Reusable Resuscitators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

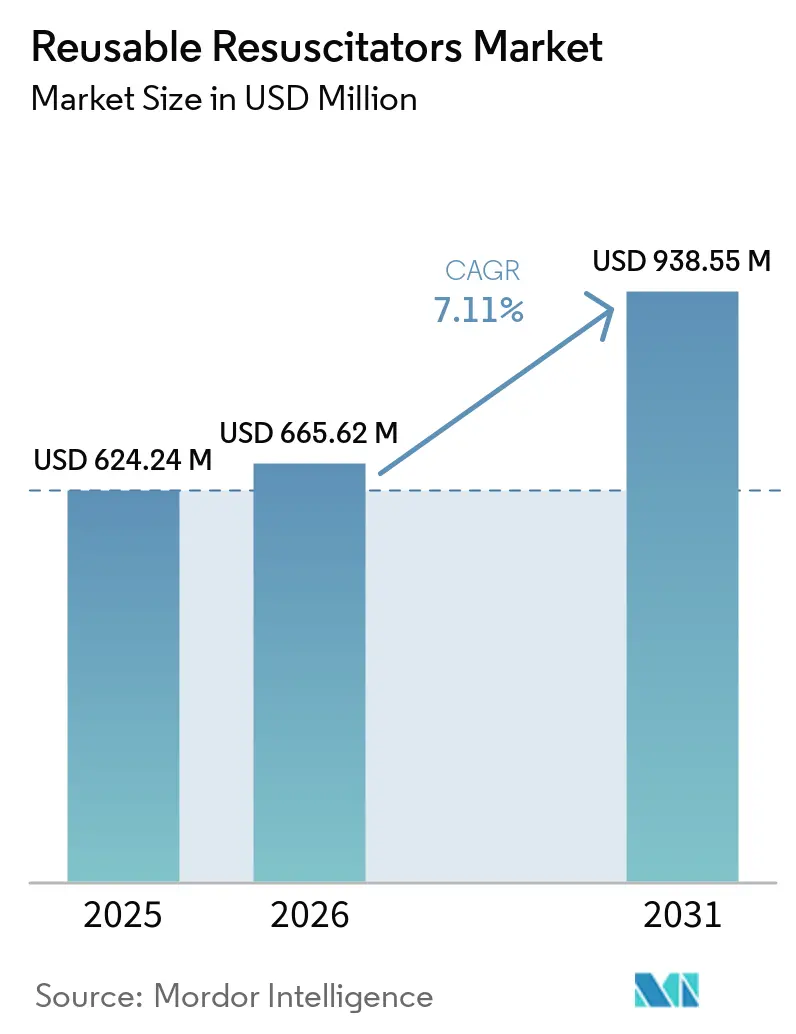

| Market Size (2026) | USD 665.62 Million |

| Market Size (2031) | USD 938.55 Million |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

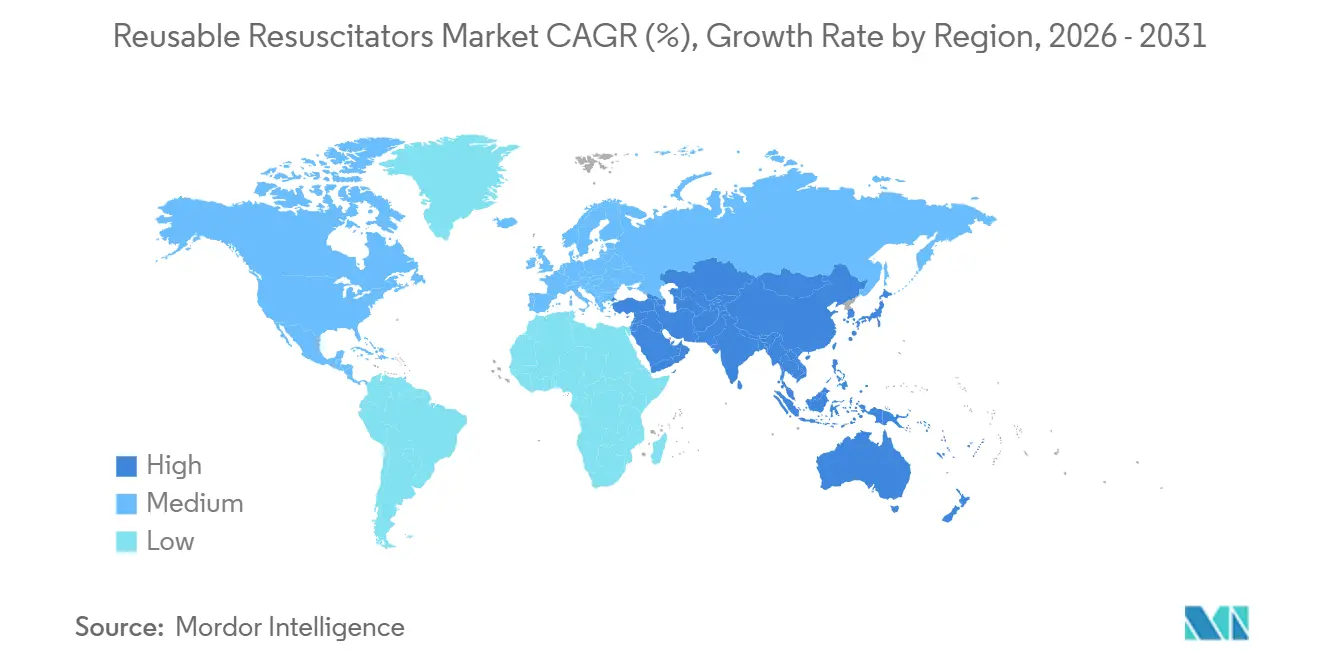

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

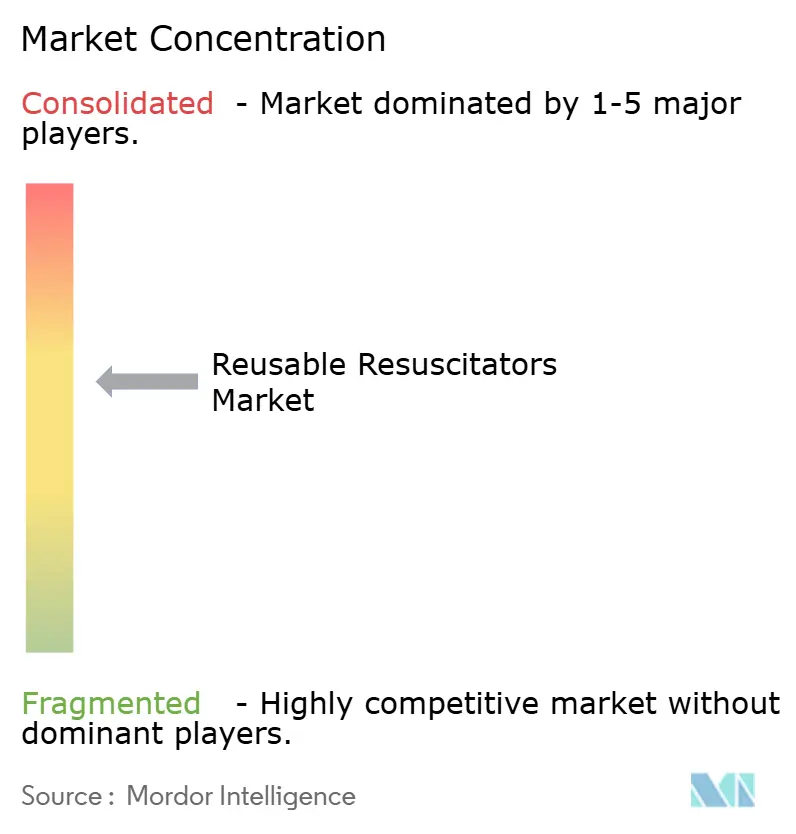

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reusable Resuscitators Market Analysis by Mordor Intelligence

The Reusable Resuscitators Market size was valued at USD 624.24 million in 2025 and is estimated to grow from USD 665.62 million in 2026 to reach USD 938.55 million by 2031, at a CAGR of 7.11% during the forecast period (2026-2031).

Demand is rising as sustainability mandates encourage healthcare systems to favor reprocessable equipment, even while infection-control protocols still prefer disposable bags in high-acuity units. Rapid adult out-of-hospital cardiac-arrest volumes, steady hospital crash-cart replacement cycles, and the procedural shift to ambulatory surgical centers keep baseline orders intact. Growth also benefits from Asia-Pacific hospital-infrastructure expansion and donor-funded neonatal programs that specify autoclavable silicone sets. Competitive pressure concentrates in ISO 10651-5-compliant portfolios from Ambu, Laerdal, and Teleflex, yet smaller firms win tenders by emphasizing autoclave durability and field-serviceable parts. Vendors that pair reusable bags with real-time ventilation feedback or low-carbon sterilization pathways are positioned for incremental share gains.

Key Report Takeaways

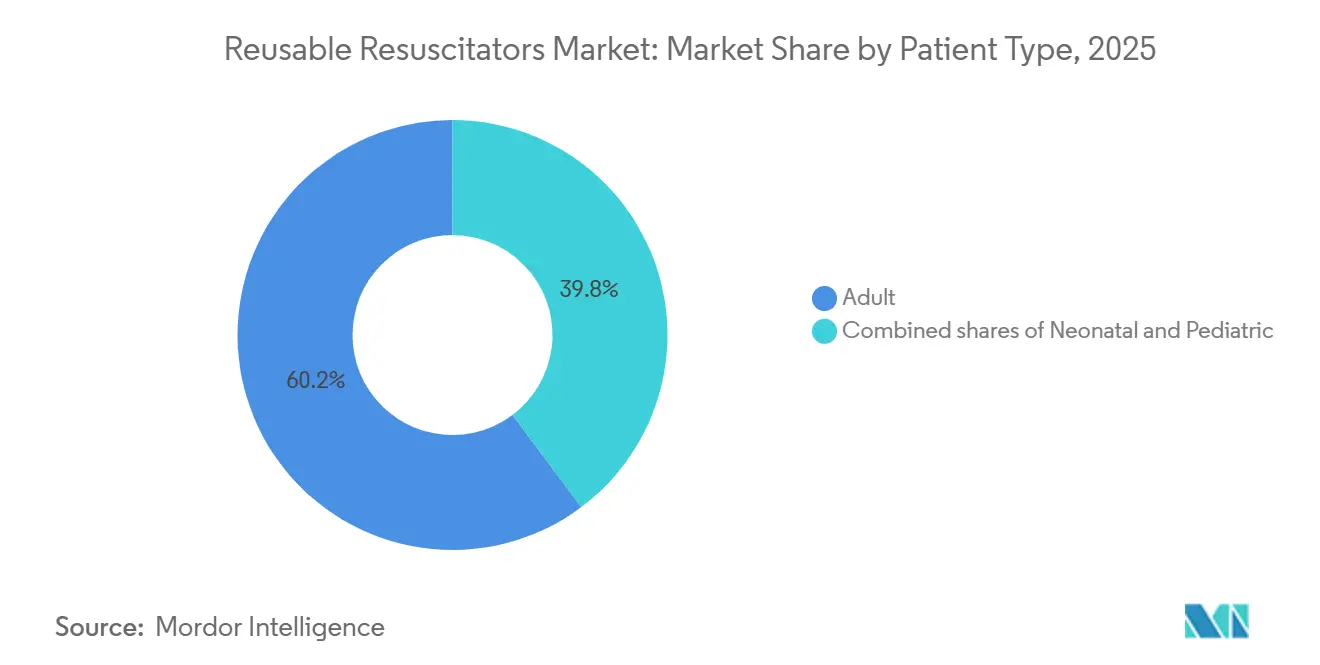

- By patient type, adult resuscitators commanded 60.23% of the reusable resuscitators market share in 2025 and are progressing at an 8.32% CAGR through 2031

- By bag type, flow-inflating bags are projected to register a 9.61% CAGR, outpacing the reusable resuscitators market size for self-inflating models between 2026 and 2031

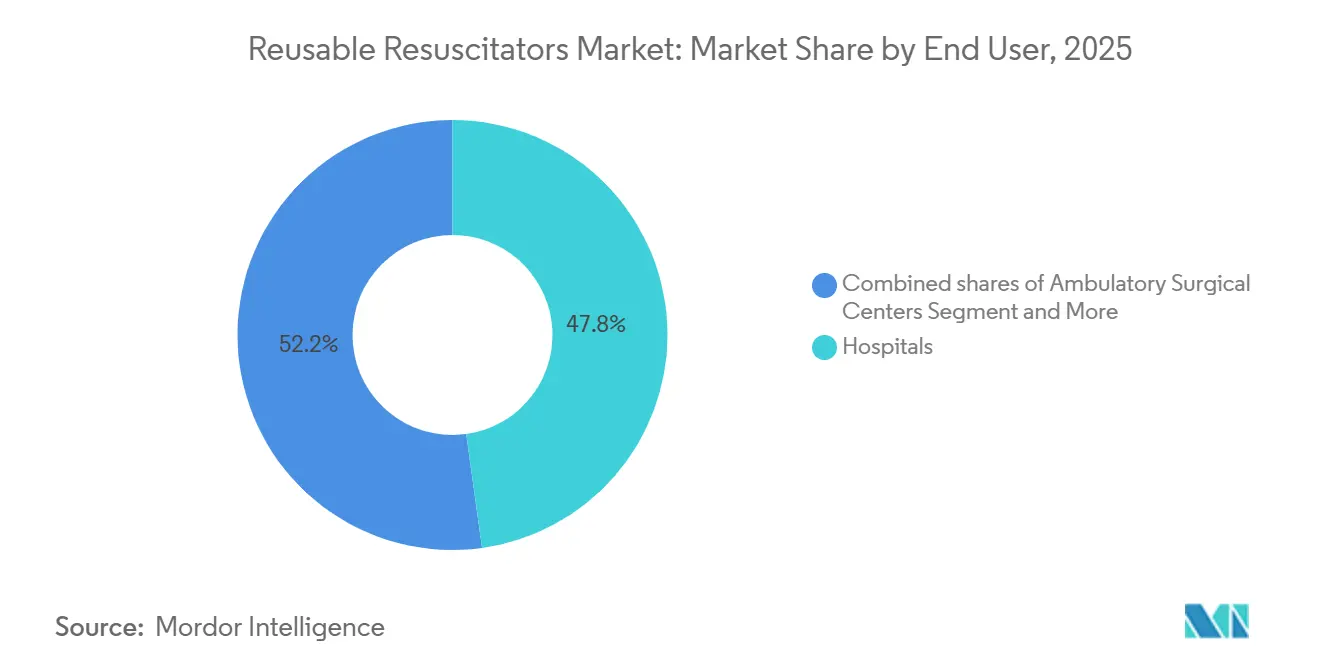

- By end user, hospitals reported 47.81% share of 2025 revenue, and ambulatory surgical centers accounted for 9.45% CAGR growth, the fastest rate within the reusable resuscitators market during 2026-2031.

- By geography, Asia-Pacific is set to post a 9.12% CAGR, eclipsing North America’s 42.67% share and mature replacement demand within the reusable resuscitators market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reusable Resuscitators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Self-inflating segment dominance supports recurring replacement, training, and upgrades | +1.2% | North America, Europe | Medium term (2-4 years) |

| Hospitals as primary end users underpin stable baseline demand and specification-led procurement | +1.5% | Global, urban APAC | Long term (≥ 4 years) |

| North America scale and APAC expansion sustain global volume and channel leverage | +1.3% | North America, China, India | Long term (≥ 4 years) |

| Out-of-hospital cardiac arrest and respiratory emergencies sustain EMS demand | +0.9% | North America, Europe | Medium term (2-4 years) |

| Donor-funded neonatal programs mandate reusable silicone sets in LMICs | +0.6% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Sustainability and total-cost pressures nudge portfolios toward reusables | +0.5% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Self-Inflating Segment Dominance Supports Recurring Replacement, Training, and Upgrades

Self-inflating bags require no external gas supply, making them indispensable for ambulances and emergency departments where oxygen lines are unavailable. Silicone components begin to harden after 15-20 autoclave cycles at 134 °C, so high-utilization fleets replace units roughly every two years, generating dependable revenue [1]BLS Systems, “Reusable Manual Resuscitators Product Catalog,” blssystems.com. Training centers also procure simulation-grade bags that never enter clinical rotation, enlarging total purchasing volumes. Device familiarity created during skills training translates into preference lists when facilities refresh crash-cart inventories. Established vendors leverage ISO 10651-5 conformity and long-term service contracts, which deter new entrants that cannot shoulder documentation and staff-education costs.

Hospitals as Primary End Users Underpin Stable Baseline Demand and Specification-Led Procurement

Hospitals held a major share of the 2025 volume because every crash cart, anesthesia machine, and patient-transfer stretcher must carry a manual resuscitator. Accreditation bodies oblige shift-by-shift functional checks, ensuring predictable replacement cycles independent of procedure counts. Large U.S. group-purchasing organizations award multiyear, specification-rich tenders, which favor manufacturers with comprehensive compliance libraries. In China, 37,946 hospitals created an unmatched procurement base in 2023, yet pricing pressure splits demand between premium-brand reusable kits and lower-priced disposables.

North America Scale and APAC Expansion Sustain Global Volume and Channel Leverage

North America supplied the majority of the 2025 turnover on the strength of 20,000 ambulance services carrying three to five bags per vehicle. Asia-Pacific will pace global growth as India’s Ayushman Bharat initiative equips 150,000 Health & Wellness Centers and China modernizes county hospitals. Multinationals leverage North America’s replacement cash flow to finance Asia-Pacific channel build-outs, outbidding regional firms during initial tender rounds. Manufacturing footprints in Malaysia and Costa Rica help bypass tariff regimes and shorten lead times.

Out-of-Hospital Cardiac Arrest and Respiratory Emergencies Sustain EMS Demand

United States out-of-hospital cardiac-arrest incidence climbed to 136,785 in 2024, while England logged 29,241 cases, reinforcing the criticality of early ventilation. EMS agencies cycle equipment every three to five years as they refresh vehicle fleets, ensuring ongoing demand. International guidelines published in 2025 advised caution on mechanical CPR platforms, keeping manual ventilation as first-line therapy. Allied Healthcare’s oxygen-powered L576 line addresses paramedics who prioritize 100% FiO₂ at high flow rates, showing that product differentiation remains possible even in a mature modality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection-control preference for single-use bags in high-acuity settings curbs reusable penetration | -1.1% | North America, Europe ICUs | Short term (≤ 2 years) |

| Sterile-processing capacity and turnaround constraints limit reprocessing at smaller sites | -0.8% | Rural North America, MEA | Medium term (2-4 years) |

| T-piece preference in neonatal care displaces bags for preterm ventilation | -0.4% | North America, Europe NICUs | Medium term (2-4 years) |

| Autoclave-cycle wear and IFU compliance risks erode lifecycle gains | -0.3% | Global high-volume sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection-Control Preference for Single-Use Bags in High-Acuity Settings Curbs Reusable Penetration

Intensive-care units often default to disposable bags to remove cross-contamination risk. A 2025 survey of Chinese sterile-processing departments showed that 73.7% skipped functional tests after reprocessing, and 28.2% lacked written cleaning procedures [2]Chinese Journal of Infection Control, “Reprocessing Quality Control Study,” cjiconline.com. U.S. facilities consulting CDC guidance classify resuscitators as semi-critical devices requiring high-level disinfection, pushing committees toward single-use workarounds. Ambu’s PVC-free SPUR II line captures much of this demand.

Sterile Processing Capacity, Training, and Turnaround Time Constraints Limit Reprocessing at Smaller Sites

Ambulatory surgical centers number 6,150 in the United States, yet many lack on-site autoclaves, making disposable bags an economic necessity. Updated ISO 80601-2-80 demands post-sterilization tidal-volume verification, a requirement that smaller centers struggle to resource [3]International Organization for Standardization, “ISO 80601-2-80:2024,” iso.org. VH₂O₂ systems speed cycles but cost more than USD 100,000, further tilting the choice toward single-use products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Patient Type: Adult Volumes Drive Replacement Cycles

Adult models accounted for 60.23% of 2025 revenue within the reusable resuscitators market and will expand at an 8.32% CAGR through 2031. High cardiac-arrest incidence, mandatory crash-cart stocking, and two-year replacement norms underpin this performance. Pediatric and neonatal units sustain smaller but essential volumes, with reusable resuscitators industry suppliers tailoring pop-off valves to 40 cmH₂O for children and 30 cmH₂O for infants. Donor programs in Africa and South Asia continue to channel upright neonatal bags that withstand repeated steam cycles, partially shielding this cohort from T-piece substitution.

Clinical preference differentiates subsegments. Adult bags emphasize ergonomic grip and 1,500 mL volume, whereas neonatal items prioritize minimal dead space and easy disassembly. Standards such as ISO 10651-5 define airflow and pressure safety thresholds across all sizes, compelling vendors to invest in material science that balances durability against autoclave-induced brittleness.

By Bag Type: Flow-Inflating Bags Gain in Precision-Driven Settings

Self-inflating devices still generated 51.56% of the 2025 value, yet flow-inflating counterparts are forecast to log a 9.61% CAGR, the steepest climb inside the reusable resuscitators market size hierarchy. Anesthesiologists favor flow-inflating bags because operators can titrate oxygen concentration and deliver continuous positive airway pressure. Hospitals with piped oxygen increasingly specify such models for intra-operative ventilation, especially during pediatric induction.

The market split illustrates a trade-off: emergency squads need equipment that functions without gas, while operating rooms demand granular control. Manufacturers respond by bundling both bag types under single SKU families, simplifying inventory management for health systems and supporting cross-training of staff.

By End User: ASCs Outpace Hospitals on Procedural Growth

Hospitals retained 47.81% of 2025 shipments, but ambulatory surgical centers will be the fastest-growing channel at 9.45% CAGR through 2031, driven by expanded outpatient-procedure lists and lower bundled reimbursement rates that still require crash-cart readiness. Many ASCs lean toward disposable kits to avoid sterilization logistics, spurring dual-strategy portfolios that offer both modes. EMS fleets, numbering over 20,000 in the United States, refresh gear every three to five years, ensuring a stable revenue floor.

Clinic and urgent-care orders remain minimal in unit terms yet essential for compliance. Group-purchasing organizations combine hospital and ASC volumes, allowing dominant suppliers to negotiate multi-year, system-wide contracts that cement account stickiness.

Geography Analysis

North America supplied 42.67% of 2025 sales in the reusable resuscitators market, supported by stringent compliance regimes and high replacement cadence. Europe follows with steady volume tied to sustainability legislation that now audits single-use waste streams. Asia-Pacific leads growth at a projected 9.12% CAGR as China’s 9.97 million hospital beds and India’s primary-care expansion turbocharge procurement.

Southeast Asian countries build 200+ hospitals each year, presenting greenfield tenders that reward firms partnering with local distributors familiar with variable device-registration rules. Japan’s aging demographic will lift the home-care segment, though tight reimbursement caps constrain per-unit pricing. Middle East and Africa volumes cluster in the Gulf states’ specialty centers, while Sub-Saharan Africa relies on donor pipelines that favor rugged, reusable silicone designs.

South America remains fragmented; Brazil’s public health budgets push suppliers toward low-margin, high-volume bids, whereas Argentina’s currency swings complicate forecast reliability. Manufacturers that bundle resuscitators with oxygen concentrators and training modules enjoy an edge in these price-sensitive arenas.

Competitive Landscape

Market concentration is moderate. Ambu, Laerdal, and Teleflex anchor large hospital contracts by offering ISO-compliant documentation, broad distribution, and flexible warranty service. Ambu reported USD 182.7 million in Q1 FY 2024/25 revenue, with anesthesia lines expanding 5% organically even as strategic focus shifts to single-use endoscopy. Laerdal reinforced its emergency-care position after the FDA cleared “The BAG” in November 2025. Teleflex exited respiratory care in 2022 but maintains legacy manual-bag sales to hospital networks, pivoting toward its interventional catalog.

Second-tier suppliers such as BLS Systems, Marshall Airway Products, GaleMed, HSINER, and Flexicare differentiate through autoclave cycle counts, modular parts, or regional pricing. ZOLL Medical’s 2024 purchase of Vyaire ventilator lines may create bundled EMS offerings, while Ambu’s 2025 partnership with Archeon Medical positions the firm to overlay real-time tidal-volume feedback on reusable bags. Materials innovation continues, with SEBS and liquid silicone rubber offering PVC-free, 15-cycle durability, yet still vulnerable to high-temperature drying. The competitive gap widens as regulatory updates, such as ISO-FDIS 18190, lift compliance costs that smaller entrants may struggle to absorb.

Reusable Resuscitators Industry Leaders

Ambu A/S

Laerdal Medical

Teleflex Incorporated

BLS Systems Limited

Marshall Airway Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NICU facilities are being encouraged to standardize T-piece resuscitation circuits and related bed warmer circuits to enhance contract alignment, optimize sourcing processes, and achieve substantial cost efficiencies.

- March 2026: Mercury Medical entered into a contract with Vizient, ensuring the availability of its manual resuscitation devices and accessories.

Global Reusable Resuscitators Market Report Scope

As per the scope of the report, reusable resuscitators, often referred to as bag-valve-masks (BVMs) or "Ambu bags," are critical medical devices used to provide manual, positive pressure ventilation to patients who are not breathing or are breathing inadequately. Unlike single-use versions, these resuscitators are constructed from durable, high-quality materials, most commonly medical-grade, latex-free silicone, allowing them to be cleaned, disinfected, and sterilized for repeated use.

The reusable resuscitators market is segmented by patient type, end users, bag type, and geography. Based on patient type, the market is segmented into neonatal, pediatric, and adult. Based on bag type, the market is segmented into Self-inflating (SIB) and Flow-inflating (Anesthesia bag). By end users, the market is segmented into hospitals, ambulatory surgical centers (ASCs), EMS/ prehospital, and clinics and urgent care. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Neonatal |

| Pediatric |

| Adult |

| Self-inflating (SIB) |

| Flow-inflating (Anesthesia bag) |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| EMS / Prehospital |

| Clinics and Urgent Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Patient Type | Neonatal | |

| Pediatric | ||

| Adult | ||

| By Bag Type | Self-inflating (SIB) | |

| Flow-inflating (Anesthesia bag) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| EMS / Prehospital | ||

| Clinics and Urgent Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the reusable resuscitators market in 2026?

The reusable resuscitators market size reached USD 665.62 million in 2026.

What is the projected CAGR for reusable manual bags to 2031?

Revenue is forecast to grow at a 7.11% CAGR over 2026-2031.

Which patient segment leads demand?

Adult models held 60.23% of 2025 revenue and show the fastest absolute dollar growth.

Why are ambulatory surgical centers an important growth channel?

Procedure migration drives a 9.45% CAGR for ASCs by 2031, requiring each center to maintain emergency ventilation gear.

Page last updated on: