Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

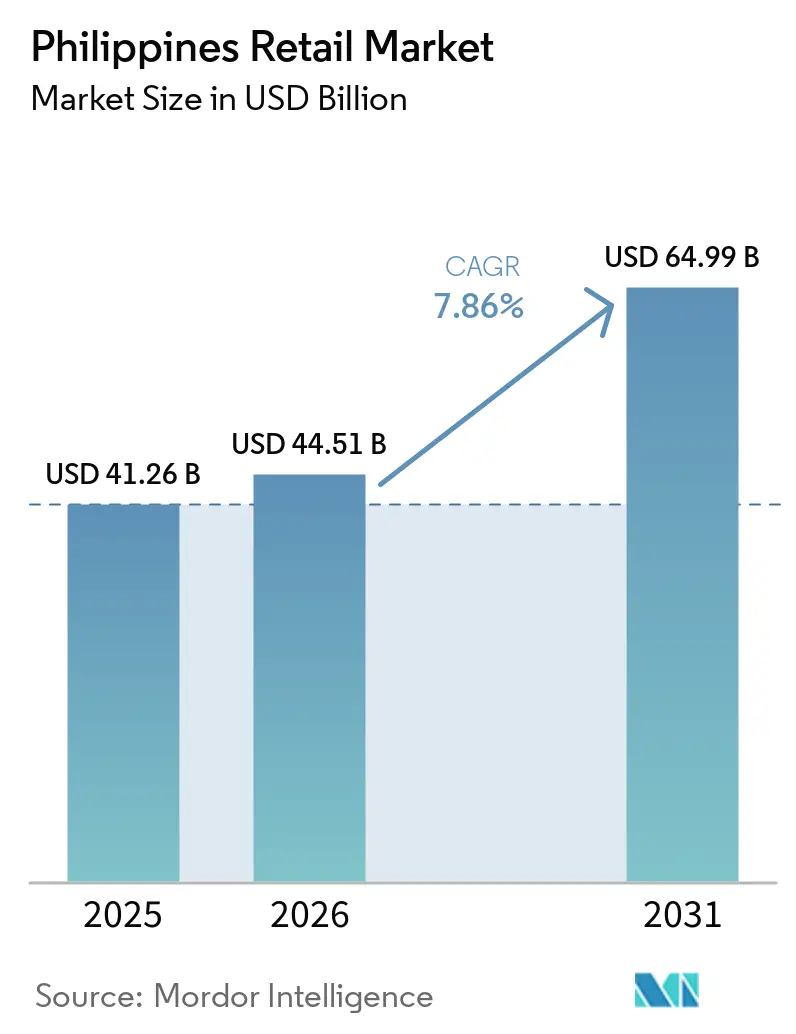

| Base Year Market Size (2025) | USD 41.26 Billion |

| Market Size (2026) | USD 44.51 Billion |

| Market Size (2031) | USD 64.99 Billion |

| Growth Rate (2026 - 2030) | 7.86% CAGR |

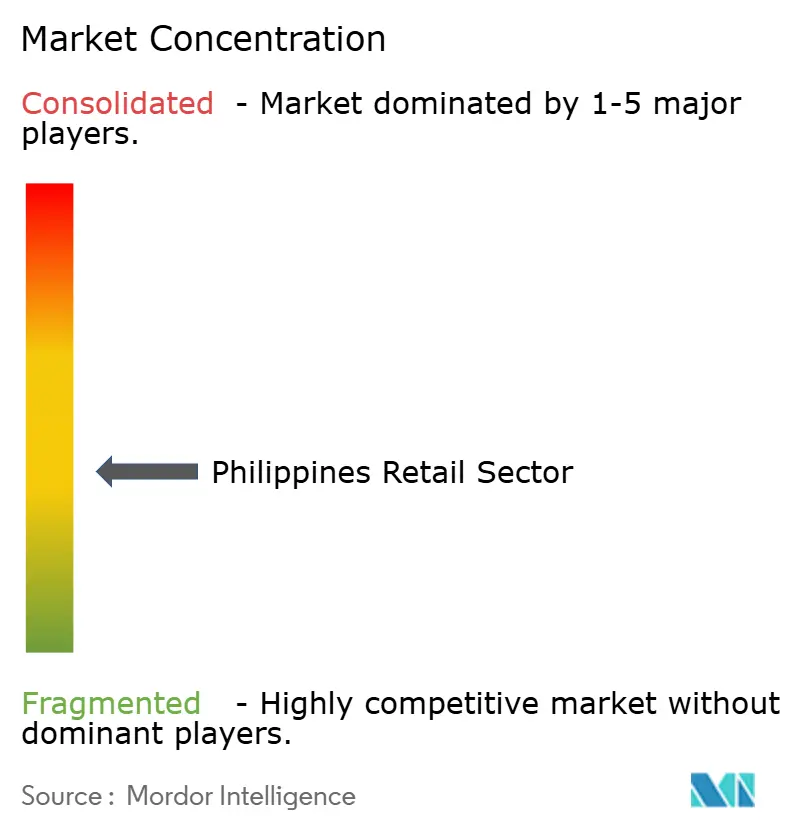

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Retail Market Analysis by Mordor Intelligence

The Philippines Retail Market size is expected to grow from USD 41.26 billion in 2025 to USD 44.51 billion in 2026 and is forecast to reach USD 64.99 billion by 2031 at a 7.86% CAGR over 2026-2031. This expansion is largely supported by resilient domestic consumption, which contributes nearly 70% of the national GDP and provides a stable demand base for retail goods. A young and growing population, combined with rising urbanization, continues to fuel spending on food, apparel, electronics, and lifestyle products. Rapid adoption of digital payment systems and e-wallets has reduced transaction friction, encouraging higher purchase frequency across both online and offline channels. Improvements in logistics, last-mile delivery, and omnichannel fulfillment have also shortened order cycles and expanded access beyond major urban centers. Government investments in infrastructure and supportive policies for foreign and domestic retailers further strengthen market fundamentals.

Key Report Takeaways

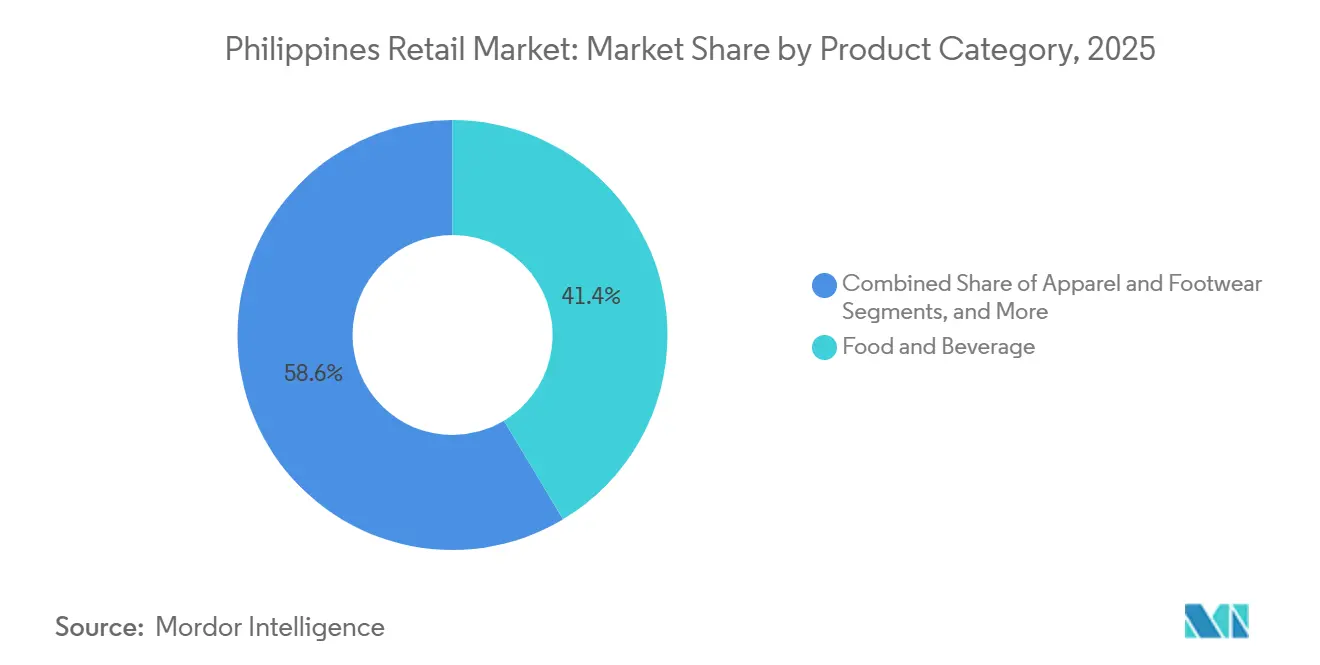

- By Product Category, Food and Beverage led with 41.38% of the Philippines' retail market share in 2025, while Health, Beauty, and Personal Care is projected to expand at an 11.87% CAGR to 2031.

- By distribution channel, Supermarkets/Hypermarkets held 35.24% of the Philippines' retail market share in 2025, while Online is forecast to grow at an 8.27% CAGR through 2031.

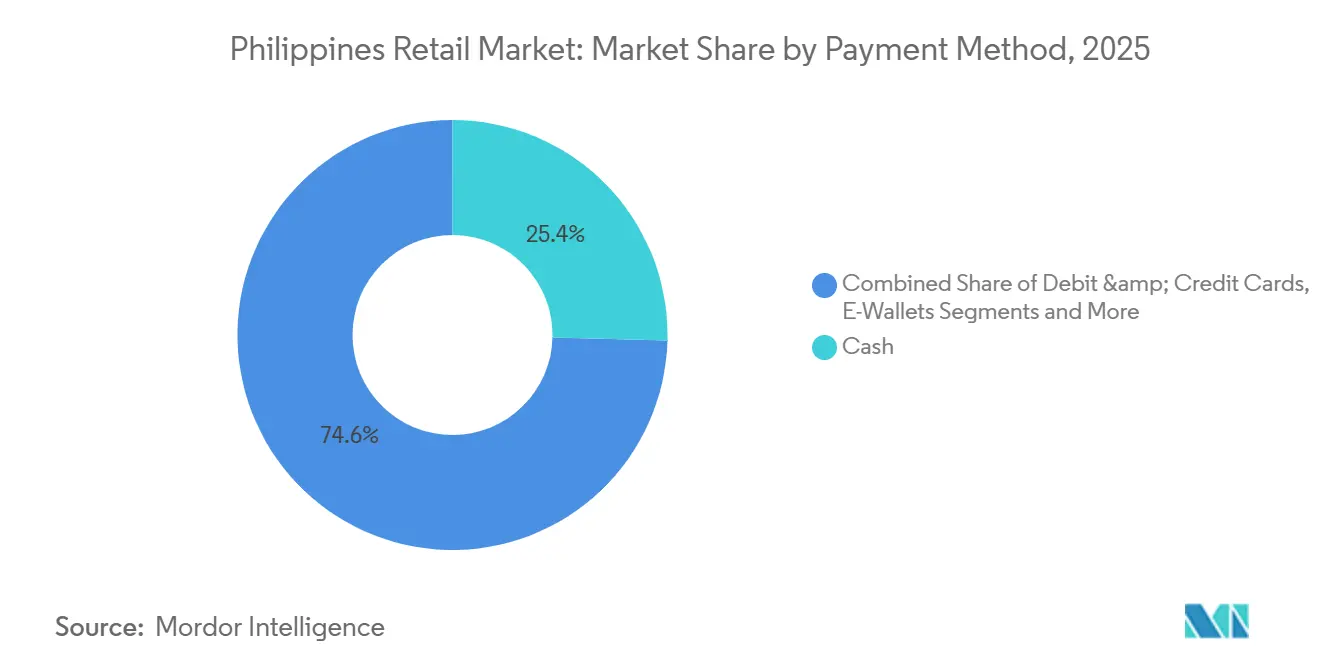

- By Payment Method, Cash accounted for 25.37% of the Philippines' retail market share in 2025, while E-Wallet is forecast to expand at a 13.87% CAGR through 2031.

- By geography, Luzon accounted for 59.39% of the Philippines' retail market share in 2025, with Mindanao recording the highest projected CAGR at 7.84% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & expanding middle class | +1.8% | Global, with concentration in Metro Manila, Calabarzon, and Central Luzon | Medium term (2-4 years) |

| Accelerating e-commerce adoption & digital payments | +2.1% | Global, early gains in Metro Manila, Cebu, Davao | Short term (≤ 2 years) |

| Growth of convenience-oriented F&B retailing | +1.3% | Urban centers nationwide, spillover to peri-urban areas | Medium term (2-4 years) |

| Government logistics infrastructure improvements | +1.2% | Luzon Economic Corridor, Mindanao ports, Visayas RoRo network | Long term (≥ 4 years) |

| Expansion of omnichannel retail & mall modernization | +0.9% | Major metro areas (Metro Manila, Cebu, Clark, Iloilo), Tier-2 cities | Medium term (2–4 years) |

| Demographic dividend & youth-led consumption growth | +0.7% | Nationwide, the strongest in urbanizing provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Expanding Middle Class

The Philippines is close to reaching upper-middle-income status, with gross national income (GNI) per capita increasing from USD 4,320 in 2023 to about USD 4,470 in 2024, just USD 26 below the World Bank’s upper-middle-income threshold of USD 4,496 [1]Gulf News, “$26 to go: Philippines nearly cracks the upper middle-income league,” GulfNews.com. . This rise in per-capita income signals improving household purchasing power and a steadily expanding middle class. Higher disposable incomes are strengthening domestic consumption, which supports growth across retail, services, and digital commerce. Although the country is still officially classified as lower-middle-income, continued economic momentum could push it into the upper-middle-income bracket by 2026 or 2027. These income gains reinforce consumer confidence and underpin long-term retail market expansion. Asset ownership data show higher penetration of refrigerators, televisions, and vehicles among middle-income households, which continues to lift demand for electronics, appliances, and higher-quality packaged foods as the Philippines retail market scales. Vulnerability persists because segments of the middle class depend on remittances and face rising living costs, so wage growth and skills programs are vital to sustain purchasing power for the retail industry in the Philippines. The Department of Trade and Industry launched Section G: Job Blueprint for Wholesale and Retail Trade in June 2025 to bolster workforce competitiveness, which can stabilize income growth for retail-affiliated workers over the medium term.

Accelerating E-commerce Adoption and Digital Payments

Digital payments reached 57.4% of retail transaction volume in 2024 and overshot the government’s 52–54% target, with merchant payments making up 66.4% of digital volume across 2.196 billion transactions valued at USD 28.8 billion. The Philippines retail market is benefiting from the rapid scaling of e-wallets and the use of real-time rails like InstaPay, where volumes grew 67.8% from 2023 to 2024 and values rose 46.3% in the same period [2]Bangko Sentral ng Pilipinas, 2024 Report on E-Payments Measurement, BSP.gov.ph. . Traditional sari-sari stores that still anchor everyday shopping are joining this shift, as surveys in 2025 showed a 75% rise in e-wallet usage among these outlets and broad adoption of GCash for business transactions, which turns neighborhood stores into digital cash-in and bill payment points[3]TechNode Global, “E-wallet use jumps 75% in sari-sari stores,” TechNode. . Regulatory tailwinds include the BSP’s 2024–2026 Digital Payments Transformation Roadmap and regional payment interoperability initiatives such as ASEAN Nexus that aim to reduce cross-border transfer fees below 3% from 2026, which may lift net disposable income for remittance recipients and reinforce demand in the Philippines retail market.

Growth of Convenience-Oriented FandB Retailing

The food and beverage segment continues to dominate the Philippines retail market, with convenience-focused formats expanding as urban consumers increasingly favor quick, frequent trips and smaller baskets. Ready-to-eat and ready-to-cook products are becoming more widespread, reflecting deeper penetration of packaged and ultra-processed categories. Small and micro store formats tied to convenience models are growing rapidly, supported by network expansions from leading retail chains that reinforce proximity-based shopping habits. Hybrid online-offline workflows, such as Buy Online, Pick Up In-Store, are improving last-mile efficiency and speeding up customer access, while integration with in-mall marketplaces allows for faster returns and collection. Efforts to strengthen cold chain infrastructure, including new hybrid storage facilities, are addressing supply constraints and helping stabilize prices for fresh and chilled products, supporting further growth in convenience-oriented retail.

Government Logistics Infrastructure Improvements

The Philippine government is investing heavily in public infrastructure to drive economic growth, improve quality of life, and address logistical gaps, with programs targeting major transport corridors, ports, and connectivity hubs. For instance, the government targets public infrastructure spending of 5%-6% of GDP from 2022 to 2028 to drive economic growth, improve the quality of life, and address infrastructure gaps. Under the "Build Better More" program, 207 Infrastructure Flagship Projects (IFP) worth USD 176.7 billion span several key sectors, with physical connectivity leading in both project count and cost [4]Bangko Sentral ng Pilipinas, PPP in the Philippines’ Infrastructure Flagship Projects (June 2025), BSP.gov.ph. . The government listed 81 locally funded port projects worth USD 95.71 million in 2024 and undertook dredging and berth upgrades to reduce turnaround times, including enhancements at Iloilo International Container Port and Poro Point Seaport that together aim to add capacity and decongest Manila gateways. Modernization and expansion of port facilities, including improvements at major hubs and dredging works, are reducing turnaround times and decongesting traditional gateways such as Manila, improving the flow of goods to urban retail centers. The development of multi-node corridors like the Luzon Economic Corridor, alongside complementary expressway links and regional food logistics hubs, is streamlining inter-island transport and lowering per-unit logistics costs for fresh produce, processed foods, electronics, and other retail categories. These infrastructure enhancements also support hybrid fulfillment models by enabling faster deliveries, reducing last-mile bottlenecks, and improving reliability across urban and peri-urban markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic traffic congestion & last-mile inefficiencies | -1.5% | Metro Manila, Metro Cebu, Metro Davao | Short term (≤ 2 years) |

| Rising utility and operating costs for modern formats | -0.9% | National, acute in Metro Manila and Calabarzon | Medium term (2-4 years) |

| Limited cold chain infrastructure for fresh and chilled goods | -1.2% | Nationwide, critical in peri-urban and rural areas | Medium term (2–4 years) |

| High dependence on import-heavy categories and supply chain disruptions | -1.0% | Urban retail hubs, especially Metro Manila and port-adjacent cities | Medium to long term (2–5 years) |

| Source: Mordor Intelligence | |||

Chronic Traffic Congestion and Last-Mile Inefficiencies

Traffic congestion in major urban centers, particularly Metro Manila, significantly increases operating and delivery costs for retailers and logistics providers serving dense markets. Slow travel speeds and high vehicle density extend transit times, reducing asset utilization and reliability of last-mile delivery windows across the retail industry in the Philippine market. These conditions compress margins on low-ticket items and complicate pricing strategies in a highly value-sensitive market. Congested roads and port bottlenecks also raise the risk of stockouts, especially for perishable goods that depend on an uninterrupted cold chain and frequent replenishment cycles. While ongoing public investments in road and port infrastructure aim to alleviate these challenges over time, retailers and logistics firms must rely on scheduling strategies, off-peak operations, and route optimization to maintain service levels in the short term.

Rising Utility and Operating Costs for Modern Formats

Retail operators in major regions such as Metro Manila and Calabarzon are facing steadily increasing operating expenses, with energy, rent, and wage costs rising faster than overall inflation, putting considerable pressure on margins for large and mid-sized store formats that carry high fixed costs. Energy costs, particularly for cold storage and refrigeration, account for a substantial portion of operating budgets, and although the adoption of energy-efficient technologies is growing, the high upfront capital requirements often limit smaller operators from implementing these solutions effectively. Wage adjustments and enhanced regulatory compliance requirements, including stricter consumer protection and quality standards equivalent to USD 10.9 million in budget allocation, further add to operational pressures in the near term. Retailers have responded by accelerating small-format store rollouts, optimizing inventory turnover, and refining cash conversion cycles to maintain financial stability while continuing to serve urban and peri-urban markets efficiently. These cost pressures also encourage operators to rethink their store strategies, favoring proximity-based formats that support hybrid online-offline fulfillment, such as click-and-collect services, to reduce per-unit costs and improve operational flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Premiumization Drives Niche Growth as Staples Anchor Volume

Food and Beverage held a 41.38% share in 2025, which secures staples as the base of the Philippines' retail market and aligns with household consumption’s outsized share of GDP. Supermarkets and hypermarkets are doubling down on private label and value assortments, as price sensitivity remains a central theme and proximity-based shopping reinforces frequent trips for essentials in the Philippines retail market. Health, Beauty, and Personal Care is the fastest-growing category at an 11.87% CAGR to 2031, which reflects income recovery and wellness-oriented spending among urban households. Health and wellness adoption, broader beauty routines, and exposure to social commerce also sustain this premiumization wave within the Philippines retail market. Convenience, product innovation, and subscription-based offerings are also shaping purchasing behavior, particularly for ready-to-use health supplements, skincare, and personal care items. Retailers are responding by creating curated premium sections, loyalty programs, and bundled offerings that cater to aspirational lifestyles while maintaining accessibility through value-tier products.

Electronics and appliances benefit from strengthening import logistics around the Luzon Economic Corridor and from resilient urban demand that prioritizes quality and brand assurance in the Philippines retail market. Apparel and furniture face competition from cross-border e-commerce offers that compress price points and shorten discovery cycles, which challenge traditional store-led growth. Retailers are countering with omnichannel outreach, curated assortments, and flexible return policies to support consideration and trial. The Philippines retail industry sees strong spillovers from cold chain upgrades that improve quality consistency for fresh and chilled products across grocery aisles, which stabilizes pricing and reduces waste. As consumption normalizes, retailers that balance value, innovation, and in-stock reliability will gain ground across categories within the Philippines retail market.

By Distribution Channel: Online Surges as Physical Retail Embraces Omnichannel Integration

Supermarkets/Hypermarkets held 35.24% share in 2025 and continue to serve as anchor channels for weekly shopping, while Online channels are projected to grow at an 8.27% CAGR through 2031 as more households adopt mobile-first commerce in the Philippines retail market. Retailers like SM Retail are expanding proximity-focused formats, opening new stores and using mall assets to facilitate returns and click-and-collect, which reduces last-mile costs and improves convenience. Marketplace-to-retail integrations launched in 2024 allow online shoppers to leverage physical stores for fulfillment, enhancing reliability and shopper experience. Expansion by chains such as Puregold into provincial cities is increasing modern retail coverage, where penetration has historically been lower. Overall, the market is shifting toward a hybrid channel model where physical stores act as pickup points while online marketplaces extend reach and discovery.

Online retail growth is further supported by mobile commerce, with the majority of e-commerce gross merchandise value coming from smartphones, enabling live-stream sales and micro-influencer-driven demand. Platforms like Shopee, Lazada, and TikTok Shop dominate traffic and enhance conversion through interactive shopping experiences. Quick commerce is also expanding, driven by dark stores and micro-fulfillment centers offering ultra-fast delivery windows. Retailers such as Robinsons Retail are launching multi-category e-commerce platforms to strengthen omnichannel presence and retain digital-first customers. As the retail industry in the Philippines evolves, chains that combine app-led promotions, reliable delivery, and store pickup are better positioned to increase customer loyalty while managing unit economics effectively.

By Payment Method: Cash Remains Dominant as E-Wallets Gain Traction

Cash remains the dominant payment method in the Philippines retail market, accounting for 25.37% of the market in 2025. Its widespread use reflects the country’s strong cash-based culture and the convenience it offers for everyday purchases, especially in traditional and smaller retail outlets. Despite digitalization trends, many consumers still prefer cash due to familiarity and limited access to digital payment options in some areas. Retailers continue to accommodate cash payments to serve a broad customer base and ensure inclusivity across different demographic segments. This persistence of cash underscores the ongoing challenge of fully transitioning to a cashless economy in the Philippines.

Meanwhile, e-wallets are rapidly gaining traction and are forecast to grow at a 13.87% CAGR through 2031 as mobile and online commerce expand. The growing adoption of smartphones and improved internet infrastructure has accelerated the shift toward digital payments, especially among younger and urban consumers. E-wallets offer enhanced convenience, faster checkout experiences, and integration with loyalty programs, which appeal to tech-savvy shoppers. Retailers and payment platforms are increasingly integrating e-wallet options into omnichannel systems to streamline the payment process both online and in physical stores. As consumer confidence in digital payments strengthens, e-wallets are poised to capture a larger share of the retail payment market in the coming years.

Geography Analysis

Luzon accounted for 59.39% share of the Philippines retail market in 2025, driven by Metro Manila’s high purchasing power and the growth of logistics corridors connecting key areas like Clark, Subic, and Batangas. The region benefits from advanced digital infrastructure and widespread smartphone use, which boost online retail participation and cross-channel shopping. The Luzon Economic Corridor is designed to reduce travel times between important hubs, helping to shorten inventory lead times for electronics and general merchandise that depend on imported components. Retailers are focusing on new store openings in Luzon, reflecting the region’s strong contribution to retail trips and share of consumer spending. Despite congestion challenges, operators are experimenting with off-peak deliveries and edge consolidation to maintain efficient service levels in Metro Manila.

The Visayas region is seeing benefits from ongoing port upgrades and the expansion of Roll-on/Roll-off routes that lower inter-island transport costs and improve the availability of perishable goods in urban and secondary cities. Established retailers in Visayas validate the density and demand in provincial locations, while new store openings suggest steady growth opportunities. Improvements in ports like Iloilo help expand capacity and facilitate trade, reducing spoilage and improving fresh supply chains that support retail banners. New malls and retail anchors contribute to increased foot traffic and stimulate development, which gradually lifts modern retail penetration in the region. Retailers with omnichannel platforms are synchronizing inventory across Visayas stores to maintain stock availability as port efficiency improves.

Mindanao is a key growth frontier and is projected to grow at a 7.84% compound annual growth rate through 2031, supported by investments in cold chain infrastructure and port modernization in cities like General Santos and Davao. These improvements extend the shelf life of products and stabilize prices, enhancing the economics of retail supply chains in the region. As logistics improve, retailers are expanding their product assortments and increasing delivery frequency to serve growing urban centers, capturing more consumer spending. Expansion by major chains into provincial cities is helping bridge gaps in retail formats as incomes rise. With food and essentials leading demand, Mindanao’s retail sector is poised for growth as better transport links reduce spoilage and improve product freshness.

Competitive Landscape

The Philippines retail market remains fragmented, with the top players collectively holding just over a third of the market share. Leading retailers are expanding their store footprints and enhancing omnichannel capabilities to maintain customer visits and basket sizes. Meanwhile, newer challengers are leveraging marketplaces, social commerce, and quick commerce models to shorten transaction times and capture consumer demand. Large retail chains are investing heavily in proximity stores within urban areas to strengthen local shopping convenience. These strategies position stores as critical hubs for pickups, returns, and neighborhood replenishment, supporting a seamless shopping experience.

There is significant potential in the quick commerce segment, which is growing rapidly and creating opportunities for operators to scale dark stores and optimize product assortments for faster delivery. Marketplace players are also investing in warehousing and sorting centers to reduce lead times, raising competition standards for traditional retail chains. Digital wallets have become widely adopted, and their integration into store operations reduces cash handling and speeds up transactions during peak hours. Retailers that effectively synchronize inventory across channels and use data-driven promotions can better respond to price fluctuations and supply shortages. However, compliance requirements related to food safety and data privacy increase operational challenges for smaller players while giving larger, more organized chains a competitive advantage.

Some retailers are experimenting with premium lifestyle store formats in densely populated communities to improve unit economics amid rising rent costs. Specialty retailers with a focus on premium products are well-positioned to benefit if consumer discretionary spending remains strong, especially in key urban districts. E-commerce platforms are being scaled to protect core product categories and enable cross-selling across a wider range of merchandise. The market is expected to remain fragmented as digital channels grow and micro-fulfillment capabilities improve to support faster delivery in major cities. Ultimately, success will depend on retailers’ ability to execute well on product assortment, availability, and convenience to gain and retain market share.

Philippines Retail Industry Leaders

SM Investments Corp. (SM Retail)

Robinsons Retail Holdings Inc

Puregold Price Club Inc

Metro Retail Stores Group Inc.

SSI Group Philippines

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SM Investments Corporation reported that SM Retail opened 367 new stores in the first nine months of 2025, including 254 SM Markets, 112 Specialty Retail stores, and one SM Store, primarily in Food and Specialty Retail formats, underscoring the company's aggressive footprint expansion and strategic pivot toward proximity-based formats that reduce last-mile costs in congested urban areas.

- October 2025: Metro Retail Stores Group Inc. inaugurated Metro Corner in Mandani Bay, Mandaue, Cebu, introducing a premium lifestyle store format tailored for vertical communities, testing whether density-based, high-margin assortments can offset escalating rent in prime urban locations and capture affluent consumers in Cebu's expanding condominium market.

- June 2025: The Department of Trade and Industry, Philippine Retailers Association, and Supply Chain Management Association of the Philippines jointly launched the Section G: Job Blueprint for Wholesale & Retail Trade on June 16, 2025, at SM North EDSA Annex, a strategic framework aimed at enhancing competitiveness, generating employment, and outlining workforce development priorities in a sector employing 10.2 million Filipinos and contributing USD 89.67 billion which is18% of GDP to the economy.

- December 2024: Puregold Price Club Inc. opened 26 new Puregold stores, 4 S&R Membership Shopping Warehouse, and 8 S&R New York Style QSR. PGOLD operates a total of 602 stores nationwide, comprising 511 Puregold stores, 29 S&R Membership Shopping Warehouses, and 62 S&R New York Style QSRs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Philippines retail market as the full value of consumer goods that reach households through modern formats such as supermarkets, convenience stores, department stores, specialty chains, pure-play e-commerce sites, and the still-dominant sari-sari and wet markets. We count each sale at its final ticket price in pesos and convert it to U S dollars using the yearly average rate.

Scope Exclusion: wholesale trade, duty-free shops serving tourists, and offshore e-commerce orders fulfilled outside the country are not included.

Segmentation Overview

- By Product Category

- Food and Beverage

- Apparel and Footwear

- Consumer Electronics and Appliances

- Home and Furniture

- Health, Beauty and Personal Care

- Others

- By Distribution Channel

- Hypermarkets and Supermarkets

- Department Stores

- Convenience Stores and Mini-markets

- Specialty Stores

- Traditional (Warung / Kiosks)

- Online

- By Payment Method

- Cash

- Debit & Credit Cards

- E-Wallets

- Bank Transfers / Pay-Later

- By Region

- Luzon

- Visayas

- Mindanao

Detailed Research Methodology and Data Validation

Primary Research

We interview store managers across Luzon and Visayas, FMCG distributors, mall developers, fintech payment executives, and logistics providers. Their insights refine average selling prices, the modern-trade share shift, and emerging online basket sizes.

Desk Research

Mordor analysts first build a demand stack from the Philippine Statistics Authority's spending surveys, Bangko Sentral household tables, Department of Trade and Industry registrations, and UN Comtrade import codes tied to consumer goods. Company filings, investor decks, and press archives accessed through Dow Jones Factiva and D&B Hoovers clarify channel turnover and pricing. White papers from the Philippine Retailers Association and ASEAN retail forums help us gauge informal volumes and inflation. The sources named are illustrative; many others underpin validation.

Market-Sizing & Forecasting

A top-down model starts with national retail turnover and splits it into product and channel pools using production data, import flows, and shopper-penetration surveys. Select bottom-up checks, rolling up listed chain revenues and estimating online gross merchandise value from payment volumes, test totals. Key drivers include real disposable income, inflation-adjusted ASPs, e-wallet penetration, new gross leasable area, and mandated wage hikes. Multivariate regression projects each driver while scenario analysis gauges shocks such as typhoons or supply disruptions; proxy ratios from comparable ASEAN markets bridge any residual gaps.

Data Validation & Update Cycle

Outputs pass dual peer reviews and variance scans against indicators like power use and freight flows. Reports refresh annually, with mid-cycle updates triggered by major policy moves or price spikes, ensuring clients receive our latest view.

Why Mordor's Philippines Retail Sector Baseline Earns Trust

Published estimates often diverge because firms vary channel scope, inflation handling, and refresh cadence. Our team shares model inputs openly, letting users trace every peso back to a public series or interview note.

Key gap drivers elsewhere include mixing wholesale with retail sales, applying blanket growth to informal outlets, or fixing peso-to-dollar rates at a single point in time. We isolate each variable first, then apply the average exchange rate for the base year, delivering a stable yet transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 41.23 B (2025) | Mordor Intelligence | - |

| USD 69.42 B (2024) | Global Consultancy A | Includes wholesale and duty-free sales; older base year; unclear FX method |

| USD 45.62 B (2024) | Regional Consultancy B | Omits informal trade; uniform price-rise assumption |

These comparisons show that Mordor's disciplined scope selection, driver-level modeling, and timely refresh supply a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the growth outlook to 2031 for the Philippines retail market?

The Philippines retail market is valued at USD 44.51 billion in 2026 and is projected to reach USD 64.99 billion by 2031, reflecting a 7.86% CAGR driven by resilient household spending and channel digitalization.

Which product categories lead today and which will grow fastest through 2031?

Food & Beverage leads with 41.38% revenue share in 2025, while Health, Beauty, and Personal Care is set to grow fastest at an 11.87% CAGR to 2031.

Which distribution channels are gaining momentum in the Philippines retail market?

Which distribution channels are gaining momentum in the Philippines retail market?

Which regions drive demand, and where is growth strongest?

Luzon accounts for 59.39% of demand, with Mindanao recording the highest projected CAGR at 7.84% through 2031, supported by cold chain and port upgrades.

Who are the key players and how are they expanding?

Leading banners include SM Investments, Robinsons Retail, and Puregold, with SM opening 367 stores in the first nine months of 2025 and Puregold budgeting PHP 6.35 billion (USD 116.21 million) for new stores and warehouses in 2025.

Page last updated on: