Medical Device Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 148.64 Billion |

| Market Size (2031) | USD 273.38 Billion |

| Growth Rate (2026 - 2031) | 12.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Outsourcing Market Analysis by Mordor Intelligence

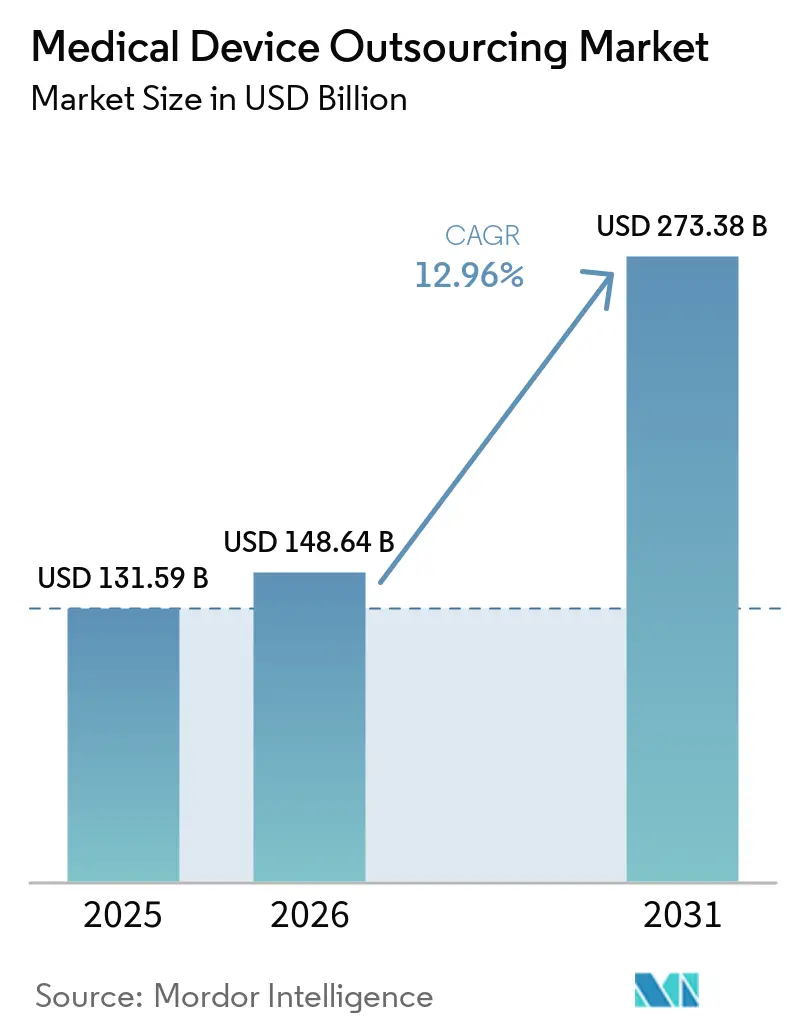

The Medical Device Outsourcing Market size was valued at USD 131.59 billion in 2025 and is estimated to grow from USD 148.64 billion in 2026 to reach USD 273.38 billion by 2031, at a CAGR of 12.96% during the forecast period (2026-2031).

OEMs are increasingly outsourcing capacities to achieve better cost structures and operational flexibility. The medical device outsourcing market has expanded beyond production to include design validation, process transfer, and post-market support, driven by rising device complexity and stricter compliance requirements. Supplier consolidation is encouraging OEMs to partner with firms capable of managing larger portions of the value chain, reducing reliance on multiple vendors. However, the market faces challenges such as quality liability, limited coating, machining, and sterilization capacities, and lengthy validation timelines for newly qualified production sites. Intellectual property concerns also persist as OEMs share more design and process knowledge with partners, but these factors are moderating growth rather than altering the market's long-term trajectory.

Key Report Takeaways

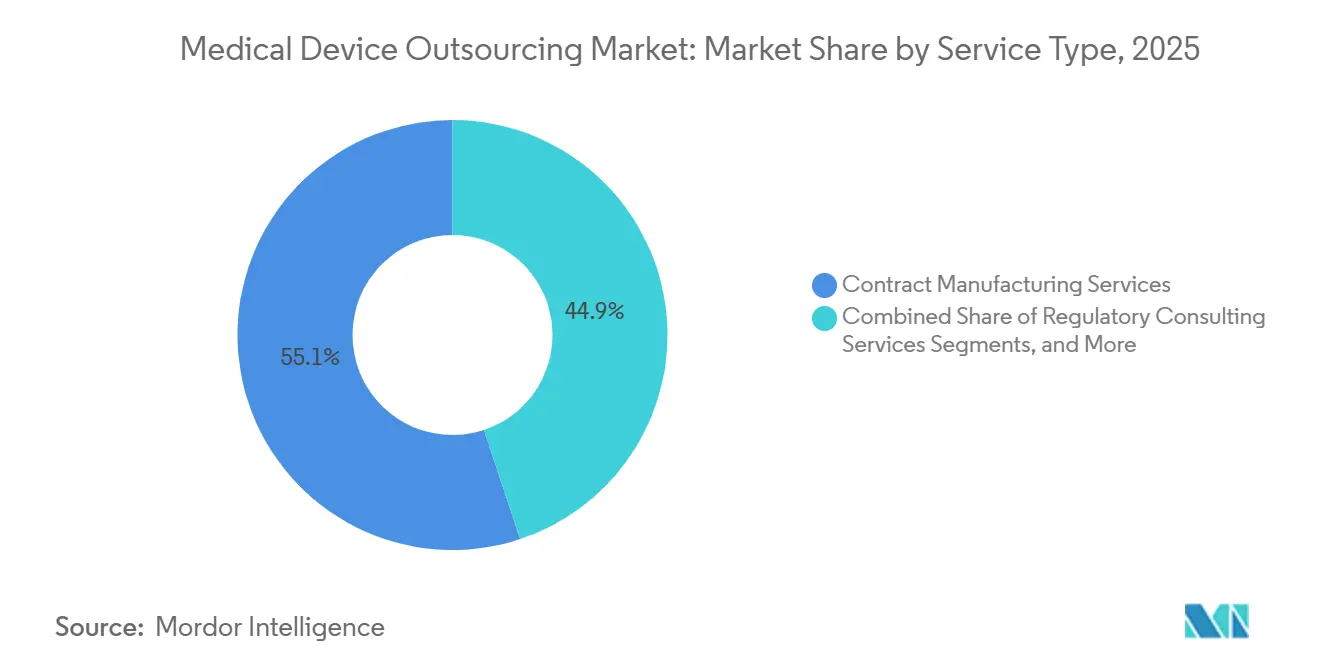

- By service type, contract manufacturing held 55.13% of revenue in 2025, while regulatory consulting services are expected to be the fastest-growing service category through 2031.

- By device class, Class II devices held 52.13% of revenue in 2025, while Class III is projected to expand at a 14.55% CAGR through 2031.

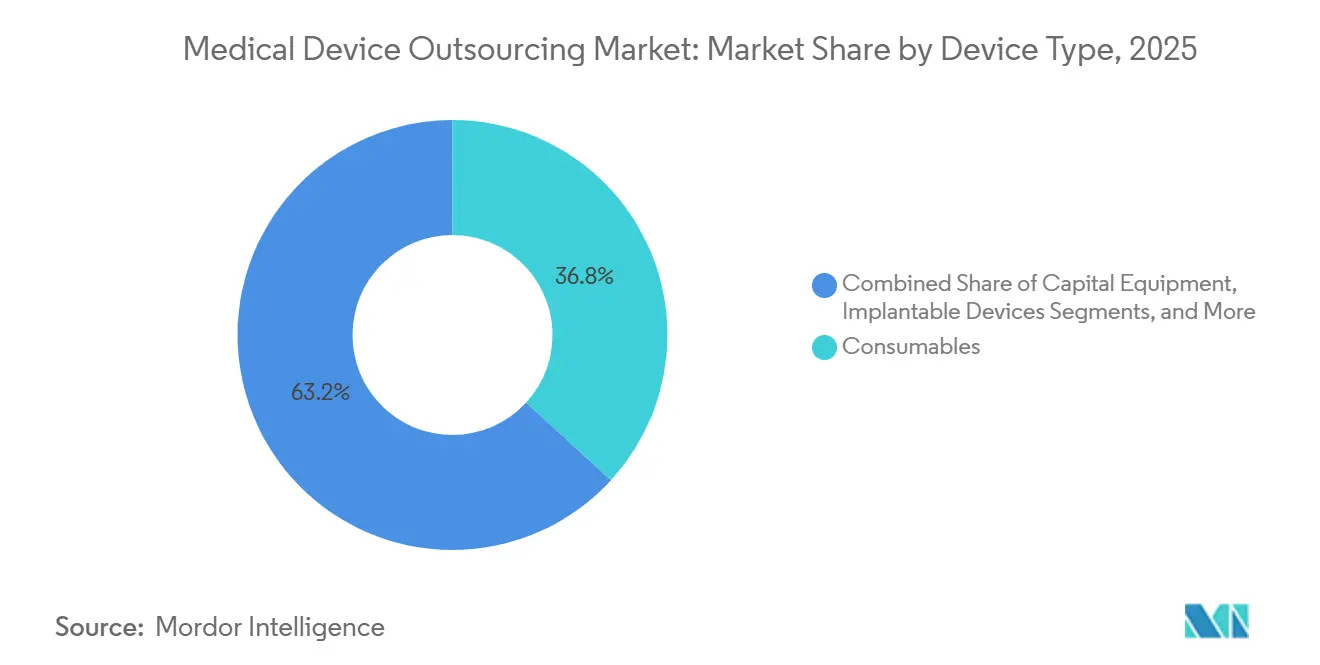

- By device type, consumables held 36.77% of revenue in 2025, while implantables are projected to expand at a 13.88% CAGR through 2031.

- By application, cardiovascular devices accounted for 25.44% of the medical device outsourcing market size in 2025, while diabetes care is expected to grow at a 14.45% CAGR through 2031.

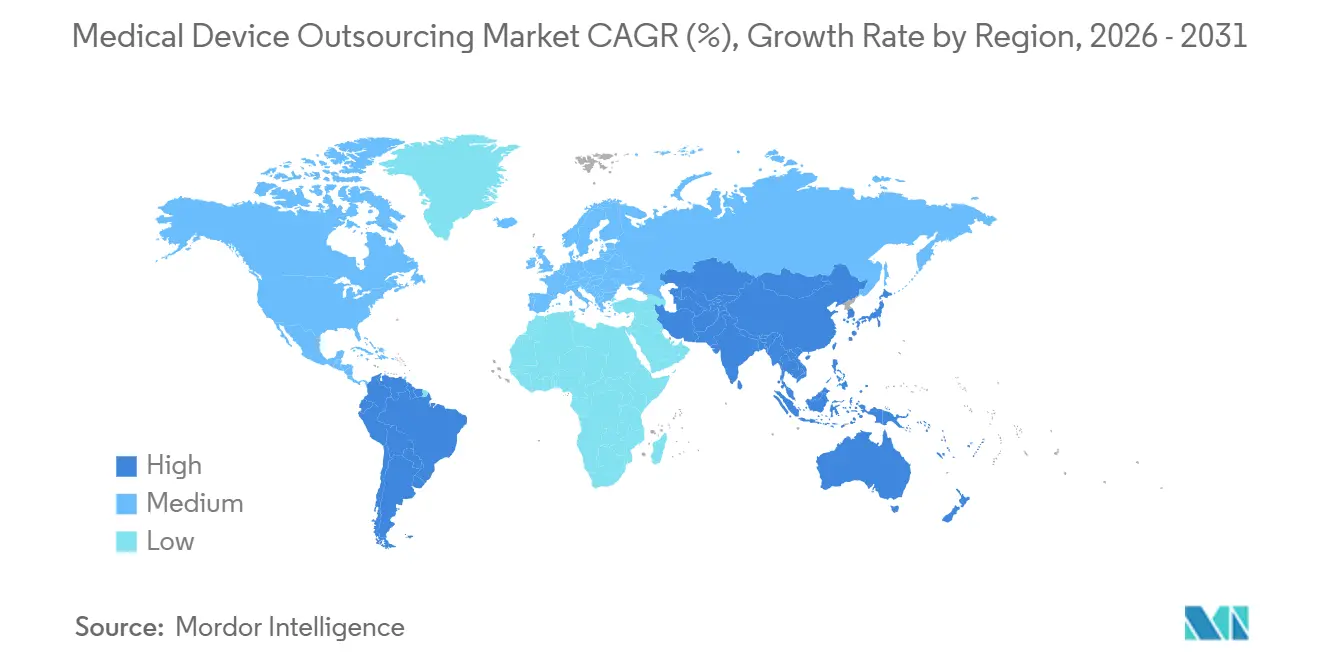

- By geography, North America held 39.56% of the medical device outsourcing market share in 2025, while Asia-Pacific is projected to record a 15.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising OEM focus on core competencies and cost optimization | +2.5% | Global, with concentration in North America and Western Europe | Short term (≤ 2 years) |

| Faster time to market for complex medical devices | +2.0% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing need for scalable regulated manufacturing capacity | +1.8% | Global, particularly Asia-Pacific and North America | Medium term (2-4 years) |

| Rising outsourcing of design, development, and validation work | +1.5% | North America, with spillover into Europe | Medium term (2-4 years) |

| Expansion of connected, software-enabled medical devices | +1.2% | Global, with early gains in the United States, Germany, Japan, and South Korea | Long term (≥ 4 years) |

| Supply chain diversification and nearshoring initiatives | +1.0% | North America and Europe, with spillover into Middle East and Africa and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising OEM Focus on Core Competencies and Cost Optimization

Medical device OEMs are concentrating on product design, intellectual property, and commercialization while outsourcing capital-intensive production tasks to specialized partners. This shift reduces the burden of managing cleanroom qualifications, sterilizations, and process validations in-house. The medical device outsourcing market benefits as OEMs treat these activities as variable operating costs rather than fixed assets. With broader therapy portfolios, qualification demands, documentation, and complexity increase, making outsourcing a strategic choice. Major platforms are integrating manufacturing, sterilization, and quality support, enabling OEMs to lower asset intensity and enhance flexibility without losing commercial focus.

Faster Time to Market for Complex Medical Devices

Speed is a critical factor for OEMs launching minimally invasive systems, connected platforms, and combination products in regulated categories. The medical device outsourcing market gains as established partners streamline documentation, verification, and pre-launch processes. Pre-validated templates and experienced quality teams reduce delays, especially for devices requiring extensive biocompatibility and sterile processing. Outsourcing partners with cleanroom capacities enable faster commercialization by eliminating the need for OEMs to build and validate new infrastructure. Partnerships like Jabil's 2025 collaboration with HSE AG highlight the focus on accelerating prototype-to-market transitions while enhancing supply chain resilience. The market thus delivers both production capacity and commercially critical time.

Growing Need for Scalable Regulated Manufacturing Capacity

Chronic disease devices reveal a capacity gap that OEMs struggle to address within required timelines. Products like continuous glucose monitoring systems and insulin patch pumps demand cleanroom assembly, precision sub-assembly, and validated quality systems. The medical device outsourcing market benefits as specialist partners rapidly expand regulated capacities, outpacing OEMs in building and qualifying internal sites. West Pharmaceutical Services, for example, completed an USD 80 million expansion in Grand Rapids and opened a 165,000-square-foot facility in Dublin in March 2026 to support high-volume injectable therapies. These expansions demonstrate proactive capacity additions in segments where scale and compliance are critical.

Rising Outsourcing of Design, Development, and Validation Work

The outsourcing scope now includes design verification, process validation, and regulatory preparations. Early collaboration between OEMs and outsourcing partners addresses manufacturing constraints before design transfers, reducing redundant qualification efforts and schedule delays. Flex's 2025 launch of a New Product Introduction Center in North America exemplifies this trend, enabling healthcare clients to transition seamlessly from design to manufacturing. The medical device outsourcing market is becoming integral to designing products for manufacturability from the outset, ensuring fewer handoffs, minimized audit gaps, and enhanced accountability.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Quality liability and recall risk across outsourced supply chains | -1.2% | Global, most acute in North America and the European Union | Medium term (2-4 years) |

| High switching costs due to validation, tooling, and requalification | -0.9% | Global | Long term (≥ 4 years) |

| Intellectual property protection and confidentiality concerns | -0.8% | Global, most acute in Asia-Pacific and multi-country networks | Medium term (2-4 years) |

| Regulatory complexity across multi-country manufacturing networks | -1.5% | European Union, North America, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Quality Liability and Recall Risk Across Outsourced Supply Chains

Legal manufacturers remain responsible for device quality, even when production involves multiple external partners. OEMs cannot fully transfer regulatory obligations through contracts, making quality oversight a critical challenge in the medical device outsourcing market. The complexity increases for devices requiring specialized suppliers for coatings, machining, sterilization, and assembly across various locations. Europe’s expanded supply chain liability adds pressure on indemnification, supplier controls, and documentation, raising costs for audits, quality agreements, and corrective actions. While the market grows, quality accountability drives cautious outsourcing decisions in sensitive categories.

High Switching Costs Due to Validation, Tooling, and Requalification

Switching outsourcing partners is challenging once a device, process, and regulatory filings are tied to a qualified manufacturing route. For high-risk devices, transitions may require new tooling, repeated validations, and regulatory submissions, delaying commercial shipments by 12 to 24 months. This creates a lock-in effect, especially for OEMs relying on validated specialized processes. Integer Holdings has strengthened this dynamic by expanding capabilities through acquisitions like Precision Coating and VSi Parylene, consolidating access to validated technologies. In the medical device outsourcing market, incumbency, technical expertise, and validated history often outweigh cost considerations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Contract Manufacturing Anchors Revenue, Consulting Grows Fastest

In 2025, contract manufacturing accounted for 55.13% of the revenue, maintaining its leading role in the medical device outsourcing market. This dominance reflects OEMs' preference for outsourcing precision machining, cleanroom assembly, sterilization integration, and subsystem qualification, which require specialized assets and stringent quality systems. Production remains the primary outsourcing choice due to its significant capital requirements and cost flexibility, anchoring revenue even as other functions gain importance.

Regulatory consulting services are the fastest-growing segment, driven by increasing compliance complexities that OEMs find challenging to manage internally. Other services, including product testing, sterilization, design and development, upgrades, maintenance, and logistics, are also expanding. Early collaboration in product design reduces design transfer issues, while logistics and aftermarket support are increasingly integrated into broader service contracts, narrowing the gap between manufacturing and service bundles.

By Device Class: Class II Underpins Volume, Class III is Fastest-Growing

Class III devices are projected to grow at a 14.55% CAGR through 2031, outpacing the overall market average. This growth is driven by increased outsourcing demand for implantable and clinically complex devices, requiring expertise in sterile processing and biocompatibility. The shift highlights that outsourcing is increasingly capability-driven, especially for high-risk, complex products, positioning Class III programs as a key growth area for specialized partners.

Class II devices remained the largest revenue segment in 2025, supported by cardiovascular, orthopedic, and diagnostic programs. Class I devices also contribute significantly, particularly in disposables and consumables, where speed and consistency are prioritized. The market shows a clear distinction between volume-driven outsourcing in Class I and II products and capability-driven outsourcing in Class III. Integer Holdings has invested over USD 700 million in acquisitions since 2025, focusing on cardiovascular systems and neuromodulation capabilities, aligning with the industry's shift toward complex platforms.

By Device Type: Consumables Lead in Volume, Implantables Redefine the Value Proposition

In 2025, consumables held a 36.77% revenue share, driven by high production volumes, steady demand for single-use devices, and economies of scale achieved by experienced contract manufacturers. OEMs often redirect capital from high-throughput lines to higher-margin areas like product development, making consumables a stable foundation for the market.

Implantables are the fastest-growing segment, reshaping value creation in the market. Their production demands, including precision machining and sterile assembly, highlight the importance of specialized partners. Other segments, such as capital equipment, IVD devices, and wearable medical devices, bring unique technical challenges, reflecting a shift from volume-centric outsourcing to a mix of throughput and high-value technical intensity.

By Application: Cardiovascular Dominates, Diabetes Care Sets the Growth Pace

In 2025, cardiovascular devices accounted for 25.44% of the market, driven by broad clinical applications and reliance on specialized capabilities like catheter extrusion and sterile assembly. These complexities foster strong partnerships with providers, ensuring cardiovascular work remains a significant revenue contributor despite the growth of newer applications.

Diabetes care is projected to grow at a 14.45% CAGR through 2031, fueled by demand for advanced systems like continuous glucose monitors and wearable drug-delivery platforms. Medtronic's product launches and partnerships, along with West Pharmaceutical Services' capacity expansions, reflect the sector's growth. Orthopedic, respiratory, drug delivery, ophthalmic, and dental applications further diversify the market across therapeutic areas.

Geography Analysis

In 2025, North America accounted for 39.56% of the medical device outsourcing market, maintaining its leading regional position. The region benefits from a strong OEM base, established CDMO networks, and alignment with FDA-regulated supply chains. Providers with expertise in 510(k) and PMA-related manufacturing strengthen the ecosystem by supporting documented transfer and scale-up processes. Nearshoring is expanding the region's influence into nearby hubs like Mexico and Costa Rica.

Asia-Pacific is the fastest-growing region in the medical device outsourcing market, with a projected 15.12% CAGR through 2031. Growth is driven by expanding healthcare infrastructure, cost-efficient production, and favorable policies attracting global outsourcing programs. China remains the largest manufacturing base due to its scale and integrated supply chains, but geopolitical uncertainties and tariffs are prompting OEMs to diversify into countries like Malaysia, Thailand, Singapore, and India.

Europe remains a key production base, led by Germany, Ireland, and the UK in cardiovascular, orthopedic, ophthalmic, and IVD programs. Ireland excels in catheter manufacturing, cleanroom assembly, and precision polymer processing. The European Commission’s 2025 proposal to simplify EU MDR and IVDR frameworks and the 2026 regulation on notified body requirements are expected to ease certification bottlenecks, enabling faster outsourcing growth. The Middle East, Africa, and South America hold smaller shares but are gaining strategic importance as OEMs seek diversified manufacturing and resilient supply chains.

Competitive Landscape

The medical device outsourcing market is moderately consolidated at the top but includes a diverse range of mid-sized and niche providers. WuXi AppTec Co., Ltd., Charles River Laboratories International, Inc., Jabil Inc., Celestica Inc., and TE Connectivity Ltd. dominate the full-service tier by combining manufacturing scale with design, engineering, and global delivery support. Their ability to offer integrated programs, rather than isolated production steps, aligns with OEMs' preference for fewer partners with broader accountability across development and manufacturing.

Specialist providers such as Integer Holdings, Viant Medical, and Minnetronix Medical focus on technically demanding areas like cardiovascular systems, implantables, and high-value components. Integer has strengthened its position through acquisitions, enhancing capabilities in coatings, precision machining, and active implantables. Flex expanded its healthcare support model in 2025 with a dedicated North American New Product Introduction Center, improving integration between design and manufacturing. West Pharmaceutical Services increased capacity for high-volume drug delivery devices, emphasizing regulated expansion to target chronic disease programs. These developments highlight that capability depth, integrated services, and timely capacity additions are key drivers in the market.

Competition below the top tier remains intense, particularly in specialized niches where technical expertise often outweighs size. The fragmented mid-layer of companies competes on specific processes, therapies, or regional manufacturing strengths, maintaining pricing pressure in certain bids. However, long validation cycles and switching costs protect established suppliers once production routes are approved and scaled. The market reflects moderate top-tier concentration alongside significant fragmentation, offering opportunities for consolidation while preserving competition in various subsegments.

Medical Device Outsourcing Industry Leaders

WuXi AppTec Co., Ltd.

Charles River Laboratories International, Inc.

Jabil Inc.

Celestica Inc.

TE Connectivity Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: West Pharmaceutical Services expanded its Damastown, Dublin facility by 165,000 square feet, enhancing automation and capabilities for high-volume injectable drug delivery devices, targeting diabetes and obesity treatments, and supporting European OEM clients.

- January 2026: Jabil Inc. partnered with TxSphere to strengthen its expertise in designing and manufacturing complex drug-device combination products, expanding its end-to-end pharmaceutical and device manufacturing capabilities.

- January 2026: Arterex acquired Synecco, an Ireland-based CDMO specializing in device engineering and manufacturing, boosting its European capabilities in structural heart treatment technologies.

- November 2025: Sanmina Corporation expanded its Fermoy, Ireland facility with a new ISO 8 clean room and automation lines for wearable medical device production, marking its largest medical manufacturing site in Europe.

- September 2025: Freudenberg Medical opened a USD 25 million, 50,000-square-foot facility in Costa Rica’s Coyol Free Zone, dedicated to high-volume catheter assembly for electrophysiology, vascular, and structural heart therapies.

Global Medical Device Outsourcing Market Report Scope

As per the scope of the report, medical device outsourcing is the business practice of hiring specialized third-party companies to handle parts of a medical device’s design, manufacturing, or testing, rather than doing everything in-house.

The medical device outsourcing market is segmented by service type, device class, device type, application, and geography. By service type, the market includes product design and development services, product testing and sterilization services, regulatory consulting services, contract manufacturing services, product upgrade services, product maintenance services, and logistics and aftermarket services. By device class, the market is segmented into Class I medical devices, Class II medical devices, and Class III medical devices. By device type, the market is categorized into consumables, capital equipment, implantable devices, in vitro diagnostics devices, and wearable medical devices. By application, the market is segmented into cardiovascular, orthopedic, dental, respiratory, drug delivery, diabetes care, ophthalmic, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Product Design And Development Services |

| Product Testing And Sterilization Services |

| Regulatory Consulting Services |

| Contract Manufacturing Services |

| Product Upgrade Services |

| Product Maintenance Services |

| Logistics And Aftermarket Services |

| Class I Medical Devices |

| Class II Medical Devices |

| Class III Medical Devices |

| Consumables |

| Capital Equipment |

| Implantable Devices |

| In Vitro Diagnostics Devices |

| Wearable Medical Devices |

| Cardiovascular |

| Orthopedic |

| Dental |

| Respiratory |

| Drug Delivery |

| Diabetes Care |

| Ophthalmic |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Product Design And Development Services | |

| Product Testing And Sterilization Services | ||

| Regulatory Consulting Services | ||

| Contract Manufacturing Services | ||

| Product Upgrade Services | ||

| Product Maintenance Services | ||

| Logistics And Aftermarket Services | ||

| By Device Class | Class I Medical Devices | |

| Class II Medical Devices | ||

| Class III Medical Devices | ||

| By Device Type | Consumables | |

| Capital Equipment | ||

| Implantable Devices | ||

| In Vitro Diagnostics Devices | ||

| Wearable Medical Devices | ||

| By Application | Cardiovascular | |

| Orthopedic | ||

| Dental | ||

| Respiratory | ||

| Drug Delivery | ||

| Diabetes Care | ||

| Ophthalmic | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in medical device outsourcing?

Growth is being driven by OEM efforts to reduce fixed manufacturing costs, shorten time to market, and access validated cleanroom, sterilization, and precision assembly capacity without building it internally.

How large is the medical device outsourcing space by 2031?

The medical device outsourcing market is forecast to reach USD 273.38 billion by 2031 from USD 148.64 billion in 2026, with a CAGR of 12.96% over the forecast period.

Which service category leads outsourced revenue?

Contract manufacturing leads with a 55.13% revenue share in 2025 because capital-intensive production remains the most widely outsourced activity.

Which device class is growing fastest through 2031?

Class III devices are growing fastest at a 14.55% CAGR, reflecting stronger demand for specialist support in implantable and life-sustaining products.

Which application area is expanding the quickest?

Diabetes care is projected to grow at a 14.45% CAGR through 2031 due to stronger outsourcing demand for CGM systems, insulin patch pumps, and connected delivery platforms.

Which region is currently strongest and which one is growing fastest?

North America leads with 39.56% share in 2025, while Asia-Pacific is the fastest-growing region with a projected 15.12% CAGR through 2031.

Page last updated on: