Biobetters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

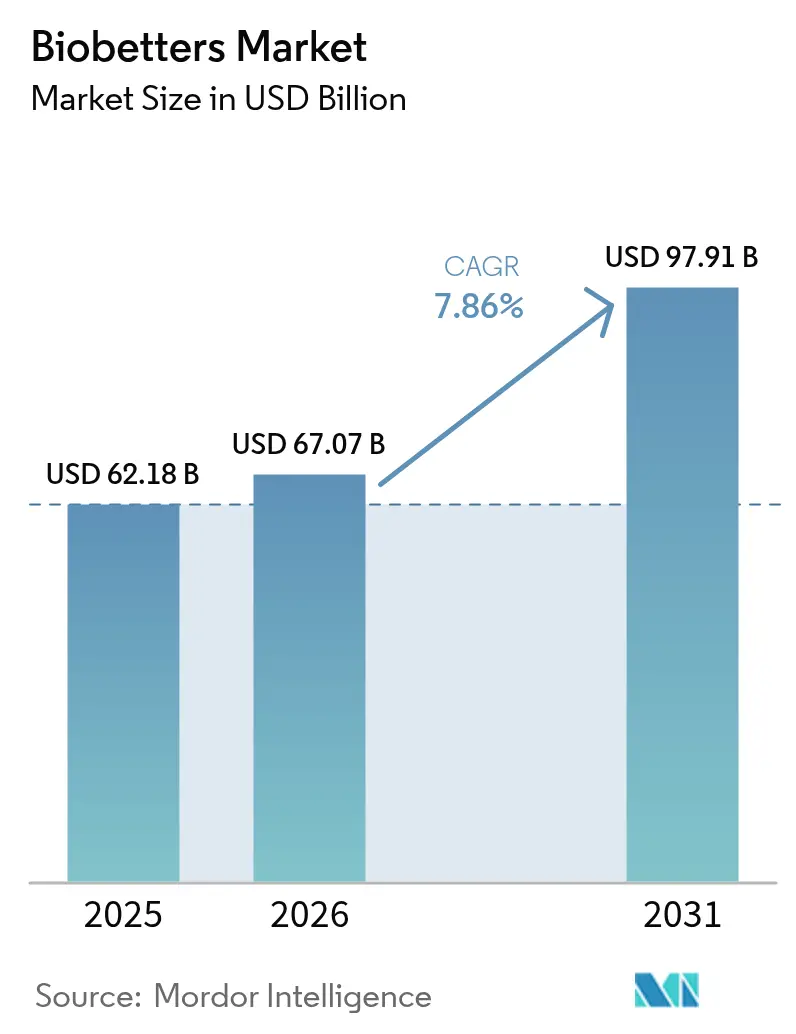

| Market Size (2026) | USD 67.07 Billion |

| Market Size (2031) | USD 97.91 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biobetters Market Analysis by Mordor Intelligence

The biobetters market size was valued at USD 62.18 billion in 2025 and estimated to grow from USD 67.07 billion in 2026 to reach USD 97.91 billion by 2031, at a CAGR of 7.86% during the forecast period (2026-2031). This expansion underscores how the pharmaceutical sector is shifting resources toward biologics that move beyond simple parity and instead deliver superior efficacy, safety, or convenience compared with their reference products. Key growth engines include an accelerating patent cliff for legacy blockbusters, steady regulatory support for clinically differentiated biologics, and strong payer appetite for therapies that can lower downstream healthcare costs. At the same time, manufacturing innovations are improving yield and consistency, reducing some historical barriers to entry. Competitive momentum has intensified as biopharma leaders pair in-house R&D with targeted acquisitions to secure advanced protein-engineering platforms, thereby broadening the addressable opportunity within the biobetters market.

Key Report Takeaways

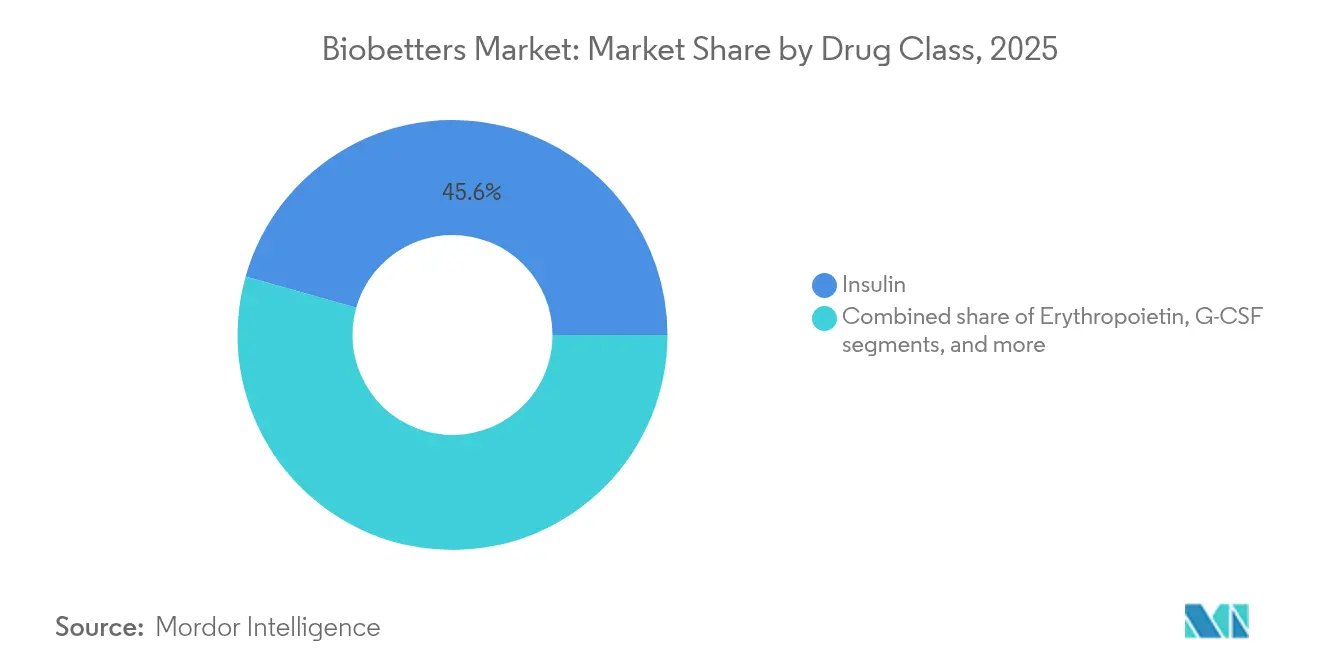

- By drug class, insulin led with 45.62% of the biobetters market share in 2025; monoclonal antibodies are forecast to expand at a 9.93% CAGR through 2031.

- By route of administration, subcutaneous delivery commanded 71.62% share of the biobetters market size in 2025, while oral formulations are projected to advance at a 10.21% CAGR to 2031.

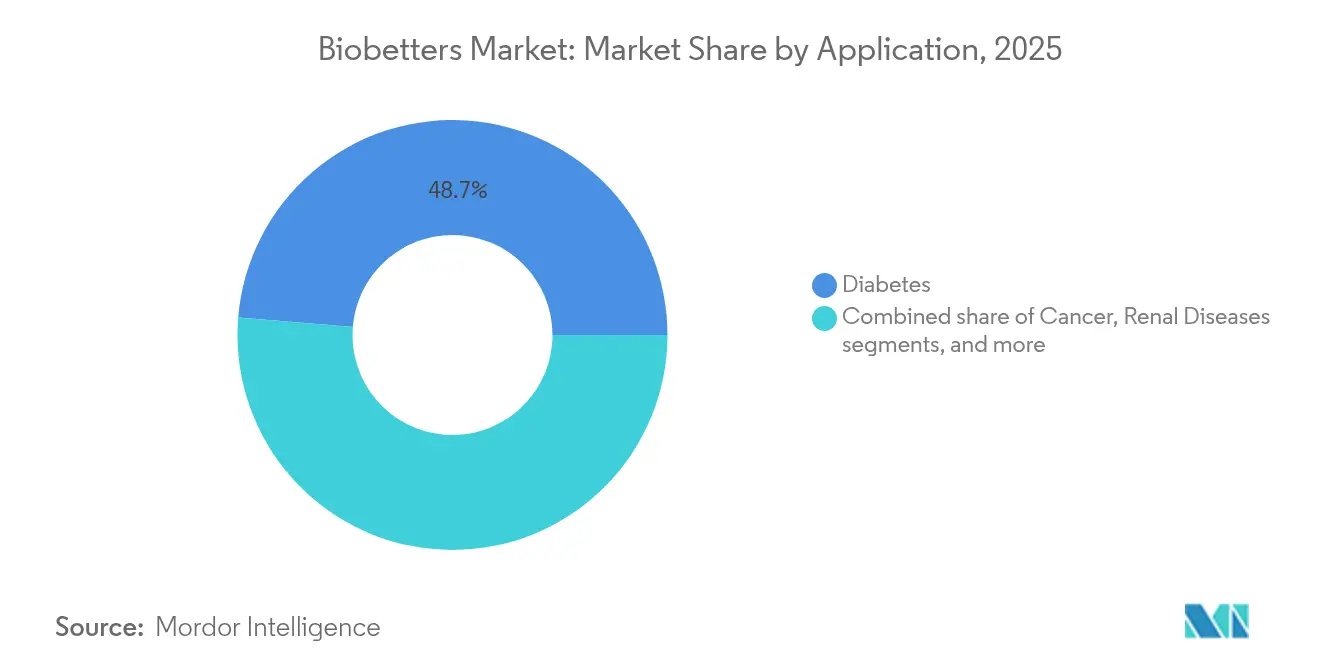

- By application, diabetes accounted for 48.71% of the biobetters market size in 2025 and oncology is advancing at an 11.02% CAGR through 2031.

- By distribution channel, hospital pharmacies held 53.41% of the biobetters market share in 2025; online channels are expected to register the fastest growth at 11.35% CAGR to 2031.

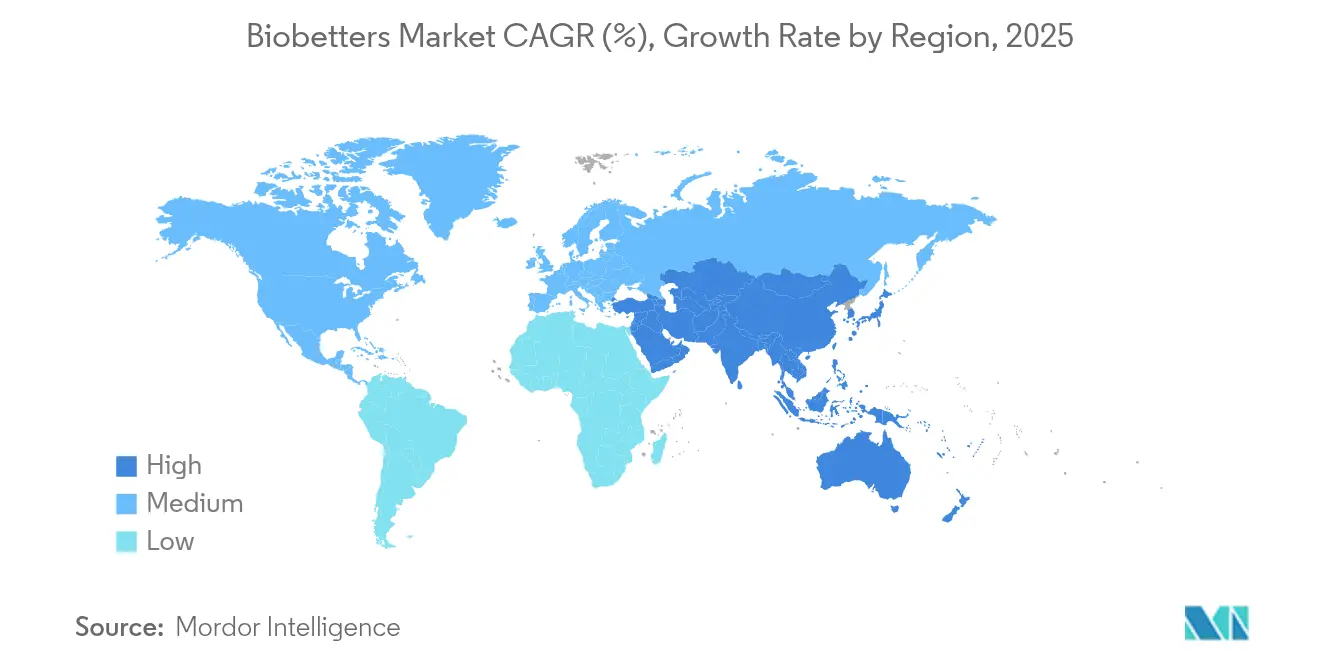

- By region, North America maintained 47.98% share of the biobetters market in 2025, whereas Asia-Pacific is on course for a 9.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biobetters Market Trends and Insights

Driver Impact Analysis*

| Driver | (`) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic diseases | +1.8% | Global; strongest in North America and Europe | Long term (≥ 4 years) |

| Patent expiry of blockbuster biologics | +2.1% | Global; concentrated in developed markets | Medium term (2-4 years) |

| Rising demand for long-acting formulations | +1.5% | North America and EU; spreading to Asia-Pacific | Medium term (2-4 years) |

| Advances in site-specific protein engineering | +1.2% | Global; led by United States and Germany | Long term (≥ 4 years) |

| Expansion of value-based reimbursement models | +0.9% | North America and Western Europe | Short term (≤ 2 years) |

| Increase in biologics contract development capacity | +0.7% | Global; major capacity in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Diseases

Chronic illnesses now account for the majority of global mortality, driving long-range demand for disease-modifying therapies. The World Health Organization projects chronic conditions will contribute to 73% of all deaths by 2030[1]World Health Organization, “Global Status Report on Noncommunicable Diseases,” who.int. Diabetes and oncology are at the forefront, where biobetters promise tighter glycemic control and more targeted cancer cell destruction. Novo Nordisk’s glucose-responsive insulin NNC2215 exemplifies this shift by modulating activity in response to real-time glucose fluctuations, thereby reducing hypoglycemia risk. Payers increasingly favor products that can avert hospitalizations and long-term complications, strengthening the economic case for premium-priced yet cost-effective biobetters. Regulators are likewise prioritizing expedited reviews for agents that address clear unmet needs in chronic care pathways.

Patent Expiry of Blockbuster Biologics

The rolling patent cliff is opening a USD 180 billion revenue gap as long-time staples such as Humira lose exclusivity[2]Health Affairs, “The Patent Cliff and Innovation,” healthaffairs.org. While biosimilars have captured a portion of this space, formulary hurdles and rebate structures have left significant untapped demand. Developers are seizing the opportunity to launch biobetter variants that extend patent life by improving dosing schedules, efficacy, or safety. FDA guidance on interchangeability has unintentionally tilted incentives toward superiority trials, where demonstrating clear clinical advantages can bypass switching-study complexities[3]Federal Register, “Guidance for Industry: Interchangeability of Biological Products,” federalregister.gov. Large-scale licensing deals in 2024 reflected this shift, with several agreements topping USD 1 billion as companies scrambled to backfill revenue lost to generic erosion.

Rising Demand for Long-Acting Formulations

Non-adherence to biologics carries a USD 100 billion annual cost burden globally. Long-acting technologies aim to solve this by cutting injection frequency. Eli Lilly’s partnership with Camurus underscores rising corporate interest in delivery platforms that extend GLP-1 activity from weekly to monthly. Pegylation and pro-drug conjugation allow steady drug release, improving real-world effectiveness and reducing clinic visits. Regulators are supporting streamlined pathways when pharmacokinetic superiority over older injectables is convincingly demonstrated.

Advances in Site-Specific Protein Engineering

Precision engineering methods such as sortase-mediated ligation are producing homogeneous antibody-drug conjugates with predictable drug-to-antibody ratios. FDA approvals of site-specific ADCs in 2024 signaled mainstream acceptance of these techniques. Glyco-optimization further enhances effector function, and cell-free synthesis accelerates variant screening, shortening development cycles. Because these technologies are hard to replicate, they also provide durable intellectual-property barriers against biosimilar erosion.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and manufacturing costs | -1.4% | Global; most acute in smaller biotech firms | Long term (≥ 4 years) |

| Intensifying biosimilar price competition | -1.1% | Developed markets; muted effect in emerging markets | Medium term (2-4 years) |

| Regulatory uncertainty for novel modification technologies | -0.9% | Global; most pronounced in the United States and European Union | Short term (≤ 2 years) |

| Limited access to high-throughput glyco-analytics platforms | -0.6% | Global; critical gap in emerging biotech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Development and Manufacturing Costs

Average outlays for a full biobetter program reach USD 2.3 billion, exceeding typical biosimilar budgets by a wide margin. Demonstrating superiority requires large, lengthy trials and specialized analytics that can add USD 50–100 million in characterization costs. Manufacturing is equally capital-intensive, often needing bespoke purification or formulation steps that cannot piggyback on existing biosimilar lines. These financial realities have prompted consolidation, with cash-rich pharma companies absorbing smaller innovators to secure pipeline depth.

Intensifying Biosimilar Price Competition

Biosimilar penetration has surpassed 80% within five years of launch in oncology categories, forcing originator products to discount by more than 50% on average. The resulting price erosion challenges the premium positioning essential for biobetter uptake. Pharmacy benefit managers leverage scale to negotiate steep rebates, particularly in TNF inhibitors and anti-VEGF classes. Developers therefore focus on areas where biosimilar replication is technically daunting, such as antibody-drug conjugates and long-acting insulins, to sustain differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Insulin Innovation Drives Market Leadership

Insulin retained 45.62% of the biobetters market share in 2025, cementing its status as the largest drug-class contributor to the biobetters market. Its dominance reflects both the rising global diabetes burden and the complexity of achieving precise glycemic control, which tilts competition toward clinically enhanced versions rather than straightforward copies. Monoclonal antibodies, although smaller in absolute revenue, posted the fastest growth, advancing at a 9.93% CAGR on the back of antibody-drug conjugate breakthroughs that widen therapeutic indices.

The segment’s momentum is illustrated by glucose-responsive candidates such as Novo Nordisk’s NNC2215, which automatically modulates potency to mitigate hypoglycemia, a risk reported in up to 70% of insulin-treated patients. These innovations extend patent life, create hefty switching barriers, and help sustain premium pricing inside the biobetters market. Growth in granulocyte-colony stimulating factors and anti-hemophilic factors continues, though uptake is tempered by biosimilar encroachment and, in erythropoietin’s case, lingering safety debates.

By Route of Administration: Subcutaneous Dominance Challenged

Subcutaneous injection accounted for 71.62% of the biobetters market in 2025 thanks to patient familiarity and the renal-sparing advantage of bypassing first-pass metabolism. Oral delivery, though still nascent, is clocking a rapid 10.21% CAGR as novel nanoparticle and enteric technologies safeguard proteins through the gastrointestinal tract. Should upcoming oral insulin programs demonstrate bioequivalence, the biobetters market size linked to diabetes therapy could widen sharply.

Intravenous routes remain indispensable for acute-care dosing and high-titer regimens, whereas inhaled administration targets respiratory conditions and systemic distribution of smaller proteins. Academic-industry consortia are overcoming gastric degradation through liposomal encapsulation and muco-adhesive polymers, raising hopes that once-daily oral forms can reach late-stage trials within the next five years. Success here would erode the injection barrier that currently discourages some patients from initiating biologic therapy.

By Application: Diabetes Leads While Oncology Accelerates

Diabetes therapies generated 48.71% of the biobetters market size in 2025, anchored by established reimbursement frameworks and the chronic nature of treatment. Real-world adherence data illustrate the economic value of better glycemic control, incentivizing payers to fund premium therapies that curb long-term complications. Oncology, however, is advancing at 11.02% CAGR and may narrow the revenue gap before 2030.

Recent trials of antibody-drug conjugates such as pivekimab sunirine, which achieved 85% overall response in a rare leukemia subtype, underscore the clinical impact of next-generation constructs. Oncology’s growth benefits from orphan-drug incentives and expedited pathways that shorten time to market, making it a focal point for venture capital and strategic pharma alliances seeking to enlarge the biobetters market.

By Distribution Channel: Hospital Dominance Under Digital Pressure

Hospital pharmacies contributed 53.41% of 2025 revenue within the biobetters market, reflecting cold-chain requirements and physician preference for controlled administration environments. Yet online channels are expanding quickly at an 11.35% CAGR, helped by robust logistics platforms that safeguard temperature-sensitive goods. Retail outlets remain a staple for stable chronic patients, while specialty pharmacies manage complex regimens for rare diseases.

COVID-19 catalyzed demand for home-based care, prompting big pharmacy chains to invest in cold-chain storage, remote-monitoring apps, and auto-replenishment services. Regulatory frameworks are evolving to secure e-prescription validation and reimbursement parity, suggesting that digital distribution will steadily chip away at hospital dominance across the biobetters market.

Geography Analysis

North America generated 47.98% of global revenue for the biobetters market in 2025. The United States anchors this leadership through an FDA framework that rewards clinical superiority and a payer system willing to reimburse differentiated therapies at premium rates. High venture capital density and an integrated academic-biotech ecosystem speed the translation of lab breakthroughs into late-phase assets. Canada, while smaller, mirrors these dynamics within a single-payer context that scrutinizes cost-effectiveness but still approves innovations offering quantifiable patient benefits.

Europe retains meaningful scale due to the European Medicines Agency’s centralized review, although national reimbursement negotiations introduce pricing complexity. Germany stands out for its pharmaceutical manufacturing base and reimbursement policies that acknowledge added therapeutic value. The United Kingdom’s post-Brexit regulatory independence could accelerate local approvals, making it an attractive launch pad for European expansion. Health technology assessments place a premium on real-world outcome data, channeling investment toward biobetters that provide measurable clinical gains.

Asia-Pacific is the fastest-growing region, posting a 9.31% CAGR that outpaces every other geography. China has rolled out policy reforms that condense review timelines for innovative biologics, enabling domestic champions such as Hansoh Pharmaceutical to attract global partners; Regeneron’s USD 2 billion license for dual GLP-1/GIP agonist HS-20094 is a prime example. Japan’s aging demographic fuels demand for chronic-disease biologics, while South Korea leverages government incentives and advanced manufacturing capacity to become a regional contract development hub. India’s vast patient pool and improving insurance coverage promise future upside, but pricing controls currently moderate premium uptake.

Competitive Landscape

Biobetters market competition is moderate, with top players balancing deep capital pools against the nimbleness of smaller innovators. Global pharmaceutical leaders wield expansive clinical networks, regulatory acumen, and manufacturing scale, allowing them to derisk late-stage programs. Specialty biotech firms differentiate through proprietary engineering technologies that create hard-to-copy molecules. Strategic licensing has thus become the prevailing commercialization route, illustrated by BioNTech and Bristol Myers Squibb’s USD 9.1 billion bispecific-antibody alliance and AbbVie’s USD 1.7 billion acquisition of FutureGen’s TL1A antibody portfolio.

Technological moats center on site-specific conjugation, advanced pegylation, and delivery systems that can stretch dosing intervals. These platforms not only enhance clinical profiles but also establish robust patent estates, shielding revenue from biosimilar encroachment. Market access dynamics are evolving as payers increasingly adopt value-based contracts, pressuring suppliers to link reimbursement to patient-level outcomes. Companies therefore invest heavily in real-world evidence programs that quantify reductions in hospitalization, improved adherence, and quality-of-life enhancements.

White-space opportunities persist in rare diseases and complex chronic conditions where biologic competition remains limited. With manufacturing capabilities becoming more distributed—particularly through Asia-Pacific CDMOs—mid-size firms can now scale production without building multi-billion-dollar facilities. Nonetheless, regulatory uncertainty around demonstrating clinical superiority and sustained pressure from biosimilar price erosion maintain a competitive tension that encourages mergers, technology-focused acquisitions, and risk-sharing development pacts with contract manufacturers and academic spinouts.

Biobetters Industry Leaders

Amgen Inc.

Novo Nordisk A/s

F. Hoffmann-La Roche

Biogen

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BioNTech and Bristol Myers Squibb announced a global partnership worth up to USD 9.1 billion to co-develop and commercialize the bispecific antibody BNT327 targeting PD-L1 and VEGF-A in solid tumors.

- June 2025: Eli Lilly entered an agreement with Camurus valued at up to USD 870 million to create long-acting GLP-1 and incretin drugs using FluidCrystal technology.

- June 2025: Hansoh Pharmaceutical granted Regeneron worldwide rights to dual GLP-1/GIP agonist HS-20094 under a deal comprising USD 80 million upfront and up to USD 1.93 billion in milestones.

- June 2024: ArriVent Biopharma and Alphamab Biopharmaceuticals signed an ADC collaboration that could total USD 615.5 million, leveraging Alphamab’s proprietary glycan-conjugation platform.

- June 2024: AbbVie licensed FG-M701, a next-generation TL1A antibody for inflammatory bowel disease, from FutureGen for USD 150 million upfront and up to USD 1.56 billion in milestones.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the biobetters market as the worldwide sales value of protein-based therapeutics that are deliberately engineered to outperform an approved reference biologic in at least one clinically meaningful aspect (efficacy, safety profile, half-life, dosing route, or patient convenience). Products are tracked from commercial launch through hospital, retail, and online channels and are classified by drug class, indication, route of administration, and geography.

Scope exclusion: veterinary or research-use-only biologic variants are left outside the frame.

Segmentation Overview

- By Drug Class

- Erythropoietin

- Insulin

- G-CSF

- Monoclonal Antibodies

- Anti-Haemophilic Factor

- Other Drug Classes

- By Route Of Administration

- Subcutaneous

- Intravenous

- Inhaled

- Oral

- Other Route Of Administrations

- By Application

- Cancer

- Diabetes

- Renal Diseases

- Neuro-Degenerative Disorders

- Genetic Disorders

- Infectious Diseases

- Other Applications

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To ground secondary signals, we hold structured calls and surveys with regulatory affairs leads, hospital pharmacists, clinical investigators, and CMC directors across North America, Europe, and key Asia-Pacific hubs. Their inputs refine adoption curves, average selling prices, and pipeline attrition rates that public data cannot capture alone.

Desk Research

Mordor analysts first map the universe using open datasets such as the FDA BLA archive, EMA Community Register, WHO ICTRP trial filings, SEER cancer incidence tables, IDF Diabetes Atlas, and trade association outlooks from groups like BIO and PhRMA. Financial clues are further parsed from company 10-Ks, investor decks, and clinical conference abstracts, then screened through paid repositories, including D&B Hoovers for company revenue splits, Dow Jones Factiva for deal flow, and Questel for patent families, to size competitive intensity. These sources form the factual spine; many more niche references support fine-grain validation.

Market-Sizing & Forecasting

A top-down demand pool, built from biologic spending, treated-patient prevalence, and new-approval counts, is cross-checked with selective bottom-up tallies (sample ASP x volume snapshots from distributor audits) before reconciliation. Variables such as annual BLA approvals, blockbuster patent expiries, biologic price inflation, insulin-using diabetes population, and oncology incidence trends feed a multivariate regression model to project 2025-2030 growth. Gaps in bottom-up granularity are bridged through expert-validated assumptions on penetration and dosing frequency.

Data Validation & Update Cycle

Outputs undergo three-layer analyst review, variance testing against external benchmarks, and anomaly flags. We refresh every twelve months, with mid-cycle tweaks if major regulatory or M&A events shift the landscape.

Why Mordor's Biobetters Baseline Commands Reliability

Published figures differ because firms choose distinct molecule scopes, base years, and conversion logic. Our disciplined definition, annual refresh, and dual-lens sizing reduce those swings. Key gap drivers include whether next-gen cell or gene therapies are folded in, the aggressiveness of pipeline success rates, and currency assumptions.

These contrasts show that when scope creep or dated baselines are removed, our 2025 number offers a balanced, transparent starting point that decision-makers can retrace with confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 62.18 B (2025) | Mordor Intelligence | - |

| USD 71.10 B (2025) | Regional Consultancy A | Broader scope adds gene-therapy adjacencies |

| USD 40.10 B (2024) | Trade Journal B | Omits insulin and G-CSF classes; uses 2024 FX averages |

| USD 52.80 B (2023) | Global Consultancy C | Earlier base year and static ASP escalation |

These contrasts show that when scope creep or dated baselines are removed, our 2025 number offers a balanced, transparent starting point that decision-makers can retrace with confidence.

Key Questions Answered in the Report

What is the current value and expected growth of the biobetters market?

The biobetters market stands at USD 67.07 billion in 2026 and is forecast to reach USD 97.91 billion by 2031, advancing at an 7.86% CAGR.

Which drug class holds the largest share of the biobetters market?

Insulin leads the drug-class landscape with 45.62% share thanks to its critical role in diabetes care and the technical complexity that favors differentiated products.

Why are monoclonal antibodies the fastest-growing segment?

Breakthrough antibody-drug conjugate technologies and site-specific protein engineering are lifting monoclonal antibodies at a 9.93% CAGR by improving tumor targeting and safety profiles.

Which region is expanding the quickest and what drives its momentum?

Asia-Pacific is growing at a 9.31% CAGR, fueled by regulatory modernization, new biomanufacturing capacity, and rising healthcare spending in China, Japan, and South Korea.

What is the primary commercial hurdle for biobetter developers in mature markets?

Intensifying price competition from biosimilars forces biobetter sponsors to prove clear clinical advantages that justify premium pricing within payer negotiations.

Page last updated on: