Nuclear Medicine Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

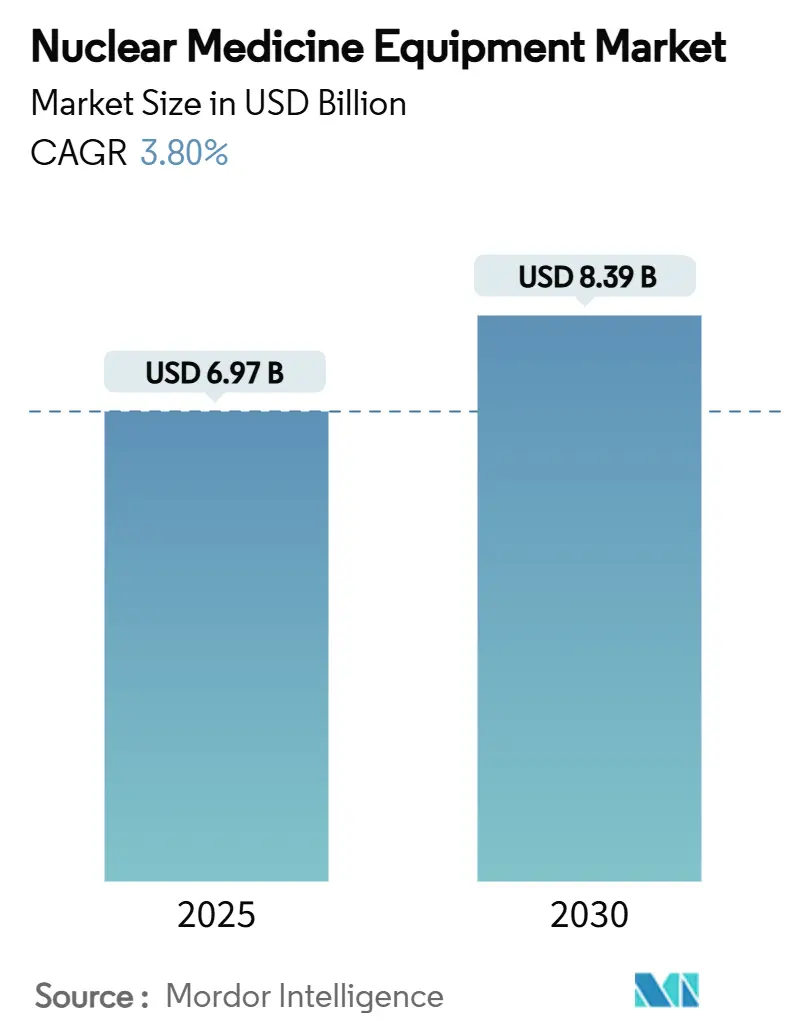

| Market Size (2025) | USD 6.97 Billion |

| Market Size (2030) | USD 8.39 Billion |

| Growth Rate (2025 - 2030) | 3.80% CAGR |

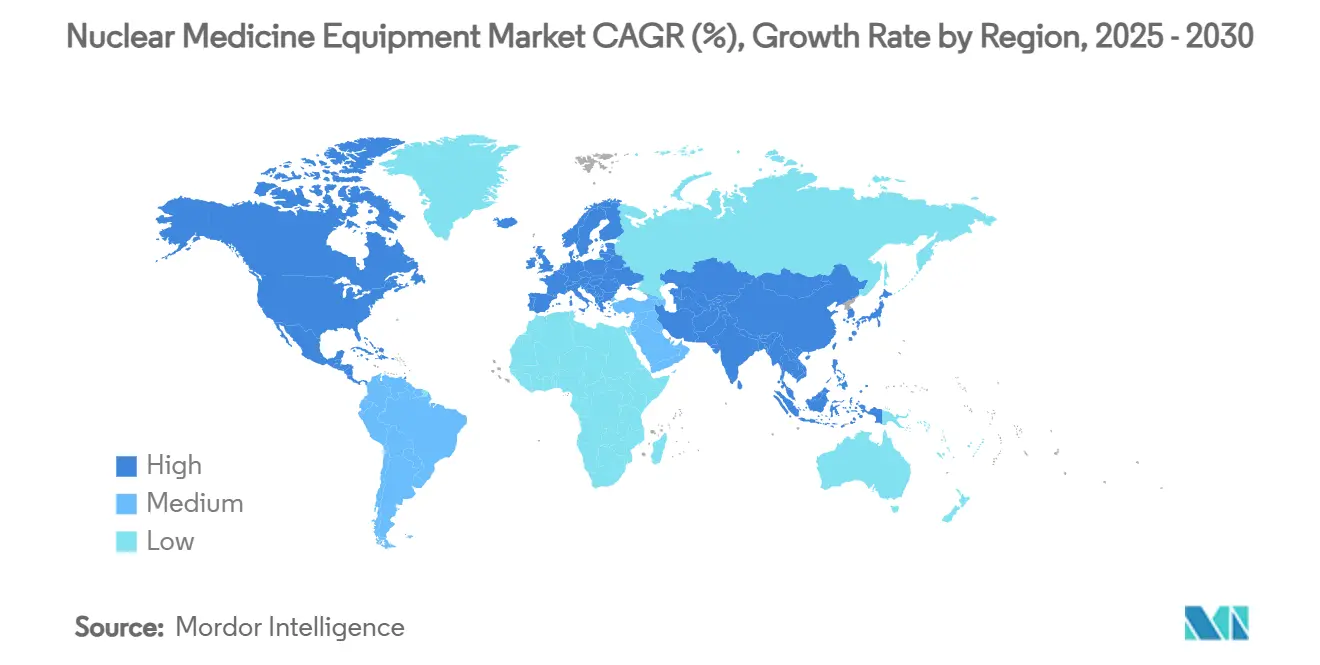

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nuclear Medicine Equipment Market Analysis by Mordor Intelligence

The nuclear medicine equipment market size reached USD 6.97 billion in 2025 and is expected to register a 3.80% CAGR, attaining USD 8.39 billion by 2030. Demand rises as molecular diagnostics become central to oncology and cardiology care, and as hybrid scanners blend anatomical and functional data in a single session. Regulatory changes accelerate this trend, most notably the 2025 US rule that grants separate payments for high-cost radiopharmaceuticals, thereby ending a long-standing bundling constraint. Hospital systems are renewing their fleets to reduce scan times and radiation doses, while governments invest in isotope production to secure supply chains after the 2024 Mo-99 shortfall. Workforce shortages and high equipment prices counterbalance momentum, yet the nuclear medicine equipment market continues to expand because clinicians view molecular imaging as vital infrastructure rather than a discretionary service.

Key Report Takeaways

- By product type, SPECT systems led with 52.3% revenue share in 2024; hybrid PET/CT is forecast to expand at a 7.9% CAGR through 2030.

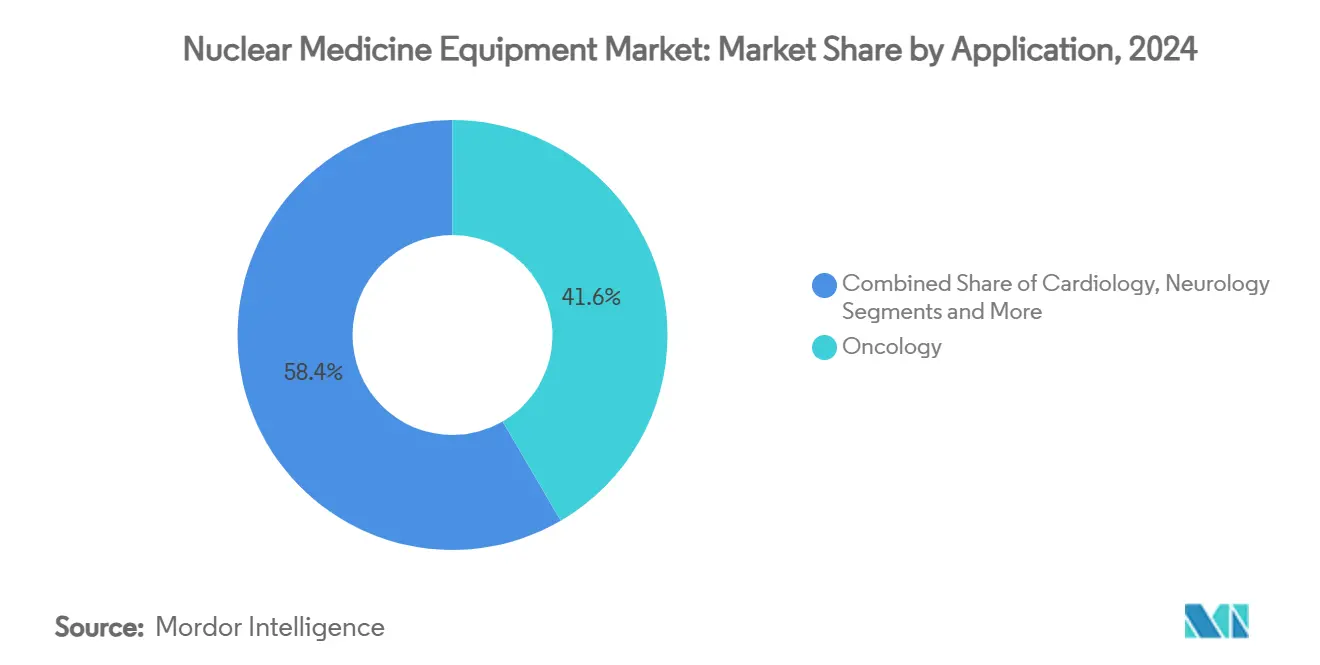

- By application, oncology accounted for a 41.6% share of the nuclear medicine equipment market in 2024, and neurology is projected to advance at a 9.4% CAGR through 2030.

- By end user, hospitals commanded a 62.5% share in 2024, and specialty clinics are projected to grow at an 8.6% CAGR through 2030.

- By detector technology, NaI cameras held a 68.1% share in 2024, whereas CZT systems are projected to grow at a 12.8% CAGR through 2030.

- By geography, North America held a 34.7% share of the nuclear medicine equipment market in 2024, while the Asia Pacific is projected to post the fastest CAGR of 7.2% from 2024 to 2030.

Global Nuclear Medicine Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of oncology & cardiology cases | +1.20% | North America, Europe, developed Asia | Long term (≥ 4 years) |

| Rapid adoption of hybrid PET/CT & SPECT/CT scanners | +0.80% | North America, EU, expanding in APAC | Medium term (2-4 years) |

| Reimbursement expansion for molecular imaging in OECD | +0.60% | United States and European health systems | Short term (≤ 2 years) |

| Government isotope-production investments | +0.40% | United States with global spillover | Medium term (2-4 years) |

| Commercial rollout of CZT digital SPECT cameras | +0.30% | Technologically advanced markets worldwide | Medium term (2-4 years) |

| Long-axial FOV PET/CT enabling ultra-low-dose workflows | +0.20% | Initially major research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Oncology & Cardiology Cases

Cancer incidence is projected to climb 47% by 2050, pushing clinicians toward molecular techniques that can track tiny treatment responses undetectable on CT or MR.[1]Society of Nuclear Medicine and Molecular Imaging, “CMS Adjusts Nuclear Medicine Reimbursement Policy,” snmmi.org The 2024 FDA nod for flurpiridaz F-18 now lets care teams perform stress PET studies with higher accuracy and lower isotope decay risk, expanding nuclear cardiology reach. Because aging populations drive both cancer and coronary disease, hospitals upgrade tracer inventories and schedule additional imaging slots to keep pace with combined oncology and cardiology demand. PET-based perfusion studies, though costlier than SPECT, gain favor as evidence mounts for better outcomes in complex coronary artery disease. Consequently, long-term procedure volume growth remains resilient regardless of short-term macroeconomic swings, reinforcing the nuclear medicine equipment market as an essential service.

Rapid Adoption of Hybrid PET/CT & SPECT/CT Scanners

Hybrid scanners fuse metabolic and anatomical data in one acquisition, eliminating registration errors and halving patient throughput time. The Biograph Trinion PET/CT, cleared in 2024, illustrates this shift with air-cooled detectors that cut power use by 46% while delivering 239-ps time-of-flight performance. Health systems view these gains as strategic because faster scans increase daily capacity without expanding staff, a critical benefit in tight labor markets. Hybrid systems also simplify reporting by synchronizing voxel-level anatomical landmarks with tracer uptake, improving diagnostic confidence in oncology staging and therapy monitoring. Long axial FOV designs, such as the uEXPLORER, cover the entire body in under 60 seconds and reduce radiopharmaceutical dose by more than 80%. These operational and clinical advantages position hybrid platforms as the growth engine of the nuclear medicine equipment market.

Reimbursement Expansion for Molecular Imaging in OECD

The 2025 CMS rule finally decouples radiopharmaceuticals priced above USD 630 from packaged imaging payments, removing the financial penalty that curtailed PET adoption in community sites. High-value agents like piflufolastat F-18 for prostate cancer can now reach more patients because hospitals are reimbursed for both the scan and the tracer. Parallel reforms are moving through European systems, with NICE expanding coverage for amyloid and PSMA imaging in 2024. These policy shifts create a feedback loop: broader access yields richer clinical datasets, which in turn support further guideline inclusion. As payers accept molecular imaging’s cost–benefit balance, procedure volumes in mid-tier hospitals rise, pushing the nuclear medicine equipment market toward wider geographic diffusion.

Government Isotope-Production Investments

Mo-99 shortages in late 2024 exposed the fragility of aging reactors and triggered significant funding for domestic production. SHINE Technologies secured USD 50 million to finish the Chrysalis plant, forecast to supply more than one-third of global Mo-99 from US soil. Legislators see isotope independence as both a public-health and national-security goal, channeling grants and tax credits into low-enriched-uranium processes that lower proliferation risk. Domestic output stabilizes tracer availability, giving hospitals confidence to expand nuclear medicine programs without fear of supply interruptions. The same facilities will also generate lutetium-177 for theranostic agents, aligning with the nuclear medicine equipment market’s trend toward combined diagnostic and therapeutic workflows.

Commercial Rollout of CZT Digital SPECT Cameras

CZT detectors convert gamma photons directly to charge, boosting energy resolution and quadrupling count sensitivity compared with conventional NaI crystals. Clinical trials show a 64.3% normal scan classification rate for cardiac studies against 28.6% on legacy systems.[2]Gytis Aleksa, “Comparative Analysis of Cardiac SPECT Myocardial Perfusion Imaging: Full-Ring Solid-State Detectors Versus Dedicated Cardiac Fixed-Angle Gamma Camera,” Medicina, mdpi.com Lower dose requirements and ten-minute scan times meet value-based care goals, while compact gantries fit older suites without major construction. As unit costs fall, mid-size hospitals purchase CZT cameras for coronary artery disease evaluation, migrating some volume from PET in resource-constrained settings. Vendor partnerships, such as Spectrum Dynamics with Hermes Medical Solutions, couple hardware with AI-enhanced software to streamline post-processing. These collaborative ecosystems reinforce the appeal of digital SPECT and propel segment growth inside the broader nuclear medicine equipment market.

Long-Axial FOV PET/CT Enabling Ultra-Low-Dose Workflows

Total-body PET/CT systems extend axial coverage past 180 cm, allowing a single continuous bed motion that captures dynamic tracer kinetics across all organs. Researchers can now study whole-body pharmacokinetics with femto-mol sensitivity using just a fraction of traditional doses, which proves invaluable for pediatrics and longitudinal drug trials. Early adopters include academic centers that leverage ultra-low-dose protocols to broaden study enrollment without the ethical concerns associated with high radiation. Over time, as capital costs decline and reimbursement codes align, community cancer centers are expected to adopt these scanners for routine staging. The technology’s capacity for unprecedented temporal resolution positions it as a future standard, establishing another platform for revenue acceleration in the nuclear medicine equipment market.

Restraints Impact Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & service contracts for scanners | -0.70% | Worldwide, most acute in emerging economies | Long term (≥ 4 years) |

| Supply-chain fragility of short-lived radio-isotopes | -0.50% | Global with single-source dependencies | Short term (≤ 2 years) |

| Tightening radioactive-waste disposal regulations | -0.30% | Primarily developed markets | Medium term (2-4 years) |

| Shortage of certified nuclear-medicine technologists | -0.40% | North America, Europe, developed Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Service Contracts for Scanners

A state-of-the-art PET/CT can cost USD 2-4 million, and annual service fees often reach 10% of the purchase price, straining the budgets of smaller hospitals. Required shielding, HVAC upgrades, and IT interfaces double project outlays, making return-on-investment calculations difficult. Financing models are evolving; Positron’s rental plan for the NeuSight PET-CT reduces upfront cash yet still locks providers into long service terms. Complex software stacks require vendor engineers for routine updates, and downtime penalties cut into margins. These realities slow penetration in mid-income nations, tempering overall growth in the nuclear medicine equipment market.

Supply-Chain Fragility of Short-Lived Radio-Isotopes

The October 2024 reactor delay in Europe reduced Mo-99 exports and left clinics scrambling for Tc-99m doses, illustrating the vulnerability of just-in-time isotope logistics. Because Mo-99’s 66-hour half-life prevents stockpiling, any transport hiccup cancels patient appointments within days. Cargo flight delays, customs hold-ups, and weather disruptions compound risk. Alternative production via cyclotrons or linear accelerators remains years from large-scale viability. Until redundancy improves, supply shocks periodically curtail scan volumes and dampen confidence in the nuclear medicine equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Systems Outpace Legacy Modalities

SPECT scanners accounted for 52.3% of revenue in 2024, as they remain affordable and reliable for routine cardiac and bone studies. Hybrid PET/CT systems, on the other hand, are expected to expand at a 7.9% CAGR as clinicians prioritize precision diagnostics. The nuclear medicine equipment market benefits from hybrid devices, which elevate clinical confidence while optimizing workflow. Advances such as AI-assisted protocol selection and iterative reconstruction increase sensitivity while reducing doses, thereby reinforcing demand. In a parallel trend, planar cameras remain steady for thyroid and sentinel-node imaging, although their share declines as 3-D modalities proliferate.

Across the forecast, vendors embed digital detectors and cloud-enabled analytics into all scanner classes. GE HealthCare’s launch of the flurpiridaz-compatible PET protocol in 2025 prompts mid-tier hospitals to add PET suites, boosting the nuclear medicine equipment market size for high-resolution cardiac imaging. Long-axial-FOV PET/CT systems extend use cases to dynamic tracer studies and whole-body dosimetry, capturing new research budgets and increasing revenue diversity.

By Detector Technology: Digital Transition Gains Pace

NaI Anger cameras delivered 68.1% of 2024 shipments, reflecting decades of a large installed base and a low unit price. Yet CZT technology is advancing at a 12.8% CAGR and increasingly captures replacement cycles. Providers adopt CZT because higher energy resolution distinguishes overlapping isotopes in dual-isotope protocols, enhancing cardiac diagnostics. SiPM-based PET detectors also see rising orders for their picosecond timing, which sharpens image quality. Analog PMT configurations remain prevalent in cost-sensitive settings, helping to sustain baseline volume in the nuclear medicine equipment market.

Clinical trials underline CZT superiority, especially in coronary perfusion, where count sensitivity directly informs treatment plans. Declining semiconductor costs and multi-vendor competition compress prices, widening access. Ongoing R&D into CdTe and HgI₂ substrates suggests further improvements in resolution. Integration with AI-powered denoising software means future systems deliver higher clarity at lower administered doses, solidifying the digital transition within the nuclear medicine equipment market.

By Application: Oncology Dominates While Neurology Accelerates

Oncology held a 41.6% share in 2024 as precision medicine protocols rely on PET tracers for tumor characterization and therapy monitoring. The introduction of PSMA agents and total-body PET scanning widens clinical staging capabilities. Neurology is projected to grow at a 9.4% CAGR, propelled by amyloid and tau imaging for Alzheimer’s research and evolving reimbursement in memory clinics. Cardiology remains central thanks to perfusion studies that guide revascularization decisions, although some volume migrates to cardiac CT in low-risk cohorts.

Theranostic pathways blend imaging with targeted therapy, deepening oncology’s revenue stream in the nuclear medicine equipment market. Agents such as lutetium-177 PSMA provide both diagnostic scans and therapeutic doses, creating cyclical imaging demand through treatment courses. In neurology, Lantheus’ acquisition of NAV-4694 propels beta-amyloid detection into community settings, expanding scan volumes beyond academic centers. The combination of aging demographics and tracer innovation ensures sustained multi-segment growth.

By End User: Hospitals Lead but Outpatient Centers Surge

Hospitals accounted for 62.5% of scans in 2024 owing to comprehensive infrastructure, emergency capacity, and oncology programs. Specialty clinics, however, are expected to grow at an 8.6% CAGR because payers favor outpatient sites for cost control. Diagnostic imaging centers optimize scheduling and staffing to maximize scanner utilization, reducing per-scan cost. Academic facilities remain innovation hubs where new tracers and ultra-low-dose protocols enter practice, seeding future demand across the nuclear medicine equipment market.

Mobile units bridge rural gaps by transporting SPECT or PET systems on scheduled routes, thereby broadening geographic access without requiring permanent installations. The growth of freestanding theranostic centers highlights a shift toward integrated care models, where imaging and therapy converge under one roof. These facilities rely on a consistent isotope supply and specialized staff, reinforcing both supply-chain and workforce priorities in the nuclear medicine equipment market.

Geography Analysis

North America generated 34.7% of 2024 revenue following the implementation of CMS reimbursement reform and ongoing research funding, which accelerated equipment renewals. Providers in the United States quickly integrate AI tools to streamline protocol selection, while Canadian hospitals invest in cyclotrons to achieve self-reliance in isotope production. Mexico upgrades imaging fleets in metropolitan areas to attract medical tourists, adding incremental volumes.

Europe ranks second in market size, anchored by Germany’s university-hospital network and the Netherlands’ isotope reactors. However, the 2024 Mo-99 shortage exposed reliance on single reactors and spurred EU grants for diversified production. The United Kingdom’s NHS embeds molecular imaging pathways in national cancer plans, stabilizing procedure volumes even during fiscal tightening. Central and Eastern European nations are experiencing double-digit growth as they modernize their diagnostic infrastructure, thereby generating new demand for nuclear medicine equipment.

The Asia Pacific is the fastest-growing region, with a 7.2% CAGR, driven by rising chronic disease incidence and government capacity-building programs. China operates more than 1,200 nuclear medicine sites serving millions of patients each year.[3]Journal of Nuclear Medicine, “Cardiac CZT SPECT Comparative Study,” jnm.snmjournals.org Japan’s mature ecosystem now benefits from GE HealthCare’s acquisition of Nihon Medi-Physics, which secures domestic tracer supply. India scales PET-CT capacity in tier-two cities, and Australia backs theranostic trials targeting rare cancers. These initiatives compound into robust regional momentum for the nuclear medicine equipment market.

Competitive Landscape

The vendor field features moderate concentration as top makers fold radiopharmaceutical partners into corporate structures. GE HealthCare’s USD 183 million purchase of Nihon Medi-Physics ensures control over Asian supply chains and supports growth in the nuclear medicine equipment market. Siemens Healthineers allocates a multi-year innovation budget exceeding USD 27 billion, underscoring its commitment to hybrid and AI integration. Canon Medical collaborates with Hermes to expand its software portfolios, while Curium’s acquisition of Monrol enhances lutetium-177 capacity across Europe.

Smaller firms carve niches. Positron focuses on lower-cost PET scanners, bundled with rental financing, to fill gaps where capital budgets are tight. Spectrum Dynamics leverages CZT expertise to challenge incumbents in cardiac SPECT. United Imaging exploits total-body PET/CT differentiation to win flagship projects at research hospitals. Competitive dynamics thus hinge on vertical integration, digital detector advances, and service ecosystems rather than headline hardware pricing, shaping sustainable advantage in the nuclear medicine equipment market.

Service sophistication is a new battleground. Multi-year enterprise agreements, such as the 2025 Sutter Health–GE partnership, span more than 300 facilities and include AI, training, and uptime guarantees. These contracts lock in brand loyalty while providing predictable revenue streams that cushion cyclical equipment sales. As more providers demand turnkey solutions, ecosystem-oriented vendors strengthen their position in the nuclear medicine equipment market.

Nuclear Medicine Equipment Industry Leaders

GE HealthCare

Siemens Healthineers

Philips Healthcare

Canon Medical Systems

Shimadzu Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare completed its USD 183 million purchase of Nihon Medi-Physics, fortifying the Asian radiopharmaceutical supply.

- March 2025: Curium finalized the acquisition of Monrol, boosting lutetium-177 output and PET footprint in Europe and the Middle East.

- February 2025: Positron secured multi-scanner agreements for the NeuSight PET-CT under its prime rental model.

- January 2025: Sutter Health and GE HealthCare announced a seven-year strategic partnership to deploy AI-powered imaging across more than 300 facilities.

Global Nuclear Medicine Equipment Market Report Scope

| SPECT Systems |

| Hybrid SPECT/CT Systems |

| PET Systems |

| Hybrid PET/CT Systems |

| Planar Scintigraphy Cameras |

| NaI Scintillation (Anger) Cameras |

| CZT Digital SPECT Cameras |

| SiPM-Based PET Detectors |

| Analog PMT PET Detectors |

| Others (CdTe, HgI?) |

| Oncology |

| Cardiology |

| Neurology |

| Orthopedics & Musculoskeletal |

| Other Clinical Areas |

| Hospitals |

| Diagnostic Imaging Centers |

| Academic & Research Institutes |

| Specialty Clinics |

| Mobile Imaging Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | SPECT Systems | |

| Hybrid SPECT/CT Systems | ||

| PET Systems | ||

| Hybrid PET/CT Systems | ||

| Planar Scintigraphy Cameras | ||

| By Detector Technology | NaI Scintillation (Anger) Cameras | |

| CZT Digital SPECT Cameras | ||

| SiPM-Based PET Detectors | ||

| Analog PMT PET Detectors | ||

| Others (CdTe, HgI?) | ||

| By Application | Oncology | |

| Cardiology | ||

| Neurology | ||

| Orthopedics & Musculoskeletal | ||

| Other Clinical Areas | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Academic & Research Institutes | ||

| Specialty Clinics | ||

| Mobile Imaging Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the nuclear medicine equipment market?

The nuclear medicine equipment market size was USD 6.97 billion in 2025 and is projected to reach USD 8.39 billion by 2030.

Which product type leads the market in revenue?

SPECT systems led with 52.3% revenue share in 2024, reflecting their entrenched role in routine diagnostics.

Why is Asia Pacific the fastest-growing region?

Asia Pacific posts a 7.2% CAGR through 2030 because governments are investing heavily in imaging infrastructure and the region’s aging population drives higher demand for oncology and cardiology diagnostics.

How will new reimbursement policies affect market growth?

The 2025 US rule that separates payment for high-cost radiopharmaceuticals removes a financial barrier, enabling wider PET adoption and accelerating overall procedure growth.

What technological development is most disruptive?

CZT digital SPECT cameras and long-axial-FOV PET/CT scanners are reshaping workflows by providing higher sensitivity, lower dose and faster acquisitions.

What limits market expansion despite rising demand?

High capital costs, isotope supply fragility and a shortage of certified technologists remain the primary brakes on rapid adoption.

Page last updated on: