Patient Lifting Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 7.73 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

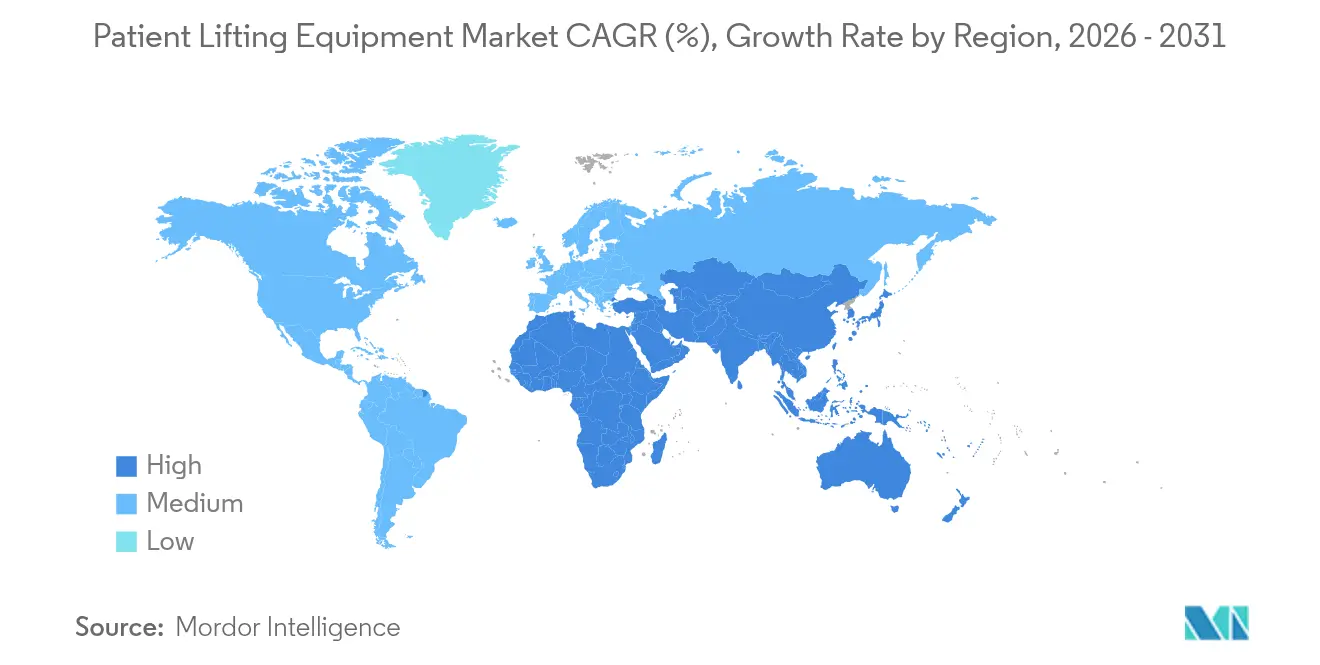

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Lifting Equipment Market Analysis by Mordor Intelligence

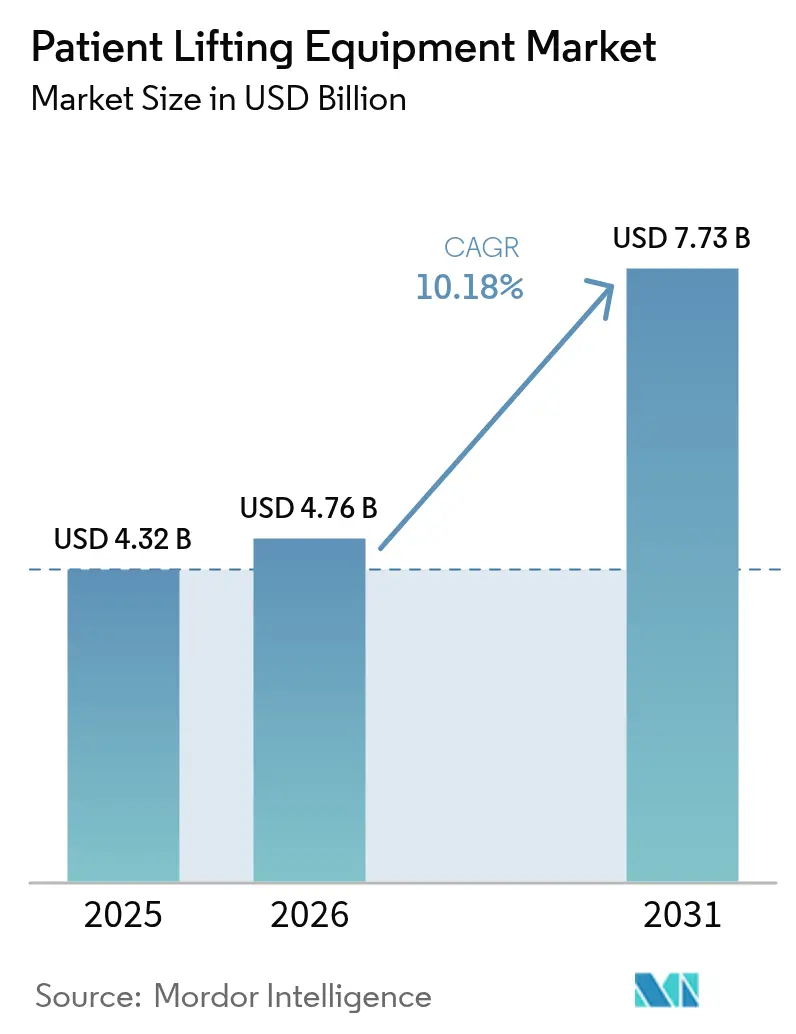

The Patient Lifting Equipment Market size was valued at USD 4.32 billion in 2025 and estimated to grow from USD 4.76 billion in 2026 to reach USD 7.73 billion by 2031, at a CAGR of 10.18% during the forecast period (2026-2031).

The expansion reflects widespread zero-lift mandates, rapid technology upgrades, and demographic aging that collectively reshape acute and long-term care delivery. Capital investments flow toward powered and IoT-ready devices that lower caregiver injury rates, align with infection-control protocols, and integrate with digital records. Asia-Pacific registers the fastest regional acceleration as hospital build-outs, domestic manufacturing incentives, and bariatric care needs converge. At the same time, rental and “equipment-as-a-service” models unlock access for cost-sensitive buyers, particularly in home settings. Competitive intensity rises as global incumbents absorb specialists, deploy smart-sensor platforms, and bundle post-sale services to secure multiyear contracts.

Key Report Takeaways

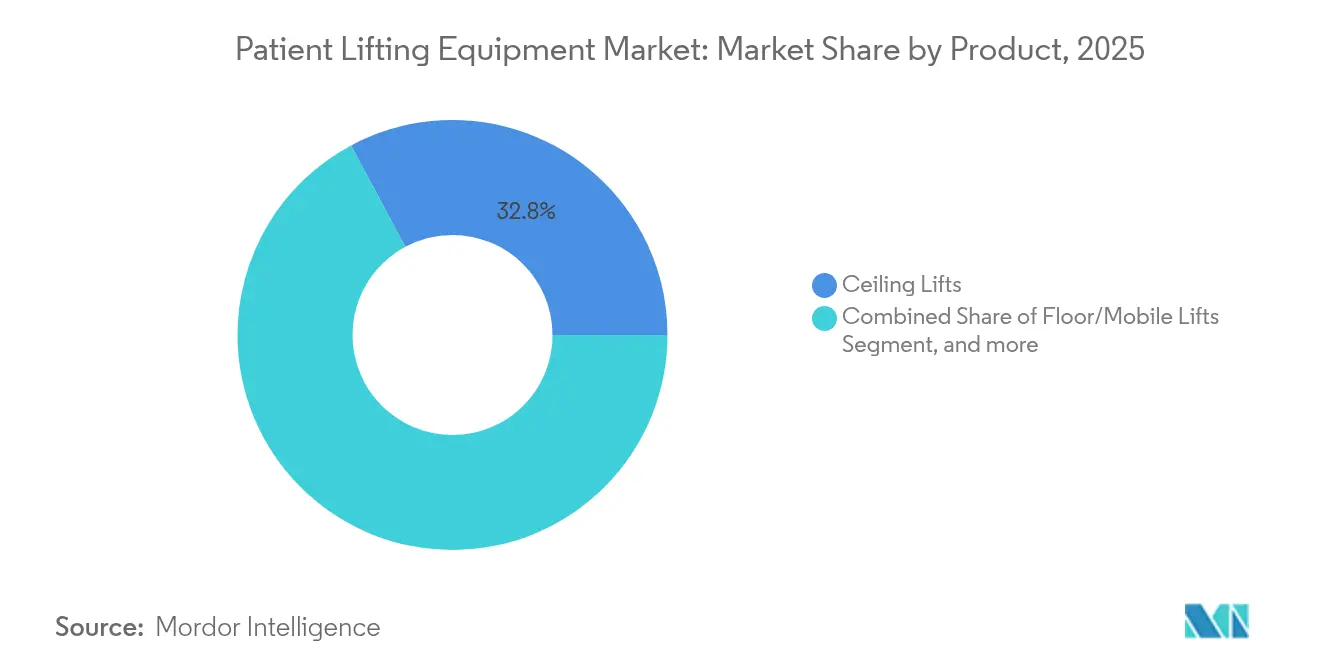

- By product category, ceiling lifts captured 32.82% revenue share of the patient lifting equipment market in 2025, while stair and wheelchair platform lifts are projected to expand at a 14.55% CAGR through 2031.

- By mechanism, powered systems held 79.53% of the patient lifting equipment market share in 2025 and are forecast to increase at a 13.21% CAGR to 2031.

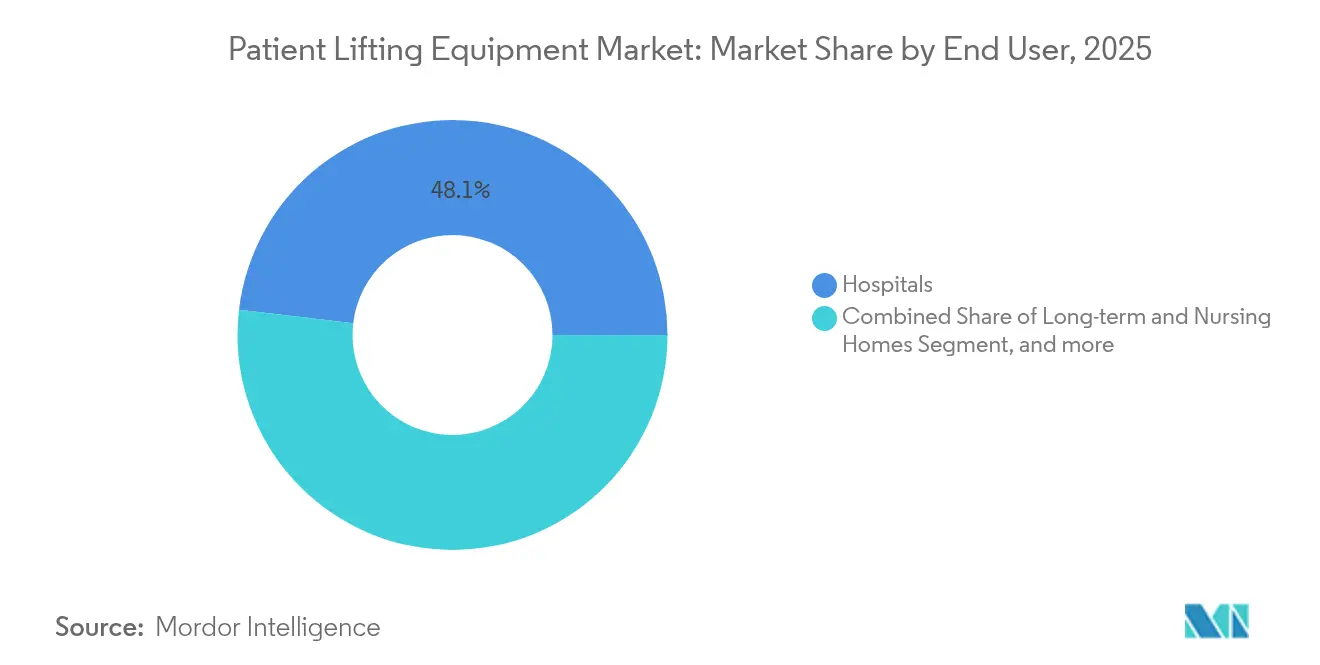

- By end user, hospitals accounted for 48.12% share of the patient lifting equipment market size in 2025, whereas home-care settings are advancing at a 17.21% CAGR during 2026-2031.

- By geography, North America led with 38.52% share in 2025; Asia-Pacific is set to register the fastest 15.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient Lifting Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Geriatric & Bariatric Population | +2.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Mandatory "Safe-Patient-Handling" Regulations | +2.1% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| Rise In Home-Based Long-Term Care | +1.9% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Technology Shift to Powered & IoT-Enabled Lifts | +1.6% | North America & Europe early adoption, APAC following | Long term (≥ 4 years) |

| Hospital "Zero-Lift" Policies to Curb Staff MSD Claims | +1.4% | Primarily North America, expanding globally | Short term (≤ 2 years) |

| Emerging Rental & As-A-Service Business Models | +0.9% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric & Bariatric Population

By 2050, the United States will support more than 88 million older adults who require long-term assistance, with the fastest growth among those aged 85 plus. Obesity prevalence compounds mobility limitations, prompting demand for bariatric-capable devices such as Arjo’s Citadel Plus, which handles up to 454 kg.[1]Arjo, “Citadel Plus Bariatric Care System Product Sheet,” arjo.com Manual handling currently causes 52% of caregiver back injuries, so hospitals treat lifting systems as essential safety infrastructure rather than discretionary capital. The longevity of demographic pressure underpins sustained procurement even through budgetary cycles, thereby anchoring a long-run growth floor for the patient lifting equipment market. Product roadmaps increasingly prioritize higher safe-working loads and wider sling geometries to serve this cohort.

Mandatory Safe-Patient-Handling Regulations

Updated 2024 AORN guidelines instruct surgical and perioperative units to adopt ceiling or boom lifts tailored to individualized transfer plans.[2]AORN, “2024 Guideline for Safe Patient Handling,” aorn.org California’s AB 1136 law exemplifies U.S. legislation demanding comprehensive safe-patient-handling frameworks, supported by UCLA Health’s Lift Champion program that monitors compliance at the unit level. OSHA advisories for nursing homes further recommend mechanical lifts, turning voluntary norms into enforceable occupational-safety commands.[3]OSHA, “Nursing Home eTool,” osha.gov Equivalent policies gain momentum across Europe and start to surface in APAC, collectively widening the addressable base for the patient lifting equipment market. Penalties tied to reimbursement and worker-compensation claims reinforce procurement urgency, accelerating the replacement of legacy manual hoists.

Rise in Home-Based Long-Term Care

AdaptHealth generated USD 3.2 billion in revenue in 2023 while serving 4.1 million home patients, illustrating the scale of domicile-centered care. U.S. Medicare’s capped rental structure allows beneficiaries to assume ownership after 13 months, smoothing adoption costs and creating recurring income for suppliers. Lightweight products such as the portable Mangar Camel Lift accept 705-pound loads and fit residential doorways, aligning with aging-in-place preferences. Pandemic-era policy waivers normalized tele-rehab and remote monitoring, further embedding lifts into home-care packages. Consequently, the home segment advances faster than institutional channels, lifting the overall patient lifting equipment market growth trajectory.

Technology Shift to Powered & IoT-Enabled Lifts

Smart sensors embedded in ceiling tracks transmit usage logs that inform preventive maintenance and caregiver training. Early pilot studies on IoT-integrated smart mattresses revealed nurse acceptance scores of 12.5/15 for workload reduction and ulcer prevention. Digital-twin analytics monitor lift cycles, battery health, and patient weight changes, feeding electronic health records to support falls analytics. Manufacturers bundle SafeSet alerts and skin microclimate modules, converting lifts into holistic mobility-and-monitoring hubs. These upgrades justify price premiums, raise switching costs, and underpin double-digit expansion of the powered segment within the patient lifting equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insufficient Caregiver Training & Compliance Gaps | -1.8% | Global, more pronounced in developing markets | Short term (≤ 2 years) |

| High Capex and Fragmented Reimbursement in Developing Economies | -2.3% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Device-Related Patient Safety Recalls & Litigation | -1.2% | Global, heightened impact in North America & Europe | Short term (≤ 2 years) |

| Short Product-Replacement Cycles Causing Budget Strain | -0.9% | Global, particularly acute in cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Insufficient Caregiver Training & Compliance Gaps

Even after equipment rollout, many hospitals record persistent musculoskeletal injury rates because staff revert to manual lifting when pressed for time. The skill deficit is acute in smaller facilities lacking dedicated ergonomics educators, which curtails the realized value of installed systems. Complex powered lifts require familiarity with programmable settings, battery checks, and sling selection to operate safely. Without continuous audits, underutilization erodes return on investment and slows uptake across the patient lifting equipment market.

High Capex and Fragmented Reimbursement in Developing Economies

Comprehensive ceiling-track installations involve structural bracing, electrical wiring, and certification, pushing project budgets beyond cash-strapped hospital thresholds in emerging economies. Reimbursement rules differ by province or insurer, delaying payback calculations and lengthening procurement cycles. Currency volatility and customs duties inflate import costs, narrowing margins for distributors. As a result, buyers gravitate toward refurbished imports or local low-spec manual devices, tempering penetration of premium solutions in parts of Asia, Latin America, and Africa within the broader patient lifting equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Ceiling Lifts Lead Infrastructure Integration

Ceiling lifts secured 32.82% of the patient lifting equipment market share in 2025 owing to seamless rail-mount integration that frees floor space and standardizes transfer routes. Their anchored presence supports infection-control zoning and minimizes trip hazards, making them default choices in new hospital construction. Floor/mobile lifts remain indispensable where retrofitting ceiling tracks is infeasible, while sit-to-stand aids provide active-mobility support in rehabilitation wards. Rapidly aging residential stock propels stair and wheelchair platform lifts at a 14.55% CAGR to 2031, reflecting accessibility retrofits under building-code revisions. Manufacturers diversify sling ecosystems; Savaria’s Silvalea line offers fabric variants for bariatric, amputee, and toileting applications.

The evolving product roadmap emphasizes modularity, enabling chassis upgrades or motor swaps without replacing rails. Bariatric payload options are spreading beyond top-tier models, signaling a design convergence that makes heavy-duty capability standard. Smart user interfaces with touch-free pendant controls address infection-prevention imperatives, while onboard diagnostics cut downtime. Collectively, these advances maintain the ceiling-lift franchise and support steady value capture across the patient lifting equipment market.

By Mechanism: Powered Systems Dominate Clinical Preference

Powered units delivered 79.53% of 2025 revenue and are projected to enlarge their lead at a 13.21% CAGR. Uniform motor output reduces caregiver exertion, curbs variance in lift technique, and limits liability exposure from over-exertion injuries. Battery chemistry advances lengthen operational cycles, and quick-swap modules ensure continuous readiness in critical-care environments. Manual hoists still fill budget-constrained or off-grid applications, yet their share erodes as smaller facilities adopt low-voltage powered models introduced at entry-level price points. Predictive maintenance algorithms embedded in powered devices transmit runtime diagnostics, enabling contract-service providers to schedule repairs before failures disrupt continuity of care. These attributes cement powered systems as the clinical gold standard within the patient lifting equipment market.

Manual devices retain a tactical niche in disaster relief, remote clinics, and home settings where simplicity and low acquisition costs outweigh efficiency gains. Manufacturers now market hybrid kits that allow field conversion from manual to powered through bolt-on motor packs, providing upgrade flexibility and reducing lifecycle cost barriers. Despite niche retention, the volume migration trend clearly favors powered technology across all care settings, sustaining upward pricing power in the patient lifting equipment market.

By End User: Hospitals Lead While Home Care Accelerates

Hospitals commanded 48.12% of 2025 revenue owing to concentrated caseloads and mandated safe-handling protocols. Capital budgets earmark lifts within broader patient-room modernization, and group purchasing contracts standardize specifications. Yet the home-care channel registers the fastest 17.21% CAGR as payers reward lower-cost community settings and families choose aging-in-place solutions. Long-term-care and nursing homes represent a stable mid-single-digit growth opportunity driven by routine upgrade cycles and stringent worker-safety inspections.

Regulatory reforms such as CMS’s 2.7% home-health payment boost in 2025 elevate reimbursement certainty, encouraging durable-medical-equipment suppliers to expand rental fleets. Portable ceiling tracks and foldable floor lifts specifically address doorframe clearances typical in residential architecture. Service models bundle periodic safety checks and sling laundering, further professionalizing home-care logistics. These dynamics reinforce multi-channel expansion of the patient lifting equipment market, with hospitals anchoring baseline volume and home environments supplying incremental acceleration.

Geography Analysis

North America’s 38.52% revenue leadership rests on robust safe-handling regulations, reimbursement frameworks, and a well-organized supply chain. Encompass Health operates 161 rehabilitation hospitals whose standard lift protocols set benchmarks for regional procurement. U.S. healthcare employment is projected to add 2.1 million jobs by 2032, heightening demand for injury-mitigation tools. The patient lifting equipment market benefits from integrated worker-safety metrics tied to reimbursement, embedding lifts in capital-planning templates of both public and private hospitals.

Asia-Pacific represents the fastest-growing corridor, with a 15.29% CAGR forecast driven by aging demographics, expanded insurance coverage, and government pushes to localize device production. China’s July 2024 policy on medical-equipment upgrades accelerates procurement of advanced lifts in county-level hospitals. Japan, grappling with population aging, directs innovation grants toward robotics-assisted mobility devices, reinforcing demand for high-specification ceiling tracks.

Europe maintains stable, regulation-driven growth as occupational-safety directives harmonize equipment standards across member states. Sustainability rules incentivize recyclable materials and energy-efficient motor platforms. Middle East & Africa and South America remain emerging frontiers where hospital-construction pipelines and clinical-quality accreditation spur initial purchases, yet currency swings and procurement bureaucracy slow large-scale rollouts. Collectively, regional variances amplify the strategic need for adaptable go-to-market models within the patient lifting equipment market.

Competitive Landscape

The patient lifting equipment market shows moderate concentration, with global multinationals expanding through M&A and adjacency plays. Baxter’s USD 12.4 billion acquisition of Hillrom in 2024 created a combined portfolio that spans beds, lifts, and connected monitoring, generating USD 350 million annual synergy potential. Arjo increased European scale by acquiring diagnostic and rental specialists, integrating service contracts that lock in long-term revenue. Invacare divested its North American business to MIGA Holdings, allowing capital restructuring and renewed R&D focus on next-gen mobility aids.

White-space opportunities surface where private-equity consolidation in adjacent wheelchair markets burdens operators with high leverage, opening share gains for lift manufacturers offering bundled mobility ecosystems. IoT-first entrants develop cloud portals that aggregate equipment health, usage analytics, and compliance dashboards, appealing to health-system procurement teams seeking integrated reporting. Companies compete on post-sale value, emphasizing lift-as-a-service models, sling subscription programs, and predictive maintenance guarantees. Safety recalls, such as Permobil’s SmartDrive motor update covering 781 units in 2024, underscore the importance of ISO-aligned quality systems and rapid field-service networks.

Patient Lifting Equipment Industry Leaders

GF Health Products

Enovis (DJO Global)

Invacare Corporation

Benmor Medical

Savaria (Handicare)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Winncare, a prominent medical device manufacturer, has introduced the Luna X5, a next-generation ceiling lift system engineered to meet the evolving needs of both residential and institutional care environments. This innovative "all-in-one" solution combines flexibility, strength, and aesthetic design, making it ideal for settings with architectural constraints.

- April 2025: Arjo, a global leader in medical device technology, has reinforced its position in the patient handling segment with the launch of Maxi Move 5, the latest generation of its flagship mobile patient floor lift. This strategic product upgrade introduces cutting-edge technical innovations aimed at enhancing caregiver safety and operational efficiency.

- November 2024: Winncare, a leading European healthcare organization, has announced the acquisition of Five Mobility, marking its third UK acquisition. This strategic move aligns with Winncare’s growth ambitions in the acute care (hospital) channel, enhancing its footprint and capabilities in one of Europe’s most dynamic healthcare markets.

- November 2024: Invacare Holdings Corporation and MIGA Holdings LLC have jointly announced the acquisition of Invacare’s North American business by MIGA. This strategic transaction marks a significant shift in the competitive landscape of the mobility and homecare equipment market, positioning MIGA for accelerated growth and operational expansion.

Global Patient Lifting Equipment Market Report Scope

Patient lifting equipment is an assistive device that allows patients in hospitals and nursing homes and people receiving health care at home to be transferred between bed and chair or other similar resting places.

The Patient Lifting Equipment Market is Segmented by Product (Ceiling Lifts, Stair & Wheelchair Lifts, Mobile Lifts, Sit-To-Stand Lifts, Bath & Pool Lifts, Lifting Slings, and Accessories), End-User (Hospitals, Homecare Setting, and Other End-Users), and Geography (North America (United States, Canada, and Mexico), Europe ) Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and the Rest of Middle East and Africa), and South America Brazil, Argentina, and Rest of South America)). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Ceiling Lifts |

| Floor/Mobile Lifts |

| Sit-to-Stand & Transfer Aids |

| Bath & Pool Lifts |

| Stair & Wheelchair Platform Lifts |

| Lifting Slings |

| Accessories |

| Powered |

| Manual |

| Hospitals |

| Long-term & Nursing Homes |

| Home-care Settings |

| Rehabilitation Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Ceiling Lifts | |

| Floor/Mobile Lifts | ||

| Sit-to-Stand & Transfer Aids | ||

| Bath & Pool Lifts | ||

| Stair & Wheelchair Platform Lifts | ||

| Lifting Slings | ||

| Accessories | ||

| By Mechanism | Powered | |

| Manual | ||

| By End User | Hospitals | |

| Long-term & Nursing Homes | ||

| Home-care Settings | ||

| Rehabilitation Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the patient lifting equipment market in 2031?

It is expected to reach USD 7.73 billion, rising from USD 4.76 billion in 2026.

Which product category currently leads sales?

Ceiling lifts lead with 32.82% revenue share of the patient lifting equipment market in 2025.

Why is Asia-Pacific growing the fastest?

Hospital build-outs, aging populations, and supportive device-localization policies drive a 15.29% CAGR through 2031.

How fast are powered systems expanding?

Powered lifts are forecast to grow at a 13.21% CAGR, reinforcing their 79.53% revenue share.

What regulatory factors influence adoption?

Safe-patient-handling laws and reimbursement penalties for manual lifting propel equipment purchases in North America and Europe.

Page last updated on: