Medical Foods Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

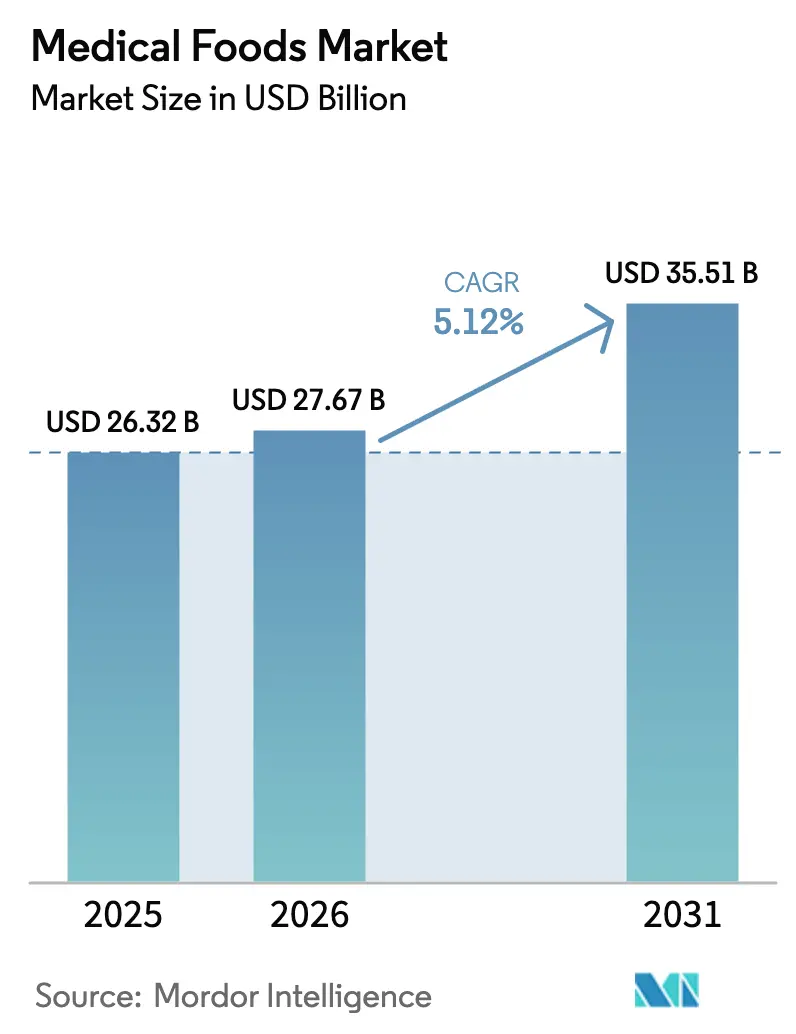

| Market Size (2026) | USD 27.67 Billion |

| Market Size (2031) | USD 35.51 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

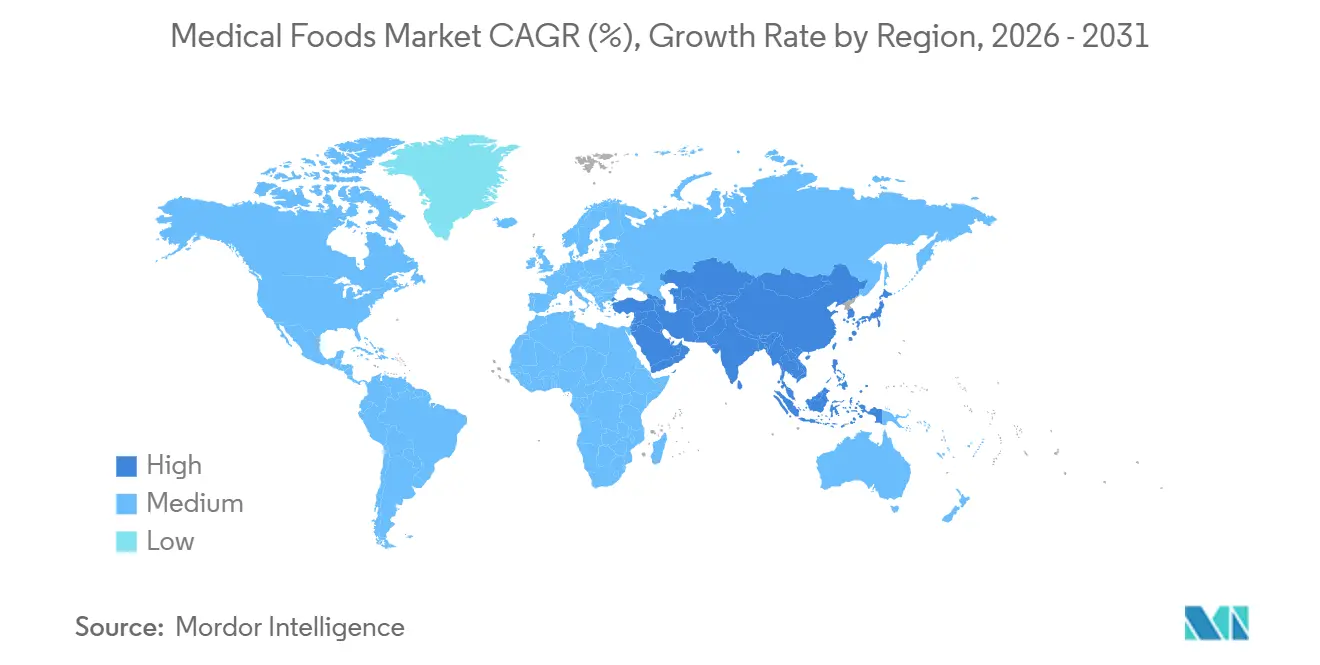

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Foods Market Analysis by Mordor Intelligence

The Medical Foods Market size is projected to expand from USD 26.32 billion in 2025 and USD 27.67 billion in 2026 to USD 35.51 billion by 2031, registering a CAGR of 5.12% between 2026 to 2031.

Clinical evidence is driving the transition of medical foods from a niche nutrition category to a recognized therapeutic adjunct. Hospital formularies are sustaining demand for powder formats that can be reconstituted in bulk. Additionally, soft-gel capsules are gaining market traction due to their lipid-based delivery system, which enhances the bioavailability of fat-soluble micronutrients used in neurological and metabolic treatments. Aging populations in OECD countries, the implementation of China’s GB 29922-2025 standard for Foods for Special Medical Purposes, and the expansion of India’s Ayushman Bharat reimbursement program are unlocking new growth opportunities. However, payer scrutiny over ingredient costs and the absence of Medicare Part B coverage for oral products in the United States are constraining the growth trajectory of the medical foods market.

Key Report Takeaways

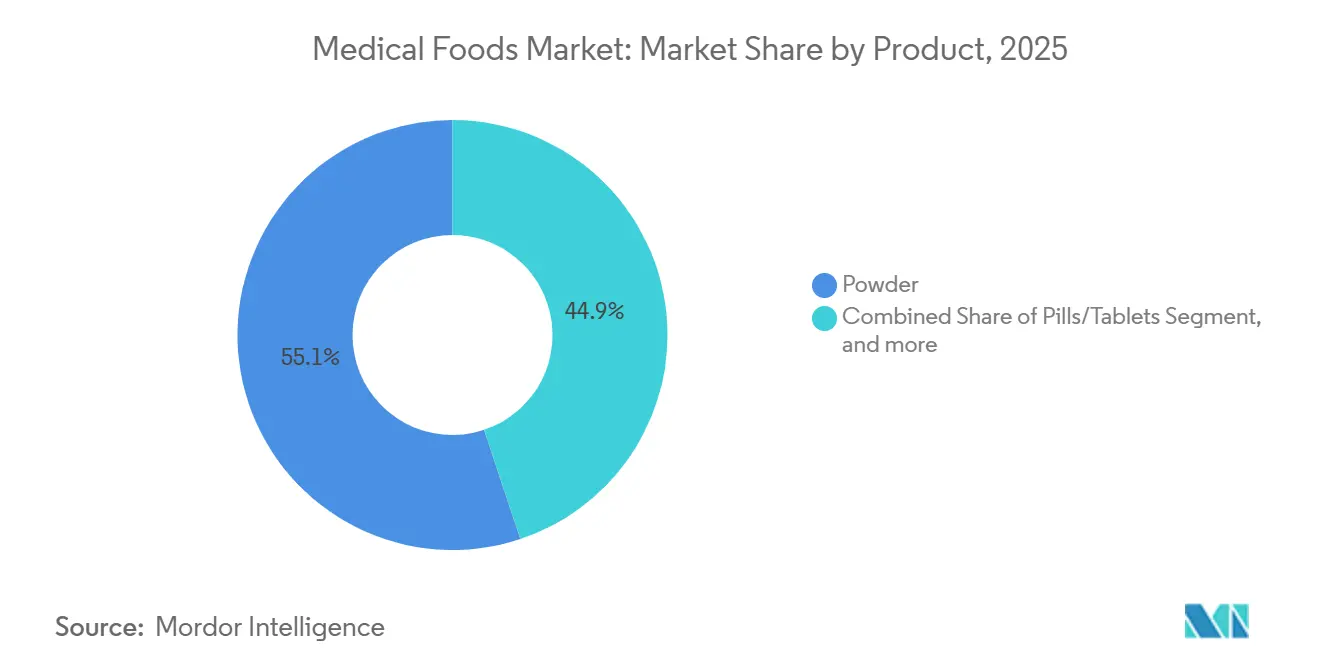

- By product category, powder formulations led with 55.12% of the medical foods market share in 2025, while soft-gel capsules are projected to post the fastest 7.54% CAGR over 2026-2031.

- By application, diabetic neuropathy accounted for 26.45% of the medical foods market size in 2025, and chronic kidney disease formulations are forecast to advance at a 7.43% CAGR through 2031.

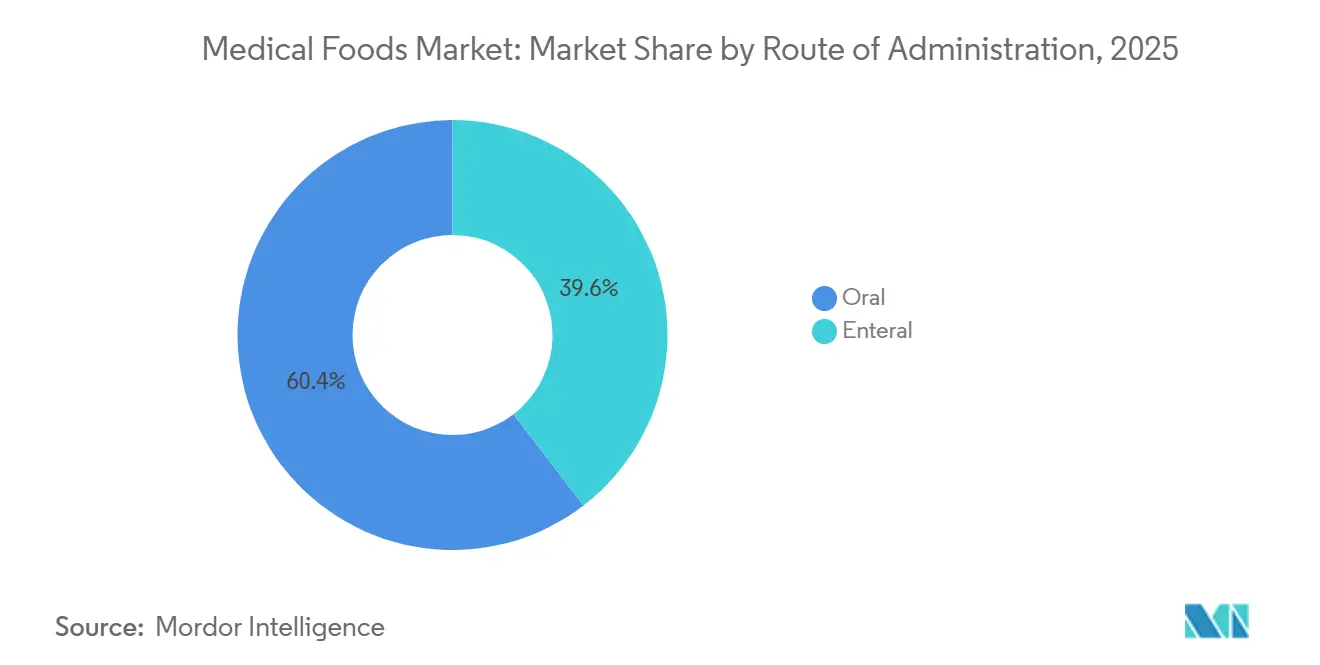

- By route of administration, oral delivery captured 60.43% share in 2025, whereas enteral formats are expected to expand at a 7.87% CAGR during 2026-2031.

- By patient group, geriatric consumers accounted for 52.76% of 2025 volume and remain the fastest-growing cohort, with an 8.11% CAGR projected through 2031.

- By distribution channel, hospital pharmacies distributed 46.76% of units in 2025, while online pharmacies are set to record the strongest 8.32% CAGR between 2026 and 2031.

- By geography, North America generated 42.43% of global value in 2025 and Asia-Pacific is anticipated to deliver the highest regional growth at a 6.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Foods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Chronic Disease Incidence | +1.4% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Escalating Geriatric Malnutrition Rates | +1.2% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Rising Demand For Personalized Medical Nutrition | +0.9% | North America, Western Europe, early adoption in China tier-1 cities | Medium term (2-4 years) |

| Technological Advancements In Formulation And Delivery | +0.8% | Global, led by North America and EU innovation hubs | Short term (≤ 2 years) |

| Expanding Healthcare Coverage In Emerging Economies | +0.7% | APAC core (China, India), spill-over to Southeast Asia and Latin America | Long term (≥ 4 years) |

| Integration Of Digital Health Tools For Patient Adherence | +0.6% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Chronic Disease Incidence

Non-communicable diseases such as diabetes, cancer, chronic kidney disease, and neurodegenerative disorders now account for 74% of global deaths, a burden that is expanding clinical adoption of condition-specific powders, liquids, and soft-gels[1]World Health Organization, “Global Health Estimates 2024,” who.int. The International Diabetes Federation projects a rise to 643 million adults with diabetes by 2030, supporting sustained demand for neuropathy and gastroparesis formulations. Oncology protocols at Memorial Sloan Kettering and MD Anderson already embed branched-chain amino acid-enriched blends for cachexia management. Nephrologists prescribe low-protein, high-calorie formulas that delay dialysis initiation, aligning directly with updated National Kidney Foundation guidelines. As chronic disease prevalence climbs, the medical foods market is becoming an indispensable element of outpatient disease management.

Escalating Geriatric Malnutrition Rates

Malnutrition afflicts up to 25% of community-dwelling older adults in high-income countries and roughly half of those in long-term care facilities[2]European Society for Clinical Nutrition and Metabolism, “ESPEN Guidelines 2025,” espen.org. Japan’s health authorities report sarcopenia in 22% of citizens aged 75 plus, prompting national screening mandates tied to protein-enriched prescriptions. In the United States, malnutrition-related hospitalizations cost Medicare USD 51 billion in 2024, catalyzing payer coverage of oral nutritional supplements as a cost-offset. A randomized controlled trial published in The New England Journal of Medicine found that 400 kcal daily of medical food reduced 90-day readmissions by 19%, reinforcing reimbursement arguments. These dynamics explain why geriatric demand remains the fulcrum of medical foods market growth.

Rising Demand for Personalized Medical Nutrition

Continuous glucose monitors, microbiome sequencing, and metabolomics are enabling patient-specific formulas that fine-tune macronutrient ratios and anti-inflammatory components. Abbott’s partnership with Levels Health synchronizes FreeStyle Libre data with Ensure Max Protein intake, enabling patients to adjust meals in real time. The ZOE PREDICT study demonstrated a 28% reduction in post-prandial glucose spikes through individualized nutrition[3]Nature Medicine, “Personalized Nutrition Study (ZOE PREDICT),” nature.com. Nestlé’s Vitaflo Choices delivers genotype-tailored amino-acid blends for phenylketonuria, signaling a new premium tier of therapy. China’s Healthy China 2030 blueprint allocates CNY 2 billion to clinical trials that validate precision nutrition. These developments add a discernible lift to the medical foods market, even though reimbursement codes for customization are still maturing.

Technological Advancements in Formulation and Delivery

Microencapsulation and taste-masking platforms such as Balchem’s VitaShure double shelf life for omega-3 and other unstable nutrients without refrigeration. Soft-gel formats enhance bioavailability of curcumin, coenzyme Q10, and medium-chain triglycerides, explaining their 7.54% CAGR in the medical foods market. Fresenius Kabi’s dual-chamber Nutriflex Lipid Plus mitigates oxidation until administration and has gained FDA 510(k) clearance across 500 hospitals. EMA’s 2024 guidance on pharmaceutical-grade excipients sets a high bar that smaller manufacturers can meet with contract partners rather than scale, redistributing innovation capacity. These advances widen the pipeline of clinically validated formats entering the medical foods market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Clinical Validation Requirements | -0.9% | EU, United States, China | Long term (≥ 4 years) |

| Limited Reimbursement and Pricing Pressures | -1.1% | North America, Western Europe, Japan | Medium term (2–4 years) |

| Low Awareness Among Healthcare Providers and Patients | -0.6% | North America, Europe, Emerging Asia-Pacific | Short term (≤ 2 years) |

| Supply Chain Volatility for Pharmaceutical-Grade Ingredients | -0.7% | Europe, North America, Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Clinical Validation Requirements

FDA draft guidance now requires randomized controlled trials for efficacy claims, adding USD 3–8 million and up to 3 years to time-to-market. In 2024, EFSA rejected 68% of health-claim submissions for medical foods due to insufficient mechanistic evidence. China’s regulator requires domestic trials even when foreign data exist, boosting costs by CNY 15 million per indication. Japan’s post-market surveillance mandate obligates manufacturers to report adverse events within 15 days, straining smaller players. These overlapping hurdles suppress new entrants and pull down the medical foods market CAGR.

Limited Reimbursement and Pricing Pressures

Medicare Part B excludes oral medical foods, forcing 85% of U.S. seniors to pay out-of-pocket USD 120 monthly. Commercial coverage slipped to only 12% of insured lives in 2024 as payers prioritized specialty drugs. Germany trimmed reimbursement rates by 8% to align with generics, while Japan pays only 70% of retail for enteral formulas and none for oral powders. European tenders shaved four percentage points from Fresenius Kabi’s gross margin, prompting SKU rationalization. Margins in the medical foods market remain under strain until public budgets expand or stronger outcomes data emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Soft-Gel Encapsulation Gains Traction

Soft-gel capsules, projected to rise at a 7.54% CAGR, outpace the broader medical foods market thanks to superior delivery of fat-soluble micronutrients. Powder formats retained 55.12% revenue in 2025 because hospitals favor bulk reconstitution for cost control, securing the largest medical foods market share among products.

Balchem’s VitaShure microencapsulation masks off-notes and extends stability, lifting patient adherence. Meiji’s Keto Caps use soft-gels to deliver precise doses of medium-chain triglycerides for Alzheimer’s protocols. Capital-intensive soft-gel lines create entry barriers, suggesting powders may slip below 50% share before 2029 without stalling overall market volume growth.

By Application: Chronic Kidney Disease Formulations Accelerate

Diabetic neuropathy held 26.45% of application-level demand in 2025, reflecting the clinical uptake of alpha-lipoic acid and benfotiamine blends. Chronic kidney disease lines are advancing at 7.43% CAGR, the fastest application tier, as nephrologists use low-protein, high-calorie powders to postpone dialysis.

Danone Nutricia’s Souvenaid cut hippocampal atrophy 45% in early Alzheimer’s and is widening coverage in France and Germany. Ultra-rare metabolic disorder products from Vitaflo and Ajinomoto Cambrooke command premium prices under orphan-drug-style reimbursement, padding profitability despite limited volume.

By Route of Administration: Enteral Delivery Gains Momentum

Enteral formats are forecast to grow at 7.87% CAGR, faster than the oral segment that held 60.43% in 2025, as payers migrate tube feeding to home care to prevent costly admissions. The medical foods market size allocated to enteral nutrition is therefore expanding faster than total category demand.

Fresenius Kabi and B. Braun dominate through bundled pump-and-formula contracts that lock in procurement departments. ISO 80369-3 connectors, mandated globally, have standardized safety, encouraging home use. Oral formats still anchor ambulatory care, but adherence challenges leave headroom for enteral to capture incremental share.

By Patient Group: Geriatric Segment Sustains Growth

Geriatric consumers accounted for 52.76% of 2025 volume and are advancing at 8.11% CAGR on the back of mandatory malnutrition screening in long-term care settings. The medical foods industry is tailoring high-leucine, calorie-dense formulations to combat sarcopenia.

Japan’s nationwide sarcopenia screening drives first-line protein prescriptions, while Morinaga’s Senior Protein Plus line capitalizes on retail pharmacy access. Pediatric and adult cohorts remain stable, but lower absolute numbers and specialized requirements limit their share escalation.

By Distribution Channel: Online Pharmacy Disrupts Traditional Models

Online pharmacies are clocking an 8.32% CAGR as payers test direct-to-patient fulfillment that trims retail mark-ups, positioning them as the fastest-growing conduit in the medical foods market. Hospital pharmacies still held 46.76% of units in 2025 due to discharge orders and enteral setups.

Abbott’s same-day Amazon Pharmacy tie-up shaved 15% off patient costs and set a new service benchmark. Nestlé’s acquisition of Persona Nutrition underlines the strategic premium on owning consumption data and automating refills. Compliance with FDA Drug Supply Chain Security Act rules has slowed smaller e-commerce entrants, but incumbents are investing in licensure infrastructure to stay ahead.

Geography Analysis

North America delivered 42.43% of global value in 2025, anchored by Medicare Advantage plans that funded oral supplements for 12 million beneficiaries. Canada expanded coverage for chronic kidney disease and cancer cachexia, while Mexico’s social insurer piloted enteral reimbursement for diabetes. Payer reluctance to include oral products under Medicare Part B, however, keeps the regional CAGR below the global pace.

Asia-Pacific is forecast to expand at a 6.54% CAGR, the highest among regions, as China’s GB 29922-2025 standard and India’s Ayushman Bharat reforms formalize reimbursement pathways. Japan’s super-aged society channels 60% of domestic spending to sarcopenia prevention, and Australia added motor neuron disease formulas to its Pharmaceutical Benefits Scheme. Despite a fragmented health-IT infrastructure, the medical foods market here is buoyed by demographic and policy tailwinds.

Europe captured 32% of global revenue in 2025, propelled by Germany, the UK, and France, each offering national reimbursement for defined indications. Germany’s daily reimbursement sits at EUR 80 for cancer cachexia enteral feeds. EFSA’s strict claim validation squeezes mid-sized entrants, yet harmonized rules reduce per-country duplication. Fiscal headwinds in Italy and Spain constrain reimbursement expansion, but private spending cushions demand. Outside the Big 3, white-space potential persists in CEE states where formularies are still evolving.

Competitive Landscape

Abbott Laboratories, Nestlé Health Science, and Danone Nutricia collectively dominate the medical foods market, capturing approximately 60% of hospital-pharmacy sales across North America and Europe. In 2024-2025, Abbott filed 14 patent applications for glucose-responsive medical foods designed to integrate with continuous monitoring systems. Concurrently, Nestlé is prioritizing the development of prebiotics that modulate the microbiome.

Fresenius Kabi and B. Braun have secured a strong market position by tying enteral pumps to proprietary formulas, locking hospitals into multi-year supply agreements. Vitaflo International and Ajinomoto Cambrooke are capitalizing on ultra-rare metabolic niches, leveraging orphan-like reimbursement models to achieve double-digit margins despite low sales volumes. Meanwhile, contract manufacturers in India and China are offering pharmaceutical-grade production capabilities at 40% lower costs, enabling mid-tier brands to shift from commoditized powder products to advanced, high-tech soft gels.

Digital adherence platforms are emerging as a cornerstone of competitive strategy. Abbott’s MyFreeStyle app integrates glucose telemetry with nutrition tracking, while Nestlé and Teladoc are embedding dietitian consultations into chronic-care solutions. Balchem’s USD 245 million acquisition of Albion Minerals reflects a strategic move toward vertical integration, focusing on chelated ingredients that enhance bioavailability in chronic kidney disease (CKD) powders. The competitive landscape is increasingly defined by the ownership of engagement data and differentiated ingredient intellectual property (IP), rather than solely by manufacturing scale.

Medical Foods Industry Leaders

Abbott Laboratories

Nestlé Health Science

Danone (Nutricia)

Fresenius Kabi

Primus Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nestlé Science unveiled research highlighting the benefits of bioactive supplementation for promoting healthy longevity. The findings suggest that specific bioactive compounds can support long-term health and aging.

- November 2023: Danone launched its first adult Foods for Special Medical Purposes (aFSMP) products in China to support patients recovering from surgery, cancer, or stroke. This expands Danone’s adult medical nutrition portfolio, complementing its existing tube-feeding products.

Global Medical Foods Market Report Scope

As per the scope of the report, medical foods are specially formulated products designed to meet the dietary needs of individuals with specific medical conditions or diseases. They are intended to manage such conditions under medical supervision and provide essential nutrients that may be lacking in regular diets. Unlike standard foods or dietary supplements, medical foods are regulated as foods but require a physician’s recommendation for use.

The Medical Foods Market is Segmented by Product (Powder, Pills/Tablets, Liquid, Soft-Gel Capsules, and Other Products), Application (Diabetic Neuropathy, Cancer-Related Cachexia, ADHD, Alzheimer's Disease, Metabolic Disorders, Gastro-Intestinal Disorders, Chronic Kidney Disease, and Other Applications), Route of Administration (Oral and Enteral), Patient Group (Pediatric, Adult, and Geriatric), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in value (USD) for the above segments.

| Powder |

| Pills / Tablets |

| Liquid |

| Soft-Gel Capsules |

| Other Products |

| Diabetic Neuropathy |

| Cancer-Related Cachexia |

| ADHD |

| Alzheimer's Disease |

| Metabolic Disorders |

| Gastro-Intestinal Disorders |

| Chronic Kidney Disease |

| Other Applications |

| Oral |

| Enteral |

| Pediatric |

| Adult |

| Geriatric |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Powder | |

| Pills / Tablets | ||

| Liquid | ||

| Soft-Gel Capsules | ||

| Other Products | ||

| By Application | Diabetic Neuropathy | |

| Cancer-Related Cachexia | ||

| ADHD | ||

| Alzheimer's Disease | ||

| Metabolic Disorders | ||

| Gastro-Intestinal Disorders | ||

| Chronic Kidney Disease | ||

| Other Applications | ||

| By Route Of Administration | Oral | |

| Enteral | ||

| By Patient Group | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What growth rate is forecast for the medical foods market between 2026 and 2031?

A CAGR of 5.12% is projected over 2026-2031, taking value to USD 35.51 million.

Which product type is growing fastest?

Soft-gel capsules are set to climb at a 7.54% CAGR because lipid matrices boost nutrient absorption.

Why are geriatric patients the largest consumer group?

Mandatory malnutrition screening in long-term care and supportive reimbursement lift geriatric volume to 52.76% with an 8.11% CAGR.

How will online pharmacies affect distribution?

Direct-to-patient models through platforms such as Amazon Pharmacy are expanding channel share at an 8.32% CAGR by lowering costs and automating refills.

What restrains U.S. growth despite high demand?

Medicare Part B excludes most oral medical foods, leaving seniors to shoulder USD 120 monthly out-of-pocket costs, which limits uptake.

Page last updated on: