Medical Affairs Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

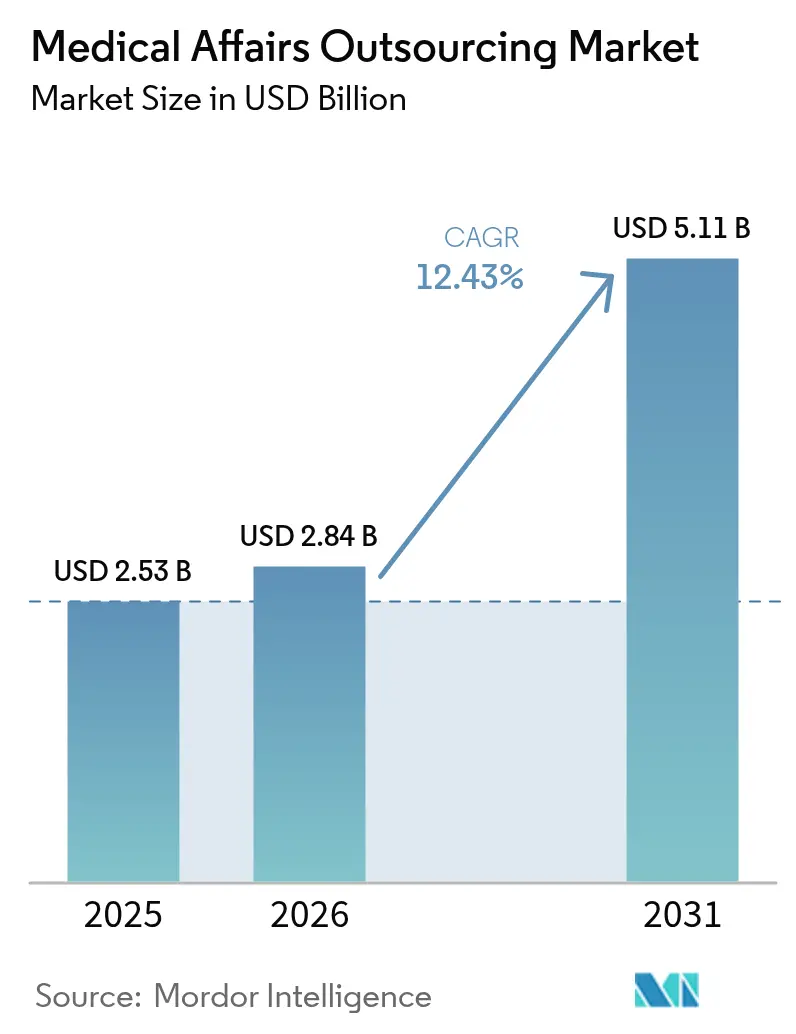

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 5.11 Billion |

| Growth Rate (2026 - 2031) | 12.43% CAGR |

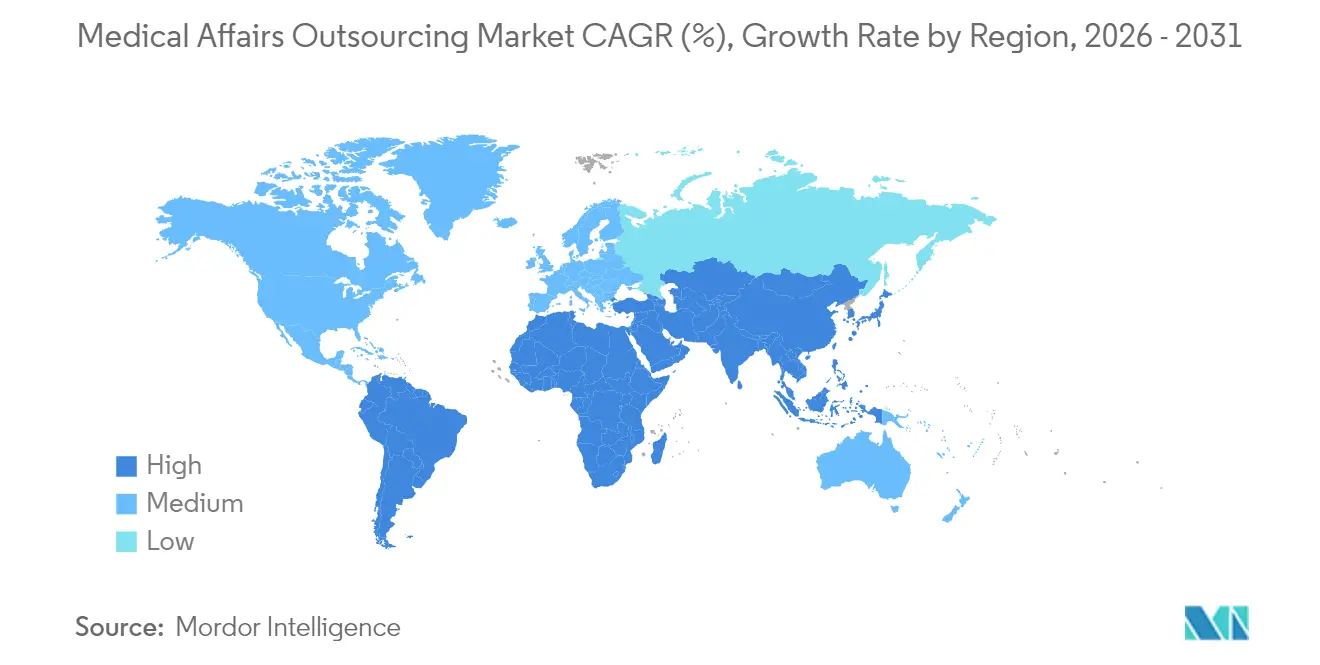

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Affairs Outsourcing Market Analysis by Mordor Intelligence

The medical affairs outsourcing market size is expected to grow from USD 2.53 billion in 2025 to USD 2.84 billion in 2026 and is forecast to reach USD 5.11 billion by 2031 at 12.43% CAGR over 2026-2031. Robust demand reflects life-science companies’ decision to focus internal resources on discovery while sourcing regulatory writing, field engagement, and compliance expertise externally. Integrated generative-AI platforms are accelerating document preparation; AstraZeneca already uses large-language-model assistants to support its goal of launching 20 new medicines by 2030. Rising volumes of biologics and specialty-drug trials, ongoing EU MDR surveillance duties, and wider adoption of hybrid and decentralized clinical-trial designs reinforce the preference for flexible, specialist partners. Consolidation among contract development and manufacturing organizations (CDMOs) is adding scale benefits, while regional service hubs in Asia Pacific are winning share through cost and speed advantages.

Key Report Takeaways

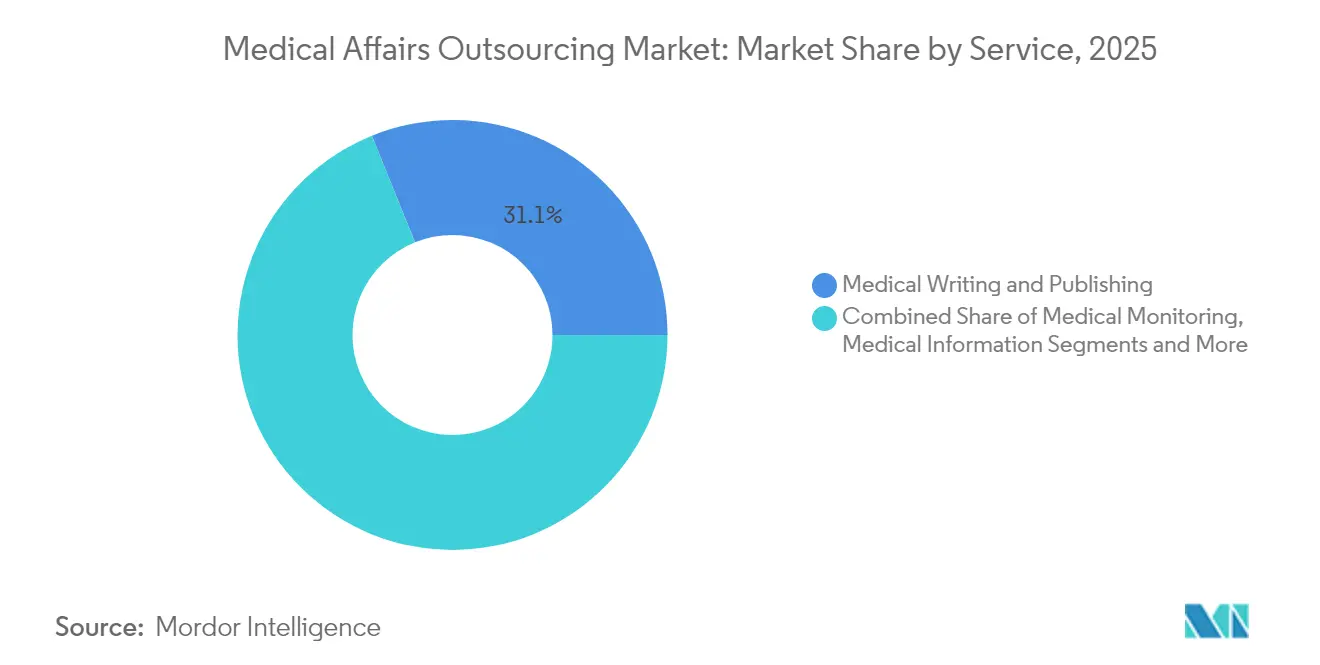

- By service, Medical Writing & Publishing led with 31.12% of the medical affairs outsourcing market share in 2025; Medical Science Liaisons (MSLs) are projected to expand at a 14.45% CAGR to 2031.

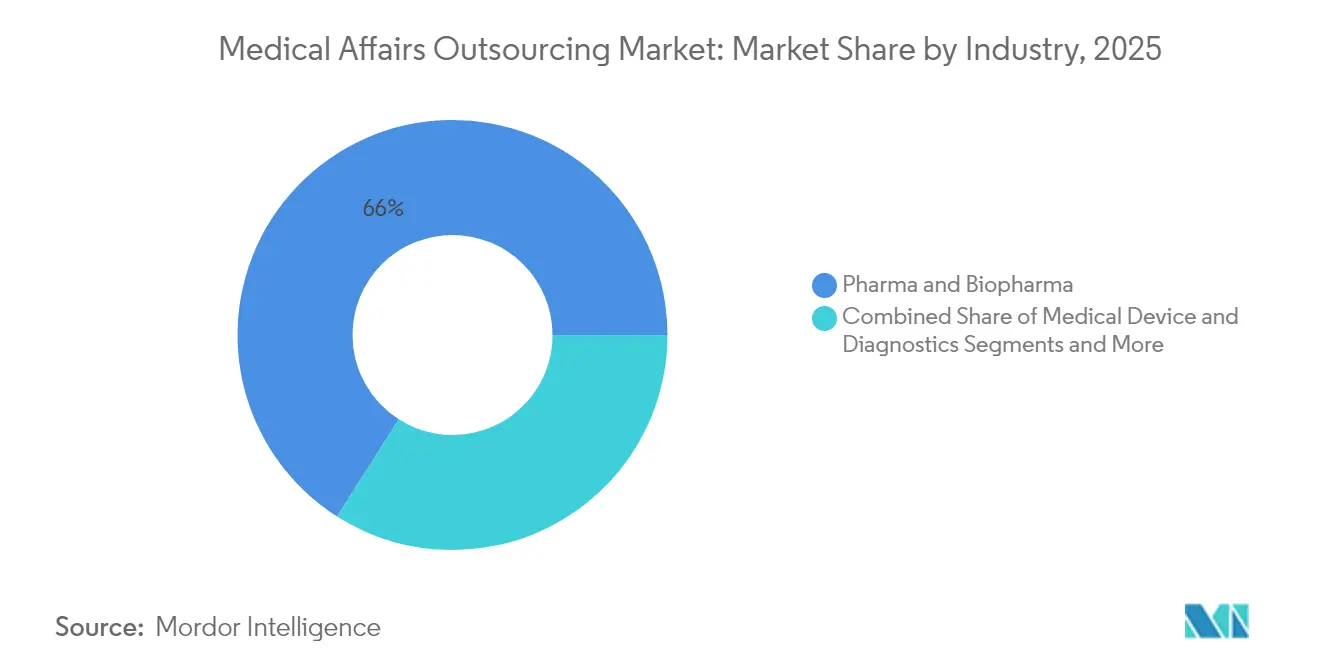

- By industry, pharmaceutical and biopharma companies controlled 65.98% of 2025 revenue, whereas emerging biotech is advancing fastest at a 15.05% CAGR through 2031.

- By geography, North America held 39.55% of 2025 revenue; Asia Pacific is forecast to record the highest regional CAGR at 14.82% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Affairs Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-efficiency & quality advantages of CROs | +2.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising clinical-trial volume & R&D spend | +2.1% | Global, concentrated in Asia Pacific emerging markets | Long term (≥ 4 years) |

| Pharma focus on core competencies | +1.9% | North America and EU primary, expanding into Asia Pacific | Medium term (2-4 years) |

| Expansion of biologics & specialty drugs | +1.7% | Global, with Asia Pacific manufacturing hubs gaining prominence | Long term (≥ 4 years) |

| GenAI-enabled scale-up of medical-writing productivity | +1.4% | North America and EU early adoption, global rollout | Short term (≤ 2 years) |

| EU-MDR post-market surveillance needs in medtech | +1.0% | Europe primary, spill-over to other regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-efficiency & quality advantages of CROs

Specialist contract research organizations pool infrastructure and therapeutic-area expertise across multiple sponsors, allowing clients to convert fixed overhead into variable spending and redirect capital toward pipeline priorities. The resulting flexibility supports virtual biotech and mid-tier pharma models that lack scale for full internal teams. Quality advantages flow from dedicated regulatory and therapeutic specialists who remain current with evolving agency expectations, reducing rework risk and audit findings.

Rising clinical-trial volume & R&D spend

Biologic, cell, and gene-therapy pipelines are expanding, each requiring complex trial designs and geographic diversity that favor experienced global partners. China and India are capturing an increasing share of multicenter studies thanks to sizeable patient pools and supportive regulatory reforms. CROs are adding remote-monitoring platforms and patient-engagement apps to manage decentralized protocols effectively.

Pharma focus on core competencies drives outsourcing

Large sponsors concentrate resources on molecule discovery, strategic portfolio decisions, and high-value scientific work. Non-core yet mandatory tasks—regulatory dossiers, safety updates, and field-medical engagement—transition to specialist vendors with proven compliance track records. The shift improves time-to-submission metrics and mitigates fixed-cost exposure during late-stage attrition.

Expansion of biologics & specialty drugs

Post-approval safety-monitoring, real-world-evidence generation, and payor-value dossiers for monoclonal antibodies and gene therapies demand niche knowledge. CDMOs with in-house medical-affairs units support end-to-end programs from manufacturing through launch, illustrated by Thermo Fisher’s earlier PPD purchase that integrated clinical research with biologics production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage & turnover of skilled talent | -1.8% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Cross-border data-privacy complexity | -1.2% | EU-US primary, spreading to Asia Pacific | Medium term (2-4 years) |

| Regulatory uncertainty over AI content | -0.9% | Global, with differing regional adoption speeds | Short term (≤ 2 years) |

| Vendor consolidation limiting supplier choice | -0.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage & turnover of skilled medical-affairs talent

The life-science workforce is ageing, and new graduates with both scientific depth and compliance knowledge remain scarce. Turnover among Medical Science Liaisons and safety physicians stretches project timelines and inflates bill rates. Large vendors invest in internal academies and AI-powered knowledge bases to attract and retain staff, yet demand still exceeds supply.

Cross-border data-privacy / compliance complexity

EU-US transfers rely on evolving mechanisms under GDPR, while Germany imposes additional restrictions on health-data cloud processing. Sponsors may choose regionalized document-authoring centers and pseudonymization layers, increasing operational duplication and eroding some cost advantages that originally drove outsourcing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Leadership of Medical Writing & Publishing with Rapid MSL Growth

Medical Writing & Publishing captured 31.12% of 2025 revenue, making it the largest slice of the medical affairs outsourcing market. High-volume clinical-study reports, risk-management plans, and structured benefit-risk templates anchor consistent demand. Generative-AI text engines reduce drafting time, yet skilled writers remain crucial for data interpretation and regulatory positioning. The segment’s scale also benefits from mandated EU MDR reports and US FDA periodic submissions.

Medical Science Liaisons generated the fastest expansion, advancing at a 14.45% CAGR to 2031. Growth reflects sponsor emphasis on scientific exchange with healthcare professionals and the need for real-world-evidence insights post-launch. Digital engagement tools allow smaller MSL teams to cover wider territories, yet therapeutic-area depth keeps head-count requirements high. Medical Information, Market Access & HEOR, and Digital/Omnichannel services round out the portfolio, each growing as pricing pressures and omnichannel outreach mature.

By Industry: Pharma Dominance Amid Accelerating Emerging-Biotech Demand

Pharmaceutical and biopharma enterprises delivered 65.98% of total 2025 spending in the medical affairs outsourcing market thanks to established operating budgets and global launch pipelines. Their multiyear framework agreements foster integrated programming across writing, safety, and stakeholder engagement, enabling knowledge continuity.

Emerging biotech shows the most rapid advance with a 15.05% CAGR through 2031 as asset-light start-ups rely on external expertise from pre-IND through commercialization. Medical device and diagnostic companies outsource safety updates and EU MDR documentation, while consumer health and nutraceutical brands engage providers for evidence packages supporting product claims. These adjacent sectors diversify vendor revenue streams and help smooth demand cycles.

Geography Analysis

North America held 39.55% of global 2025 revenue, supported by the largest concentration of R&D budgets, FDA-aligned regulatory timelines, and a mature ecosystem of full-service CROs. Policy initiatives encouraging AI use in drug development further reinforce the region’s appetite for advanced knowledge services. Canada’s bilingual workforce and Mexico’s near-shore cost advantages complement US capacity, creating a resilient regional hub.

Asia Pacific is forecast to generate the highest growth at a 14.82% CAGR. China and India supply expansive patient pools and competitive costs for clinical operations, while Japan, South Korea, and Australia contribute high-quality regulatory and data-analytics capabilities. Harmonization projects such as ASEAN CTPG reduce submission variance, accelerating multi-country trials. Regional governments also invest in digital-health sandboxes, enticing vendors to base data-science teams locally.

Europe maintains a substantial share despite Brexit-related operational redraws. New device-surveillance rules under EU MDR sustain outsourcing demand for PSUR drafting and vigilance analytics. Initiatives like the European Health Data Space aim to unlock secondary-use datasets, creating longer-term opportunities for evidence-generation specialists. Eastern-European member states offer cost-efficient delivery centers, balancing higher labor costs in Germany and the Netherlands.

Competitive Landscape

The medical affairs outsourcing market remains moderately fragmented, yet top-tier players deepen scale through targeted deals. Novo Holdings’ USD 16.5 billion Catalent acquisition adds fill-finish and gene-therapy capacity, positioning the combined group as an end-to-end partner from manufacturing through post-market medical communications. IQVIA leverages a data-analytics backbone to integrate safety, writing, and field-medical programs, reporting USD 3.83 billion in Q1 2025 revenue with strength in technology solutions.

Syneos Health’s appointment of a new CEO signals renewed focus on operational efficiency and client retention. Parexel’s multi-year agreement with Palantir halves data-delivery timelines in complex trials, underscoring the strategic value of AI-led platforms.[3]Parexel Newsroom Team, “Parexel and Palantir Expand Collaboration to Accelerate Clinical Development,” Parexel Newsroom, newsroom.parexel.com Niche innovators such as Envision Pharma’s 4Sight suite aggregate literature analytics, insight management, and omnichannel planning into unified dashboards, challenging incumbents on speed and transparency.

Strategic priorities center on generating differentiated evidence packages for high-cost therapies, scaling omnichannel HCP engagement, and embedding governance for AI-authored content. Talent acquisition remains a battleground; vendors court experienced MSLs and safety physicians with hybrid work models and upskilling pathways. White-space opportunities persist in digital therapeutics, companion-diagnostic support, and sustainability reporting, areas where few providers yet claim mature offerings.

Medical Affairs Outsourcing Industry Leaders

ICON plc

IQVIA Holdings, Inc.

Syneos Health, Inc.

Thermo Fischer Scientific Inc.

Parexel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Simplify Healthcare and Atento launched a pilot-first customer-experience program for US payers, using the Xperience1 platform to enhance member and provider engagement.

- June 2025: hellocare.ai began collaborating with Mayo Clinic on ambient clinical-intelligence solutions targeting reduced hospitalizations.

- April 2025: HeartBeam and AccurKardia partnered to broaden access to ambulatory ECG monitoring with AI-enabled analytics.

Global Medical Affairs Outsourcing Market Report Scope

As per the scope of the report, medical affairs outsourcing refers to a process that enables patients, healthcare professionals, and government bodies to gain deep insights into healthcare policies, operations, and patient data. The Medical Affairs Outsourcing Market is Segmented By Services (Medical Monitoring, Medical Writing & Publishing, Medical Information, Medical Science Liaisons, and Others), Industry (Medical Devices and Pharma and biopharmaceuticals), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report offers the market size and forecasts in value (USD million) for the above segments. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD million) for the above segments.

| Medical Monitoring |

| Medical Writing & Publishing |

| Medical Information |

| Medical Science Liaisons (MSLs) |

| Market Access & HEOR Support |

| Digital / Omnichannel Medical Affairs |

| Other Niche Services |

| Pharma & Biopharma |

| Medical Device & Diagnostics |

| Emerging Biotech |

| Consumer Health & Nutraceuticals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Medical Monitoring | |

| Medical Writing & Publishing | ||

| Medical Information | ||

| Medical Science Liaisons (MSLs) | ||

| Market Access & HEOR Support | ||

| Digital / Omnichannel Medical Affairs | ||

| Other Niche Services | ||

| By Industry | Pharma & Biopharma | |

| Medical Device & Diagnostics | ||

| Emerging Biotech | ||

| Consumer Health & Nutraceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical affairs outsourcing market?

The market is valued at USD 2.84 billion in 2026.

What annual growth rate will the medical affairs outsourcing market register through 2031?

The forecast calls for a 12.43% CAGR, lifting revenue to USD 5.11 billion by 2031.

Which service segment holds the largest share of market revenue?

Medical Writing & Publishing leads with 31.12% of 2025 revenue, driven by regulatory-document volume and scientific-communication needs.

Which region will grow the fastest over 2026-2031?

Asia Pacific is projected to expand at a 14.82% CAGR, supported by rising clinical-trial activity and regulatory harmonization.

What is the most significant restraint affecting market expansion?

A global shortage and high turnover of skilled medical-affairs talent, estimated at a 35% deficit by 2030, is exerting a −1.8% drag on forecast CAGR.

How is generative AI influencing medical affairs outsourcing demand?

GenAI tools shorten document-preparation cycles and add an estimated +1.4% to CAGR by boosting medical-writing productivity and freeing experts for higher-value analysis.

Page last updated on: