Carglumic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

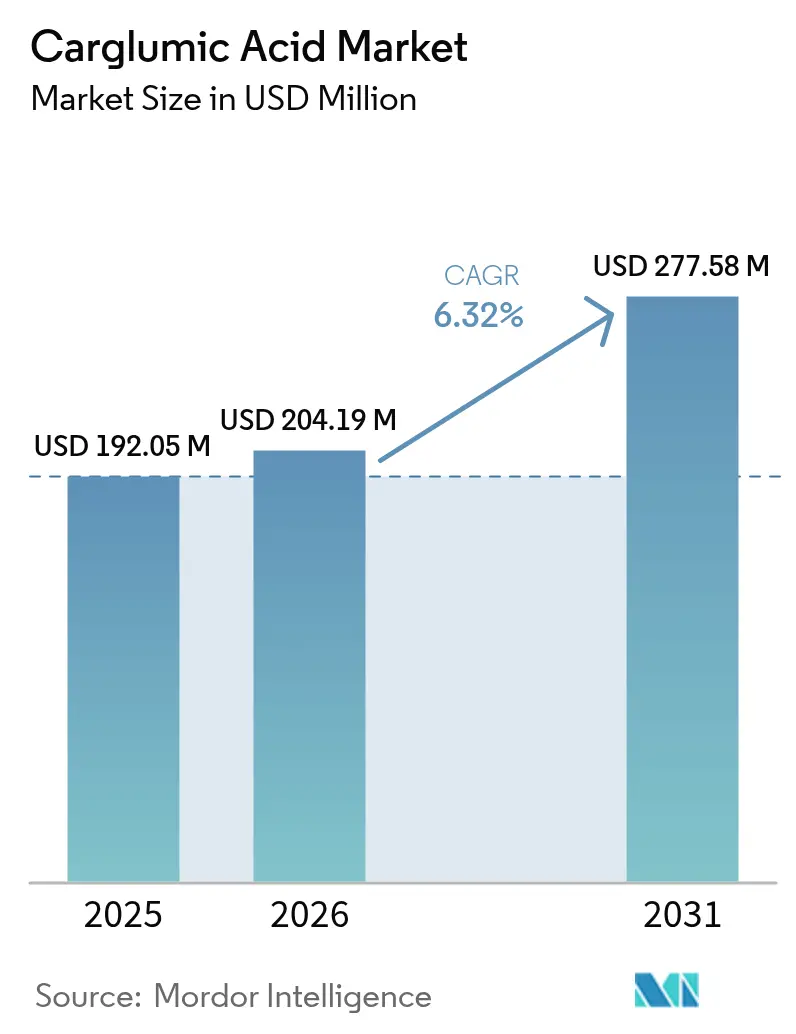

| Market Size (2026) | USD 204.19 Million |

| Market Size (2031) | USD 277.58 Million |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

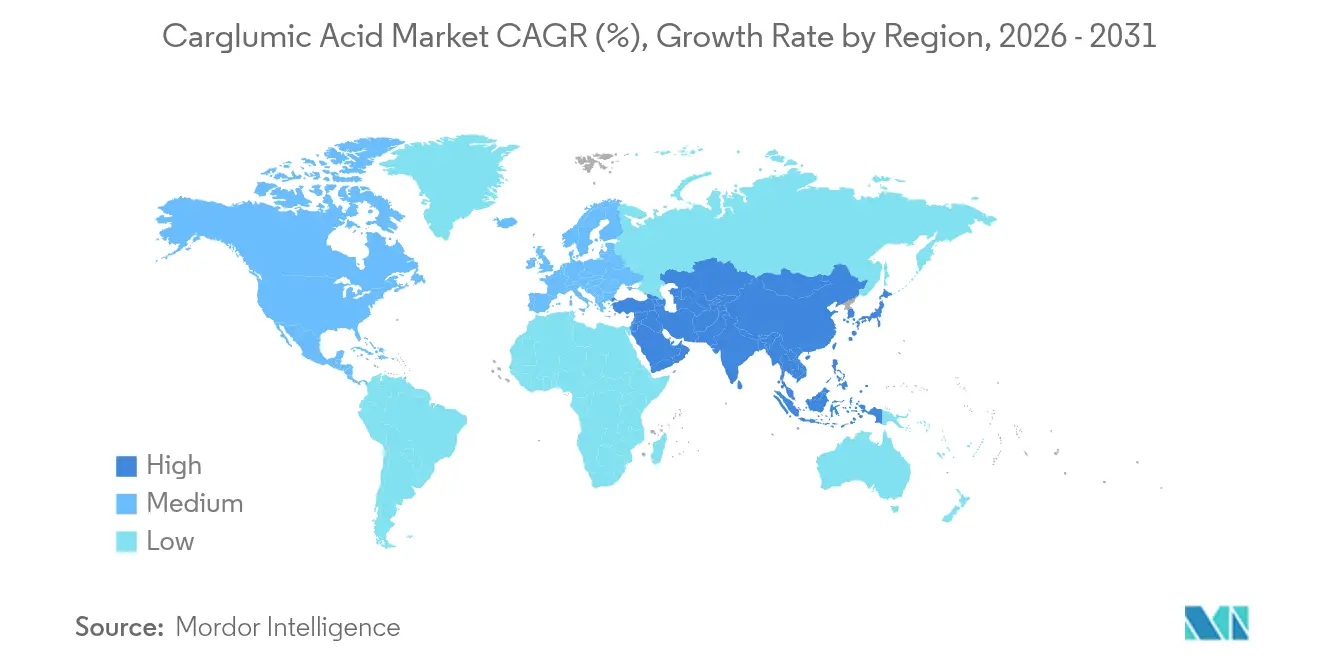

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carglumic Acid Market Analysis by Mordor Intelligence

The carglumic acid market size was valued at USD 192.05 million in 2025 and estimated to grow from USD 204.19 million in 2026 to reach USD 277.58 million by 2031, at a CAGR of 6.32% during the forecast period (2026-2031). Robust growth stems from earlier diagnosis of N-acetylglutamate synthase (NAGS) deficiency and organic acidurias, faster orphan-drug reviews, and wider newborn screening that feeds a predictable treatment pipeline. Single-source active pharmaceutical ingredient (API) dependence keeps supply chains tight but also supports premium pricing. Orally disintegrating tablets (ODTs) lead adoption, aided by taste-masking innovations that simplify pediatric administration. Hospital pharmacies dominate distribution, mirroring the acute-care setting of hyperammonemic crises, while e-commerce channels register the fastest growth on the back of telehealth uptake. Regionally, North America benefits from mature orphan-drug incentives, whereas Asia-Pacific (APAC) exhibits the quickest expansion thanks to newborn screening roll-outs and evolving rare-disease policies.

Key Report Takeaways

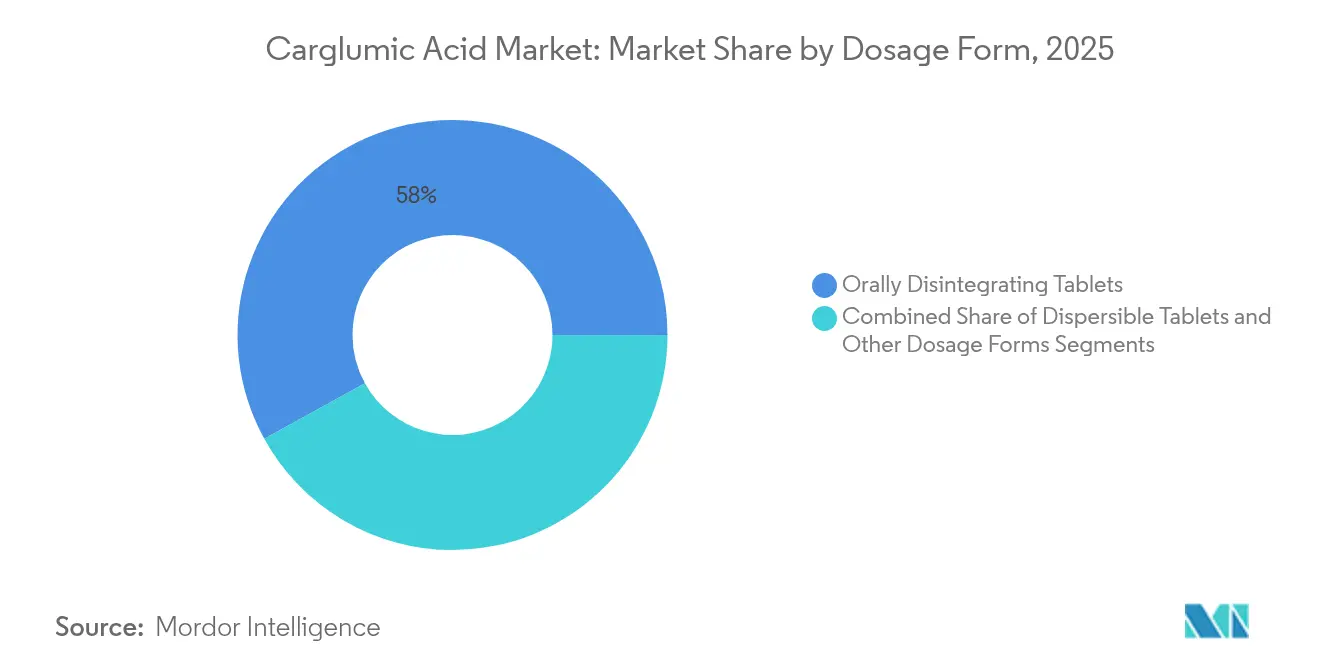

- By dosage form, ODTs commanded 58.02% of carglumic acid market share in 2025 and are tracking a 6.95% CAGR through 2031.

- By route of administration, oral products held 90.85% share of the carglumic acid market size in 2025 and are projected to rise at a 6.62% CAGR to 2031.

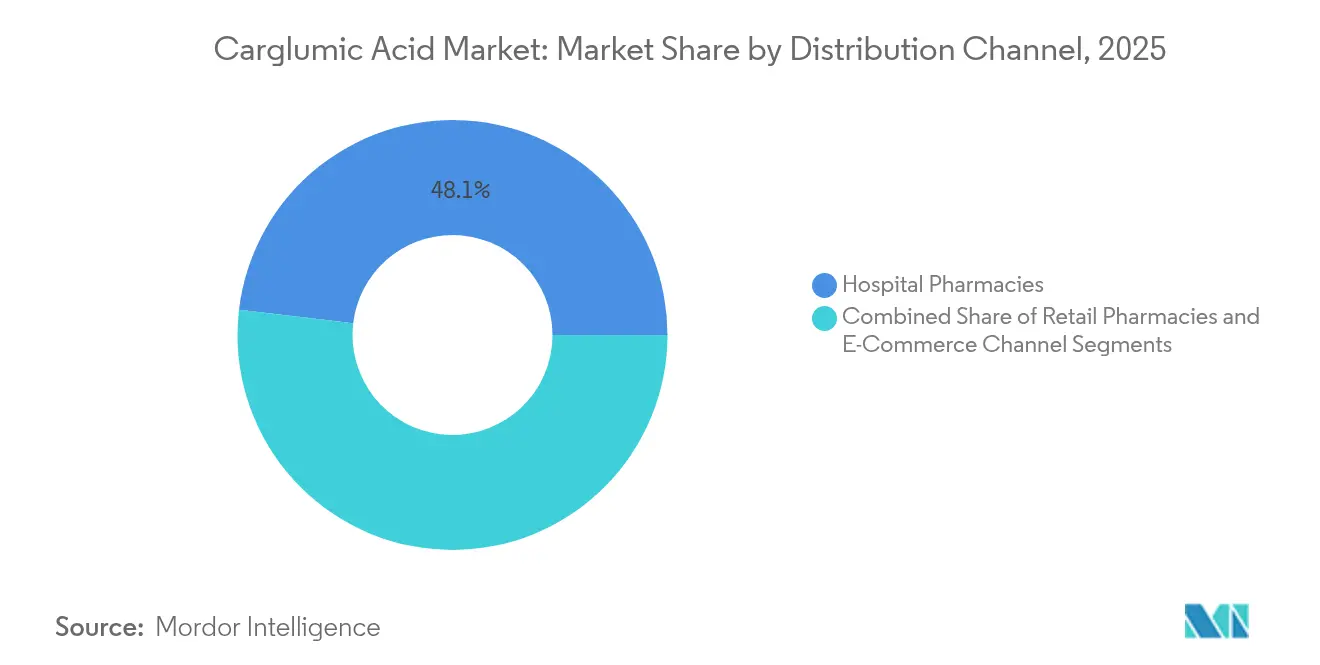

- By distribution channel, hospital pharmacies accounted for 48.12% of the carglumic acid market in 2025, while e-commerce is poised for a 7.55% CAGR through 2031.

- By geography, North America led with 39.12% revenue share in 2025; APAC is expected to expand at a 7.42% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carglumic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of NAGS Deficiency & Organic Acidurias | +1.2% | Global, with concentration in consanguineous populations | Medium term (2-4 years) |

| Accelerated Orphan-drug Approval Pathways | +0.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Broader Neonatal Hyper-ammonemia Screening Programs | +1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Reimbursement Expansion for Rare-disease Therapies | +0.9% | Global, with regional variations | Medium term (2-4 years) |

| Patient-tailored Micro-dosing & Compounding Innovations | +0.6% | North America & EU | Short term (≤ 2 years) |

| Strategic Stockpiling for Metabolic Crisis Management | +0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of NAGS Deficiency & Organic Acidurias

Growing diagnostic capacity is uncovering more inborn errors of metabolism, particularly in regions with high consanguinity. A Saudi newborn-screening study using tandem mass spectrometry found fresh cases that standard panels would have missed, illustrating how better analytics directly swell patient numbers. Hainan’s rare-disease cost burden climbed from CNY 34.26 million in 2019 to CNY 64.74 million in 2023 as detection improved, underscoring the economic ripple effect. Specialized metabolic centers are now embedded in tertiary hospitals, ensuring rapid confirmation and swift carglumic acid initiation. These hubs create a consistent feed of treated patients, underpinning sustained carglumic acid market growth. In parallel, advocacy groups advance registries that further refine prevalence data, shaping forecast accuracy for stakeholders.

Accelerated Orphan-Drug Approval Pathways

Regulators continue to shrink development timelines. The US FDA’s Rare Pediatric Disease Priority Review Voucher program recently granted a USD 150 million voucher alongside a fast-track label, trimming review cycles by up to 12 months and speeding revenue capture. The European Medicines Agency offers 10-year market exclusivity for designated orphan products, cushioning investment risk. China’s National Medical Products Administration has launched patient-focused rare-disease frameworks that open the world’s second-largest pharmaceutical arena to carglumic acid applicants. Collectively, these policies lower hurdles for innovators and stimulate portfolio investment, reinforcing a bullish carglumic acid market outlook.

Broader Neonatal Hyper-ammonemia Screening Programs

Universal screening is widening fast. Thailand’s nationwide review found that only 46.80% of recommended rare-disease medicines are registered, flagging the scale of future demand as screening widens. Tandem mass spectrometry now detects multiple organic acidurias in one run, cutting per-test costs and boosting detection efficiency. Positive results trigger direct referral to metabolic specialists, ensuring carglumic acid is prescribed before irreversible neurologic injury occurs. The result is a pipeline of early-stage patients whose lifetime therapy needs fuel the carglumic acid market size. Government grants for equipment procurement further institutionalize screening, ensuring long-term stability of demand.

Reimbursement Expansion for Rare-Disease Therapies

Payers are trialing subscription and outcome-based models that ease budget shocks linked to high-cost orphan drugs. European health technology assessments now accept surrogate endpoints and smaller sample sizes, smoothing reimbursement decisions for ultra-rare conditions. In Japan, a fixed-co-payment ceiling for chronic disorders curbs out-of-pocket expenses, preserving adherence to carglumic acid regimens. These innovations reduce financial friction for prescribers and patients, opening fresh therapy starts and underpinning carglumic acid market expansion. Manufacturers reciprocate with risk-sharing agreements that align pricing with real-world outcomes, reinforcing payer confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Orphan-drug pricing keeps therapy cost prohibitive | -1.1% | Global; acute in emerging markets | Medium term (2-4 years) |

| Severe gastrointestinal & infection-related adverse events | -0.7% | Global | Short term (≤ 2 years) |

| Single-source API & Intermediate Supply-chain Fragility | -0.5% | Global | Medium term (2-4 years) |

| Pipeline Gene-therapy & Ammonia-scavenger Competition | -0.4% | Developed and Emerging Markets | Long Term (>4 Years) |

| Source: Mordor Intelligence | |||

Severe Gastrointestinal & Infection-Related Adverse Events

Carglumic acid is generally well tolerated, yet vomiting, diarrhea, and abdominal pain can limit adherence, especially among infants and neonates already compromised by metabolic stress. Clinicians often resort to antiemetics or dose titration, complicating care pathways and inflating costs. Infection-related events add further risk because metabolic patients have reduced physiological reserves. Heightened pharmacovigilance requirements can delay adoption in newer markets, moderating near-term carglumic acid market uptake. Research into taste-masked, lower-dose ODTs aims to mitigate gastrointestinal effects, but clinical evidence is still emerging.

Orphan-Drug Pricing Keeps Therapy Cost Prohibitive

Global list prices remain steep, with many orphan drugs exceeding USD 100,000 per annum. Emerging economies face acute affordability issues, restricting formulary listings for carglumic acid. Evidence gaps in cost-effectiveness analyses compound payer hesitation, as traditional quality-adjusted life-year thresholds struggle to capture rare-disease value. While innovative payment models are gaining traction, immediate access in low-resource settings lags, restraining the carglumic acid market size in those geographies. Tiered pricing and patient-assistance programs partly offset the burden but fall short of universal coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: ODT Innovation Drives Market Leadership

The carglumic acid market size for orally disintegrating tablets was USD 111.43 million in 2025, equivalent to 58.02% revenue share. Rapid dissolution allows dosing during metabolic crises without water or nasogastric preparation, lowering aspiration risk in neonates. The segment is set for a 6.95% CAGR as taste-masking polymers and micro-encapsulation heighten palatability, boosting adherence. Manufacturers invest in continuous manufacturing that cuts batch costs and supports flexible global supply. Dispersible tablets, while trailing ODTs, retain value where feeding tubes enable precise titration, notably in intensive-care units. Compounded preparations fill small but critical gaps for dose extremes that commercial SKUs cannot accommodate.

Patient feedback highlights flavor novelty as a driver of sustained adherence, prompting R&D into berry and citrus profiles that mask carglumic acid’s natural acidity. Regulatory agencies permit accelerated stability testing for ODTs, shortening time to market for reformulations. These dynamics cement ODTs as the lodestar of dosage-form innovation, ensuring the segment remains central to the broader carglumic acid market through 2031.

By Route of Administration: Oral Dominance Reflects Treatment Protocols

Oral formulations held 90.85% of the carglumic acid market share in 2025, equating to USD 174.47 million. Clinical guidelines specify oral carglumic acid for first-line, chronic management of NAGS deficiency, underpinning a 6.62% CAGR to 2031. Injectable options, though niche, address acute scenarios where gastrointestinal absorption is compromised or where coma precludes swallowing. Pipeline research explores sub-lingual films that could offer even faster onset than current ODTs, yet commercial timelines remain tentative.

Outpatient care models value the convenience of oral therapy, enabling home-based metabolic control and reducing hospital bed-days. Bulk dispensing programs in Europe provide three-month supplies, lowering pharmacy visits and trimming system costs. Gene-therapy alternatives under clinical review may later compete for hyperammonemia care, but current uncertainty keeps the carglumic acid market rooted in oral pharmacotherapy for the forecast window.

By Distribution Channel: E-Commerce Disrupts Traditional Pharmacy Models

Hospital pharmacies captured USD 92.42 million in 2025, translating to a 48.12% share. Their privileged position reflects the need for immediate availability during hyperammonemic emergencies. However, e-commerce platforms grew 16% year-over-year and are on track for a 7.55% CAGR through 2031 as telemedicine removes geographic barriers. Caregivers value home delivery during long-term management, especially when monthly dose adjustments occur.

Digital pharmacies leverage automated refill reminders and adherence analytics, integrating with electronic health records and metabolic clinic dashboards. Retail pharmacies, although contending with lower margins, remain essential for in-person counseling, bridging discharge and community care. Policy frameworks in the EU now mandate temperature-controlled last-mile logistics, enhancing confidence in direct-to-patient distribution. This structural shift diversifies supply, bolstering overall resilience in the carglumic acid market.

Geography Analysis

North America’s carglumic acid market size reached USD 75.1 million in 2025, backed by established orphan-drug tax credits, newborn screening in all 50 states, and centralized metabolic networks. Reimbursement is generally comprehensive, with most private payers covering carglumic acid under specialty tiers. The region’s modest 5.18% CAGR reflects near-saturation in diagnosis and access, yet pipeline additions such as urease inhibitors are reinforcing clinical interest.

Europe retained a USD 63.3 million valuation in 2025, aided by contiguous rare-disease reference networks that standardize care. EMA’s 10-year exclusivity remains a magnet for manufacturers, while national health systems negotiate volume-based rebates that temper budget impact. The EHDS-driven data-sharing initiative promises richer real-world evidence, improving payer confidence and potentially speeding formularies for follow-on formulations.

Asia-Pacific generated USD 38.1 million in 2025 but exhibits the fastest trajectory, with a 7.42% CAGR to 2031 as India, China, and South-East Asian states expand newborn panels and align regulatory pathways. China’s Anti-Espionage Law briefly delayed foreign plant inspections, exposing single-source API risks; in response, domestic firms upgraded facilities to meet PIC/S standards, diversifying supply. In Latin America, Brazil spearheads policy harmonization via CONITEC evaluations, yet reimbursement lags remain. The Middle East and Africa see incremental progress as Gulf Cooperation Council states include carglumic acid in national formularies, whereas many sub-Saharan countries still rely on donor programs.

Competitive Landscape

The carglumic acid market hosts a handful of specialized producers, yielding a moderate concentration. Recordati Rare Diseases anchors leadership with its Carbaglu brand, supported by multi-centric trial data and a footprint spanning more than 60 countries[1]Recordati Rare Diseases, “Q1 2025 Financial Results,” recordati.com . The firm posted 11.9% revenue growth in Q1 2025, underscoring enduring demand for ultra-rare metabolic drugs. Ultragenyx strengthens the field with LEMS portfolio synergies and reported USD 139 million Q1 2025 revenue, signaling commercial vitality[2]Ultragenyx Pharmaceutical, “First-Quarter 2025 Results,” ultragenyx.com.

Strategic imperatives include API security; the US Department of Health and Human Services recently earmarked USD 105 million to relaunch domestic synthesis lines, lessening reliance on foreign inspection regimes[3]U.S. Department of Health and Human Services, “Strengthening Domestic API Manufacturing,” hhs.gov. Indian contract manufacturers are courting multinational partners, building dedicated cGMP suites to capture supply contracts and hedge geopolitical exposure. Competitive differentiation increasingly revolves around formulation advances—taste-masked micro-granules, abuse-deterrent coatings, and micro-dosing sachets—rather than pure price. Gene-editing entrants are monitoring the hyperammonemia space, yet regulatory and long-term safety hurdles postpone direct competitive pressure until after 2030.

Companies deploy digital patient-support programs that bundle adherence apps with nurse helplines, translating into persistency rates above 80%. Collaborative registries capture longitudinal outcome data, feeding post-marketing commitments and reinforcing brand-equity barriers. The interplay of exclusivity cliffs and biosimilar policies will shape the next decade, but manufacturing complexity and small patient pools temper the immediacy of price-based rivalry in the carglumic acid market.

Carglumic Acid Industry Leaders

Recordati Rare Diseases Inc

Dipharma Francis S.r.l

Biophore India Pharmaceuticals Pvt Ltd

Torrent Pharmaceuticals Ltd

Zydus Lifesciences Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA set the regulatory review period for VOYDEYA patent extension, signaling continued rare-disease innovation.

- May 2025: Recordati reaffirmed 2025 guidance after posting 11.9% Q1 revenue growth.

- May 2025: Ultragenyx reported Q1 2025 revenue of USD 139 million and reiterated full-year guidance of USD 640-670 million.

- March 2025: Prime Therapeutics highlighted pegzilarginase for Arginase 1 deficiency, with FDA review expected May-Jul 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the carglumic acid market as all prescription-grade formulations of carglumic acid used to treat confirmed cases of N-acetyl-glutamate synthase (NAGS) deficiency-related hyperammonemia, together with recurrent maintenance therapy dispensed through hospital, retail, or online pharmacies. Because carglumic acid is an orphan product, our analysts at Mordor Intelligence frame the market in value terms, capturing ex-manufacturer sales flowing through regulated channels.

Scope Exclusion. We do not size compounded preparations, investigational pipeline molecules, or off-label research reagents, so our numbers stay tethered to commercial demand alone.

Segmentation Overview

- By Dosage Form

- Orally Disintegrating Tablets

- Dispersible Tablets

- Other Dosage Forms

- By Route of Administration

- Oral

- Injectable

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-Commerce Channel

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed metabolic-disease clinicians, hospital pharmacists, and patient-advocacy coordinators across North America, Europe, and key Asia-Pacific economies. These conversations allowed us to test prevalence estimates, typical dosing patterns, and channel split assumptions that could not be teased out of secondary data alone, thereby sharpening model parameters.

Desk Research

We began by gathering publicly available evidence from tier-1 sources such as the U.S. Food & Drug Administration safety database, the European Medicines Agency orphan-drug registry, Medicare Part D utilization files, and national rare-disease surveillance registries in Canada, Japan, and Australia. Trade association white papers from the National Organization for Rare Disorders, peer-reviewed prevalence studies indexed in PubMed, and customs shipment data covering carglumic acid API flows enriched the baseline.

Annual reports, 10-K filings, and price lists from specialty-pharma manufacturers helped us benchmark average selling prices, while news archives accessed via Dow Jones Factiva tracked tender wins and new-indication approvals. This list is illustrative; many other documents were screened to validate inputs and close information gaps.

Market-Sizing & Forecasting

We built the 2025 baseline through a top-down and bottom-up blended approach. Prevalence-to-treated-cohort reconstruction from epidemiological sources supplied the demand pool; this was reconciled with sampled ASP × volume invoices gathered from selected hospital pharmacies to check totals. Key variables monitored include newborn screening coverage, therapy adherence rates, average tablet strength, orphan-drug price erosion, regulatory expansions, and regional reimbursement decisions. Multivariate regression with scenario analysis projects these drivers forward to 2030, and any residual gaps in bottom-up rolls are adjusted proportionally to observed supply-chain throughput.

Data Validation & Update Cycle

Model outputs pass two analyst reviews that flag anomalies versus historical consumption, currency swings, and new labeling changes. We refresh every twelve months, with interim updates when price controls, new generics, or pivotal trial results materially shift demand.

Why Mordor's Carglumic Acid Baseline Commands Reliability

Published estimates often diverge because each publisher frames the market through a different lens, selects distinct input years, or rolls pipeline optimism into current sales.

Key gap drivers include variation in therapeutic scope, contrasting price assumptions, and refresh cadence differences that can magnify currency effects or generics penetration. Our disciplined scope selection and annual data sweep keep the baseline stable yet current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 192.05 m (2025) | Mordor Intelligence | - |

| USD 137.2 m (2023) | Global Consultancy A | Excludes maintenance dosing beyond first year and relies on older FX rates |

| USD 270.0 m (2024) | Industry Insights B | Bundles experimental oncology indications and pipeline asset valuations |

In summary, our numbers rest on verifiable prevalence data, live price audits, and clearly documented adjustments, giving decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current global carglumic acid market size?

The carglumic acid market size is USD 204.19 million in 2026.

How fast is the carglumic acid market expected to grow?

The market is projected to post a 6.32% CAGR, reaching USD 277.58 million by 2031.

Which dosage form holds the highest share in the carglumic acid market?

Orally disintegrating tablets lead with 58.02% market share thanks to ease of pediatric use.

Why is Asia-Pacific the fastest-growing region?

Expanding newborn screening programs and newly formalized rare-disease reimbursement frameworks push APAC to a 7.42% CAGR.

What are the main restraints on carglumic acid uptake?

High orphan-drug pricing and gastrointestinal side effects limit adoption, particularly in cost-sensitive markets.

Who is the leading company in the carglumic acid market?

Recordati Rare Diseases, with its Carbaglu brand, currently holds the largest revenue share globally.

Page last updated on: