Medical Device Reprocessing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.87 Billion |

| Market Size (2031) | USD 11.97 Billion |

| Growth Rate (2026 - 2031) | 15.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Reprocessing Market Analysis by Mordor Intelligence

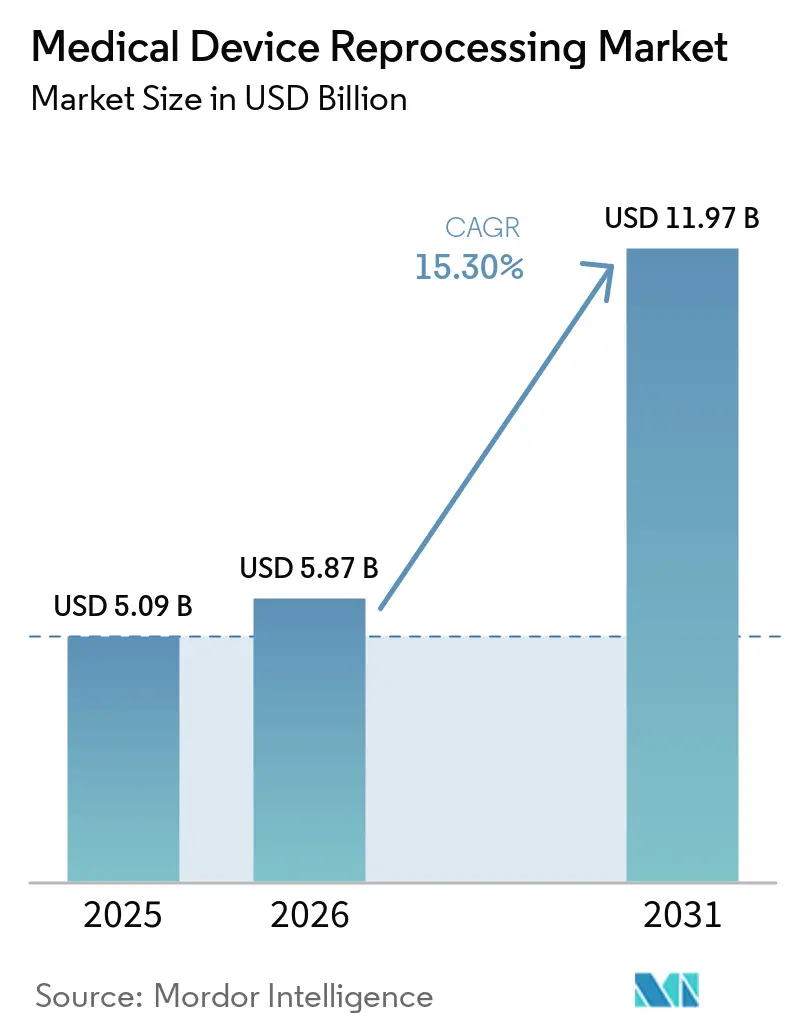

The Medical Device Reprocessing Market size is expected to grow from USD 5.09 billion in 2025 to USD 5.87 billion in 2026 and is forecast to reach USD 11.97 billion by 2031 at 15.30% CAGR over 2026-2031.

Hospital cost pressures are driving the growth of the medical device reprocessing market, as reprocessed devices offer 30% to 50% per-unit savings compared to OEM list prices. In 2025, AMDR members documented hospital savings of USD 495.5 million through the sale of 39,387,336 reprocessed single-use devices across 11,458 facilities in 18 countries.[1]Association of Medical Device Reprocessors, “Hospitals Saved Nearly $500 Million and Eliminated More Than 39,000 Tons of Emissions By Using Reprocessed SUDs From AMDR Members in 2025,” AMDR, amdr.org These savings have elevated reprocessing from a sustainability initiative to a key component of multi-year hospital budgets. Sustainability reporting, carbon scoring in supplier evaluations, and improved digital tracking of trays and cycles are driving adoption by reducing environmental impact and compliance challenges. Competitive activity is intensifying as major service providers expand capacity and software capabilities, although uncertainties in sterilization permitting present short-term operational risks.

Key Report Takeaways

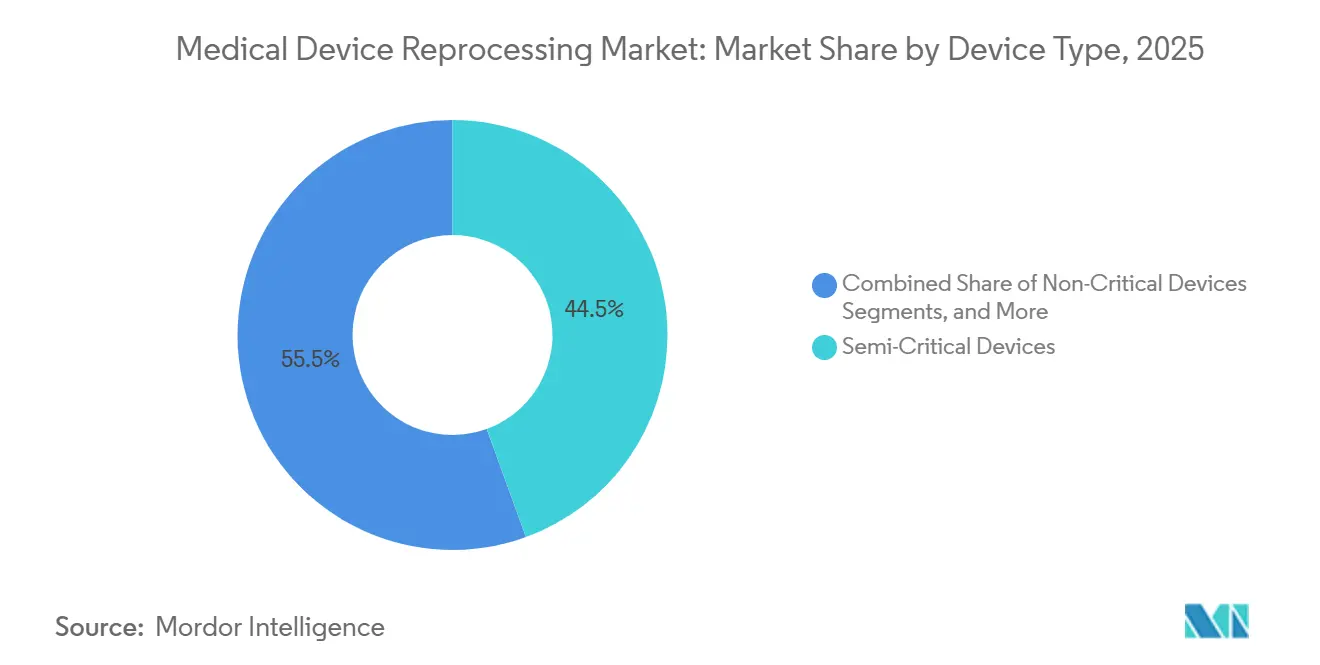

- By device type, semi-critical devices held 44.45% share in 2025, while critical devices recorded the fastest projected CAGR at 16.45% through 2031.

- By offering type, reprocessed medical devices accounted for 62.55% share in 2025, while reprocessing support and services are projected to grow at 16.77% CAGR through 2031.

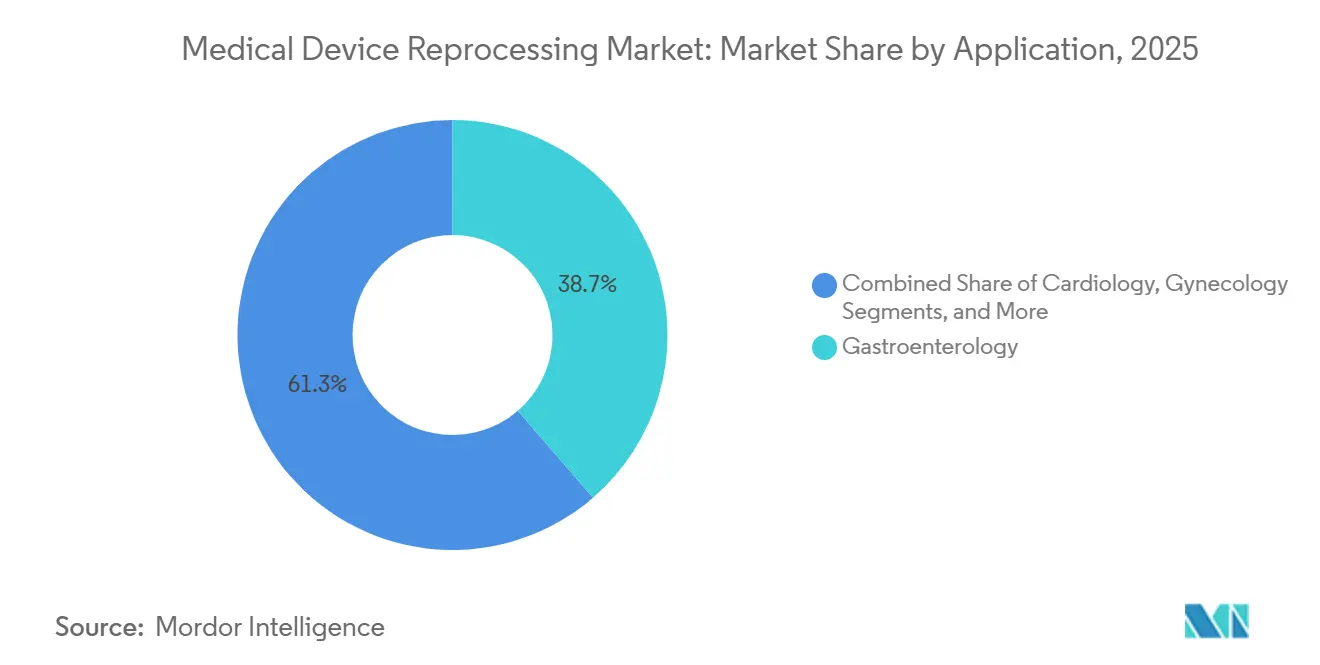

- By application, gastroenterology held 38.65% share in 2025, while cardiology is projected to expand at 17.23% CAGR through 2031.

- By end user, hospitals accounted for 55.03% share in 2025, while ambulatory surgical centers are projected to grow at 17.35% CAGR through 2031.

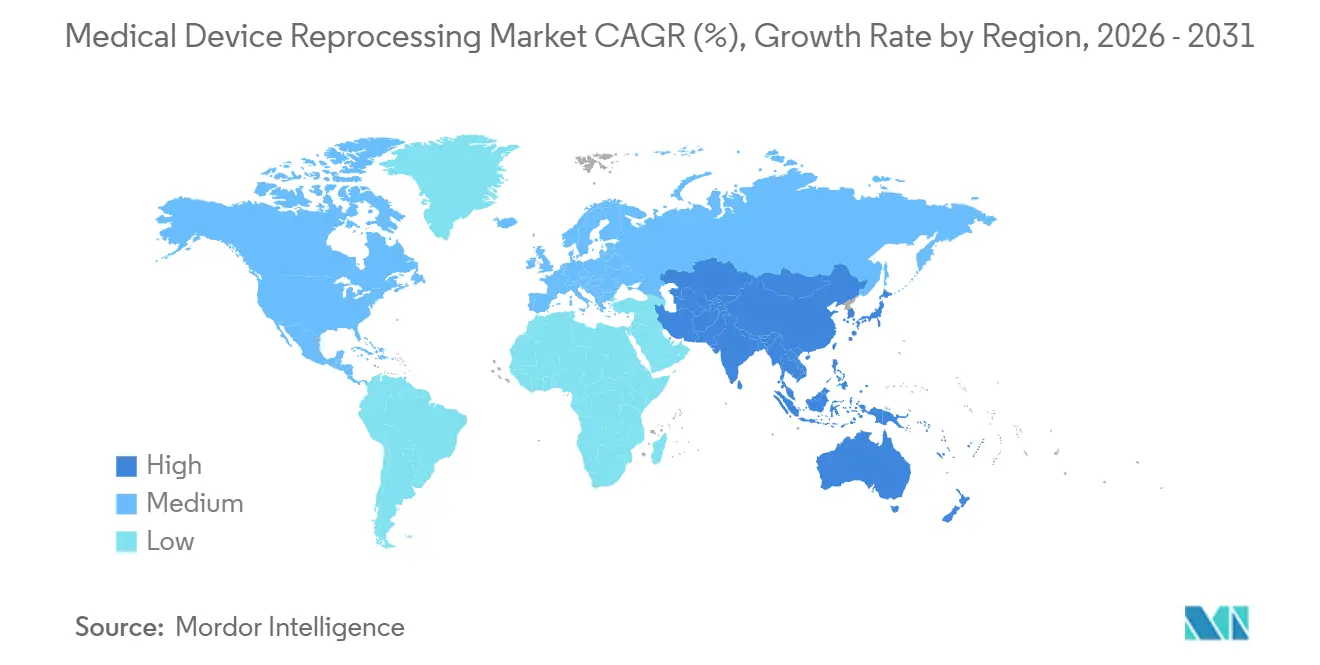

- By geography, North America held 42.99% of the medical device reprocessing market share in 2025, while Asia-Pacific is projected to expand at 15.96% CAGR, marking the fastest rise in medical device reprocessing market size through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device Reprocessing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hospital supply cost containment and recurring per-procedure savings | +4.2% | Global, with core gains in North America and Western Europe | Short term (≤ 2 years) |

| Sustainability reporting pressure on health systems | +2.3% | EU, North America, Australia | Medium term (2-4 years) |

| Expanded oem reprocessed-device portfolios | +2.8% | Global, with early-mover concentration in North America | Medium term (2-4 years) |

| Heterogeneous reprocessing rules across key markets | +1.5% | EU, APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Ai-enabled tray and cycle tracking improves compliance | +1.9% | North America and EU, with APAC adoption accelerating | Medium term (2-4 years) |

| Ethylene oxide capacity, emissions, and permitting constraints slow supply | +0.8% | North America, EU, spill-over to APAC sterilization hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hospital Supply Cost Containment and Recurring Per-Procedure Savings

In 2025, AMDR member companies sold 39,387,336 reprocessed single-use devices to 11,458 healthcare facilities across 18 countries, generating USD 495.5 million in documented savings for hospitals. AMDR highlighted that if all US hospitals reprocessed at the rate of the top 10% of adopters, the annual savings opportunity could reach USD 2.43 billion. This gap emphasizes the increasing focus on the medical device reprocessing market within major health systems, where purchasing decisions are evaluated against operating margins, liquidity, and supply efficiency. Financial stakes are also evident in the Veterans Health Administration debate, where AMDR estimated that current restrictions left USD 167 million in annual taxpayer savings unrealized in 2025. With device-level savings often reaching 40 to 60% against OEM list prices, the medical device reprocessing market aligns well with procurement strategies prioritizing repeatable savings at the procedure level.

Sustainability Reporting Pressure on Health Systems

Sustainability goals are becoming a key factor in the medical device reprocessing market as hospital systems face increasing pressure to demonstrate progress on Scope 3 emissions. Reprocessed devices are identified as a rare supply-chain action that reduces both costs and emissions, offering procurement teams a clear strategy to balance cost and climate objectives. In fiscal 2025, Cardinal Health's Sustainable Technologies business collected 21.6 million single-use devices, diverting 6.6 million pounds of waste from landfills, and avoiding 1,900 metric tons of carbon dioxide equivalent emissions. European policy movements further support this trend, with Denmark authorizing commercial single-use device reprocessing in January 2025 and France initiating a hospital reprocessing experiment in September 2025. Procurement rules increasingly recognize environmental performance as integral to supplier value in the medical device reprocessing market.

AI-Enabled Tray and Cycle Tracking Improves Compliance

Digital traceability is addressing a major operational challenge in the medical device reprocessing market: the effort required to document every cycle, tray, and device history. CensisAI² reported a 20% reduction in missing instrument spend by generating real-time tray validation records, meeting Joint Commission audit requirements in hospitals. AI-driven surgical instrument recognition can nearly eliminate unnecessary tray reopening rates in central sterile settings, reducing chemical use and energy consumption per cycle. The FDA's Quality Management System Regulation, effective February 2, 2026, aligns oversight more closely with ISO 13485:2016, increasing the importance of validated digital tracking in compliance-heavy environments.[2]U.S. Food and Drug Administration, “Remanufacturing and Servicing Medical Devices,” FDA, fda.gov Hospitals seeking fewer manual steps and stronger audit readiness benefit from software tools that make compliance a measurable operational function.

Expanded OEM Reprocessed-Device Portfolios

The medical device reprocessing market is expanding as manufacturers transition older product generations out of premium portfolios, broadening device eligibility. This shift allows more devices to enter approved reprocessing channels without waiting for extensive regulatory resets in individual countries. In 2025, Stryker's Sustainable Solutions program served nearly 3,500 US hospitals, including almost all institutions listed in U.S. News & World Report's "Best Hospitals," indicating that reprocessing has become a mainstream practice. The acceptance of reprocessed devices is no longer limited to low-acuity categories, with growing adoption of electrophysiology catheters and laparoscopic instruments. This evolution reduces reliance on sporadic approvals and emphasizes the need to expand the device universe across high-value clinical areas.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| OEM contracting tactics and device lock-in | -2.1% | Global, with highest intensity in North America for high-acuity device categories | Medium term (2-4 years) |

| Clinical trust barriers for reprocessed high-acuity devices | -1.5% | APAC, MEA, South America, residual impact in EU for critical-class devices | Medium term (2-4 years) |

| Limited device eligibility and validation burden | -1.2% | EU, APAC, with improving trajectory in North America | Long term (≥ 4 years) |

| Sterilization capacity constraints and capital intensity | -0.8% | North America, EU, emerging pressure in APAC sterilization hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM Contracting Tactics and Device Lock-In

OEM contracting practices continue to limit the medical device reprocessing market, particularly in high-value categories influenced by proprietary systems. In May 2025, a jury ruled against Johnson & Johnson's Biosense Webster unit, and a permanent injunction in September 2025 prohibited actions such as linking clinical support to new device purchases, disabling reprocessed devices with embedded chips, and withholding used devices essential for reprocessing. The damages totaled USD 442 million after being tripled, highlighting the commercial significance of the issue. However, softer resistance persists, including software lockouts, reduced staff training, and restrictive contract structures that hinder hospital transitions. Federal agencies addressed the issue in 2025 by launching an anonymous reporting portal for anticompetitive practices in the medical device sector. While access has improved in some product categories, inconsistent procurement freedom continues to slow progress in other areas.

Clinical Trust Barriers for Reprocessed High-Acuity Devices

Trust in reprocessed medical devices, especially those used in high-acuity procedures, remains uneven. A 2025 systematic review found no increased safety risks for reprocessed cardiac catheterization devices, but limited randomized trial data led to low confidence in the findings. Procurement committees often hesitate despite clear cost advantages when clinical evidence is narrow. A 2024 European Commission document highlighted acceptance challenges for critical-class device reprocessing across EU nations and called for stronger surveillance frameworks.[3]Health Care Without Harm Europe, “Reprocessing, a Vital Component for a Greener Healthcare System in the EU, Focus on Denmark,” Health Care Without Harm Europe, europe.noharm.org Categories with the highest savings potential face the strongest resistance, and without robust post-market evidence, adoption in critical areas will likely remain slow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Critical Devices Lead the Next Growth Wave

In 2025, Semi-Critical Devices dominated the medical device reprocessing market, accounting for 44.45% of the segment's revenue. This stronghold is attributed to established reprocessing pathways for items like flexible endoscopes and respiratory therapy circuits. Many hospital sterile supply departments have standardized high-level disinfection protocols for these devices. Clinicians are more accepting of these categories due to hospitals' extensive operating experience and clear handling routines. Non-Critical Devices, which include electrodes and pulse oximeter sensors, made up the remaining share. While reprocessing is accepted for these items, the savings per unit are smaller due to their lower original acquisition costs.

Critical Devices are set to experience a robust growth rate of 16.45% CAGR through 2031, making them the fastest-growing category in the medical device reprocessing market. This surge is linked to the growing acceptance of reprocessed electrophysiology catheters and laparoscopic instruments in the U.S., alongside an expansion of eligibility under EU MDR frameworks in Europe. Furthermore, a September 2025 injunction against Biosense Webster has eased access conditions in a previously constrained device class. While Semi-Critical Devices currently dominate the market share, the trend indicates a shift in value creation towards critical devices. This shift is bolstered by the advent of digital audit trails and validation systems, simplifying complex reprocessing programs for clinical and regulatory reviews.

By Offering Type: Reprocessing Support and Services Capture Premium Economics

In 2025, Reprocessed Medical Devices made up 62.55% of the offering-type revenue, underscoring the market's reliance on physical device throughput over service-only contracts. High demand in fields like gastroenterology and cardiology drives this segment, as hospitals frequently replace these items and can directly measure savings. This dynamic fosters a consistent procurement rhythm across extensive hospital networks. It also highlights that buyers typically enter the market through specific device categories before branching out into broader partnerships.

Reprocessing Support and Services is on track to grow at a robust 16.77% CAGR through 2031, positioning it as the more dynamic segment of the medical device reprocessing market. Major health systems are increasingly seeking integrated solutions, desiring collection logistics, validation support, and tracking software as a cohesive program rather than standalone purchases. Cardinal Health exemplified this trend in 2026, merging ValueLink analytics with its Sustainable Technologies offering to enhance supply-chain efficiency for large health systems. A 2025 life cycle study emphasized collection logistics and sterilization design as key areas for environmental enhancement, bolstering the case for service-led differentiation. As price competition tightens device margins, operators demonstrating savings, compliance, and environmental performance as a bundled service stand to capture more value in the market.

By Application: Cardiology Breaks Through Historically Restricted Territory

Gastroenterology, accounting for 38.65% of application revenue in 2025, emerged as the focal point of the medical device reprocessing market. This prominence stems from the bustling procedural flow in GI endoscopy suites and established reuse pathways for devices like gastrointestinal scopes and biopsy forceps. Orthopedics also carved out a significant presence, with tools and components yielding substantial savings in high-volume joint and sports medicine settings. Other specialties, including gynecology and urology, contributed to a diverse demand, ensuring the market's breadth.

Cardiology is poised for a robust growth trajectory, with a forecasted 17.23% CAGR through 2031, marking it as the fastest-expanding application in the medical device reprocessing market. The momentum surged post a 2025 antitrust ruling against Biosense Webster, which lifted a significant barrier in electrophysiology catheter reprocessing. This development is pivotal; cardiac devices, with their frequent use and high unit economics, present a lucrative revenue opportunity once commercial access is secured. It's also why niche players like Innovative Health are honing in on cardiology, rather than diversifying their portfolios. In the realm of medical device reprocessing, cardiology stands out as the application where regulatory access, litigation outcomes, and savings potential have found a harmonious alignment.

By End User: Ambulatory Surgical Centers Outpace Inpatient Growth

In 2025, hospitals led the charge in the medical device reprocessing market, accounting for 55.03% of end-user revenue. Their dominance is bolstered by advantages like multi-department device collection and a centralized sterile supply infrastructure. While specialty clinics and other end users remain smaller players, they're carving out niches in fields like ophthalmology and cardiac rhythm management. This dynamic underscores the market's heavy reliance on hospitals, even as outpatient sites gain traction.

Ambulatory Surgical Centers are set to outpace their inpatient counterparts, with a projected growth rate of 17.35% CAGR through 2031. This surge is driven by a notable shift of surgical activities from inpatient to outpatient settings, where supply costs are more transparent. Given their tighter operating structures, ASC's find reprocessed devices—offering savings of 30 to 50% per unit—particularly appealing. As private-equity-backed ASC networks consolidate, they're gravitating towards network-level purchasing contracts with major providers like Stryker and Cardinal Health. This evolution not only unveils a fresh growth avenue for the medical device reprocessing market but also underscores the heightened importance of efficient pickup, return, and documentation systems tailored for smaller outpatient sites.

Geography Analysis

In 2025, North America accounted for 42.99% of global revenue in the medical device reprocessing market, securing the largest regional share. This dominance stems from extensive commercial adoption, strong Group Purchasing Organization frameworks, and a regulatory environment holding third-party reprocessors to standards similar to original manufacturers. The US EPA's March 2026 proposal to revisit parts of the 2024 ethylene oxide rule highlighted the direct impact of sterilization policies on regional supply capacity.

Europe remains a critical regulatory hub for the medical device reprocessing market, with adoption heavily influenced by country-specific legal frameworks and hospital procurement policies. In 2025, France initiated a hospital trial for reprocessing single-use devices, including electrophysiology catheters, under Décret n° 2025-895. A public policy review in France estimated 35% to 59% savings per reprocessed device, supporting broader hospital participation if the pilot expands. Denmark's approval of commercial reprocessing for single-use devices in January 2025 signaled a shift toward sustainability-focused health systems. EU MDR Article 17 and ISO 13485:2016 continue to shape market entry, favoring operators with validated quality systems and strong documentation capabilities.

Asia-Pacific is projected to grow at a 15.96% CAGR through 2031, making it the fastest-growing region in the medical device reprocessing market. Growth is driven by rising surgical volumes, hospital infrastructure investments, and improved procurement practices in countries like China, India, South Korea, Australia, and Japan. Cardinal Health's remanufacturing facility in Beresfield, Newcastle, Australia, set for full operation in FY2027, marks a significant international expansion. While South Korea and Japan offer regulatory maturity, China and India present large-scale opportunities as compliance frameworks strengthen and hospital purchasing systems formalize.

Competitive Landscape

The medical device reprocessing market experiences moderate consolidation at the large-account level. Key players such as Stryker, Cardinal Health, and STERIS utilize extensive device portfolios, collection networks, and compliance capabilities to serve major health systems. Outside North America, the market is less concentrated, with regional specialists playing a significant role in Europe and the Asia-Pacific. This creates a market dynamic that combines scale advantages in mature regions with fragmented conditions in areas where local regulations and hospital purchasing patterns vary widely. Competitive positioning increasingly depends on service execution, traceability, and contract design rather than solely on device pricing.

Stryker's Sustainable Solutions platform, which reached nearly 3,500 US hospitals by 2025, strengthens its presence across integrated delivery networks. Cardinal Health drives market growth through operational and geographic expansion, integrating ValueLink analytics into its reprocessing program and establishing its first international remanufacturing facility in Australia. STERIS demonstrated its commitment by announcing a USD 60 million investment over two years for a new sterility assurance manufacturing plant in Mentor, Ohio, enhancing its healthcare processing infrastructure.

Growth opportunities are most prominent in cardiology, mid-market accounts in the Asia-Pacific, and ambulatory surgical centers, where procurement systems remain less developed than in hospital networks. The 2025 ruling and injunction against Biosense Webster reshaped competition, demonstrating the ability to challenge OEM resistance in high-value device categories. Smaller players like Vanguard AG, Konoike Co., Ltd., MedSalv Australia, MidWest Reprocessing Center, and NEScientific remain competitive by tailoring programs to local regulations and specialized needs.

Medical Device Reprocessing Industry Leaders

Stryker Corporation

Medline Industries, LP

Vanguard AG

Johnson & Johnson

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: STERIS plc announced a USD 60 million investment over two years to establish a sterility assurance manufacturing plant in Mentor, Ohio. This facility will consolidate US production into a single center of excellence, expected to be operational by late 2027, and expand reprocessing and sterilization capacity for healthcare clients.

- March 2026: The US EPA proposed repealing or revising the 2024 NESHAP ethylene oxide emission standards for commercial sterilization facilities, citing risks of medical supply chain disruptions. The public comment period closed on May 15, 2026.

- December 2025: Saraya has unveiled the official page for Power Quick, its dedicated brand for cleaning and maintenance agents tailored for medical devices. The new brand page highlights ARAYA's Medical Device Reprocessing System Series.

Global Medical Device Reprocessing Market Report Scope

As per the scope of the report, medical device reprocessing is the multistep process of cleaning, disinfecting, and sterilizing used medical tools. It makes instruments safe to use on patients again.

The medical device reprocessing market is segmented by device type, offering type, application, end-user, and geography. By device type, the market includes critical devices, semi-critical devices, and non-critical devices. By offering type, the market is segmented into reprocessed medical devices and reprocessing support and services. By application, the market is categorized into cardiology, gastroenterology, orthopedics, gynecology, general surgery, and other applications. By end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Critical Devices |

| Semi-Critical Devices |

| Non-Critical Devices |

| Reprocessed Medical Devices |

| Reprocessing Support and Services |

| Cardiology |

| Gastroenterology |

| Orthopedics |

| Gynecology |

| General Surgery |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Critical Devices | |

| Semi-Critical Devices | ||

| Non-Critical Devices | ||

| By Offering Type | Reprocessed Medical Devices | |

| Reprocessing Support and Services | ||

| By Application | Cardiology | |

| Gastroenterology | ||

| Orthopedics | ||

| Gynecology | ||

| General Surgery | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medical device reprocessing market?

The medical device reprocessing market was valued at USD 5.87 billion in 2026 and is forecast to reach USD 11.97 billion by 2031 at a CAGR of 15.30%.

Which region leads revenue generation for reprocessed medical devices?

North America led with 42.99% of global revenue in 2025, supported by mature hospital contracting structures and a clear regulatory path.

Which application area is expanding the fastest in this space?

Cardiology is the fastest-growing application, with a projected CAGR of 17.23% through 2031, helped by broader access to reprocessed electrophysiology catheters.

Why are hospitals increasing adoption of reprocessed devices?

Hospitals are using reprocessed devices more often because they can save 30 to 50% per unit, and AMDR members documented USD 495.5 million in hospital savings in 2025.

Which end user group is creating the strongest growth opportunity?

Ambulatory Surgical Centers are growing the fastest at 17.35% CAGR through 2031 because supply costs are highly visible in outpatient procedure economics.

What are the main barriers slowing wider adoption?

OEM lock-in strategies, uneven clinician trust in high-acuity categories, validation burden, and sterilization capacity constraints continue to slow adoption in some device classes and regions.

Page last updated on: