Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.68 Billion |

| Market Size (2026) | USD 19.44 Billion |

| Market Size (2031) | USD 23.69 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Retail Market Analysis by Mordor Intelligence

Qatar retail market size in 2026 is estimated at USD 19.44 billion, growing from 2025 value of USD 18.68 billion with 2031 projections showing USD 23.69 billion, growing at 4.05% CAGR over 2026-2031. A wealthy consumer base with GDP per-capita of USD 95,273 continues to favor premium, sustainable, and technology-enhanced products, making the Qatar retail market a laboratory for upscale concepts and smart-store pilots. Logistics assets such as Hamad Port’s 7.5 million TEU capacity and Qatar Airways’ record 40 million passengers funnel global merchandise and travelers into local storefronts, bolstering omnichannel growth and duty-free turnover. Retailers also prepare for the imminent VAT regime and a 15% global minimum tax, which together tighten cost controls and encourage digital accounting platforms that improve margin visibility.

Technology adoption has become a baseline expectation: 90% of chief executives already deploy generative AI, while the state’s USD 2.4 billion incentive package underwrites data-science projects that make predictive-ordering and cashier-less checkout normal features across the Qatar retail market. Consumer surveys reveal that 57% of residents seek sustainable products and 43% shop by phone, so retailers integrate carbon-footprint labels, mobile loyalty programs, and on-demand delivery to stay relevant. Competitive intensity remains moderate because the top five players hold 65% market share, yet that concentration forces smaller operators to specialize in convenience and premium niches to avoid direct scale competition, especially as Lulu Group leverages 29.6% private-label penetration to reinforce leadership. All told, the combination of affluent shoppers, smart infrastructure, and regulatory shifts sets the stage for sustained, innovation-driven expansion across the Qatar retail market over the next five years.

Key Report Takeaways

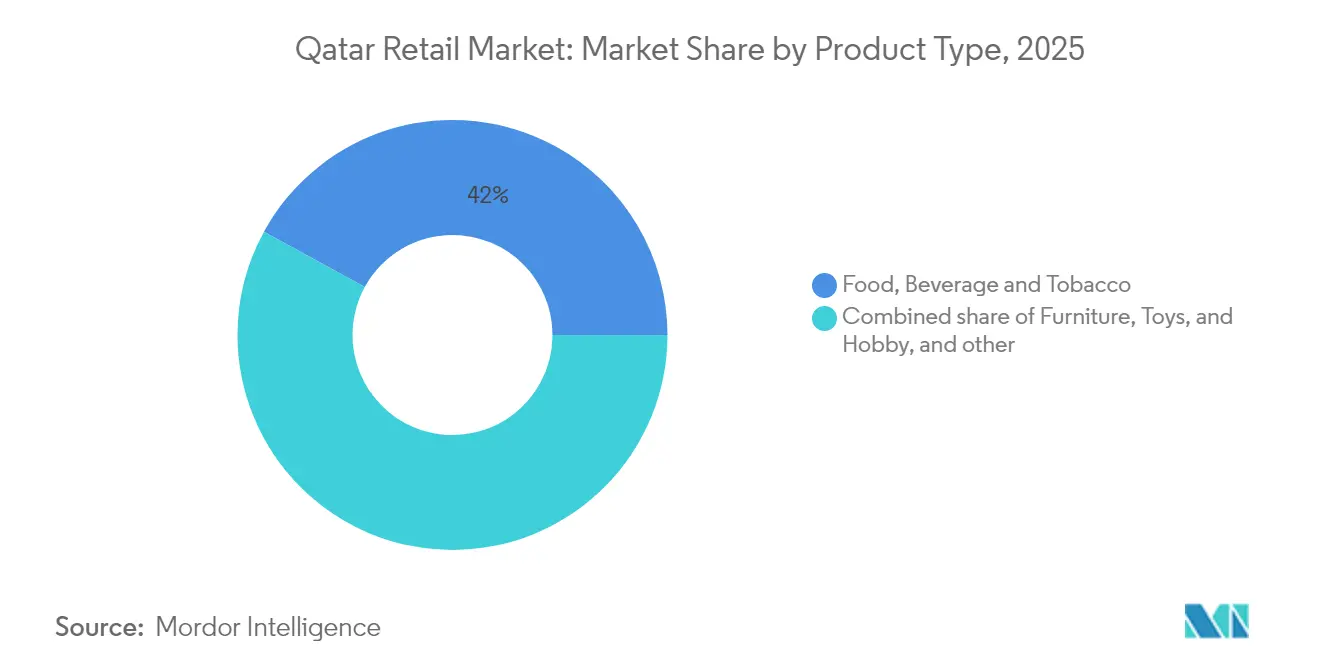

- By product category, Food, Beverage & Tobacco commanded 42.02% of the Qatar retail market share in 2025, whereas Electronic & Household Appliances is projected to post 11.28% CAGR to 2031.

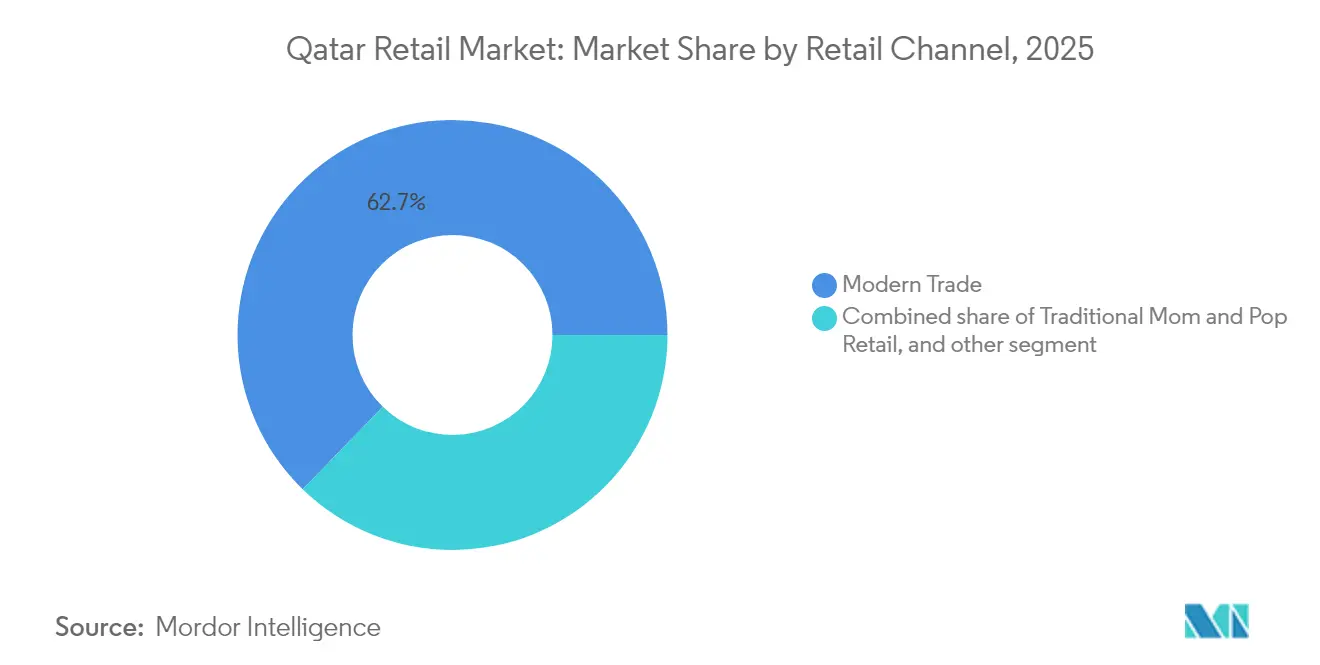

- By retail channel, Modern Trade captured 62.73% of the Qatar retail market size in 2025, while E-Commerce & Others is advancing at 17.95% CAGR through 2031.

- By format, Hypermarkets held 47.66% revenue share in 2025; Convenience Stores are forecast to expand at 13.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FIFA 2022 legacy tourism surge | +0.8% | National, concentrated in Doha Municipality | Medium term (2-4 years) |

| Rising disposable income & expatriate inflows | +0.6% | National, with premium segments in Lusail and West Bay | Long term (≥ 4 years) |

| Expansion of modern retail infrastructure | +0.5% | National, with major developments in Doha and Al Wakrah | Medium term (2-4 years) |

| AI-driven analytics & cashier-less pilots | +0.3% | Urban centers, early adoption in hypermarkets | Short term (≤ 2 years) |

| Government logistics free-zones for omnichannel | +0.4% | Ras Bufontas and Umm Al Houl zones | Medium term (2-4 years) |

| Premium halal & health-oriented demand | +0.3% | National, with higher penetration in affluent districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FIFA 2022 Legacy Tourism Surge

Tourist arrivals reached 2.8 million during the first nine months of 2023 and eclipsed previous full-year totals, supporting airport, hotel, and downtown retail turnover in the Qatar retail market [2]Hala Matar Choufany, “Qatar – Beyond the World Cup,” hvs.com. . Qatar Airways logged QAR 6.1 billion net profit and 40 million passengers in 2023-24, driving duty-free sales up 22% as travelers funneled spending into luxury goods and souvenirs. Mega-developments such as Place Vendôme, once crowned “World’s Most Beautiful Shopping Mall,” integrate hotels, entertainment, and marina access that lengthen dwell time and encourage experiential spend. The government targets 6 million annual visitors by 2030, planning more festivals and cruise-port calls that raise weekday and shoulder-season traffic. Retailers therefore curate Gulf-exclusive SKUs, host pop-up art exhibits, and localize loyalty programs in Mandarin to tap high-spend tourists from China. Airport operators reserve additional airside footage for premium fashion and confectionery concessions to monetize the forecast flow. Collectively, tourism keeps footfall robust in prime malls and buffers sales against any oil-price volatility, reinforcing steady growth for the Qatar retail market.

Rising Disposable Income & Expatriate Inflows

Non-hydrocarbon activity now accounts for 64% of real GDP, giving households diversified income sources and lifting discretionary budgets across the Qatar retail market. February 2024’s Mustaqel Visa allows skilled professionals to secure five-year residence, creating a stable customer segment keen on premium electronics, gourmet foods, and designer apparel. Mobile-commerce penetration sits at 43%, and sustainability remains a purchase driver for 57% of consumers, so apps feature carbon-score badges and refill-pack subscriptions that attract eco-minded shoppers. The USD 2.4 billion AI incentive package lures data engineers whose high earnings translate into smart-home device upgrades that stimulate the electronics segment’s 11.75% CAGR. Expatriate communities also demand authentic cuisine, prompting supermarkets to expand ethnic aisles and use dynamic shelf labels in multiple languages. Luxury boutiques located in Lusail City host bilingual stylists and remote-shopping services for business travelers who extend stays. As more professionals settle long-term, home-furnishings chains observe larger basket sizes on durable goods, aiding margin expansion in the Qatar retail market.

Expansion of Modern Retail Infrastructure

Place Vendôme’s 1.15 million m², Mall of Qatar’s 256,000 m², and Doha Festival City’s 433,847 m² footprints collectively redefine shopping in Qatar, blending retail, leisure, and cultural activities that position malls as day-trip destinations. Reduced business-license fees cut by up to 90% in July 2024 lower tenant entry barriers and accelerate concept rollouts in the Qatar retail market. Hamad Port’s bonded warehouses and Ras Bufontas free-zone plots further shorten supply chains, letting brands replenish flagship stores within forty-eight hours of customs clearance. Developers equip malls with 5G, curbside pickup lanes, and AI-based crowd-management dashboards that orchestrate tenant promotions in real time. Luxury landlords co-create seasonal art biennales with tourism authorities to drive incremental footfall outside peak travel windows. Still, retail GLA per capita now exceeds 1.3 m², so operators adopt multi-tenant entertainment anchors, such as indoor cliffs and VR arenas, to differentiate. The net effect is a modern infrastructure backbone that sustains shopper engagement but demands ongoing innovation to mitigate vacancy risk in the Qatar retail market.

AI-Driven Analytics & Cashier-Less Pilots

Generative-AI pilots span demand forecasting, real-time pricing, and autonomous checkout lanes across hypermarkets and specialty stores in the Qatar retail market. The Ministry of Communications and Information Technology drafts an AI-governance framework to assure data ethics, thereby encouraging broader deployment [3]Ministry of Communications and Information Technology, “AI Regulatory Framework Draft,” thepeninsulaqatar.com. . Qatar Central Bank complements these efforts with Request-to-Pay functionality on its Fawran network, letting merchants nudge shoppers for instant settlement and reduce failed-transaction rates. Lulu Group’s AI-enabled demand-sensing tool already trimmed stock-outs by 14% and supported 70% e-commerce revenue growth in 2024, proving ROI for data-driven replenishment. Convenience-store operators test vision-based checkout pods that cut queue times below thirty seconds and free staff for upselling. Electronics chains integrate AI chatbots into Arabic and English websites, guiding buyers on smart-home compatibility. As adoption spreads, predictive maintenance on cold-chain assets and energy-use analytics in malls reduce operating costs, embedding AI as a non-negotiable pillar of competitiveness across the Qatar retail market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shopping-mall over-supply & cannibalization | -0.7% | Doha Municipality | Short term (≤ 2 years) |

| Import-dependence & supply-chain volatility | -0.5% | National, acute for perishables | Medium term (2-4 years) |

| Rising operational costs (utilities, rent, labor) | -0.6% | Urban retail hubs | Medium term (2–4 years) |

| Saturation of mid-tier retail segments | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shopping-Mall Over-Supply & Cannibalization

Vacancy already tops 20% in several Doha malls as rapid GLA expansion outpaced immediate consumer demand, prompting rental rebates and shorter lease cycles in the Qatar retail market. The almost simultaneous debuts of Place Vendôme, Mall of Qatar, and Doha Festival City fragmented shopper traffic and diluted sales per square meter. Majid Al Futtaim’s 6% regional revenue dip and closure of eleven Carrefour branches underscore the stress large operators face when overlap is unchecked. Secondary malls lacking entertainment anchors resort to community-service tenancies—clinics, co-working hubs, and public-sector kiosks—to stay relevant. Retailers rationalize footprints by merging underperforming outlets into online-plus-showroom hybrids with dark-store backrooms. Developers accelerate mixed-use conversions, adding residential towers or hotel wings to diversify cash flow. Nevertheless, cannibalization pressure will linger until population growth and tourism arrivals fully absorb the expanded capacity in the Qatar retail market.

Import-Dependence & Supply-Chain Volatility

Imports cover 85% of merchandise volume, so freight shocks, exchange swings, and geopolitical chokepoints quickly feed into shelf prices across the Qatar retail market. Cold-chain gaps outside Doha limit same-day delivery for produce, pushing grocers to maintain higher inventory buffers that erode working capital. VAT’s phased rollout further complicates landed-cost calculations, forcing IT upgrades to integrate tax codes and reprice barcodes overnight. Smaller retailers with limited bargaining power cannot hedge freight surcharges effectively and face profit squeeze when promotional calendars clash with shipment delays. Currency-denominated luxury goods invite markdown risk if rial depreciation coincides with soft demand. Government food-security hothouses provide long-term relief but need years to scale, so supply-chain resilience—multi-sourcing, bonded warehousing, and AI risk alerts—becomes a survival imperative for the Qatar retail market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Resilience Amid Electronics Acceleration

Food, Beverage & Tobacco accounted for 42.02% of the Qatar retail market share in 2025, anchored by everyday demand and hospitality customs that drive high basket frequency. Electronic & Household Appliances is projected to grow 11.28% CAGR through 2031, lifted by the national AI roadmap and rising smart-home adoption, signaling category shift within the overall Qatar retail market size. Personal-care lines gain traction from sustainability labels and refill stations that answer 57% of shoppers’ eco preferences. Apparel and accessories ride luxury-tourism inflows, especially in mall flagships that curate capsule collections for regional festivals. Furniture purchases strengthen as five-year visas encourage expatriates to invest in permanent housing setups, benefiting mid-market Scandinavian and premium Italian ranges. Industrial and automotive lines lag because metro expansion and ride-hailing options offset car ownership urges. Across categories, VAT readiness pushes suppliers to renegotiate payment terms, compelling retailers to prioritize fast-turn stock to maintain healthy Qatar retail market economics.

Electronics chains cross-list groceries via marketplace tabs, while supermarkets stock branded earbuds and smart speakers at checkout lanes, blurring category lines in pursuit of wallet share. Food retailers foster partnerships with hydroponic farms to ensure same-day freshness claims that justify price premiums. Tobacco import controls now require pre-arrival notifications, so specialty tobacconists implement blockchain traceability to clear customs seamlessly. Beauty brands install AI skin-diagnosis kiosks that upsell nutritional supplements, tightening synergy with health-oriented groceries. Luxury fashion hosts resale corners to attract thrift-minded Gen Z expatriates, thereby prolonging product life cycles. Overall, product-level diversification underpinned by data insights keeps inventory nimble and shopper engagement high in the Qatar retail market.

By Retail Channel: Modern Trade Hegemony Meets Digital Momentum

Modern Trade captured 62.73% of the Qatar retail market size in 2025 because hypermarkets married bulk-buy savings with expansive imported assortments that appeal to large expatriate families. Digital platforms are racing at 17.95% CAGR thanks to 94% internet connectivity, low processing fees via NAPS, and duty-free last-mile logistics that make cross-border listings competitive. Neighborhood stores survive on proximity and cultural familiarity, stocking ethnic staples and offering informal credit lines during pay-cycle gaps. Marketplaces integrate groceries, electronics, and fashion in single-cart checkouts, using auto-translation to serve thirty languages. Qatar Airways Cargo’s Cainiao partnership promises two-day GCC delivery, expanding selection beyond what physical aisles can hold. Fintech-enabled request-to-pay tools improve collection rates for SMEs, opening doors for craft brands. Modern chains counter by converting some stores into dark warehouses for thirty-minute delivery slots, ensuring the Qatar retail market remains omnichannel at its core.

E-commerce firms experiment with mobile caravans—van showrooms that park near office blocks during lunch breaks—combining instant trials with QR-checkout for later doorstep delivery. Hypermarkets test live-stream flash sales from in-store studios, capturing impulse buys while clearing overstock. Mom-and-pop shops link WhatsApp catalogs to neighborhood cycling couriers, extending reach at minimal cost. Loyalty programs migrate to single-QR wallets that aggregate points across malls, fuel stations, and grocery chains, so shoppers bank rewards faster and stay within ecosystem spending loops. VAT software auto-formats digital invoices, easing returns across online and offline channels. Collectively, hybridization replaces binary channel thinking, confirming that the Qatar retail market thrives on fluid shopper journeys.

By Format: Hypermarket Scale Faces Convenience Agility

Hypermarkets retained 47.66% revenue share in 2025 by offering full-basket value bundles and family amenities that command weekend footfall. Convenience stores, forecast to grow 13.21% CAGR, ride urban densification and gig-worker snack demand, sprouting in metro exits and residential towers. Supermarkets occupy mid-tier positioning with curated fresh produce and deli counters that appeal to health-conscious families. Department stores rethink layouts toward hands-on workshops and consignment boutiques as monobrand labels accelerate direct-to-consumer moves. Specialty outlets within Place Vendôme showcase luxury watches with augmented-reality timepiece try-ons, drawing high-net-worth tourists. Cash-and-carry depots cater to hospitality, but B2B portals nibble share by aggregating bulk orders across restaurants. Convenience chains pilot 24-hour micro-markets in office lobbies with RFID entry, compressing checkout to near-instant and suiting Qatar’s diverse work schedules.

Hypermarkets downsize into compact urban formats branded “express” to reclaim weekday breakfast traffic and compete with corner stores. Convenience operators integrate parcel lockers, turning outlets into last-mile nodes that support e-commerce returns, thereby reducing logistics opacity in the Qatar retail market. Department stores sign drop-ship agreements with regional marketplaces to extend virtual aisles without risking inventory. Specialty players collaborate with hotel concierges for private shopping nights, boosting off-peak efficiency. Workforce localization rules push hypermarkets to automate stock-taking, freeing Qatari staff for higher-value service roles. The net result is a dynamic format portfolio where agility and technology increasingly trump square footage. .

Competitive Landscape

The Qatar retail market is moderately concentrated, with the top players holding a significant share in 2024. Among them, Lulu Group stands out as the market leader, leveraging its scale to drive efficiencies in procurement, logistics, and AI-driven analytics, further strengthening its competitive edge. Majid Al Futtaim, strained by regional headwinds, launched its HyperMax banner to reposition value messaging after Carrefour exits in Oman and Jordan, highlighting the need for localized brand strategies. Qatar Duty Free, bolstered by the national carrier’s tourist pipeline, diversifies into wellness-spa boutiques and Michelin-chef pop-ups, capturing incremental spend while flights rebound. Technology uptake differentiates winners: AI merchandising, computer-vision shelf scanners, and predictive maintenance on HVAC systems cut costs and lift service levels, helping chains defend share in the Qatar retail market. Workforce localization via Qatarisation Law No. 12 of 2024 increases payroll complexity, so large groups deploy learning-management systems to accelerate citizen upskilling and meet quota thresholds without service degradation.

Strategic partnerships shape the battlefield. Qatar Airways Cargo’s arrangement with Cainiao unlocks China-to-GCC express lanes, empowering e-commerce sellers to deliver within forty-eight hours, while Snoonu’s USD 320 million acquisition by Saudi’s Jahez signals cross-border consolidation in food delivery that bolsters digital order density. Hypermarket groups sign collaborative forecasting agreements with local hydroponic farms to secure priority harvest slots, enhancing fresh-food provenance. Convenience chains ink franchise deals with global C-store majors, seeking supply-chain synergies and brand equity. Specialty luxury operators negotiate shop-in-shop leases inside prestige hotels, capturing tourist impulse buys outside mall hours. Meanwhile, fintech start-ups embed installment options at POS terminals, attracting mid-income shoppers without compromising premium brand positioning, and in turn deepening competitive lines along payment-experience innovation.

Emerging disruptors exploit white spaces. Tech-native grocers offer thirty-minute delivery on 4,000 SKUs across Doha’s central districts, relying on micro-fulfillment nodes and AI-routed riders. Health-focused retailers curate imported keto, vegan, and gluten-free lines rarely stocked by mass chains, commanding price premiums buffered by affluent demographics. Outlet villages near border checkpoints aim to capture price-sensitive expatriates on weekend drives, creating a value counterpoint to flagship luxury malls. Department store operators plan resale corners and rental services to court eco-conscious Gen Z shoppers, differentiating from fast-fashion chains. Overall, competitive dynamics in the Qatar retail market revolve around scale, tech agility, and niche focus, with each axis offering a viable pathway to defend or win share over the forecast horizon.

Qatar Retail Industry Leaders

LuLu Group International

Carrefour Qatar (MAF Retail)

Al Meera Consumer Goods

Safari Group

Monoprix Qatar (Ali Bin Ali)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Lulu Retail reported preliminary FY 2024 results showing revenue growth of 4.7% to USD 7.6 billion and net profit increase of 12.6% to USD 216.2 million, while expanding its network by 21 new stores to reach 250 locations across the GCC.

- January 2025: Qatar Central Bank introduced the Request-to-Pay feature through its Fawran instant-payment service, enhancing transaction efficiency for retail operations.

- July 2024: Saudi Arabia’s Jahez acquired a majority stake in Qatar’s leading food-delivery platform Snoonu, valuing the company at USD 320 million.

- June 2024: Qatar Central Bank announced completion of infrastructure for its Central Bank Digital Currency project, entering an experimental phase through October 2024.

Qatar Retail Market Report Scope

A retail market involves selling goods or services directly to consumers for their consumption. The Qatar retail industry is segmented by products and distribution channels. By product, the market is segmented into food and beverages, personal and household care, apparel, footwear and accessories, furniture, toys and hobbies, electronic and household appliances, and other products. By distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, department stores, specialty stores, online, and other distribution channels). The report offers market size forecasts for the retail industry in Qatar in terms of value (USD) for all the above segments.

By Product Type

| Food, Beverage, and Tobacco Products |

| Personal Care and Household Care |

| Apparel, Footwear, and Accessories |

| Furniture, Toys, and Hobby |

| Industrial and Automotive |

| Electronic and Household Appliances |

| Other Products |

By Retail Channel

| Traditional Mom and Pop Retail |

| Modern Trade Retail |

| E-Commerce and Others |

By Format

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (Drugstore, Cash and Carry, Wholesaler) |

| By Product Type | Food, Beverage, and Tobacco Products |

| Personal Care and Household Care | |

| Apparel, Footwear, and Accessories | |

| Furniture, Toys, and Hobby | |

| Industrial and Automotive | |

| Electronic and Household Appliances | |

| Other Products | |

| By Retail Channel | Traditional Mom and Pop Retail |

| Modern Trade Retail | |

| E-Commerce and Others | |

| By Format | Hypermarkets |

| Supermarkets | |

| Convenience Stores | |

| Department Stores | |

| Specialty Stores | |

| Others (Drugstore, Cash and Carry, Wholesaler) |

Key Questions Answered in the Report

How large is the Qatar retail market in 2026 and how fast is it growing?

The Qatar retail market size is USD 19.44 billion in 2026 and is projected to advance at a 4.05% CAGR to reach USD 23.69 billion by 2031.

Which product segment is expanding the quickest?

Electronic & Household Appliances is forecast to grow at 11.28% CAGR through 2031, propelled by smart-home adoption and the government’s AI incentive program.

What retail channel shows the strongest growth outlook?

E-Commerce & Others is expected to post an 17.95% CAGR thanks to 94% internet penetration, duty-free logistics, and fintech-enabled instant payments.

Why is Doha Municipality dominant in retail sales?

Doha hosts mega-malls, corporate offices, and the country’s main airport, giving it 53.60% market share and sustained tourist and resident footfall.

How will upcoming VAT and global minimum tax rules affect retailers?

Both measures raise compliance requirements and heighten cost-visibility pressures, encouraging retailers to adopt digital tax-accounting systems and renegotiate supplier terms to protect margins.

Which store formats are gaining traction besides hypermarkets?

Convenience stores are set to grow 13.21% CAGR as urban density, 24-hour lifestyles, and AI-powered cashier-less technology encourage shoppers to favor quick-trip missions.

Page last updated on: