Intensive Care Unit (ICU) Ventilators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

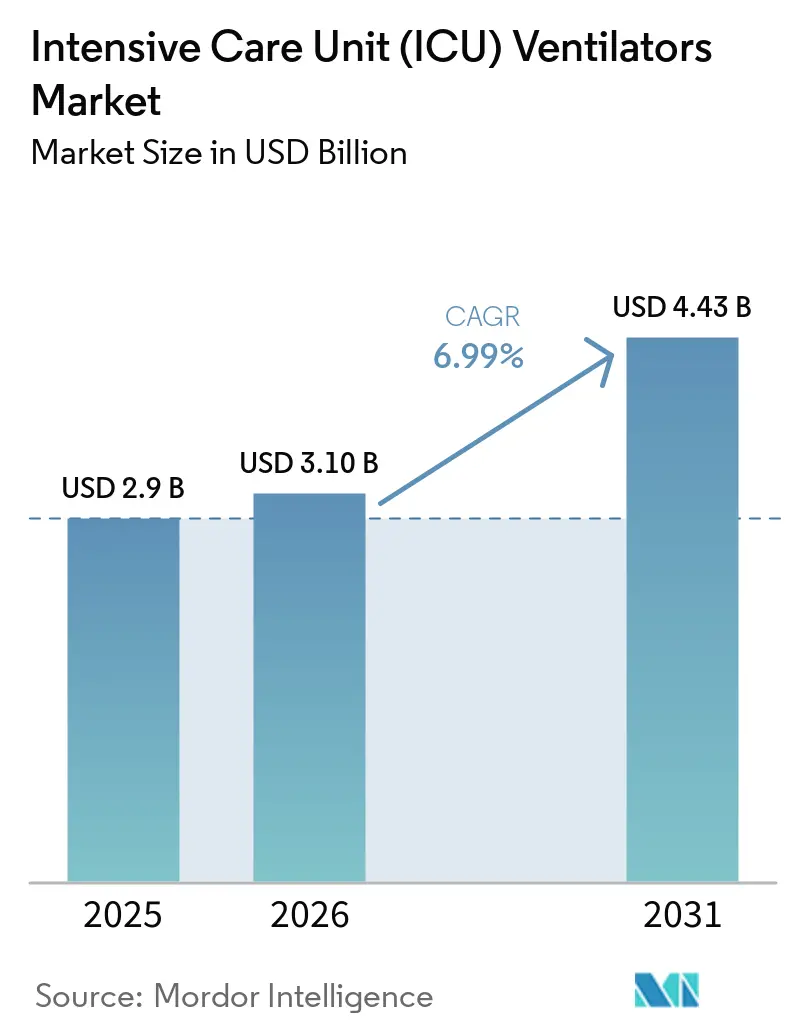

| Market Size (2026) | USD 3.10 Billion |

| Market Size (2031) | USD 4.43 Billion |

| Growth Rate (2025 - 2031) | 6.99% CAGR |

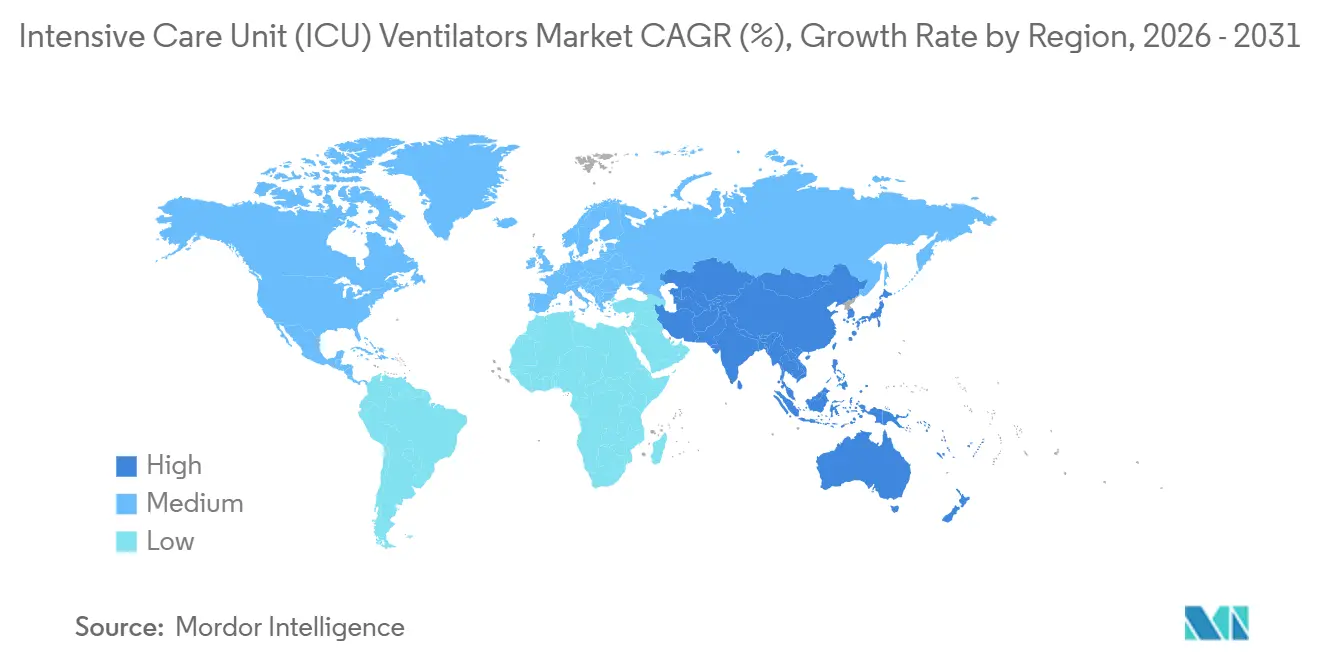

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

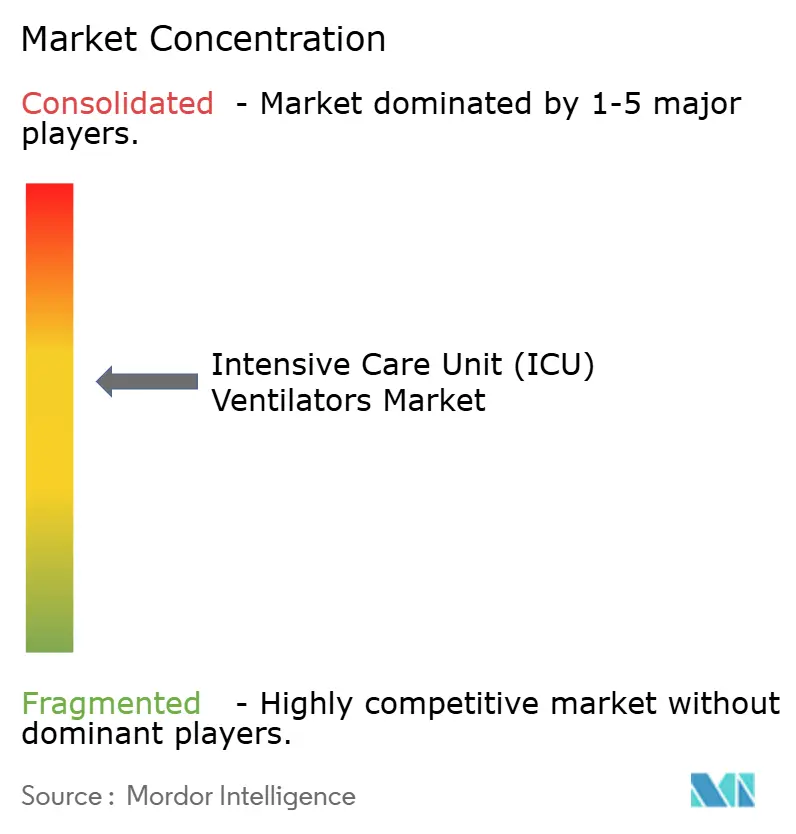

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intensive Care Unit (ICU) Ventilators Market Analysis by Mordor Intelligence

The Intensive Care Unit Ventilators Market size is expected to increase from USD 2.9 billion in 2025 to USD 3.10 billion in 2026 and reach USD 4.43 billion by 2031, growing at a CAGR of 6.99% over 2026-2031.

Continued demand for critical-care capacity, the shift to turbine-based portables, and the rollout of closed-loop automation support this expected expansion. Hospitals are refreshing inventories with energy-efficient models that satisfy both value-based care rules and carbon-reduction targets. At the same time, non-invasive ventilation (NIV) devices reduce the average ICU length of stay. Manufacturers that embed AI-driven weaning protocols into mid-tier units create cost-effective alternatives for emerging-market tenders. In parallel, regulatory guidance on software change-control plans accelerates product updates and encourages cloud-connected fleets in North America and Western Europe. Portable systems enable new revenue streams in ambulatory surgical centers, and sustainability mandates in the European Union and select U.S. states reward low-wattage designs.

Key Report Takeaways

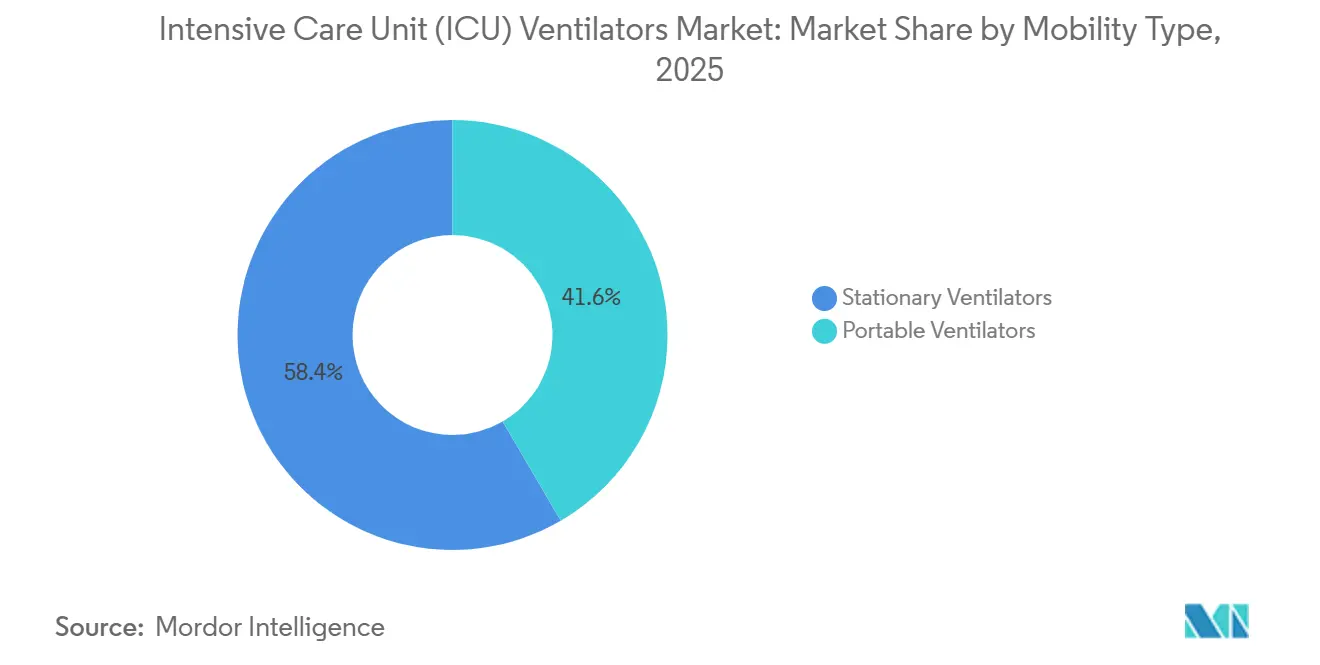

- By mobility type, stationary ventilators held 58.4% of the ICU ventilators market share in 2025, while portable systems are forecast to grow at a 7.50% CAGR through 2031.

- By product type, high-end ventilators accounted for 52.1% of the ICU ventilators market size in 2025, whereas the mid-end segment is projected to rise at a 7.35% CAGR during the same period.

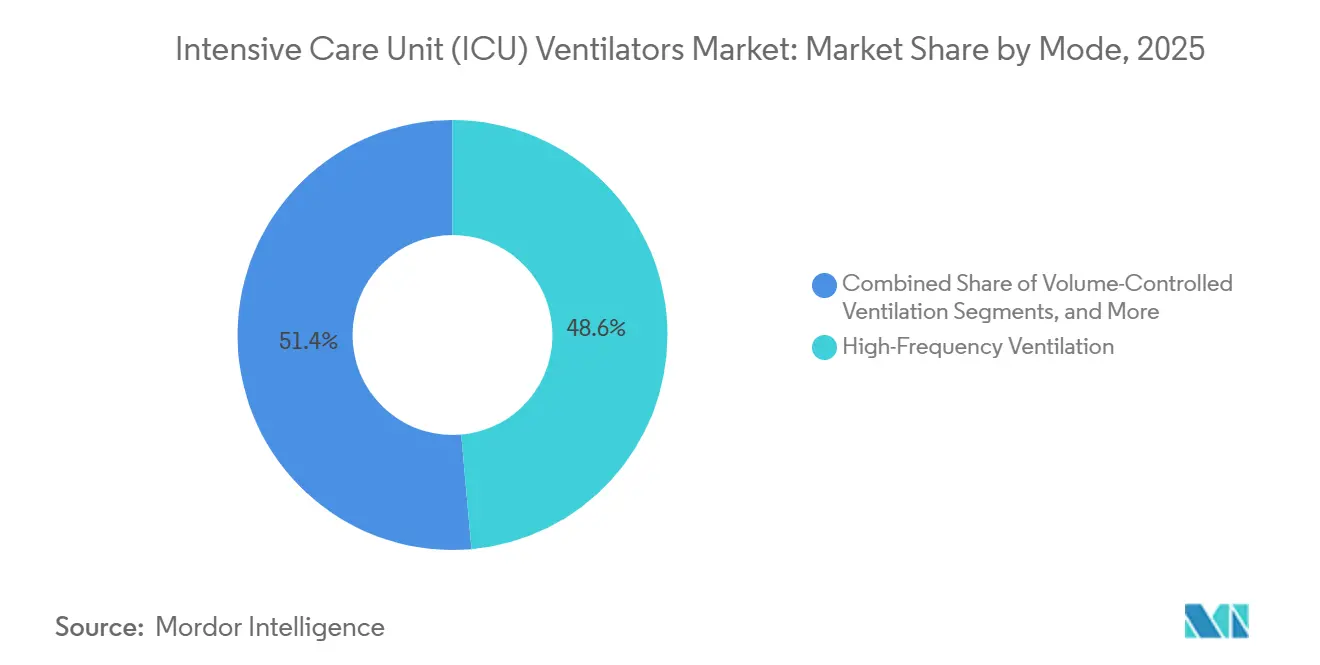

- By mode, high-frequency ventilation led with a 48.6% revenue share in 2025, and combined modes are expected to expand at a 7.42% CAGR to 2031.

- By patient age group, adult applications commanded 56.5% of the ICU ventilators market size in 2025 and are progressing at a 7.27% CAGR.

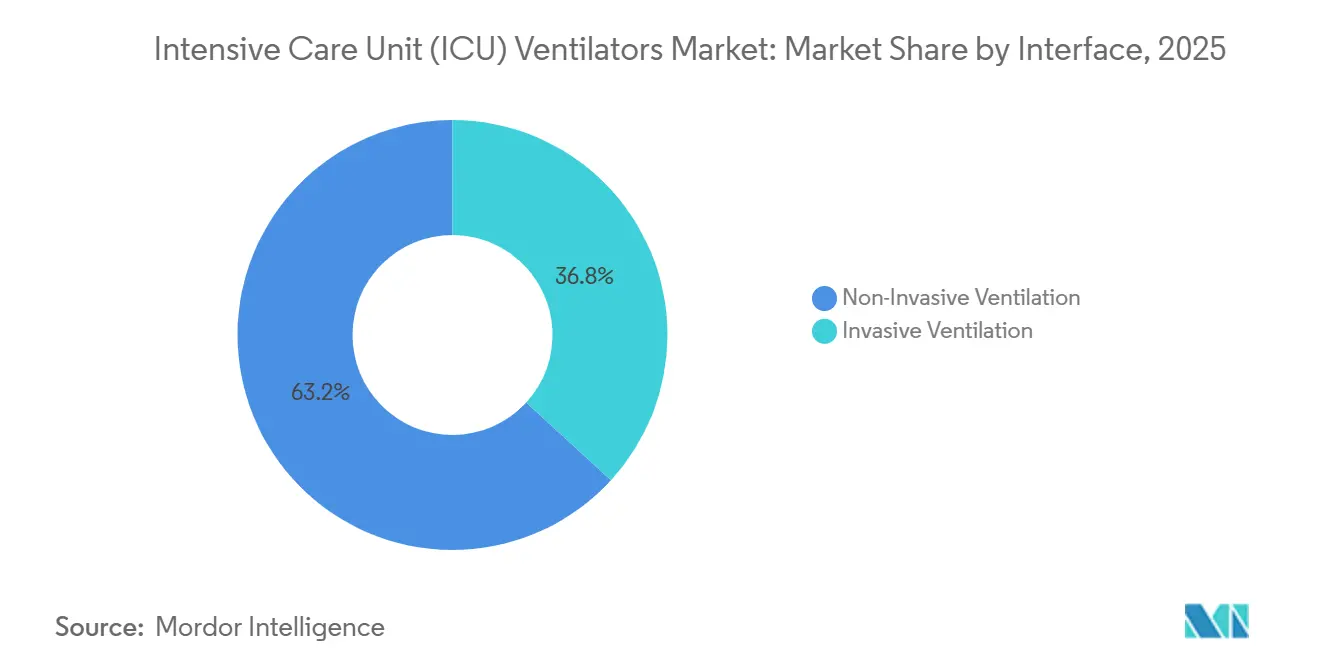

- By interface, non-invasive ventilation devices secured 63.2% share of the ICU ventilators market in 2025 and will advance at a 7.47% CAGR through 2031.

- By end-user, hospitals captured 47.3% demand in 2025, with portable NIV units in ambulatory surgical centers showing the highest projected growth trajectory.

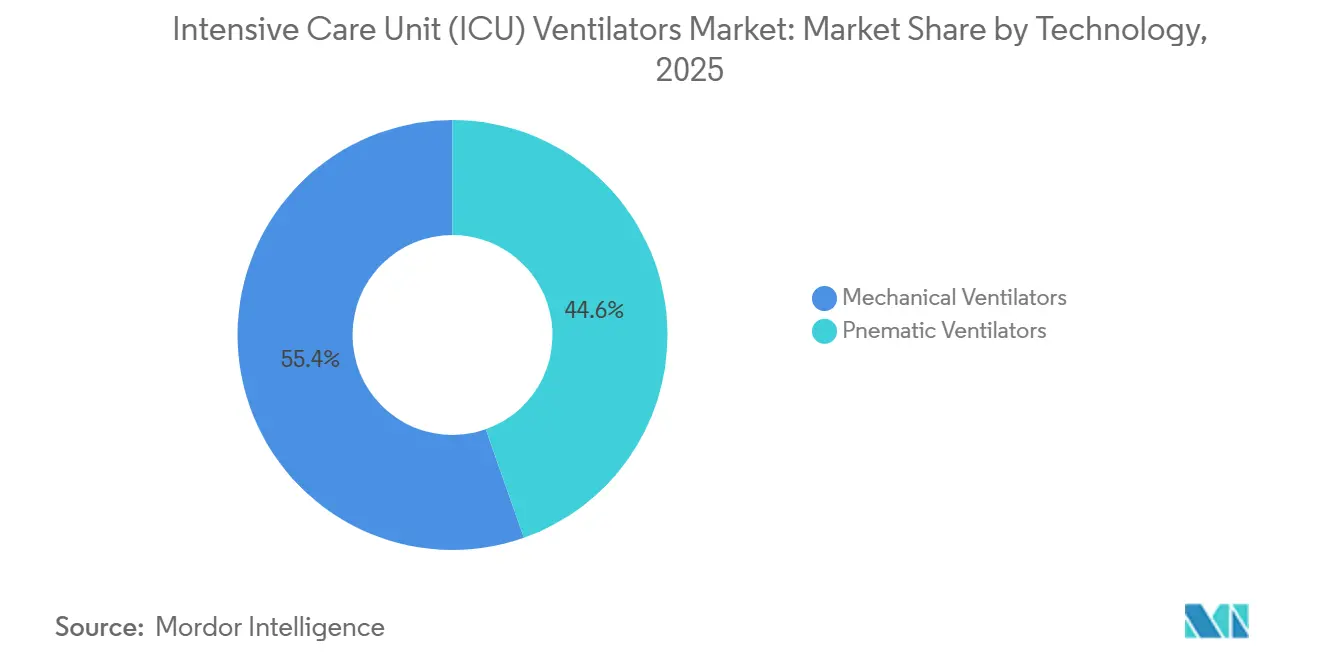

- By technology, mechanical ventilators held 55.4% share of the ICU ventilators market size in 2025 and are moving forward at a 7.17% CAGR.

- By geography, North America accounted for 37.2% of 2025 revenue, whereas Asia-Pacific is poised to expand at an 7.23% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Intensive Care Unit (ICU) Ventilators Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging incidence of acute respiratory distress syndrome (ARDS) | 1.2% | Global, with concentration in North America, Europe, and urban APAC | Medium term (2-4 years) |

| Government-funded ICU capacity expansion in LMICs | 1.5% | APAC core (India, Indonesia, Philippines), Sub-Saharan Africa, spill-over to Latin America | Long term (≥ 4 years) |

| Integration of turbine-based portable ventilators | 0.9% | North America, Europe, GCC; early adoption in Australia and Japan | Short term (≤ 2 years) |

| Rapid installation of ai-driven closed-loop ventilation | 1.1% | North America, Western Europe, Singapore, South Korea | Medium term (2-4 years) |

| Rising adoption of non-invasive ventilation in general wards | 1.3% | Global, with accelerated uptake in Europe and North America | Short term (≤ 2 years) |

| Hospital sustainability mandates for energy-efficient fleets | 0.7% | EU-27, UK, California, New York; emerging in Canada and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Incidence of Acute Respiratory Distress Syndrome

ARDS remains a core demand driver for the ICU ventilators market. U.S. incidence stands at 64 per 100,000 population, and the condition accounts for 10%–15% of global ICU admissions.[1]American Thoracic Society, “Acute Respiratory Distress Syndrome,” thoracic.org Mortality of 30%–50% keeps clinical focus on precision-titrated ventilation that limits lung injury. Seasonal wildfire smoke in North America and persistent air-quality challenges in South Asia elevate ARDS case peaks. As OECD populations age, hospitals front-load replacement cycles even while pandemic stockpiles depreciate. Together, these patterns sustain baseline procurement beyond crisis surges.

Government-Funded ICU Capacity Expansion in LMICs

Low- and middle-income countries allocate multiyear budgets to critical-care infrastructure. India’s Ayushman Bharat program sets aside INR 64,180 crore for 2025-2026, with 12% geared to ventilators in district hospitals.[2]Government of India Ministry of Health and Family Welfare, “Ayushman Bharat Program 2025-2026,” mohfw.gov.in Subsidies under the Production-Linked Incentive scheme reimburse up to 5% of incremental sales, shortening lead times for domestically assembled units. Mid-end mechanical ventilators priced under USD 25,000 meet technical requirements while aligning with fiscal constraints, expanding the ICU ventilators market in price-sensitive regions.

Integration of Turbine-Based Portable Ventilators

Turbine designs eliminate reliance on central gas systems, making them essential for ambulances, helicopters, and home settings. Hamilton Medical’s C3 weighs 4.2 kg, offers a 6-hour battery, and supports both invasive and non-invasive modes. Average power draw of 35 watts fits EU Green Deal energy thresholds. Hospitals pursuing carbon targets now factor wattage scores into tenders, pushing turbine adoption within the ICU ventilators market.

Rapid Installation of AI-Driven Closed-Loop Ventilation

Machine-learning algorithms automate PEEP, tidal volume, and FiO2 adjustments. September 2023 FDA guidance on predetermined change control plans streamlines post-market software updates. Philips’ IntelliSync platform integrates with electronic health records and cuts setup errors by 23% at early-adopter sites. Uptake concentrates in high-acuity centers with analytics teams, indicating phased diffusion across the ICU ventilators market over the next three years.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply-chain fragility for critical ventilator components | -0.8% | Global, with acute exposure in North America and Europe dependent on Asian semiconductor fabs | Short term (≤ 2 years) |

| Stringent regulatory re-certification for software-driven units | -0.6% | North America (FDA 510(k)), Europe (EU MDR), spillover to Australia (TGA) and Canada (Health Canada) | Medium term (2-4 years) |

| Persistent post-pandemic ICU overcapacity in developed markets | -0.5% | North America, Western Europe, with pockets in Australia and Japan | Short term (≤ 2 years) |

| Uptake of high-flow nasal cannula curbing ventilator demand | -0.4% | Global, with fastest substitution in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Fragility for Critical Ventilator Components

Semiconductor and turbine shortages extend device lead times to 16-22 weeks. FDA guidance on supply resilience flags turbines and pressure transducers as high-risk parts. Precision-machined titanium housings rely on a limited vendor base in Germany and Japan, constraining portable production. Backlogs hamper timely fulfillment and limit revenue capture in the ICU ventilators market.

Stringent Regulatory Re-Certification for Software-Driven Units

Software iterations that alter ventilator performance now demand additional evidence under both U.S. 510(k) and EU MDR frameworks. Extra verification adds 4-6 months to launch schedules and raises compliance outlays to around EUR 500,000 per product line, favoring incumbents with larger regulatory teams.[3]European Commission, “European Green Deal for Healthcare Sector,” ec.europa.eu Smaller suppliers face prolonged queues, delaying innovation diffusion across the ICU ventilators market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mobility Type – Portable Growth Outpaces Stationary Demand

Portable ventilators are forecast to grow at 7.50% CAGR through 2031, a rate that surpasses the 6.99% average for the ICU ventilators market. Demand arises from emergency services, military units, and home-care transitions that value battery autonomy and turbine blowers. Portable models bypass the hospital pipeline oxygen, enabling a broader geographic reach. Stationary systems, which captured 58.4% share in 2025, remain essential for high-acuity ICUs with integrated monitoring networks, yet overcapacity in developed markets lengthens their replacement intervals to nine years. The FDA guidance that clarifies battery testing streamlined approvals by three months, accelerating portable launches and supporting their climb within the ICU ventilators market.

Stationary units still dominate in tertiary hospitals that embed ventilators into networked alarm systems and centralized gas supplies. Maintenance contracts now emphasize remote diagnostics and software upgrades, helping vendors preserve margin despite slower unit turnover. As sustainability targets tighten, even large fixed platforms must meet lower wattage thresholds, nudging manufacturers to retrofit turbines and optimize airflow paths. These upgrades keep the stationary base relevant while portable expansion unlocks new revenue streams, balancing the mobility landscape of the ICU ventilators market.

By Product Type – Mid-End Platforms Narrow the Technology Gap

Mid-end ventilators are projected to advance at a 7.35% CAGR, buoyed by emerging-market tenders that demand sophisticated modes at mid-tier prices. Manufacturers now embed airway pressure release ventilation and neurally adjusted ventilatory assist into sub-USD 20,000 units, narrowing functional gaps with high-end systems. High-end platforms held 52.1% share of the ICU ventilators market size in 2025, sustained by quaternary hospitals that require seamless EHR integration and advanced monitoring. Yet price premiums soften as mid-end units deliver comparable clinical outcomes.

Low-end devices maintain footholds in rural clinics and disaster stockpiles, but their limited feature sets and inability to meet new ISO alarm standards restrict volume—competitive focus, therefore, swings to mid-range models. Companies leverage AI-driven weaning algorithms to add value while holding costs, expanding mid-end traction in public procurement, and reshaping product mix across the ICU ventilators market.

By Mode: Combined Modes Gain Traction in Neonatal ICUs

Advanced and combined ventilation modes are expanding at 7.42% CAGR through 2031, outpacing high-frequency ventilation's 48.6% market share in 2025, as neonatal intensive care units adopt synchronized intermittent mandatory ventilation and volume-guarantee algorithms that minimize barotrauma in preterm infants. High-frequency ventilation remains the workhorse for severe ARDS and neonatal respiratory distress syndrome, delivering 300 to 900 breaths per minute to maintain alveolar recruitment while limiting peak airway pressures. Volume-controlled and pressure-controlled modes serve the bulk of adult ICU cases, offering clinician familiarity and regulatory approval across all geographies. Manufacturers are responding with hybrid platforms. Drägerwerk's Babylog VN800 offers high-frequency, volume-controlled, and neurally adjusted modes in a single device that reduce capital expenditure for hospitals managing diverse patient populations.

By Patient Age Group: Adult Segment Dominates, Neonatal Innovations Accelerate

Adult patients accounted for 56.5% of ICU ventilator demand in 2025, growing at 7.27% CAGR through 2031, propelled by aging populations in OECD markets and rising ARDS incidence tied to pollution and sepsis. Pediatric ventilators serve a smaller but clinically distinct cohort, requiring tidal volumes as low as 20 mL and pressure limits under 30 cm H2O to prevent lung injury in patients weighing 3 to 40 kg. Neonatal ventilators, designed for infants under 3 kg, are witnessing rapid innovation in high-frequency oscillation and neurally adjusted ventilation, technologies that synchronize mechanical breaths with the infant's diaphragmatic activity to reduce ventilator-induced lung injury.

By Interface: Non-Invasive Ventilation Expands Beyond COPD

Non-invasive ventilation interfaces captured 63.2% market share in 2025 and are advancing at 7.47% CAGR through 2031, the fastest rate among interface types, as clinical protocols extend NIV to heart failure, post-extubation support, and immunocompromised patients where intubation carries infection risks. Invasive ventilation remains essential for severe ARDS, multi-organ failure, and patients requiring neuromuscular blockade. Still, its share is eroding as high-flow nasal cannula and NIV reduce intubation rates by 15% to 28% in eligible cohorts.

By End-User: Hospitals Dominate, ASCs Emerge as Growth Pocket

Hospitals held 47.3% of end-user demand in 2025, growing at 7.32% CAGR through 2031, as ICU bed expansions in Asia-Pacific and the Middle East offset replacement-cycle delays in North America and Europe. Ambulatory surgical centers are adopting portable, non-invasive ventilators for post-anesthesia care and same-day procedures requiring brief respiratory support, a use case that bypasses traditional ICU capital-expenditure cycles. Specialty clinics focused on sleep medicine, pulmonary rehabilitation, and long-term acute care represent a fragmented segment where reimbursement variability and regulatory ambiguity slow adoption. The hospital segment's resilience stems from its role as the primary ICU operator; even as outpatient procedures migrate to ASCs, complex cases requiring mechanical ventilation remain hospital-centric.

By Technology: Mechanical Ventilators Lead, Pneumatic Phase-Out Accelerates

Mechanical ventilators commanded 55.4% technology share in 2025, advancing at 7.17% CAGR through 2031, as turbine-driven and piston-based designs offer superior portability, energy efficiency, and software-upgrade pathways versus pneumatic systems. Pneumatic ventilators, which rely on compressed oxygen and air, persist in settings with robust pipeline infrastructure and limited access to electrical power, but their share is declining as hospitals prioritize platforms compatible with AI-driven closed-loop algorithms. Mechanical ventilators' dominance reflects their alignment with regulatory and sustainability mandates: ISO 80601-2-12 compliance for software-driven alarm management is more straightforward in microcontroller-based mechanical units than in pneumatic designs that use analog pressure regulators.

Geography Analysis

North America held 37.2% share in 2025, yet future growth is moderated by stockpile-driven overcapacity that delays fleet refresh. The region leads in AI-enabled closed-loop adoption and turbine portable penetration. Canada pilots carbon dashboards that score device emissions, tying procurement to net-zero milestones. Vendors increasingly package analytics subscriptions with hardware to unlock service revenue in the ICU ventilators market.

Asia-Pacific is the fastest-growing region at 7.23% CAGR through 2031. China issues accelerated clearances for domestic suppliers such as Mindray and Comen, while India’s production incentives strive for USD 1.5 billion medical-device output by 2028.ASEAN harmonization trims regulatory timelines by six months. Japan’s aging population, with 27% over 65 years in 2025, sustains ICU admissions for pneumonia and COPD. These dynamics enlarge the regional share of the ICU ventilators market.

Europe faces Medical Device Regulation recertification expenses averaging EUR 500,000 per line. High compliance cost favors incumbents but slows new product rollouts. Italy and Spain pilot leasing models that shift ventilator costs from capital to operating budgets, easing fiscal pressure on hospitals while maintaining flow in the ICU ventilators market.

Competitive Landscape

The ICU ventilators market shows moderate concentration. The top five firms, Getinge, Drägerwerk, Philips, Medtronic, and GE Healthcare, held about 48% combined share in 2025. Regional players such as Mindray, Nihon Kohden, and Comen capitalize on domestic sourcing policies to gain share. Mid-end and portable segments face aggressive pricing, so manufacturers differentiate with predictive maintenance, clinician training, and software subscriptions that extend lifecycle revenue.

Hamilton Medical and Fisher & Paykel win share by specializing in turbine portables and HFNC-ventilator hybrids. Patent filings illustrate the innovation race: Philips filed 14 patents in 2024-2025 for AI weaning algorithms and turbine geometries. Medtronic secured a 2025 patent on a hybrid pneumatic-mechanical ventilator suited to field hospitals. Participation in ISO working groups lets companies influence alarm standards, shaping competitive rules that secure design advantages in the ICU ventilators market.

Regulation creates uneven playing fields. FDA change-control guidance allows incumbents to deploy over-the-air updates four months faster than challengers. EU MDR demands full clinical evaluations for software modifications, raising costs that smaller builders struggle to absorb, thereby reinforcing incumbent strength. As service models mature, predictive maintenance contracts and data analytics dashboards become primary differentiation levers, anchoring customer loyalty and recurring revenue streams.

Intensive Care Unit (ICU) Ventilators Industry Leaders

GE Healthcare

Medtronic PLC

Dragerwerk AG & Co. KGaA

Getinge AB

ResMed

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mindray has strategically strengthened its presence in the North American ventilator market with the launch of its SV900 and SV700 Ventilators.

- March 2026: Cleveland has integrated advanced portable ICU ventilators into its ambulance fleet, enhancing the delivery of intensive care services during emergency transportation.

- August 2025: Chenwei Medical emphasized the advanced capabilities of its T80 ICU Ventilator, designed to provide intelligent, precise, and adaptable respiratory support for ICU, emergency, and post-operative care applications.

Global Intensive Care Unit (ICU) Ventilators Market Report Scope

As per the scope of the report, ICU ventilators are advanced medical devices essential for critical care settings, designed to support or fully manage a patient's breathing when they are unable to do so independently. These devices deliver oxygen-enriched air to the lungs and remove carbon dioxide, using either invasive tubes or non-invasive masks. They play a critical role in managing respiratory failure, treating severe infections, and providing post-surgical respiratory support.

The segmentation of the ICU ventilators market is categorized by mobility type, product type, mode, patient age group, interface, end-user, technology, and geography. By mobility type, the market includes stationary and portable ventilators. By product type, it is segmented into high-end, mid-end, and low-end ventilators. By mode, the categories include volume-controlled, pressure-controlled, high-frequency, and others. By patient age group, the market is divided into adult, pediatric, and neonatal. By interface, it is segmented into invasive and non-invasive ventilators. By end-user, the market includes hospitals, ASCs, specialty clinics, and others. By technology, it is categorized into mechanical, pneumatic, and other types. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Stationary Ventilators |

| Portable Ventilators |

| High-End ICU Ventilators |

| Mid-End ICU Ventilators |

| Low-End ICU Ventilators |

| Volume-Controlled Ventilation |

| Pressure-Controlled Ventilation |

| High-Frequency Ventilation |

| Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation) |

| Adult |

| Pediatric |

| Neonatal |

| Invasive Ventilation |

| Non-Invasive Ventilation |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation) |

| Mechanical Ventilators |

| Pnematic Ventilators |

| Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Mobility Type | Stationary Ventilators | |

| Portable Ventilators | ||

| By Product Type | High-End ICU Ventilators | |

| Mid-End ICU Ventilators | ||

| Low-End ICU Ventilators | ||

| By Mode | Volume-Controlled Ventilation | |

| Pressure-Controlled Ventilation | ||

| High-Frequency Ventilation | ||

| Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation) | ||

| By Patient Age Group | Adult | |

| Pediatric | ||

| Neonatal | ||

| By Interface | Invasive Ventilation | |

| Non-Invasive Ventilation | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation) | ||

| By Technology (Value) | Mechanical Ventilators | |

| Pnematic Ventilators | ||

| Others (Combined / Advanced Modes, Synchronized Intermittent Mandatory Ventilation) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected valuation of the ICU ventilators market by 2031?

It is forecast to reach USD 4.43 billion as fleets modernize and portable volumes climb.

Which mobility category is growing fastest within ICU ventilation?

Portable turbine-based systems are expected to rise at a 7.50% CAGR through 2031.

How are sustainability mandates influencing ventilator procurement?

Hospitals in the EU and select U.S. states now favor energy-efficient models that consume below 50 watts per patient day.

Why are mid-end ventilators gaining popularity in emerging economies?

They deliver advanced modes at prices 40% lower than high-end units, aligning with cost-sensitive public tenders.

What role do AI-driven closed-loop features play in new ventilators?

Machine-learning algorithms automate key settings, cut clinician workload, and are a primary differentiator for new product launches.

Page last updated on: