Medical Device Testing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

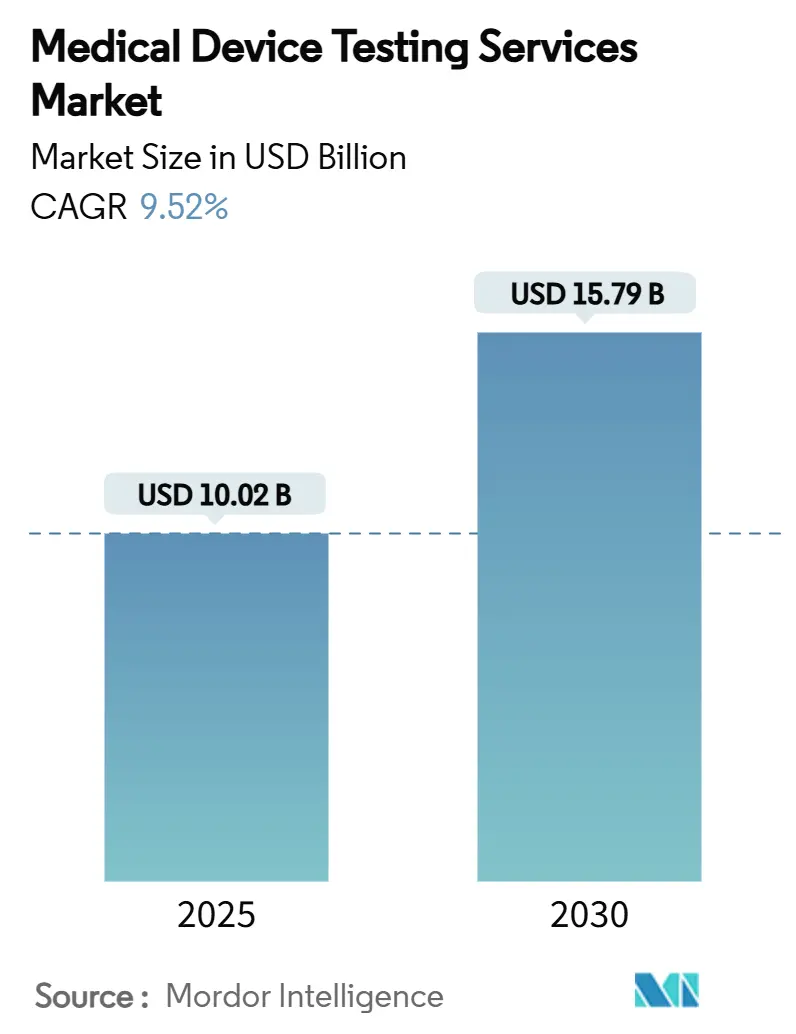

| Market Size (2025) | USD 10.02 Billion |

| Market Size (2030) | USD 15.79 Billion |

| Growth Rate (2025 - 2030) | 9.52% CAGR |

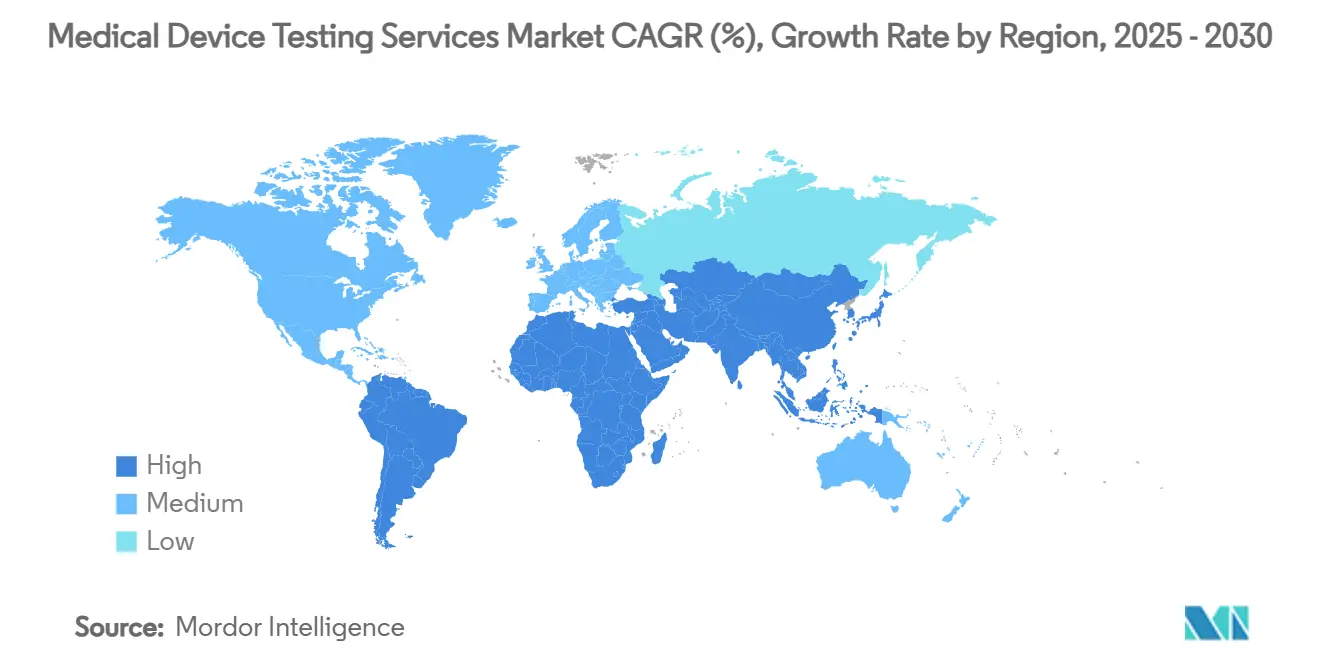

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

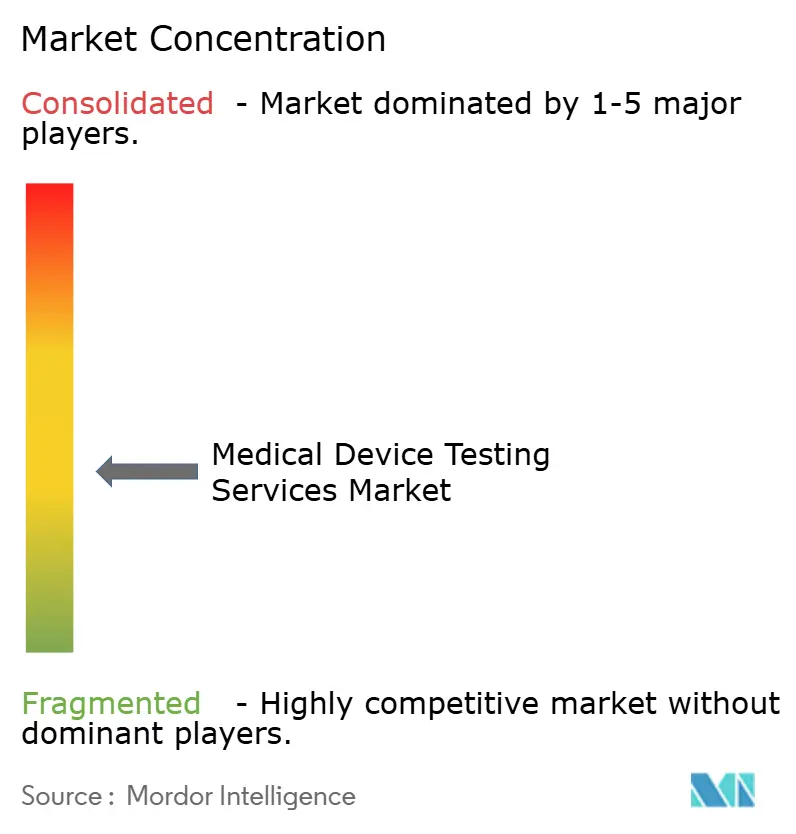

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Device Testing Services Market Analysis by Mordor Intelligence

The global medical device testing services market size reached USD 10.02 billion in 2025 and is projected to climb to USD 15.79 billion by 2030, reflecting a 9.52% CAGR during the forecast window. Intensifying global regulation—most visibly the FDA's cybersecurity mandates and the European Union's Medical Device Regulation—pushes manufacturers to external partners that already maintain accredited facilities, cross-disciplinary talent, and continuously updated quality systems.[1]Medical Device Coordination Group, "MDCG 2021-25 Rev.1," European Commission, ec.europa.eu Demand also benefits from the surge in AI-enabled implantables and connected wearables that must clear electrical immunity, software lifecycle, and biocompatibility hurdles in one integrated dossier. Shorter product refresh cycles compress validation timelines, creating throughput pressures that favor scalable external labs, while Asia-Pacific's march toward ISO-aligned oversight adds fresh volume to an already active export base. Meanwhile, simulation tools begin to replace selected wet-lab protocols, trimming revenue in certain legacy segments yet rewarding providers that blend in-silico and bench expertise for complete lifecycle support.

Key Report Takeaways

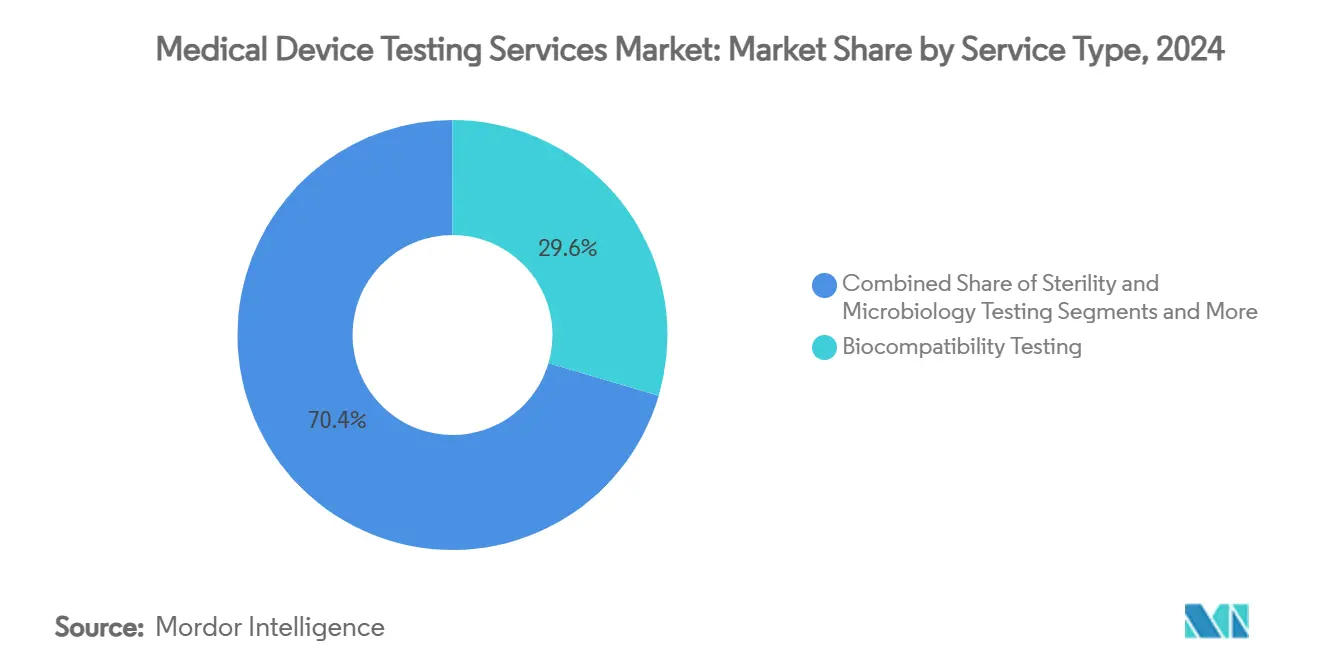

- By service type, biocompatibility testing held 29.56% of medical device testing services market share in 2024, whereas electrical safety and EMC testing is forecast to post the fastest 13.44% CAGR through 2030.

- By development phase, pre-clinical protocols accounted for 44.56% of medical device testing services market size in 2024, while post-market surveillance testing will advance at a 12.78% CAGR to 2030.

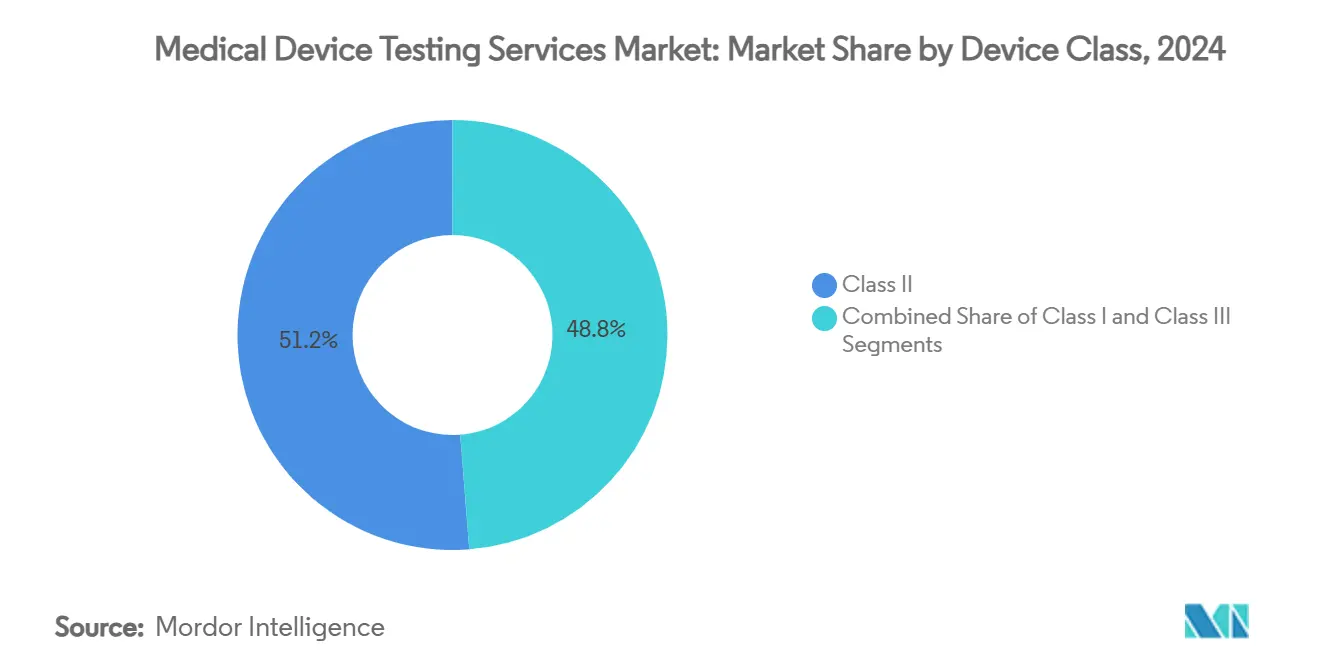

- By device class, Class II devices represented 51.24% of global testing demand in 2024, and Class III device testing is set to grow at a 13.77% CAGR through 2030.

- By end user, medical device OEMs generated 56.73% of total demand in 2024, whereas contract research organizations are forecast to expand at an 11.83% CAGR to 2030.

- North America retained 36.58% revenue share in 2024, yet Asia-Pacific will post the strongest 12.04% CAGR through the forecast period.

Global Medical Device Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global regulatory requirements accelerating outsourced testing | +2.1% | North America & EU | Medium term (2–4 years) |

| Rapid growth of complex implantables & wearables | +1.8% | North America & Asia-Pacific | Long term (≥ 4 years) |

| Expanding chronic-disease patient pool boosting device volumes | +1.6% | Global | Long term (≥ 4 years) |

| Shrinking product life-cycles creating testing throughput pressure | +1.4% | Global | Short term (≤ 2 years) |

| EU-MDR post-market surveillance rules driving real-world performance testing | +1.2% | EU | Medium term (2–4 years) |

| Cybersecurity & AI-algorithm validation for software-as-medical-device | +1.1% | North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Regulatory Requirements Accelerating Outsourced Testing

Regulation has never been as rigorous or multifaceted, and few in-house teams can maintain the equipment, talent and documentation controls now expected. The FDA’s March 2024 cybersecurity update obliges every connected device to submit detailed secure-development artifacts, vulnerability assessments and risk-control matrices, expanding test scope beyond legacy electro-mechanical checks.[2]Center for Devices and Radiological Health, “Select Updates for the Premarket Cybersecurity Guidance,” Food and Drug Administration, fda.govConcurrently, the EU-MDR lengthened legacy-product transition periods to 2028 but imposed real-world evidence obligations and stricter notified-body oversight, stretching manufacturer resources. Because accredited third-party laboratories already comply with ISO 17025 and maintain specialized benches, sponsors shift spend toward the medical device testing services market to keep launches on schedule. Providers that pair regulatory intelligence with integrated quality-management systems become pivotal partners, turning compliance complexity into a sustained revenue engine.

Rapid Growth of Complex Implantables & Wearables

Multifunction devices weave sensors, AI and wireless modules into miniature form factors that demand simultaneous biocompatibility, EMC and software validation. The FDA now instructs AI-enabled diagnostic sponsors to prove algorithm performance across sex, ethnicity and comorbidity strata before clearance. Meanwhile, IEC 60601-1-2 revision 4 mandates distinct immunity levels for professional, home and special environments, forcing elaborate shielding and coexistence tests on wearables and implantables. Developing that infrastructure internally is capital-prohibitive, so OEMs route programs to external experts, reinforcing growth in the medical device testing services market.

Expanding Chronic-Disease Patient Pool Boosting Device Volumes

Aging demographics and lifestyle-related illnesses elevate device consumption worldwide. Asia-Pacific medical-technology spending alone is forecast at USD 225 billion by 2030, mirroring hospital build-outs, insurance expansion and physician adoption of minimally invasive procedures. Rising volumes translate directly into more batch, lot and change-control validations, giving accredited labs an expanding funnel. Harmonization with ISO, IEC and IMDRF standards lets multinationals leverage one dossier across multiple markets, multiplying throughput at test centers and cementing the medical device testing services market as a mission-critical external competency.

Shrinking Product Life-Cycles Creating Testing Throughput Pressure

Cloud connectivity and software-as-medical-device paradigms foster quarterly, sometimes monthly, feature releases. The FDA’s predetermined change-control plan framework allows algorithm tweaks without a fresh 510(k) if preapproved validation pathways are followed, yet those pathways still require performance re-verification under production loads. Sponsors scale external benches to perform iterative cybersecurity scans, regression EMC sweeps and re-executed biocompatibility endpoints, increasing reliance on the medical device testing services market for rapid, repeatable capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cost & turnaround time for multi-modal test panels | –1.3% | Global | Short term (≤ 2 years) |

| Scarcity of ISO-17025 compliant lab capacity in emerging regions | –1.1% | Asia-Pacific & Latin America | Medium term (2–4 years) |

| FDA warnings on data-integrity forcing expensive re-tests | –0.9% | Global | Short term (≤ 2 years) |

| Adoption of in-silico simulation reducing certain wet-lab revenues | –0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cost & Turnaround Time for Multi-Modal Test Panels

Expanded guidance folds biocompatibility, chemical characterization, software security and electrical safety into one dossier, requiring additional equipment, personnel training and method validations. Aligning FDA biocompatibility policy with ISO 10993-1, while reducing animal use, still compels labs to invest in new in-vitro toxicology suites and high-content imaging systems, expenses ultimately passed to sponsors. Smaller firms face budget strain, slowing near-term uptake in parts of the medical device testing services market.

Adoption of In-Silico Simulation Reducing Certain Wet-Lab Revenues

High-fidelity computational models can replicate hemodynamics, orthopedic load paths or electrical propagation with regulatory acceptance if validated for credibility. The FDA’s endorsement of virtual trials allows sponsors to replace some bench or animal work, particularly for incremental design changes, reducing throughput in traditional labs.[3]Kenneth I. Aycock et al., “Toward Trustworthy Medical Device In-Silico Clinical Trials,” Frontiers in Medicine, frontiersin.orgLaboratories investing in simulation services can offset losses, but providers that rely heavily on commoditized wet-lab volumes face slower growth inside the medical device testing services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Biocompatibility Leads, EMC Outpaces

Biocompatibility testing retained 29.56% of the medical device testing services market share in 2024, anchoring the segment’s contribution to the overall medical device testing services market size. The service remains foundational because every implantable, invasive or prolonged-contact product must clear cytotoxicity, sensitization and irritation endpoints before regulators accept clinical data. Electrical-safety and electromagnetic-compatibility (EMC) protocols, propelled by connected hardware and IEC 60601-1-2 immunity revisions, are forecast to post a 13.44% CAGR through 2030 . Sterility and microbiology studies hold a stable slice of demand thanks to single-use disposables and orthopedic implants that require validated sterilization cycles, while analytical chemistry gains prominence as sponsors probe extractables, leachables and material interactions. Packaging and shelf-life validation is expanding as the FDA emphasizes real-time aging over accelerated extrapolation, obliging manufacturers to prove integrity across longer distribution chains.

Cybersecurity and AI-algorithm audits, still grouped under “other services,” are small in absolute dollars yet log triple-digit project counts and will become a discrete pillar of the medical device testing services market size by mid-decade. Laboratories that integrate hardware, software and data-science benches win complex contracts, displacing single-modality providers that cannot meet multi-endpoint dossiers. As connected devices proliferate, EMC houses are adding wireless coexistence chambers, while biocompatibility specialists invest in in-vitro alternatives aligned with ISO 10993-1 to curb animal use. The resulting capex raises entry barriers, reinforcing the advantages of incumbent players with global footprints. Sponsors gravitate toward labs that offer menu-based bundling, allowing them to combine biocompatibility, EMC and packaging within one quote to reduce time-to-submission. Consequently, service-mix evolution is shifting revenue toward higher-value, technology-heavy protocols even as traditional wet-bench studies continue underpinning baseline cash flow across the medical device testing services market.

By Development Phase: Pre-Clinical Dominates, Post-Market Gains

Pre-clinical validation commanded 44.56% of the medical device testing services market share in 2024, underscoring its role as the largest contributor to the medical device testing services market size. Sponsors rely on benchtop performance, biocompatibility, mechanical and chemical characterization data to support 510(k), PMA and CE-mark filings, generating predictable laboratory throughput. Controlled clinical-stage testing is smaller in volume but higher in per-study revenue because it entails human-factors, pivotal safety and effectiveness assessments that require IRB oversight and sophisticated statistics.

Post-market surveillance testing, however, is projected to expand at a 12.78% CAGR through 2030, a pace that will steadily raise its share of the medical device testing services market size. EU-MDR obligates trend-reporting, periodic safety updates and corrective-action confirmation for every marketed device class, pushing manufacturers to contract external partners for real-world data analytics and follow-up bench studies. Laboratories that fuse epidemiological analysis with physical retesting secure multi-year agreements, dampening revenue cyclicality tied to new-product pipelines. The evolution from front-loaded validation to continuous lifecycle evidence reshapes staffing models, demanding statisticians and data engineers alongside traditional bench scientists. Over time, pre-clinical work will still dominate absolute dollars, but post-market programs will account for a larger slice of incremental growth in the medical device testing services market.

By Device Class: Class II Holds Sway, Class III Surges

Class II devices generated 51.24% of global testing spend in 2024, cementing their position as the largest driver of the medical device testing services market size. These moderate-risk products—including infusion pumps, surgical energy systems and imaging accessories—require special controls plus comprehensive bench and sometimes limited clinical evidence, creating steady laboratory demand. Class I items, governed mainly by general controls, maintain a modest but consistent stream of bioburden and electrical-safety work.

Class III submissions, although fewer in unit count, will expand at a 13.77% CAGR and capture a rising portion of the medical device testing services market share through 2030. Life-sustaining implantables such as ventricular assist devices or neuro-stimulators mandate exhaustive pre-clinical, large-animal, human-factors and post-market programs, producing test budgets five to ten times larger than mid-risk products. The FDA’s growing emphasis on clinical performance and combined benefit–risk assessment amplifies data requirements, driving sponsors to partner with labs that can coordinate toxicology, simulated-use, hemodynamic and algorithm-validation workstreams under a unified quality system. With venture-backed innovators pushing the envelope on bioresorbables and smart prosthetics, the Class III pipeline suggests a durable revenue catalyst for full-service providers in the medical device testing services market.

By End User: OEMs Drive Spend, CROs Accelerate

Original-equipment manufacturers (OEMs) accounted for 56.73% of 2024 revenue, making them the dominant customer group and the principal determinant of the medical device testing services market size. Their corporate quality systems and regulatory-submission obligations compel systematic outsourcing across biocompatibility, sterility, EMC and cyber assessments. Contract manufacturing organizations (CMOs) contribute a stable mid-single-digit share by funding lot-release and process-validation studies to maintain GMP compliance.

Contract research organizations (CROs) are projected to grow at an 11.83% CAGR, raising their slice of the medical device testing services market share as sponsors consolidate bench, animal and clinical services under single master agreements. CROs acquire or partner with test laboratories to offer cradle-to-commercialization packages, allowing OEMs to streamline vendor lists and accelerate timelines. Smaller OEMs, lacking internal regulatory teams, often default to CRO-managed programs that bundle toxicology, usability and regulatory writing, further boosting external spend. Academic and hospital research centers add incremental volume through investigator-initiated studies and translational projects but remain niche relative to commercial demand. As device complexity rises and global submissions multiply, end users increasingly favor full-service suppliers capable of cross-jurisdiction dossiers, sustaining robust growth prospects for outsourced providers in the medical device testing services market.

Geography Analysis

North America commanded 36.58% of global revenue in 2024, supported by rigorous FDA oversight, strong payer systems and a dense network of ISO-accredited laboratories covering every major modality of the medical device testing services market. The United States leads regulatory innovation in cybersecurity and AI, compelling sponsors to maintain domestic testing pipelines even when manufacturing sits offshore, while Charles River Laboratories, for example, posted USD 4.05 billion 2024 revenue and announced new CRADL vivarium capacity in Cambridge, Massachusetts to cater to Class III implant studies. Canada ensures market proximity through Health Canada’s alignment with IMDRF principles, and Mexico leverages maquiladora production hubs that require local lot-release testing, feeding cross-border lab traffic.

Europe remains the second-largest region, with extended MDR transition periods keeping thousands of legacy devices in queue for conformity assessment, driving sustained utilization of TÜV SÜD, BSI and DEKRA facilities. TÜV SÜD reported revenue above EUR 3 billion in 2024 and continues splitting capital between extra German benches and expanding US and Asia-Pacific satellites, reflecting demand for integrated, globalized test suites. Germany leads on volume, but the United Kingdom and France remain premium centers for usability, human-factors and digital-health validation. Southern European nations, while smaller, offer cost-effective chemical and microbiology capacity, absorbing overflow from saturated core markets within the medical device testing services market.

Asia-Pacific is forecast to post a 12.04% CAGR, outpacing every other geography. China’s State Administration for Market Regulation modernized device classification catalogues and bolstered local clinical-evaluation guidance, boosting domestic lab investments, while multinationals still run pivotal trials abroad to meet FDA or EU endpoints. Japan sustains high technology demand through PMDA’s fast-track review for breakthrough devices, yet often requires duplicate biocompatibility data, adding to test volumes. India’s Medical Device Rules 2024 extended mandatory licensing to previously unregulated categories, stimulating local demand but sending high-risk dossiers to Singapore or Europe due to capacity gaps. South Korea and Australia advance harmonization with IMDRF, yet rely on regional partners for Class III hemodynamic modeling or electromagnetic exposures. Middle East, Africa and South America show rising import substitution programs that necessitate in-country lot testing, but the lack of widespread ISO-17025 infrastructure keeps complex validations anchored to established players in the broader medical device testing services market.

Competitive Landscape

The medical device testing services market is moderately consolidated. Eurofins Scientific logged EUR 5.142 billion for the first nine months of 2024 and acquired Infinity Laboratories to extend microbiology and sterilization strengths across the United States. SGS deepened its North American footprint by purchasing Applied Technical Services for USD 1.325 billion in July 2025, instantly adding aerospace-grade fatigue benches and expanding its regulated-market client base. Intertek focuses on connected devices, recently unveiling an AI-security center in California, while TÜV SÜD reinforces digital-health certification programs spanning Europe, Asia and the United States.

Strategic acquisitions show no sign of slowing. Applus+ bought Keystone Compliance in November 2024, securing EMC and environmental chambers tailormade for military-grade durability testing, which it now cross-sells into medical throw-shock and vibration studies. NAMSA’s alliance with Terumo epitomizes end-to-end outsourcing, bundling toxicology, clinical monitoring and regulatory writing under master-service frameworks that streamline portfolio management for large sponsors. Specialty providers—Nelson Labs in microbiology, Element in materials and WuXi AppTec in China-FDA dual filings—leverage deep domain knowledge to defend margins despite megacorp scale advantages.

Technology is the new differentiator. Market leaders invest heavily in robotics-assisted sample prep, artificial-intelligence result interpretation and encrypted cloud portals that feed dashboards directly to sponsor quality-systems. Laboratories that automate traceability and integrate digital twin simulations cut cycle times and win premium pricing, while laggards risk relegation to commoditized, low-margin bioburden counts. This competitive dynamic stimulates continual capex and acquisition activity, shaping the innovation trajectory of the medical device testing services market.

Medical Device Testing Services Industry Leaders

-

Eurofins Scientific

-

SGS SA

-

Intertek Group plc

-

TÜV SÜD AG

-

WuXi AppTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SGS agreed to acquire Applied Technical Services for USD 1.325 billion, creating a North American testing and inspection platform with annual sales surpassing USD 1.5 billion.

- November 2024: Applus+ bought Keystone Compliance, adding EMC/EMI, environmental and packaging expertise to bolster its United States footprint.

- October 2024: NAMSA and Terumo signed a strategic outsourcing partnership to accelerate regulatory approvals across Terumo’s global medical-device pipeline.

Global Medical Device Testing Services Market Report Scope

| Biocompatibility Testing |

| Sterility & Microbiology Testing |

| Material Characterization & Analytical Chemistry |

| Electrical Safety & EMC Testing |

| Packaging & Shelf-life Testing |

| Others |

| Pre-clinical |

| Clinical |

| Post-Market / PMS |

| Class I |

| Class II |

| Class III |

| Medical Device OEMs |

| Contract Manufacturing Organizations (CMOs) |

| Contract Research Organizations (CROs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Biocompatibility Testing | |

| Sterility & Microbiology Testing | ||

| Material Characterization & Analytical Chemistry | ||

| Electrical Safety & EMC Testing | ||

| Packaging & Shelf-life Testing | ||

| Others | ||

| By Development Phase | Pre-clinical | |

| Clinical | ||

| Post-Market / PMS | ||

| By Device Class | Class I | |

| Class II | ||

| Class III | ||

| By End User | Medical Device OEMs | |

| Contract Manufacturing Organizations (CMOs) | ||

| Contract Research Organizations (CROs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the projected growth rate of the medical device testing services market?

The medical device testing services market is expected to expand at a 9.52% CAGR from 2025 to 2030, growing from USD 10.02 billion to USD 15.79 billion.

2. Which testing service will experience the fastest growth?

Electrical safety and electromagnetic-compatibility testing will rise at a 13.44% CAGR, propelled by connected-device proliferation and updated IEC immunity standards.

3. Why is post-market surveillance testing gaining importance?

EU-MDR and comparable regulations require manufacturers to gather real-world performance data throughout a product’s lifecycle, elevating demand for continuous validation and analytics services.

4. Which region is forecast to grow the quickest?

Asia-Pacific is set for a 12.04% CAGR thanks to expanding manufacturing bases, regulatory harmonization and rising healthcare investment.

Page last updated on: