace traffic. Physical retailers respond with self-checkout, targeted store refreshes, and last-mile options to defend convenience and reduce queue times. Chains extend their digital storefronts and offer same-day or next-day delivery through owned apps or partners to reduce channel leakage. Scale players can absorb the upfront investment, while smaller operators face a higher hurdle rate for technology projects. The outcome is a more competitive Malaysia retail market where differentiation depends on inventory velocity, convenience, and curated experiences that justify a trip.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Essentials Anchor Volume, Electronics Lead Value Growth

Food, Beverage, and Tobacco accounted for 57.39% of the Malaysia retail market share in 2025, which underscores the resilience of essential spending as budgets tighten and households prioritize staples. The category continues to benefit from steady population growth and stable volume patterns, which support footfall in proximity and mass formats. Category management has focused on pack-size variety, private label, and basic first assortments that protect transaction counts. Operators with efficient sourcing and low distribution costs defend price points better and retain loyalty when discretionary wallets contract. These patterns reinforce a steady base in the Malaysia retail market across a volatile macro backdrop.

Electronic and Household Appliances are the fastest growing product category through 2031 and are projected to lead value growth as deferred upgrades return. The Malaysia retail market size for Electronic and Household Appliances is projected to expand at a 4.65% CAGR through 2031 as device cycles, connectivity upgrades, and home-improvement needs normalize. Retailers combine online discovery with in-store demo zones to address service and trust needs that matter in higher-ticket purchases. Inventory and last-mile coordination are key because shoppers expect rapid fulfillment that mirrors marketplace standards. As price sensitivity persists, warranties, financing options, and trade-in programs also support conversion and repeat purchase. The blend of online research and store engagement supports a sustainable path for value creation in this category.

By Retail Channel: Mom-and-Pop Resilience Meets E-Commerce Acceleration

Traditional mom-and-pop retail held 48.37% of distribution in 2025, which reflects the reach of neighborhood stores and the convenience of close-to-home shopping. The ubiquity of QR payments supports transaction growth for micro and small merchants, which improves viability and speeds checkout. Cashless acceptance through interoperable QR has expanded the customer base for these stores and reduced dependence on cash logistics. The retail industry in Malaysia continues to balance these small-format anchors with larger banners that operate regional supply chains. The result is a channel mix where local relevance and proximity maintain importance even as digital options expand.

E-commerce and others are the fastest-growing channels and are projected to expand at a 5.01% CAGR through 2031 as mobile-first habits mature. The Malaysia retail market size associated with this channel gains from widespread smartphone usage and logistics investments that shorten delivery windows. Branded Mall ecosystems that guarantee authenticity and return win a higher share of online baskets, which support premiumization even in price-sensitive times. Store-led retailers expand click-and-collect and same-day delivery to reduce leakage to marketplaces and to harness store inventories for speed. As channel lines blur, the most successful operators deliver consistent price, service, and returns across online and in-store touchpoints. This hybrid approach aligns with shopper journeys and helps sustain growth while platforms compete for attention.

By Format: Convenience Stores Dominate Volume and Growth Velocity

Convenience stores led the 2025 landscape with 51.82% of the Malaysia retail market share, and the format is projected to expand at a 5.11% CAGR through 2031. The format’s strength reflects daily-use missions, late-hour access, and location density across urban corridors and secondary towns. Chains leverage integrated supply chains, multi-DC coverage, and direct sourcing to compress costs and defend shelf prices. Value-focused mini-markets add width to assortments while keeping floor plans simple to speed replenishment and shopping time. These factors sustain high visit frequency and predictable sell-through even when discretionary budgets soften.

The Malaysia retail market size tied to convenience formats also benefits from capital efficiency and fast store payback, which supports steady network expansion. Scale banners continue to open outlets in under-penetrated regions while enhancing last-mile replenishment through new distribution centers. Company reports show transaction counts per outlet rising alongside same-store growth as mobility normalizes. Larger groups invest in automation and data to refine inventory turns and reduce shrinkage, which supports value-led price positions. These moves reinforce a cycle where lower operating costs translate into competitive pricing and higher throughput across the network.

Geography Analysis

Klang Valley remains the center of gravity for the Malaysia retail market, given population density, income concentration, and retail infrastructure. Retail corridors in Kuala Lumpur and Selangor support both mass and specialty formats, which encourages a mixed store portfolio across banners. Operators report ongoing store refreshes, new concept launches, and mall projects that increase retail space and broaden tenant mixes. The pipeline includes upgrades and new centers that should add capacity and lift footfall in the medium term. A mix of domestic demand and inbound tourism linked to Visit Malaysia 2026 supports higher traffic in key malls and shopping streets[4].

Johor Bahru and Penang provide additional momentum as cross-border and tourism flows benefit store traffic and dining corridors. Johor’s proximity to Singapore lifts weekend footfall and supports premium categories, while family spending anchors grocery and home needs. Penang’s blend of manufacturing wages and heritage-led tourism creates steady demand for essentials and lifestyle goods. Retailers tailor assortments and price ladders to local income profiles, which supports steady conversion across formats. The Malaysia retail market extends north and east as chain coverage and DC networks improve delivery economics.

East Malaysia remains under-penetrated relative to Peninsular Malaysia and represents a priority for network expansion. Company disclosures confirm active investment in distribution capacity to serve Sarawak and Sabah with shorter routes and higher service levels. As mini-markets and specialty chains add outlets, consumers gain access to broader assortments and digital payments at neighborhood stores. The retail industry in Malaysia will benefit from improved logistics reliability and lower cost-to-serve as DCs ramp to full utilization. Broader QR acceptance and merchant onboarding also support the adoption of cashless transactions across smaller towns. Retailers with the ability to scale assortments and sustain low prices will convert growth in these markets into durable share.

Competitive Landscape

The Malaysia retail market remains moderately fragmented at the national level, while scale at the banner level matters for cost control, sourcing, and service quality. Essentials-focused mini-markets grow on the back of logistics density and procurement leverage, which protect price positions. Hypermarket and supermarket banners maintain one-stop missions and integrate same-day delivery to defend convenience. Specialty retailers lean on category authority, private label, and store experiences to support traffic and margin. E-commerce platforms raise service benchmarks and influence price perception, which compels store-led retailers to refine their own digital journeys.

Capabilities that separate leaders include integrated supply chains, the use of data to manage assortments, and new fulfillment models that speed delivery. Self-checkout deployments and app-linked loyalty programs reduce queues and personalize value across owned channels. Store refreshes and remodels support discovery and lift dwell time, which helps experiential categories and food traffic. Company disclosures show investments in automation and new warehouses to strengthen supply chain resilience and reduce handling costs. These moves fit a broader pattern where operational discipline funds sharper pricing and customer-service enhancements. The Malaysia retail market rewards banners that combine value pricing with reliable service and consistent availability.

Strategic moves since 2025 highlight the focus on scale, logistics, and digital enablement. 99 Speed Mart reports a dense DC network, regular fleet upgrades, and continued outlet additions to extend reach and improve replenishment speed. MR D.I.Y. delivered record quarterly profit on the back of store openings and margin gains tied to procurement, while preparing an automated warehouse for full operations. AEON rolled out hundreds of self-checkout units, sustained high occupancy in malls, and expanded omnichannel coverage to reduce friction across shopping missions. The Malaysia retail market continues to see alliances and product extensions that improve loyalty and create convenience across touchpoints.

Malaysia Retail Industry Leaders

99 Speed Mart Retail Holdings

AEON Co. (M) Bhd

Tesco / Lotus’s Malaysia

GCH Retail (Giant)

Mydin Mohamed Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 99 Speed Mart accelerated expansion plans after its late-2024 listing, supported by a larger outlet base, new distribution centers, and a stronger balance sheet. Disclosures confirm progress on new logistics sites to serve East Malaysia and continued store openings to deepen national coverage.

- April 2025: AEON Co. (M) Bhd implemented a dual-pronged strategy, balancing new openings with asset revitalization and omnichannel expansion. In FY2024, AEON reported increased revenue and profit after tax, supported by high occupancy rates and positive rent adjustments in malls. The company opened and renovated stores while introducing concepts focused on customer discovery and family needs. Its pipeline included a new mall in Kuala Lumpur and expansions at select assets.

- May 2025: MR D.I.Y. Group reported revenue and profit growth in Q1 FY2025, driven by new stores and like-for-like gains. The company opened more than a hundred stores in 2025 and improved its gross margin due to procurement scale and currency support. An automated warehouse in Selangor progressed toward full operation to enhance supply chain efficiency.

- November 2024: Payments Network Malaysia reported continued expansion in e-payments and recognized leading merchants and platforms at the Malaysian e-Payments Excellence Awards.

Malaysia Retail Market Report Scope

The retail market encompasses the sale of goods and services directly to end consumers through physical stores, online platforms, and other sales channels.The report on the Malaysian retail sector provides a comprehensive evaluation of the market, with an analysis of the segments in the market. Moreover, the report also provides the competitive profile of the key manufacturers, along with regional analysis.

Tobacco Products; Personal Care and Household Care; Apparel, Footwear, and Accessories; Furniture, Toys, and Hobby; Industrial and Automotive; Electronic and Household Appliances; Other Products), Retail Channel (Traditional Mom and Pop Retail; Modern Trade Retail; E-Commerce and Others), and Format (Hypermarkets; Supermarkets; Convenience Stores; Department Stores; Specialty Stores; Others including Drugstore, Cash & Carry, Wholesaler).

By Product Type (Value)

| Food, Beverage, and Tobacco Products |

| Personal Care and Household Care |

| Apparel, Footwear, and Accessories |

| Furniture, Toys, and Hobby |

| Industrial and Automotive |

| Electronic and Household Appliances |

| Other Products |

By Retail Channel (Value)

| Traditional Mom and Pop Retail |

| Modern Trade Retail |

| E-Commerce and Others |

By Format (Value)

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (Drugstore, Cash & Carry, Wholesaler) |

By Region

| Peninsular Malaysia | Northern Region |

| Central Region | |

| Southern Region | |

| East Coast Region | |

| East Malaysia | Sabah |

| Sarawak | |

| Labuan |

| By Product Type (Value) | Food, Beverage, and Tobacco Products | |

| Personal Care and Household Care | ||

| Apparel, Footwear, and Accessories | ||

| Furniture, Toys, and Hobby | ||

| Industrial and Automotive | ||

| Electronic and Household Appliances | ||

| Other Products | ||

| By Retail Channel (Value) | Traditional Mom and Pop Retail | |

| Modern Trade Retail | ||

| E-Commerce and Others | ||

| By Format (Value) | Hypermarkets | |

| Supermarkets | ||

| Convenience Stores | ||

| Department Stores | ||

| Specialty Stores | ||

| Others (Drugstore, Cash & Carry, Wholesaler) | ||

| By Region | Peninsular Malaysia | Northern Region |

| Central Region | ||

| Southern Region | ||

| East Coast Region | ||

| East Malaysia | Sabah | |

| Sarawak | ||

| Labuan | ||

Key Questions Answered in the Report

What is the Malaysia retail market size and projected growth to 2031?

The Malaysia retail market size is USD 132.28 billion in 2026 and is projected to reach USD 159.96 billion by 2031 at a 3.87% CAGR.

Which product category leads the Malaysia retail market in 2025?

Food, Beverage, and Tobacco lead with a 57.39% share in 2025, reflecting the resilience of essential spending during cost-of-living pressure.

Which channel is growing fastest in the Malaysia retail market through 2031?

E-commerce and others are the fastest-growing channels, projected to expand at a 5.01% CAGR through 2031 as mobile-first habits mature and service levels improve.

Which format holds the largest share in the Malaysia retail market?

Convenience stores hold the largest share at 51.82% in 2025 and are projected to grow at a 5.11% CAGR through 2031 due to proximity, availability, and logistics scale.

What macro factor most supports retail spending in 2026?

Stable employment, targeted policy support, and ongoing digital payment adoption collectively support retail spending, with private consumption continuing as a large part of GDP.

How are retailers responding to competitive pressure from marketplaces?

Leading banners invest in self-checkout, store refreshes, and last-mile options, while expanding omnichannel services and logistics automation to protect value and convenience.

Page last updated on: