Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

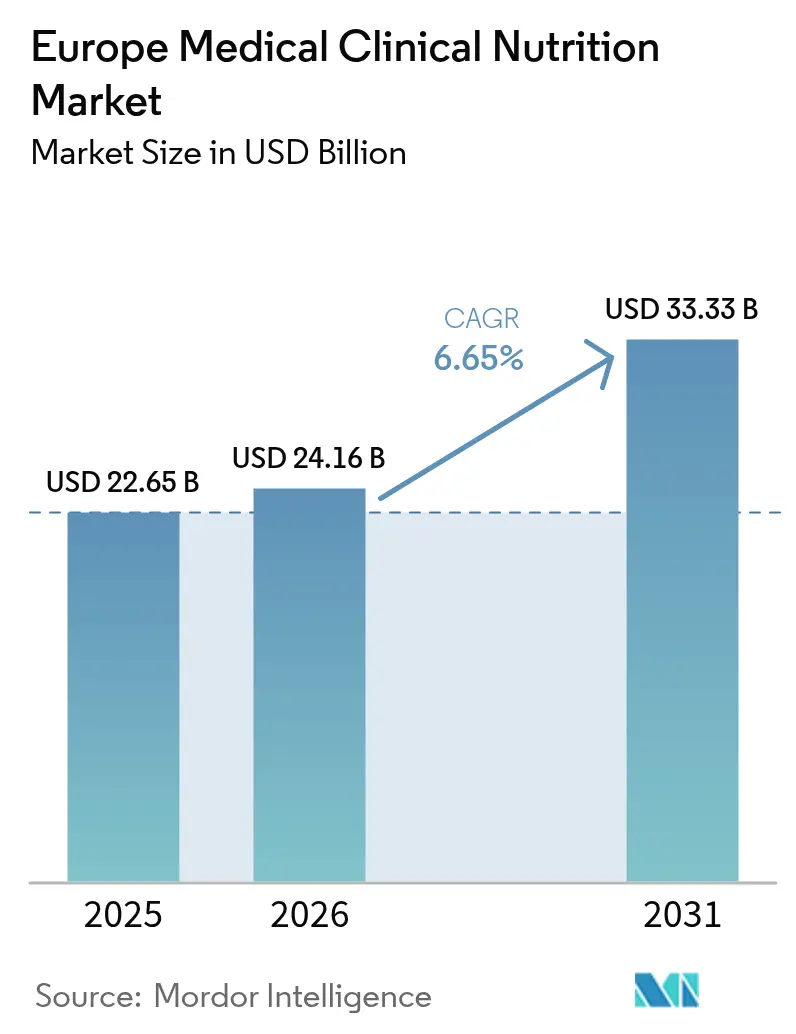

| Base Year Market Size (2025) | USD 22.65 Billion |

| Market Size (2026) | USD 24.16 Billion |

| Market Size (2031) | USD 33.33 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

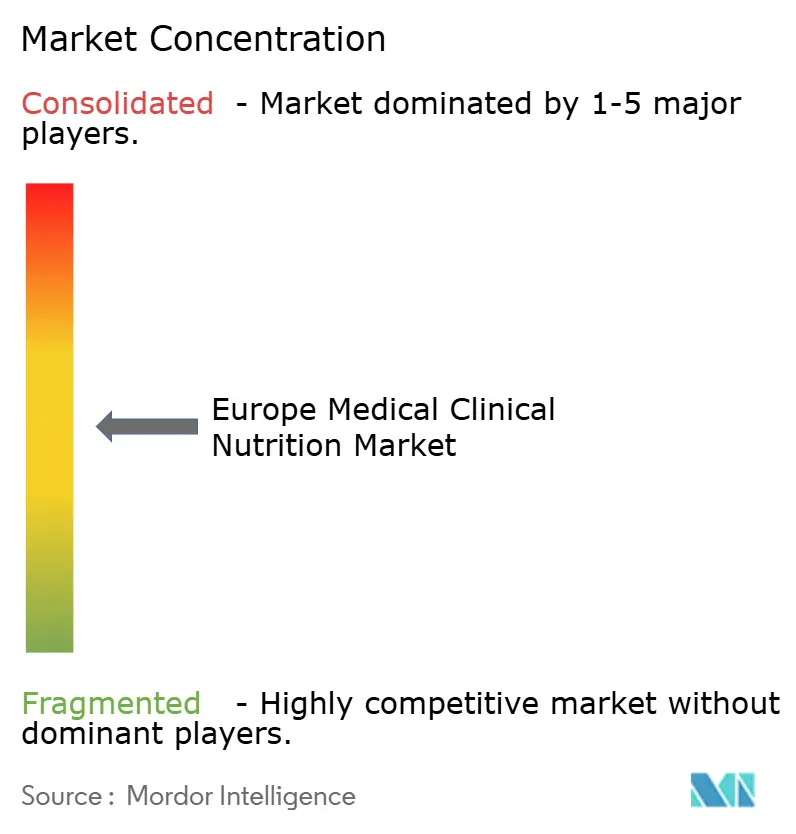

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medical Clinical Nutrition Market Analysis by Mordor Intelligence

The Europe medical clinical nutrition market size is projected to be USD 22.65 billion in 2025, USD 24.16 billion in 2026, and reach USD 33.33 billion by 2031, growing at a CAGR of 6.65% from 2026 to 2031. Demand no longer rises in small, linear steps. Instead, reimbursement reforms, mandatory peri-operative feeding protocols, and home-care expansion are entrenching clinical nutrition as a foundational therapy across hospitals, long-term-care facilities, and domiciliary settings. Enhanced Recovery After Surgery (ERAS) pathways now cover 85% of European surgical centers and typically trim two to three inpatient days per case. ESPEN’s 2024 guidelines re-classified sarcopenia as a stand-alone diagnosis, immediately opening reimbursement in Germany, France, and the Netherlands for high-protein oral nutrition supplements. Parallel growth in home parenteral nutrition (HPN) programs is accelerating product uptake in Scandinavia and the Benelux region, while the EU’s 2024 e-pharmacy directive is pushing double-digit online sales. The Europe medical clinical nutrition market is therefore shifting from discretionary supplementation toward protocolized, reimbursed therapy that improves outcomes and frees acute-care capacity.

Key Report Takeaways

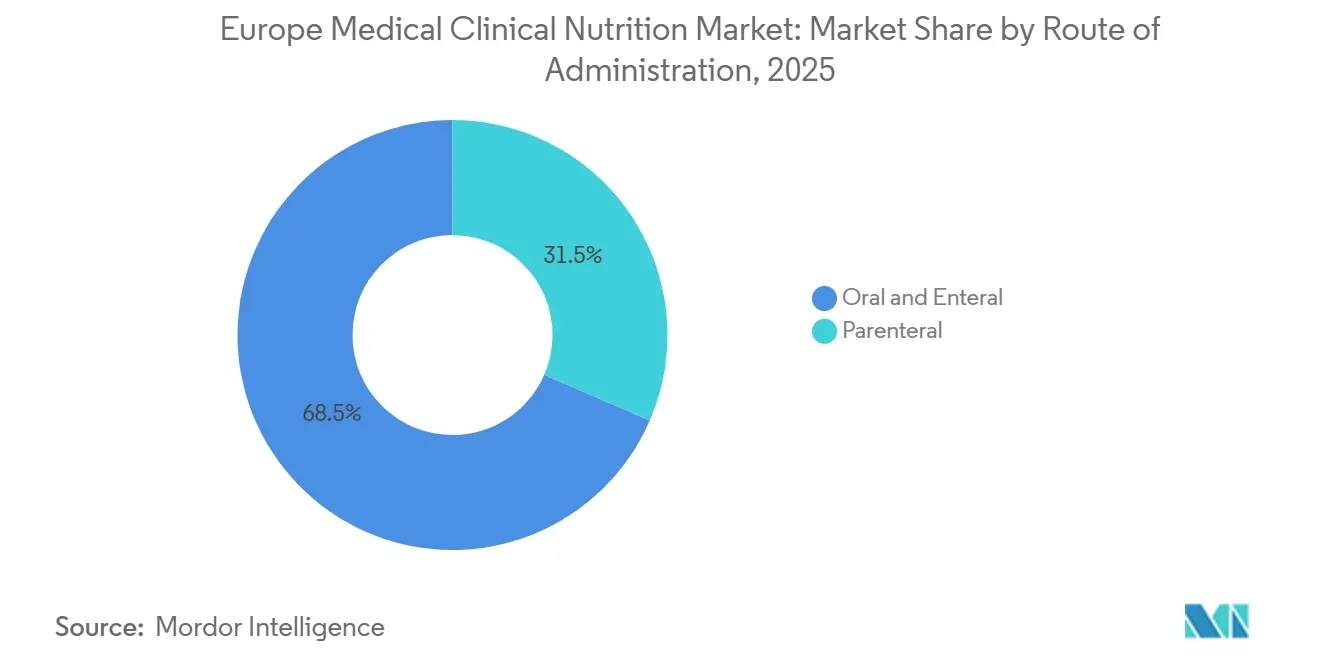

- By route of administration, oral and enteral nutrition held 68.55% of Europe medical clinical nutrition market share in 2025, whereas parenteral nutrition is advancing at an 8.25% CAGR through 2031.

- By product type, standardized enteral formulas captured 45.53% of the Europe medical clinical nutrition market size in 2025, while parenteral macronutrient solutions are projected to expand at a 7.75% CAGR to 2031.

- By application, oncology led with 31.15% revenue share in 2025; gastrointestinal disease formulas are the fastest-growing at a 9.82% CAGR through 2031.

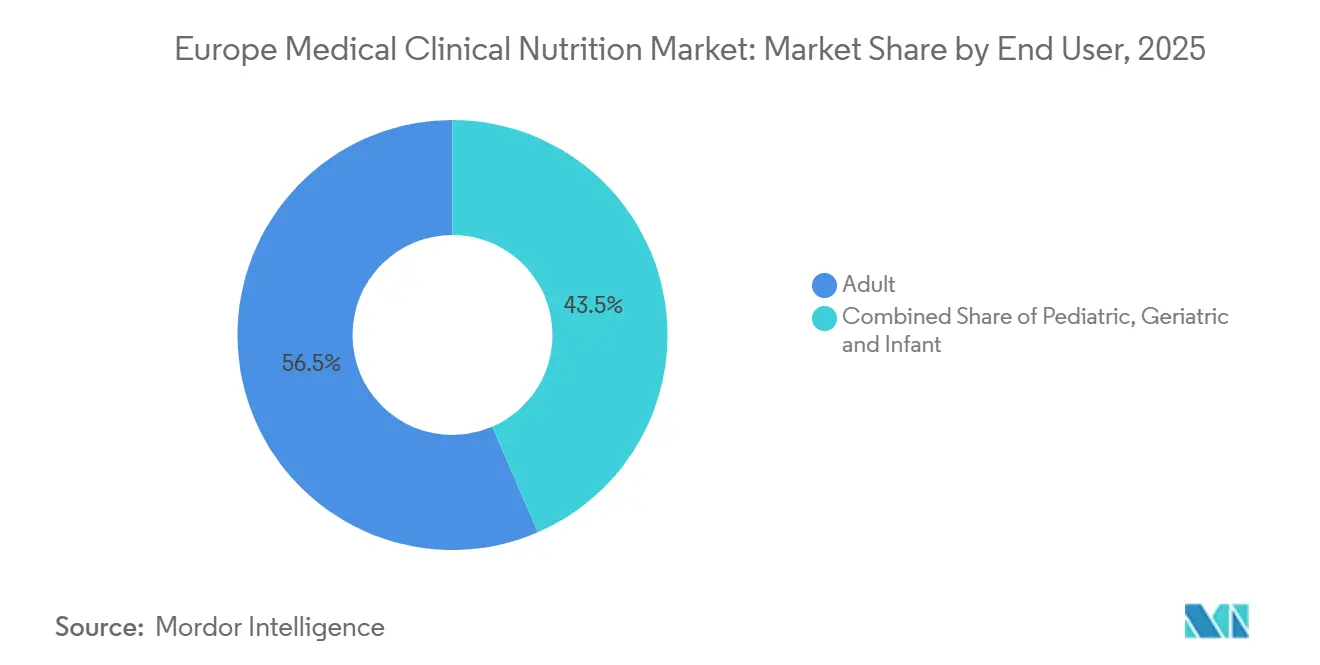

- By end user, adults commanded 56.65% of the Europe medical clinical nutrition market share in 2025, yet the geriatric segment shows the highest projected growth at 7.32% CAGR.

- By distribution channel, hospital pharmacies contributed 42.23% of 2025 revenue, whereas online pharmacies are set to rise at a 10.42% CAGR to 2031.

- By geography, Germany generated 32.23% of 2025 revenue, while the United Kingdom is forecast to post the quickest national growth at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Medical Clinical Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & metabolic disorders | +1.2% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Aging population & escalating healthcare spend | +1.5% | Germany, Italy, Spain, Nordics | Long term (≥ 4 years) |

| Home-based enteral nutrition adoption surge | +0.9% | Netherlands, Belgium, Scandinavia, UK | Short term (≤ 2 years) |

| ERAS-driven clinical-nutrition stewardship | +1.1% | Germany, France, UK, Switzerland | Medium term (2-4 years) |

| AI-enabled personalized nutrient profiling | +0.7% | Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| EU e-pharmacy liberalization broadening D2C reach | +1.0% | Spain, Italy, Poland, rural EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Metabolic Disorders

Cancer cases climbed to 4.2 million in 2024 and cachexia now affects up to 80% of late-stage patients, prompting ESMO’s 2025 protocol that pairs high-protein oral supplements with resistance exercise within 48 hours of diagnosis, improving six-month survival by 18%[1]European Society for Medical Oncology, “Cachexia Guidelines 2025,” ESMO.ORG. Type 2 diabetes counts 62 million European adults, and EASD backs low-glycemic enteral formulas that hold post-prandial glucose 35% lower than polymeric alternatives. IBD prevalence exceeded 3.2 million in 2024; ECCO guidelines upgraded exclusive enteral nutrition to first-line pediatric Crohn’s therapy, lifting remission to 65% and reshaping hospital formularies in Germany, France, and the Netherlands. Nephrologists now rely on renal-specific formulas to defer dialysis 12-18 months for 15% of adults with chronic kidney disease.

Aging Population & Escalating Healthcare Spend

Europe will host 150 million residents aged 65-plus by 2030; one-third of hospitalized seniors already present with protein-energy malnutrition, lengthening stays 4-6 days. ESPEN designated sarcopenia as a reimbursable condition in 2024, enabling high-protein oral nutrition supplement coverage across Germany, France, and the Netherlands. EU healthcare outlays reached EUR 1.8 trillion (USD 1.95 trillion) in 2024, but systematic nutrition screening cut total costs 12% through fewer complications[2]OECD, “Healthcare Expenditure Statistics 2024,” OECD.ORG. The NHS England framework mandated 24-hour malnutrition screening from April 2025 and standard prescription criteria for oral supplements, abolishing postcode disparities that had excluded 30% of qualifying patients.

Home-Based Enteral Nutrition Adoption Surge

Home enteral nutrition volumes jumped 22% in the Netherlands during 2025 as hospitals sought to release capacity and patients favored safer domiciliary care. Belgium and Denmark require five-day caregiver competency training, lowering catheter complications 35%. The UK introduced a national HEN tariff of GBP 120 (USD 155) per patient per week that freed 1,200 acute beds in 2025. Portable pumps with wireless telemetry now transmit adherence data, diminishing unplanned visits 28%.

ERAS-Driven Clinical-Nutrition Stewardship

ERAS bundles now mandate carbohydrate loading two to three hours pre-anesthesia and oral or enteral feeding inside 24 hours post-surgery in 85% of centers, cutting surgical-site infections 20%. Immunonutrition enriched with arginine and omega-3 fatty acids lowers postoperative complications 30% in major gastrointestinal cases. Germany reports 92% ERAS compliance in colorectal resections, while France’s national registry links ≥80% adherence to 15% fewer 30-day readmissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited patient / HCP awareness of clinical nutrition | -0.6% | Italy, Spain, Portugal, Poland, Romania, Bulgaria | Medium term (2-4 years) |

| Complex EU regulatory & reimbursement landscape | -0.8% | Pan-European; acute in Italy, Spain, Poland, Hungary | Long term (≥ 4 years) |

| Volatile polymer & packaging input costs | -0.5% | All EU manufacturers, spillover to Benelux & UK | Short term (≤ 2 years) |

| Stricter macronutrient caps in specialised formulas | -0.3% | Germany, France, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Patient / HCP Awareness of Clinical Nutrition

Malnutrition screening still reaches under 50% of admissions in Italy and Spain, leaving 40% of at-risk patients untreated. Only 35% of European general practitioners routinely prescribe oral nutrition supplements, citing limited product knowledge. Rural Portuguese uptake of validated tools such as MUST stands below 30% despite a national campaign that trained 5,000 physicians in 2025. Patient misconceptions persist; 70% of cancer patients in Italy and Spain do not know nutritional therapy can mitigate chemotherapy-related weight loss. Eastern Europe is further constrained by dietitian-to-patient ratios of 1:10,000 versus 1:2,500 in Western Europe.

Complex EU Regulatory & Reimbursement Landscape

Foods for special medical purposes (FSMPs) skirt centralized EMA review and instead navigate 27 national reimbursement schemes. Germany reimburses instantly, yet Italy’s regional approvals delay initiation 10-14 days. Spain’s devolution generates postcode disparities: Catalonia covers 85% of costs while Andalusia reimburses only 40%. Technical roll-out for cross-border e-scripts lags in 19 member states, muting near-term harmonization benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Parenteral Gains Ground In Home-Care Shift

Oral and enteral modalities retained 68.55% Europe medical clinical nutrition market share in 2025, anchored by ESPEN’s “gut-first” doctrine that favors tube feeding whenever the intestine is functional. Early enteral delivery within 48 hours of ICU admission now covers 45% of patients and trims ventilator-associated pneumonia by 25%. Standard oral supplements dominate geriatric and oncology cohorts, supplying 60% of high-protein prescriptions.

Parenteral therapy is nevertheless accelerating at an 8.25% CAGR through 2031 as national insurers expand HPN coverage. Scandinavia’s registries logged 12% annual growth and extended median catheter life to 26 months thanks to omega-3 lipid emulsions that curb occlusion. Fresenius Kabi’s ready-to-infuse Numeta bags reduced preparation time from 45 to under five minutes and lowered compounding errors 70%, illustrating how innovation can reposition parenteral solutions for home environments.

By Product Type: Disease-Specific Formulas Gain Clinical Traction

Generic polymeric formulas held 45.53% of 2025 revenue, remaining the workhorse in mixed medical-surgical wards. Fiber-enriched versions now cut diarrhea 30% and improve glycemic profiles.

High-acuity care is tilting toward disease-specific blends. The Europe medical clinical nutrition market size for parenteral macronutrient solutions is on pace to advance 7.75% annually, powered by fourth-generation lipid emulsions licensed by the EMA in 2024-2025 that lower bloodstream infections 30%. Germany’s insurer now reimburses 90% of these lipids, freeing ICUs from prior-authorization bottlenecks.

By Application: Gastrointestinal Diseases Drive Formula Innovation

Oncology captured 31.15% of 2025 revenue as cachexia management moved into guidelines and payer formularies. Immunonutrition now benefits 35% of major gastrointestinal surgery cases and lowers postoperative complications 30%.

Gastrointestinal indications represent the fastest expansion at a 9.82% CAGR. ECCO’s 2024 directive placing exclusive enteral nutrition ahead of corticosteroids for pediatric Crohn’s raised EEN adoption to 55% in Dutch clinics by 2025. Polymeric blends are preferred for cost, while partial-enteral CDED regimens are improving adherence and remission rates.

By End User: Geriatric Segment Accelerates On Sarcopenia Recognition

Adults still generated 56.65% of 2025 revenue, reflecting large surgical and chronic-disease caseloads. ERAS mandates carbohydrate drinks and early feeding that shorten stays two to three days.

Geriatrics, however, is the growth engine, expected to outpace all other groups at 7.32% CAGR. Reimbursed high-protein formulas now target sarcopenia for the first time; a German community study showed 15% better grip strength after 12 weeks of supplementation. Europe medical clinical nutrition market size gains here will compound as the over-65 cohort adds 10 million residents by 2030.

By Distribution Channel: Online Pharmacies Surge On Cross-Border E-Prescriptions

Hospital pharmacies remained dominant at 42.23% in 2025, bundling tender contracts across Western Europe. France’s purchasing consortium reduced unit prices 15% through a three-year award to two suppliers.

Still, digital fulfillment is the clear growth story. Online outlets are slated to climb 10.42% per year as eight countries already exchange e-prescriptions, and Germany reimburses delivery fees. Europe medical clinical nutrition market share captured by e-pharmacies will widen as Italy, Spain, and Poland finalize technical integration over 2026-2027.

Geography Analysis

Germany generated 32.23% of 2025 revenue on the back of broad statutory insurance coverage and 1,200 hospital nutrition teams. Reimbursement expansion for home enteral nutrition in January 2025 added 8,000 new users inside six months[3]German Federal Ministry of Health, “Home Enteral Nutrition Reimbursement Expansion 2025,” BUNDESGESUNDHEITSMINISTERIUM.DE. ERAS compliance in colorectal surgery tops 90% and cuts 30-day readmissions 15%.

The United Kingdom is the region’s fastest climber at a 7.42% CAGR through 2031. The April 2025 NHS framework standardized screening and prescription criteria, eliminating postcode inequity and freeing 1,200 beds annually. A national HEN tariff now reimburses GBP 120 weekly for dietitian monitoring, fueling growth in home care.

France, Italy, and Spain together form a large but uneven terrain. France added 12 formulas to its reimbursement list in 2024 yet still requires 18 months per update. Italy’s regional approvals delay therapy 10-14 days, and Spain’s devolution generates 45-point reimbursement gaps among communities. Nordics and Benelux lead HPN adoption, while Eastern Europe is closing gaps by reimbursing dietitian consults and slashing VAT on formulas.

Competitive Landscape

The Europe medical clinical nutrition market remains moderately consolidated. Abbott, Fresenius Kabi, Nestlé Health Science, and Danone (Nutricia) own the strongest brands and hospital contracts. Fresenius Kabi’s Numeta pediatric bags, launched in 15 markets, underpinned 70% fewer compounding errors and captured 120 neonatal ICU contracts. Abbott gained 12% within six months of launching Ensure Plus Advance targeting reimbursed sarcopenia patients. Nestlé’s Peptamen and its digital home-monitoring platform cut unplanned visits 28%, reinforcing retention.

B. Braun and Baxter are scaling parenteral offerings; B. Braun’s Nutriflex omega-3 emulsions, cleared by the EMA in 2024, lower infection risk 30%. Challenger brands AYMES Nutrition and Nualtra are penetrating UK formularies with value-priced oral supplements. AI-driven nutrient-profiling startups are emerging in Germany, hinting at future premium product tiers.

Europe Medical Clinical Nutrition Industry Leaders

Abbott

Fresenius Kabi

Nestlé Health Science

Danone (Nutricia)

Baxter International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Fresenius Kabi and the European Society of Intensive Care Medicine extended their partnership to advance medical nutrition in critical care.

- January 2026: Arla Foods Ingredients introduced a ready-to-stir beta-lactoglobulin powder that raises protein density for patients requiring enriched medical nutrition.

Europe Medical Clinical Nutrition Market Report Scope

As per the scope of the report, clinical nutrition is the overall analysis of the relationship between ingested food and the overall well-being of the human body. Clinical nutrition is largely concerned with the prevention, diagnosis, and management of nutritional alterations in individuals who have chronic illnesses and disorders. Clinical nutrition products are useful in maintaining the patient's health and enabling the improvement of the body's metabolic system by providing adequate supplements, such as minerals, vitamins, and other supplements.

The Europe medical clinical nutrition market is segmented by route of administration into oral and enteral, and parenteral. By product type, the market is categorized into standardized enteral formulas, disease-specific enteral formulas, and parenteral macronutrient solutions. Based on application, the market is divided into oncology, metabolic disorders, gastro-intestinal diseases, neurological disorders, and other diseases. By end user, the segmentation includes infant, pediatric, adult, and geriatric populations. The distribution channel segmentation comprises hospital pharmacies, retail pharmacies, online pharmacies, and institutional/tender sales. Geographically, the market is analyzed across Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe. The report offers the value (in USD) for the above segments.

By Route of Administration

| Oral & Enteral |

| Parenteral |

By Product Type

| Standardised Enteral Formulas |

| Disease-specific Enteral Formulas |

| Parenteral Macronutrient Solutions |

By Application

| Oncology |

| Metabolic Disorders |

| Gastro-intestinal Diseases |

| Neurological Disorders |

| Other Diseases |

By End User

| Infant |

| Pediatric |

| Adult |

| Geriatric |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Institutional / Tender Sales |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Route of Administration | Oral & Enteral |

| Parenteral | |

| By Product Type | Standardised Enteral Formulas |

| Disease-specific Enteral Formulas | |

| Parenteral Macronutrient Solutions | |

| By Application | Oncology |

| Metabolic Disorders | |

| Gastro-intestinal Diseases | |

| Neurological Disorders | |

| Other Diseases | |

| By End User | Infant |

| Pediatric | |

| Adult | |

| Geriatric | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| Institutional / Tender Sales | |

| Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe medical clinical nutrition market by 2031?

Forecasts place the market at USD 33.33 billion by 2031.

How fast will home parenteral nutrition grow in Europe?

HPN volumes are rising at an 8.25% CAGR thanks to expanded reimbursement and caregiver training programs.

Which application segment is growing fastest?

Gastrointestinal disease formulas, lifted by first-line use of exclusive enteral nutrition in pediatric Crohns, are advancing at a 9.82% CAGR.

Why is the geriatric user segment gaining momentum?

Sarcopenia became a reimbursable diagnosis in 2024, driving 7.32% CAGR for high-protein oral supplements among seniors.

How has the EU's e-pharmacy directive affected distribution?

It enabled cross-border e-prescriptions, helping online pharmacies grow at a 10.42% CAGR as rural patients gain easier access.

Which country leads the market and which is growing fastest?

Germany leads with 32.23% of 2025 revenue, while the United Kingdom shows the quickest growth at a 7.42% CAGR.

Page last updated on: