Ambulance Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

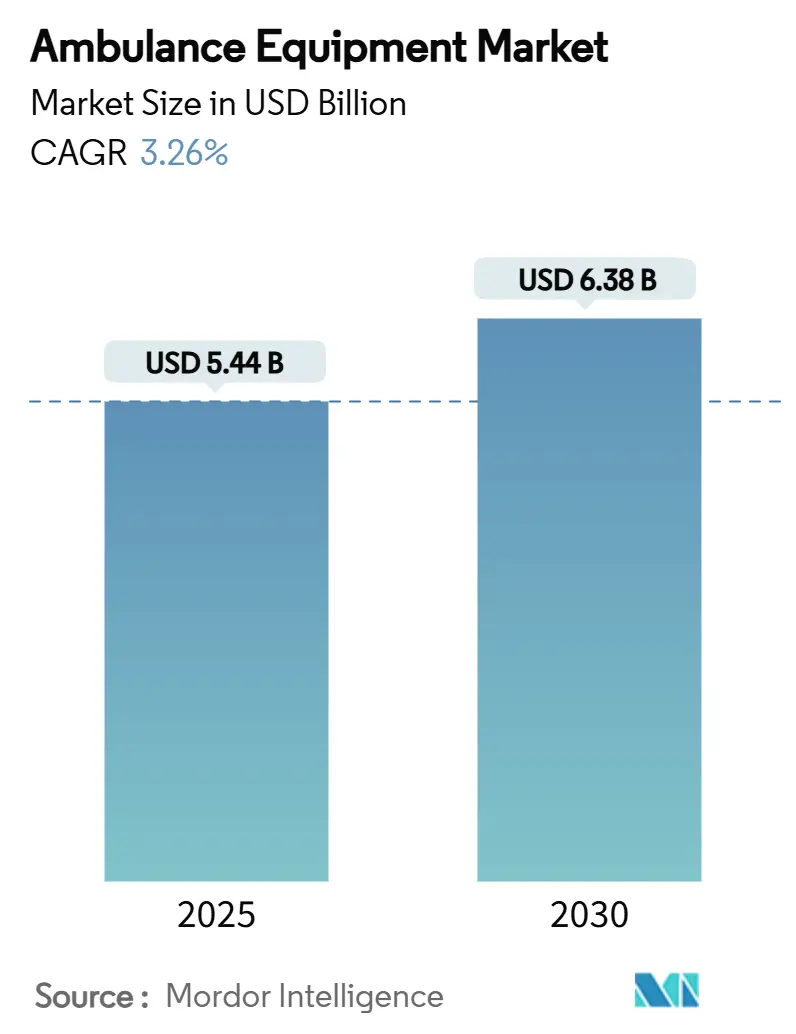

| Market Size (2025) | USD 5.44 Billion |

| Market Size (2030) | USD 6.38 Billion |

| Growth Rate (2025 - 2030) | 3.26% CAGR |

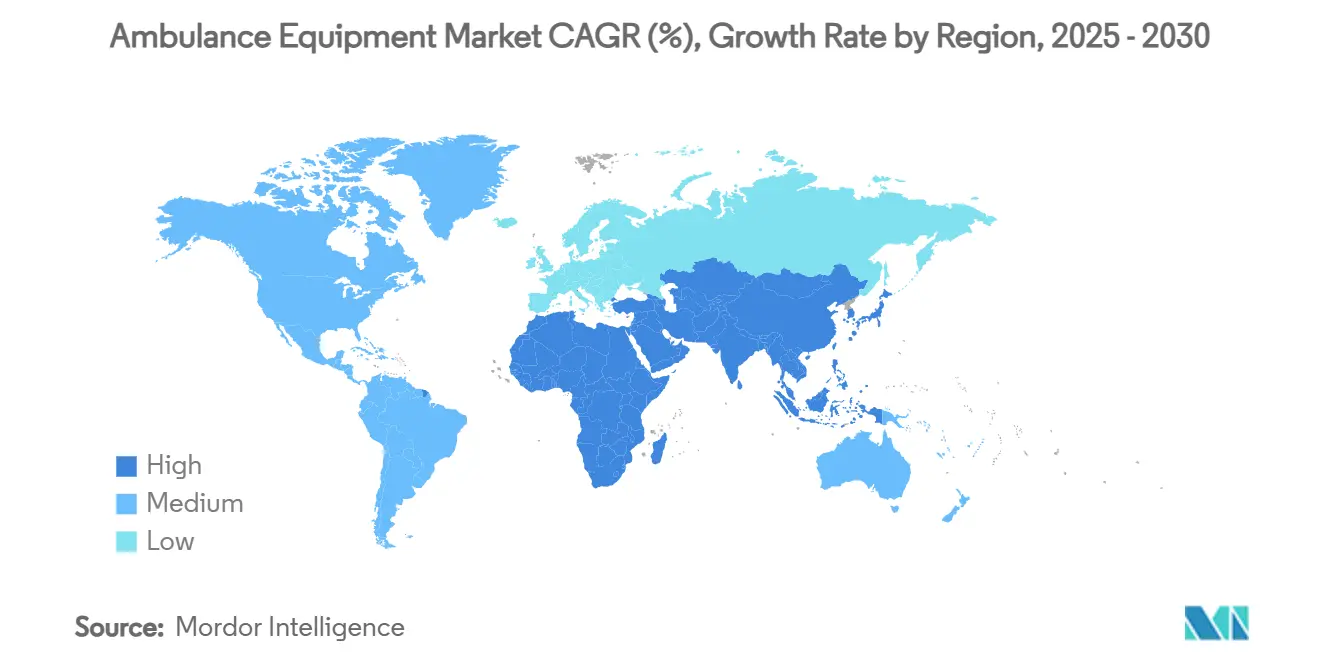

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambulance Equipment Market Analysis by Mordor Intelligence

The ambulance equipment market size stands at USD 5.44 billion in 2025 and is forecast to reach USD 6.38 billion by 2030, advancing at a 3.26% CAGR over the period. This modest but steady trajectory indicates a maturing marketplace in which aging populations, rising road-traffic injuries, and widening government expectations for pre-hospital care create an enduring demand baseline. Robust replacement cycles in high-income countries coexist with first-time procurements across low- and middle-income regions, especially where national health budgets are expanding. North America remains the largest regional contributor, underpinned by stringent equipment standards and high health-care spending, while Asia-Pacific records the fastest trajectory as new EMS infrastructures come on line. Air medical fleets, the embrace of low-emission vehicles, and rapid device miniaturization reinforce an innovation-centric competitive climate.

Key Report Takeaways

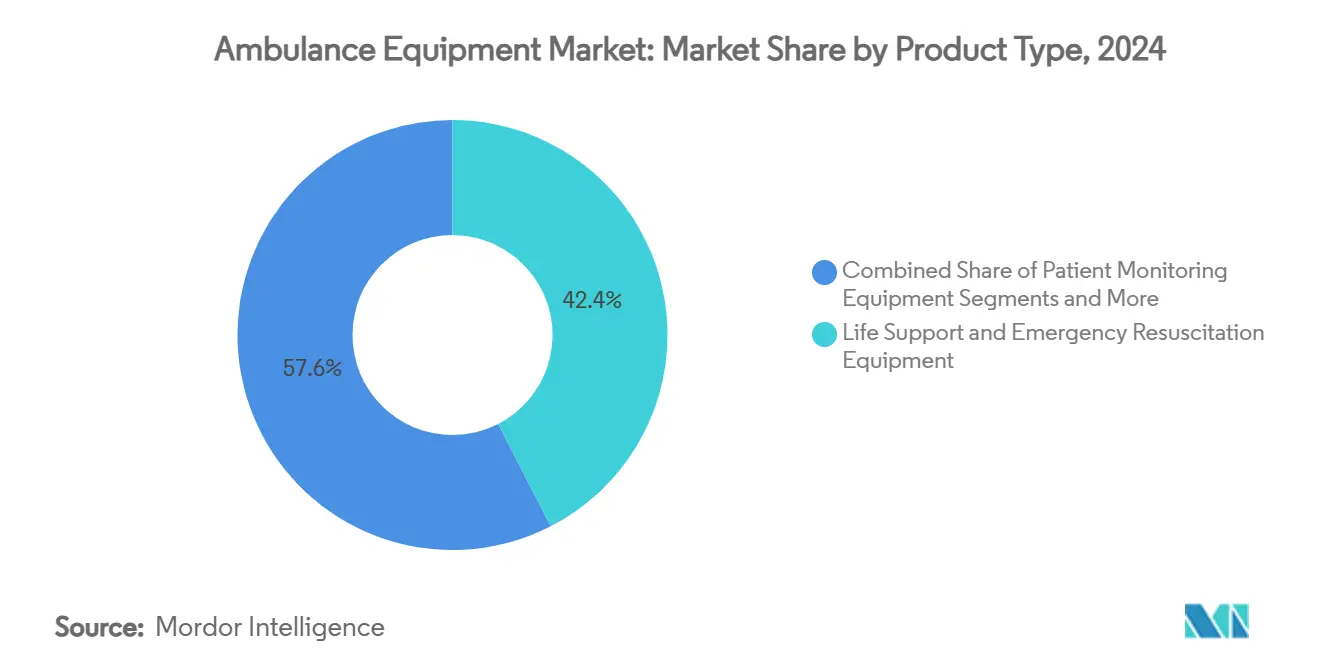

- By product type, life support and emergency resuscitation equipment accounted for 42.44% of the ambulance equipment market size in 2024, while respiratory and airway management devices are set to expand at a 6.79% CAGR through 2030.

- By vehicle type, ground ambulances led with 71.34% of ambulance equipment market share in 2024; air ambulances are projected to grow at a 5.83% CAGR to 2030.

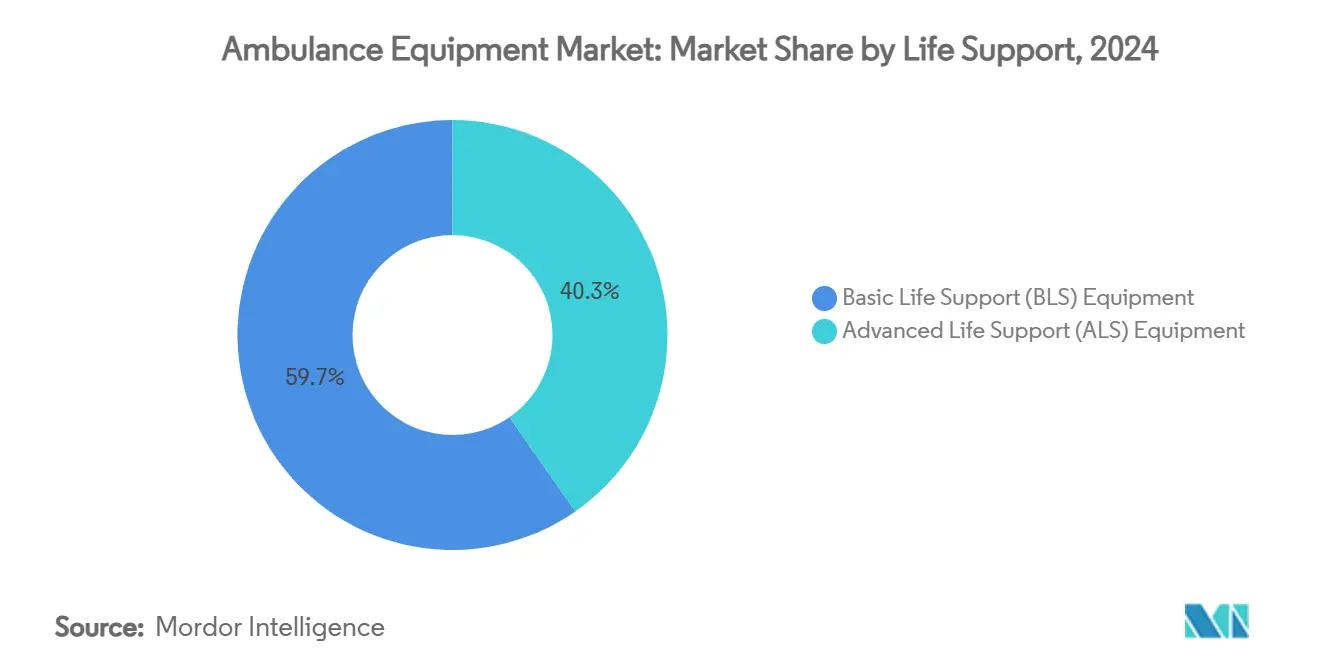

- By life-support level, basic life support equipment captured 59.66% share of the ambulance equipment market in 2024; advanced life support equipment is advancing at a 7.89% CAGR to 2030.

- By end user, hospitals and trauma centres held 51.23% share of the ambulance equipment market size in 2024, whereas emergency medical service providers are forecast to post a 6.57% CAGR between 2025-2030.

- By geography, North America commanded 35.48% of ambulance equipment market share in 2024; Asia-Pacific is projected to deliver a 5.73% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Ambulance Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Road Traffic Accidents & Medical Emergencies | +0.8% | Global, with highest impact in Asia-Pacific and developing regions | Medium term (2-4 years) |

| Growing Prevalence Of Cardiovascular & Chronic Diseases Requiring Pre-Hospital Care | +0.7% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Government Mandates For Advanced Life-Support (ALS) Standards In Ambulances | +0.6% | North America, Europe, and select Asia-Pacific markets | Medium term (2-4 years) |

| Rapid Miniaturisation & Connectivity Of Critical Care Devices | +0.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Adoption Of Battery-Powered, Low-Emission Equipment To Meet Fleet Decarbonisation Goals | +0.4% | Europe, North America, and progressive Asia-Pacific cities | Long term (≥ 4 years) |

| Smart-City Emergency Response Platforms Accelerating Demand For Connected Devices | +0.3% | Urban centers globally, particularly in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising incidence of road traffic accidents & medical emergencies

Annual emergency calls continue to escalate, with U.S. EMS teams responding to more than 350,000 out-of-hospital cardiac arrests in 2025. Urbanization intensifies collision risk, while ageing road infrastructure limits rapid response in many emerging markets. Provincial data from Maharashtra’s “108” service indicate that congestion can delay ambulance arrival by over seven minutes on average, a gap now being addressed through upgraded cardiac monitors and automated vehicle routing.[1]Sujata Saunik, “Analyzing the Maharashtra Ambulance Service ‘108’: The Prospect and Challenges,” Taylor & Francis Online, tandfonline.comGovernments are reacting: the Philippines has committed PHP 2 billion to procure 1,000 patient transport vehicles, widening equipment demand in Southeast Asia. Artificial-intelligence triage tools developed at Chalmers University demonstrated a potential 30% accuracy gain in patient-severity allocation across 47,000 ambulance cases, underscoring the imperative for data-enabled defibrillators and monitors. As emergency services pivot from reactive dispatch to predictive deployment, capital budgets prioritize interoperable, connected life-support platforms.

Growing prevalence of cardiovascular & chronic diseases requiring pre-hospital care

Cardiovascular disease remains the leading global mortality factor and reshapes ambulance kit configurations. Public-private campaigns such as ZOLL Medical’s partnership with professional athlete Damar Hamlin boost AED literacy amid low bystander confidence. Comparative research covering 25,000 cardiac arrest incidents shows that ZOLL X Series units delivered 63% return-of-spontaneous-circulation versus 56% for alternative devices, indicating that equipment choice can materially influence survival odds.[2]Bo Løfgren, “Association Between Defibrillation Using LIFEPAK 15 or ZOLL X Series and Survival Outcomes in Out-of-Hospital Cardiac Arrest,” Journal of the American Heart Association, ahajournals.org Portable ECMO systems, costing USD 127,000-139,000 and now deployable by specialized air medical teams, extend hospital-level intervention into pre-hospital domains. As chronic disease burdens mount, procurement priorities extend beyond defibrillation toward integrated cardiopulmonary platforms and real-time telemetry.

Government mandates for advanced life-support standards in ambulances

Regulators increasingly codify equipment minima. Ontario’s Advanced Life Support Patient Care Standards (Version 5.3) impose new monitor, ventilator, and drug-delivery baselines effective 2024. The U.S. Department of Homeland Security’s SAVER assessments guide procurement by benchmarking life-support technology for municipal EMS operators.[3]U.S. Department of Homeland Security, “Advanced Life Support Monitoring Systems for EMS,” dhs.gov In Europe, vertical take-off and landing (VTOL) airframes earmarked for medical missions must meet performance and cabin-layout standards outlined by the European Union Aviation Safety Agency. Moving from prescriptive lists to performance-based frameworks obliges manufacturers to integrate connectivity, weight efficiency, and cybersecurity by design, fueling a continuous upgrade cycle across the ambulance equipment market.

Rapid miniaturization and connectivity of critical-care devices

Device footprints shrink while functionality grows. Stryker’s 5 kg LIFEPAK 35 consolidates monitoring and defibrillation in a smaller housing and streams waveforms to hospital dashboards in real time. GE HealthCare’s CARESCAPE Canvas platform, cleared by the FDA, leverages modular hardware and software to scale up or down according to patient acuity, enabling EMS providers to equip compact vehicles without clinical compromise. Philips’ Tempus ALS couples lightweight monitors with a secure telehealth hub, allowing physicians to observe vitals before patient arrival. These advances ease vehicle weight constraints, free interior space for additional therapy options, and lay the groundwork for predictive maintenance programs that improve fleet uptime.

Restraints Impact Analysis of Ambulance Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Of Advanced Equipment In Low- & Middle-Income Regions | -0.9% | Asia-Pacific (excluding developed markets), Africa, Latin America | Long term (≥ 4 years) |

| Lengthy Regulatory Approval & Certification Cycles | -0.6% | Global, particularly stringent in North America and Europe | Medium term (2-4 years) |

| Semiconductor Supply-Chain Bottlenecks For Patient-Monitor Sub-Assemblies | -0.7% | Global, with highest impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Electromagnetic Interference Issues Inside New EV Ambulances Limiting Legacy Gear | -0.4% | Europe, North America, and progressive cities adopting electric fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of advanced equipment in low- and middle-income regions

Sophisticated defibrillators, portable ultrasound, and ECMO systems remain financially out of reach for many public EMS operators. A single ECMO kit costs USD 127,000-139,000, equivalent to the annual operating budget of smaller municipal services in parts of Africa and South Asia. Resource-limited airway management studies list equipment shortages and constrained training as persistent barriers. While national grants, such as the Philippines’ PHP 2 billion roll-out of 1,000 transport vehicles, mitigate gaps, funding rarely covers top-tier devices. Suppliers therefore pursue tiered product strategies—ruggedized, budget-priced monitors for basic life support and premium connected devices for advanced care markets—fragmenting global demand profiles within the ambulance equipment market.

Semiconductor supply-chain bottlenecks for patient-monitor sub-assemblies

Half of all medical devices depend on specialized chips, making cardiac monitors and ventilator controllers vulnerable to production stoppages. Geopolitical friction in Eastern Europe and the Middle East has prolonged lead times; the medical device sector is now allocating 3-5% of annual revenue to supply-chain resilience initiatives. The FDA’s January 2025 alert spotlights risks to pediatric ventilator repairs owing to component scarcity. Manufacturers that redesign boards around standard chips or diversify foundry contracts enjoy a competitive edge, but higher bill-of-materials costs feed through to procurement budgets, tempering demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ambulance Equipment Market Segment Analysis

By Product Type:

Life support remains anchor while respiratory care acceleratesLife support and emergency resuscitation equipment represented 42.44% of ambulance equipment market share in 2024 as automated external defibrillators, multiparameter monitors, and infusion pumps formed the clinical core of most fleets. Elevated cardiovascular disease incidence keeps defibrillator replacement cycles brisk, while regulators in North America require two-channel waveform capability for all newly licensed units. The respiratory and airway management category logs a 6.79% CAGR through 2030, buoyed by new ventilation protocols and innovations such as the MEDUMAT Easy CPR portable ventilator that now operates in more than 100 countries. The infection-control sub-segment maintains post-pandemic momentum, with hydrogen-peroxide vapor decontamination systems capable of 6-log sporicidal reduction in 45 minutes—appealing to hospital-linked EMS operators seeking to minimize turnaround times.

Demand patterns are diversifying: multi-function patient monitors with Bluetooth gateways and cloud dashboards are replacing legacy three-parameter devices. Suppliers embed predictive analytics that alert crews to impending hypoxia, pushing ambulance equipment market size for premium monitors upward despite slower unit growth. Manufacturers also invest in rugged casings and IP-rated connectors to withstand vibration in off-road missions across emerging economies, bridging high-tech capability with low-resource reliability.

By Vehicle Type:

Ground fleets dominant as air capacity expandsGround ambulances generated 71.34% of ambulance equipment market revenue in 2024, anchored by broad urban and rural coverage requirements and government fleet replacement subsidies. The shift toward electric drivetrains is rapid: the United Kingdom’s National Health Service plans a USD 637 million investment in low-emission models, stimulating redesign of monitors and suction pumps to operate efficiently on auxiliary batteries. Air ambulances register a 5.83% CAGR to 2030, propelled by Global Medical Response’s newly signed option for up to 15 Airbus H140 helicopters that feature capacious cabins ideal for ECMO kits.

Regulations encouraging VTOL craft could accelerate airborne market penetration in densely populated European corridors where rooftop landing zones are feasible. Water ambulances remain niche, servicing archipelago nations and remote riverine communities but contributing modestly to overall ambulance equipment market size.

By Life-Support Level:

Basic coverage widespread; advanced capabilities risingBasic life support packages—stretcher, oxygen supply, and manual defibrillation—represented 59.66% of ambulance equipment market share in 2024 as most municipal operators standardize on this cost-effective baseline. Training manikins from Ambu and Laerdal reinforce competency for tens of thousands of new EMTs annually. However, advanced life support deployments are growing at 7.89% CAGR, catalyzed by provincial mandates that require waveform capnography, infusion pumps, and point-of-care ultrasound on all high-acuity runs. BARDA’s partnership with GE HealthCare to create AI-augmented portable ultrasound units exemplifies the push to embed sophisticated diagnostics in compact frames.

The ambulance equipment market size for ALS devices will accelerate further as payers reimburse field-initiated thrombolysis and blood-pressure-guided fluid therapy. Simulation firms such as iSimulate now ship Atlas ALS manikins that replicate real-time vitals on a tablet, shortening skills acquisition loops for paramedics.

By End User:

Hospitals anchor purchasing while EMS providers scale fastestHospitals and trauma centres influenced 51.23% of global spend in 2024, leveraging integrated supply chains and capital budgets to set equipment specifications for contracted ambulance operators. Large academic centres routinely purchase state-of-the-art monitors expressly to standardize data feeds into electronic health records upon patient arrival. Emergency medical service providers—public, private, and hybrid—are forecast to grow equipment outlays at a 6.57% CAGR, fueled by expanding urban catchment zones and the emergence of tele-EMS triage programs.

Military and defence agencies continue to shape high-specification mobile intensive-care units, evident in the U.S. Army’s MEDEVAC cabin demonstrator that incorporates paramedic feedback on stretcher ergonomics and equipment rails. Veterans Affairs contracts, such as the Phoenix VA agreement covering more than 139,000 beneficiaries, underline the scale and specialization of government ambulance procurement .

Geography Analysis

North America Ambulance Equipment Market

North America maintained 35.48% of 2024 revenue owing to well-funded EMS systems and detailed certification regimes. U.S. standards from bodies such as the Department of Homeland Security set reference equipment lists that municipalities emulate, reinforcing replacement demand every five to seven years. Canadian provinces are aligning with similar protocols; Ontario updated its ALS guideline in 2024, compelling ambulance services to upgrade monitoring and ventilation assets. Mexico’s expanding Seguro Popular coverage and federal-state matching grants spur incremental market growth, particularly for basic life support kits.

Europe Ambulance Equipment Market

Europe benefits from regulatory harmonization under the Medical Device Regulation and a policy drive toward green fleets. The United Kingdom’s USD 637 million electric ambulance program accelerates purchases of low-power monitors and suction units optimized for battery operation. Germany’s air ambulance charities, such as DRF Luftrettung, trial sustainable aviation fuel, prompting avionics-compatible medical devices.

APAC Ambulance Equipment Market

Asia-Pacific is the fastest-growing regional segment, registering a 5.73% CAGR to 2030. Government investments include the Philippines’ rollout of 1,000 patient transport vehicles and Japan’s adoption of compact electric ambulances suited to dense urban layouts. China’s tiered EMS network reforms incentivize rural county fleets to acquire ventilator-equipped vans, while Australia deploys telehealth-enabled units across vast remote territories.

MEA and South America Ambulance Equipment Market

The Middle East and Africa present mixed dynamics: oil-rich Gulf states buy high-end connected monitors, whereas lower-income sub-Saharan nations rely on donor-funded basic life support packages. South America records mid-single-digit growth as urbanization and private-sector insurance penetration expand EMS provider networks, leading to sustained demand for rugged, cost-efficient devices.

Competitive Landscape

The ambulance equipment market hosts a blend of multinational medical device leaders and agile specialists. Stryker, GE HealthCare, Philips, and ZOLL are leveraging global manufacturing footprints and regulatory expertise. Smaller firms such as WEINMANN Emergency, Demers, and LifeSigns thrive in niche domains—portable ventilators, electric chassis integration, and IoT middleware respectively—differentiating through rapid innovation cycles.

Strategic moves accentuate solution bundling. Stryker opened a Customer Experience Centre in India to demonstrate full-fleet interoperability from stretcher to cloud dashboard. Global Medical Response’s long-term helicopter order strengthens vertical integration by marrying airframe and medical kit procurement. Battery-powered product lines expand as environmental rules tighten: Demers unveiled the eFX prototype ambulance, incorporating modular lithium-ion packs and low-draw ventilators.

Supply-chain resilience is a competitive differentiator. Medtronic shrank its supplier base by 30% to mitigate chip scarcity, while start-ups that secure foundry partnerships capture share from incumbents constrained by allocation quotas. As AI adoption rises, relationships with cloud and telecom providers such as floLIVE become pivotal, evidenced by the 5GIoT connected ambulance consortium.

Looking forward, consolidation is likely in mid-tier segments where price competition compresses margins, while premium players pursue subscription models for data analytics that complement hardware sales. Robust intellectual property portfolios around waveform analysis and wireless telemetry will be a decisive moat as commoditization pressures rise in basic equipment categories.

Ambulance Equipment Industry Leaders

Stryker Corporation

GE HealthCare

Drägerwerk AG & Co. KGaA

Philips Healthcare

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Ambulance Equipment Market Companies Covered in this Report

- Stryker

- GE HealthCare Technologies

- Dragerwerk

- Koninklijke Philips

- Medtronic

- Zoll Medical (Asahi Kasei)

- Smiths Group

- Ferno-Washington

- Laerdal Medical

- Ambu

- Allied Healthcare Products

- Bound Tree Medical

- Medline Industries

- B. Braun

- Terumo

- Cardinal Health

- Solventum

- Smiths Detection

- Airon Corp.

- Flexicare Medical

Recent Industry Developments in Ambulance Equipment Market

- March 2025: Global Medical Response signed an agreement with Airbus for up to 15 H140 helicopters configured for emergency medical services.

- September 2024: B. Braun Medical received FDA clearance for the Introcan Safety 2 Deep Access IV Catheter with passive needlestick protection.

- July 2024: B. Braun Medical announced Gillette Children’s Hospital as the first U.S. facility to convert to NRFit connectors for neuraxial administrations.

- June 2024: Stryker released the LIFEPAK 35 monitor/defibrillator featuring real-time data streaming and workflow-oriented ergonomics.

Global Ambulance Equipment Market Report Scope

Segmentation Overview

| Life Support & Emergency Resuscitation Equipment |

| Patient Monitoring Equipment |

| Patient Handling & Transport Equipment |

| Respiratory & Airway Management Devices |

| Infection-Control & Consumables |

| Ground Ambulances |

| Air Ambulances |

| Water Ambulances |

| Basic Life Support (BLS) Equipment |

| Advanced Life Support (ALS) Equipment |

| Hospitals & Trauma Centres |

| Emergency Medical Service (EMS) Providers |

| Military & Defence Agencies |

| Ambulatory Surgical Centres & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Product Type | Life Support & Emergency Resuscitation Equipment | |

| Patient Monitoring Equipment | ||

| Patient Handling & Transport Equipment | ||

| Respiratory & Airway Management Devices | ||

| Infection-Control & Consumables | ||

| Vehicle Type | Ground Ambulances | |

| Air Ambulances | ||

| Water Ambulances | ||

| Life Support Level | Basic Life Support (BLS) Equipment | |

| Advanced Life Support (ALS) Equipment | ||

| End User | Hospitals & Trauma Centres | |

| Emergency Medical Service (EMS) Providers | ||

| Military & Defence Agencies | ||

| Ambulatory Surgical Centres & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the ambulance equipment market?

The ambulance equipment market size is USD 5.44 billion in 2025 and is projected to reach USD 6.38 billion by 2030.

2. Which region shows the fastest growth?

Asia-Pacific is forecast to grow at a 5.73% CAGR through 2030, propelled by large-scale government fleet investments and expanding EMS infrastructure.

3. What product segment dominates spending?

Life support and emergency resuscitation equipment commands the largest share at 42.44% of 2024 revenues, driven by cardiac-care priorities.

4. How significant are air ambulances to future demand?

Air ambulances are the fastest-growing vehicle category at a 5.83% CAGR, supported by helicopter fleet expansions and portable ECMO adoption.

5. Why are semiconductor shortages a concern for EMS operators?

Patient monitors and ventilators rely on specialized chips; ongoing supply bottlenecks elevate costs and delay deliveries, damping near-term market growth.

Page last updated on: