Halal Pharmaceuticals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

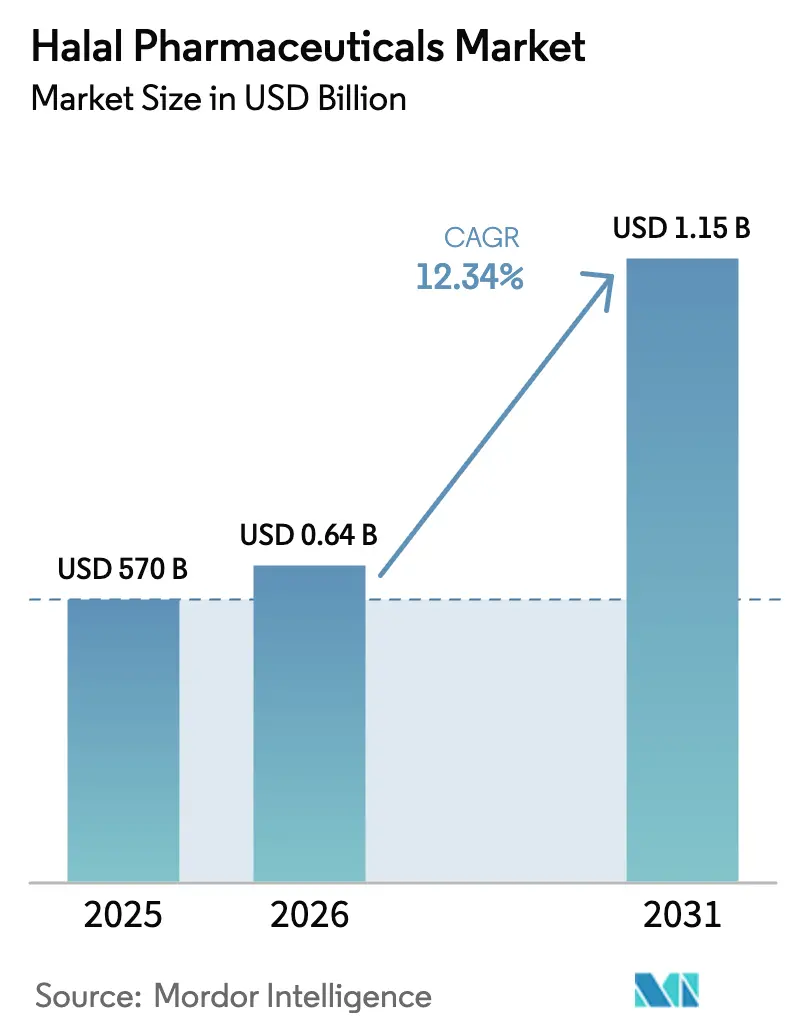

| Market Size (2026) | USD 0.64 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 12.34% CAGR |

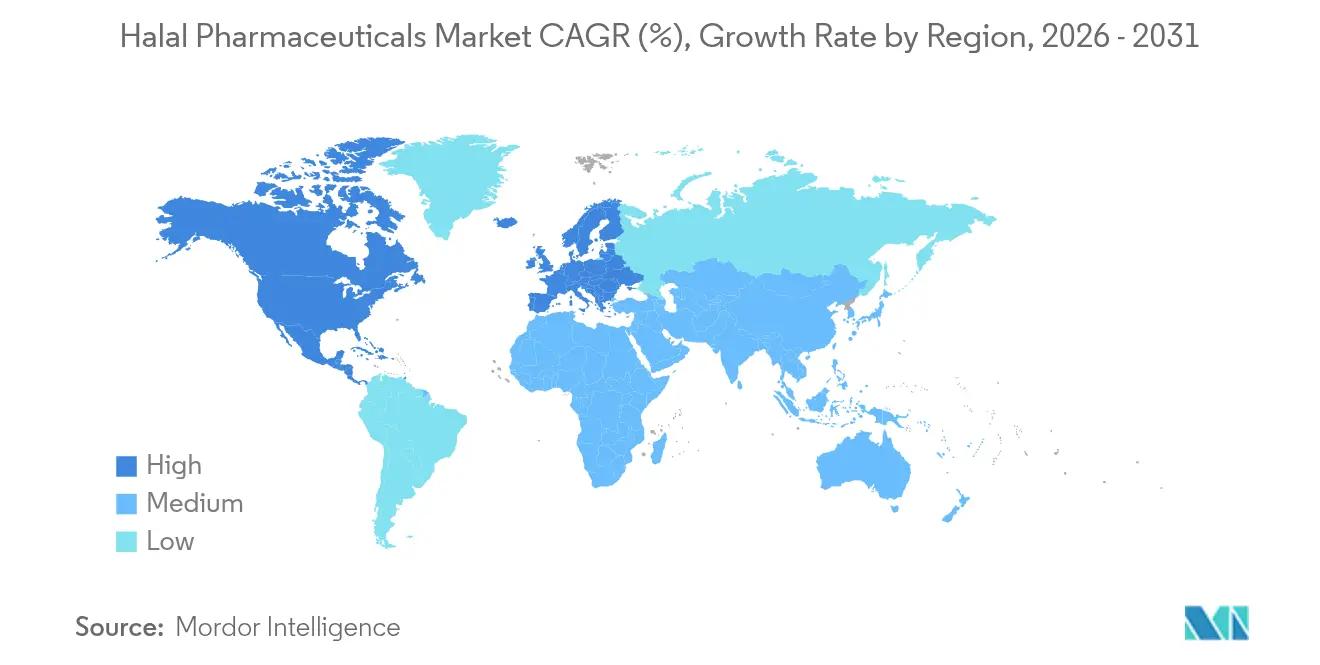

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Halal Pharmaceuticals Market Analysis by Mordor Intelligence

halal pharmaceuticals market size in 2026 is estimated at USD 640.34 million, growing from 2025 value of USD 570 million with 2031 projections showing USD 1.15 billion, growing at 12.34% CAGR over 2026-2031. Sustained growth stems from a confluence of demographic momentum, stricter certification rules, and production technologies that simplify animal-free formulation. Robust demand is anchored by the world’s 1.8 billion Muslim consumers who increasingly insist on medicines that meet both therapeutic and religious criteria. North American manufacturers benefit from well-established plants able to switch to halal-compliant runs, while dedicated green-field sites across Asia-Pacific shorten regional supply chains and reduce certification overheads. Regulatory deadlines such as Indonesia’s 2026 mandatory logo push have accelerated capital spending on isolated production lines, and AI-powered DNA assays now allow real-time porcine detection at trace levels, boosting trust in the halal pharmaceuticals market. Venture-backed formulation start-ups and contract manufacturing organizations (CMOs) are capitalizing on these shifts, offering turnkey halal platforms to large drug sponsors.

Key Report Takeaways

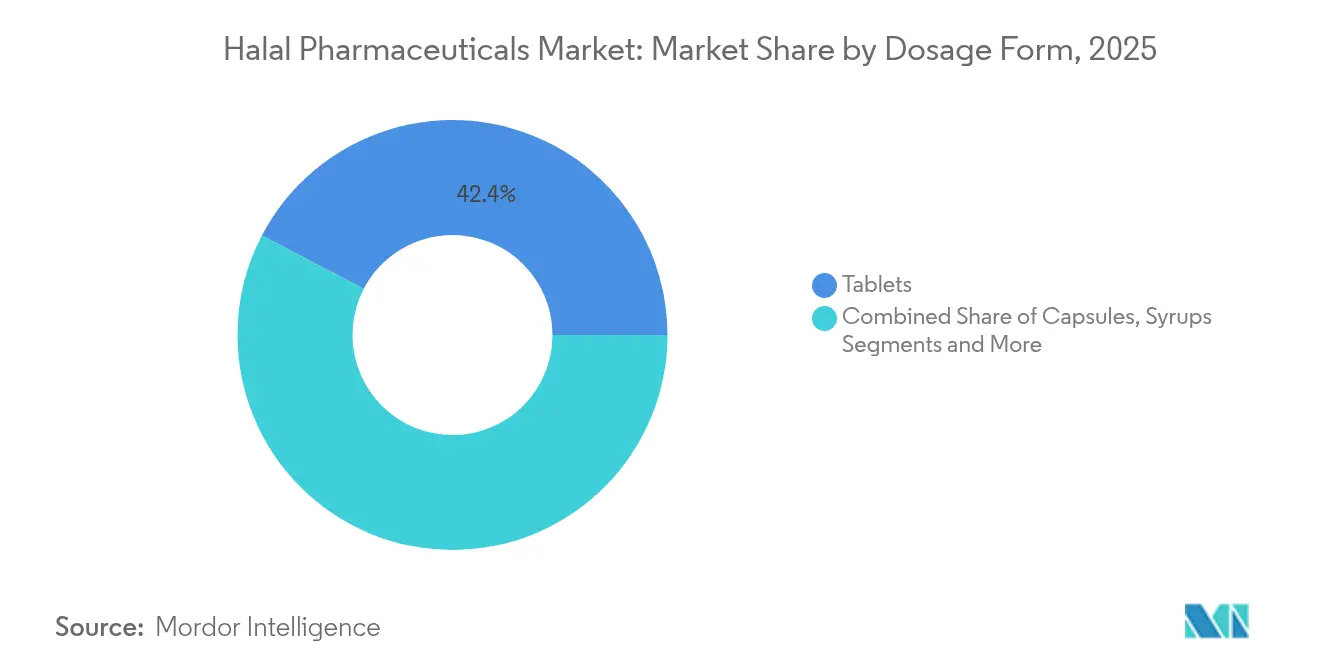

- By dosage form, tablets captured 42.35% of halal pharmaceuticals market share in 2025, whereas capsules are projected to expand at 13.31% CAGR through 2031.

- By drug class, analgesics held 22.85% share of the halal pharmaceuticals market size in 2025, while respiratory medications are on track for a 13.62% CAGR to 2031.

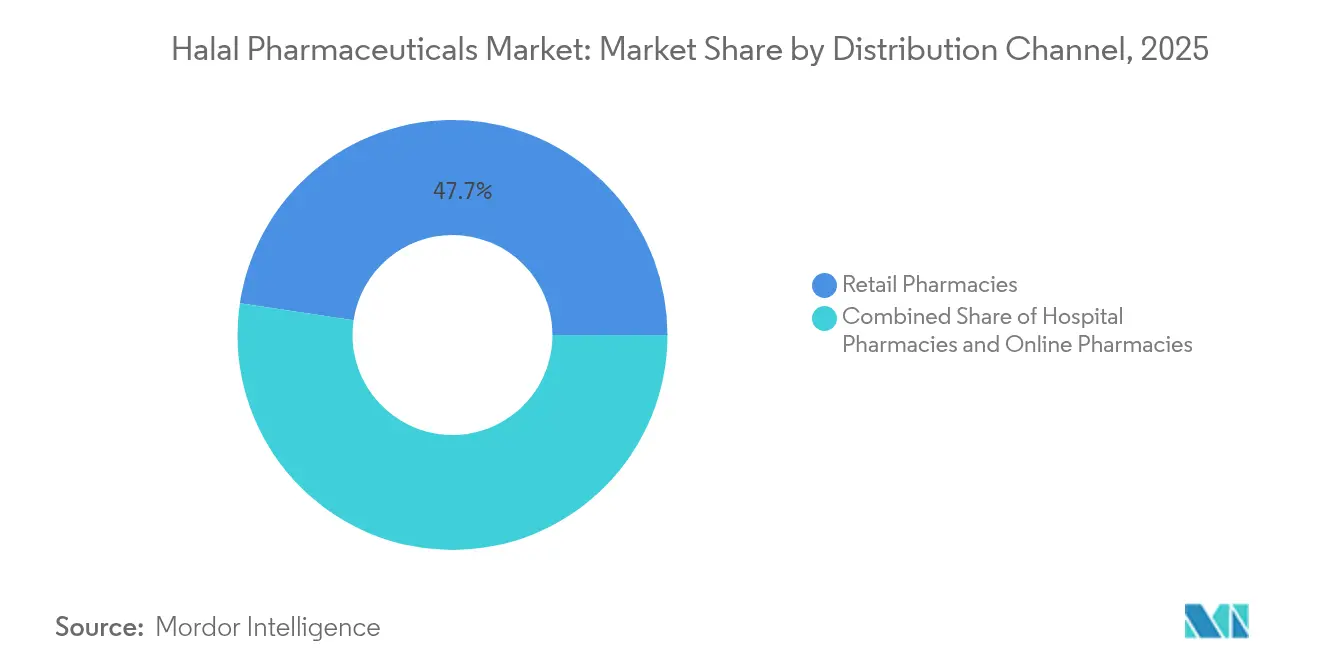

- By distribution channel, retail pharmacies accounted for 47.65% share of the halal pharmaceuticals market size in 2025; online pharmacies represent the fastest route, rising at a 13.88% CAGR to 2031.

- By geography, North America led with 42.30% halal pharmaceuticals market share in 2025, whereas Asia-Pacific is advancing at a 14.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Halal Pharmaceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Muslim population & vegan-friendly demand | +3.2% | Global, concentrated in APAC & MEA | Long term (≥ 4 years) |

| Growing elderly population & chronic-disease burden | +2.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Regulatory push for mandatory halal logos | +2.1% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| AI-enabled DNA testing to track porcine contamination | +1.7% | Global, early adoption in Malaysia & UAE | Medium term (2-4 years) |

| Surge in halal-compliant plant-based excipient supply chains | +1.4% | Global, hubs in Asia | Medium term (2-4 years) |

| Venture funding in Muslim-majority biotech hubs | +1.0% | MEA & Brunei | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in Muslim Population & Vegan-Friendly Demand

Muslim demographics, projected to top 2 billion within the next decade, continue to raise the base of patients seeking faith-aligned care. Rising disposable income across Indonesia, Türkiye, and Gulf states turns halal preference into an everyday purchasing norm rather than a festival-centric choice. In parallel, global interest in plant-based lifestyles widens the addressable pool of consumers who equate halal with cleaner labels and higher safety controls. Surveys show over 80% of community pharmacists in Canada and the United Kingdom still have limited familiarity with halal alternatives, opening a service gap that brand owners are filling through accredited training modules. Social-media-driven ethical consumerism further amplifies visibility for the halal pharmaceuticals market, prompting mainstream retailers to flag compliant SKUs on shelves and e-commerce landing pages.

Growing Elderly Population & Chronic-Disease Burden

Life expectancy gains in Muslim-majority and diaspora regions create a swelling cohort of seniors managing diabetes, hypertension, and osteoarthritis. Elderly patients often take multiple medications daily, magnifying the risk of non-adherence when products conflict with religious doctrine. Hospitals in the United States have started to stock halal-certified insulin, cardiovascular drugs, and analgesics to meet cultural competence metrics, showing clear linkage between accommodation and improved outcomes. Chronic-care demand also nudges formulators to swap porcine-based gelatin shells for hydroxypropyl methylcellulose (HPMC) capsules that provide comparable dissolution and shelf-life metrics. Over the medium term, the interaction between aging curves and chronic disease prevalence is likely to add close to +2.8 percentage points to the baseline CAGR of the halal pharmaceuticals market.

Regulatory Push for Mandatory Halal Logos (Indonesia 2026)

Presidential Regulation 6/2023 obliges every medicinal product sold in Indonesia to display an accredited halal symbol by 2026, transforming compliance from optional marketing into a prerequisite for market entry. Multinationals are now retro-engineering pig-derived excipients out of legacy blockbusters or setting up dedicated “halal-only” lines in Bekasi and Johor. The rule feeds a domino effect: Malaysia is revising MS 2424 to tighten cross-contamination clauses, while the UAE is drafting a unified Gulf Cooperation Council (GCC) pharmacopoeia annex for halal standards. The near-term scramble is costly but promises long-run efficiency as uniform protocols emerge.

AI-Enabled DNA Testing to Track Porcine Contamination

Real-time PCR paired with machine-learning algorithms pinpoints porcine DNA fragments down to 5 pg, cutting analysis turnaround from days to minutes. Automated sampling arms integrated into clean-room ceilings now screen every batch without halting production, shrinking recalls and certification lapses. Blockchain-based ledgers record each assay’s timestamp and geolocation, assuring regulators and consumers alike. Early adopters in Malaysia report double-digit gains in audit throughput and brand trust, reinforcing technology investment as a growth lever for the halal pharmaceuticals market.

Surge in Halal-Compliant Plant-Based Excipient Supply Chains

Demand for carrageenan, pullulan, and microcrystalline cellulose is rising as formulators pivot away from bovine and porcine derivatives. ASEAN ingredient hubs offer cost-competitive sourcing that meets both halal and vegan benchmarks, helping compress excipient lead times by 15% on average. Scale benefits feed back into lower finished-dose costs, countering the long-standing perception that halal products carry premium price tags.

Venture Funding in Muslim-Majority Biotech Hubs

Sovereign-wealth vehicles such as Saudi Arabia’s Public Investment Fund and Brunei Darussalam’s Yayasan are channeling early-stage capital into biopharma accelerators focused on halal biologics and vaccines. These programs pair state-of-the-art pilot plants with Sharia governance councils, shortening lab-to-market cycles and exporting know-how to Africa and Central Asia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs & dual manufacturing lines | -2.4% | Global, smaller manufacturers hit hardest | Short term (≤ 2 years) |

| Scarcity of harmonised global halal standards | -1.8% | Worldwide | Medium term (2-4 years) |

| Limited pharmacist awareness of halal alternatives | -1.2% | North America & EU | Medium term (2-4 years) |

| Supply-chain vulnerabilities for halal-grade gelatin | -0.9% | APAC-centric | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs & Dual Manufacturing Lines

Operating isolated clean-rooms, storage, and water-for-injection loops doubles depreciation and utilities for SMEs, depressing gross margins by as much as 7 points during the first two years post-conversion [1]Journal of Halal Science, Industry, and Business, “Cost Structure of Dual Manufacturing Lines,” halal-journal.org. Labor retraining and incremental validation runs add further burden. While CMOs with multi-tenant campuses can amortize costs across clients, single-brand factories often confront stark go-or-no-go decisions on halal specialization.

Scarcity of Harmonised Global Halal Standards

Fragmented certification regimes force parallel audits. A capsule batch cleared by Malaysia’s JAKIM still undergoes full dossier review by Indonesia’s BPJPH and the UAE’s ESMA, leading to redundant fees and staggered launch calendars. The resulting drag subtracts an estimated 1.8 percentage points from the baseline CAGR of the halal pharmaceuticals market until greater mutual recognition emerges.

Limited Pharmacist Awareness of Halal Alternatives

Community pharmacists in Toronto, Paris, and Sydney routinely substitute generics on cost grounds without checking excipient origin, undermining patient trust and dampening repeat uptake. Continuing-education modules remain optional, elongating the learning curve and tempering category velocity over the medium term.

Supply-Chain Vulnerabilities for Halal-Grade Gelatin

Although bovine-derived gelatin is permissible if sourced from animals slaughtered per Islamic rites, upstream abattoir oversight varies, occasionally halting shipments. Intermittent shortages compel emergency re-formulation or costly airfreight of HPMC shells, shaving close to 0.9 percentage points off anticipated growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Plant-Based Alternatives Drive Innovation

Tablets dominated the halal pharmaceuticals market, accounting for 42.35% revenue in 2025 thanks to mature presses, low unit costs, and patient familiarity. Capsules, however, are on a steeper trajectory with a 13.31% CAGR, propelled by advancements in HPMC and pullulan that maintain moisture barrier performance while eliminating animal inputs. Syrups retain importance for pediatrics and geriatrics, yet their growth rate lags due to sugar-content scrutiny and cold-chain logistics. Powders meet rising demand for personalized sachet dosing in sports medicine and metabolic disorders. Gels and ointments, although niche, benefit from topical application advantages that avoid ingestion concerns altogether.

Adoption of 3-D printed solid dosage forms is broadening design freedom, enabling polypill constructs that align multiple actives in one swallow, minimizing pill burden for chronic-care patients. Continuous manufacturing lines validated under the U.S. FDA’s Emerging Technology Program deliver near-zero batch variability, bolstering lot release speed and trimming scrap rates. These process gains lower conversion costs and enhance global competitiveness for halal-focused CDMOs, helping the halal pharmaceuticals market secure orders that once defaulted to conventional plants.

By Drug Class: Respiratory Medications Lead Growth Acceleration

Analgesics held 22.85% share of the halal pharmaceuticals market size in 2025 due to widespread chronic pain prevalence among aging Muslim cohorts. Post-pandemic sensitivity to air-quality risks propels respiratory drugs at a 13.62% CAGR, the highest among therapeutic clusters. Anti-inflammatory medicines maintain solid baseline demand, fueled by osteoarthritis management in markets where lifestyle patterns shift toward sedentarism. Cardiovascular agents present a long-run upswing potential as Gulf Cooperation Council nations confront elevated obesity rates. Gastrointestinal treatments see incremental gains where halal positioning overlaps with dietary guidelines that discourage alcohol-based solvents.

Innovation pipelines for anti-infectives focus on synthetic fermentation pathways that bypass porcine enzymes, eliminating a critical compliance hurdle without sacrificing potency. Specialty segments, notably orphan drugs, remain under-supplied in halal form, offering premium pricing latitude. Respiratory biologics formulated with animal-free stabilizers are entering phase-III trials, underscoring how next-generation modalities will broaden therapeutic scope.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Retail outlets commanded 47.65% share of the halal pharmaceuticals market in 2025, anchored by pharmacist counsel and immediate product access. Yet e-commerce is expanding 13.88% annually as mobile-centric consumers appreciate at-home authenticity validation via QR-coded certificates. Hospital pharmacies, though representing a smaller slice, exercise outsized influence on formulary decisions, increasingly embedding halal status in tender specifications.

Blockchain-verified e-pharmacies now upload laboratory certificates that match each SKU’s batch number, sharply reducing counterfeit risk. Tele-consult platforms integrate filters that propose halal equivalents during prescribing, nudging adoption beyond Muslim users to anyone seeking porcine-free options. Direct-to-consumer brands leverage subscription models for chronic medicines, bundling adherence apps that alert when refills are due, thereby reinforcing loyalty within the halal pharmaceuticals market.

Geography Analysis

North America accounted for 42.30% halal pharmaceuticals market share in 2025, benefiting from high chronic-disease incidence, sizable Muslim diasporas, and flexible manufacturing licenses that enable quick halal re-tooling. U.S. hospital buying groups have begun stipulating dual certification—FDA and accredited halal body—as part of inclusive procurement charters, boosting institutional demand. Canada’s centralized health system is piloting reimbursement incentives when halal substitutes increase adherence among elderly immigrants.

Asia-Pacific is forecast to post a 14.12% CAGR through 2031, underpinned by Indonesia’s upcoming 2026 mandate and Malaysia’s established MS 2424 standard that gives clarity to investors. Johor’s BioXcell and Selangor’s Halal Pharmaceutical Park offer tax holidays and fast-track permits, drawing multinationals to localize high-volume lines. China’s western provinces are courting Arab joint ventures to co-produce active pharmaceutical ingredients (APIs) using Sharia-compliant slaughterhouses for bovine-based inputs.

The Middle East & Africa region leverages cultural affinity and sovereign funding to bolster supply autonomy. Saudi Arabia’s Lifera CDMO, launched in 2023, is building a dedicated biologics wing able to fill 30 million vials annually for GCC distribution. The UAE’s new pharma law condenses licensing to 180 days and earmarks grants for animal-free adjuvant R&D. Nigeria and Egypt are evaluating import tariffs on non-certified drugs, signaling future upside for halal-approved imports.

Europe shows steady but lower-base gains. France and the United Kingdom together host nearly 10 million Muslims and are rolling out pharmacy awareness campaigns to mitigate adherence gaps. Germany’s generics companies experiment with halal line extensions to capture diaspora demand and to diversify away from price-eroding tenders within the conventional market. Regulatory heterogeneity persists, yet mutual recognition pilots among the Netherlands, Belgium, and Luxembourg hint at a coming shift toward bloc-wide treatment of halal audits.

Latin America remains nascent but promising; Brazil’s dominant halal meat infrastructure makes gelatin feedstock readily available, opening raw-material export lanes to formulation hubs worldwide.

Competitive Landscape

The halal pharmaceuticals market remains moderately fragmented. The firm’s tie-ups with Chinese API makers hedge supply risk and open corridors into Belt-and-Road countries seeking halal compliance. Catalent clocked USD 4.38 billion in fiscal 2024 sales, leveraging its network of soft-gel plants to offer turnkey, halal-compatible production suites for multinational sponsors [2]U.S. Securities and Exchange Commission, “Catalent FY-2024 10-K,” sec.gov. These players set the performance benchmark in an arena where smaller outfits often struggle with duplicate capital outlays.

Technology adoption is the main differentiator. Blockchain traceability modules, AI-driven contamination analytics, and continuous manufacturing hubs allow early movers to shorten campaign switchover by 30% and trim working capital tied up in quarantined lots. Licensing deals are proliferating: a UAE-based biologics start-up recently inked an exclusive agreement with a Canadian firm to co-develop halal monoclonal antibodies targeting respiratory syncytial virus. Private-equity funds in Singapore and Bahrain are scouring specialty niches such as ophthalmic gels, aiming to roll up fragmented producers into regional champions with end-to-end halal compliance.

Barriers to entry rest less on patents than on certification know-how, halal-compliant supplier networks, and the ability to scale cost-effectively. As mandatory regulations spread, late entrants face the prospect of expensive retrofits or strategic exits, potentially triggering an uptick in merger activity and reinforcing moderate concentration within the halal pharmaceuticals market.

Halal Pharmaceuticals Industry Leaders

Greenfield Nutritions

Vitabiotics Ltd

Canvita

Zaytun

Vitabiotics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2023: Indonesian Vice-President launched the Indonesian Halal Industry Master Plan 2023–2029 during the Indonesia Sharia Economic Festival

- June 2023: Saudi Arabia’s Public Investment Fund unveiled Lifera, a CDMO aimed at scaling local halal pharmaceutical output

Global Halal Pharmaceuticals Market Report Scope

As per the scope of the report, halal pharmaceuticals involve drugs, medicinal ingredients, traditional medicines, and cosmetics that contain permitted ingredients and are produced according to Islamic rules and regulations.

The halal pharmaceuticals market is segmented by dosage form, drug class, and geography. By dosage form, the market is segmented into syrups, capsules, tablets, and other dosage forms. By drug class, the market is segmented into analgesics, anti-inflammatory drugs, respiratory drugs, cardiovascular drugs, vaccines, and other drug classes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.

| Tablets |

| Capsules |

| Syrups |

| Powders |

| Gels & Ointments |

| Analgesics |

| Anti-inflammatory |

| Cardiovascular |

| Respiratory |

| Gastro-intestinal |

| Anti-infectives |

| Other Classes |

| Retail Pharmacies |

| Online Pharmacies |

| Hospital Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Tablets | |

| Capsules | ||

| Syrups | ||

| Powders | ||

| Gels & Ointments | ||

| By Drug Class | Analgesics | |

| Anti-inflammatory | ||

| Cardiovascular | ||

| Respiratory | ||

| Gastro-intestinal | ||

| Anti-infectives | ||

| Other Classes | ||

| By Distribution Channel | Retail Pharmacies | |

| Online Pharmacies | ||

| Hospital Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Halal Pharmaceuticals Market?

The Halal Pharmaceuticals Market size is expected to reach USD 640.34 million in 2026 and grow at a CAGR of 12.34% to reach USD 1.15 billion by 2031.

Which dosage form is growing fastest?

Capsules, particularly HPMC and pullulan variants, are expanding at a 13.31% CAGR through 2031.

Why are respiratory drugs a key growth segment?

Heightened post-pandemic awareness and high adoption of animal-free stabilizers are driving a 13.62% CAGR for respiratory medications.

Which is the fastest growing region in Halal Pharmaceuticals Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Halal Pharmaceuticals Market?

In 2025, North America accounts for the largest market share in Halal Pharmaceuticals Market.

Page last updated on: