Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

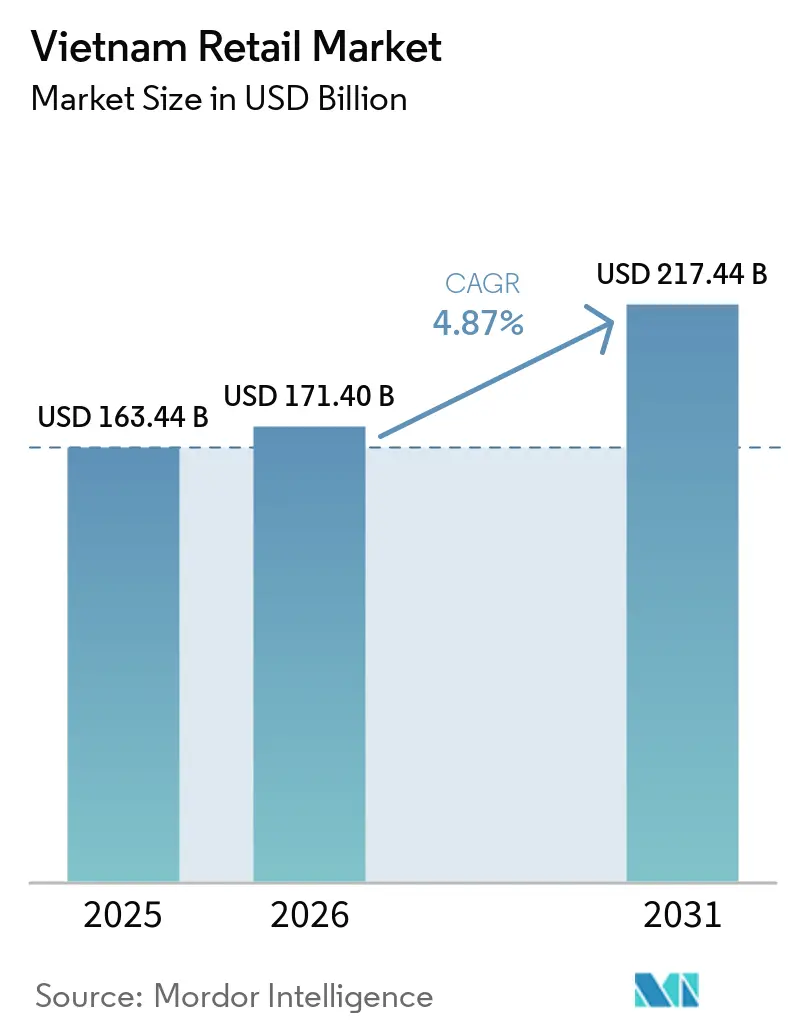

| Base Year Market Size (2025) | USD 163.44 Billion |

| Market Size (2026) | USD 171.40 Billion |

| Market Size (2031) | USD 217.44 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Retail Market Analysis by Mordor Intelligence

The Vietnam Retail Market size is projected to expand from USD 163.44 billion in 2025 and USD 171.40 billion in 2026 to USD 217.44 billion by 2031, registering a CAGR of 4.87% between 2026 to 2031.

Expansion in 2026 reflects a consolidation phase after the post-pandemic rebound and indicates that growth is shifting from volume to value as urban cores near saturation and as chains prioritize margin defense. Official policy direction targets faster growth through 2030, yet actual performance trails the ambition as retailers balance expansion with profitability and supply chain upgrades. Channel mix continues to evolve as social-commerce and hybrid models scale, while e-invoice enforcement supports digital payments and the formalization of small merchants. Format choices are moving toward convenience footprints that match dense urban living and quick-trip missions, and logistics investment is building the base for a larger fresh assortment and higher-quality execution.

Key Report Takeaways

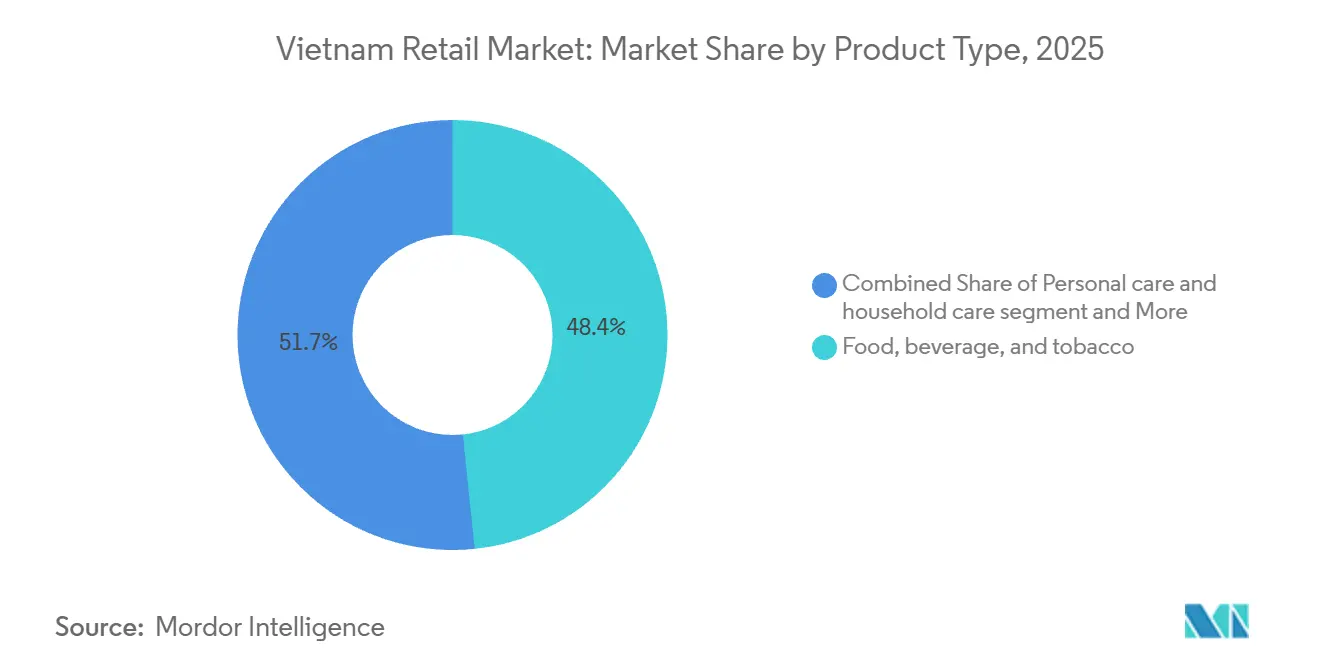

- By product type, Food, Beverage & Tobacco captured 48.35% of the Vietnam retail market share in 2025, while Personal Care & Household is projected to grow at a 6.46% CAGR through 2031.

- By retail channel, traditional mom-and-pop stores captured 59.35% of the Vietnam retail market share in 2025, while E-commerce and hybrid models recorded a 5.75% projected CAGR for 2026 to 2031.

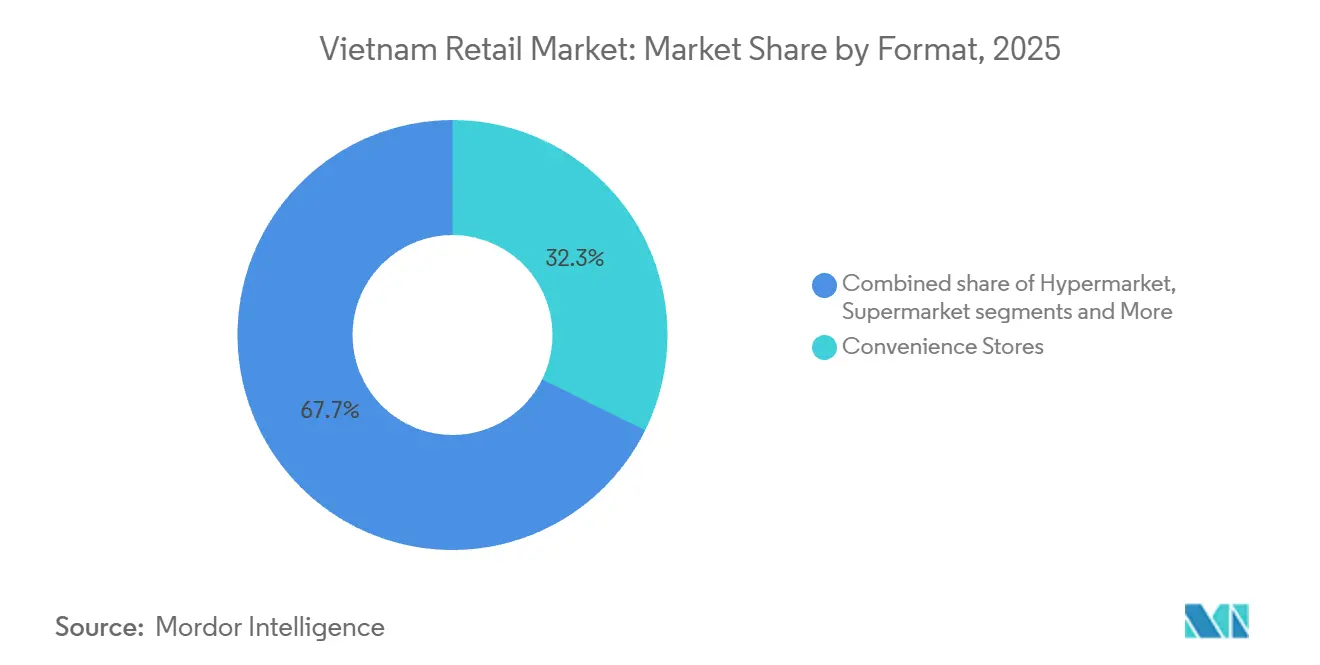

- By format, convenience stores commanded a 32.32% share in 2025 and are forecast to grow at a 6.35% CAGR through 2031, showing how proximity retail anchors the Vietnam retail market size and accelerates daily needs purchase occasions beyond supermarkets and hypermarkets.

- By geography, the Central and Central Highlands regions represented about one-fourth of the national retail value in 2025, and Mekong Delta provinces recorded significant retail sales growth in 2024, which frames the regional distribution of the Vietnam retail market size beyond the two major metros.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Retail Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of middle-class disposable income | +1.2% | National, concentrated in HCMC, Hanoi, Da Nang | Medium term (2-4 years) |

| Expanding urban grocery penetration beyond Tier-1 cities | +1.5% | Northern industrial belt, including Hai Phong and Quang Ninh, Mekong | Long term (≥ 4 years) |

| Acceleration of last-mile cold-chain logistics | +0.8% | National, with early gains in Long An, Dong Nai, and Can Tho | Medium term (2-4 years) |

| Mandatory e-invoice regime improving tax compliance | +0.6% | National, stronger enforcement in HCMC and Hanoi | Short term (≤ 2 years) |

| Growing uptake of social-commerce livestreaming | +0.9% | National, with Gen Z and Millennial strength in urban centers | Short term (≤ 2 years) |

| Cross-border “gray” imports eroding local assortment | +0.5% | Border provinces (Lang Son, Lao Cai), major urban markets including HCMC and Hanoi | Short to Medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

Rise of Middle-Class Disposable Income

Vietnam’s middle-income cohort widened in 2025, shifting spend toward packaged convenience foods, imported personal-care brands, and ready-to-eat solutions that carry premiums above traditional formats. This trend lifted own-label trajectories as retailers used private-label margins to counter rising rents and labor costs while keeping price points attractive to value-focused shoppers. The pattern is strongest in HCMC and Hanoi, where the threshold for modern retail adoption has moved downward and widened the base of households that frequent chain stores and malls. Discretionary categories like apparel and footwear captured more incremental wallet share while staple food spend moderated as households diversified consumption toward packaged and premium alternatives. Foreign mall operators capitalized by curating premium specialty zones at new flagship centers, with Lotte Mall West Lake Hanoi reporting high traffic and sales during its first 15 months, which drew international beauty and fashion brands to the capital’s retail stage.[1] KEDGLOBAL.COM https://www.kedglobal.com/retail/newsView/ked202509160001.

Expanding Urban Grocery Penetration Beyond Tier-1 Cities

Tier-2 and Tier-3 cities like Hai Phong, Quang Ninh, Can Tho, and Da Nang posted faster 2024 retail sales growth than HCMC, opening whitespace for modern grocery formats to scale networks beyond saturated metro cores. Mobile World’s Bach Hoa Xanh reached company-level profitability in 2024 and is targeting hundreds of new grocery stores focused on Central Vietnam as management aims to balance network density in the south with expansion into underpenetrated provinces. Improved transport links have cut travel times and logistics costs in the Mekong, lifting consumer access to larger-format outlets while giving suppliers better routing to distribution hubs. Central Retail’s project pipeline for new malls in Hung Yen and Yen Bai supports the push into the northern corridor that has seen faster retail growth tied to industrial expansion and worker inflows.[2]CENTRALRETAIL.COM https://www.centralretail.com/en/newsroom/news-and-activities/994/central-retail-posts-q1-2025-revenue-of-69280-million-baht-profit-of-2337-million-baht-gearing-up-for-bold-growth-across-local-and-global-markets. Pharmacy chains also validated the multi-format playbook in secondary cities as Long Chau scaled coverage across all provinces and used health services to drive recurring store traffic and cross-selling activity.

Acceleration of Last-Mile Cold-Chain Logistics

Cold-storage capacity and distribution build-out are critical to lift fresh mix and reduce waste, and a series of company investments since 2024 point to ongoing improvements across nodes near southern industrial zones. LOTTE Global Logistics began construction in Dong Nai on a dedicated cold facility slated to open in 2026, and Nichirei TBA Logistics launched a new cold store in Long An to serve food manufacturers, grocers, and food-service operators. Institutional investors also entered with long-tenor leases in cold storage, which signals confidence in demand from large 3PL customers and retail networks that plan to widen chilled and frozen assortments in fast-growing neighborhoods. As stores gain temperature-controlled capacity and routes improve, grocers can raise fresh category mix and reduce shrink, which supports margin and traffic despite rent inflation. Bach Hoa Xanh’s revenue per store improved in 2024 as assortment and in-store refrigeration upgrades supported higher ticket sizes, while third-party distribution partnerships extended reach into adjacent districts.[3]MWG.VN https://cdnv2.tgdd.vn/mwgvn/investorrelations/files/posts/2025/4/3099/bd/b4/bdb4909af7f69858abb538dac47b2e76.pdf. Seafood export and meat import trends before 2025 reinforced the need for temperature control across retail and food-service channels that are now growing in tandem with logistics investment.[4]MOIT.GOV.VN https://moit.gov.vn/en/news/latest-news/ministry-of-industry-and-trade-holds-regular-press-conference-for-q3-2025.html.

Mandatory E-Invoice Regime Improving Tax Compliance

The government enforced e-invoice integration to curb tax evasion and promote cashless payments, which pushed merchants to connect point-of-sale systems with the tax authority’s centralized platforms. This push helped accelerate cashless transactions to nearly 18 billion over the first nine months of 2025, while QR payments rose sharply on volume and value measures as consumers adopted mobile-first payment journeys.[5]VIETNAMPLUS.VNP Cross-border payments are not commensurate with market demand | Vietnam+ (VietnamPlus). Smaller merchants faced integration costs that encouraged exits or affiliation with franchise networks, and that dynamic supported gradual consolidation as modern trade widened its advantages in systems, data, and compliance. Internet and mobile transaction volumes scaled in 2025 alongside steady bank account penetration, which underpins omnichannel retail models even where cash-on-delivery remains common outside the major metros. The policy and enforcement cadence is faster in HCMC and Hanoi and is expected to move outward, linking tax compliance to digital receipts and inventory controls that raise transparency for all retail subsegments.

Restraints Impact Analysis*

| RESTRAINT | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High commercial-rent inflation in prime retail corridors | -0.4% | HCMC District 1, Hanoi Hoan Kiem and Ba Dinh, Da Nang city center | Short term (≤ 2 years) |

| Fragmented supply chain of fresh categories | -0.3% | National, acute in the Central Highlands and Mekong Delta | Medium term (2-4 years) |

| Persistent cash-on-delivery preference is slowing digital payments | -0.2% | Rural provinces in the Central and Northern regions | Medium term (2-4 years) |

| Limited nationwide data-analytics talent pool for modern retail | -0.1% | National, with gaps outside HCMC and Hanoi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Commercial-Rent Inflation in Prime Retail Corridors

Prime street-level retail rents in central districts of HCMC and Hanoi approached USD 150 per square meter per month by mid-2025, and that moved occupancy decisions toward smaller footprints and secondary streets where traffic is lower but occupancy costs are sustainable. This pressure compressed convenience chain margins and spurred network optimization and relocation decisions that reduced exposure to premium corridors in favor of multi-node coverage and dark-store fulfillment. Electronics retailers trimmed locations in 2024 when density and rent escalations reduced sales per square meter and placed pressure on store economics. Malls held relatively stable occupancy on average, yet street-facing stores faced higher tenant churn when lease renewals reset rents in line with tourist recovery and weekday office footfall. Operators responded by shifting growth to fulfillment-only sites and logistics-linked clusters in secondary cities where inbound demand supports 30-minute delivery in dense neighborhoods at a fraction of prime street rents.

Fragmented Supply Chain of Fresh Categories

Fresh produce flows through many intermediaries and traditional markets, which raises post-harvest losses and limits consistent quality on supermarket shelves. Cold chain remains a constraint relative to regional peers, and that forces dual sourcing from wet markets and contracted farms, which elevates procurement costs and shrinks. Provinces in the Mekong contribute a large share of fruit and vegetables but lack a full set of pack-houses, grading sites, and cross-dock capacity, which reduces saleable inventory and increases in-store culling. In the Central Highlands, multi-layered distribution adds days to lead times and reduces freshness on arrival, which impacts retailers who aim to scale private-label fresh offerings that depend on traceability and tighter temperature control. New collection center programs are planned and could trim intermediary layers if funding and timelines hold through delivery in 2027 and beyond.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Personal Care Outpaces Staple Food Growth

Food, beverage, and tobacco secured a 48.35% share in 2025 within the Vietnam retail market, while personal care and household care are tracking a 6.46% CAGR from 2026 to 2031 as imported skincare and premium detergents gain shelf space and command higher price points. This mix reflects how modern grocery, malls, and livestreaming are reinforcing premiumization while consumers maintain stable spending on staple categories. Electronics and appliances generated sizeable revenue through chain distribution in 2024, which underscores how households balance upgrades with basic food spending. Apparel and footwear captured a larger share of new wallet additions between 2024 and 2025 on the back of fast-fashion churn and online content that amplifies product discovery. Furniture and hobby categories saw slower growth as smaller urban dwellings and shorter replacement cycles constrained ticket sizes, while a delayed international entry kept local assemblers and online platforms in the lead.

The category mix is evolving from a 2020 baseline toward higher-value packaged foods and dairy as cold storage and transport improve and as retailers push chilled ready meals and imported SKUs into convenience footprints. Personal care leaders worked with platforms to capture growth during mega-sales periods, which produced outsized gains and showed that video-first merchandising accelerates conversion for beauty brands. Private-label penetration at cooperatives and chain grocers rose in 2024 as a subset of shoppers traded down to high-quality equivalents priced below branded rivals, and that deepened as loyalty programs and store membership nudged repeat purchase. Pharmacy chains added health services that drove basket expansion into health-adjacent items like supplements and personal care, and that widened the halo effect for convenience and grocery retail. These shifts illustrate how the Vietnam retail market combines stable staples with faster premiumization in health and beauty segments that build unit economics beyond base categories.

By Retail Channel: E-Commerce Erodes Traditional Dominance

Traditional mom-and-pop outlets held 59.35% in 2025, and e-commerce and hybrid channels are set to grow at 5.75% CAGR from 2026 to 2031, which shows the Vietnam retail market size is pivoting toward digital formats while long-tail street retail remains prominent in rural and peri-urban areas. Modern trade expanded its share by adding convenience boxes and full-service supermarkets that backfill assortment and payment options not available in informal channels. Platform ecosystems reported strong 2024 gains in value and volumes as millions of SKUs were listed and cross-border sellers entered through gray-import pathways that challenge tax compliance. Policy responses in 2025 aimed to tighten accountability across platforms and sellers, while definitions and enforcement mechanisms for livestream content and identification are still developing. The overall shape of channel shift depends on how quickly payments and logistics spread beyond metro cores and how regulation closes reporting gaps.

The traditional channel saw an absolute sales dip in 2024 as shoppers moved to chains with consistent pricing and integrated payments that reduce friction at checkout. Informal traders still hold structural advantages in fresh categories where tactile inspection matters, particularly in wet-market-anchored neighborhoods of the Mekong, where income gains fed higher purchase rates through 2024. E-commerce penetration is lower than in some regional markets due to cash-on-delivery preferences and rural delivery costs that lift the share of logistics in order value compared with urban hubs. Livestream selling posted conversion rates far above conventional online browsing and attracted a third of consumers in 2025 into event-style promotions, which prompted retailers to invest in content and community features. Platform share dynamics shifted as TikTok Shop’s push compelled rivals to subsidize fees and strengthen influencer programs to hold GMV share while they manage unit economics in a more promotional environment.

By Format: Convenience Stores Dominate Proximity-Driven Demand

Convenience stores held 32.32% format share in 2025 and are projected to expand at a 6.35% CAGR through 2031, and this supports the retail industry in Vietnam as consumers favor 24-hour access and small-basket missions near home and work. Store rollout plans from Circle K, 7-Eleven, and GS25 target hundreds of new locations by 2026 with a focus on emerging districts in Hanoi and expansion corridors on the edges of HCMC where rent levels match quick-service economics. Pharmacy-led convenience added health services and impulse categories that lifted tickets and increased frequency, while chains invested in omnichannel tools that integrated pickup and delivery into small boxes. Minimart grocery returned to profitability at a major chain in 2024 thanks to a rebuilt assortment across fresh and prepared foods supported by better in-store refrigeration and a refreshed pricing and promotion model. This combination continues to pull quick trips away from hypermarkets and larger supermarkets that depend on weekend traffic and bulk baskets.

Supermarket count increased into early 2026, while like-for-like sales gains were modest due to overlap with convenience formats and e-commerce on baskets under USD 7.6. Mini formats under national chains logged stronger like-for-like growth in rural and blended urban models when unlocked by loyalty platforms that reached a large share of households. Hypermarkets faced structural headwinds as destination shopping softened in 2024 and consumers opted for frequent small runs and app-based grocery options, and that dynamic pushed operators to test new layouts and tenant mixes. Department store and mall operators maintained stable occupancy while rotating toward entertainment, food service, and beauty services to drive visits and dwell time as soft-line retail sales contracted. Specialty retailers in electronics, sports, pharmacy, and mother-and-baby maintained defensible positions through category depth, consultative selling, and extended services that are less exposed to price-only online competition.

Geography Analysis

HCMC posted 5.2% retail sales growth in 2024, which was the slowest among the main metros, and that aligns with higher modern-trade penetration and premium street rents that squeeze small-box economics in the core and shift expansion to surrounding districts. Quang Ninh and Hai Phong recorded 9.7% and 9.6% growth, and planned mall openings in Hung Yen and Yen Bai are positioned to capture similar northern corridor demand as logistics and industry add jobs. Hanoi reported USD 23.42 billion in retail and consumer service revenue for the first eight months of 2025 and recorded double-digit growth that was helped by domestic travel and events recovery, which supported mall traffic and specialty category sales. Lotte Mall West Lake drew strong cumulative visitors and sales during its first 15 months in the capital and used premium beauty zones to attract higher-spending cohorts. These relative growth differences confirm how the retail market in Vietnam spreads beyond the two largest cities, as capital and store investments move up the northern coast and into central hubs.

Mekong Delta provinces together achieved 14.4% retail sales growth in 2024, which outpaced the national average during the same period, and that reflects agricultural income gains and transport upgrades that cut logistics costs on key connectors. Ben Tre reached USD 2.69 billion in retail sales in 2024 and faced elevated spoilage in leafy greens, which spotlighted the gaps in cold storage and upstream sorting. Central and Central Highlands accounted for roughly 24% of the national retail value in 2025 based on regional data and local reporting on market structure, and that share indicates the Vietnam retail market share is distributed beyond the largest two urban centers. Da Nang and Can Tho posted robust 2025 growth in the first three quarters that came from tourism recovery, service sector hiring, and steady logistics investment that supported regional distribution. These inter-regional patterns also show how rent and talent remain more manageable outside core CBDs, which helps chains lift store counts without compressing unit economics.

Growth decelerated in HCMC relative to 2023 while Hanoi accelerated, and that points to the effect of public infrastructure, income dynamics, and office-centered footfall in reshaping retail demand. Policy targets from the National Retail Market Development Strategy set a national growth path that depends on channel formalization, small merchant digital integration, and new corridors that connect inland provinces to coastal trade nodes. Execution on wholesale market upgrades, cold chain subsidies, and e-commerce compliance will influence the regional distribution of store formats and omnichannel fulfillment density. The Vietnam retail market size will be shaped by how these investments align with private capital, particularly in Tier-2 and Tier-3 cities that are drawing a rising share of store openings and mall developments. The interplay of regional wage growth, logistics nodes, and urbanization speed will define store network rollouts and delivery radii over the forecast period.

Competitive Landscape

The Vietnam retail market is fragmented, with the top five players holding about one-fifth of total value, which leaves most share with traditional markets and independent retailers that serve dense neighborhoods across provinces. Competition intensified as domestic groups scaled omnichannel features, loyalty programs, and private-label architectures that lift margin and stickiness despite rising occupancy and operating costs. Mobile World delivered USD 5.09 billion revenue in 2024 from a 5,292-store ecosystem across electronics, grocery, pharmacy, and mother-and-baby, and the company reached leadership through dense coverage, store productivity, and growing online sales contribution. Masan’s WinCommerce returned to profitability in 2024 with USD 1.25 billion revenue from a broad footprint and used WiN membership to drive a majority of sales through targeted promotions and financial service adjacencies. These moves align with how the retail industry in Vietnam is building stronger engines for scale in data, payments, and supply partnerships that can reach beyond megacities.

White space remains in Tier-2 city omnichannel grocery, where dark-store economics beat prime street rents and enable fast delivery that matches consumer expectations built on social-commerce experiences. Private-label offers room for margin expansion in fresh and chilled categories once cold chain coverage rises and farm-to-store contracts scale across regions. Social-commerce platforms disrupted customer acquisition costs and conversion funnels in 2025 and forced leading e-commerce incumbents to defend share with fee subsidies and influencer commitments even as take rates tightened. AEON’s specialty store portfolio in Vietnam grew sharply in FY2024, and the firm outlined a path to expand the mall network toward 2030 with a large capital plan, while Lotte accelerated premium mall positioning with West Lake in Hanoi and signaled plans for more complexes in major cities. These strategies indicate how international players view the Vietnam retail market as a long runway for experiential formats and premium assortments that complement convenience-led networks.

Central Retail announced investment plans through 2026 to scale food and non-food coverage and to expand mall and supermarket brands toward a near-nationwide footprint by 2026, which will intensify competition in Central and northern provinces. Vincom Retail reported improved occupancy at its malls in 2024 and strong financial results, which support tenant mix rebalancing toward categories that drive repeat visits and food and entertainment anchors. Saigon Co.op reported higher online contributions in 2024 and set new targets for e-commerce in 2025, while also expanding its store network with new locations that tap suburban and provincial demand. The retail market in Vietnam continues to reward operators that integrate offline and online, use data to refine assortment and promotions, and invest in logistics that reduce shrinkage and increase fresh depth. Execution on these elements will define which portfolios sustain double-digit growth in select categories while the long tail of small retailers adapts to regulatory and cost pressures.

Vietnam Retail Industry Leaders

Masan Group (WinCommerce/WinMart)

Saigon Co.op

Mobile World Investment Corp. (The Gioi Di Dong, Dien May Xanh, Bach Hoa Xanh)

AEON Vietnam

Central Retail Vietnam (GO!/Big C)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Vietnam's National Assembly approved Decision No. 2326/QD-TTg establishing the National Retail Market Development Strategy, targeting 11-11.5% annual growth in total retail sales through 2030 alongside 15-20% e-commerce growth, with policy support for SME digital integration and logistics infrastructure.

- September 2025: Lotte Shopping Co. has announced plans to open two to three additional premium shopping malls in major Vietnamese cities by 2030, building on the success of its flagship Lotte Mall West Lake Hanoi. The expansion is part of the company’s broader strategy to strengthen its overseas retail presence and drive growth in Southeast Asia.

- July 2025: Deputy Prime Minister Ho Duc Phoc issued Official Dispatch 124/CD-TTg mandating enforcement of e-invoice and non-cash transactions to prevent tax evasion, accelerating QR-code payment adoption, which recorded 61.6% volume growth and 150.7% value growth year-over-year in the first nine months of 2025.

- May 2025: Central Retail Vietnam announced a USD 258.7 million investment for food and non-food expansion through 2026, targeting 57 provinces with 6-8 new GO! hypermarkets and malls, 10-12 mini-Go! stores, and 10-15 Tops Market supermarkets to reach USD 1.52 billion in revenue.

Vietnam Retail Market Report Scope

Retail is the process of selling consumer goods or services to customers through multiple channels of distribution to earn a profit. A complete background analysis of the Vietnam Retail Market includes an assessment of the emerging trends by segments, significant changes in market dynamics, and a market overview.

The Vietnam Retail Market Report is Segmented by Product Type (Food, Beverage, and Tobacco; Personal Care and Household Care; Apparel, Footwear, and Accessories; Furniture, Toys, and Hobby; Industrial and Automotive; Electronic and Household Appliances; Other Products), Retail Channel (Traditional Mom and Pop; Modern Trade; E-Commerce and Others), and by Format (Hypermarkets; Supermarkets; Convenience Stores; Department Stores; Specialty Stores; Others).

By Product Type

| Food, Beverage, and Tobacco Products |

| Personal Care and Household Care |

| Apparel, Footwear, and Accessories |

| Furniture, Toys, and Hobby |

| Industrial and Automotive |

| Electronic and Household Appliances |

| Other Products |

By Retail Channel

| Traditional Mom and Pop Retail |

| Modern Trade Retail |

| E-Commerce and Others |

By Format

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (drugstore, cash & carry, wholesaler) |

| By Product Type | Food, Beverage, and Tobacco Products |

| Personal Care and Household Care | |

| Apparel, Footwear, and Accessories | |

| Furniture, Toys, and Hobby | |

| Industrial and Automotive | |

| Electronic and Household Appliances | |

| Other Products | |

| By Retail Channel | Traditional Mom and Pop Retail |

| Modern Trade Retail | |

| E-Commerce and Others | |

| By Format | Hypermarkets |

| Supermarkets | |

| Convenience Stores | |

| Department Stores | |

| Specialty Stores | |

| Others (drugstore, cash & carry, wholesaler) |

Key Questions Answered in the Report

What is the Vietnam retail market size and growth outlook to 2031?

The Vietnam retail market size is USD 171.40 billion in 2026 and is projected to reach USD 217.44 billion by 2031 at a 4.87% CAGR.

Which product categories are leading and which are growing fastest in Vietnam retail ?

Food, beverage, and tobacco led with 48.35% share in 2025, while personal care and household care is the fastest growing at 14.36% CAGR for 2026 to 2031.

How is the channel mix shifting in the Vietnam retail market?

Traditional outlets held 59.35% of sales in 2025, while e-commerce and hybrid models are set to grow at 20.29% CAGR in 2026 to 2031 as social-commerce livestreaming lifts conversion.

Which format is expanding fastest in Vietnam retail?

Convenience stores held 32.32% share in 2025 and is forecast to grow at 16.35% CAGR through 2031, outpacing supermarkets and hypermarkets.

Which companies are making notable strategic moves in the Vietnam retail?

Mobile World and Masan’s WinCommerce reported 2024 profitability improvements and footprint scale, AEON outlined plans to expand its mall network toward 2030, and Central Retail committed new capital for expansion through 2026.

Page last updated on: