Anorexiants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

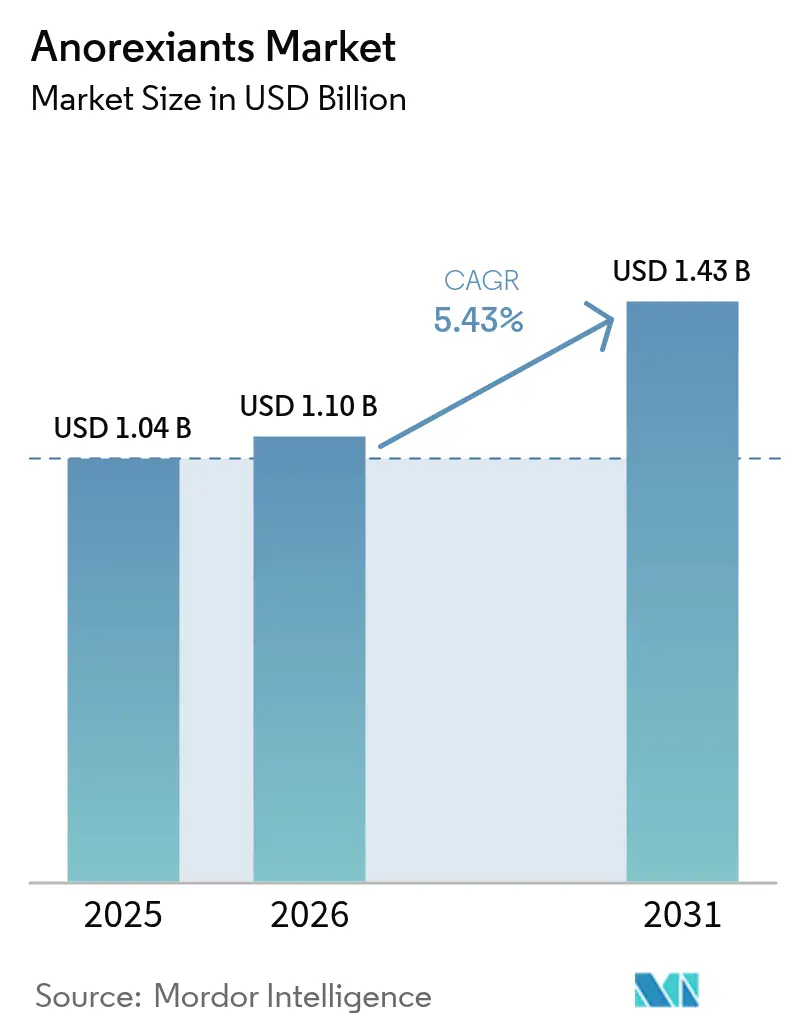

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

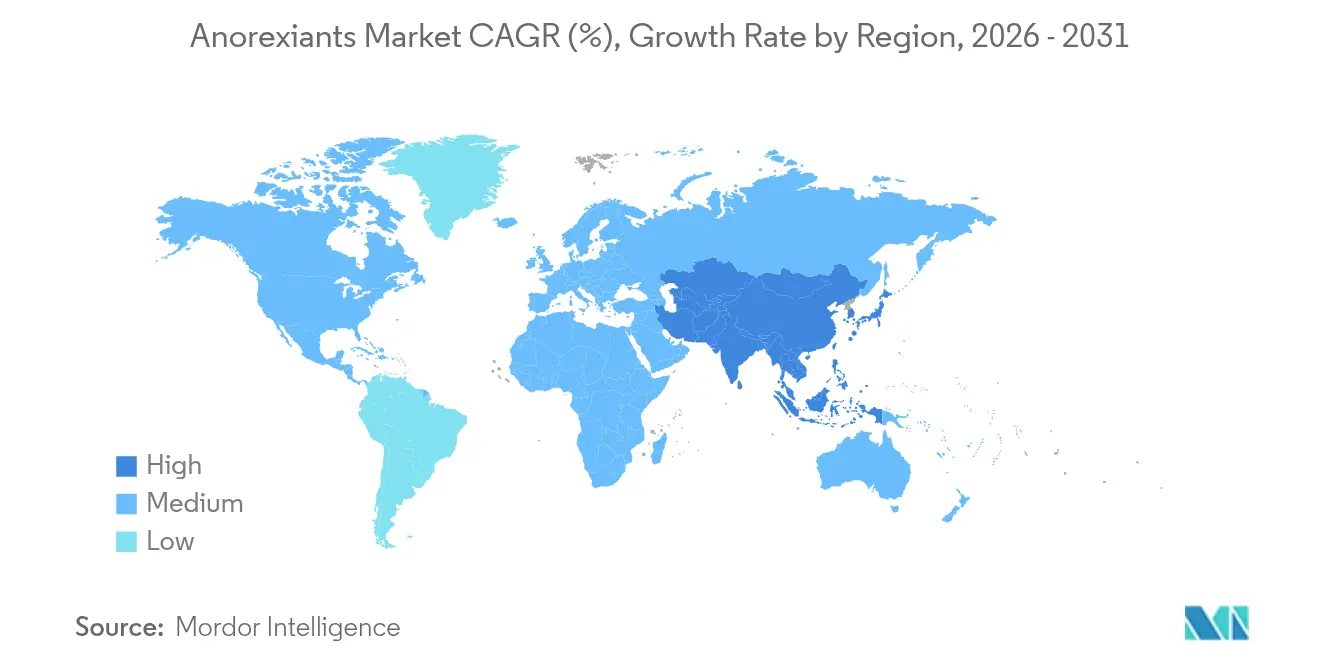

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

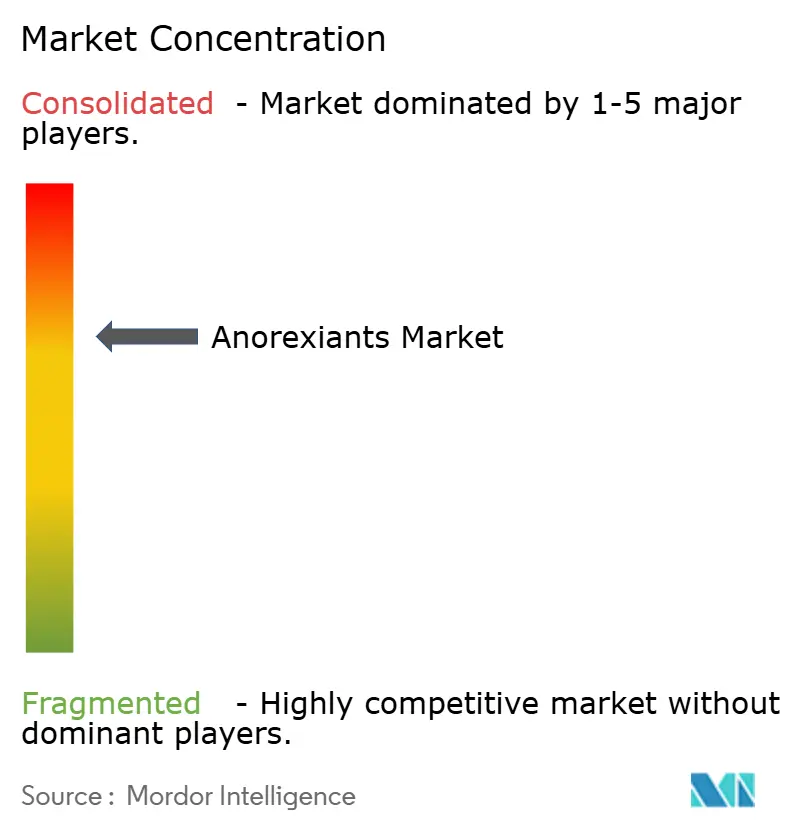

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anorexiants Market Analysis by Mordor Intelligence

Anorexiants market size in 2026 is estimated at USD 1.1 billion, growing from 2025 value of USD 1.04 billion with 2031 projections showing USD 1.43 billion, growing at 5.43% CAGR over 2026-2031.

Persistent clinical proof of metabolic risk reduction, an expanded payer focus on chronic-disease management, and rapid supply-chain investments by leading manufacturers are jointly sustaining this growth. GLP-1 receptor agonists anchor the competitive landscape, capturing over three-fifths of global prescriptions and drawing follow-on innovation in multi-agonist combinations. Subcutaneous injectables still dominate the delivery mix, yet breakthrough oral formulations are enlarging the addressable patient pool by removing needle-related barriers. Digitally enabled tele-obesity services are lowering access hurdles, particularly in rural regions, and driving new direct-to-consumer demand streams. Regionally, North America leverages favorable reimbursement reforms, while Asia-Pacific is accelerating on the back of fresh approvals and scalable local manufacturing capacity.

Key Report Takeaways

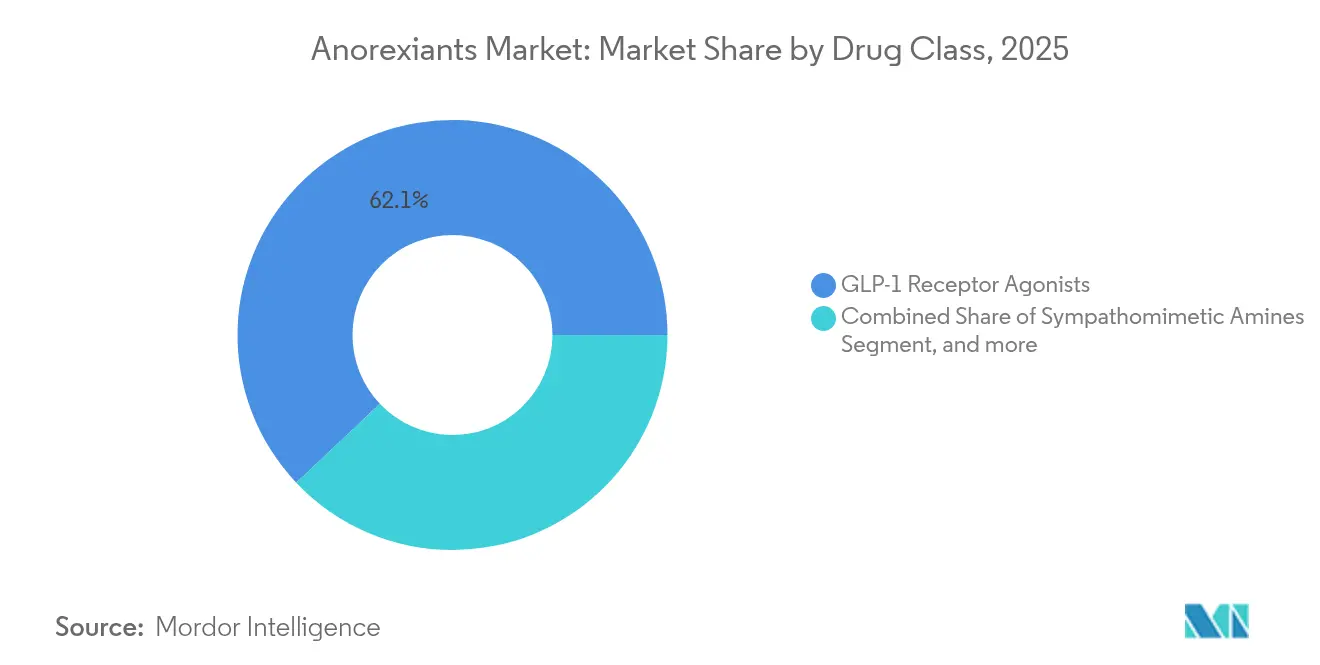

- By drug class, GLP-1 receptor agonists controlled 62.05% of anorexiants market share in 2025 and are on track for an 7.95% CAGR through 2031.

- By route of administration, oral formulations are projected to post the quickest expansion at 7.15% CAGR, although subcutaneous products still command 75.40% of 2025 revenue.

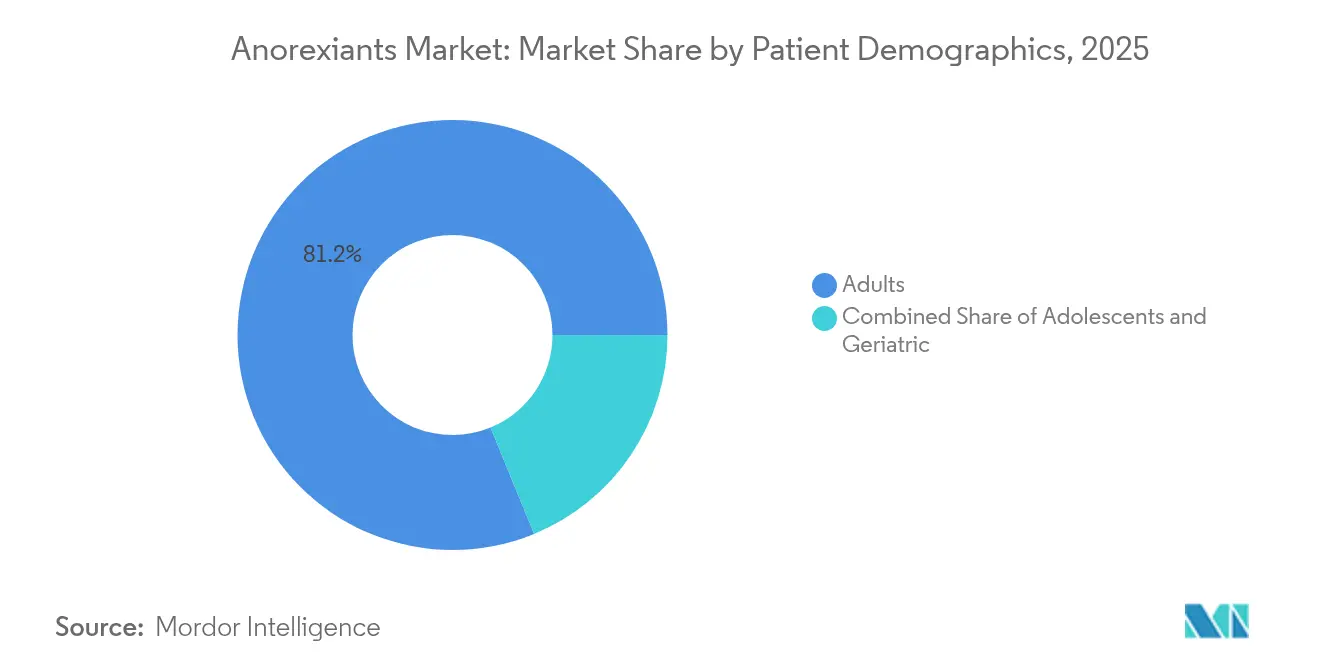

- By patient demographics, adults accounted for 81.20% of 2025 prescriptions, whereas adolescent therapies are advancing at a 6.75% CAGR on the back of new pediatric approvals.

- By distribution channel, online pharmacies are recording a 8.60% CAGR through 2031, while hospital pharmacies retained 51.10% revenue share in 2025.

- By geography, Asia-Pacific is expected to lead growth at 7.70% CAGR, yet North America held 43.90% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anorexiants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging prevalence of obesity and metabolic syndrome | +1.2% | Global (North America, Europe highest) | Long term (≥ 4 years) |

| GLP-1 reimbursement expansions in employer-sponsored plans | +0.8% | North America, expanding to Europe | Medium term (2-4 years) |

| Pivot from aesthetics to metabolic risk reduction among payers | +0.6% | North America, EU, Australia | Medium term (2-4 years) |

| Consumer-led tele-obesity platforms expanding prescription access | +0.4% | Global, North America lead | Short term (≤ 2 years) |

| Pill-based multi-agonist pipeline promising bariatric-level efficacy | +0.3% | Global | Long term (≥ 4 years) |

| AI-driven dose-titration apps boosting long-term adherence | +0.2% | North America, EU, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Prevalence of Obesity and Metabolic Syndrome

WHO projects that nearly 2 billion individuals will be classified as obese by 2035, pushing annual global medical costs above USD 4 trillion.[1]World Health Organization, “Obesity and Overweight,” who.int This unprecedented disease burden is compelling payers to reposition obesity therapies as frontline metabolic interventions rather than lifestyle aids. With non-alcoholic fatty liver disease and cardiovascular comorbidities rising, prescribers are fast-tracking pharmacological solutions, thereby lifting baseline prescription volumes. The trend is visible in both developed and rapidly urbanizing economies where sedentary habits are ingrained. Consequently, long-term demand visibility is strengthening capital allocation toward enlarged peptide production and real-world outcome analytics.

GLP-1 Reimbursement Expansions in Employer-Sponsored Plans

Large US employers such as Amazon and Walmart now include GLP-1 coverage in comprehensive wellness packages.[2]Eli Lilly, “Employer Health Plan Outcomes Data,” lilly.com Actuarial reviews indicate lower downstream spend on diabetes and cardiovascular events, prompting additional companies to follow suit. The employer segment circumvents slower Medicare and Medicaid rulemaking, providing an immediate commercial lift across working-age demographics. As utilization grows, richer real-world datasets further validate cost-effectiveness claims, reinforcing payer confidence. Parallel pilots are underway in Europe, signaling a spillover that could normalize corporate reimbursement frameworks globally within the medium term.

Pivot From Aesthetics to Metabolic Risk Reduction Among Payers

Results from a 17,604-patient trial showed 20% fewer major adverse cardiac events among Wegovy users versus placebo, leading FDA to approve the drug for cardiovascular risk reduction in March 2024.[3]Novo Nordisk, “SELECT Trial Cardiovascular Outcomes,” novonordisk.com The ruling allowed payers to classify therapy under essential cardiovascular care, unlocking broader coverage. NICE quickly recommended tirzepatide for similar use in the United Kingdom, setting a precedent for other European agencies. By framing treatment as chronic disease management, reimbursement committees have side-stepped prior objections anchored in cosmetic positioning, accelerating uptake across high-risk patient pools.

Consumer-Led Tele-Obesity Platforms Expanding Prescription Access

Telehealth operators such as Teladoc deploy licensed physicians for virtual consultations, e-prescribing GLP-1 drugs and arranging doorstep delivery. The digital model shortens wait times and reaches rural patients who lack specialist clinics. Proprietary algorithms support eligibility screening, while continuous remote monitoring sustains adherence, reducing weight-regain relapse. Out-of-pocket acceptance is strong: 80% of global GLP-1 sales outside the United States involve self-payment, illustrating demand elasticity despite premium price points. Elevated convenience, privacy, and integrated coaching are widening the market beyond traditional hospital settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global semaglutide / tirzepatide API supply bottlenecks | -0.7% | Global (emerging markets most acute) | Short term (≤ 2 years) |

| Sticker shock & co-pay fatigue in self-pay segments | -0.5% | Global, price-sensitive markets | Medium term (2-4 years) |

| Safety concerns over muscle-mass loss in chronic use | -0.4% | North America, Europe | Medium term (2-4 years) |

| Momentum of non-pharmacologic GLP-1 “compound clinics” | -0.3% | North America, expanding to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global Semaglutide/Tirzepatide API Supply Bottlenecks

Peptide synthesis demands specialized reactors and lengthy purification cycles, limiting rapid scale-up. Both molecules remained on the US FDA shortage list until early 2025. Novo Nordisk earmarked USD 4 billion for new US facilities and Eli Lilly allotted USD 27 billion for global capacity, yet full ramp-up spans multiple years. Meanwhile, branded inventory is preferentially shipped to high-margin markets, delaying penetration in lower-income regions. Compounding pharmacies filled the gap, but the FDA delisted the drugs from shortage status, curbing compounders’ legal latitude and temporarily tightening supply.

Sticker Shock & Co-Pay Fatigue in Self-Pay Segments

Monthly therapy costs often top USD 1,400, outstripping many household healthcare budgets. While patient-assistance programs exist, eligibility caps leave sizable populations exposed to high co-pays, prompting discontinuation after initial weight loss. Mature markets observe adherence drop-offs after six fills, undermining long-term outcome metrics that justify payer coverage. Tiered global pricing is under evaluation, yet harmonizing affordability with margin preservation remains complex, especially where generic competition is on the horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: GLP-1 Dominance Reshapes Competitive Dynamics

GLP-1 receptor agonists represented 62.05% of 2025 revenue, anchoring the anorexiants market size leadership and expanding at 7.95% CAGR through 2031. The dual action on glucose and satiety underpins first-line guideline status across multiple geographies. As clinical endpoints broaden to cardiovascular risk reduction, formularies prioritize GLP-1 over legacy sympathomimetics, accelerating class consolidation. Combination pipelines—such as Eli Lilly’s tirzepatide join GIP and glucagon targets for amplified efficacy, raising competitive thresholds for future entrants. Sympathomimetic amines persist mainly in cost-constrained settings, while serotonin-2C agonists serve contraindicated subgroups. AbbVie’s USD 350 million upfront for a long-acting amylin analog underscores the shift toward multi-hormone modulation beyond appetite suppression.

Despite intense focus on GLP-1, alternative mechanisms are widening the innovation funnel. Melanocortin-4 receptor agonists and leptin-mimetics seek to replicate hypothalamic signaling pathways, offering differentiated efficacy-safety profiles. Clinical readouts over the next five years will clarify whether these entrants can carve meaningful share from the entrenched GLP-1 class or coexist as adjunct options. As competition diversifies, manufacturers must balance indication breadth against payer willingness to reimburse premium list prices, a calculus that will shape portfolio strategies throughout the forecast window.

By Route of Administration: Oral Innovation Challenges Injectable Supremacy

Subcutaneous injectables contributed 75.40% of 2025 sales, underlining their entrenched role in rapid weight-loss induction regimens. Weekly dosing convenience and abundant real-world evidence sustain prescriber confidence. Nonetheless, the oral segment is tracking a 7.15% CAGR on the strength of late-stage candidates demonstrating efficacy equivalence. Eli Lilly’s orforglipron reported mean weight reductions approaching 12% at 36 weeks, matching injectable benchmarks. Success would reset patient preference dynamics, particularly for chronic maintenance therapy where pill regimens outrank injections in adherence surveys.

Development focus has shifted toward permeability enhancers and enteric coatings that safeguard peptide integrity against gastrointestinal degradation. OPKO Health and Entera Bio are co-engineering a dual-agonist tablet leveraging proprietary absorption technology. Beyond tablets, intranasal and transdermal patches populate early pipelines, targeting cohorts with gastroparesis or needle phobia. Should these alternative routes reach commercialization, the anorexiants market share hierarchy could undergo marked realignment by 2030.

By Patient Demographics: Adult Dominance with Adolescent Acceleration

Adults encompassed 81.20% of prescriptions in 2025, commanding the largest anorexiants market share thanks to entrenched treatment paradigms and employer health-plan coverage. Cardiometabolic comorbidities within this group continue to drive high clinical urgency and reimbursement support. Simultaneously, the adolescent segment is posting a 6.75% CAGR through 2031 after FDA clearance of semaglutide for teens aged 12-17, signaling endorsement of early pharmacologic intervention. Clinicians recognize that timely therapy can avert lifelong metabolic complications, encouraging guideline revisions that advocate earlier screening and treatment thresholds.

Geriatric patients present under-served potential, yet dose-adjustment complexities tied to renal and hepatic function slow uptake. Device makers are exploring auto-injectors with lower force requirements to aid seniors with dexterity limitations. Pediatric formulations, including fruit-flavored oral suspensions under investigation, may further expand penetration into younger age brackets over the long run, reshaping lifecycle management strategies for incumbent brands.

By Distribution Channel: Digital Disruption Transforms Traditional Dispensing

Hospital-affiliated specialty pharmacies retained 51.10% of 2025 revenue, owing to streamlined prior-authorization workflows and embedded clinical monitoring infrastructure. However, online pharmacies, interlinked with telehealth ecosystems, are rising at 8.60% CAGR, broadening the anorexiants market size through convenience-led demand. Platforms integrate e-consultation, payment, and discreet shipping, outperforming brick-and-mortar outlets on turnaround speed. Retail chains contend by rolling out pharmacist-led GLP-1 counseling programs and adherence apps, yet margin pressure persists as payers channel volume to lower-cost digital pathways.

Partnership models are evolving: Amwell collaborates with Vida Health to unify virtual coaching and pharmacy fulfillment, creating end-to-end obesity care pathways. Regional wholesalers are piloting drop-shipment agreements to cut distribution overhead. Regulatory bodies are drafting e-pharmacy accreditation norms aimed at safeguarding drug authenticity, a prerequisite for long-term channel stability.

Geography Analysis

North America generated 43.90% of 2025 revenue, underscoring its primacy in global adoption and pricing power. Medicare’s 2024 decision to reimburse GLP-1 therapies for cardiovascular risk reduction immediately catalyzed formulary inclusion across private insurers. Canada is converging, as province-level reviews favor coverage extensions; meanwhile, Mexico authorized semaglutide 2.4 mg under updated obesity guidelines, expanding regional footprint. Robust telehealth infrastructure and employer benefit designs are expected to sustain growth, even as price negotiations gradually temper unit revenues.

Asia-Pacific is tracking the fastest expansion at 7.70% CAGR, propelled by soaring urban obesity rates and recently secured approvals. China’s NMPA cleared Innovent Biologics’ mazdutide, the nation’s first domestic GLP-1/GIP dual agonist, intensifying competition and localizing supply. Japan green-lit Zepbound for sleep-apnea-related weight loss, illustrating indication diversification. India is slated to review tirzepatide in 2025, with domestic firms preparing value-tier formulations to address price sensitivity. Regional manufacturing hubs reduce logistics overhead and shield against global peptide shortages, reinforcing structural growth.

Europe maintains moderate yet steady uptake. EMA approval of Wegovy’s cardiovascular label extension and NICE’s positive appraisal of tirzepatide improve reimbursement certainty across major markets. Country-specific budget caps, however, stagger rollout timing, leading to heterogeneous access. Switzerland and Norway quickly aligned with pan-European guidance, while some Southern European states defer adoption pending cost-effectiveness negotiations. Regulatory discourse now centers on integrating digital adherence tools and outcome-based pricing, initiatives that could accelerate uniform adoption beyond 2027.

Competitive Landscape

Novo Nordisk and Eli Lilly form a two-player axis dominating GLP-1 supply, leveraging patent portfolios, manufacturing muscle, and comprehensive real-world evidence libraries. Both companies are investing in vertical integration: Novo Nordisk’s USD 4 billion US expansion and Eli Lilly’s USD 27 billion global build-out aim to neutralize supply shocks and lock in economies of scale. Horizontal diversification unfolds through acquisitions and licensing Novo Nordisk’s USD 200 million pact for UBT251 and Eli Lilly’s multi-agonist pipeline highlight aggressive portfolio widening.

Challengers are advancing on multiple fronts. Biosimilar developers in South Korea and India are scaling peptide platforms for post-2027 launches. AbbVie’s alliance with Gubra to co-develop an amylin analog positions the company for entry into the high-growth combination-therapy niche. Meanwhile, digital-first operators collaborate with compound pharmacies, creating alternative fulfillment networks during branded stockouts, though recent FDA enforcement is curtailing that window.

Technology integration is an emerging differentiator. Players pair drugs with AI titration apps, remote monitoring, and gamified adherence features, forging ecosystem moats. Intellectual-property litigation intensifies as expiration dates near; top manufacturers file secondary patents around delivery devices and digital companions to prolong exclusivity. Success will hinge on harmonizing production scale-up with payer willingness to underwrite broad access, a balance that will shape competitive contours through the decade.

Anorexiants Industry Leaders

F. Hoffmann-La Roche AG

Pfizer Inc.

Novo Nordisk A/S

Lannett Company Inc.

Currax Pharmaceuticals LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AbbVie and Gubra announced a license agreement worth up to USD 1.8 billion to develop GUB014295, a long-acting amylin analog for obesity treatment, marking AbbVie's strategic entry into the obesity market with USD 350 million upfront payment and potential milestone payments. This partnership leverages Gubra's expertise in peptide-based drug discovery and positions AbbVie to compete in the rapidly expanding obesity therapeutics market.

- March 2025: Novo Nordisk expanded its obesity drug pipeline through a USD 200 million deal with China-based United Laboratories to develop UBT251, a triple-agonist treatment targeting GLP-1, GIP, and glucagon receptors. This strategic collaboration strengthens Novo's position in the Chinese market while advancing next-generation multi-agonist therapies that could deliver superior efficacy compared to current single-target treatments.

Global Anorexiants Market Report Scope

Anorexiants are therapeutics used to treat obesity by increasing basal metabolic rate. These drugs stimulate hypothalamic and limbic regions that control gastric emptying. Thus, it acts by suppressing the appetite and causing earlier satiety resultant decreasing the intake of the individual. Obesity is identified as the leading preventable cause of preventable death, thus the demand for anorexiants is expected to increase over the forecast period driving the market.

| GLP-1 Receptor Agonists |

| Sympathomimetic Amines |

| Combination Therapies |

| Serotonin-2C Agonists |

| Others |

| Oral |

| Subcutaneous |

| Other Route of Administration |

| Adults |

| Adolescents |

| Geriatric |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | GLP-1 Receptor Agonists | |

| Sympathomimetic Amines | ||

| Combination Therapies | ||

| Serotonin-2C Agonists | ||

| Others | ||

| By Route of Administration | Oral | |

| Subcutaneous | ||

| Other Route of Administration | ||

| By Patient Demographics | Adults | |

| Adolescents | ||

| Geriatric | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the anorexiants market in 2026?

The anorexiants market size reached USD 1.1 billion in 2026.

What is the projected growth rate for anorexiant drugs through 2031?

Global revenue is expected to advance at a 5.43% CAGR between 2026 and 2031.

Which drug class leads current prescriptions?

GLP-1 receptor agonists captured 62.05% of 2025 revenue and remain the fastest-growing class.

Why are oral formulations gaining attention?

Late-stage oral GLP-1 candidates have shown weight-loss efficacy comparable to injectables, removing needle-related barriers and broadening adherence.

Which region is poised for the fastest expansion?

Asia-Pacific is set to register an 7.70% CAGR through 2031 due to fresh approvals and localized manufacturing.

What factors could restrain near-term growth?

Peptide API shortages and high out-of-pocket costs may limit immediate uptake despite strong clinical demand.

Page last updated on: