US Biotechnology And Pharmaceutical Services Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

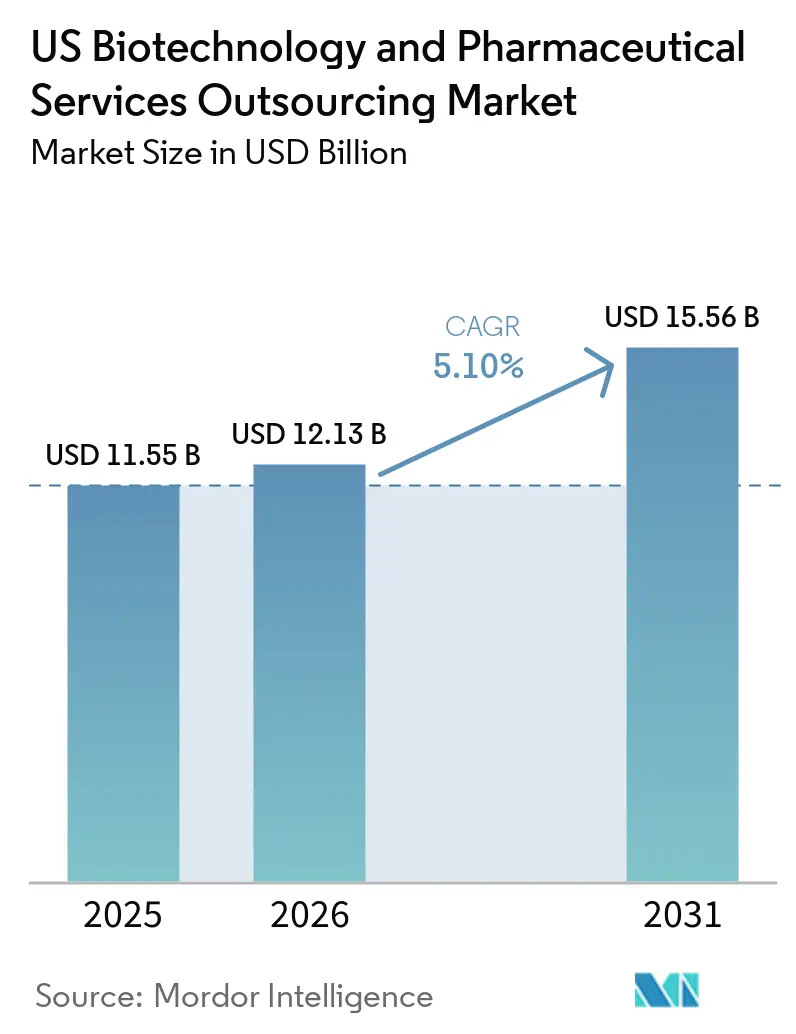

| Base Year Market Size (2025) | USD 11.55 Billion |

| Market Size (2026) | USD 12.13 Billion |

| Market Size (2031) | USD 15.56 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Biotechnology And Pharmaceutical Services Outsourcing Market Analysis by Mordor Intelligence

The US Biotechnology And Pharmaceutical Services Outsourcing Market size is expected to increase from USD 11.55 billion in 2025 to USD 12.13 billion in 2026 and reach USD 15.56 billion by 2031, growing at a CAGR of 5.10% over 2026-2031.

Biopharmaceutical sponsors are increasingly outsourcing manufacturing, development, and clinical execution while focusing internal budgets on commercialization, portfolio management, and asset acquisition. In 2024, global clinical trial starts reached 5,318, returning to pre-pandemic activity levels and driving demand for CRO and CDMO services.[1]IQVIA Institute for Human Data Science, “Global Trends in R&D 2025, Signs of Higher Efficiency and Productivity,” IQVIA, iqvia.com United States biotech funding remained strong in 2025, with 256 financing rounds raising USD 18.5 billion, supporting sponsors reliant on outsourced infrastructure and operational support.[2]IQVIA Institute for Human Data Science, “Global Trends in R&D 2025, Signs of Higher Efficiency and Productivity,” IQVIA, iqvia.com The highest demand stems from biologics, cell therapies, gene therapies, and other complex programs requiring specialized GMP systems, advanced analytics, and experienced clinical teams, which many sponsors lack internally. Providers with comprehensive development, manufacturing, regulatory, and data capabilities are gaining a competitive edge as sponsors aim to reduce vendor overlap and enhance execution speed.

Key Report Takeaways

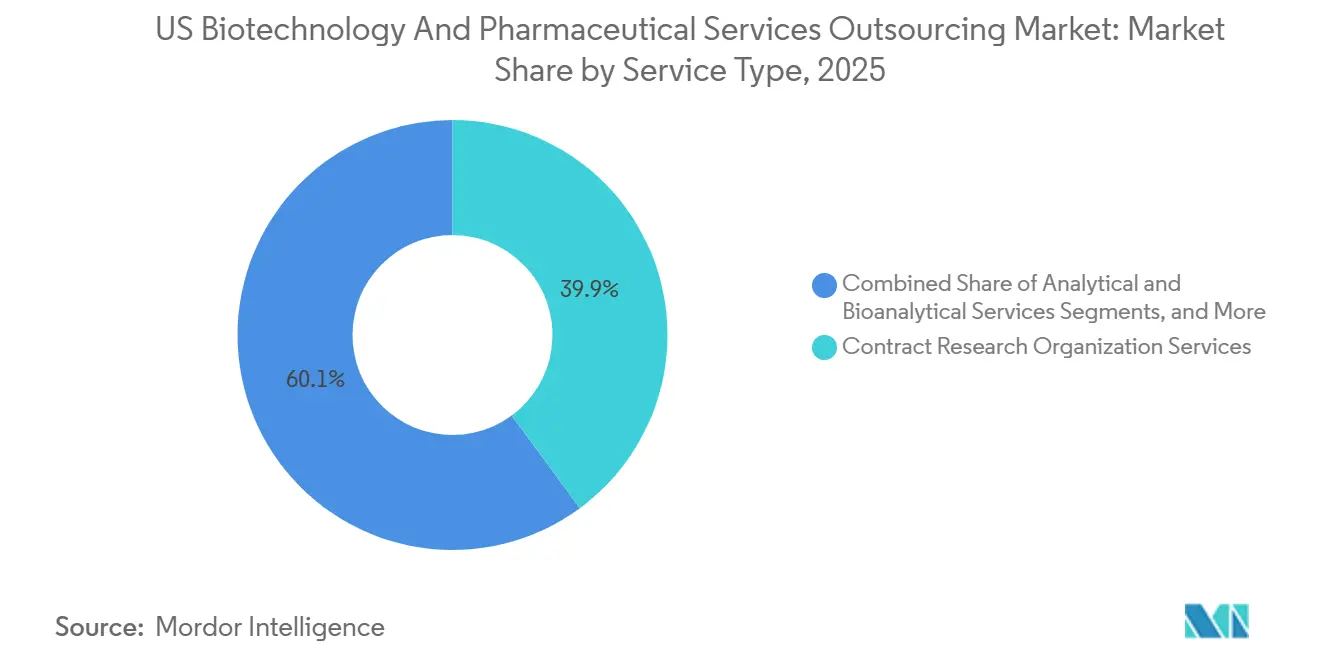

- By service type, contract research organization services held 39.88% of the US biotechnology and pharmaceutical services outsourcing market share in 2025, while contract development and manufacturing organization services are projected to grow at a 7.45% CAGR through 2031.

- By drug type, small molecules accounted for 42.35% of revenue in 2025, while cell and gene therapies are forecasted to expand at an 8.88% CAGR through 2031.

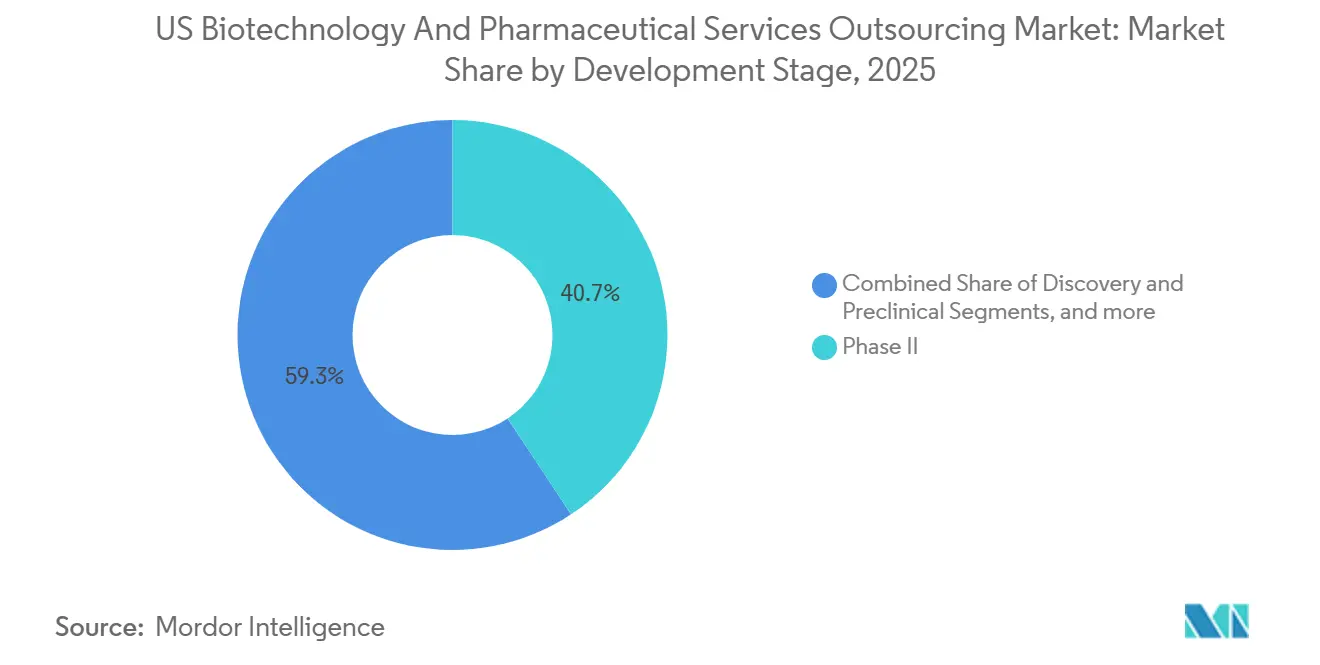

- By development stage, phase II represented 40.67% of the US biotechnology and pharmaceutical services outsourcing market size in 2025, while discovery and preclinical services are projected to record a 7.52% CAGR through 2031.

- By end user, pharmaceutical companies contributed 51.34% of revenue in 2025, while biotechnology companies are expected to grow at a 6.9% CAGR through 2031.

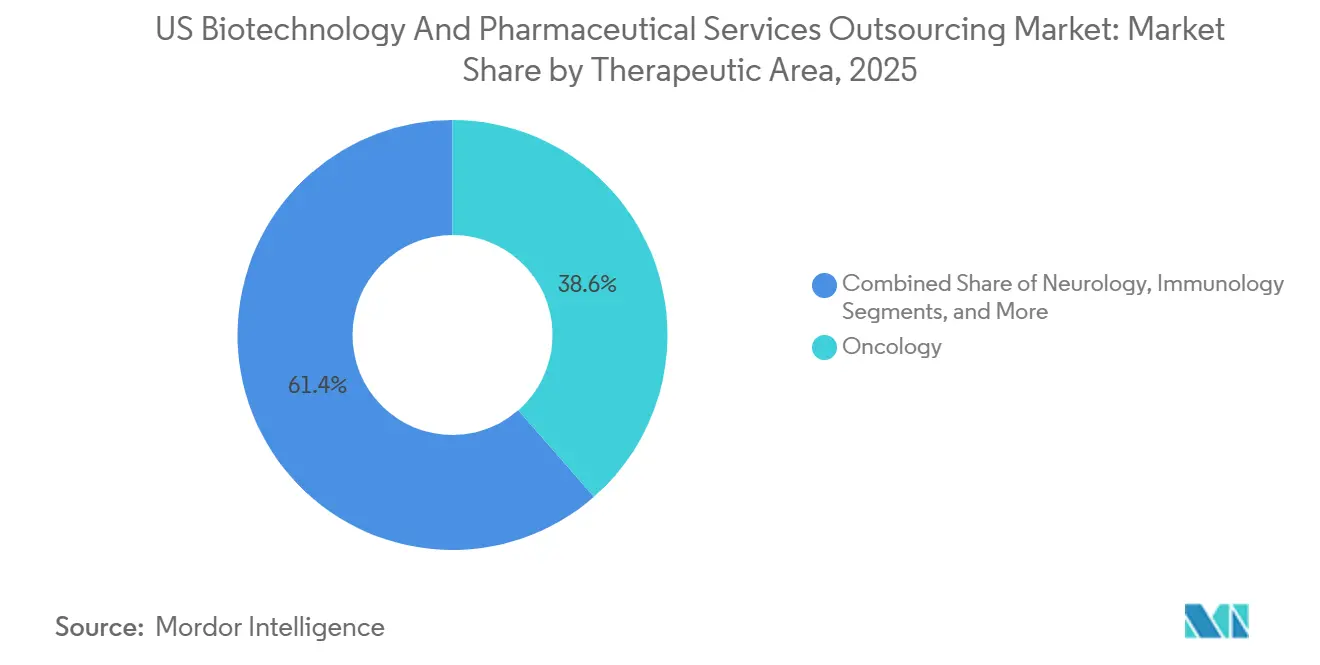

- By therapeutic area, oncology accounted for 38.55% of revenue in 2025, while neurology is forecasted to advance at a 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Biotechnology And Pharmaceutical Services Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising complexity of biologics, cell and gene therapy pipelines | +1.7% | National, concentrated in Northeast and Bay Area biotech hubs | Short term (≤ 2 years) |

| Sponsor push for fixed-cost, variable-capacity operating models | +1.0% | National | Medium term (2-4 years) |

| Demand for integrated end-to-end development and manufacturing partners | +1.2% | National, early gains in Boston, Research Triangle, and San Francisco clusters | Medium term (2-4 years) |

| Reshoring and North American supply chain risk diversification | +0.9% | National | Short term (≤ 2 years) |

| Data-heavy clinical operations favor scalable US-based technology platforms | +0.7% | National | Medium term (2-4 years) |

| Faster protocol design and enrollment support for complex trials | +0.5% | National, early gains in NC, NJ, and MA trial corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Complexity of Biologics, Cell and Gene Therapy Pipelines

The shift towards biologics, cell therapies, and gene therapies is the primary demand driver in the United States biotechnology and pharmaceutical services outsourcing market. These programs require specialized GMP suites, modality-specific analytical methods, complex cold-chain processes, and regulatory expertise that are challenging to develop quickly. In 2024, oncology, immunology, neurology, and cardiovascular programs accounted for 71% of the 5,318 clinical trial starts, reflecting the focus on complex areas.[3]US Food and Drug Administration, “Conducting Clinical Trials With Decentralized Elements,” FDA, fda.gov Novel oncology modalities, including cell and gene therapies, antibody-drug conjugates, and multispecific antibodies, represented 35% of oncology trials, increasing demand for CDMOs with advanced capabilities. Autologous CAR-T programs involve multiple specialized tasks, spreading work across various vendors, which drives higher outsourcing volumes, program costs, and longer provider relationships.

Demand for Integrated End-to-End Development and Manufacturing Partners

Sponsors in the United States biotechnology and pharmaceutical services outsourcing market are reducing the number of outsourcing partners per program, favoring providers that manage end-to-end processes from development to regulatory submission. Integrated CDMO and CRO models have been shown to accelerate timelines, with adoption by over 120 biotechs across 350-plus protocols. This trend is concentrating revenue among providers with broader capabilities, while smaller specialists form partnerships to expand service offerings. Procurement teams prioritize speed and fewer handoffs, giving integrated platforms pricing leverage and stronger sponsor relationships.

Reshoring and North American Supply Chain Risk Diversification

Supply chain reconfiguration is driving demand in the United States biotechnology and pharmaceutical services outsourcing market. The BIOSECURE Act, enacted in December 2025, restricts U.S. agencies and contractors from working with certain Chinese biotechnology providers, redirecting work to U.S. and allied-nation providers.[4]Morrison Foerster, “BIOSECURE Act Update,” Morrison Foerster, mofo.com This shift is tightening domestic GMP manufacturing capacity, particularly for viral vectors, plasmid DNA, and lipid nanoparticles. Providers with compliant U.S. facilities and available capacity are well-positioned to absorb this demand, though the transition will take time as existing agreements conclude.

Data-Heavy Clinical Operations Favor Scalable US-Based Technology Platforms

Clinical operations in the United States biotechnology and pharmaceutical services outsourcing market are increasingly data-intensive, especially in mid- and late-stage trials. Wearables, electronic patient-reported outcomes, decentralized trial components, and real-world data are shaping Phase II and III program designs. The FDA’s 2024 guidance on decentralized trials and the finalized ICH E6(R3) in 2025 emphasize risk-based quality management and scalable digital systems. U.S.-based platforms with advanced tools and automated workflows are becoming essential, enabling larger providers to secure higher-value contracts, while weaker platforms face competitive pressure.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sponsor concentration risk and vendor consolidation | -0.8% | National | Medium term (2-4 years) |

| Regulatory and quality compliance burden across multi-site programs | -0.6% | National | Short term (≤ 2 years) |

| Capacity bottlenecks in specialized modalities and GMP suites | -0.4% | National, most pronounced in NJ-PA corridor and Research Triangle | Medium term (2-4 years) |

| Margin pressure from bid competition and pricing compression | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sponsor Concentration Risk and Vendor Consolidation

In the United States biotechnology and pharmaceutical services outsourcing market, vendor consolidation among major sponsors is limiting growth opportunities. Many leading pharmaceutical firms now work with a select few preferred CROs and CDMOs across service categories. While this approach streamlines oversight and cost management, it exposes providers to significant revenue risks if they lose a preferred status. Mid-tier companies face added pressure as they often invest in quality systems, staffing, and facilities before securing contracts. Smaller biotech clients provide some balance, but their demand fluctuates with financing and portfolio changes, making revenue quality sensitive to client concentration and renewal cycles.

Capacity Bottlenecks in Specialized Modalities and GMP Suites

Capacity limitations in specialized manufacturing remain a challenge in the United States biotechnology and pharmaceutical services outsourcing market. High-demand areas like viral vector production, sterile fill-finish for biologics, and HPAPI synthesis face tight supply. Establishing an aseptic fill-finish line requires USD 150 million to USD 200 million and 3 to 4 years for validation, slowing supply response to rising demand. With only 12 United States plants offering SafeBridge-certified HPAPI containment at a commercial scale, supply is concentrated among a few operators. Cambrex's planned USD 120 million HPAPI expansion in Iowa by March 2025 will take time to reach full capacity, prompting sponsors in advanced therapy programs to book capacity well in advance, reducing outsourcing efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: CRO Services Lead While CDMOs Gain Ground Through Integration

In 2025, Contract Research Organization (CRO) services dominated the US biotechnology and pharmaceutical services outsourcing market, accounting for 39.88% of the revenue. This dominance is largely attributed to ongoing Phase II to Phase IV activities in oncology and neurology, fields where trial execution is both data-intensive and operationally intricate. CROs are broadening their scope, moving beyond traditional monitoring and site management to include protocol design support, patient recruitment analytics, pharmacovigilance, and integrated quality oversight. This evolution is driving up average contract values, as sponsors opt for comprehensive execution packages over standalone services. The market is increasingly favoring providers that seamlessly blend clinical operations with robust regulatory and technological backing.

Services in Regulatory Affairs and Quality Assurance are thriving, thanks to heightened oversight standards across multi-site programs. Sponsors are increasingly seeking assistance in managing quality systems across vendors. As trial designs become richer in biomarkers, the demand for Analytical and Bioanalytical services is surging, especially in oncology. Pharmacovigilance and Drug Safety services are transitioning to automated models, with providers channeling investments into rapid signal detection and expansive case-processing tools. While Packaging, Labeling, and Serialization services remain niche, their significance is paramount in advanced therapy programs, where maintaining chain-of-custody control is critical.

By Drug Type: Small Molecules Anchor Revenue as Advanced Therapies Reshape Mix

In 2025, small molecules constituted 42.35% of the revenue, solidifying their position as the leading drug-type segment in the US biotechnology and pharmaceutical services outsourcing market. Their stronghold is bolstered by a pipeline teeming with new chemical entities and high-potency compounds. Outsourcing is already prevalent in API synthesis and oral solid dose manufacturing, particularly for programs involving controlled substances or stringent containment needs. Consequently, future growth in this segment is anticipated to stem more from an improved mix rather than a significant shift in outsourcing rates. The rising contract values, driven by higher-potency compounds and intricate synthesis routes, are evident even without a proportional increase in program counts.

Cell and gene therapies are emerging as the fastest-growing drug type, with an anticipated 8.88% CAGR through 2031 in the US biotechnology and pharmaceutical services outsourcing market. Their ascent is fueled by increasing IND activity and the scarcity of sponsors possessing in-house capabilities for vector, plasmid, cell-processing, and release-testing. Novel oncology modalities, encompassing cell and gene therapies, antibody-drug conjugates, and multispecific antibodies, now represent 35% of oncology trials, sustaining a heightened demand for specialized manufacturing and analytical support.

By Development Stage: Phase II as the Revenue Center, Early Stages Accelerating

Phase II, accounting for 40.67% of the market size in 2025, emerged as the primary revenue generator across development stages. This stage demands substantial investment, as sponsors seek proof-of-concept data, precise patient targeting, biomarker support, and adaptive protocols. With oncology and neurology programs heavily represented, the complexity of site coordination and data management surpasses that of simpler historical designs. Factors like adaptive designs, interim analyses, decentralized elements, and specialty endpoints are amplifying the outsourced workload per study. Consequently, mid-stage trials are driving a significant portion of CRO revenue, even prior to advancing to larger Phase III programs.

Discovery and Preclinical services are on track to grow at a 7.52% CAGR through 2031, marking them as the fastest-growing stage in the market. This growth is a testament to improving funding conditions and the increasing movement of early assets into IND-enabling work. Phase I outsourcing is also gaining momentum, bolstered by providers expanding their early-phase infrastructure across diverse regions and therapeutic niches. For instance, in May 2026, ICON broadened its US early-phase footprint with a new Clinical Research Unit in San Antonio and outpatient clinics in Houston and Lawrence, Kansas, enhancing access for first-in-human and patient cohort studies.

By End User: Pharma Companies Anchor Revenue as Biotech Drives Forward

In 2025, pharmaceutical companies accounted for 51.34% of the revenue, solidifying their position as the primary end-user in the market. Their dominance is underscored by extensive multi-year outsourcing programs spanning clinical development, manufacturing, and commercial supply. Furthermore, large pharmaceutical firms are increasingly adopting structured partnership models, such as preferred-provider arrangements, milestone-based pricing, and integrated service teams. This evolution has transformed outsourcing from a mere transactional function to a strategic operational model for many established sponsors. Given their expansive portfolios and extended planning cycles, pharmaceutical companies continue to provide a stable revenue foundation in the market.

Biotechnology companies, projected to expand at a 6.9% CAGR through 2031, are emerging as the fastest-growing end-user segment. In 2025, US-based biotech firms secured USD 18.5 billion across 256 financing rounds, bolstering a dynamic group of smaller sponsors with limited in-house development and manufacturing capabilities. These biotech entities typically outsource a staggering 80% to 90% of their program expenditures, given their lack of full GMP or clinical operations teams.

By Therapeutic Area: Oncology Dominates as Neurology Gains Strategic Depth

In 2025, oncology commanded 38.55% of the revenue, establishing itself as the leading therapeutic segment in the market. This aligns with oncology's sustained prominence in trial activities and its heightened operational demands. Factors such as patient recruitment, biomarker analysis, companion diagnostics, and protocol intricacies elevate the outsourced expenditure for oncology programs. Supporting this trend, IQVIA highlighted that oncology constituted 38% of all industry-sponsored trial initiations from Phase I to III in 2025. The market's close ties to oncology are evident, given the therapy area's ability to generate both substantial program volumes and intensified service demands.

Neurology is poised for growth, with projections indicating a 6.56% CAGR through 2031. This expansion is driven by intensified clinical investments in areas like neurodegeneration, CNS rare diseases, and psychiatric disorders. Over the past five years leading up to 2024, conditions such as Alzheimer’s, depression, and Parkinson’s each saw upwards of 200 new trial initiations. Concurrently, diseases like ALS, multiple sclerosis, and muscular dystrophy are witnessing a surge in early-stage activities.

Geography Analysis

The United States biotechnology and pharmaceutical services outsourcing market is concentrated in key biopharma corridors. Greater Boston and Cambridge dominate as East Coast hubs for preclinical CRO activities and early-phase CDMO partnerships, driven by dense biotech activity, academic hospitals, and translational research infrastructure. New Jersey and Pennsylvania serve as the mid-Atlantic manufacturing belt, benefiting from strong talent pools, legacy production infrastructure, and proximity to major sponsor headquarters. These factors create a corridor structure where sponsor density and service provider maturity heavily influence outsourcing decisions.

The San Francisco Bay Area leads as the West Coast hub for biotech innovation, fueling pre-IND and Phase I demand within local CRO and laboratory networks. In 2024, Lonza completed the integration of Roche's Vacaville biologics site, valued at USD 1.2 billion, making it part of the largest contract mammalian biologics network in the United States with 332,000 liters of bioreactor capacity across 10 buildings. Texas is also emerging as a key operational base, with sponsors seeking patient access and early-phase infrastructure beyond traditional coastal hubs. ICON’s 2026 expansion into San Antonio, Houston, and Lawrence reflects this shift toward the South and Midwest.

North Carolina’s Research Triangle Park is gaining prominence in late-stage and commercial manufacturing, particularly in cell therapy and complex biologic programs. In April 2026, Kincell Bio announced the addition of two ISO 7 cleanroom suites to its RTP facility, targeting full operational readiness by Q3 2026. The Midwest is also becoming significant, with cities like Chicago, Indianapolis, Cincinnati, and Madison offering lower facility and labor costs, enabling providers to expand manufacturing and research capacity while staying close to large patient populations. These developments highlight the market's transition from a coastal-centric model to a more distributed, multi-hub structure.

Competitive Landscape

The United States biotechnology and pharmaceutical services outsourcing market exhibits moderately concentration among top players, while specialist providers maintain a significant presence. Large full-service CROs and CDMOs dominate complex outsourced programs in biologics, advanced therapies, and global clinical operations. However, sponsor procurement strategies, which involve multiple preferred partners, prevent extreme concentration, ensuring competitive dynamics where scale, capability breadth, quality, digital systems, and capacity availability are equally critical.

Integrated providers are gaining traction as sponsors seek to reduce handoffs across development, manufacturing, safety, and regulatory support. Thermo Fisher Scientific’s integrated CDMO and CRO model emphasizes faster program execution. Lonza, in March 2026, sharpened its focus on a pure-play CDMO model by divesting its Capsules and Health Ingredients business. Catalent strengthened its advanced therapy position in 2026 through partnerships, including late-phase AAV manufacturing for Elpida Therapeutics and iPSC-derived cell therapy work with GelMEDIX.

The BIOSECURE Act is altering competitive dynamics by redirecting outsourcing demand from certain Chinese biotechnology service providers to domestic or allied alternatives. This shift is particularly impactful in manufacturing and high-compliance services, where switching providers is operationally challenging and capacity remains tight. In February 2026, Charles River Laboratories sold CDMO sites in Tennessee, Maryland, and California, generating USD 143 million in 2025 revenue, signaling a pivot toward research models, scientific services, and early-phase work.

US Biotechnology And Pharmaceutical Services Outsourcing Industry Leaders

IQVIA

ICON plc

Charles River Laboratories International, Inc.

Samsung Biologics Co., Ltd.

Lonza Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ICON plc opened a new Clinical Research Unit in San Antonio, Texas, with satellite clinics in Houston and Lawrence, expanding its early-phase research capabilities in the U.S.

- May 2026: Catalent, Inc. partnered with Elpida Therapeutics for exclusive manufacturing of AAV9 gene therapies, strengthening its position in advanced therapy manufacturing.

- May 2026: Thermo Fisher Scientific collaborated with Nuvation Bio for U.S.-based manufacturing of IBTROZI, a therapy for ROS1-positive non-small cell lung cancer.

- April 2026: Parexel International acquired Vitrana to enhance automated safety reporting and signal detection across clinical programs from Phases I to IV.

- April 2026: Kincell Bio announced the expansion of its North Carolina facility to support late-stage and commercial cell therapy manufacturing by Q3 2026.

- March 2026: Catalent, Inc. partnered with GelMEDIX to develop and manufacture iPSC-derived cell therapies for ocular and retinal diseases.

US Biotechnology And Pharmaceutical Services Outsourcing Market Report Scope

As per the scope of the report, Biotechnology and pharmaceutical services outsourcing is the practice of contracting third-party organizations, such as Contract Research Organizations (CROs) or Contract Manufacturing Organizations (CMOs), to handle specific R&D, manufacturing, or regulatory functions. It allows life sciences companies to reduce costs, access specialized expertise, and scale operations.

The US biotechnology and pharmaceutical services outsourcing market is segmented by service type, drug type, development stage, end-user, and therapeutic area. By service type, the market includes contract research organization services, contract development and manufacturing organization services, analytical and bioanalytical services, regulatory affairs and quality assurance services, pharmacovigilance and drug safety services, market access and medical affairs services, and packaging, labeling, and serialization services. By drug type, the market is segmented into small molecules, large molecules, cell and gene therapies, vaccines, and other drug types. By development stage, the market is categorized into discovery and preclinical, Phase I, Phase II, Phase III, and Phase IV and post-marketing. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, medical device companies, academic and research institutions, and government and public health organizations. By therapeutic area, the market includes oncology, neurology, immunology, infectious diseases, cardiovascular diseases, rare diseases, metabolic disorders, and other therapeutic areas. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Contract Research Organization Services |

| Contract Development and Manufacturing Organization Services |

| Analytical and Bioanalytical Services |

| Regulatory Affairs and Quality Assurance Services |

| Pharmacovigilance and Drug Safety Services |

| Market Access and Medical Affairs Services |

| Packaging, Labeling and Serialization Services |

| Small Molecules |

| Large Molecules |

| Cell and Gene Therapies |

| Vaccines |

| Other Drug Types |

| Discovery and Preclinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV and Post-Marketing |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical Device Companies |

| Academic and Research Institutions |

| Government and Public Health Organizations |

| Oncology |

| Neurology |

| Immunology |

| Infectious Diseases |

| Cardiovascular Diseases |

| Rare Diseases |

| Metabolic Disorders |

| Other Therapeutic Areas |

| By Service Type | Contract Research Organization Services |

| Contract Development and Manufacturing Organization Services | |

| Analytical and Bioanalytical Services | |

| Regulatory Affairs and Quality Assurance Services | |

| Pharmacovigilance and Drug Safety Services | |

| Market Access and Medical Affairs Services | |

| Packaging, Labeling and Serialization Services | |

| By Drug Type | Small Molecules |

| Large Molecules | |

| Cell and Gene Therapies | |

| Vaccines | |

| Other Drug Types | |

| By Development Stage | Discovery and Preclinical |

| Phase I | |

| Phase II | |

| Phase III | |

| Phase IV and Post-Marketing | |

| By End User | Pharmaceutical Companies |

| Biotechnology Companies | |

| Medical Device Companies | |

| Academic and Research Institutions | |

| Government and Public Health Organizations | |

| By Therapeutic Area | Oncology |

| Neurology | |

| Immunology | |

| Infectious Diseases | |

| Cardiovascular Diseases | |

| Rare Diseases | |

| Metabolic Disorders | |

| Other Therapeutic Areas |

Key Questions Answered in the Report

What is the size of the US biotechnology and pharmaceutical services outsourcing market in 2026?

The US biotechnology and pharmaceutical services outsourcing market stands at USD 12.13 billion in 2026 and is projected to reach USD 15.56 billion by 2031 at a 5.10% CAGR.

Which service category leads revenue in pharmaceutical outsourcing in the United States?

Contract Research Organization services lead with 39.88% of revenue in 2025, supported by sustained Phase II to Phase IV trial activity.

Which service category is growing the fastest through 2031?

Contract Development and Manufacturing Organization services are the fastest-growing service type, with a projected 7.45% CAGR through 2031.

Why are cell and gene therapies increasing outsourcing demand?

These programs need specialized GMP suites, vector manufacturing, analytical testing, and chain-of-custody systems that many sponsors do not have internally.

Which therapeutic area generates the most outsourced spending?

Oncology leads with 38.55% of therapeutic-area revenue in 2025 because of its high trial volume and more complex operating requirements.

Which end users are driving future growth the most?

Biotechnology companies are expected to grow the fastest at a 6.9% CAGR through 2031, while pharmaceutical companies remain the largest end-user group with 51.34% of revenue in 2025.

Page last updated on: