Medical Ventilator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 4.33 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

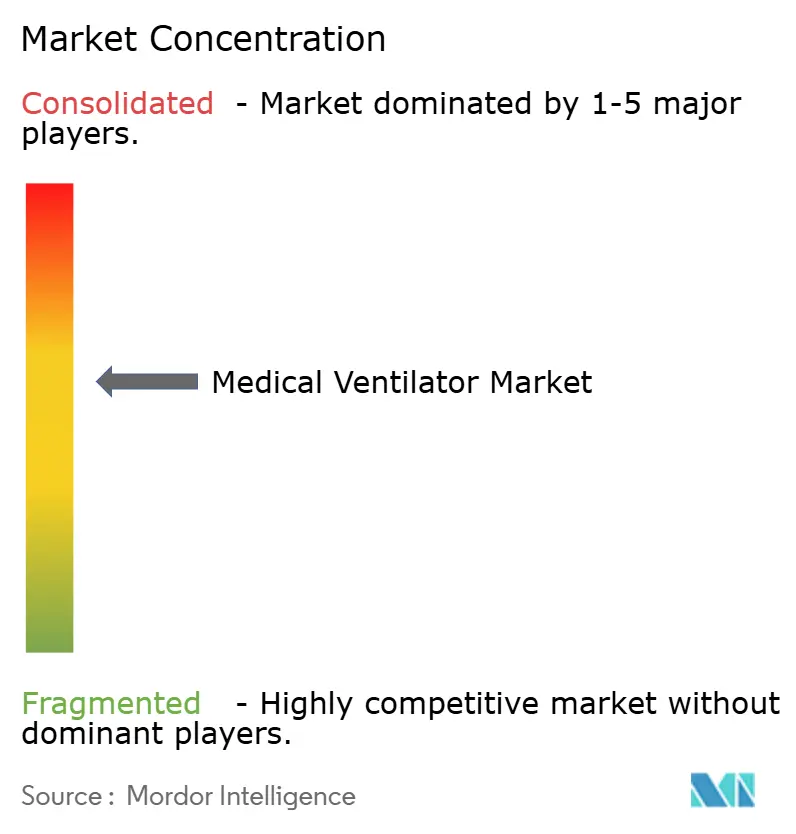

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Ventilator Market Analysis by Mordor Intelligence

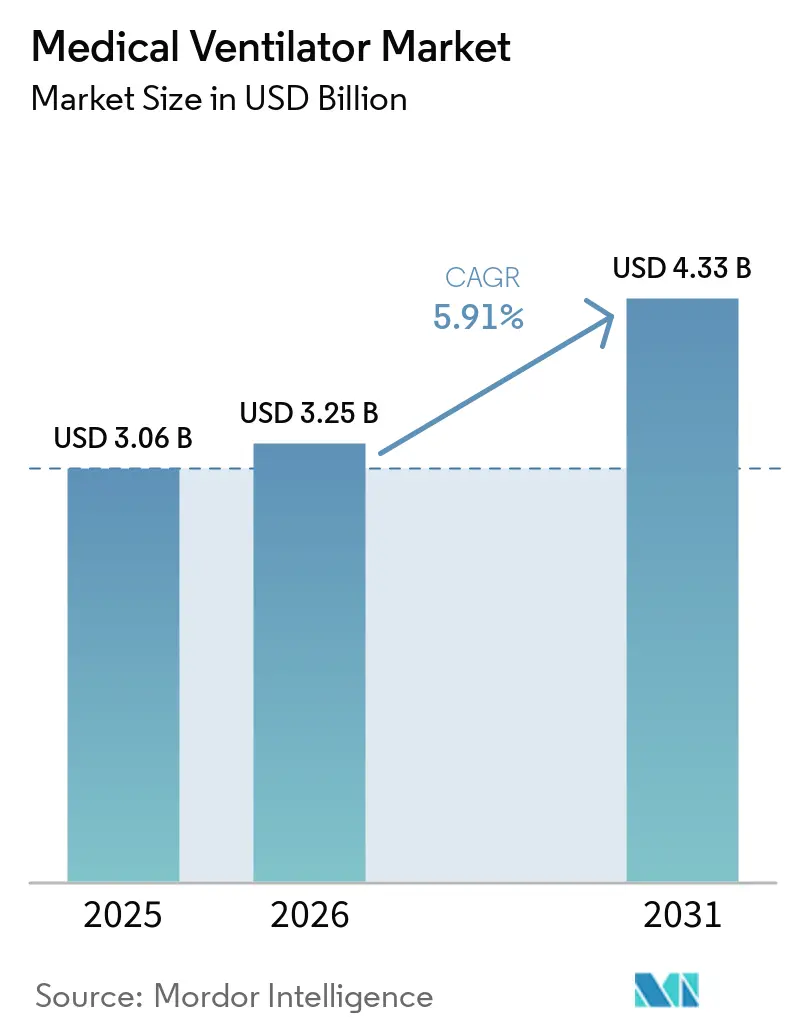

The Medical Ventilator Market size is expected to increase from USD 3.06 billion in 2025 to USD 3.25 billion in 2026 and reach USD 4.33 billion by 2031, growing at a CAGR of 5.91% over 2026-2031.

The core demand base for the medical ventilator market remains tied to the significant global burden of chronic respiratory diseases, with 569.2 million cases recorded in 2025. A joint WHO and European Respiratory Society assessment also projected a 23% rise in COPD cases globally between 2020 and 2050, with a sharper impact on women and low- and middle-income countries, reinforcing a stable and long-term demand for ventilatory support.[1]GBD 2023 Chronic Respiratory Disease Collaborators, “Global, Regional, and National Burden of Chronic Respiratory Diseases and Impact of the COVID-19 Pandemic, 1990–2023, A Global Burden of Disease Study,” Nature Medicine, The medical ventilator market is transitioning from emergency-driven purchases to structured investments in chronic care, ICU modernization, and home respiratory management. Vendors are focusing on software intelligence, connected monitoring, and service-led models to meet providers' needs for improved clinical performance, streamlined workflows, and predictable costs. This shift is driving growth opportunities in both premium hospital systems and cost-effective portable and home-use devices as care delivery becomes more decentralized.

Key Report Takeaways

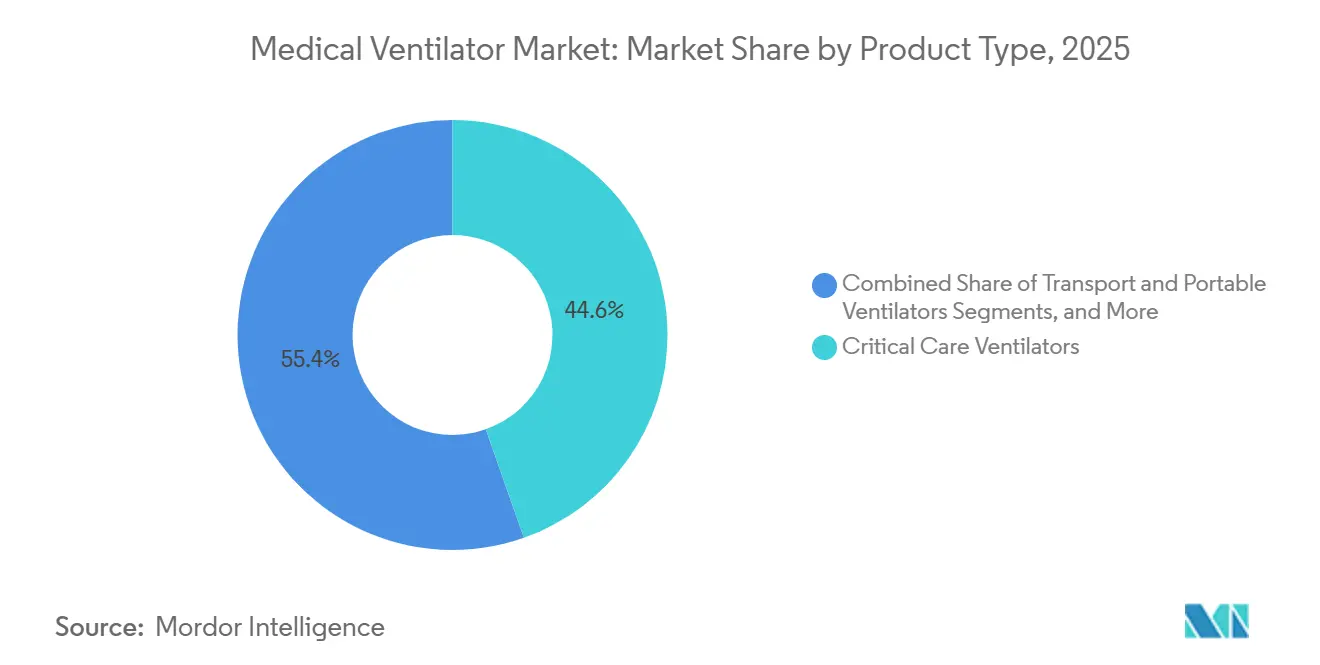

- By product type, critical care ventilators held 44.58% of the medical ventilator market share in 2025, while transport and portable ventilators recorded the fastest projected growth at a 6.72% CAGR through 2031.

- By interface, invasive ventilation accounted for 64.88% of the medical ventilator market size in 2025, while non-invasive ventilation is projected to expand at a 6.45% CAGR during 2026 to 2031.

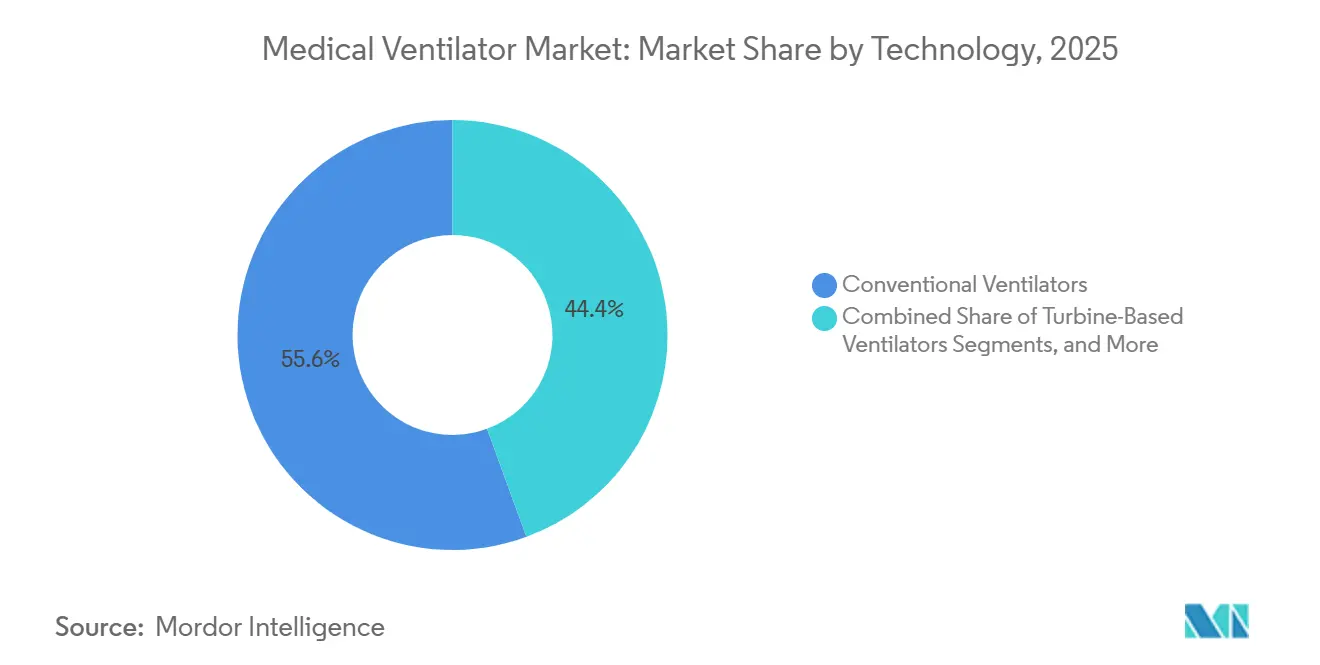

- By technology, conventional ventilators led with 55.6% share in 2025, while intelligent and closed-loop ventilators posted the highest expected CAGR at 7.12% through 2031.

- By end user, hospitals represented 65.7% of demand in 2025, while home care settings are projected to grow fastest at a 7.45% CAGR over 2026 to 2031.

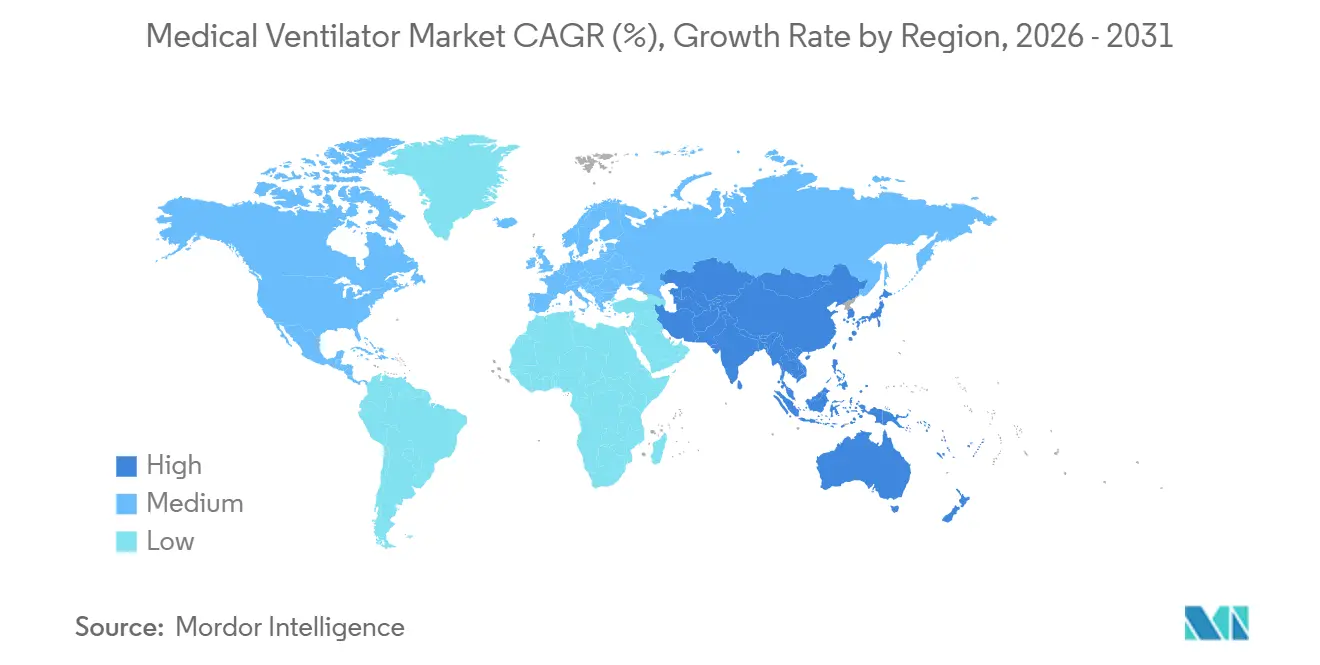

- By geography, North America captured 38.99% share in 2025, while Asia-Pacific is expected to advance at the fastest regional CAGR of 8.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Ventilator Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of chronic respiratory diseases | +1.5% | Global, highest incidence in South and East Asia and in low and middle income countries | Long term (≥ 4 years) |

| Aging population requiring assisted ventilation | +1.0% | North America, Europe, Japan, Australia, with rising relevance in China | Medium term (2-4 years) |

| Expansion of home-based non-invasive ventilation | +0.9% | North America, Europe, and developed Asia-Pacific | Medium term (2-4 years) |

| Replacement demand for connected and smart ventilators | +0.7% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Need for supply chain localization in critical care equipment | +1.0% | North America, Europe, Japan, Australia, with rising relevance in China | Medium term (2-4 years) |

| Risk-adjusted procurement favoring multi-mode ventilation platforms | +0.8% | North America, Europe, and developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden Of Chronic Respiratory Diseases

Chronic respiratory diseases, particularly COPD and acute respiratory distress cases, are the primary drivers of demand in the medical ventilator market. In 2025, the Global Burden of Disease Study highlighted 569.2 million cases of chronic respiratory diseases globally, underscoring the vast treatment pool in both advanced and developing health systems.[2]World Health Organization Regional Office for South-East Asia, “Chronic Respiratory Diseases in South-East Asia, Burden, Risk Factors and Services for Prevention and Management 2025,” World Health Organization The WHO pointed out that chronic respiratory diseases pose a significant mortality challenge in South-East Asia, linking ventilation demand to routine care rather than just emergencies. Furthermore, the WHO and ERS highlighted that Europe underdiagnoses chronic respiratory diseases, with COPD responsible for 80% of related deaths. This suggests a substantial future demand not yet reflected in current procurement trends. As screening and diagnosis improve in middle-income countries, there's a potential shift from a hidden demand to active purchasing in the medical ventilator market, particularly in the Asia-Pacific region.

Aging Population Requiring Assisted Ventilation

Older adults, who frequently face challenges like COPD and post-surgical respiratory failures, are a significant demographic driving the medical ventilator market. The WHO, in October 2024, projected that by mid-century, 80% of the world's elderly population will reside in developing nations. This trend indicates a growing care burden in regions still enhancing their respiratory care capabilities.[3]World Health Organization Regional Office for South-East Asia, “Chronic Respiratory Diseases in South-East Asia, Burden, Risk Factors and Services for Prevention and Management 2025,” World Health Organization Given their weaker respiratory muscles and multiple health challenges, older patients often experience prolonged ventilator use in hospitals. This extended usage can slow ICU bed turnover, prompting healthcare providers to seek devices that facilitate both immediate stabilization and a smoother recovery. Moreover, a significant number of elderly patients require continued respiratory support post-discharge, bolstering the demand for home respiratory assistance.

Expansion Of Home-Based Non-Invasive Ventilation

Home-based care is transforming the medical ventilator landscape, shifting respiratory management from costly institutions to more affordable home settings for stable chronic patients. A pivotal moment occurred in 2025 when CMS approved home noninvasive positive pressure ventilation for COPD-related chronic respiratory failure, with reimbursements starting later that year. This move alleviated reimbursement uncertainties, encouraging providers to invest in home ventilation capabilities. A 2026 cost-utility analysis indicated that home mechanical ventilation for qualifying COPD patients could reduce long-term institutional care costs, further piquing payer interest in this model. While operational risks persist, especially concerning documentation quality and provider margins, the medical ventilator market stands to gain as reimbursement, cost management, and patient preferences increasingly favor home-based non-invasive support.

Replacement Demand For Connected And Smart Ventilators

Replacement demand is emerging as a significant growth driver in the medical ventilator market, with hospitals increasingly upgrading to advanced ventilators for their software capabilities rather than waiting for hardware malfunctions. A clinical trial with 1,514 patients demonstrated that automated closed-loop ventilation outperformed conventional methods in reducing severe hypercapnia and hypoxemia events, bolstering the case for next-gen systems. Another study in 2025 highlighted Hamilton Medical’s INTELLiVENT-ASV, which not only minimized manual nursing interventions but also garnered better acceptance from nurses compared to traditional methods, a crucial factor in understaffed ICU settings.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High total cost of ownership and service burden | -1.0% | Global, strongest in low and middle income countries and in cost-sensitive public systems | Medium term (2-4 years) |

| Reimbursement pressure on long-term home ventilation | -0.8% | North America, Europe, and developed Asia-Pacific | Medium term (2-4 years) |

| Regulatory recertification and compliance delays | -0.9% | Global, strongest in low and middle income countries and in cost-sensitive public systems | Medium term (2-4 years) |

| Under-reporting of ventilator demand outside large hospital networks | -0.5% | North America, Europe, and developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost Of Ownership And Service Burden

The medical ventilator market faces significant cost challenges, as ownership involves more than just the purchase price. High-acuity critical care systems cost between USD 5,000 and over USD 50,000 per unit, with additional expenses for calibration, consumables, servicing, software updates, and repairs. Public hospitals and resource-limited systems, operating under tight budgets, find these costs difficult to manage. Rapid technology advancements make older units appear outdated before their hardware lifecycle ends, pushing buyers toward rental models and bundled service contracts. While these models aid adoption, they delay one-time hardware revenue realization in the market.

Reimbursement Pressure On Long-Term Home Ventilation

Adoption of medical ventilators in home care remains slow due to reimbursement policies that fail to address the complexities of long-term respiratory support. A U.S. OIG audit in August 2024 identified USD 79.4 million in improper inpatient mechanical ventilation payments over six years, primarily due to coding errors and insufficient documentation, leading to increased payer scrutiny. Despite the CMS coverage expansion for home NIPPV in June 2025, providers face higher documentation requirements and operational costs without proportional payment increases. This limits the scalability of durable medical equipment providers, even with growing clinical demand. Readmission risks post-discharge also persist, as adherence and follow-up in home settings are often inadequately managed. Payment systems must consistently reward outcomes and monitoring to unlock the full growth potential of this segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Critical Care Leads While Portable Devices Expand Faster

In 2025, critical care ventilators held a 44.58% share of the medical ventilator market, driven by their essential role in ICU admissions requiring high-acuity and complex ventilation. These ventilators are critical for invasive ventilation, perioperative care, and prolonged respiratory support, where reliability and multi-mode capabilities are vital. Hospitals prioritize these systems in capital planning due to their importance in critical care readiness and emergency response, ensuring a strong installed base despite selective procurement trends. This category remains indispensable in tertiary care settings.

Transport and portable ventilators are the fastest-growing segment, with a projected 6.72% CAGR from 2026 to 2031. This growth reflects the industry's shift toward mobility, distributed care, and uninterrupted respiratory support across locations. Demand is rising for battery-efficient turbine systems capable of maintaining stable performance during emergency transport, military operations, and intrahospital transfers. Clinical advancements in adaptive minute ventilation further enhance the role of portable devices, positioning them as a significant segment in the medical ventilator market.

By Interface: Non-Invasive Ventilation Builds Broader Use Cases

In 2025, invasive ventilation accounted for 64.88% of the medical ventilator market, underscoring its critical role in ICU care, emergency stabilization, and post-surgical respiratory management. Endotracheal intubation and tracheostomy-based support remain essential for patients unable to maintain ventilation or airway protection, keeping invasive systems central to hospital purchasing and clinical workflows. This segment continues to dominate despite the growing adoption of non-invasive care.

Non-invasive ventilation is the fastest-growing interface segment, with a 6.45% CAGR expected from 2026 to 2031. Its growth stems from expanding applications in acute care, post-surgical recovery, and long-term COPD management. Evolving care standards and next-generation features enhancing clinical usability are driving broader adoption. Combined with expanded home reimbursement policies, non-invasive support is poised for significant growth in the medical ventilator market.

By Technology: Conventional Systems Remain Largest While Intelligent Platforms Gain Ground

Conventional ventilators retained a 55.6% market share in 2025, supported by a large installed base and cost-conscious procurement in mid-tier hospitals. These systems remain widely used due to their familiarity, clinical acceptance, and affordability, particularly in emerging economies. However, their dominance is gradually being challenged by the growing adoption of intelligent platforms.

Intelligent and closed-loop ventilators are the fastest-growing technology segment, with a 7.12% CAGR projected from 2026 to 2031. Software-led differentiation and evidence of improved clinical outcomes are driving this growth. Studies highlighting reduced manual interventions and better workflow efficiency are encouraging hospitals to transition to intelligent fleets, particularly in academic and organized procurement settings.

By End User: Hospitals Dominate While Home Care Advances Faster

Hospitals represented 65.7% of end-user demand in 2025, maintaining their central role in the medical ventilator market. They cater to diverse use cases, including ICU, emergency response, and neonatal support, resulting in the largest installed base and highest purchasing volumes. Hospitals also influence technology adoption by setting standards for clinical integration and service contracts.

Home care settings are projected to grow at a 7.45% CAGR from 2026 to 2031, reflecting a shift toward managing chronic respiratory conditions outside hospitals. Regulatory changes in 2025 stabilized reimbursement for home NIPPV in COPD patients, encouraging provider investments. Vendors offering comprehensive solutions, including patient follow-up and monitoring, are well-positioned to capture growth in this segment of the medical ventilator market.

Geography Analysis

In 2025, North America held 38.99% of the medical ventilator market share, driven by a strong ICU infrastructure, established reimbursement systems, and rapid adoption of software-integrated ventilation platforms. The U.S. leads demand as hospitals upgrade to advanced critical care systems, supported by the June 2025 CMS decision expanding home non-invasive support beyond acute settings. This creates a balanced demand mix across high-acuity hospital care and post-discharge respiratory management. Canada and Mexico also contribute to growth through infrastructure investments and fleet upgrades. However, administrative challenges, such as documentation quality and billing discipline, remain barriers to smoother reimbursement processes.

Europe, a mature yet evolving market, is expected to add over USD 430 million in value between 2026 and 2031. Germany anchors the market with a strong manufacturing base and steady hospital replacement demand. Dräger reported record net sales of EUR 3 billion in fiscal 2025, with its medical division order intake growing 8.9% to EUR 2,046.6 million (approximately USD 2.21 billion). Stricter EU device regulations are increasing compliance and post-market surveillance costs, pressuring smaller manufacturers. Fisher & Paykel Healthcare demonstrated growth in recurring revenue, with FY2026 hospital product group revenue reaching NZD 1.51 billion (approximately USD 906 million), up 18% year over year.

Asia-Pacific is the fastest-growing region in the medical ventilator market, with an 8.12% CAGR projected from 2026 to 2031. Growth is fueled by government-led ICU expansions, aging populations, and a stronger domestic manufacturing base in countries like China and India. In 2025, China’s public hospitals procured 17,448 ventilators worth CNY 2.65 billion (approximately USD 365 million), with Mindray Bio-Medical holding a 40.74% value share, followed by Dräger at 15.62% and KOMAN at 12.43%. These top three brands controlled 68.79% of the domestic public procurement market. China’s 15th Five-Year Plan in 2026 supports domestic high-end medical equipment development, intensifying local competition. India and Indonesia also drive growth through local manufacturing partnerships and increased in-country value addition.

Competitive Landscape

The medical ventilator market is moderately consolidated, with a core group of manufacturers, including Dräger, Hamilton Medical, Getinge, GE HealthCare, Mindray, Fisher & Paykel Healthcare, and ResMed. These companies compete across critical care, transport, home care, and respiratory support ecosystems rather than focusing solely on standalone ventilator hardware. Competition has shifted from hardware specifications to software intelligence, usability, and workflow impact. Hospitals now emphasize clinical validation in tenders, seeking evidence that smart platforms can improve outcomes or reduce staff workload. As a result, features like embedded algorithms, alarm reduction, synchrony support, and data connectivity have become critical differentiators in the medical ventilator market.

Recent strategic moves highlight how vendors are repositioning themselves. In June 2025, Getinge expanded its Servo-c ventilator with a neonatal option, enabling one platform to support premature newborns from 500 grams to adults, helping hospitals reduce fleet complexity. ZOLL Medical enhanced its respiratory portfolio by acquiring selected Vyaire ventilator product lines in October 2024, gaining scale in portable, neonatal, and high-frequency oscillation categories. Mindray introduced a next-generation ventilation solution at ESICM 2025, focusing on bridging the gap between diagnosis and outcome, reinforcing its position in advanced critical care. These developments indicate that the market increasingly rewards platform breadth, software depth, and category adjacency.

Price-performance pressure is rising as regional manufacturing and domestic tendering gain importance. In Asia-Pacific, local assembly, domestic sourcing, and national procurement priorities are shaping brand scalability. Vendors relying solely on premium pricing face challenges unless they demonstrate superior clinical value or service performance. In North America and Europe, replacement demand favors companies with a large installed base and a strong digital roadmap. The market dynamics show that premium hospital systems, value-conscious public tenders, and home care channels reward different strengths. Companies offering connected platforms, robust service support, and efficient manufacturing are better positioned to maintain market share.

Medical Ventilator Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

Getinge AB

Drägerwerk AG and Co. KGaA

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mindray Bio-Medical guided international business to return to rapid growth in 2026, identifying emerging markets and Europe as lead growth engines. Mindray also confirmed that the SV900 and SV700 critical care ventilators are commercially available in the U.S. market.

- March 2026: Mindray has strategically strengthened its presence in the North American ventilator market with the launch of its SV900 and SV700 Ventilators.

- March 2026: Cleveland has integrated advanced portable ICU ventilators into its ambulance fleet, enhancing the delivery of intensive care services during emergency transportation.

- June 2025: Getinge introduced a neonatal option for its Servo-c ventilator, designed to support premature newborns weighing 500 grams and above, as well as adults. The ventilator features invasive leakage compensation and complies with international standards for safety, biocompatibility, and cybersecurity.

Global Medical Ventilator Market Report Scope

As per the scope of the report, a medical ventilator is a life-support machine that helps people breathe when they cannot do so well enough on their own. It pushes oxygen-rich air into the lungs and removes waste gas (carbon dioxide).

The medical ventilator market is segmented by product type, interface, technology, end-user, and geography. By product type, the market includes critical care ventilators, neonatal ventilators, transport and portable ventilators, and home care ventilators. By interface, the market is segmented into invasive ventilation and non-invasive ventilation. By technology, the market is categorized into conventional ventilators, intelligent and closed-loop ventilators, and turbine-based ventilators. By end-user, the market is segmented into hospitals, home care settings, ambulatory surgical centers, and emergency and prehospital care providers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Critical Care Ventilators |

| Neonatal Ventilators |

| Transport and Portable Ventilators |

| Home Care Ventilators |

| Invasive Ventilation |

| Non-Invasive Ventilation |

| Conventional Ventilators |

| Intelligent and Closed-Loop Ventilators |

| Turbine-Based Ventilators |

| Hospitals |

| Home Care Settings |

| Ambulatory Surgical Centers |

| Emergency and Prehospital Care Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Critical Care Ventilators | |

| Neonatal Ventilators | ||

| Transport and Portable Ventilators | ||

| Home Care Ventilators | ||

| By Interface | Invasive Ventilation | |

| Non-Invasive Ventilation | ||

| By Technology | Conventional Ventilators | |

| Intelligent and Closed-Loop Ventilators | ||

| Turbine-Based Ventilators | ||

| By End User | Hospitals | |

| Home Care Settings | ||

| Ambulatory Surgical Centers | ||

| Emergency and Prehospital Care Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical ventilator market?

The medical ventilator market size stands at USD 3.25 billion in 2026 and is projected to reach USD 4.33 billion by 2031 at a 5.91% CAGR.

Which product segment leads ventilator demand?

Critical care ventilators lead with a 44.58% share in 2025 because they remain central to ICU, perioperative, and invasive respiratory support.

Which ventilator type is growing fastest through 2031?

Transport and portable ventilators are growing fastest among product types at a 6.72% CAGR, supported by demand across emergency, transport, and distributed care settings.

Why is home respiratory support becoming more important?

Home care is the fastest-growing end-user segment at a 7.45% CAGR, supported by CMS coverage expansion in 2025 and evidence that home ventilation can reduce long-term institutional costs for eligible COPD patients.

Which region is expanding fastest in ventilators?

Asia-Pacific is the fastest-growing region with an 8.12% CAGR through 2031, driven by ICU expansion, aging populations, and stronger domestic manufacturing capacity.

What is changing competition among ventilator manufacturers?

Competition is moving away from hardware alone and toward software intelligence, workflow efficiency, portability, and service support, as shown by recent moves from Getinge, Mindray, and ZOLL.

Page last updated on: