Microelectronic Medical Implants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

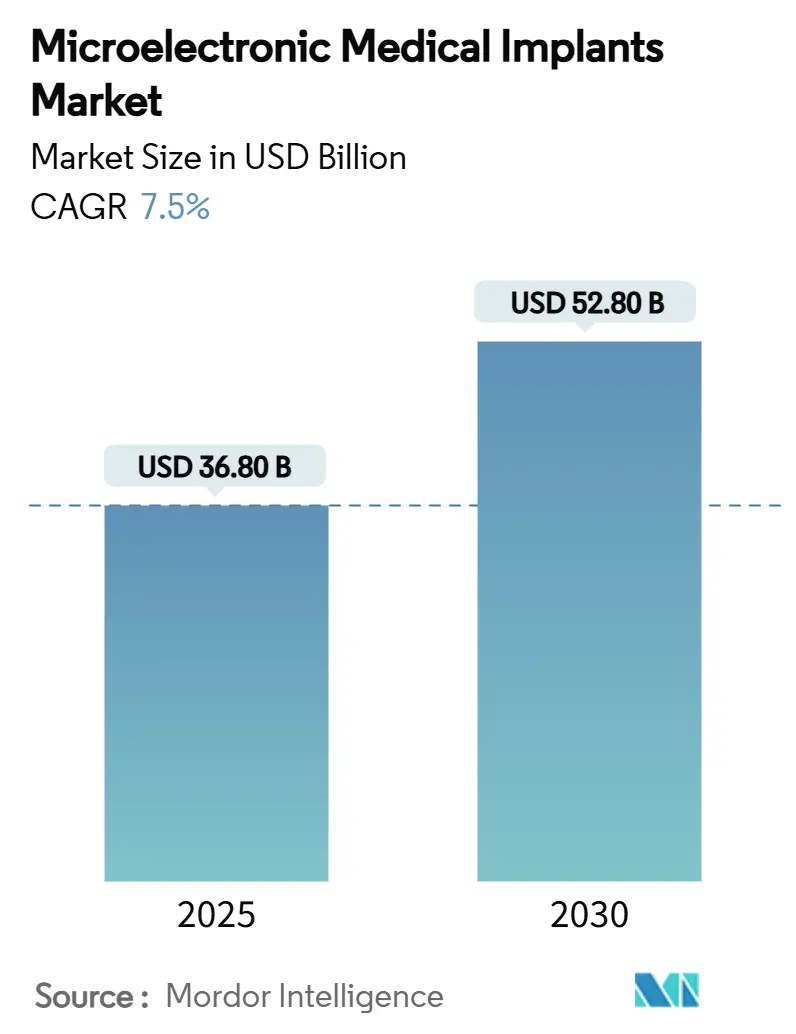

| Market Size (2025) | USD 36.80 Billion |

| Market Size (2030) | USD 52.80 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

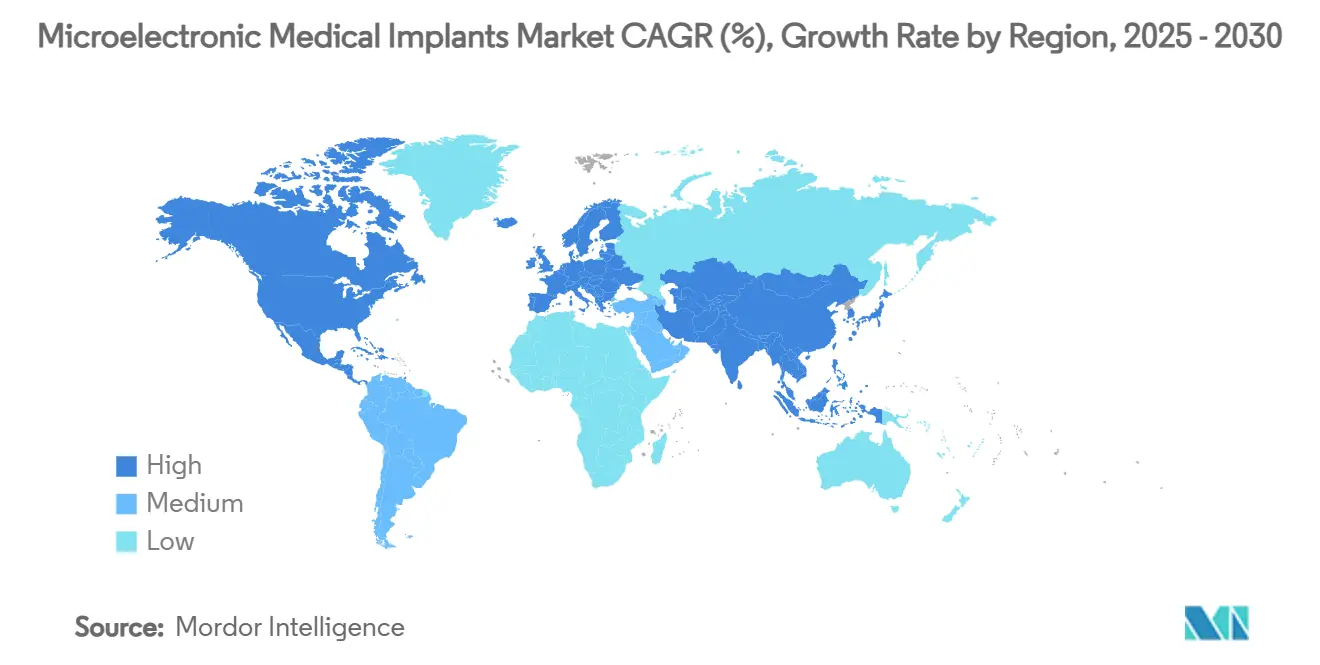

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microelectronic Medical Implants Market Analysis by Mordor Intelligence

The microelectronic medical implants market size is USD 36.8 billion in 2025 and is projected to reach USD 52.8 billion by 2030, registering a 7.50% CAGR over the forecast period. Demand expands as aging populations intersect with the rapid miniaturization of semiconductors, new battery chemistries, and the first wave of AI-enabled closed-loop platforms that continuously adapt therapy to patient-specific signals. Cardiac rhythm management devices still anchor revenues, but double-digit growth shifts toward neurostimulation, bioresorbable monitoring systems, and energy-harvesting form factors. Industry leaders accelerate vertical integration to secure sensors, algorithms, and specialized substrates, even as cybersecurity rules and semiconductor supply bottlenecks add cost and complexity. Growth disparities also emerge geographically: North America remains the single largest market while Asia-Pacific records the fastest compounded gains as hospitals modernize and chronic disease prevalence rises.

Key Report Takeaways

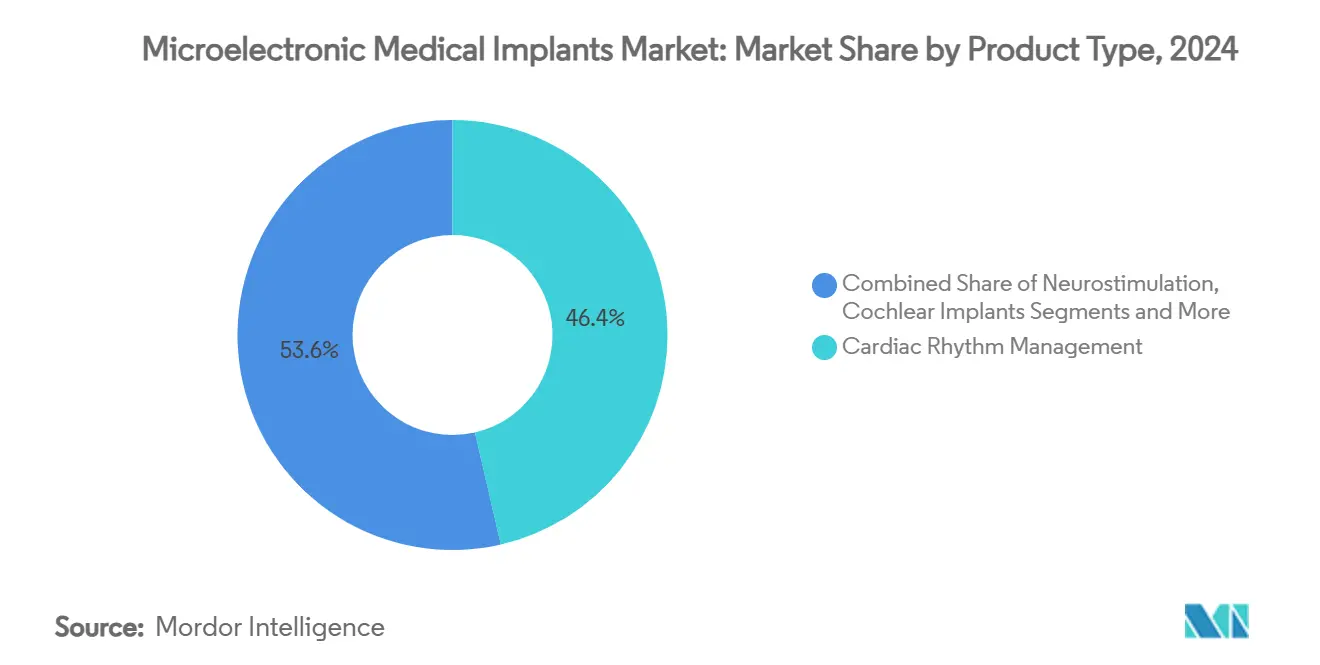

- By product type, cardiac rhythm management devices held 46.4% of the microelectronic medical implants market share in 2024, whereas neurostimulation devices are advancing at an 11.5% CAGR through 2030.

- By communication & power, primary battery-powered systems accounted for 74.6% of the microelectronic medical implants market size in 2024, yet bioresorbable electronics are forecast to surge at a 20.3% CAGR to 2030.

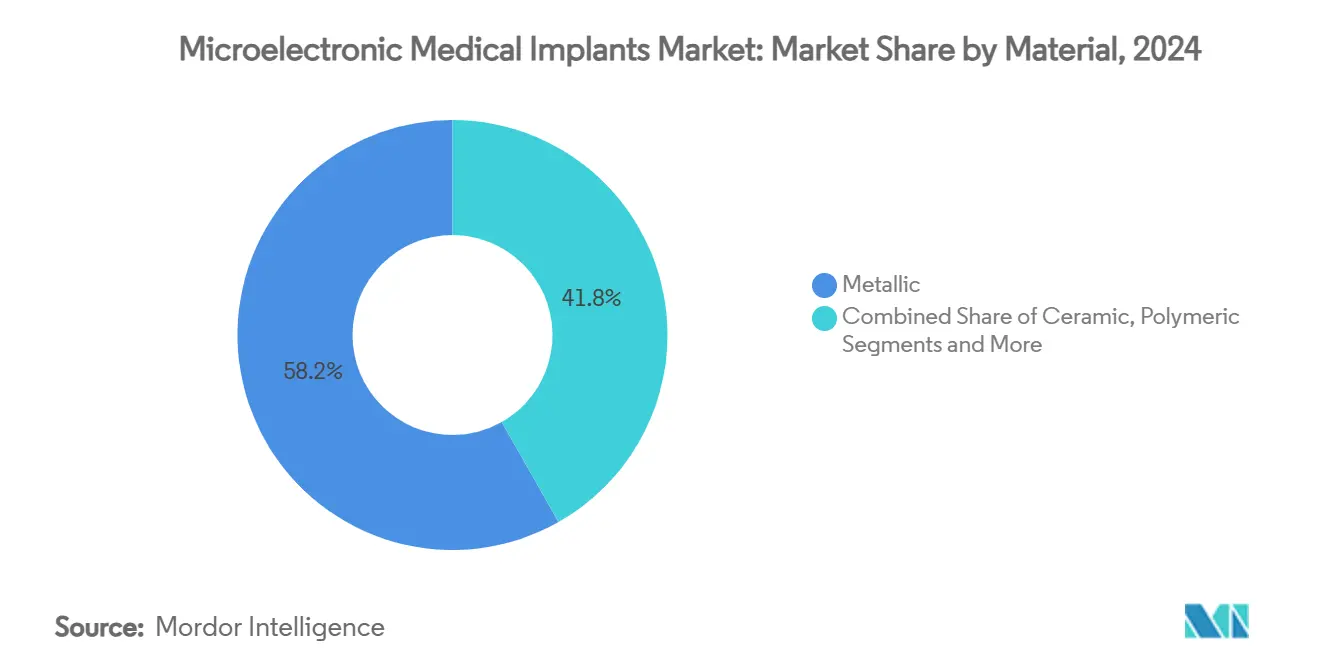

- By material, metallic implants dominated with 58.2% revenue contribution in 2024, while conductive polymers will expand at a 15.6% CAGR between 2025 and 2030.

- By end user, hospitals captured 62.7% of 2024 revenues; home-care settings are expected to deliver the highest CAGR at 10.8% through 2030.

- By geography, North America led with a 39.5% revenue share in 2024, whereas Asia-Pacific is projected to grow at a 9.7% CAGR over the same period.

Global Microelectronic Medical Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging demographics & chronic disease burden | +1.50% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Device miniaturization & advanced batteries | +1.20% | Global; APAC manufacturing hubs lead | Medium term (2-4 years) |

| Growing adoption of neurostimulators | +0.80% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Expanding reimbursement for implantables | +0.60% | Developed markets first, gradual uptake in APAC | Long term (≥ 4 years) |

| AI-enabled closed-loop bioelectronic systems | +0.90% | North America & Europe early adoption; APAC following | Short term (≤ 2 years) |

| Bioresorbable temporary electronics | +0.70% | Global; R&D concentrated in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Demographics & Chronic Disease Burden

Populations aged 65 years and above already represent more than 20% of residents in several high-income countries, creating persistent demand for implants that deliver long-term cardiovascular and neurological management. Prevalence of diabetes, heart failure, and Parkinson’s disease all climb with age, pushing hospitals toward devices that can continuously monitor physiology and intervene automatically. Economists estimate that chronic diseases will cost global health systems tens of trillions of USD between now and 2030, prompting payers to favor technologies able to avert hospitalizations through predictive analytics and early-warning alerts. Yet reimbursement caps in those same mature markets often lag technology cycles, forcing manufacturers to defend premium pricing even where clinical demand is highest.

Device Miniaturization & Advanced Battery Chemistries

Shrinking semiconductor nodes enable leadless pacemakers and capsule-sized pressure sensors to perform functions once restricted to can-style generators. Parallel advances in lithium-ion cathode design, solid-state electrolytes, and graphene current collectors extend battery life beyond 12 years, reducing costly replacement surgeries. Academic groups now demonstrate piezoelectric, triboelectric, and enzymatic biofuel cells that harvest mechanical motion or glucose oxidation, hinting at fully energy-autonomous implants. When longer life combines with smaller size, patient acceptance improves and procedure volumes rise, particularly in minimally invasive cardiology and neurology.

Growing Adoption of Neurostimulators for Pain and Movement Disorders

Closed-loop deep-brain stimulation (DBS) systems incorporate sensing electrodes that read local field potentials and alter pulse width or amplitude in real time. The US FDA cleared Medtronic’s BrainSense Adaptive DBS in 2025, the first commercial example of such dynamic programming. Clinical trials show improved symptom control with lower energy use, delaying battery depletion and minimizing side effects. Indications rapidly widen from Parkinson’s to essential tremor, chronic pain, epilepsy, and treatment-resistant depression, all of which expand addressable volume beyond traditional movement-disorder centers.

Expanding Reimbursement Frameworks for Implantable Therapies

Value-based payment schemes in the United States and parts of Europe reward avoided admissions rather than procedural throughput, aligning payer incentives with the continuous monitoring features that implantables deliver. The US FDA’s Total Product Life Cycle Advisory Program now offers earlier clinical feedback opportunities, accelerating time-to-market for novel devices.[1]FDA, “Marketing Submission Recommendations for a Predetermined Change Control Plan for Artificial Intelligence-Enabled Device Software Functions,” fda.gov Nonetheless, reimbursement remains uneven across regions; emerging economies still rely heavily on out-of-pocket spending, stalling penetration of premium neurostimulators and fully implantable hearing systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Jurisdictional Regulatory Hurdles | -0.90% | Global, with varying intensity across regions | Medium term (2-4 years) |

| High Upfront Device & Procedure Costs With Reimbursement Gaps | -0.60% | Emerging markets primarily, selective impact in developed markets | Long term (≥ 4 years) |

| Cyber-Security And Patient Data-Privacy Vulnerabilities | -0.40% | Global, with heightened focus in North America & Europe | Short term (≤ 2 years) |

| Limited Supply Of Specialty Semiconductor Substrates & Packaging Capacity | -0.30% | Global, with concentration in APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdictional Regulatory Hurdles

The US FDA finalized its Quality Management System Regulation in early 2025, compelling manufacturers to harmonize with ISO 13485 by February 2026.[2]FDA, “Marketing Submission Recommendations for a Predetermined Change Control Plan for Artificial Intelligence-Enabled Device Software Functions,” fda.gov Europe’s Medical Device Regulation similarly demands exhaustive clinical evaluation and post-market surveillance dossiers. Layer on new cybersecurity mandates for network-connected implants, and smaller innovators face multi-million-USD compliance costs that can delay launches by two years or more. Established incumbents absorb these hurdles more easily, reinforcing market concentration.

High Upfront Device & Procedure Costs With Reimbursement Gaps

Implant packages—including generator, leads, surgical consumables, and operating-room time—often exceed USD 50,000 in mature markets and are higher on a purchasing-power basis in low-income economies. Coverage remains uneven for next-generation platforms such as fully implantable cochlear systems or energy-harvesting neurostimulators. Hospitals must therefore justify capital purchases with robust real-world evidence, slowing uptake even where clinical benefit is established. Lower-cost domestically manufactured alternatives appear in China and India, but questions linger about long-term reliability, reinforcing a price–quality divide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cardiac Dominance Faces Neurological Disruption

Cardiac rhythm management accounted for 46.4% of revenues in 2024, underpinned by decades of clinical validation and reimbursement familiarity. Despite this weight, neurostimulation is projected to outpace every other category at an 11.5% CAGR, reflecting strong demand for DBS, spinal cord stimulation, and emerging vagus-nerve and sacral-nerve indications. The market size of microelectronic medical implants for neurostimulation is expected to more than double, capturing share from plateauing cardiac applications. Product advances such as Medtronic’s adaptive DBS platform and Abbott’s AVEIR DR leadless pacemaker show divergent innovation pathways: one leverages AI to improve outcomes, the other removes leads to cut complication rates.

Competition in cardiac segments now revolves around incremental battery extensions and MR-conditional labeling, suggesting commoditization. Meanwhile, neuro devices explore novel targets, including depression, stroke rehabilitation, and cognitive enhancement, broadening addressable populations far beyond movement disorders. Cochlear implants benefit from discreet microphone integration, while retinal prostheses pursue higher pixel density for functional vision restoration. These shifts collectively alter capital allocation, with venture funding increasingly preferring neurologically focused startups over legacy cardiac franchises.

By Communication & Power: Battery Evolution Toward Energy Independence

Primary cells still power nearly three-quarters of implants shipped in 2024, underscoring their reliability and regulatory familiarity. Nonetheless, bioresorbable electronics log a 20.3% CAGR because they eliminate explant surgeries, an attractive value proposition for post-operative monitoring. Rechargeable spinal cord stimulators and LVAD controllers hold specialized niches but face patient-adherence hurdles for routine charging.

Energy harvesting marks the next frontier. Triboelectric nanogenerators integrated into pacemaker leads convert myocardial motion into microwatts of power; piezoelectric cantilevers adjacent to the diaphragm harness respiratory movement. Seoul National University’s wireless drug-delivery capsule receives power and data through inductive coupling at fourfold the efficiency of earlier prototypes.[3]Phys.org, “Wireless implant delivers chemotherapy deep into tumors without side effects,” phys.org As conversion efficiency rises, the microelectronic medical implants market expects a gradual migration from batteries toward hybrid or fully self-powered architectures, especially in low-load sensing applications.

By Material: Advanced Polymers Challenge Metallic Dominance

Metallic housings—primarily titanium—made up 58.2% of shipments in 2024 due to unmatched corrosion resistance and hermetic sealing. Yet conductive polymers now register a 15.6% CAGR, driven by the need for flexible neural interfaces. A 2025 Nature report details PEDOT: PSS structures with 8,500 S/cm conductivity, narrowing the performance gap with metals while retaining tissue compliance.

Ceramics such as alumina and zirconia provide insulation for high-frequency stimulation circuits but struggle with complex 3-D geometries. Polyether-ether-ketone (PEEK) and silicone elastomers offer chemical inertness and form-factor versatility. Composite stacks that layer metals for conductivity and polymers for flexibility gain traction, though multilayer manufacturing raises validation complexity. Overall, the microelectronic medical implants market perceives materials innovation as central to next-generation neural and cardiovascular implants.

By End User: Hospital Dominance Shifts Toward Distributed Care

Hospitals consumed 62.7% of devices in 2024, yet home-care settings will post the highest 10.8% CAGR to 2030 as telemonitoring and minimally invasive techniques allow outpatient implantation and remote follow-up. The microelectronic medical implants market size for home-care use cases grows in tandem with broadband penetration and payer support for remote patient management. Ambulatory surgical centers are also rising, handling straightforward leadless pacemaker placements and neurostimulator generator changes in less than half the cost of inpatient surgery.

The pivot to home-based care demands cybersecurity-hardened telemetry and patient-friendly charging or energy-harvesting solutions. It also strains traditional device-clinic business models that rely on generator replacements for revenue. Consequently, manufacturers now bundle cloud analytics and virtual coaching subscriptions to offset shrinking hardware margins.

By Application: Cardiology Leadership Faces Neurological Challenge

Cardiology maintains the largest absolute revenue today because heart-failure prevalence and life-saving imperatives drive implantable defibrillator and CRT volumes. Still, neurology registers the swiftest rise, aided by adaptive DBS and spinal cord stimulation for intractable pain. Results from the ADAPT-PD trial revealed superior on-time and reduced dyskinesia with closed-loop stimulation versus continuous output, reinforcing neurologists’ willingness to implant earlier in disease progression.

Ophthalmology pushes toward artificial retinas with 1,024-pixel matrices, while endocrinology explores implantable glucose and glucagon reservoirs that interface with wearables for autonomous insulin dosing. Orthopedics integrates embedded stimulators inside fracture plates to accelerate osteogenesis, yet reimbursement uncertainty slows uptake. Across these specialties, the microelectronic medical implants market gains diversification, reducing reliance on any single therapeutic domain.

Geography Analysis

North America commanded 39.5% of 2024 revenues through strong payor coverage, sophisticated electrophysiology labs, and the earliest adoption of AI-ready platforms. The region benefits from a regulatory environment that now allows predetermined software updates, shortening iteration cycles and encouraging the launch of algorithm-heavy devices. However, price transparency initiatives and site-of-care shifts put margin pressure on premium implants, forcing vendors to couple devices with digital services to defend value propositions.

Asia-Pacific is forecast to grow at a 9.7% CAGR, the fastest worldwide, as governments expand universal health programs and local manufacturers scale cost-competitive production. China invests heavily in brain-computer interfaces, funding start-ups like NeuroXess to develop Mandarin-optimized speech prostheses. Meanwhile, Southeast Asian contract manufacturers supply titanium housings and CMOS sensor chips, anchoring the global microelectronic medical implants market supply chain. Regulatory harmonization via the ASEAN Medical Device Directive progresses slowly, which could temper near-term device flow but ultimately streamline cross-border approvals.

Europe presents a mixed landscape. Germany and the Netherlands maintain high implant volumes, but austerity measures in France led to a 25% cut in orthopedic implant tariffs in 2025, pressuring hospital purchasing committees. The EU’s Medical Device Regulation tightens post-market surveillance, adding compliance cost that smaller firms struggle to absorb. Nonetheless, CE-mark approvals such as Edwards Lifesciences’ transfemoral mitral valve implant show that innovation continues where clinical and economic value align.

Competitive Landscape

The microelectronic medical implants market is moderately concentrated, with the top five suppliers holding roughly 55% of global revenue. Medtronic, Abbott, and Boston Scientific maintain extensive cardiology and neurology portfolios that leverage decades of physician relationships. Yet vertical integration and AI differentiation now drive mergers: Globus Medical spent USD 3.1 billion to acquire Nevro and fuse spinal hardware with stimulation algorithms, a template for orthobiologics plus electronics convergence.

Innovation clusters outside the incumbents pursue niche dominance. Synchron’s endovascular Stentrode bypasses craniotomy, providing a less invasive brain-computer interface pathway that could erode DBS' share in certain indications. Boston Scientific broadened its pain portfolio by purchasing Cortex Medical Technologies, gaining proprietary burst-waveforms for spinal cord stimulation. Material science startups focusing on bioresorbable sensors attract strategic investment from device majors eager to hedge against commoditization.

Supply security becomes strategic after recent semiconductor substrate shortages. Larger firms negotiate long-term contracts with gallium-nitride and silicon-carbide foundries, while smaller entrants explore additive manufacturing to localize production. Cybersecurity emerges as a differentiator: products with hardware-root-of-trust chips and over-the-air patch capability meet impending FDA requirements sooner, appealing to hospital IT buyers.

Microelectronic Medical Implants Industry Leaders

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

Cochlear Limited

BIOTRONIK SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Edwards Lifesciences received CE mark for its transfemoral mitral valve implant, broadening European minimally invasive options.

- February 2025: Medtronic obtained FDA clearance for the BrainSense Adaptive DBS, the first closed-loop neurostimulator that modulates therapy based on sensed neural activity.

- January 2025: Globus Medical finalized its USD 3.1 billion acquisition of Nevro, combining spinal fixation hardware with neurostimulation algorithms.

Global Microelectronic Medical Implants Market Report Scope

| Cardiac Rhythm Management Devices |

| Neurostimulation Devices |

| Cochlear & Auditory Implants |

| Retinal Implants |

| Implantable Drug-Delivery Pumps |

| Smart Orthopedic/Bone-Growth Stimulators |

| Primary Battery-Powered |

| Rechargeable Battery-Powered |

| Inductive Wireless-Power |

| Energy-Harvesting / Triboelectric |

| Bioresorbable Electronics |

| Leadless Capsule / Endoscopic Form-Factor |

| Metallic (Titanium & Alloys) |

| Ceramic (Alumina, Zirconia) |

| Polymeric (Silicone, PEEK) |

| Conductive Polymers (PEDOT:PSS) |

| Composite & Hybrid |

| Cardiology |

| Neurology & Chronic Pain |

| Otology |

| Ophthalmology |

| Endocrinology & Metabolic Disorders |

| Orthopedics |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Cardiac Rhythm Management Devices | |

| Neurostimulation Devices | ||

| Cochlear & Auditory Implants | ||

| Retinal Implants | ||

| Implantable Drug-Delivery Pumps | ||

| Smart Orthopedic/Bone-Growth Stimulators | ||

| By Communication & Power Technology | Primary Battery-Powered | |

| Rechargeable Battery-Powered | ||

| Inductive Wireless-Power | ||

| Energy-Harvesting / Triboelectric | ||

| Bioresorbable Electronics | ||

| Leadless Capsule / Endoscopic Form-Factor | ||

| By Material | Metallic (Titanium & Alloys) | |

| Ceramic (Alumina, Zirconia) | ||

| Polymeric (Silicone, PEEK) | ||

| Conductive Polymers (PEDOT:PSS) | ||

| Composite & Hybrid | ||

| By Application | Cardiology | |

| Neurology & Chronic Pain | ||

| Otology | ||

| Ophthalmology | ||

| Endocrinology & Metabolic Disorders | ||

| Orthopedics | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the microelectronic medical implants market?

The market is valued at USD 36.8 billion in 2025 and is set to reach USD 52.8 billion by 2030.

Which segment is growing the fastest?

Neurostimulation devices are expanding at an 11.5% CAGR, the highest among all product categories.

Why are bioresorbable electronics attracting attention?

They dissolve after completing their task, eliminating explant surgeries and cutting procedural risks.

Which region will add the most new revenue by 2030?

Asia-Pacific, forecast to post a 9.7% CAGR, will contribute the largest incremental revenue.

How are AI algorithms changing implant performance?

AI enables closed-loop systems that sense physiological changes and adjust therapy in real time, improving outcomes and battery life.

What regulatory change most affects future product launches?

The US FDA’s predetermined change-control plan guidance allows pre-approved software updates, accelerating the iteration of AI-enabled implants.

Page last updated on: