Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

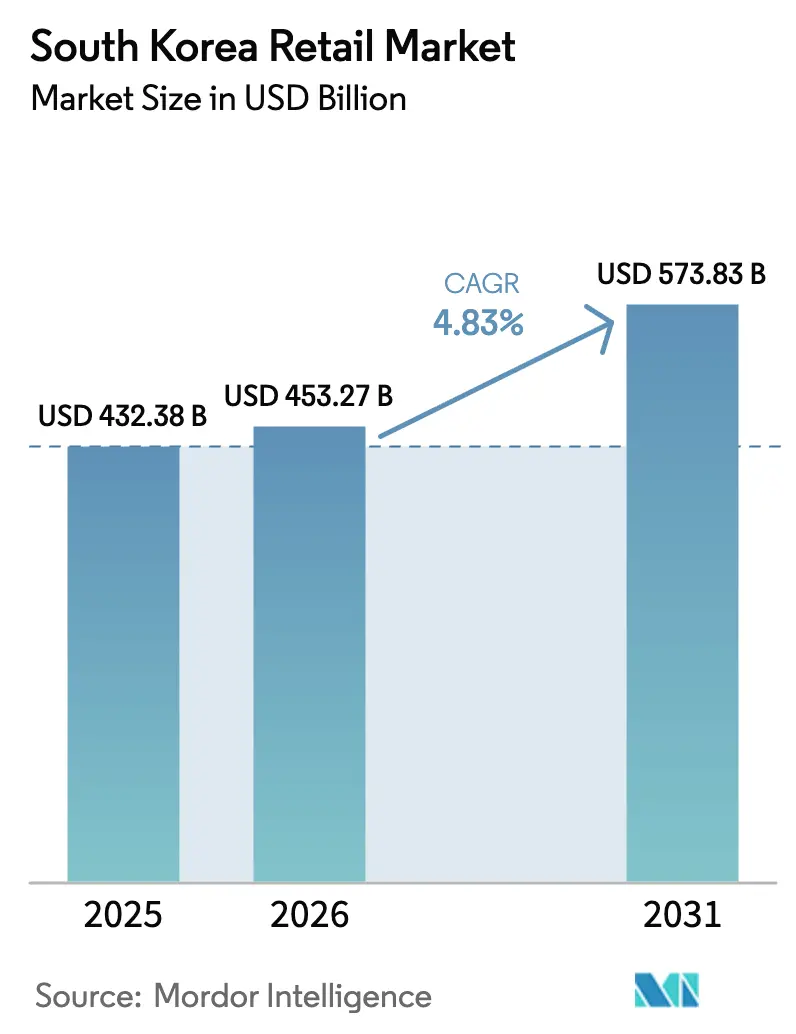

| Base Year Market Size (2025) | USD 432.38 Billion |

| Market Size (2026) | USD 453.27 Billion |

| Market Size (2031) | USD 573.83 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Retail Market Analysis by Mordor Intelligence

The South Korea retail market size is expected to grow from USD 432.38 billion in 2025 to USD 453.27 billion in 2026 and is forecast to reach USD 573.83 billion by 2031 at a 4.83% CAGR over 2026-2031. Growth reflects a shift from pandemic volatility toward modernization as ultra-fast logistics and mobile-first commerce reshape competition and margins. E-commerce depth is a structural feature, yet resilient offline formats in convenience and department stores continue to serve urban proximity and luxury demand. Omni-channel grocery emerges as the fastest-growing retail channel, as chains use physical footprints to enable same-day delivery and real-time inventory visibility. Regulatory reforms are tightening payment risk controls while supporting innovation in digital finance and data protection, which stabilizes trust in the South Korea retail market.

Key Report Takeaways

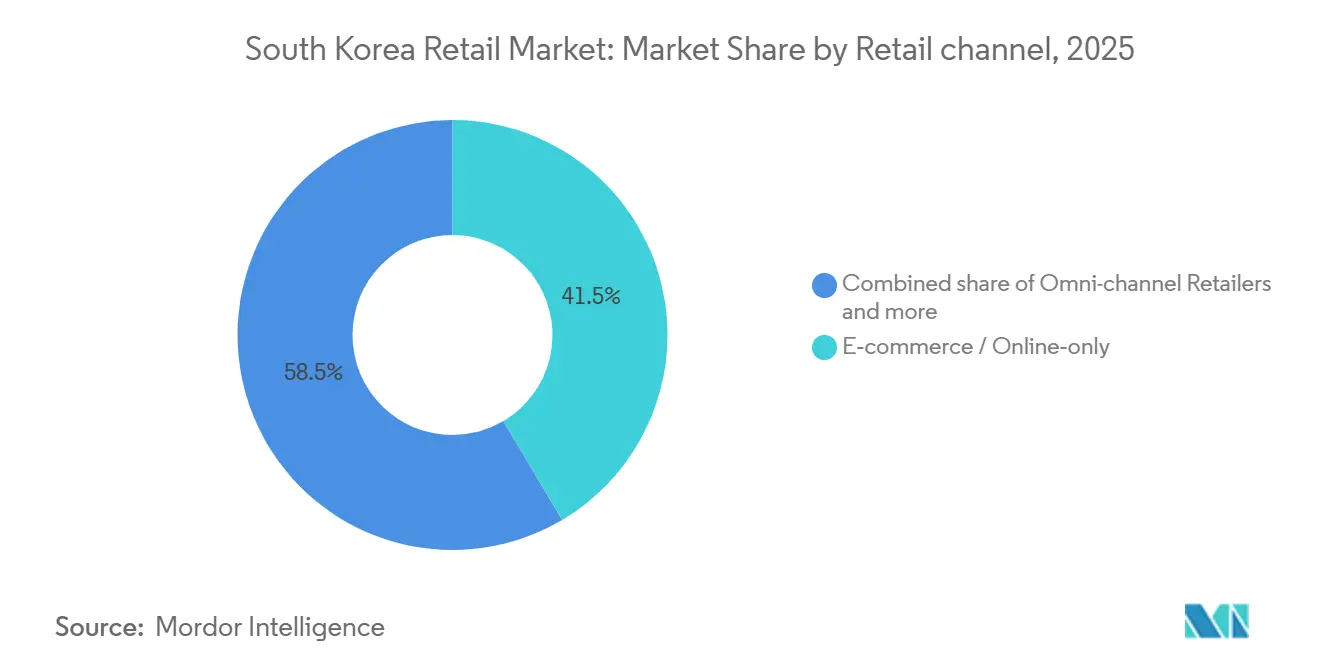

- By retail channel, e-commerce and online-only held 41.48% revenue share in 2025, while omni-channel grocery is forecast to expand at a 6.48% CAGR through 2031.

- By product category, grocery and food led with a 31.47% revenue share in 2025, while beauty and personal care are projected to grow at a 5.82% CAGR through 2031.

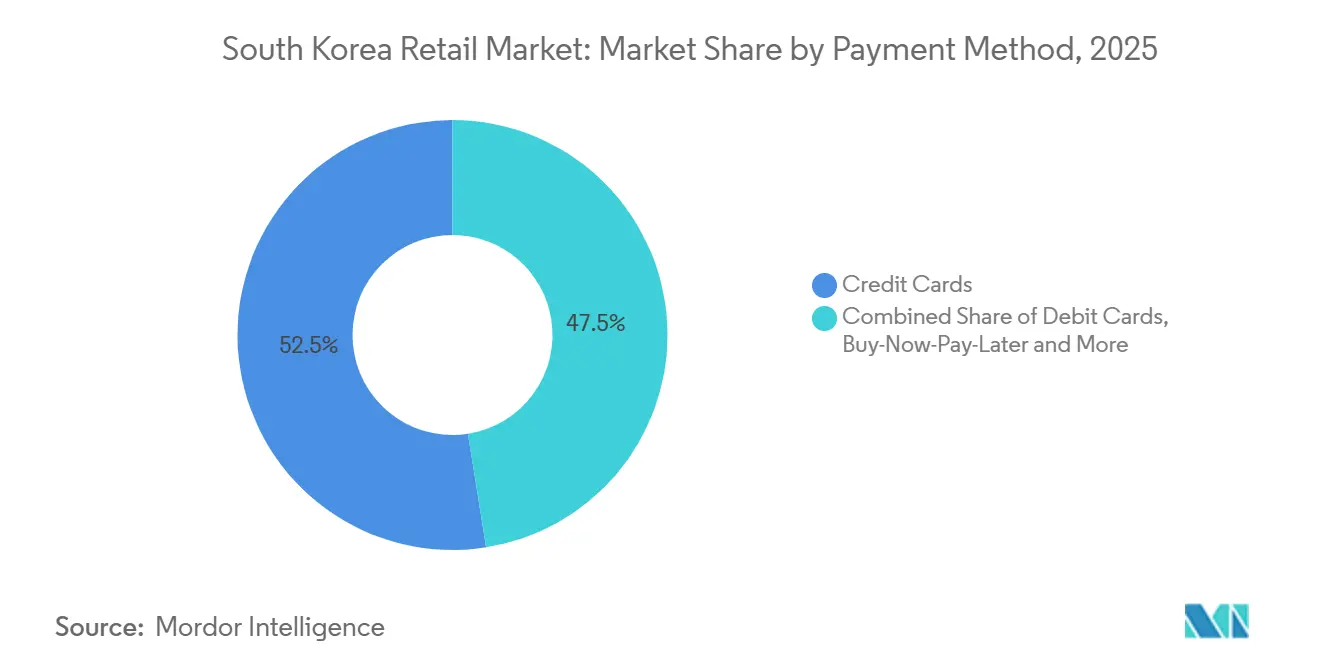

- By payment method, credit cards accounted for a 52.49% share in 2025, and buy-now-pay-later is expected to grow at a 7.29% CAGR through 2031.

- By region, the Seoul Capital Area commanded a 47.25% share in 2025, while Jeju is projected to post a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of mobile & e-commerce channels | +1.2% | Global, peak in Seoul Capital Area and Incheon | Medium term (2-4 years) |

| High penetration of digital payments & super-apps | +0.9% | National, urban centers with smartphone penetration | Short term (≤ 2 years) |

| Expansion of convenience formats for single-person households | +0.7% | National, with early gains in Seoul, Busan, and university districts | Medium term (2-4 years) |

| Government support for cold-chain logistics & smart retail | +0.5% | Busan Port logistics hub and rural areas for fresh delivery | Long term (≥ 4 years) |

| Retail-media networks unlocking new revenue streams | +0.4% | Platform-centric, Coupang and Naver ecosystems | Medium term (2-4 years) |

| AI-driven hyper-personalisation in super-apps | +0.3% | National, led by Naver, Kakao, and vertical platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth Of Mobile & E-Commerce Channels

Mobile transactions accounted for 77.7% of online shopping value in October 2025, up from 75.9% in September, underscoring a smartphone-first shift in buyer behavior in South Korea. Ultra-fast fulfillment continues to set expectations as fresh grocery reach within 24 hours scales to 98% of the population, compressing inventory cycles across the South Korea retail market. Coupang reported October 2025 daily average product commerce revenue of USD 323 per active customer, up 7% year over year on a constant currency basis, which signals platform stickiness despite price competition from Chinese entrants. Online shopping grew 15.8% year over year in the first half of 2025 as offline retail stagnated near zero growth, pointing to structural channel migration. That outperformance is moderating since online transaction value growth slowed to 4.5% in 2025 versus 8.5% in 2024, implying saturation effects that will test growth strategies in the South Korea retail market.

High Penetration Of Digital Payments & Super-Apps

Cash usage declined to 14.6% of transactions by 2021, and mobile wallets captured 32.9% of e-commerce payments in 2023, reflecting a long-running policy push toward cashless activity. Simple payment services with biometric authentication processed a daily average of USD 0.72 billion in the first half of 2025, while prepaid electronic payments reached USD 0.89 billion per day. Card payments accessed via mobile devices represented 53.8% of total card transaction value in the first half of 2025 as physical card usage contracted. The Electronic Financial Transactions Act, revised in December 2025, requires payment gateways to externally manage 100% of unsettled funds by December 2026, phased to 60% in year one, 80% in year two, and full compliance in year three. In parallel, the Bank of Korea’s retail CBDC pilot “Project Han River” enrolled 51,766 digital wallets and processed 29,591 transactions in April 2025, testing retail use with convenience stores and home shopping channels[1]Bank of Korea, “Payment and Settlement Statistics H1 2025,” Bank of Korea, bok.or.kr.

Expansion Of Convenience Formats For Single-Person Households

Single-person households reached 8.05 million in 2024, or 36.1% of all households, increasing structural demand for small-basket, 24-hour formats. Nationwide convenience store count totaled 54,780, with the top three chains operating 48,315 stores as of May 2025, although the format saw a net decline of 667 units over six months to November 2025. BGF Retail, operator of CU with 18,458 stores, reported 2024 consolidated sales of USD 6.03 billion and operating income of USD 0.17 billion amid higher automation and franchise support costs[2]BGF Retail, “BGF Retail 2024 Annual Results,” BGF Retail, bgfretail.com. GS Retail’s convenience business posted Q2 2025 revenue of USD 1.54 billion with an operating profit of USD 0.04 billion as transformation spending weighed on margins. Meal-replacement sales grew faster than the segment average, which aligns with rising time pressure among urban consumers in the South Korea retail market.

Government Support For Cold-Chain Logistics & Smart Retail

Fiscal incentives during promotional events in late 2025 lifted home appliance sales, signaling that policy can nudge higher-ticket retail and adjacent logistics upgrades. Lotte planned USD 0.52 billion in smart logistics at the Busan Port Authority and introduced 30-minute delivery for 10,000 items to speed cross-border e-commerce flows. Coupang invested USD 0.14 billion to expand Rocket Fresh Everywhere cold-chain coverage to 98% of the population by the end of 2024, using micro-fulfillment in underserved areas. BGF Retail approved USD 0.13 billion for a new Busan logistics center, to be completed in 2026, to strengthen cold-chain capacity for fresh and ready-to-eat assortments. The Korea Customs Service deployed AI-based risk screening for express e-commerce, cutting high-risk analysis time and yielding estimated annual savings of USD 0.08 billion.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturation & cannibalisation among convenience stores | -0.6% | National, acute in Seoul metro dense areas | Short term (≤ 2 years) |

| Escalating labour and real-estate costs | -0.5% | Seoul Capital Area, key commercial districts | Medium term (2-4 years) |

| Low NFC terminal penetration is hindering Apple Pay uptake | -0.2% | National, legacy MST infrastructure | Medium term (2-4 years) |

| Gen-Alpha shift to recommerce platforms | -0.2% | Urban youth markets and university towns | Long term (≥ 4 years) |

| Regulatory compliance burdens on gateways and data flows | -0.2% | National across payment gateways and data | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Saturation And Cannibalisation Among Convenience Stores

Store density is high in metro cores, which results in formats competing within short distances and eroding unit economics. A net decline of 667 stores over six months to November 2025 marks the first sustained contraction since 1988, even as single-person household demand grows. BGF Retail posted USD 6.04 billion in 2024 sales and USD 0.17 billion in operating income, while margin compression reflected automation depreciation and higher franchise support. GS Retail’s convenience segment reported USD 1.55 billion in Q2 2025 revenue and USD 0.04 billion in operating profit, showing similar cost headwinds. The USDA Foreign Agricultural Service estimated convenience stores at a 23% grocery retail share in 2024, exceeding supermarkets and hypermarkets, which underscores format importance despite saturation[3]USDA Foreign Agricultural Service, “Korea Retail Foods Update 2024,” USDA FAS, fas.usda.gov.

Escalating Labour And Real-Estate Costs

Costs are concentrated in the Seoul Capital Area, where commercial rents and wages remain elevated, which weighs on unit profitability in dense trade areas. Operating trends at major chains show higher SG&A from digital and store technology investments, suggesting limited room to absorb fixed cost inflation without pricing or mix shifts. Convenience and hypermarket operators continue to rationalize footprints and seek a higher-margin mix, which is consistent with the slower growth reported in 2025. Department stores have leaned into luxury and tourist spending to offset cost pressure, which aligns with the premium segment’s recent outperformance. These cost dynamics create uneven pressure across formats and amplify the role of logistics, data, and media monetization in the South Korea retail market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Retail Channel: Platform Duopoly Drives Digital, Omni-Channel Bridges the Gap

E-commerce and online-only platforms accounted for 41.48% of South Korea's retail market share in 2025, placing the country among the most digitally penetrated retail economies globally. The market combines rapid digital adoption with offline resilience, as convenience and department store formats meet demand driven by proximity and luxury. Omni-channel grocery, integrating dense store networks with short delivery times, is shaping the market. Hypermarkets experienced negative growth during several months, while proximity-focused Super Supermarkets (SSMs) showed growth, reflecting differing offline grocery dynamics. Department stores recorded a 2.8% year-over-year increase in August, supported by luxury and tourism spending.

Omni-channel grocery is the fastest-growing segment, with its market size expected to grow at a 6.48% CAGR from 2026 to 2031. Retailers leverage app-based inventory, three-hour delivery, and curbside pickup. Platform-scale logistics drive growth, as seen in Coupang’s Q3 2025 product commerce momentum and fulfillment solutions for third-party sellers. Naver’s commerce advertising expansion and NAVER Pay’s Q1 2025 TPV of USD 13.60 billion enhance digital retail conversion. Platform concentration is significant, with CR2 above 46% of e-commerce GMV and CR10 near 68% in 2024, balancing platform economics with neighborhood accessibility for speed, selection, and service.

By Product Category: Beauty Outpaces Grocery As Experience Trumps Commodity

Grocery and food commanded a 31.47% share of the South Korea retail market in 2025, supported by steady online demand for food and beverage categories. Online food and beverage sales rose 16.3% year over year in August 2025, and fresh food categories posted double-digit gains during mid-2025 as buying shifted from bulk trips to app-based replenishment. The South Korean retail market has also seen beauty and personal care emerge as the fastest growing category on the K-beauty strength and specialty chain scale. Consumer electronics posted uneven trends tied to device launch cycles, which limit sustained uplift outside marquee release windows. Home and living grew during H1 2025, aided by incentives that lifted appliance purchases during key events.

Beauty and personal care are projected to grow at a 5.82% CAGR through 2031, with CJ Olive Young’s 71.3% share in health-and-beauty retail and fiscal 2024 revenue of USD 3.32 billion, reinforcing category momentum. CJ Olive Young recorded an operating profit of USD 0.32 billion and 9.42 million foreign transactions in FY2024, highlighting inbound tourism exposure and margin advantage. Fashion shows a split picture, as offline clothing sales fell in 2024, while online clothing transaction value reached USD 15.26 billion in 2024, with cross-border purchases from China at USD 1.70 billion. The South Korea retail market also includes specialty retail and niche warehouse formats that use price or curation to defend share amid platform scale. Data show food products at 13.8% and food services at 15.6% of online shopping value in June 2025, with e-coupons declining due to the wind-down of stimulus effects.

By Payment Method: Credit Cards Dominate, BNPL Surges Among Youth

Credit cards held a 52.49% share of retail payments in 2025 and continued to outperform debit as consumers favored installment flexibility. Prepaid and debit modes showed mixed trends as classification changes affected reporting and as simple payments absorbed incremental growth. Mobile device-accessed card payments reached 53.8% of total card transaction value in H1 2025, while physical card usage contracted at a modest rate. Samsung Pay’s USD 50.79 billion 2023 transaction volume established an infrastructure that enables QR and MST acceptance across legacy terminals. KakaoPay reported Q3 2025 TPV of USD 32.61 billion with robust offline growth from wider acceptance and public coupon integration.

Buy-now-pay-later is the fastest-growing payment method, with South Korea retail market size for BNPL projected to expand at a 7.29% CAGR from 2026 to 2031 as fintechs embed installment options at checkout. The Bank of Korea’s survey pointed to a strong preference for mobile among younger cohorts, with credit cards leading for middle-aged users, and cash still used among older demographics. The FSC’s December 2025 revision mandates 100% external management of unsettled funds by December 2026, phased 60%, 80%, then 100% and raises capital requirements for gateways above USD 0.02 billion quarterly volume from USD 0.69 million to USD 1.38 million. Account transfers via the small value payment network averaged USD 69.94 billion per day in H1 2025, while Open Banking growth slowed as simple payment services gained. These developments anchor confidence in digital transactions across the South Korea retail market as payment rails evolve.

Geography Analysis

The Seoul Capital Area held a 47.25% share of the South Korea retail market in 2025, supported by its dense population, high incomes, and logistics hubs. Retail sales declined 2.7% year over year in Q3 2025 due to saturation in duty-free, supermarket, and convenience store formats in urban districts. Incheon’s retail sales rose 5.5% year over year in Q3 2025, driven by gateway and mobility-related spending in automotive-adjacent categories. Major retailers are expanding into regional cities, with Hyundai Department Store planning large-format projects in Busan and Gwangju, while Shinsegae’s Starfield expansion reflects confidence in regional consumption corridors.

Sejong led the Chungcheong Region with 8.8% year-over-year retail sales growth in Q3 2025, while Chungbuk and Chungnam saw modest gains. The Connect Hyundai Cheongju opening in June 2025 introduced new brand assortments and omnichannel formats. Consumer sentiment reached 101.8 in May 2025, aiding recovery in discretionary categories and highlighting second-tier cities’ potential to adopt modern retail concepts. Persistent housing and cost pressures in the capital are likely to shift focus to regional markets.

In the Gyeongsang Region, Busan’s retail sales grew 1.9% year over year in Q3 2025, Gyeongnam rose 2.3%, while Gyeongbuk saw a slight decline. South Gyeongsang’s GRDP was USD 104.92 billion in 2024, with strong shipbuilding and defense activities, though retail trade lagged. Jeolla showed subdued growth, Gangwon declined 0.6% in Q3 2025, and Jeju, despite a projected 6.74% CAGR to 2031, saw sales dip in 2025 due to reduced tourism and increased service spending.

Competitive Landscape

The South Korea retail market shows high platform concentration, with Coupang and Naver Shopping controlling over 46% of e-commerce GMV. Offline retail remains fragmented across convenience stores, hypermarkets, and department stores. Hypermarkets focus on price and speed, while department stores rely on luxury and tourist demand for growth. Specialty platforms monetize community and curation to maintain defensible take rates. E-commerce growth is supported by retail-media monetization and seller services, enhancing network effects.

In recent years, strategic initiatives have emphasized last-mile logistics, AI adoption, and partnerships. Coupang’s USD 0.13 billion cold-chain expansion and credit facilities bolster logistics and fulfillment. Naver scales commerce advertising and NAVER Pay while using AI to improve engagement and conversion. Kakao integrates AI agents into commerce and expands offline payment acceptance to boost TPV. E-Mart’s joint venture with AliExpress International and Gmarket enhances cross-border sourcing and logistics[4]Kakao Corporation, “TPV and AI Commerce Initiatives,” Kakao, kakaocorp.com.

Technology remains a key differentiator as retailers deploy AI for pricing, recommendations, and operations. BGF Retail’s USD 0.13 billion Busan logistics center supports chilled and ready-to-eat product growth. CJ Olive Young uses AI for content integrity and campaign speed while scaling global sales through physical and digital channels. Regulatory oversight on MFN clauses, search rankings, and payment risk management is reshaping platform conduct and merchant economics in the South Korean retail market.

South Korea Retail Industry Leaders

Coupang Corp.

Naver Corp. (Naver Shopping)

SSG.COM

E-Mart Inc.

Lotte Shopping Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Lotte Shopping partnered with Export Development Canada (EDC) to expand its private brand products into the Canadian market, marking a significant international push.

- July 2025: Kakao Pay withdrew from its planned acquisition of Shinsegae's SSG Pay, ending negotiations for a strategic partnership in mobile payments.

- May 2025: Lotte Cinema and Megabox, two major cinema chains in South Korea, announced their merger, potentially reshaping the exhibition landscape in the retail and entertainment sector.

- May 2025: Shinsegae Group, in partnership with Ascent Equity Partners, considered acquiring color cosmetics manufacturer C&C International in May 2025 to bolster its beauty portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea retail sector as all business-to-consumer transactions for goods that reach households through store-based outlets, e-commerce platforms, and omnichannel formats inside the national borders. The valuation captures gross merchandise value (GMV) inclusive of sales tax but net of product returns and intra-trade between retailers.

Scope Exclusions: Institutional wholesale trade, duty-free sales to in-transit travelers, and pure service categories such as food service are not counted.

Segmentation Overview

- By Retail Channel

- E-commerce / Online-only

- Omni-channel Retailers

- Hypermarkets & Supermarkets

- Department Stores

- Convenience Stores

- Discount & Variety Stores

- Traditional Markets

- Specialty Stores

- By Product Category

- Grocery & Food

- Fashion & Apparel

- Consumer Electronics

- Beauty & Personal Care

- Home & Living

- Health & Wellness

- Sports & Leisure Equipment

- By Payment Method

- Credit Cards

- Debit Cards

- Digital Wallets / Mobile Payments

- Buy-Now-Pay-Later

- Cash

- By Region

- Seoul Capital Area

- Chungcheong Region

- Gyeongsang Region

- Jeolla Region

- Gangwon Region

- Jeju Region

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with senior merchandisers at supermarket chains, logistics partners handling last-mile parcels, and payment gateway executives in Seoul, Busan, and inland provinces. These conversations validated discounting patterns, mobile checkout penetration, and the share of cross-border spend that is re-routed via third-party reshippers, filling gaps left by desk research before we triangulated the final numbers.

Desk Research

We first built a historical foundation from open data released by Statistics Korea, the Bank of Korea's monthly retail turnover tables, and customs shipment codes that signal cross-border e-commerce inflows. Trade associations such as the Korea Chain Store Association and the Korea Chamber of Commerce provided store counts and average ticket sizes that helped refine channel splits. Annual reports and investor decks from listed retail groups, along with household expenditure files in the OECD Data Explorer, supplied price and mix insights. Paid intelligence sources drawn from D&B Hoovers and Dow Jones Factiva furnished audited revenue trails and news on format expansions. This list is illustrative; many other public and subscription sources supported verification and context building.

Market-Sizing & Forecasting

A top-down reconstruction starts with Statistics Korea's monthly retail receipts, which are then re-segmented by channel using government card transaction dashboards and adjusted for informal street market activity gleaned from municipal tax bulletins. Select bottom-up checks, such as sampling the consolidated revenues of ten large listed retailers and multiplying average selling price by parcel volumes for leading online platforms, serve as guardrails against over- or under-count. Key variables that drive the model include household disposable income growth, smartphone-enabled commerce share, inbound tourist arrivals, national consumer sentiment, convenience store footprint density, and inflation-adjusted average selling price trajectories. A multivariate regression links these drivers to baseline sales, while scenario analysis cushions macro shocks. Forecast gaps where private firms do not disclose revenues are bridged by channel-specific penetration ratios agreed upon during expert interviews.

Data Validation & Update Cycle

Outputs go through variance checks against independent indices, and anomaly flags trigger re-runs. Two analysts review every data point before sign-off. The study refreshes each year, and interim updates occur when material policy or currency shifts emerge. Right before release, a fresh validation pass ensures clients receive the latest view.

Building Trust in Our Baseline for South Korea Retail Sector

Published estimates often diverge because each provider chooses different channel sets, tax treatments, and currency bases.

Key gap drivers include: some studies overlook travel inflow adjustments, others exclude informal kiosks, and a few apply static exchange rates or project e-commerce growth from narrow samples, whereas Mordor's base case rolls forward monthly receipts and blends them with verified retailer disclosures and parcel counts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 432.3 B (2025) | Mordor Intelligence | - |

| USD 423.6 B (2024) | Global Consultancy A | Omits travel retail and informal traditional markets |

| USD 435.5 B (2024) | Trade Journal B | Uses nominal receipt data without cross-border e-commerce adjustment |

These comparisons show that when variables, scope, and refresh cadence are disciplined, Mordor delivers a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

What is the current size and growth outlook for the South Korea retail market?

The South Korea retail market size is USD 453.27 billion in 2026 and is projected to reach USD 573.83 billion by 2031 at a 4.83% CAGR.

Which retail channels are leading and growing fastest in South Korea?

E-commerce and online-only hold a 41.48% share in 2025, while omni-channel grocery is the fastest-growing with a 6.48% CAGR forecast to 2031.

Which categories are outperforming in the South Korea retail market?

Grocery and food led with 31.47% share in 2025, and beauty and personal care are the fastest-growing at a 5.82% CAGR through 2031.

How are payments shifting across South Korea retail?

Credit cards held a 52.49% share in 2025, mobile device-accessed card payments made up 53.8% of total card transaction value in H1 2025, and BNPL is the fastest-growing with a 7.29% CAGR from 2026 to 2031.

Which regions are most important for South Korea retail growth?

The Seoul Capital Area holds a 47.25% share in 2025, while Jeju is projected to grow fastest at a 6.74% CAGR to 2031.

How concentrated is competition in the South Korea retail market?

Platform concentration is high with the top two controlling over 46% of e-commerce GMV, but offline fragmentation keeps overall retail moderately concentrated.

Page last updated on: