Hardware Stores Retail Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Trillion |

| Market Size (2031) | USD 2.51 Trillion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

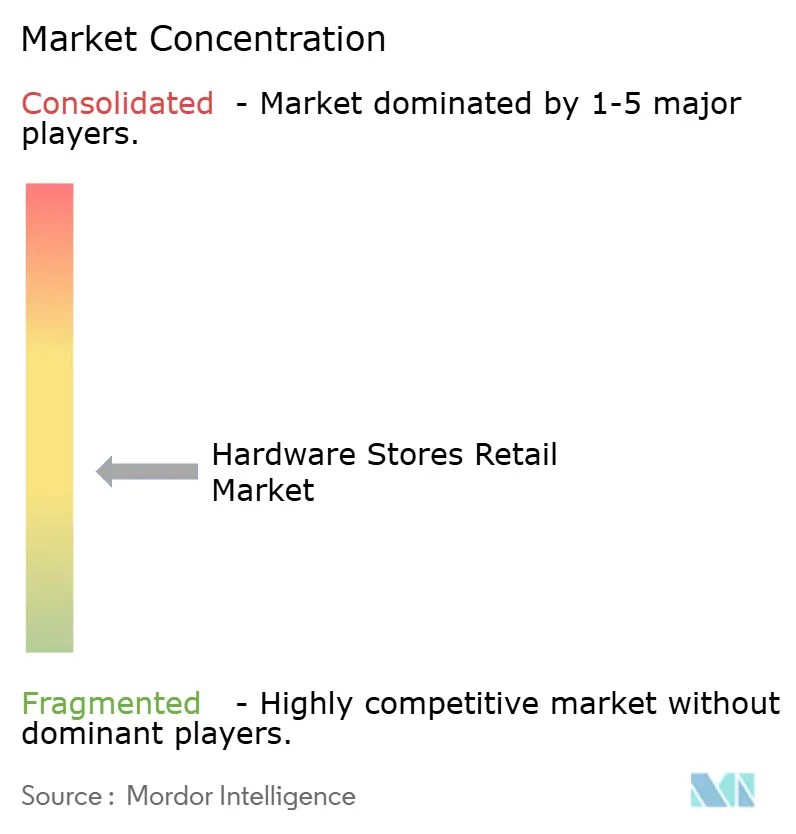

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hardware Stores Retail Market Analysis by Mordor Intelligence

The Hardware Stores Retail Market size is projected to be USD 1.92 trillion in 2025, USD 2.01 trillion in 2026, and reach USD 2.51 trillion by 2031, growing at a CAGR of 4.54% from 2026 to 2031.

The hardware retail market is moving through a more demanding operating cycle because weak housing turnover in the U.S. and Europe is limiting move-related purchases, while renovation and retrofit work at existing homes is keeping demand active. The Home Improvement Research Institute reported that single-family permits fell to 909,600 in 2025, while nearly 80% of U.S. homeowners planned maintenance or improvement projects in Q1 2026, which shows that project spending is being redirected rather than removed. HIRI also found in Q4 2025 that 34% of homeowners planned to increase home improvement spending in 2026, and forecast disposable income growth of 3.2% supported retailer confidence in replenishment cycles. The hardware retail market is also gaining support from electrification upgrades, pro-contractor account growth, and tighter omnichannel integration, which are shifting retailer focus toward service depth, project-scale inventory, and faster fulfillment. Competition in the hardware retail market is becoming more intense as large chains use acquisitions, installed-service platforms, and supply-chain investments to widen their reach. At the same time, independent stores continue to protect local demand through convenience and service quality.[1]Home Improvement Research Institute, “Home Improvement Products Market Analysis,” HIRI Blog, hiri.org

Key Report Takeaways

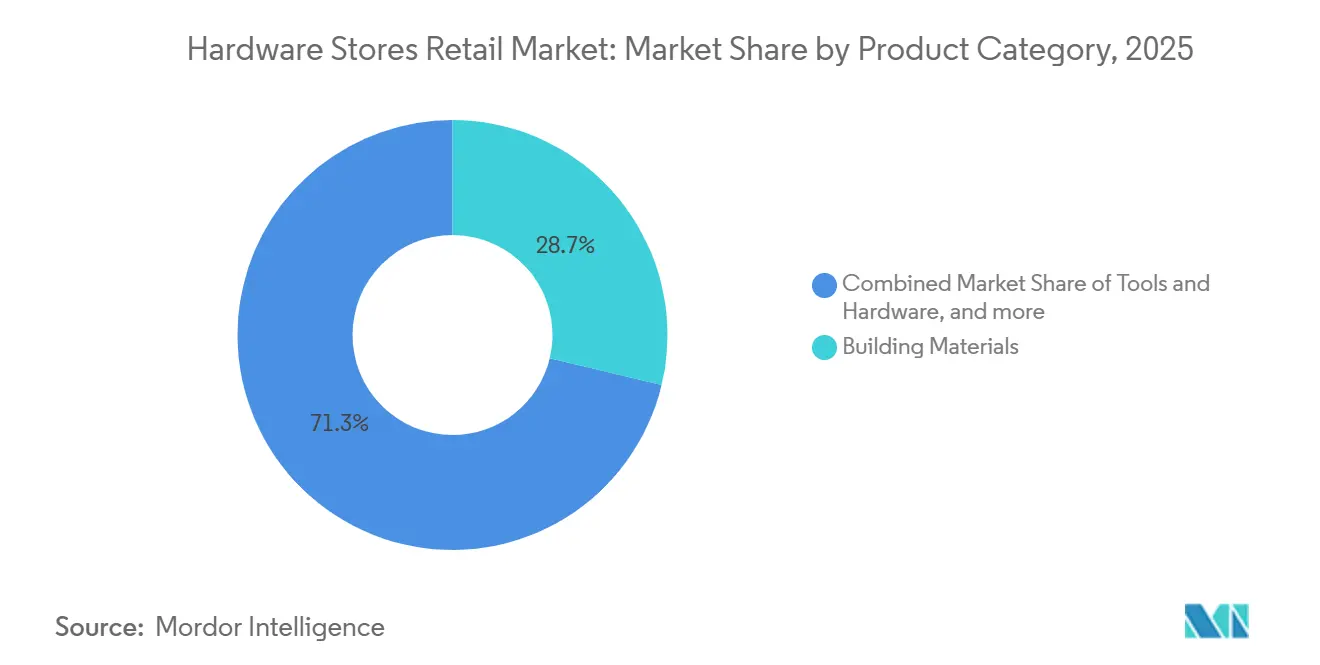

- By product category, Building Materials held 28.73% of total value in 2025, while Plumbing & Electrical is projected to expand at a 5.46% CAGR through 2031.

- By customer type, DIY Consumers acppounted 53.92% of total value in 2025, while Professional Contractors & Tradespeople are projected to record the highest CAGR at 5.11% through 2031.

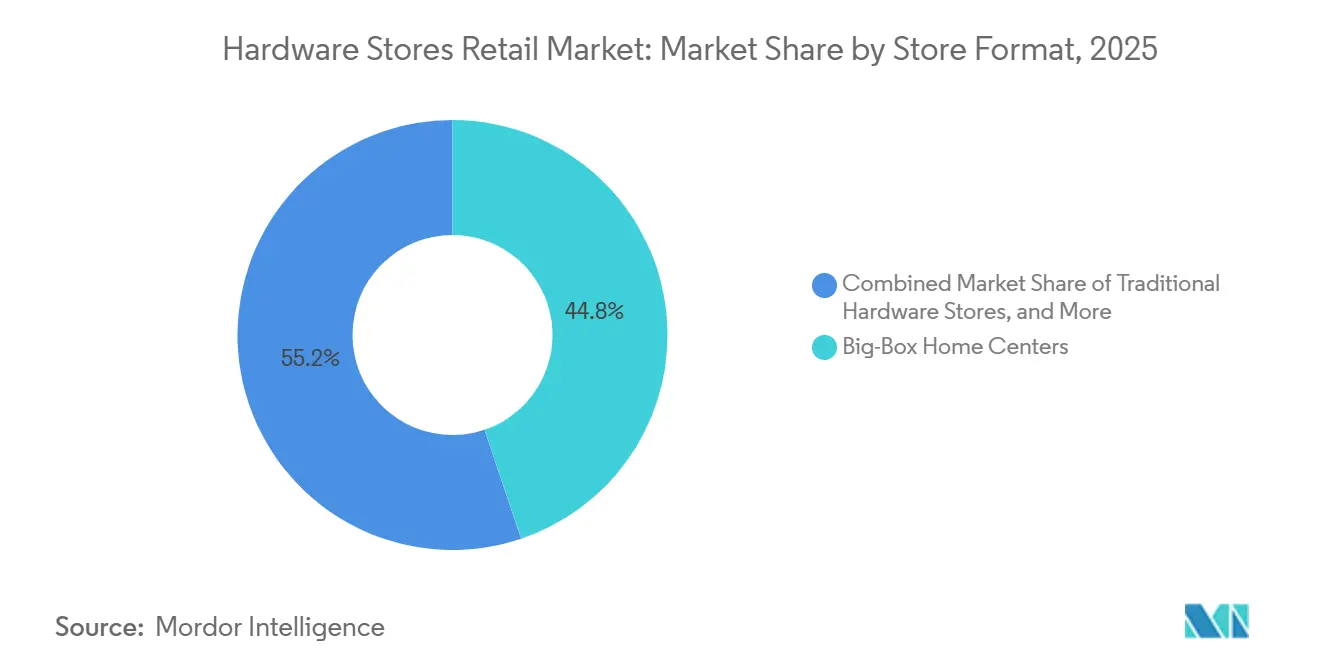

- By store format, Big-Box Home Centers accounted for 44.81% of total value in 2025, while Online-Only Platforms are projected to grow fastest at a 5.83% CAGR through 2031.

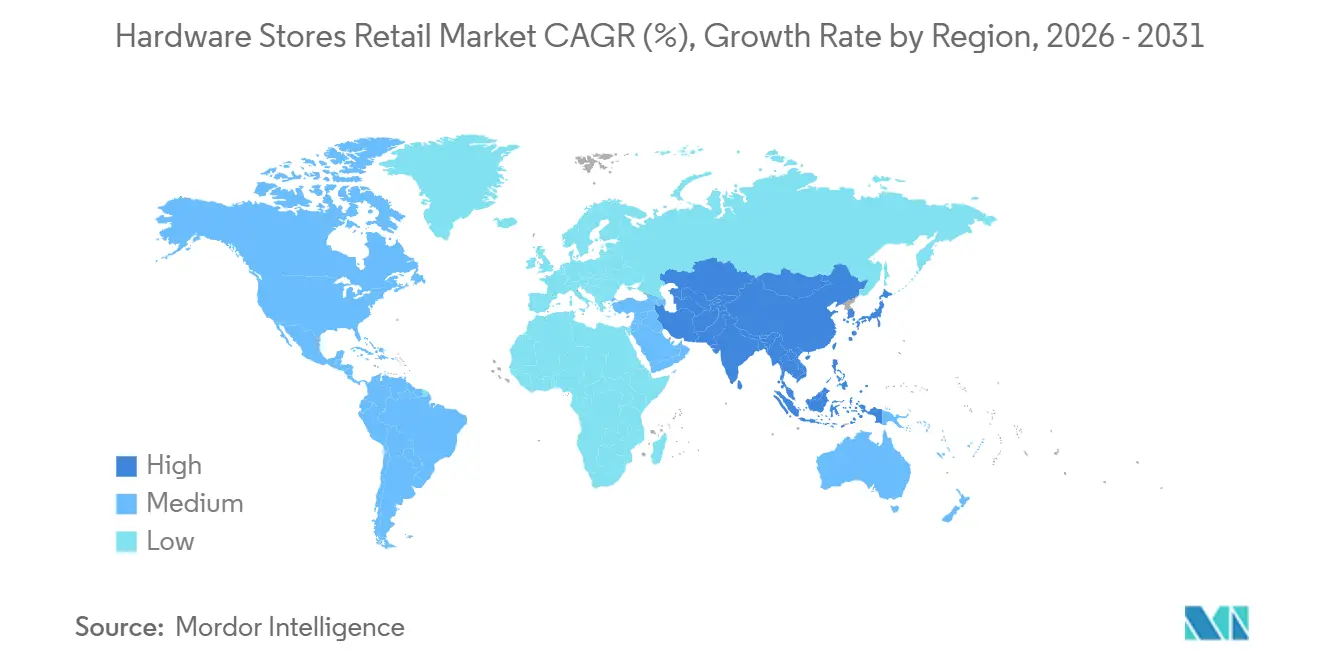

- By geography, North America held 37.95% of global value in 2025, while Asia-Pacific is projected to expand at a 5.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hardware Stores Retail Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Renovation Over Relocation Trend | +1.2% | North America, with spillover to the U.K. and Australia | Medium term (2-4 years) |

| Social Media Driven DIY Learning Adoption | +0.6% | Global | Short term (≤ 2 years) |

| Growing Omnichannel Click-and-Collect Demand | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing Energy Efficiency Retrofit Upgrades | +0.9% | North America and Europe | Medium term (2-4 years) |

| Expansion of State Rebate Electrification Programs | +0.4% | North America, especially the U.S. at state level | Short term (≤ 2 years) |

| Rising Wildfire Hardening Retrofit Initiatives | +0.3% | Western U.S. and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Renovation Over Relocation Trend

The renovation-over-relocation pattern remains the clearest demand base for the hardware retail market in 2026. U.S. existing home sales were running at a 3.91 million annual rate in January 2026, while single-family permits fell to a seven-year low in 2025, prompting more households to improve their current homes rather than move. HIRI reported that professional market sales are projected to grow faster than consumer market sales in 2025, pointing to larger and more technical projects moving toward skilled execution. This mix is lifting average ticket values in the hardware retail market, even when store visit frequency becomes less predictable. Retailers with deeper project assortments, stronger installed-sales links, and contractor-ready inventory are better placed to capture spending. At the same time, the housing lock-in effect stays in place through the forecast period.

Social Media Driven DIY Learning Adoption

Social media is lowering the confidence barrier to first-time project work, giving the hardware retail market a wider entry funnel for smaller repair and improvement jobs. Short-form project demonstrations are helping consumers understand tool selection, material needs, and sequencing before they visit a store or place an online order. That behavior matters most in categories such as paint, adhesives, storage, garden products, and entry-level tools, where product discovery often starts with simple project ideas rather than planned replacement cycles. The hardware retail market is therefore benefiting from a broader set of inspiration-led purchases that can be converted through search, digital merchandising, and same-day pickup. The effect is strongest in the short term because it encourages participation and product trial, even if more advanced work still shifts toward professional execution.

Growing Omnichannel Click-and-Collect Demand

Click-and-collect is changing how the hardware retail market converts digital traffic into store sales. Lowe’s reported that online sales grew 15.5% in Q1 2026, which showed that digital research and purchasing continue to gain weight in the channel. Ace Hardware reported 30% digital sales growth in Q1 2026, and its 5,266 domestic stores gave it a large local fulfillment base for fast pickup and last-mile access. The hardware retail market benefits from this model because bulky goods, urgent repairs, and contractor needs still require local availability, even when product searches begin online. Retailers that connect real-time inventory, store fulfillment, and project-based recommendations are likely to hold a stronger position as customers place more value on speed and certainty.

Increasing Energy Efficiency Retrofit Upgrades

Energy-efficiency retrofit work is becoming a steady demand stream for the hardware retail market, especially in Plumbing & Electrical and adjacent installation categories. ENERGY STAR states that federal tax credits can reach USD 3,200 annually for qualifying upgrades, and the Home Efficiency Rebates program offers up to USD 8,000 for eligible heat pump installations. These incentives support purchases of higher-value electrical components, controls, and HVAC-linked accessories that are increasingly part of mainstream hardware baskets. The demand is not solely incentive-driven, as stricter renovation standards in major markets are making energy performance part of code compliance and replacement planning. In the hardware retail market, stores that can explain product eligibility, installation requirements, and rebate paperwork are gaining an advantage over formats that compete only on price.[2]ENERGY STAR, “Home Efficiency Rebates (HEAR),” U.S. Environmental Protection Agency, energystar.gov

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From DIY to DIFM Services | -0.5% | North America and Europe | Medium term (2-4 years) |

| Housing Affordability Limiting Projects | -0.5% | North America, Europe, and Australia | Long term (≥ 4 years) |

| Rising Organized Retail Crime Incidents | -0.3% | North America | Short term (≤ 2 years) |

| Policy Volatility in Rebates and Tariffs | -0.4% | North America and the EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift From DIY to DIFM Services

The shift from do-it-yourself to do-it-for-me activity is narrowing the direct consumer opportunity in parts of the hardware retail market. HIRI reported that professional market sales are projected to grow faster than consumer market sales in 2025, which shows that more project volume is moving toward skilled execution. Wickes also reported that TradePro membership reached 643,000 in FY2025, up 10.7% from 581,000 in 2024, highlighting retailers' efforts to retain this spend through trade-focused loyalty systems. For the hardware retail market, the issue is less about demand disappearance and more about who controls procurement at the point of sale. Retailers that fail to serve both consumer and contractor missions in the same ecosystem risk losing volume to trade distributors and specialist merchant channels.

Housing Affordability Limiting Projects

Housing affordability remains a longer-running constraint on the hardware retail market because elevated financing pressure reduces project appetite for expensive discretionary work. Existing home sales in the U.S. were weak at the start of 2026, and single-family permits in 2025 were the lowest since 2019, reflecting broader caution shaping household decisions. In this setting, consumers tend to protect essential maintenance and defer larger remodeling scopes, especially in categories that require financing or full-room replacement. The hardware retail market is therefore more exposed at the premium end of kitchen, bath, and major structural renovation programs than in everyday repair-and-maintenance lines. This restraint is most visible in rate-sensitive markets, where affordability pressures are already limiting home purchase activity and confidence in large-ticket spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Building Materials Leads, Electrification Lifts Plumbing & Electrical

Building Materials accounted for 28.73% of the total value in 2025, making it the largest product segment in the hardware retail market. Its scale is tied to steady renovation demand for sheathing, insulation, framing lumber, and roofing products, especially when households choose to improve existing homes rather than relocate. This category continues to benefit from repair, rehabilitation, and structural retrofit work in aging housing markets, where project depth matters more than new-home turnover. Plumbing & Electrical is projected to grow at a 5.46% CAGR through 2031, making it the fastest-growing product line in the hardware retail market under the current forecast. That trajectory reflects stronger demand for electrical panels, wiring, controls, and heat pump components as electrification programs and efficiency upgrades expand.

The product mix shift matters because the hardware retail industry is no longer driven only by low-ticket tools and routine consumables. Plumbing & Electrical is gaining strategic weight as a higher-value category with more configuration needs, better attachment opportunities, and stronger links to licensed installation work. Building Materials still anchors volume because it captures both essential repair spend and structural renovation outlays, which gives it a broad role across consumer and contractor demand. The NHPA’s 2026 survey found that 48% of hardware retailers were investing in paint and sundries, while 43% were investing in lawn and garden, which shows that merchants are actively widening category balance around the traditional core. Paint, adhesives, outdoor products, and premium kitchen and bath lines remain important because they support repeat purchases, seasonal traffic, and margin expansion even as large project work becomes more selective.

By Customer Type: DIY Dominates by Volume, Contractors Drive Value Growth

DIY Consumers accounted for 53.92% of the value in 2025, making them the largest customer group in the hardware retail market. That share rested on repeat purchases across consumables, maintenance products, paint, garden lines, and small project supplies that do not depend on full remodeling cycles. Professional Contractors & Tradespeople are forecast to expand at a 5.11% CAGR through 2031, which shows where the strongest value growth is shifting within the hardware retail market. Retailers are responding by building pro desks, credit programs, digital ordering tools, and jobsite fulfillment services that make contractor spending more predictable and easier to retain. This is also consistent with HIRI’s 2025 reading, which showed the professional segment rising 6.7%, and the consumer segment falling 1.7%, indicating that larger projects are moving toward skilled execution.

The customer mix is therefore moving toward accounts that buy more frequently, order in larger quantities, and expect faster service recovery. Institutional and MRO buyers remain less developed in the hardware retail market, even though local pickup convenience and emergency replacement needs can create a good fit for selected retailers. That gap leaves room for operators that can offer catalog depth, invoice terms, and account-based pricing without losing store-level responsiveness. DIY traffic will remain important because it supports breadth and recurring store visits, but the next stage of growth will favor retailers that can serve both household and professional needs on the same platform. In practical terms, the hardware retail market is rewarding businesses that combine consumer merchandising, trade relationships, and fulfillment discipline rather than relying on a single buyer type.

By Store Format: Big-Box Centers Anchor Volume, Online Platforms Reshape Competitive Dynamics

Big-Box Home Centers accounted for 44.81% of the total value in 2025, making them the largest format in the hardware retail market. Their scale reflects broad assortments, national sourcing power, and the ability to stock heavy and project-based goods that still depend on physical handling and local inventory. Online-Only Platforms are projected to grow at a 5.83% CAGR through 2031, making them the fastest-growing format, even though their revenue share remains lower than store-led models. The gap between growth rate and size is important because heavy materials, urgent repairs, and contractor procurement still favor local availability and rapid pickup. This means the hardware retail market is not moving toward a simple store-to-online substitution, but toward a hybrid model where discovery, comparison, and transaction timing are spread across channels.

Traditional hardware stores continue to hold defensible positions because service quality, proximity, and familiarity matter in repair-led and neighborhood demand. HIRI found that the share of DIY homeowners shopping at local hardware stores rose from 21% in Q3 2024 to nearly one-third by Q3 2025, which confirms that smaller operators can still win on convenience and advice. Lumber and building material yards remain closely tied to contractor workflows, while farm and ranch formats serve rural use cases that large metro-focused chains do not fully address. Online-only competitors will continue to gain relevance in researched and standardized purchases, but they still face structural limits in same-day, bulky, and code-sensitive buying occasions. Across formats, the hardware retail market is increasingly being shaped by inventory visibility, pickup speed, and the quality of product guidance rather than by channel identity alone.

Geography Analysis

North America accounted for 37.95% of the global value in 2025, making it the largest regional market in hardware retail. The region benefits from a large home-improvement base, widespread organized retail networks, and a durable culture of household investment in repair and renovation. HIRI reported that single-family permits fell to 909,600 in 2025, yet nearly 80% of U.S. homeowners were still planning maintenance or improvement work in Q1 2026, which shows why renovation demand remains the main support line. North America also remains the main test bed for omnichannel execution, contractor account development, and digitally supported fulfillment models. State-level electrification rebates and wildfire-hardening requirements add another layer of local demand variation, which makes regional inventory planning more important across the hardware retail market.

Asia-Pacific is projected to grow at a 5.69% CAGR through 2031, which makes it the fastest-expanding geography in the hardware retail market. Growth is being supported by rapid urbanization, rising homeownership, and the continued development of organized hardware retail structures in India and Southeast Asia. The opportunity is especially notable in markets where fragmented local trade still dominates procurement and modern chain penetration remains limited. That underpenetration gives large-format chains, local networks, and hybrid retail models room to expand store count, service coverage, and category sophistication over time. In more mature parts of the region, energy-efficiency upgrades, smart-home integration, and aging-home renovation offer a different growth path, less dependent on network expansion and more on product mix.

Europe sits between mature demand conditions and uneven country-level performance in the hardware retail market. The region shows that the same macro pressure does not yield identical outcomes because housing policy, consumer sentiment, and channel structure differ widely across countries. Store-based players in Europe are under pressure to improve digital access, pickup speed, and trade-customer service as project demand becomes more selective and online research becomes more important. South America, the Middle East, and Africa remain smaller in absolute terms, but they still offer incremental demand through urban development, repair activity, and the gradual formalization of hardware buying. Across all these regions, the hardware retail market is being shaped by the balance between local store density, renovation demand, and the pace at which organized retail can improve convenience and product access.[3]U.S. Census Bureau, “2025 Annual Housing Permits and Residential Construction Report,” U.S. Department of Commerce, census.gov

Competitive Landscape

The global hardware retail market remains moderately concentrated at the top, but it is still fragmented when viewed across regional and local operators. Large chains such as The Home Depot, Lowe’s, Ace Hardware, and Bunnings have strong positions in their core geographies. Yet, they do not eliminate the role of independents, specialty yards, and neighborhood stores in other regions. The competitive model is shifting toward service depth, pro-contractor relationships, and tighter digital-to-store integration rather than simple store-count expansion alone. In the hardware retail market, scale now matters because it supports distribution reach, installation services, procurement leverage, and technology investment. Smaller operators remain relevant where customers value local knowledge, quick access, and project guidance over broad national assortments.

Strategic moves from 2024 through 2026 show how leading players are expanding their operating scope in the hardware retail market. The Home Depot completed the acquisition of SRS Distribution in 2024, expanding its access to pro-focused distribution and increasing its reach in trade-oriented supply lines. The company then expanded that platform in May 2026 through the acquisition of Mingledorff’s, an HVAC distributor with 42 locations across 5 southeastern U.S. states, which deepened its specialty trade offering. Ace Hardware also reported Q1 2026 revenue growth, 30% growth in digital sales, and continued domestic store expansion, demonstrating that cooperative and local-service models can still scale effectively in the hardware retail market.

Competition is also widening beyond product breadth into workflow support, assortment precision, and response time. Retailers that can serve both DIY and professional buyers through a single system are better positioned to retain share as procurement patterns become more fragmented. Product certification and compliance are creating another competitive layer because first movers can become preferred supply points for code-sensitive work in electrification and wildfire-hardening categories. LP Building Solutions and Westlake Royal Building Products both launched code-aligned products in 2026, which gives retailers new tools to build contractor trust in regulated use cases. The hardware retail market is therefore competing on a broader set of capabilities, including trade access, technical readiness, fulfillment speed, and local problem-solving.

Hardware Stores Retail Industry Leaders

The Home Depot, Inc.

Lowe's Companies, Inc.

ADEO

Kingfisher plc

Wesfarmers Limited (Bunnings Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Home Depot expanded its SRS Distribution platform by acquiring Mingledorff's, an HVAC distributor with 42 locations across 5 southeastern US states, extending its pro-contractor services offering into specialty trade supply and deepening its USD 700 billion professional market TAM strategy.

- April 2026: HORNBACH Group expanded its existing European footprint by opening a massive new 17,600-square-meter hardware store in Trnava, Slovakia.

- April 2026: Westlake Royal Building Products launched FYRATEK, the first WUI-listed fire and ember-resistant roofing underlayment, positioning it as a compliant product for hardware retailers in California, Oregon, Washington, and Australian bushfire zones where code requirements are tightening.

- March 2026: LP Building Solutions launched LP BurnGuard FRT OSB, the first fire-retardant treated oriented strand board certified under both the International Building Code and International Residential Code, creating a new code-compliant sheathing category for hardware stores serving WUI-zone contractors.

Global Hardware Stores Retail Market Report Scope

| Tools & Hardware |

| Building Materials |

| Plumbing & Electrical |

| Paint, Adhesives & Home Improvement Consumables |

| Outdoor & Garden |

| Kitchen, Bath & Storage |

| DIY Consumers |

| Professional Contractors & Tradespeople |

| Institutional & MRO Buyers |

| Big-Box Home Centers |

| Traditional Hardware Stores |

| Lumber & Building Material Yards |

| Farm & Ranch Supply Stores |

| Online-Only Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Category | Tools & Hardware | |

| Building Materials | ||

| Plumbing & Electrical | ||

| Paint, Adhesives & Home Improvement Consumables | ||

| Outdoor & Garden | ||

| Kitchen, Bath & Storage | ||

| By Customer Type | DIY Consumers | |

| Professional Contractors & Tradespeople | ||

| Institutional & MRO Buyers | ||

| By Store Format | Big-Box Home Centers | |

| Traditional Hardware Stores | ||

| Lumber & Building Material Yards | ||

| Farm & Ranch Supply Stores | ||

| Online-Only Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the projected value of hardware retail by 2031?

The hardware retail market is projected to reach USD 2.51 trillion by 2031, rising from USD 2.01 trillion in 2026 at a CAGR of 4.54%.

Which region leads global demand for hardware stores?

North America led with 37.95% of global value in 2025 because of its large renovation base, dense chain presence, and strong household repair culture.

Which product group is growing fastest through 2031?

Plumbing & Electrical is forecast to grow at a 5.46% CAGR through 2031, supported by electrification, heat pump upgrades, and higher-value component demand.

Why are renovation projects supporting sales even with weak housing turnover?

More households are staying in place and improving existing homes. HIRI showed single-family permits fell to 909,600 in 2025, while nearly 80% of U.S. homeowners still planned maintenance or improvement work in Q1 2026.

Are DIY buyers still the largest customer base?

Yes. DIY Consumers accounted for 53.92% of value in 2025, although Professional Contractors & Tradespeople are growing faster at a 5.11% CAGR through 2031.

Which store format is expanding fastest?

Online-Only Platforms are forecast to grow at a 5.83% CAGR through 2031, but big-box centers still held the largest share at 44.81% in 2025 because bulky goods and urgent purchases still favor physical networks.

Page last updated on: