Medical Grade Silicone Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.77 Billion |

| Market Size (2030) | USD 2.41 Billion |

| Growth Rate (2025 - 2030) | 6.41% CAGR |

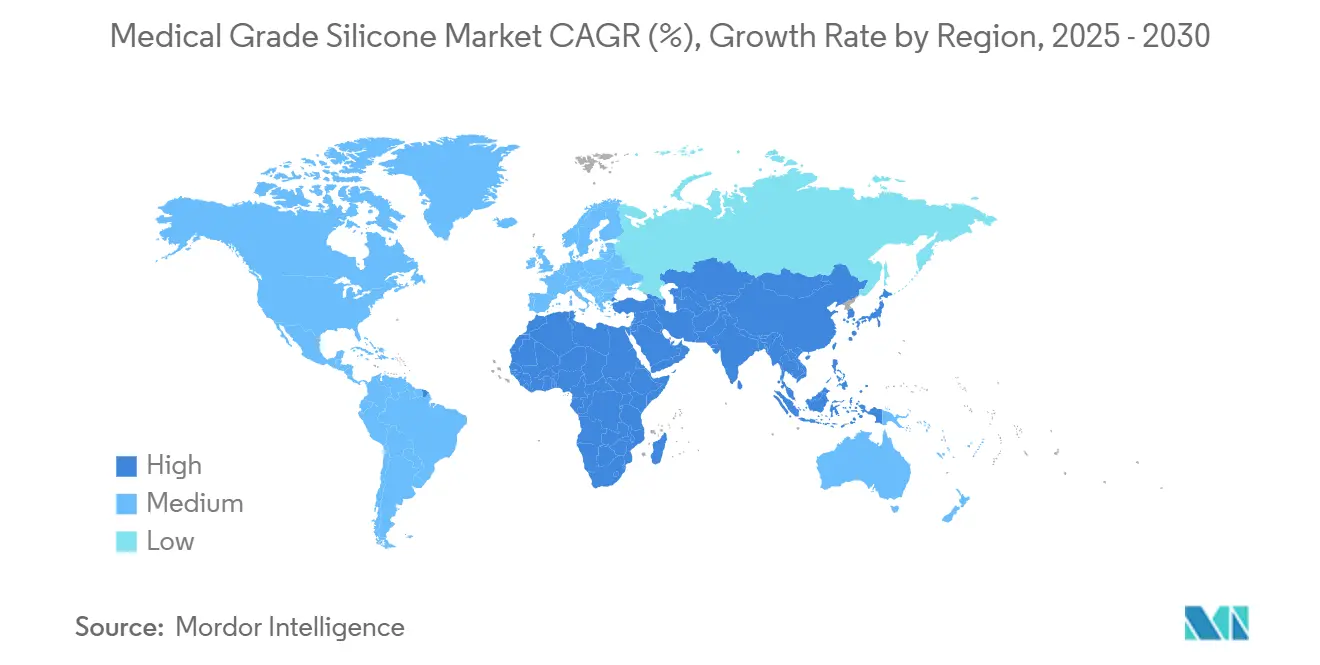

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

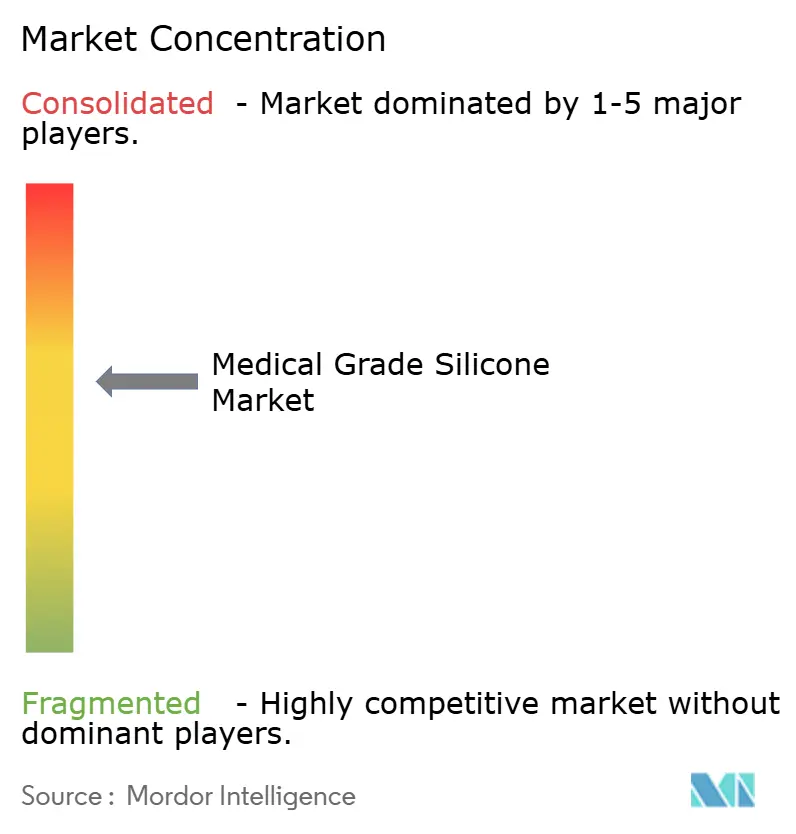

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Grade Silicone Market Analysis by Mordor Intelligence

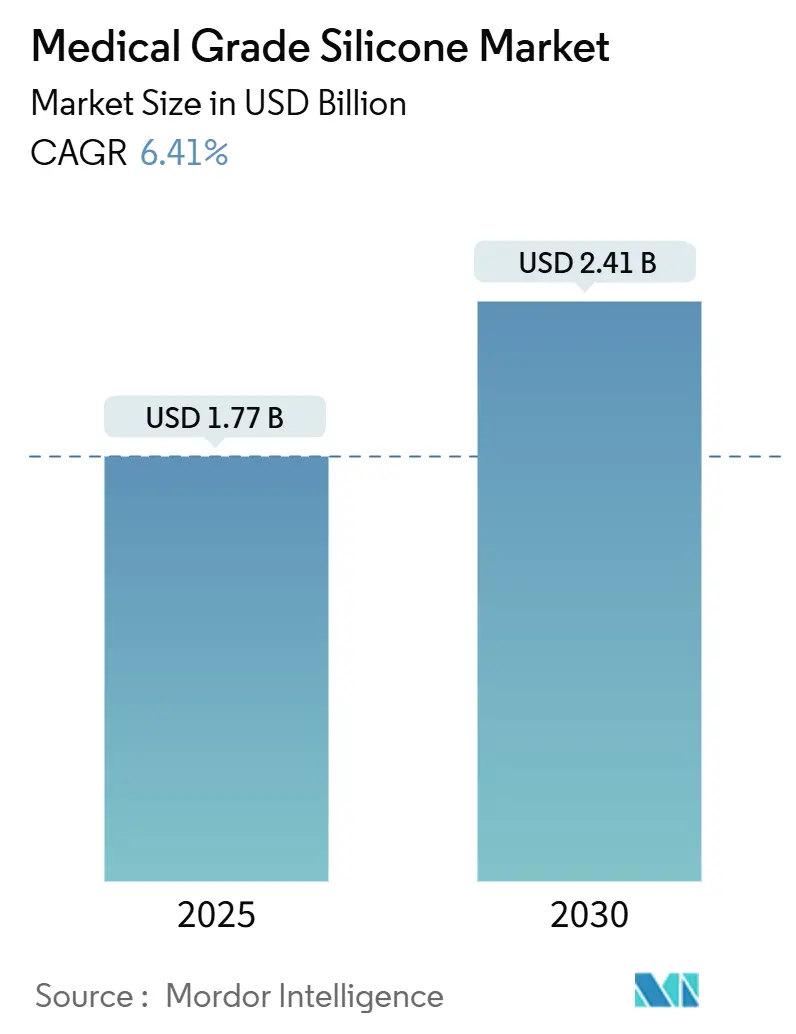

The global medical grade silicone market size stands at USD 1.77 billion in 2025 and is projected to reach USD 2.41 billion by 2030, registering a 6.41% CAGR through the forecast period. Demographic aging, ISO-10993–driven material mandates, and rapid advances in smart drug-delivery wearables keep demand resilient even as the sector matures. Broader healthcare digitization pulls silicone into applications that blend electronics with implant-safe polymers, while cost-competitive Asian production supports price stability for device makers. Moderate consolidation among upstream suppliers ensures consistent quality, yet specialist formulators push innovation in ultrathin films and 3-D-printed prosthetic components. These intersecting forces create headroom for both volume and value expansion across the medical grade silicone market.

Key Report Takeaways

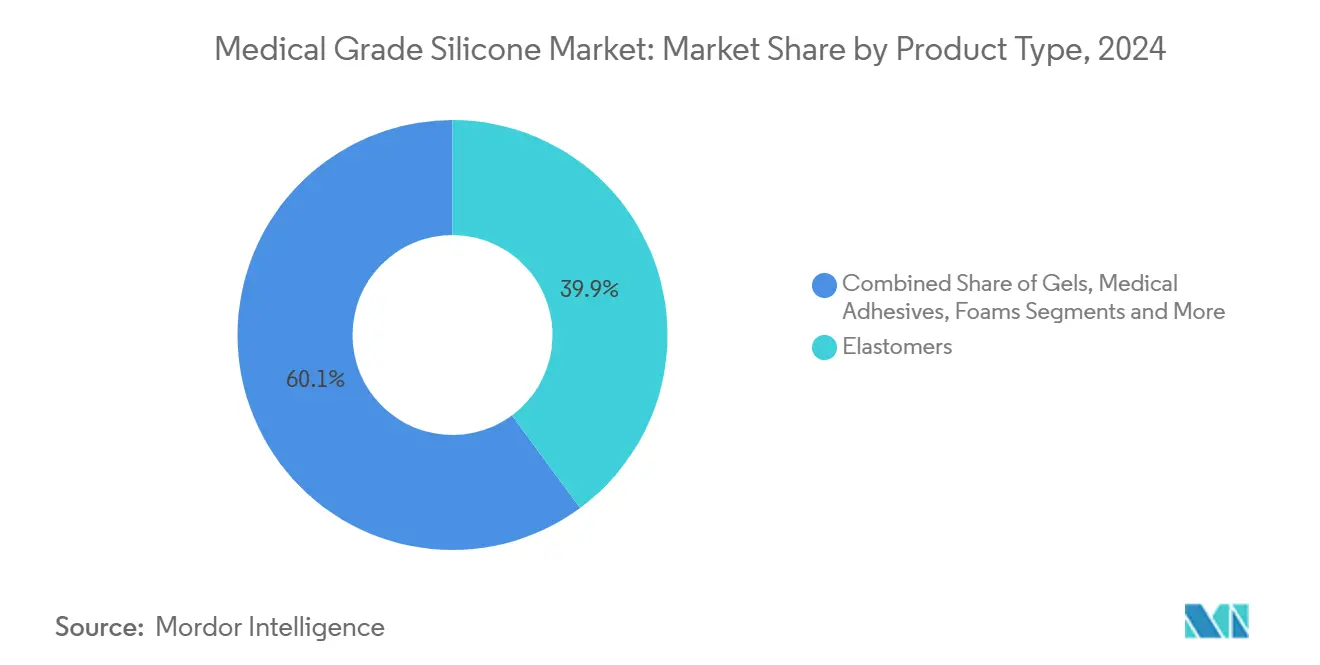

- By product type, elastomers led with 39.88% revenue share in 2024; medical adhesives are forecast to expand at a 9.37% CAGR through 2030.

- By form, liquid silicone rubber accounted for a 45.22% medical grade silicone market share in 2024, while silicone films are projected to rise at an 8.66% CAGR to 2030.

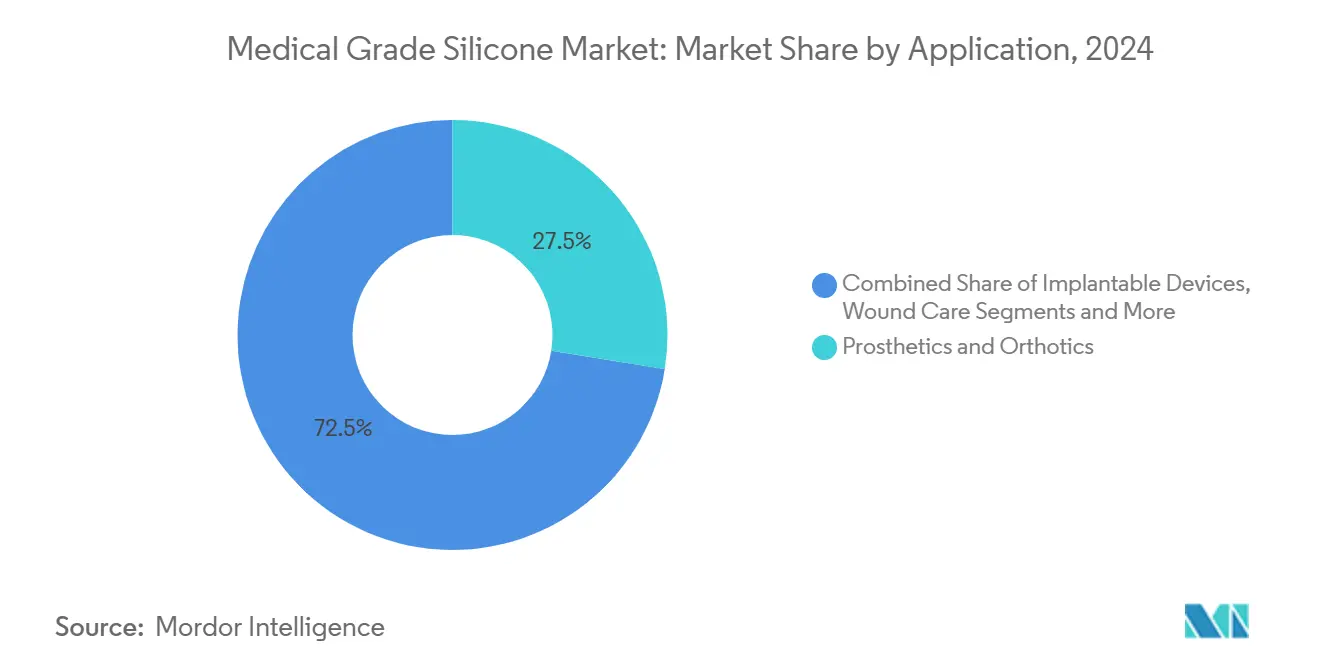

- By application, prosthetics & orthotics held 27.52% of the medical grade silicone market size in 2024; drug-delivery devices are advancing at a 10.38% CAGR through 2030.

- By end-user, medical device manufacturers commanded 39.83% share of the medical grade silicone market size in 2024, whereas OEM contract manufacturers record the highest projected CAGR at 9.21% to 2030.

- By geography, Asia-Pacific captured 41.22% of medical grade silicone market share in 2024 and is forecast to post an 8.77% CAGR through 2030.

Global Medical Grade Silicone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-population-led implant surge | +1.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Regulatory preference for ISO-10993 polymers | +1.2% | North America, Europe | Medium term (2-4 years) |

| Wearable microneedle drug-delivery advances | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Micro-fluidic diagnostics uptake | +0.7% | Global, Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Medical electronics encapsulation demand | +0.6% | Asia-Pacific core, spill-over to North America, EU | Short term (≤ 2 years) |

| 3-D-printed bespoke prosthetics | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Population-Led Implant Surge

Joint replacements, cardiac rhythm devices, and neurostimulators track the doubling of the 65-plus cohort by 2050, locking in long-run consumption of implant-grade elastomers.[1]International Organization for Standardization, “ISO/FDIS 10993-1:2025 Biological Evaluation of Medical Devices,” iso.org Medical grade silicone resists protein adsorption and minimizes foreign-body response, enabling performance spans measured in decades. Orthopedic trauma volumes tied to fragility fractures illustrate a demand curve largely insulated from macroeconomic shocks. Device designers increasingly integrate silicone with sensors and Bluetooth modules, turning once-passive implants into active therapeutics. These hybrid systems broaden revenue pools beyond the original implant sale. In turn, raw-material suppliers gain predictable offtake that encourages backward-integration strategies for siloxane feedstocks.

Regulatory Preference for ISO-10993 Compliant Polymers

The 2025 revision of ISO-10993-1 strengthens risk-based biological assessments, pushing manufacturers toward legacy materials that carry deep clinical dossiers.[2]International Organization for Standardization, “ISO 10993-18:2025 Chemical Characterization,” iso.org Medical grade silicone’s decades-long safety record lowers the cost and time needed to clear 510(k) or CE-mark filings. Revised ISO-10993-18 chemical-characterization rules reward materials with stable extractables profiles, a strong suit for cross-linked silicones. U.S. and EU regulators also intensify scrutiny on leachables from soft polymers, a domain where platinum-cured silicones outperform peroxide-cured alternatives. As compliance workloads climb, OEMs prefer suppliers offering audit-ready documentation, thereby reinforcing the medical grade silicone market’s attraction relative to newer thermoplastics.

Wearable Microneedle Drug-Delivery Breakthroughs

Electrically triggered microneedle patches fabricated from medical grade silicone films now deliver insulin and biologics with minute-level precision.[3]Y. Chen, “Digital Automation of Transdermal Drug Delivery with High Spatiotemporal Resolution,” Nature Communications, nature.com Multifunctional skin patches that monitor vitals and release therapeutics on demand forge a closed loop between diagnostics and therapy.[4]S. Lee, “Vialess Heterogeneous Skin Patch for Multimodal Monitoring and Stimulation,” Nature Communications, nature.com Silicone’s elasticity maintains skin conformity through thousands of flex cycles, preserving dose accuracy over chronic wear. Automated roll-to-roll production of microneedle arrays in Asia drives unit-cost compression and accelerates scale-up. Pharmaceutical firms, incentivized by patent-life extension strategies, back these delivery systems to refresh mature molecules. As a result, the medical grade silicone market captures value from both device hardware and drug partner revenues.

Micro-Fluidic Diagnostics Adopting Silicone

Polydimethylsiloxane (PDMS) is the workhorse for lab-on-chip devices that consolidate multiple assays on a credit-card-sized substrate. Optical clarity and oxygen permeability let reagents and cells interact as intended without surface fouling. Capillary-driven flow paths in PDMS eliminate external pumps, shrinking form factors for at-home test kits. Asia-Pacific molders leverage high-precision tooling to mass-produce disposable cartridges at competitive cost, reinforcing the region’s 41.22% market lead. Public-health agencies champion such diagnostics to decentralize screening for infectious diseases, a tailwind that funnels additional volume to medical grade silicone suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile siloxane monomer prices | -0.8% | Global, APAC production hubs | Short term (≤ 2 years) |

| Lengthy implant-grade material approvals | -0.6% | North America, Europe | Medium term (2-4 years) |

| TPE substitution in short-term devices | -0.5% | Cost-sensitive global applications | Medium term (2-4 years) |

| Platinum-catalyst environmental scrutiny | -0.3% | Europe primary, global ripple | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Siloxane Monomer Prices

Crude-oil swings echo quickly into siloxane feedstocks, compressing margins for converters that supply high-volume disposables. Manufacturers serving capped-price hospital tenders lack headroom to pass on surcharges, prompting inventory hedging that ties up working capital. Geographic clustering of monomer capacity in East Asia magnifies risk when outages strike, as witnessed during 2024 facility shutdowns tied to local energy rationing. Some suppliers pursue methane-to-silane pilot routes, yet commercial viability sits several years out. Until alternative feedstocks mature, raw-material volatility tempers near-term profitability in the medical grade silicone market.

Lengthy Implant-Grade Material Approvals

U.S. PMA or EU MDR filings trigger exhaustive material dossiers, extending commercialization cycles for novel silicone grades. Prototype iterations must remain compositionally static throughout trials, curbing rapid optimization. Small innovators often lack resources for three-year biocompatibility programs, deterring entry and holding back niche application growth. Regulatory harmonization efforts promise relief but will not materially truncate timelines before the latter half of the decade. Consequently, adoption curves for breakthrough grades flatten, marginally shaving growth off the overall medical grade silicone market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Elastomers Retain Command as Adhesives Accelerate

Elastomers generated USD 0.71 billion in 2024, equal to 39.88% of the medical grade silicone market size, underpinned by their unmatched combination of elongation, tear strength, and implant safety. Medical adhesives, though starting from a smaller base, achieved 9.37% CAGR, the highest within this segmentation, propelled by wear-friendly wound dressings and transdermal patches that require gentle yet secure bonding to fragile skin. Across device classes, formulators exploit elastomer resilience for sealing heart-pump housings, cushioning prosthetic sockets, and insulating neuromodulation leads, anchoring their dominance in value terms.

A parallel innovation storyline unfolds in adhesives. Hybrid silicone-acrylate systems deliver moisture-vapor transmission rates suitable for multi-day wear while avoiding epidermal stripping—a critical patient-comfort metric. Pharmaceutical partnerships funnel R&D dollars into drug-eluting adhesive matrices, aligning the segment with burgeoning digital-health ecosystems. Gels, foams, and fluids round out the product-type landscape, serving niches such as ostomy rings, negative-pressure wound-therapy pads, and sterile lubricants. Competitive intensity grows as specialty chemical firms try to capture formulary positions inside OEM approved-supplier lists, yet elastomers’ incumbency shields share against rapid erosion.

By Form: LSR Dominates, Silicone Films Stretch Growth Frontiers

Liquid silicone rubber contributed 45.22% to 2024 revenue, translating to the single largest slice of medical grade silicone market share. Automated high-cavitation molding lines run LSR at cycle times under 15 seconds, ideal for syringe plungers and valve components that must meet tight dimensional tolerances. In contrast, silicone films, though representing a modest value presently, pace the field with an 8.66% CAGR to 2030. Sub-100-micron continuous-casting processes yield roll goods that integrate seamlessly into stretchable circuit assemblies for biosensing wearables.

High consistency rubber remains relevant where mechanical load cycles exceed 1 million, such as orthopedic implant sleeves. Room-temperature-vulcanizing grades address in-situ sealing for imaging probes and hospital equipment where heat-curing would damage electronics. Silicone gels support shock-absorption inserts in breast prostheses and pediatric orthotics. Collectively, form-factor diversity enables the medical grade silicone market to penetrate an ever-wider matrix of end-use scenarios, from hospital consumables to at-home therapy devices.

By Application: Drug-Delivery Devices Lap Traditional Segments

Drug-delivery devices are set to increase their share of the medical-grade silicone market at a 10.38% CAGR. Microneedle arrays, osmotic pumps, and refillable subcutaneous depots thrive on silicone’s permeability control, ensuring steady pharmacokinetic profiles. Conversely, prosthetics and orthotics secured a 27.52% revenue share in 2024 due to volume demand for limb-replacement liners and exoskeletal cushioning. The steady aging trend guarantees baseline growth, yet value migration favors active therapeutic systems that intertwine with digital adherence platforms.

Implantable cardiac and neuro devices leverage silicone for hermetic lead insulation, while wound-care dressings use soft-tack silicones to avert skin maceration. Wearable monitors integrate silicone housings that survive repeated disinfection without leaching additives. Dental and ophthalmic uses extend the material’s reach but contribute smaller revenue fractions. The application mosaic underscores how the medical grade silicone market derives resilience from multiple growth vectors rather than any single blockbuster.

By End-User: OEM Contract Manufacturing Gains Momentum

Medical device manufacturers still purchased 39.83% of 2024 value, yet OEM contract manufacturers chart the briskest expansion at 9.21% CAGR as value-chain specialization deepens. Brand owners outsource molding, clean-room assembly, and sterilization to partners possessing ISO 13485 certification and domain expertise in silicone processing. Hospitals and clinics buy finished consumables rather than raw materials, so their role materializes indirectly through demand pull. Pharmaceutical companies emerge as a high-growth buyer group for combination-product platforms, commissioning silicone reservoirs and septa designed for controlled drug release.

Academic research institutes, though contributing marginal revenue, form an innovation incubator that spins prototypes into commercial pipelines. Over the forecast horizon, capacity investments from Asian contract manufacturers are set to elevate their sourcing influence, reinforcing Asia-Pacific’s supremacy within the medical grade silicone market.

Geography Analysis

Asia-Pacific held 41.22% of 2024 revenue and will post an 8.77% CAGR through 2030, driven by integrated chemical clusters in China and South Korea that supply feedstock and finished elastomers within a single economic zone. Aging demographics in Japan and mainland China expand implant volumes, while Southeast Asian economies ramp healthcare spending and local assembly of dialysis consumables. Policy incentives—such as China’s volume-based procurement for cardiovascular stents—favor materials with proven biocompatibility, sustaining the medical grade silicone market across the region.

North America retains its position as innovation crucible, hosting R&D hubs that pioneer additive-manufactured silicone valves and neuromodulation devices. Stringent FDA 510(k) pathways lengthen entry cycles but ensure stable demand for legacy-qualified grades, insulating suppliers from rapid substitutions. The United States accounts for over 85% of regional expenditure, supported by high per-capita orthopedic procedure rates and rapid uptake of closed-loop insulin pumps that depend on silicone membranes for sensor isolation. Canada complements with specialty contract-manufacturing clusters focusing on catheter extrusion and silicone-film coating.

Europe contributes balanced growth, underpinned by Germany’s export-oriented medtech sector and Scandinavia’s early adoption of remote-patient-monitoring wearables. Environmental scrutiny intensifies focus on platinum-recovery schemes and silicone recycling, nudging OEMs toward suppliers that can document cradle-to-grave stewardship. Despite higher energy costs, established quality infrastructures and workforce skillsets maintain Europe’s relevance in high-precision molding and specialty formulation. Collectively, the triad of Asia-Pacific, North America, and Europe underwrites more than 90% of the medical grade silicone market, anchoring global supply resilience.

Competitive Landscape

The market exhibits a moderate concentration index, with Dow, Wacker Chemie, Elkem, and Shin-Etsu collectively controlling roughly 55% of global capacity. Vertical integration from siloxane monomer through compounded elastomer affords these incumbents leverage in price negotiations and supply assurance. Dow highlights continuous-flow hydrosilylation reactors that trim catalyst consumption and carbon footprint, aligning material innovation with ESG imperatives. Wacker Chemie’s 2025 strategy centers on specialty silicones that command premium pricing, evidenced by new Q- and H-silane lines in Zhangjiagang and Tsukuba.

Meanwhile, niche challengers exploit additive manufacturing and micro-fluidics to erode share at the application edge. Stratasys’ launch of P3 Silicone 25A opens photopolymerizable pathways that incumbents did not previously supply, signaling a pivot toward digital production workflows. Start-ups specializing in platinum-recovery catalysts promise to trim environmental compliance costs, an angle that could reconfigure supply-chain partnerships. Patent filings in self-healing silicones and low-Pt hydrosilylation inferred from Industrial & Engineering Chemistry Research journals reflect ongoing core-chemistry races.

Pricing discipline remains intact because capacity additions lag demand growth, yet the mix shift toward high-functionality grades lifts average selling prices. Contract manufacturers deepen ties with material suppliers through exclusive formulation agreements that lock in seven-year supply windows. Taken together, competitive dynamics favor players combining feedstock control, application engineering depth, and regulatory dossier support—traits that help them capture outsized value from the expanding medical grade silicone market.

Medical Grade Silicone Industry Leaders

Dow Inc.

Wacker Chemie AG

Elkem ASA

Avantor, Inc.

Momentive Performance Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Stratasys Ltd. unveiled P3 Silicone 25A for its Origin platform, enabling production-grade flexible parts that mirror traditionally molded silicone.

- May 2025: Wacker completed mechanical construction of new Zhangjiagang facilities slated to add silicone fluids, emulsions, and elastomer gels production.

- January 2025: Wacker Chemie AG commissioned specialty silicone plants in Tsukuba, Japan, and Jincheon, South Korea, to meet rising regional demand.

Global Medical Grade Silicone Market Report Scope

| Elastomers |

| Gels |

| Medical Adhesives |

| Medical Coatings |

| Foams |

| Fluids & Oils |

| Liquid Silicone Rubber (LSR) |

| High Consistency Rubber (HCR) |

| Room-Temperature Vulcanizing (RTV) |

| Silicone Films |

| Silicone Gels |

| Prosthetics & Orthotics |

| Implantable Devices |

| Drug-Delivery Devices |

| Wearable/Monitoring Devices |

| Wound Care |

| Surgical Instruments & Tools |

| Diagnostics & IVD |

| Contact Lenses & Eye-Care |

| Dental |

| Medical Device Manufacturers |

| Hospitals & Clinics |

| Pharmaceutical Companies |

| OEM Contract Manufacturers |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Elastomers | |

| Gels | ||

| Medical Adhesives | ||

| Medical Coatings | ||

| Foams | ||

| Fluids & Oils | ||

| By Form | Liquid Silicone Rubber (LSR) | |

| High Consistency Rubber (HCR) | ||

| Room-Temperature Vulcanizing (RTV) | ||

| Silicone Films | ||

| Silicone Gels | ||

| By Application | Prosthetics & Orthotics | |

| Implantable Devices | ||

| Drug-Delivery Devices | ||

| Wearable/Monitoring Devices | ||

| Wound Care | ||

| Surgical Instruments & Tools | ||

| Diagnostics & IVD | ||

| Contact Lenses & Eye-Care | ||

| Dental | ||

| By End-User | Medical Device Manufacturers | |

| Hospitals & Clinics | ||

| Pharmaceutical Companies | ||

| OEM Contract Manufacturers | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the medical grade silicone market in 2025?

The medical grade silicone market size is USD 1.77 billion in 2025, and it is forecast to climb to USD 2.41 billion by 2030.

What CAGR is projected for medical grade silicone from 2025 to 2030?

The market is expected to expand at a 6.41% CAGR during the forecast window.

Which region leads demand for medical grade silicone?

Asia-Pacific holds 41.22% market share and is also the fastest-growing region, supported by 8.77% CAGR.

Which application segment is growing quickest?

Drug-delivery devices show the highest growth, advancing at a 10.38% CAGR through 2030 thanks to microneedle patches and implantable pumps.

Who are the major suppliers of medical grade silicone?

Key players include Dow, Wacker Chemie, Elkem, and Shin-Etsu, which together control over half of global capacity.

Page last updated on: