Plasma Sterilizers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

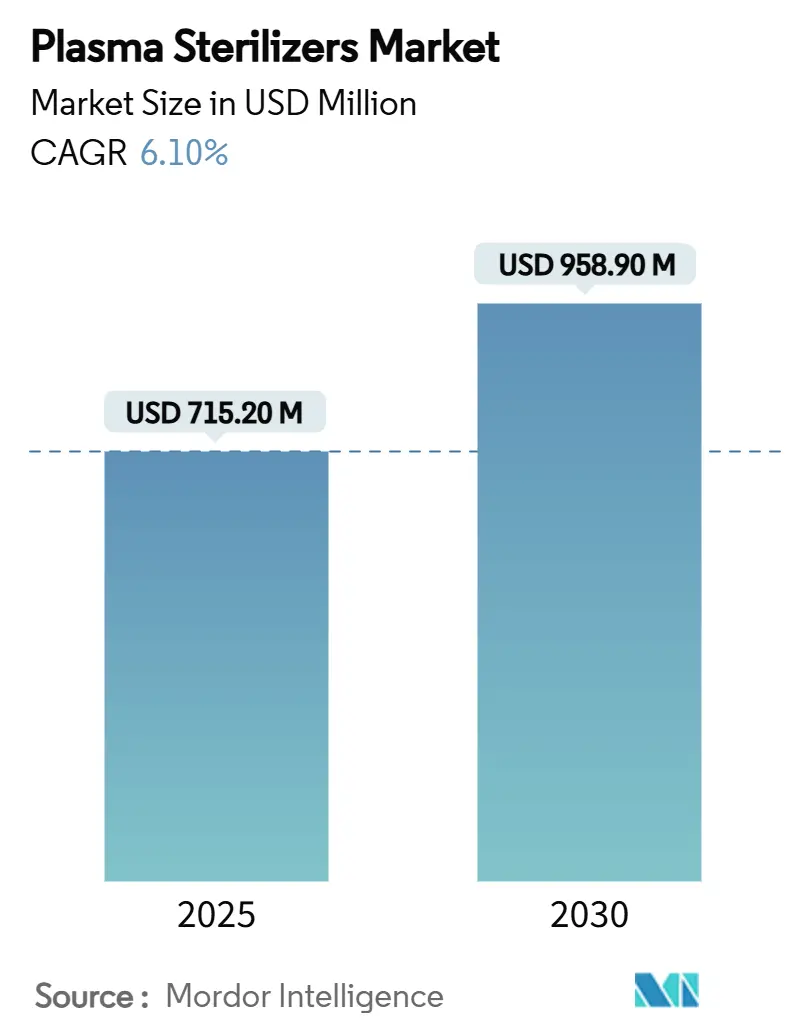

| Market Size (2025) | USD 715.20 Million |

| Market Size (2030) | USD 958.90 Million |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

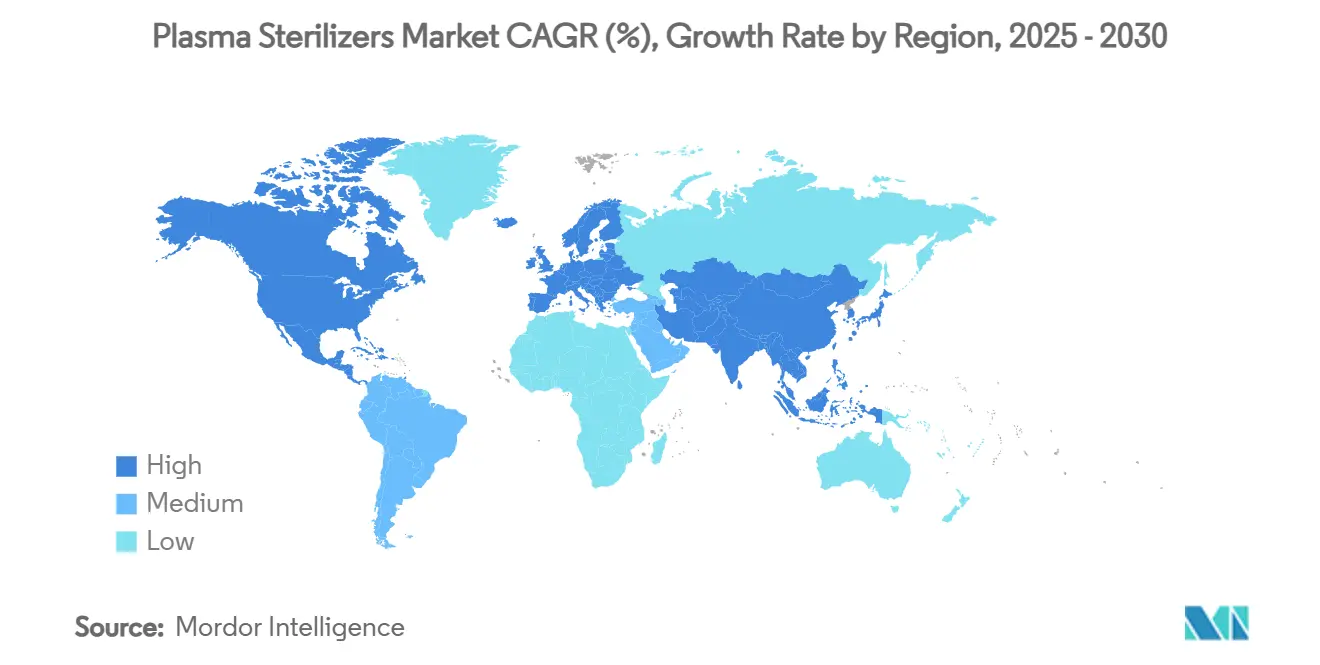

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasma Sterilizers Market Analysis by Mordor Intelligence

The plasma sterilizers market size is valued at USD 715.2 million in 2025 and is forecast to reach USD 958.9 million by 2030, advancing at a 6.10% CAGR over the period. Heightened regulatory focus on ethylene-oxide emissions, the FDA’s 2024 recognition of vaporized hydrogen peroxide as a Category A method, and the rising incidence of healthcare-associated infections are steering hospitals and device makers toward low-temperature hydrogen-peroxide gas plasma systems. Adoption is bolstered by proven sterility assurance for narrow-lumen and polymer devices, shorter turnaround versus ethylene oxide, and the technology’s benign by-products of water and oxygen. Strategic acquisitions by leading vendors are sharpening service portfolios, while contract sterilizers scale multi-modality hubs to meet OEM outsourcing demand. Robust investments in mid-range (100-300 L) chambers, which balance throughput and footprint, underscore the market’s shift toward decentralized sterile processing in ambulatory settings.

Key Report Takeaways

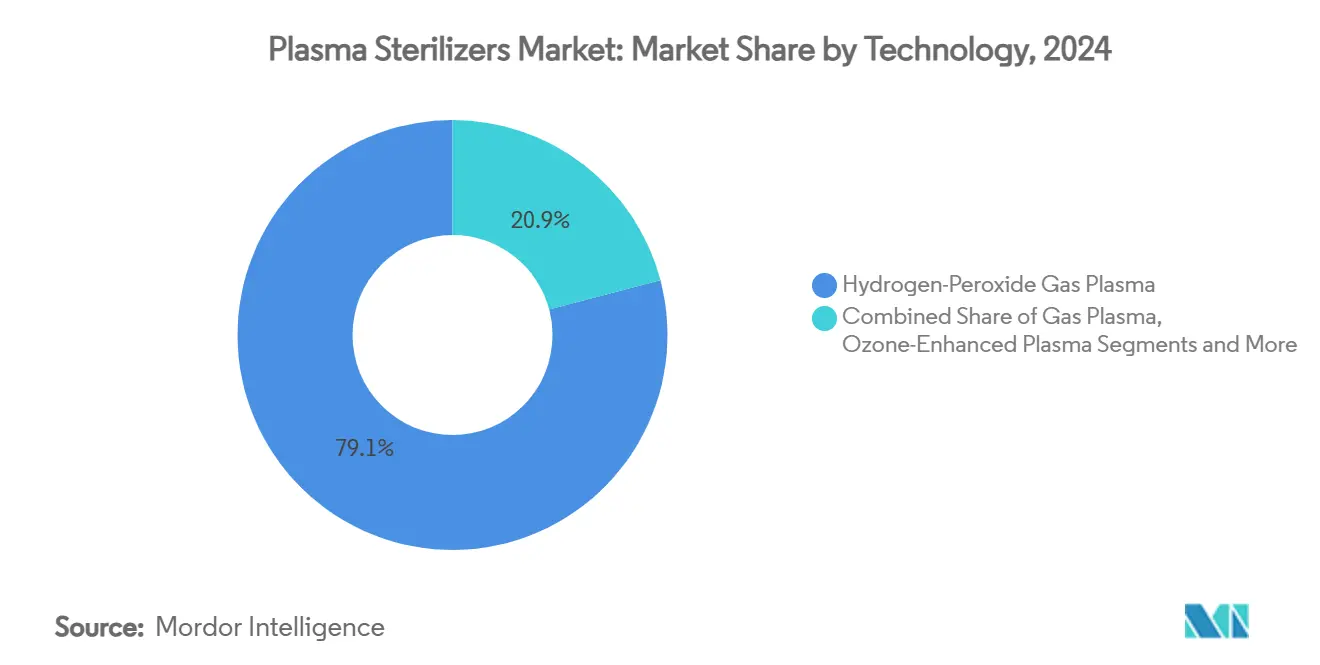

- By technology, hydrogen-peroxide gas plasma held 79.1% of plasma sterilizers market share in 2024, whereas ozone-enhanced plasma is projected to grow at 6.4% CAGR through 2030.

- By capacity, the 100-300 L segment commanded 44.3% share of the plasma sterilizers market size in 2024, while chambers less than 100 L are forecast to expand at 5.2% CAGR to 2030.

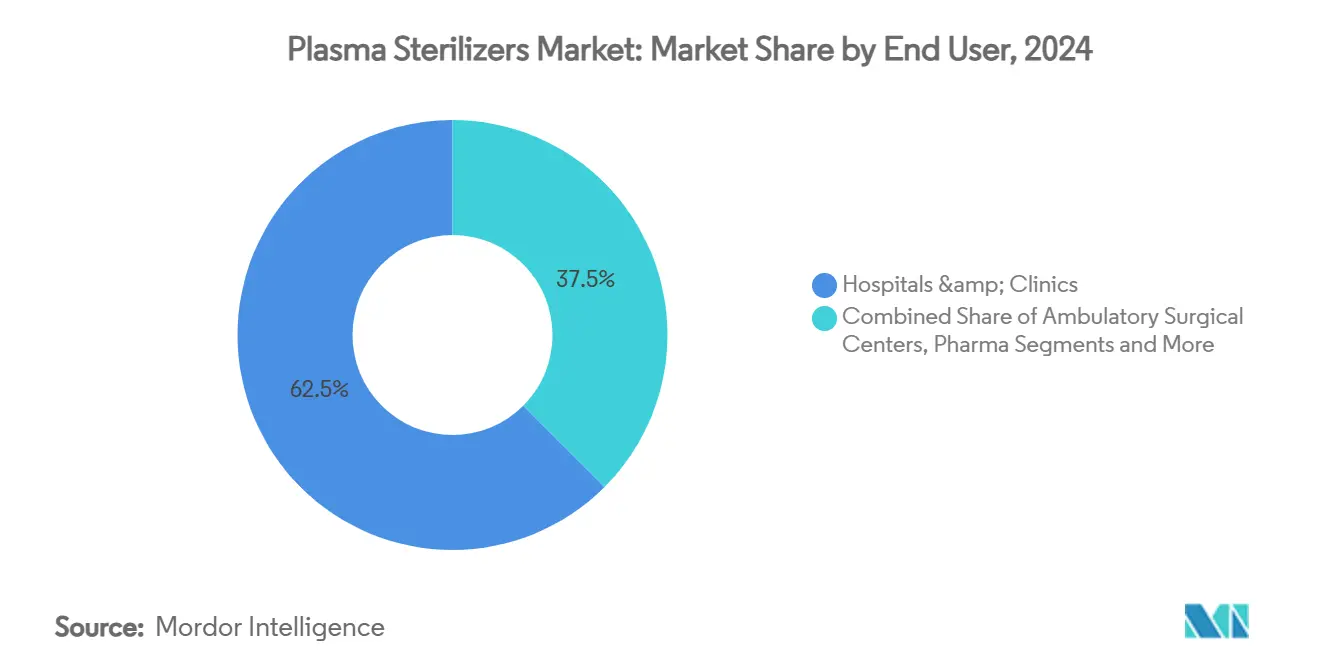

- By end user, hospitals and clinics controlled 62.5% share of the plasma sterilizers market in 2024; ambulatory surgical centers are expected to grow at 6.2% CAGR through 2030.

- By geography, North America led with 40.8% revenue share in 2024, whereas Asia-Pacific is poised for the fastest 7.5% CAGR to 2030.

Global Plasma Sterilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising healthcare-associated infections | +0.90% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Stringent sterilization & patient-safety rules | +1.20% | Global, led by FDA & EPA changes | Short term (≤ 2 years) |

| Surge in heat-sensitive device portfolio | +0.70% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Shift away from ethylene oxide | +1.10% | Global, regulatory pressure in developed markets | Medium term (2-4 years) |

| Expansion of ambulatory surgical sites | +0.60% | North America & APAC core markets | Long term (≥ 4 years) |

| Growth of contract sterilization providers | +0.50% | Global, manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Healthcare-Associated Infections

Intensive care and surgical units report stubborn biofilm-related outbreaks, prompting infection-prevention teams to adopt plasma systems that deliver 10-⁶ sterility for complex instruments. The CDC’s guideline update highlights hydrogen-peroxide gas plasma as the validated low-temperature option for heat-sensitive scopes, ensuring material integrity while neutralizing multidrug-resistant organisms.[1]Centers for Disease Control and Prevention, “Guideline for Disinfection and Sterilization in Healthcare Facilities,” cdc.gov Hospitals justify capital spend by offsetting infection costs that often exceed USD 25,000 per episode, reinforcing uptake across flagship facilities within the plasma sterilizers market. Device reprocessing teams emphasize the technology’s superior lumen penetration, quick cycles, and zero toxic residues, features now embedded in hospital patient-safety charters. Accelerating nosocomial infection penalties further positions plasma platforms as essential infrastructure.

Stringent International Sterilization and Patient-Safety Regulations

The EPA’s 2024 rule mandates 99.99% EtO emission cuts, spurring rapid migration toward plasma methods that emit only water vapor and oxygen. Simultaneously, the FDA’s enforcement discretion for Class III devices encourages manufacturers to validate alternative sterilization earlier in product life cycles, reducing regulatory bottlenecks. ISO 17665:2024 tightened moist-heat protocols, indirectly elevating plasma adoption for polymers unsuited to steam.[2]Amber Wood, “Sterilization: AORN's Updated Guideline for Enhanced Patient Safety,” aorn.org European GMP Annex 1 revisions now demand visual confirmation and traceable packaging, criteria readily satisfied by hydrogen-peroxide plasma pouches with built-in color indicators. Together, these synchronized policies create compliance-driven momentum that enlarges the plasma sterilizers market footprint.

Rapid Growth of Heat-Sensitive Medical Device Portfolio

Next-generation implants and 3D-printed polymers—such as PLA, PPSU, and PEEK—maintain structural and mechanical properties through repeated plasma exposure, enabling more device iterations without costly redesign. Complex MIS instruments with ultra-narrow channels present aeration-time and material challenges for EtO, yet they sterilize efficiently in 35-minute hydrogen-peroxide plasma cycles. Surface-modified cardiovascular and orthopedic devices further benefit from plasma’s ability to preserve nano-scale coatings essential for biocompatibility. The expanding heat-sensitive portfolio therefore amplifies demand for validated low-temperature chambers within the plasma sterilizers market.

Global Shift from Ethylene Oxide toward Environment-Friendly Technologies

Hospitals facing community scrutiny over carcinogenic EtO emissions view plasma as an immediate, facility-level sustainability win. Hydrogen-peroxide systems require no aeration rooms, lower cycle energy, and minimize occupational exposure risks, aligning with ESG key-performance indicators. Vendors showcase cycle-cancellation rates below 1% via algorithms that auto-adjust parameters, making plasma more predictable than chlorine-dioxide or nitrogen-dioxide competitors. Procurement teams cite lower chemical disposal fees and faster instrument release as concrete savings that offset higher capital, sustaining a double-digit replacement rate for aging EtO chambers across the plasma sterilizers industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| High capital expenditure & total cost | -1.50% | Global, acute in emerging markets |

| Material & lumen compatibility challenges | -0.90% | Global, technical limitations across regions |

| Supply vulnerability for medical-grade H₂O₂ | -0.70% | Global, concentrated in manufacturing regions |

| Shortage of skilled personnel | -0.60% | Global, severe in APAC emerging markets |

| Source: Mordor Intelligence | ||

High Capital Expenditure and Total Cost of Ownership

Premium hydrogen-peroxide chambers can cost two to three times a steam autoclave, challenging budgets at community hospitals and ambulatory centers. Expenses extend to consumable cassettes, biological indicators, and validation documentation that together inflate lifecycle costs. Although reduced aeration and device longevity yield operational benefits, financing hurdles in emerging economies curb penetration, temporarily restraining overall plasma sterilizers market growth. Vendors respond with leasing models and trade-in programs, but near-term uptake remains sensitive to capital cycles.

Material and Lumen Compatibility Challenges

Absorbent materials, intricate multi-material assemblies, and ultra-long lumens still pose validation hurdles despite software advances. Device makers must run exhaustive bioburden and permeability tests, lengthening submission timelines. Research shows lumen sterilization efficacy is pressure-dependent; failure to tune parameters risks incomplete kill rates, necessitating extra cycles that erode workflow gains.[3]Clair Koo et al., “Simulation of Excited Molecule Propagation to Determine Plasma Sterilization Effectiveness in Lumens,” jsr.org These compatibility gaps moderate adoption in selected cardiovascular and dental lines within the plasma sterilizers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hydrogen-Peroxide Dominance Drives Innovation

Hydrogen-peroxide gas plasma systems account for 79.1% of 2024 revenue, reflecting broad polymer compatibility and a 23,000-device validation library. The segment’s demonstrated 10-⁶ sterility assurance makes it the workhorse of the plasma sterilizers market, attracting continual software and sensor upgrades that shrink aborted cycles. Ozone-enhanced plasma, while holding a smaller base, posts a robust 6.4% CAGR to 2030, propelled by rapid decomposition into oxygen and stronger virucidal activity that appeals to ophthalmology and dental clinics.

The other category—nitrogen dioxide and chlorine dioxide—garners niche demand where short dwell times outweigh capital cost. Nonetheless, hydrogen-peroxide vendors integrate AI-driven load recognition and integrated dosing to cement leadership. As regulatory clarity around alternative gases improves, competitive dynamics in the plasma sterilizers market will hinge on validated material libraries and turnkey service packages.

By Capacity: Mid-Range Systems Optimize Hospital Workflows

Chambers sized 100–300 L captured 44.3% of 2024 revenue, mirroring the daily mix of instrument sets in tertiary hospitals. These units balance throughput with spatial constraints, fitting into legacy sterile-processing layouts without structural remodeling. They also facilitate batch flexibility, from orthopedic trays to delicate endoscopes, cementing their role at the core of the plasma sterilizers market size for acute-care facilities.

Sub-100 L models, however, post the swiftest 5.2% CAGR on the back of ambulatory center build-outs. Their 35-minute cycles deliver on same-day surgery turnover, reducing courier risks. Conversely, chambers above 300 L serve integrated delivery networks centralizing reprocessing at hub sites; conveyor loaders and robotics are common to drive staffing efficiency. Capacity choices, therefore, map directly to evolving care models and throughput economics across the plasma sterilizers market.

By End User: Hospitals Lead While ASCs Accelerate

Hospitals and clinics accounted for 62.5% of 2024 spending, leveraging multi-modality setups where plasma sterilization protects heat-sensitive scopes and implants. Capital planning often synchronizes with OR expansion, so replacement cycles align with surgical wing upgrades, sustaining the hospital segment within the plasma sterilizers market.

Ambulatory surgical centers display a 6.2% CAGR thanks to reimbursement shifts favoring outpatient arthroscopy, cataract, and GI procedures. Compact plasma units fit their space and staffing profile, enabling on-premises reprocessing instead of third-party courier routes. Pharmaceutical cleanrooms and medical device OEMs form smaller but technically demanding niches, seeking GMP-aligned documentation that plasma systems now integrate via cloud-based audit trails. Contract sterilizers round out demand by offering technology-neutral capacity to OEMs lacking capital budgets.

Geography Analysis

North America retained 40.8% revenue in 2024 on the back of strict FDA classification and early vaporized hydrogen-peroxide endorsements that accelerated hospital purchasing decisions. Ethylene-oxide emission rules published in 2024 further nudged facilities toward plasma, driving retrofits at over 120 U.S. sterilization plants. Clustered device OEMs and national GPO purchasing amplify scale benefits for leading suppliers, safeguarding regional leadership within the plasma sterilizers market.

Asia-Pacific posts the fastest 7.5% CAGR to 2030. China’s device makers moving up-market require export-grade sterilization validation, while India’s hospital buildouts embed low-temperature capability from day one. Japan’s USD 40 billion medical-device sector, growing at 5.5% through 2027, also fuels demand for plasma chambers that protect premium polymer implants. Regional governments channel infection-control grants to tertiary centers, spurring capacity additions that lift the plasma sterilizers market size across APAC.

Europe maintains steady share driven by GMP Annex 1 upgrades and sustainability mandates that headline health-system procurement. Vendors showcase Annex 1-compliant windowed pouches and end-to-end traceability modules, addressing auditor expectations. Getinge’s SEK 2 billion quality remediation and strategic acquisition of Healthmark illustrate the compliance-first lens guiding European investments. Simultaneously, Middle East hubs like the UAE import turnkey sterile-processing suites, providing incremental opportunities.

Competitive Landscape

The plasma sterilizers market exhibits moderate concentration. STERIS and Advanced Sterilization Products anchor the field through patent portfolios, cycle databases, and service footprints that jointly span thousands of validated devices. STERIS’s 2024 purchase of Healthmark for USD 320 million expands sterile-reprocessing accessories, signaling a move toward holistic ecosystem control. ASP highlights ALLClear A.I. algorithms that cut aborts below 1%, marketing operational reliability as a differentiator.

Mid-tier challengers focus on ozone-assisted or hybrid chemistries, pitching niche material compatibility. Contract sterilizer Sterigenics retrofits 48 sites with plasma chambers, positioning itself as the one-stop provider for OEMs needing redundancy. Regional entrants in APAC emphasize cost-optimized <100 L models tailored to ambulatory centers. Sustained R&D into cold atmospheric plasma for surface applications could open adjacency plays, though scale-up hurdles persist.

Plasma Sterilizers Industry Leaders

Advanced Sterilization Products (ASP)

STERIS plc

Getinge AB

Shinva Medical

Tuttnauer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sonata Scientific unveiled the Helios MP500 EtO abatement unit, which achieves 99% destruction removal efficiency and targets medical device sterilization facilities.

- January 2025: STERIS expanded CRCST and CFER certification courses to mitigate technician shortages in sterile-processing departments.

- June 2024: Getinge closed its USD 320 million Healthmark acquisition, reinforcing its U.S. sterile-reprocessing presence.

Global Plasma Sterilizers Market Report Scope

| Hydrogen-Peroxide Gas Plasma |

| Ozone-Enhanced Plasma |

| Others |

| Less Than 100 L |

| 100 - 300 L |

| More Than 300 L |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Pharma & Biotech Clean-rooms |

| Medical Device OEMs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Hydrogen-Peroxide Gas Plasma | |

| Ozone-Enhanced Plasma | ||

| Others | ||

| By Capacity | Less Than 100 L | |

| 100 - 300 L | ||

| More Than 300 L | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Pharma & Biotech Clean-rooms | ||

| Medical Device OEMs | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is projected for the plasma sterilizers market through 2030?

The market is forecast to grow at 6.10% CAGR from 2025 to 2030.

Which technology currently dominates sales?

Hydrogen-peroxide gas plasma systems hold 79.1% revenue share in 2024.

Which region is expected to expand the fastest?

Asia-Pacific is projected to register a 7.5% CAGR through 2030.

Why are ambulatory surgical centers investing in plasma systems?

Compact chambers enable 35-minute cycles that support high procedure turnover in outpatient settings.

What is the main environmental advantage over ethylene oxide?

Hydrogen-peroxide plasma produces only water and oxygen, eliminating carcinogenic emissions and aeration delays.

Page last updated on: