Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

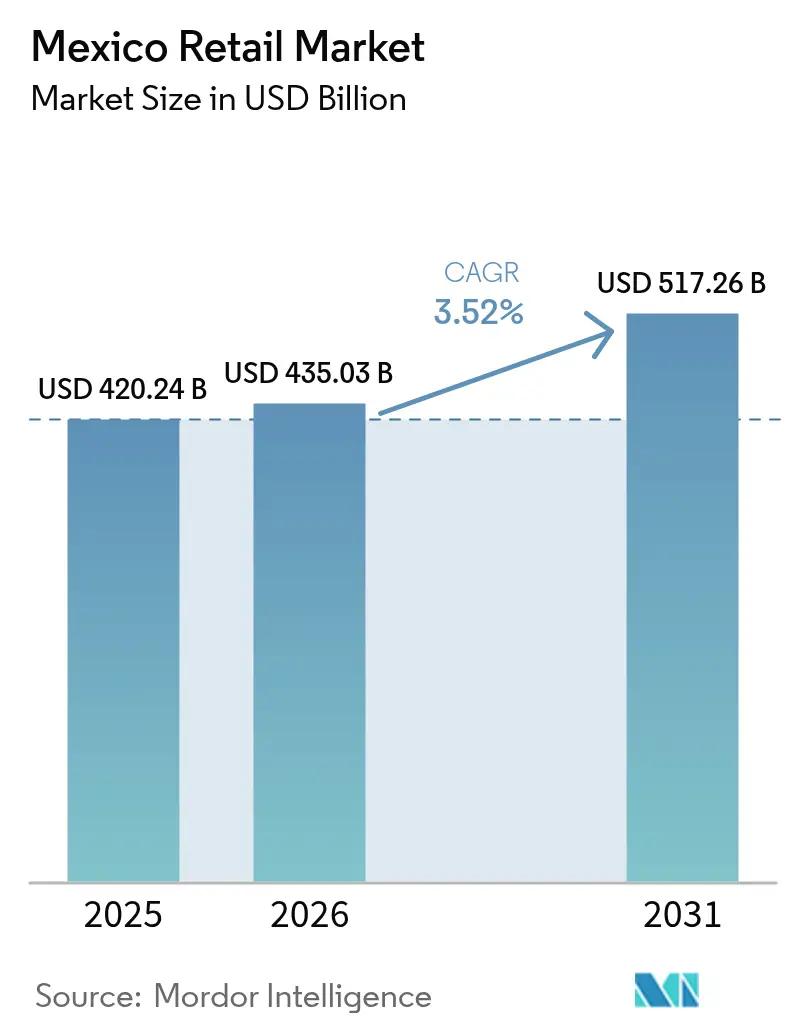

| Base Year Market Size (2025) | USD 420.24 Billion |

| Market Size (2026) | USD 435.03 Billion |

| Market Size (2031) | USD 517.26 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Retail Market Analysis by Mordor Intelligence

The Mexico retail market size was valued at USD 420.24 billion in 2025 and estimated to grow from USD 435.03 billion in 2026 to reach USD 517.26 billion by 2031, at a CAGR of 3.52% during the forecast period (2026-2031). Nearshoring-driven wage gains in northern industrial hubs are lifting discretionary spending on electronics, home improvement supplies, and automotive accessories, while Mexico’s large informal economy continues to anchor grocery and personal-care demand in traditional corner stores. E-commerce adoption is accelerating as smartphone penetration surpasses 85% of adults and digital payments reach 45% of retailers, encouraging omnichannel investments among incumbent chains. Fintech micro-lending models expand purchasing power for low-income households and help modern retailers penetrate cash-dominant rural markets. Retail real-estate additions of more than 500,000 square meters in 2024 illustrate developers’ confidence in modern trade growth potential, even as organized crime-related cargo theft raises distribution costs for high-value consumer goods. Competitive intensity remains moderate, with the top five players accounting for 36.2% of total revenues, leaving white-space opportunities for specialty formats and discount chains to capture share in underserved geographies.

Key Report Takeaways

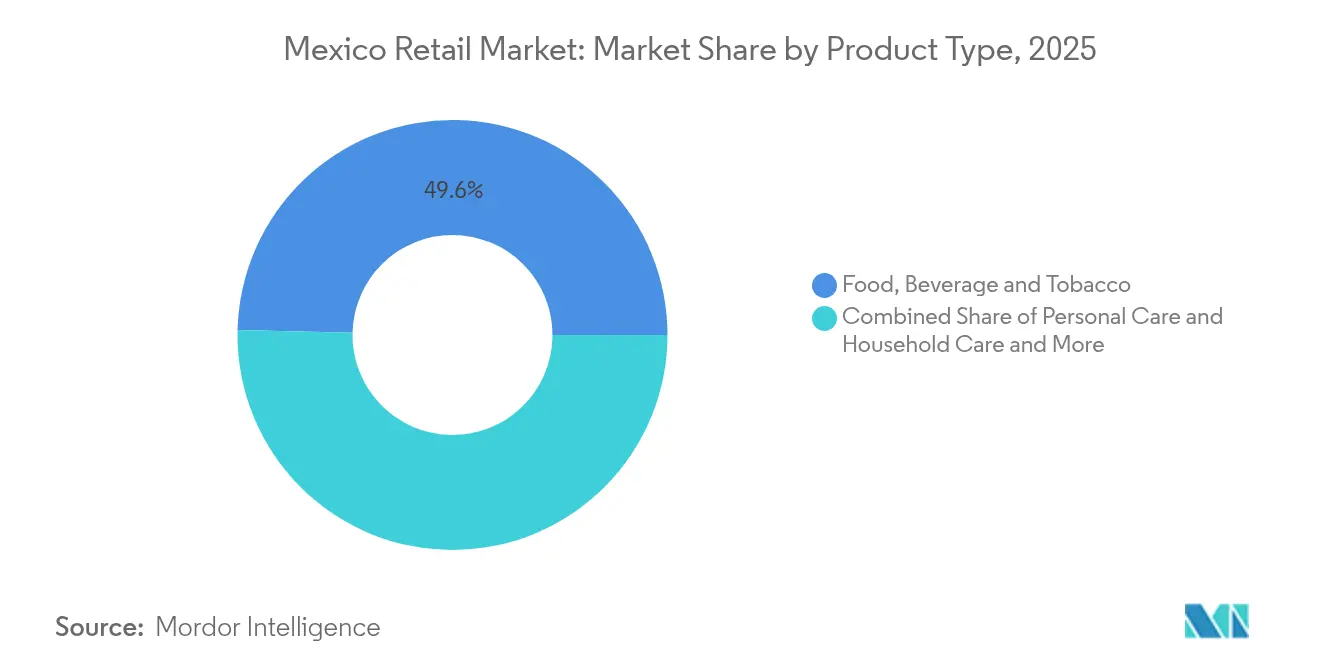

- By product type, food, beverage & tobacco held 49.63% of the Mexico retail market share in 2025, while electronic & household appliances are forecast to advance at a 10.21% CAGR through 2031.

- By retail channel, traditional mom & pop stores controlled 41.25% of the Mexico retail market size in 2025, yet e-commerce & others are growing at a brisk 15.44% CAGR to 2031.

- By format, convenience stores led with 28.94% of the Mexico retail market share in 2025, whereas specialty stores are set to expand at a 10.35% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & middle-class expansion | +0.8% | Mexico, with concentrated gains in Central and Northern regions | Medium term (2-4 years) |

| Accelerating e-commerce & digital payment adoption | +1.2% | National, with urban concentration in CDMX, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Rapid roll-out of modern trade formats | +0.6% | Mexico, strongest in Central and Southeast regions | Medium term (2-4 years) |

| Near-shoring boom lifting industrial & auto retail | +0.5% | Northern Mexico, spillover to Central regions | Long term (≥ 4 years) |

| Front-of-pack labelling driving healthier product mixes | +0.3% | National, with higher compliance in urban areas | Medium term (2-4 years) |

| Fintech micro-credit unlocking rural consumption | +0.4% | Rural Mexico, expanding to semi-urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Middle-Class Expansion

Nearshoring investment of USD 46 billion over five years has raised manufacturing wages 15-20% above national averages, boosting purchasing power around industrial corridors[1]Source: Banco de México, “Quarterly Report Q1 2024,” banxico.org.mx. Elevated income levels translate into premiumization across electronics, appliances, and automotive accessories, encouraging retailers to widen assortments of higher-margin branded goods. Consumption upgrades spur format diversification as workers seek modern trade conveniences absent in traditional outlets. Retailers located in Monterrey, Ciudad Juárez, and Tijuana report double-digit same-store sales growth in discretionary categories, indicating robust elasticity to rising wages. Regional spillovers reach service sectors, expanding demand for dining, fashion, and wellness products. These patterns reinforce the Mexico retail market’s resilience to macro volatility by diversifying consumer spending sources.

Accelerating E-Commerce and Digital Payment Adoption

Digital payment acceptance climbed from 22% to 45% of retail merchants between 2014 and 2022, and online purchases now account for two-thirds of smartphone transactions[2]Source: Instituto Nacional de Estadística y Geografía, “Encuesta Mensual de Comercio Minorista 2024,” inegi.org.mx. E-commerce revenues grew 24.6% year-on-year in 2024 and are set to surpass USD 63 billion in 2025, making Mexico Latin America’s fastest-rising digital retail arena. Buy-now-pay-later (BNPL) offerings from startups such as Aplazo extend micro-credit to unbanked consumers, raising average ticket sizes in fashion and electronics stores. Amazon’s partnership with Kueski exemplifies how global platforms adapt to local financial infrastructure gaps to stimulate demand. Domestic chains respond by integrating click-and-collect services, while 56% of retail executives deploy AI-based marketing tools to personalize promotions and boost conversion. Collectively, these shifts accelerate the Mexico retail market’s channel migration from cash-heavy legacy systems to data-rich digital ecosystems.

Rapid Roll-Out of Modern Trade Formats

Shopping-center inventory expanded 234,000 square meters in 2023, with an additional 500,000 square meters scheduled for completion in 2024. Developers concentrate 61% of new space in Central and Southeast regions, where urban density supports small-format supermarkets and hybrid convenience-supermarket concepts. Retailers optimize footprints by combining broad assortments with quick-service kiosks to fit Mexico’s compact living spaces and frequent shopping habits. OXXO’s financial-service counters and Soriana’s 24-hour stores reveal experimentation aimed at increasing trip frequency and basket size. Specialty stores in electronics and home improvement increasingly cluster within mixed-use real-estate projects to capture weekend leisure traffic. As modern trade spreads, supply-chain efficiencies improve, narrowing price gaps with informal outlets and strengthening the Mexico retail market’s formalization trend.

Near-Shoring Boom Lifting Industrial and Auto Retail

Mexico became the United States’ top trading partner in 2024, catalyzing demand for industrial supplies, tools, and automotive components. Home Depot earmarked USD 1.3 billion for Mexico through 2030, with 100% local sourcing targets that boost domestic manufacturing linkages. Warehouse-club operators expand bulk-purchase assortments of industrial consumables, addressing newfound demand from factory contractors. Automotive aftermarket retailers add distribution centers near assembly plants to support higher vehicle output and cross-border service requirements. Rising industrial employment also fuels B2C spending on durable goods, reinforcing multi-format retailers’ push into northern states. The Mexico retail market benefits from these dual B2B-B2C revenue streams, raising cyclical stability compared with purely consumer-driven economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High informality limits modern retail penetration | -0.7% | National, most pronounced in rural and semi-urban areas | Long term (≥ 4 years) |

| Logistics bottlenecks inflate distribution costs | -0.5% | National, severe impact on North-South corridors | Medium term (2-4 years) |

| Security concerns in key commercial zones deter investment | -0.6% | Regional, with elevated risk in northern and border states | Medium term (2–4 years) |

| Regulatory complexity and slow permitting for new stores | -0.4% | National, especially in high-density urban municipalities | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

High Informality Limits Modern Retail Penetration

Informal employment covers 56% of Mexico’s workforce, preserving the dominance of cash-based corner stores in food and personal-care categories. These merchants offer flexible credit, personalized service, and doorstep proximity that organized chains find costly to replicate. CFDI 4.0 e-invoicing rules, while promoting tax compliance, impose technology costs that many small operators cannot absorb, risking further entrenchment of informal practices. As a result, modern retailers must maintain dual cash-and-digital systems, complicating inventory and accounting processes. The persistent informal share dilutes economies of scale, constrains pricing power, and slows the Mexico retail market’s path to full formalization. Without targeted fiscal incentives or infrastructure support, uptake of modern trade among micro-merchants will likely remain gradual.

Logistics Bottlenecks Inflate Distribution Costs

More than 24,000 cargo-theft incidents in 2024 raised insurance premiums and security outlays for retail fleets, particularly in high-value electronics and liquor shipments[3]Source: National Chamber of Cargo Transportation, “Annual Security Report 2024,” canacar.com.mx. Highway congestion between Mexico City and northern border crossings limits reliable delivery windows, forcing retailers to keep extra safety stock. Port delays in Manzanillo and Veracruz add days to lead times for imported apparel and home furnishings, shortening fashion seasons and markdown windows. Mid-tier chains lacking advanced route-optimization tools incur disproportionate costs, hampering price competitiveness against larger peers. Adoption of GPS tracking and private security escorts mitigates risk but adds operating expense that ultimately passes to consumers. Together, these factors drag down the Mexico retail market’s supply-chain efficiency and squeeze retail margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Dominates, Electronics Accelerate

Food, beverage & tobacco sustained 49.63% of the Mexico retail market size in 2025 as grocery purchases remained households’ largest expenditure. Electronics & household appliances delivered a leading 10.21% CAGR and are set to capture a higher slice of the Mexico retail market share by 2031 as nearshoring lifts industrial wages and stimulates demand for home-improvement gadgets. Personal-care and household-care brands capitalize on premiumization, while apparel growth softens under 35% textile import tariffs that lift prices and encourage resale channels. Furniture and hobby products follow disposable-income trajectories, but seasonal tourism in coastal states adds niche demand for décor and sports equipment. Industrial and automotive products benefit from supplier proximity to new manufacturing plants, enabling shorter replenishment cycles. Cross-category marketing via loyalty apps promotes bundle purchases, smoothing category volatility and reinforcing revenue diversification inside the Mexico retail market.

Consumer electronics retailers intensify omnichannel tactics, integrating BNPL at checkout to raise conversion among credit-thin millennials, whereas grocery chains test dark-store micro-fulfillment to shorten delivery windows. Beverage manufacturers reformulate recipes to avoid front-of-pack warning labels, supplying retailers with healthier alternatives that carry higher margins. Tobacco volumes drift downward as excise taxes climb, but vaping accessories emerge as replacement sub-category. Retailer-owned brands scale in personal-care aisles, capturing price-sensitive shoppers without eroding premium brand allocations. Apparel specialists face sourcing challenges from tariff changes but remain competitive through rapid private-label design cycles and influencer marketing. Overall, diversified category performance stabilizes the Mexico retail market size against macro shocks.

By Retail Channel: Traditional Resilience Meets Digital Disruption

Traditional mom & pop outlets retained 41.25% of the Mexico retail market share in 2025, underpinned by cultural preference for neighborhood service and flexible store credit. E-Commerce & others, however, posted a vigorous 15.44% CAGR, supported by smartphone penetration, BNPL adoption, and logistical innovations like pickup lockers. Modern trade retailers merge physical and digital channels through click-and-collect counters and app-based loyalty programs that offer cashback on repeat purchases. CFDI 4.0 compliance affords large chains operational transparency that streamlines invoicing and inventory reconciliation, widening efficiency gaps versus informal rivals. Government social-assistance deposits on digital wallets stimulate low-income e-commerce spend, further attracting platform investments. This channel migration diversifies revenue streams and elevates data analytics capabilities essential to the Mexico retail industry’s next phase of growth.

Despite digital momentum, informal tiendas remain defenders of last-mile convenience in rural towns, where logistic infrastructure lags and cash wages dominate. Modern chains experiment with nano-store formats under 150 square meters to match informal proximity while preserving assortment advantages. Online marketplaces supplement rural coverage by partnering with taxi networks for same-day delivery, blending informal transport with formal retail tech stacks. Increasingly, omnichannel strategies hinge on trust-building, requiring clear return policies and localized fulfillment to lure habitual cash shoppers online. Competitive tension between legacy and emerging channels sustains innovation that ultimately broadens customer choice across the Mexico retail market.

By Format: Convenience Stores Lead, Specialty Formats Surge

Convenience stores captured 28.94% of the Mexico retail market size in 2025, thanks to high urban density and consumers’ frequent small-basket shopping behavior. Specialty stores, ranging from beauty boutiques to hardware shops, are forecast to outpace all other formats with a 10.35% CAGR, reflecting demand for curated assortments and service expertise. Hypermarkets and supermarkets preserve scale benefits in fresh food and general merchandise but confront margin pressure as online grocers add price comparison tools. Department stores modernize loyalty programs and introduce cross-border e-commerce to revive footwear and cosmetics sales. Warehouse clubs pursue aggressive expansion, adding 30 new locations annually to address bulk purchase appetite among growing middle-class households. Format innovation such as cash-free micro-markets inside office parks and autonomous kiosks at transport hubs expands pathways to capture incremental spend in the Mexico retail market.

FEMSA’s OXXO integrates bill-payment counters and fintech kiosks that broaden revenue per square meter while locking in daily footfall. Amazon leverages its Just Walk Out technology in pilot grocery sites, encouraging local competitors to trial self-checkout to cut labor costs. Costco’s largest store in Mexico City includes expanded seasonal aisles and fresh-food courts that extend dwell time and basket size. Specialty electronics chains deploy in-store service labs, differentiating on repairs and installations beyond online competitors’ capabilities. Format convergence accelerates as supermarkets add ready-to-eat meals and drugstore sections, while convenience stores trial fresh produce, blurring traditional boundaries. This dynamism secures multiple growth vectors within the Mexico retail market share.

Competitive Landscape

The Mexico retail market is moderately fragmented, with the top five chains holding a significant share of the market, while a mix of regional specialists and informal shops dominates the rest. Walmart Mexico earmarked USD 6 billion to expand supercenter, Bodega Aurrera, and e-commerce operations, underlining incumbents’ intent to fortify leadership positions. Chedraui plans 140 openings in secondary cities, signaling aggressive turf battles outside core metros. Tiendas 3B’s MXN 1.6 billion (USD 94.10 million) spent for 420 stores demonstrates momentum in discount formats appealing to cost-conscious shoppers. Dollar General’s Mexico entry intensifies competition in the value segment, leveraging U.S. sourcing efficiencies to challenge local discounters. Ulta Beauty’s partnership with Axo introduces global cosmetics brands, elevating specialty beauty competition. AI deployment across merchandising and logistics systems accelerates among leading players, with 90% adopting predictive analytics for inventory optimization.

Sustainability emerges as a differentiation lever, evidenced by FEMSA and Coca-Cola FEMSA securing spots in the S&P Global Sustainability Yearbook 2025. ESG transparency not only attracts socially responsible investors but also resonates with younger consumers, influencing brand affinity. Regulatory compliance prowess, particularly with new CINIF sustainability disclosure standards, offers large firms reputation advantages over smaller peers struggling with data capture. Cargo-theft mitigation strategies, such as jointly funded secure corridors, foster industry collaboration while raising barriers for new entrants. Overall, competitive dynamics pivot on omnichannel capability, operational efficiency, and ESG credentials, with scale players consolidating share yet leaving room for nimble specialists to thrive.

Mexico Retail Industry Leaders

Walmart de México y Centroamérica (Walmex)

Organización Soriana

FEMSA Comercio (OXXO)

Chedraui

Liverpool

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Home Depot announced USD 1.3 billion investment in Mexico through 2030 to achieve 100% local sourcing by 2028, adding over 20,000 jobs.

- February 2025: Walmart Mexico joined the Hecho en Mexico campaign across 3,200 stores and online platforms, strengthening supplier localization.

- January 2025: New CINIF sustainability disclosure standards became mandatory, requiring 30 basic environmental, social, and governance indicators in financial reports.

- August 2024: FEMSA acquired Delek US for USD 385 million, adding 249 U.S. convenience stores to be re-branded as OXXO.

Mexico Retail Market Report Scope

The retail industry is a market that includes activities like selling goods or services directly to the consumer by a company that is usually purchased for personal or family use. Traders can be both retail and institutional.

Mexico's retail industry is segmented into product and distribution channels. By product, the market is segmented into food and beverage, tobacco products, personal and household care, apparel, footwear and accessories, furniture, toys, hobby, industrial, automotive, and electronic household appliances. The market is segmented by distribution channel into hypermarkets, supermarkets, convenience stores, department stores, and specialty stores. The report offers market size forecasts in value (USD) for all the above segments.

By Product Type

| Food, Beverage & Tobacco Products |

| Personal Care & Household Care |

| Apparel, Footwear & Accessories |

| Furniture, Toys & Hobby |

| Industrial & Automotive |

| Electronic & Household Appliances |

| Other Products |

By Retail Channel

| Traditional Mom & Pop Retail |

| Modern Trade Retail |

| E-Commerce & Others |

By Format

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (drugstore, cash-&-carry, wholesaler) |

| By Product Type | Food, Beverage & Tobacco Products |

| Personal Care & Household Care | |

| Apparel, Footwear & Accessories | |

| Furniture, Toys & Hobby | |

| Industrial & Automotive | |

| Electronic & Household Appliances | |

| Other Products | |

| By Retail Channel | Traditional Mom & Pop Retail |

| Modern Trade Retail | |

| E-Commerce & Others | |

| By Format | Hypermarkets |

| Supermarkets | |

| Convenience Stores | |

| Department Stores | |

| Specialty Stores | |

| Others (drugstore, cash-&-carry, wholesaler) |

Key Questions Answered in the Report

How large is the Mexico retail market in 2026 and what growth is expected by 2031?

The market is valued at USD 435.03 billion in 2026 and is forecast to reach USD 517.26 billion by 2031, reflecting a 3.52% CAGR.

Which product category generates the highest revenue in Mexican stores today?

Food, Beverage & Tobacco products lead, accounting for 49.63% of retail sales in 2025.

Which retail channel is expanding fastest across Mexico?

E-Commerce & Others is the fastest, registering a 15.44% CAGR through 2031 as smartphone and digital-payment usage rises.

What regulatory changes will most affect retailers in the next few years?

Mandatory sustainability disclosures under CINIF and continued rollout of CFDI 4.0 e-invoicing will raise compliance demands and favor organized chains.

Page last updated on: