United States Medical Billing Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

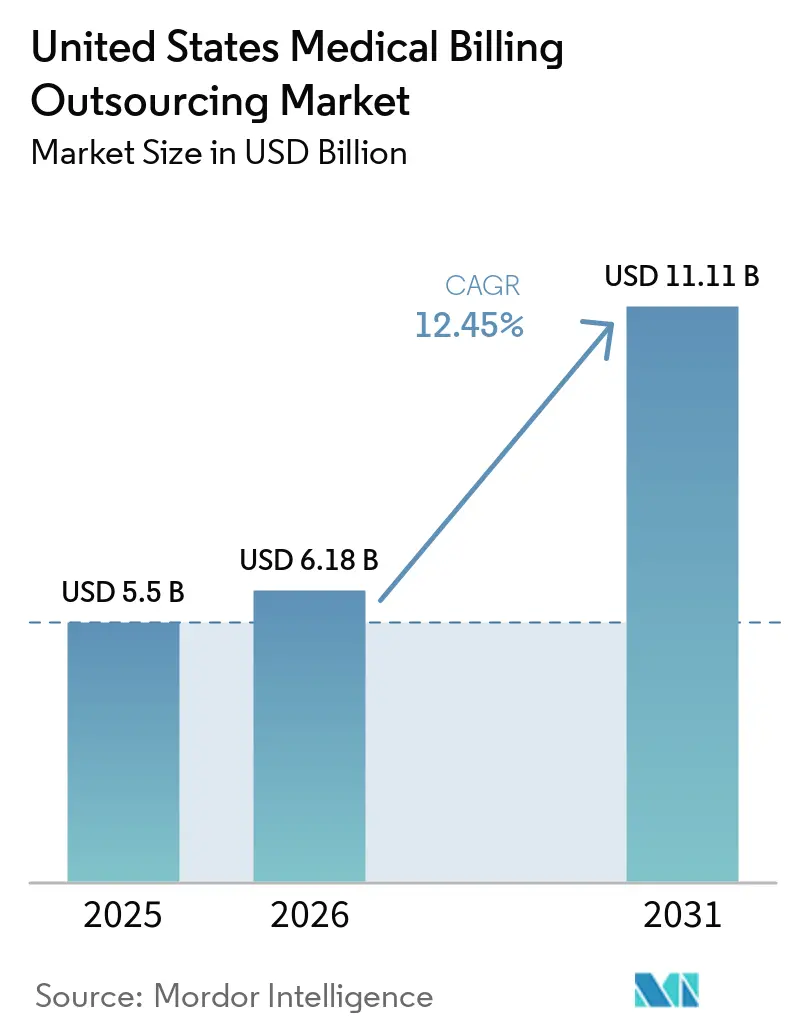

| Base Year Market Size (2025) | USD 5.5 Billion |

| Market Size (2026) | USD 6.18 Billion |

| Market Size (2031) | USD 11.11 Billion |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Medical Billing Outsourcing Market Analysis by Mordor Intelligence

The United States Medical Billing Outsourcing Market size was valued at USD 5.5 billion in 2025 and is estimated to grow from USD 6.18 billion in 2026 to reach USD 11.11 billion by 2031, at a CAGR of 12.45% during the forecast period (2026-2031).

The market is expanding because provider finances remain under sustained strain, with hospitals on the Kodiak Solutions platform losing more than USD 48 billion in net revenue to final denials and uncollected patient balances in 2025, up from USD 38.6 billion in 2024. That scale of leakage is harder to absorb in-house, especially for mid-sized systems that must manage multiple payer contracts, more prior authorization steps, and faster denial cycles at the same time. The United States medical billing outsourcing market is also being shaped by rising administrative complexity, wider use of AI in coding and denial prevention, and tighter payer oversight through audits and utilization controls. Demand remains strongest in the South and Southwest, where hospital consolidation and physician roll-up activity create the billing volume needed to support enterprise outsourcing contracts. The United States medical billing outsourcing market is therefore moving toward technology-augmented delivery, while cybersecurity standards, platform depth, and measurable collection outcomes are becoming more important than simple labor savings.

Key Report Takeaways

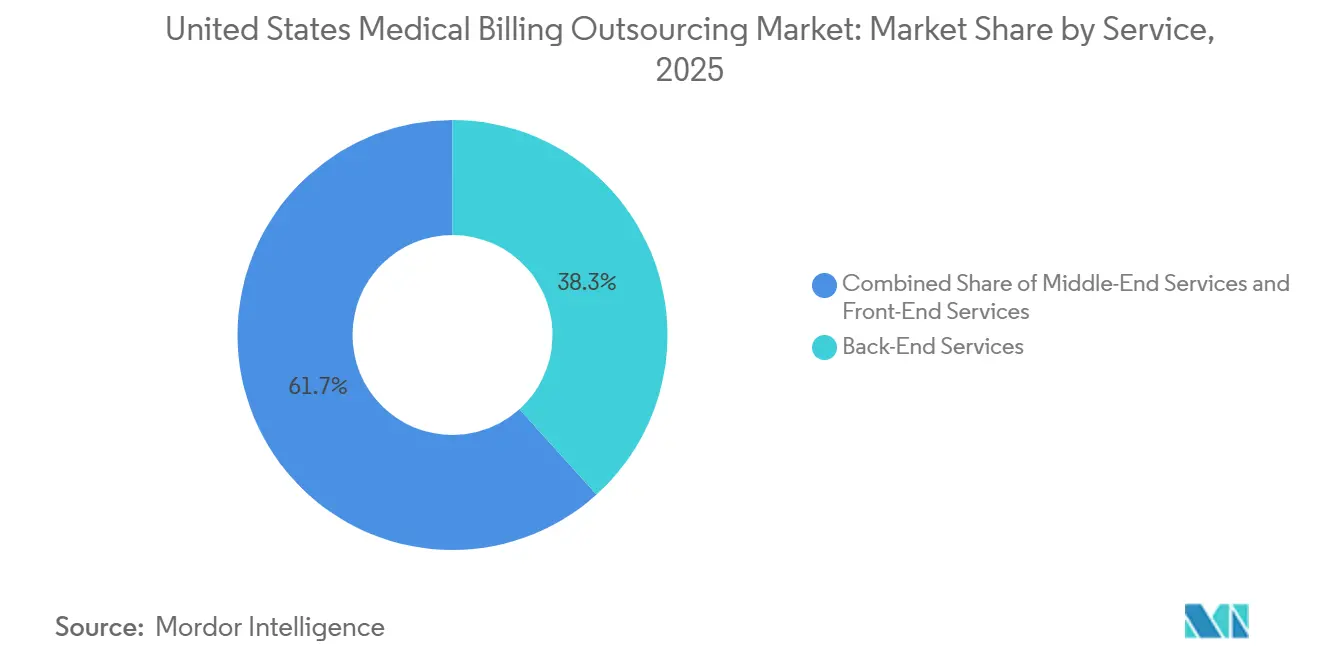

- By service, Back-End Services held 38.3% of the United States medical billing outsourcing market share in 2025, while Middle-End Services is projected to grow at a 13.4% CAGR through 2031.

- By outsourcing model, Full-Service Outsourcing accounted for 42.2% of the market in 2025, while Software-Enabled Managed Services is forecast to expand at a 14.5% CAGR through 2031.

- By deployment, Cloud-Based delivery captured 62.5% of the United States medical billing outsourcing market size in 2025, while Hybrid Cloud is projected to advance at a 13.3% CAGR through 2031.

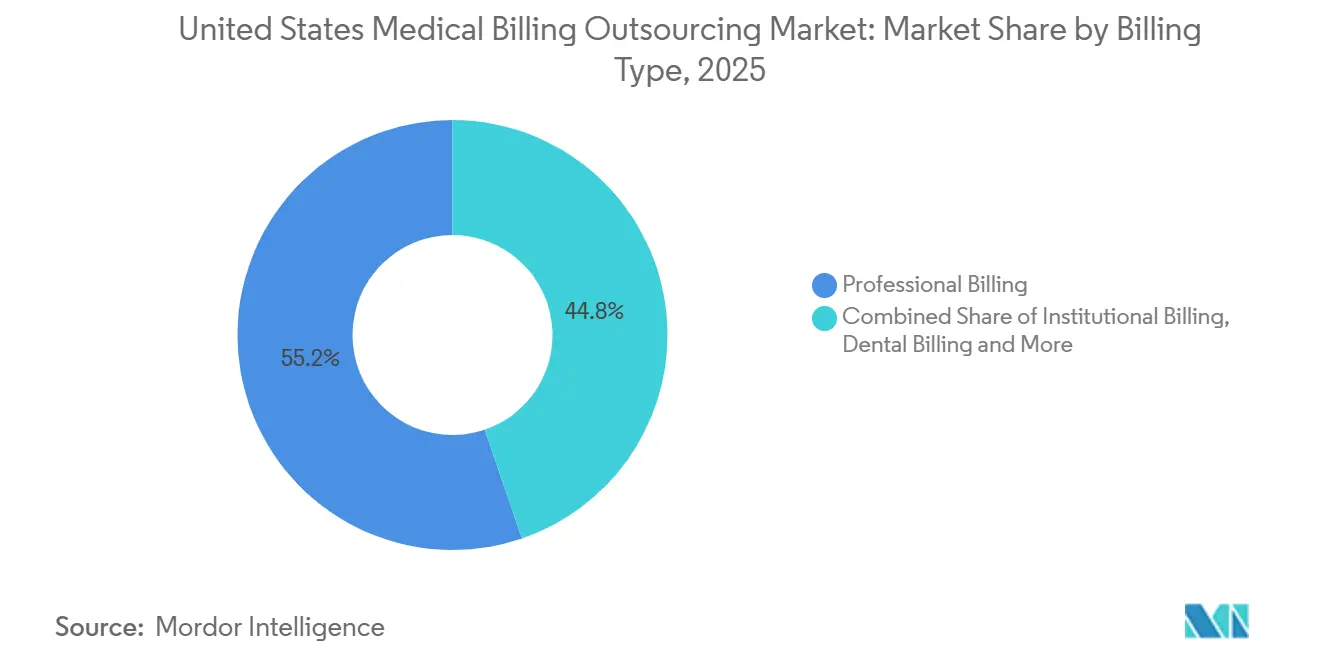

- By billing type, Professional Billing led with a 55.2% share in 2025, while Institutional Billing is expected to grow at a 13.4% CAGR through 2031.

- By end user, Hospitals and Health Systems represented 48.4% of the market in 2025, while Ambulatory Surgery Centers are forecast to grow at a 14.8% CAGR through 2031.

- By specialty, Primary Care held 24.2% of the market in 2025, while Behavioral Health is projected to expand at a 15.9% CAGR through 2031.

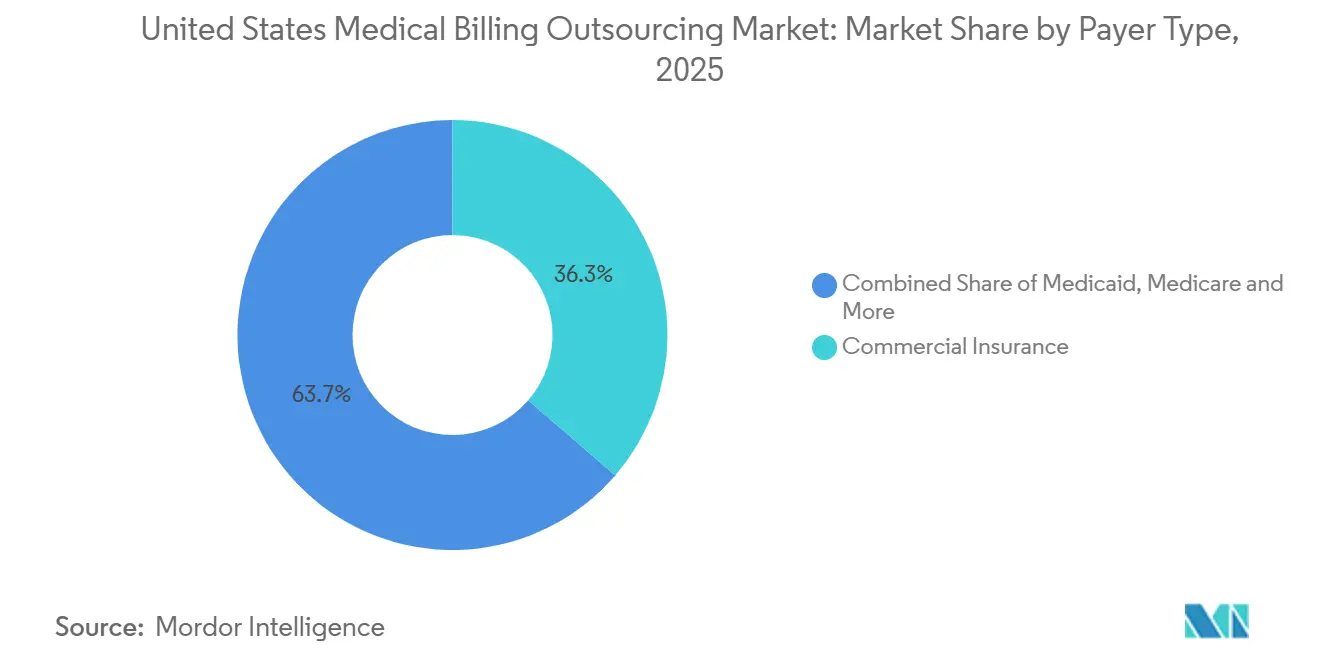

- By payer type, Commercial Insurance held 36.3% of the United States medical billing outsourcing market share in 2025, while Medicaid is projected to grow at a 14.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Medical Billing Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Claim Complexity And Documentation Burden | +2.8% | Global, concentrated in high-denial states including TX, FL, NC, OH | Short term (≤ 2 years) |

| Cost Pressure To Reduce In-House Billing Overhead | +2.5% | National, with early gains in Southeast and Midwest rural markets | Medium term (2-4 years) |

| Payer Denial Intensity And Audit Escalation | +2.2% | National, with heavier exposure in Medicare Advantage-heavy markets including FL, AZ, CA | Short term (≤ 2 years) |

| Shift To Value-Based Reimbursement Models | +1.8% | National, advanced in CMS Innovation Center pilot states including NY, MA, TN | Long term (≥ 4 years) |

| Prior Authorization Digitization Creating Outsourced Workflow Demand | +2.3% | National, with stronger exposure in large commercial insurance states | Short term (≤ 2 years) |

| Specialty-Specific Autonomous Coding Adoption | +1.5% | National, with early gains in tertiary care centers in Boston, Houston, Chicago | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Claim Complexity and Documentation Burden

The market continues to benefit from the widening gap between claim complexity and the capacity of internal billing teams. Providers are working through a steady stream of coding and documentation updates, which shortens the time available to prepare staff and hardens the risk of submission errors. Experian Health reported in 2025 that 41% of providers were facing denial rates of 10% or higher, while 50% identified missing or inaccurate data as the leading cause of those denials[1]Experian Health, “Experian Health’s 3rd Annual State of Claims Survey Finds Denials Still on the Rise Amid Escalating Challenges,” Experian PLC Newsroom, experianplc.com. HFMA also noted that payer-side automation is sending some denials within seconds of claim receipt, which makes slow manual correction loops less workable for providers that still depend on internal teams. In this setting, vendors that can maintain current coding logic, pre-submission claim edits, and continuous denial feedback loops are better placed to manage the operating pace now expected in the United States medical billing outsourcing market.

Cost Pressure to Reduce In-House Billing Overhead

The United States medical billing outsourcing market is also being pushed forward by the need to lower fixed billing overhead at a time when provider margins are already under pressure. Hospitals on the Kodiak Solutions platform lost more than USD 48 billion in net revenue to final denials and uncollected patient balances in 2025, which makes every avoidable billing error more expensive than it was a year earlier. Smaller practices and community-based provider groups face an even harder equation because compliance tools, staff training, analytics, and payer workflow updates do not scale efficiently at low claim volume. Outsourced vendors can spread the cost of automation, coding oversight, and denial analytics across a large client base, which changes the economics in their favor. The result is that the United States medical billing outsourcing market is increasingly supported by operating leverage, not just by labor substitution.

Payer Denial Intensity and Audit Escalation

The market is gaining support from the clear rise in payer denial pressure and audit scrutiny. MDaudit reported in 2025 that total at-risk amounts in payer audits rose 30%, hospital inpatient average denial amounts increased 14%, and Request for Information plus medical necessity denials for Medicare Advantage plans rose nearly fivefold[2]MDaudit, “MDaudit’s 2025 Benchmark Report Reveals Ongoing Acceleration of Payer Audits, Troubling Rise in Denials and Outpatient Coding Issues,” Access Newswire, accessnewswire.com. HFMA analysis of Kodiak Solutions data showed that the initial denial rate reached 11.7% through November 2025, while prior authorization and precertification denials rose to 1.6% from 1.5% in 2024. Higher payer automation has not reduced the need for external support, because it forces providers to respond with better payer-specific analytics, cleaner audit trails, and quicker appeal workflows. That is why denial management remains one of the strongest operating anchors for the United States medical billing outsourcing market.

Shift to Value-Based Reimbursement Models

The United States medical billing outsourcing market is also being lifted by the growing difficulty of managing fee-for-service and value-based payment workflows together. CMS finalized the CY 2026 Medicare Physician Fee Schedule with separate conversion factor tracks, including a higher path for Qualifying Alternative Payment Model participants, which ties billing accuracy more closely to quality-related payment outcomes[3]Centers for Medicare & Medicaid Services, “Calendar Year (CY) 2026 Medicare Physician Fee Schedule Final Rule (CMS-1832-F),” CMS Newsroom Fact Sheet, cms.gov. This creates more operational work around measure capture, documentation precision, coding integrity, and reconciliation across multiple payment models. Most in-house billing teams are not set up to manage Risk Adjustment Factor scoring, MIPS reporting, and episode-based payment workflows at the same time without creating bottlenecks elsewhere in the revenue cycle. Vendors that can link claims execution with quality reporting are therefore taking on a broader role in the United States medical billing outsourcing market than traditional billing firms did in earlier years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy And Cybersecurity Exposure | -1.5% | National, with clearinghouse concentration risk highest in TX and MN | Short term (≤ 2 years) |

| Legislative And Payer-Policy Volatility | -1.2% | National, with Medicaid policy sensitivity concentrated in expansion states including CA, NY, IL, OH | Medium term (2-4 years) |

| Large IDN Insourcing Through Enterprise RCM Platforms | -0.8% | National, concentrated in large academic IDNs in MA, NY, CA | Long term (≥ 4 years) |

| Payer Portal Restrictions On Automation And Offshore Access | -0.6% | National, with greater pressure in commercial-heavy states including TX, FL, OH, IL | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Exposure

Cybersecurity remains the clearest operating restraint on the United States medical billing outsourcing market. HHS stated that the Change Healthcare cybersecurity incident ultimately affected an estimated 192.7 million individuals, exposing how a centralized claims and payment infrastructure can create system-wide disruption when a single platform fails. Buyers now place much greater weight on security architecture, access controls, incident response readiness, and third-party assurance when evaluating vendors. This extends sales cycles and raises the cost of doing business, especially for vendors that rely on distributed delivery models or smaller compliance teams. The United States medical billing outsourcing market still has strong demand, but cybersecurity is now a core gatekeeper to contract growth rather than a background IT issue.

Legislative and Payer-Policy Volatility

Legislative and payer-policy volatility slows decision making in the United States medical billing outsourcing market because providers are reluctant to lock into multi-year scopes when reimbursement rules keep changing. CMS policy changes around prior authorization, interoperability, and physician payment design have increased the need for fast operating adjustments across billing teams and vendor platforms. State Medicaid rule shifts and the post-pandemic eligibility reset have also created uneven workflow spikes and reimbursement uncertainty for provider groups with large public payer exposure. In that setting, providers worry that outsourced contracts may not adapt quickly enough if scope, coding, or compliance requirements change in the middle of a contract term. This does not reverse adoption, but it does make flexibility and governance a more important buying factor in the United States medical billing outsourcing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Back-End Complexity Drives Near-Term Outsourcing Concentration

Back-End Services held 38.3% of the United States medical billing outsourcing market in 2025, making it the largest service layer because denial management, appeals, and accounts receivable follow-up carry the greatest financial urgency. Kodiak Solutions reported that hospitals on its platform lost more than USD 48 billion in net revenue to final denials and uncollected patient balances in 2025, while the median final denial rate rose to 2.7% from 2.5% in 2024. Those figures explain why provider buyers continue to treat recovery and follow-up capability as the most valuable part of an outsourcing contract. Front-End Services remains the second-largest tier, but its share faces gradual pressure as eligibility checks and basic intake tasks become easier to automate.

Middle-End Services is the fastest-growing service category, expanding at a 13.4% CAGR through 2031, because coding, clinical documentation improvement, and charge capture now sit closer to the point where reimbursement risk first appears. The United States medical billing outsourcing market is not reducing demand for middle-end specialists, because AI deployment still requires exception handling, validation, and payer-rule oversight. IKS Health’s April 2026 launch of an audit-ready autonomous coding engine showed how vendors are repositioning themselves as operational stewards of automation, not just as providers of manual coding labor. That same shift keeps middle-end services tied to long-term vendor contracts, since providers need both technology and audit governance. In practice, the United States medical billing outsourcing market is becoming more dependent on vendors that can connect clean coding, pre-bill review, and downstream denial prevention into one operating loop.

By Outsourcing Model: Full Ownership Dominant, Software-Led Managed Services Accelerating

Full-Service Outsourcing accounted for 42.2% of the United States medical billing outsourcing market in 2025, reflecting the appeal of single-vendor accountability for health systems that want one partner across intake, coding, billing, denial management, and collections. This model works best for organizations that need a full operating reset rather than narrow task support. It also fits providers that want clearer performance ownership when revenue leakage is already material and persistent. In the current United States medical billing outsourcing market, end-to-end scope remains the easiest way for large clients to standardize governance across multiple facilities and payer contracts.

Software-Enabled Managed Services is the fastest-growing outsourcing model, with a 14.5% CAGR through 2031, because buyers now expect more than staff augmentation. Vendors are layering AI, rules engines, analytics, and workflow orchestration into managed contracts so that pricing can be linked more closely to outcomes instead of transaction counts. Waystar’s acquisition of Iodine Software in October 2025 reinforced this direction by combining clinical intelligence and financial workflow capabilities under one platform strategy. R1 also signaled the same path when it moved to acquire Phare Health in 2025 to deepen automation in inpatient coding and pre-bill clinical documentation improvement. The United States medical billing outsourcing market is therefore shifting from broad labor coverage toward platform-led managed execution.

By Deployment: Cloud Dominance Established, Hybrid Architectures Capture Growth

Cloud-Based deployment represented 62.5% of the United States medical billing outsourcing market size in 2025, showing how firmly SaaS-based operating models have taken hold across billing and revenue cycle workflows. Providers favor cloud delivery because it reduces local infrastructure burden and makes software updates, analytics deployment, and security patching easier to manage at scale. This advantage is especially relevant when payer rule changes and coding logic updates need to move quickly across multiple facilities. Within the United States medical billing outsourcing market, cloud delivery has become the default path for vendors that want to support enterprise contracts with AI and analytics embedded.

Hybrid Cloud is the fastest-growing deployment mode, with a 13.3% CAGR through 2031, because large health systems still want to keep some clinical data and governance controls closer to core systems while shifting billing workflows outward. That architecture is well suited to academic medical centers and large IDNs that are modernizing revenue cycle operations without fully giving up local control. Ensemble Health Partners’ March 2026 partnership with Cohere shows why cloud-capable infrastructure matters, because the company is building an RCM-native large language model trained on operational data and deployed through AI agents in workflow settings. On-premise models continue to lose share, but they remain relevant where governance, ownership, or state-specific data rules limit broader migration. The United States medical billing outsourcing market is therefore not split between cloud and local systems in a simple way, because many of the fastest-growing accounts are choosing a mixed architecture instead.

By Billing Type: Professional Billing Scale Meets Institutional Billing Growth

Professional Billing held a 55.2% majority share in 2025, supported by the large volume of physician practice claims generated across primary care, multispecialty groups, and ambulatory settings. This remains the broadest transaction pool in the United States medical billing outsourcing market, which is why vendors continue to invest in physician-facing workflows and payer edits. CMS added more pressure at this level when it finalized the CY 2026 Medicare Physician Fee Schedule with separate conversion factor tracks that make documentation quality and reporting alignment more consequential for physician reimbursement. As billing rules become more layered, smaller physician groups gain fewer advantages from keeping these tasks fully in-house.

Institutional Billing is the fastest-growing billing type, advancing at a 13.4% CAGR through 2031, because hospital outpatient and inpatient reimbursement rules are facing stronger scrutiny from payers and auditors. MDaudit reported in 2025 that outpatient coding-related denials rose 26%, which supports the move toward specialist vendor support in hospital-linked billing environments. Laboratory and diagnostic billing, dental billing, and durable medical equipment workflows remain smaller but more specialized niches where coding precision directly affects collection timing and denial exposure. GeBBS Healthcare strengthened its position in one of those niches through its March 2026 acquisition of RND OptimizAR, a company focused on DME and home medical equipment billing. The United States medical billing outsourcing market continues to reward vendors that can combine high-volume professional claims capability with deeper skill in targeted specialty billing lines.

By End User: Hospitals Anchor Volume, ASCs Drive Margin-Led Growth

Hospitals and Health Systems accounted for 48.4% of the United States medical billing outsourcing market in 2025, which keeps them at the center of vendor revenue and contract design. Their size, payer mix complexity, and internal coordination needs make both full-service and co-managed revenue cycle structures commercially viable. This end-user group also feels the impact of denials most directly, because the absolute revenue at stake is much larger than it is for small practices or single-site providers. That is why the United States medical billing outsourcing industry continues to rely on hospital demand as its broadest base of contract value.

Physician Practices remain the second-largest end-user segment, but the faster growth story is in Ambulatory Surgery Centers, which are expected to expand at a 14.8% CAGR through 2031. ASC billing brings together modifier usage, implant cost coding, procedure-specific payer rules, and timing-sensitive claims handling, which makes specialized outsourcing more defensible than standard back-office support. Diagnostic Laboratories also sustain demand because local coverage decisions and documentation expectations can create steady compliance pressure. Dental Practices are drawing more specialized vendors as benefit complexity increases and generalist platforms prove less effective in that setting. Other end users, including behavioral health organizations and telehealth-focused providers, add a smaller revenue base but a much higher level of billing complexity per dollar of collections, which keeps them important to the United States medical billing outsourcing market.

By Specialty: Primary Care Volume Leads, Behavioral Health Redefines Urgency

Primary Care held 24.2% of specialty billing outsourcing in 2025, making it the largest specialty in the United States medical billing outsourcing market because of its broad patient base and recurring claims volume. Its importance is increasing, not decreasing, because primary care now sits closer to risk adjustment, quality capture, chronic care coding, and managed care reporting than it did in the past. Billing partners in this specialty need to understand both traditional fee-for-service claims and value-linked documentation demands. As a result, the United States medical billing outsourcing market still treats primary care as a volume anchor even while faster-growing specialties gain attention.

Behavioral Health is the fastest-growing specialty, with a 15.9% CAGR through 2031, because telehealth use, payer carve-out structures, and time-based billing rules create a difficult compliance environment for general billing teams. Valant launched a purpose-built behavioral health RCM solution in March 2026, which reflected growing recognition that this specialty needs more tailored workflow design than standard billing products usually provide. Radiology, orthopedics, cardiology, and oncology each retain meaningful billing demand, with oncology standing out because drug billing, evaluation and management services, and trial-related coding all interact in the same workflow. Emergency medicine also remains important because No Surprises Act compliance adds another layer of process discipline around reimbursement and patient responsibility. These conditions help explain why specialty-focused vendors are gaining relevance inside the United States medical billing outsourcing market.

By Payer Type: Commercial Insurance Dominates, Medicaid Carries Fastest Growth

Commercial Insurance held the largest payer-type share at 36.3% in 2025, which reflects the higher per-claim value and contract complexity attached to commercial billing work. That makes commercial claims one of the most valuable operating lines in the United States medical billing outsourcing market. Medicare remains the second-largest payer category, with Medicare Advantage drawing particular attention because denial frequency and audit intensity are elevated in that population. Kodiak Solutions data cited by HFMA showed that payer-side automation and denial activity remained a major concern in 2025, reinforcing the need for payer-specific billing expertise.

Medicaid is the fastest-growing payer segment, with a 14.6% CAGR through 2031, partly because managed care expansion adds eligibility, enrollment, and prior authorization complexity that is difficult for provider teams to absorb on their own. The post-pandemic unwinding period in 2024 and 2025 intensified that pressure in states with large Medicaid populations, especially where coverage changes created abrupt shifts in eligibility verification work. Workers’ Compensation remains smaller but operationally distinct because documentation, timing, and claim routing rules differ from mainstream medical claims. Self-Pay has also become more important to outsourcing decisions as patient financial responsibility rises and providers need better digital engagement to improve collection performance. These patterns show that the United States medical billing outsourcing market is not driven only by claim volume, because payer rule complexity can be just as important as scale.

Geography Analysis

The United States medical billing outsourcing market is most concentrated in the South and Southwest, where Texas and Florida generate large demand pools because they combine multi-hospital systems, high Medicare Advantage exposure, and active physician platform consolidation. These states also create the billing volume that supports enterprise-scale contracts and deeper vendor specialization. Post-pandemic Medicaid eligibility resets added further pressure in Texas and Florida, where enrollment changes and managed care workflows increased the need for outside support on verification and reimbursement operations. Georgia and North Carolina are also strengthening their role in the United States medical billing outsourcing market because they offer a growing mix of provider expansion, domestic delivery infrastructure, and favorable operating economics for outsourced service models. Taken together, the Southeast corridor is moving from a secondary support region into a core demand cluster for revenue cycle outsourcing.

The Northeast presents a different pattern, shaped by academic medical centers, complex payer contracting, and governance-heavy nonprofit systems that often prefer tightly structured vendor relationships. CMS interoperability and prior authorization rules have made data exchange standards more important in these markets, especially after the January 1, 2026 policy implementation point. Boston and New York remain more selective in using full outsourcing, but staffing gaps and the cost of AI investment are pushing more systems toward co-managed and software-enabled models. The Midwest operates as a value-oriented part of the United States medical billing outsourcing market, where lower labor costs and a large base of regional plans create a steady flow of transaction-heavy billing work.

Rural markets across the Great Plains, Appalachia, and the Deep South face a more urgent version of the same problem, because many critical access hospitals and rural clinics do not have enough billing staff to keep up with payer complexity. In those settings, outsourcing often functions as financial stabilization rather than as a pure efficiency program. This makes rural demand structurally sticky, even if contract sizes are smaller than they are in large urban systems. A second geographic shift is happening in delivery location rather than in end demand, as buyers show greater interest in nearshore models that offer time-zone alignment and bilingual support without the same level of regulatory concern tied to distant offshore setups. The United States medical billing outsourcing market is therefore spreading along two maps at once, one based on where provider demand is strongest and another based on where compliant service delivery can be scaled most effectively.

Competitive Landscape

The United States medical billing outsourcing market is moderately concentrated, with a visible upper tier that includes Optum, R1 RCM, Ensemble Health Partners, Waystar, and CorroHealth. These firms compete on platform breadth, automation depth, payer connectivity, and the ability to serve large health systems across multiple facilities and specialties. Beneath them, the market remains fragmented across hundreds of midsize, regional, and specialty-focused vendors. That long tail keeps pricing and specialization pressure alive, especially in behavioral health, dental, DME, and other focused billing categories. The United States medical billing outsourcing market therefore combines a scaled leadership group with a broad field of niche competitors.

Private equity and strategic capital continue to speed consolidation among the largest platforms. TowerBrook Capital Partners and Clayton, Dubilier & Rice completed the acquisition of R1 RCM in November 2024 for USD 8.9 billion, which showed the value investors place on automation-ready scale in revenue cycle operations. Waystar closed its acquisition of Iodine Software in October 2025, strengthening the link between clinical intelligence and financial workflow as a competitive differentiator. GeBBS Healthcare added another strategic example in March 2026 when it acquired RND OptimizAR to deepen its position in DME and home medical equipment billing.

Platform development is moving just as quickly as ownership change. Ensemble Health Partners partnered with Cohere in March 2026 to build an RCM-native large language model, showing how vendors are trying to embed workflow intelligence directly into operating systems instead of treating AI as a side tool. Innovaccer and IKS Health are also targeting the coding layer with more autonomous tools, which raises competitive pressure on labor-heavy legacy models. At the same time, the Change Healthcare incident has made security readiness a larger competitive filter, since HHS scrutiny after the breach raised expectations around resilience and governance. Over the next 3 years, the United States medical billing outsourcing market is likely to reward vendors that can prove measurable improvement in net collection performance while also meeting stricter security and interoperability expectations. That combination favors well-capitalized incumbents, but it still leaves room for focused challengers with strong specialty execution.

United States Medical Billing Outsourcing Industry Leaders

Optum Inc.

R1 RCM Inc.

Conifer Health Solutions LLC

Ensemble Health Partners

Omega Healthcare Management Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: R1 RCM announced the expansion of Phare OS, described as healthcare's first revenue management operating system, designed to help providers navigate payer complexity and margin pressure through integrated AI-driven automation across the full revenue cycle. The launch extends R1's strategy to move toward real-time claims adjudication.

- November 2025: CharmHealth announced its new CharmBillerPro platform. Completely redesigned to address the growing complexity of revenue cycle management, the platform now includes AI-driven automations and integrated payment solutions as well as several enhanced capabilities for highly efficient operations and collections.

United States Medical Billing Outsourcing Market Report Scope

As per the scope of the report, medical billing outsourcing is the process of contracting an external company or service provider to handle the medical billing functions of a healthcare practice or facility.

The United States medical billing outsourcing market is segmented by service into front-end services, middle-end services, and back-end services. By outsourcing model, the market is categorized into full-service outsourcing, selective function outsourcing, extended business office, co-managed revenue cycle, and software-enabled managed services. By deployment, the segmentation includes cloud-based, hybrid cloud, and on-premise. By billing type, the market is divided into professional billing, institutional billing, laboratory and diagnostic billing, dental billing, and durable medical equipment billing. By end user, the segmentation covers hospitals and health systems, physician practices, ambulatory surgery centers, diagnostic laboratories, dental practices, and other end users. By specialty, the market is segmented into primary care, emergency medicine, radiology, orthopedics, cardiology, oncology, behavioral health, and other specialties. By payer type, the market is categorized into commercial insurance, Medicare, Medicaid, workers’ compensation, and self-pay. For each segment, the market size and forecast are provided in terms of value (USD).

| Front-End Services |

| Middle-End Services |

| Back-End Services |

| Full-Service Outsourcing |

| Selective Function Outsourcing |

| Extended Business Office |

| Co-Managed Revenue Cycle |

| Software-Enabled Managed Services |

| Cloud-Based |

| Hybrid Cloud |

| On-Premise |

| Professional Billing |

| Institutional Billing |

| Laboratory and Diagnostic Billing |

| Dental Billing |

| Durable Medical Equipment Billing |

| Hospitals and Health Systems |

| Physician Practices |

| Ambulatory Surgery Centers |

| Diagnostic Laboratories |

| Dental Practices |

| Other End Users |

| Primary Care |

| Emergency Medicine |

| Radiology |

| Orthopedics |

| Cardiology |

| Oncology |

| Behavioral Health |

| Other Specialties |

| Commercial Insurance |

| Medicare |

| Medicaid |

| Workers' Compensation |

| Self-Pay |

| By Service | Front-End Services |

| Middle-End Services | |

| Back-End Services | |

| By Outsourcing Model | Full-Service Outsourcing |

| Selective Function Outsourcing | |

| Extended Business Office | |

| Co-Managed Revenue Cycle | |

| Software-Enabled Managed Services | |

| By Deployment | Cloud-Based |

| Hybrid Cloud | |

| On-Premise | |

| By Billing Type | Professional Billing |

| Institutional Billing | |

| Laboratory and Diagnostic Billing | |

| Dental Billing | |

| Durable Medical Equipment Billing | |

| By End User | Hospitals and Health Systems |

| Physician Practices | |

| Ambulatory Surgery Centers | |

| Diagnostic Laboratories | |

| Dental Practices | |

| Other End Users | |

| By Specialty | Primary Care |

| Emergency Medicine | |

| Radiology | |

| Orthopedics | |

| Cardiology | |

| Oncology | |

| Behavioral Health | |

| Other Specialties | |

| By Payer Type | Commercial Insurance |

| Medicare | |

| Medicaid | |

| Workers' Compensation | |

| Self-Pay |

Key Questions Answered in the Report

What is the 2031 outlook for medical billing outsourcing in the United States?

The United States medical billing outsourcing market is projected to reach USD 11.11 billion by 2031, rising from USD 6.18 billion in 2026 at a 12.45% CAGR over 2026-2031.

Why are hospitals turning more of the revenue cycle over to outside vendors?

A major reason is rising revenue leakage. Hospitals on the Kodiak Solutions platform lost more than USD 48 billion to final denials and uncollected patient balances in 2025, which increases the value of specialized denial management and follow-up.

Which service area is currently the largest?

Back-End Services led with a 38.3% share in 2025, reflecting strong demand for denial management, appeals handling, and accounts receivable recovery.

Which end-user group is growing the fastest?

Ambulatory Surgery Centers are projected to grow at a 14.8% CAGR through 2031 because their billing rules are specialized and margin pressure makes in-house staffing harder to justify.

What makes behavioral health such a fast-rising specialty?

Behavioral Health is forecast to expand at a 15.9% CAGR through 2031 due to telehealth use, time-based coding, and payer carve-out structures that general billing teams often struggle to manage well.

How is AI changing competition among vendors?

AI is shifting value away from basic transaction processing and toward coding automation, denial analytics, and workflow orchestration, which is why moves such as Waystar's Iodine deal and Ensemble's Cohere partnership matter.

Page last updated on: