Pharmaceutical Contract Sales Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

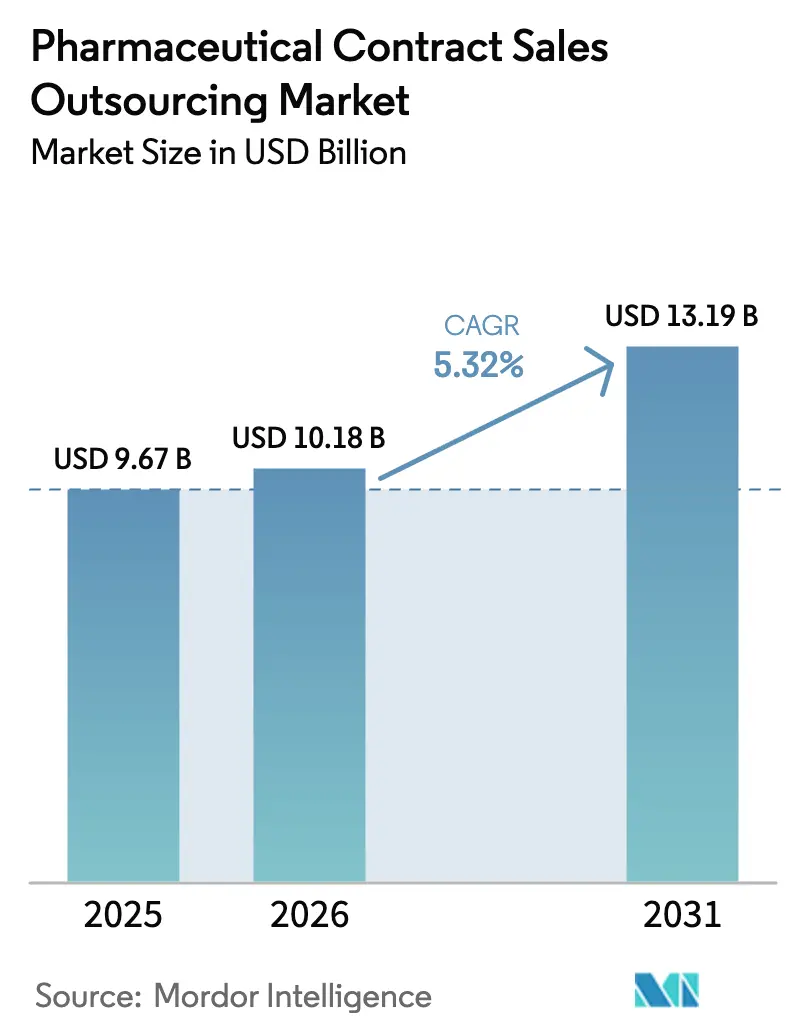

| Market Size (2026) | USD 10.18 Billion |

| Market Size (2031) | USD 13.19 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

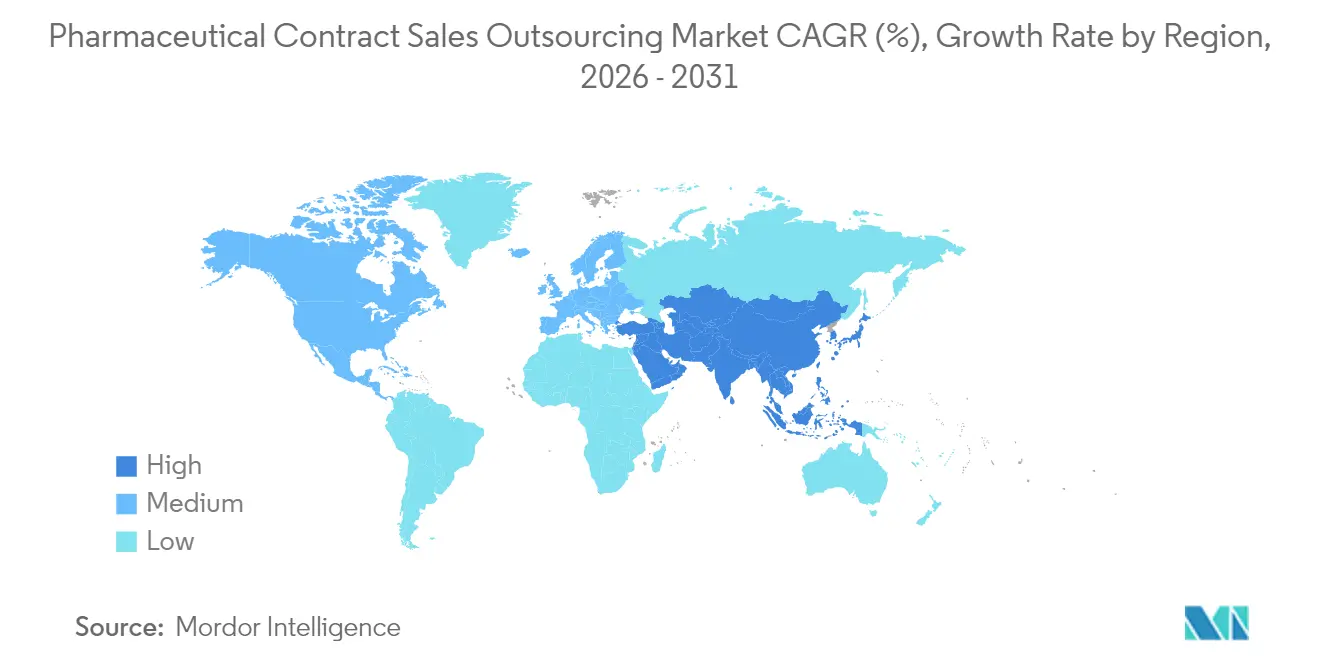

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Contract Sales Outsourcing Market Analysis by Mordor Intelligence

The pharmaceutical contract sales outsourcing market size was valued at USD 9.67 billion in 2025 and estimated to grow from USD 10.18 billion in 2026 to reach USD 13.19 billion by 2031, at a CAGR of 5.32% during the forecast period (2026-2031). The expansion reflects a strategic corporate shift toward variable-cost commercial models that preserve cash while sustaining physician reach. Strong demand for specialty detailing, escalating launch volumes in oncology and orphan drugs, and AI-driven territory design collectively propel growth. North America anchors global revenues through mature hybrid engagement models, whereas Asia-Pacific accelerates on the back of multilingual talent pools and surging clinical pipelines. Consolidation among global contract sales organizations (CSOs) continues, but nimble regional specialists remain competitive by pairing therapeutic depth with digital engagement tools.

Key Report Takeaways

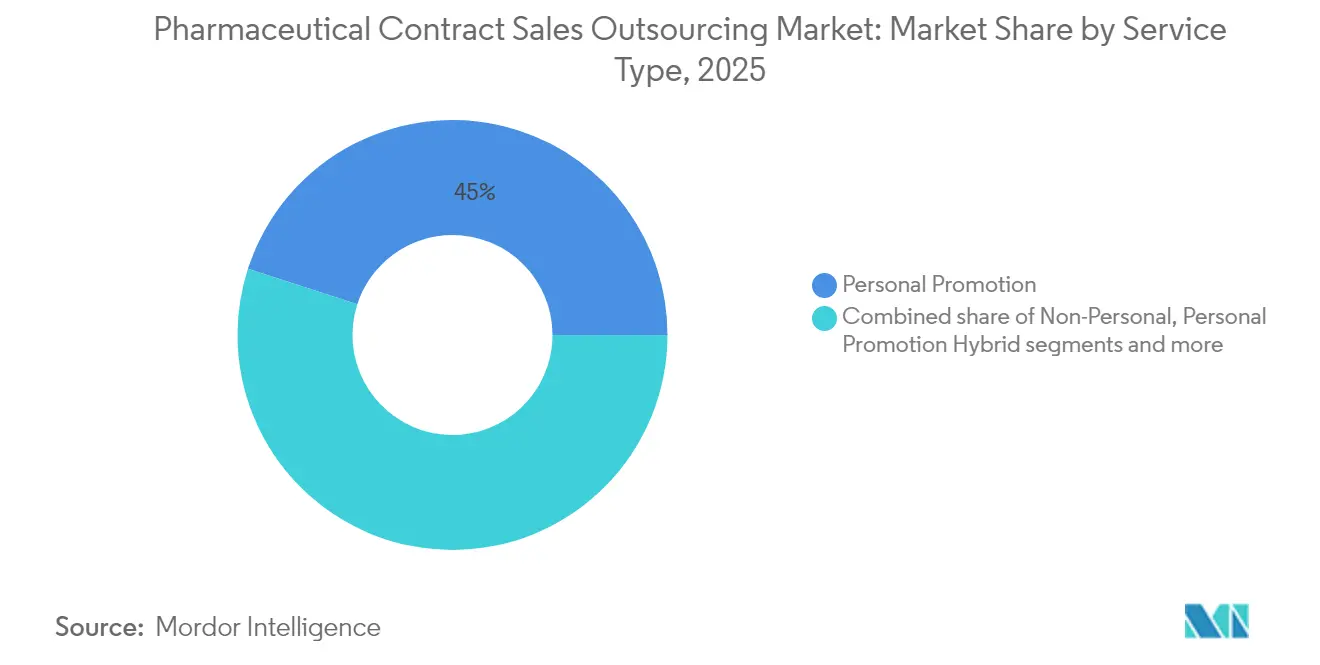

- By service type, personal promotion commanded 45.02% of pharmaceutical contract sales outsourcing market share in 2025, while the personal-promotion hybrid segment is projected to expand at a 6.78% CAGR through 2031.

- By therapeutic area, oncology generated 32.27% of 2025 revenue; neurology is the fastest-growing segment, advancing at a 6.12% CAGR between 2026-2031.

- By geography, North America led with 40.11% share in 2025; Asia-Pacific is forecast to post an 8.21% CAGR to 2031.

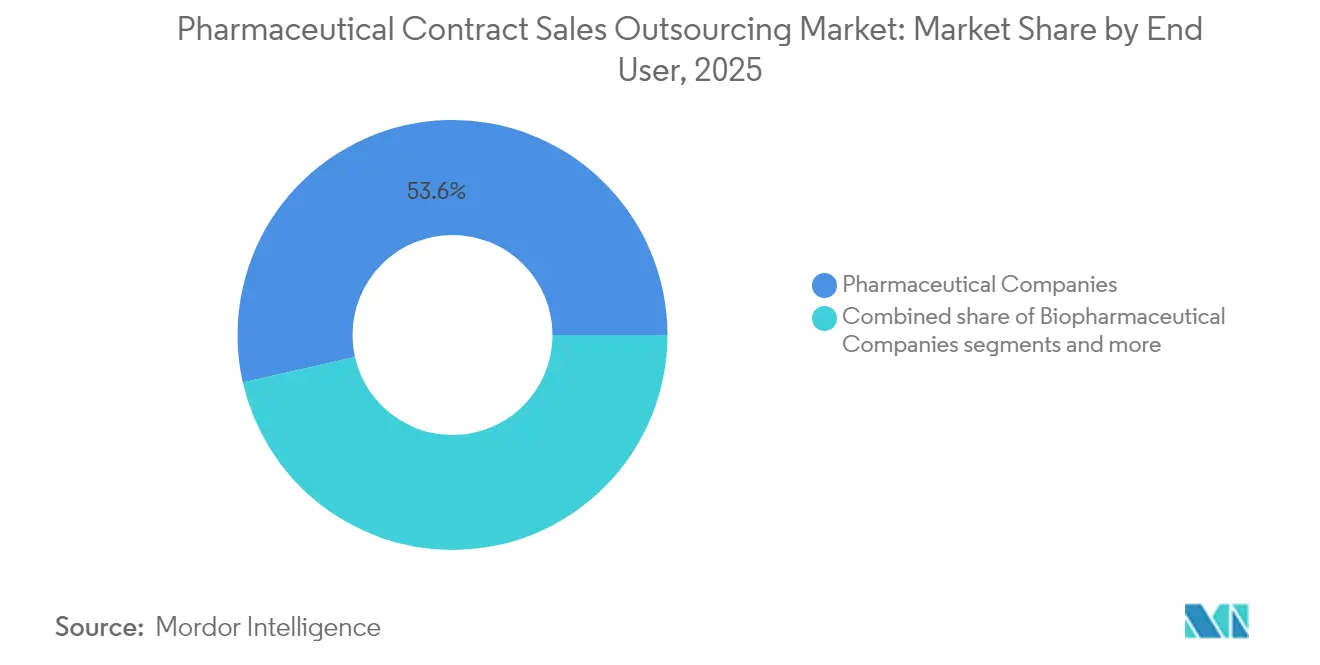

- By end user, pharmaceutical companies held 53.55% of 2025 revenue, whereas biopharmaceutical firms are forecast to grow at a 6.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Contract Sales Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Specialty & Orphan-Drug Launches Elevating Dedicated Oncology Detailing Demand | +1.4% | North America & Europe | Medium term |

| Increasing Pressure on Pharmaceutical Companies to Reduce Cost Associated with Sales | +1.7% | Global | Short term |

| APAC Pipeline Expansion Necessitating Multilingual KOL Access & Local Compliance | +1.1% | Asia-Pacific, with spillover to Middle East | Medium term |

| AI-Enabled Territory Optimisation Increasing CSO ROI & Winning Share | +0.8% | North America & Europe | Long term |

| Convergence of Medical Affairs with Commercial Creating Hybrid MSL–Sales Teams | +0.6% | North America | Medium term |

| Source: Mordor Intelligence | |||

Surge in Specialty & Orphan-Drug Launches Elevating Dedicated Oncology Detailing Demand

The global wave of specialty approvals is rendering generalized sales approaches obsolete. Complex therapies such as personalized cancer vaccines require in-depth scientific dialogue with key opinion leaders. Even large pharma companies are sourcing oncology-trained CSOs to fill this gap, evidenced by Novo Nordisk’s CagriSema program that demonstrated 22.7% weight-loss efficacy and triggered immediate demand for highly technical representatives. The U.S. FDA has cleared about 1,000 AI-enabled medical devices and logged 550 AI-based drug submissions, amplifying the knowledge burden on sales teams[1]Source: U.S. Food & Drug Administration, “Artificial Intelligence and Machine Learning (AI/ML)-Enabled Medical Devices,” fda.gov . CSOs that maintain certified oncology field forces therefore enjoy sustained volume growth, particularly across North American and European centers of excellence.

Increasing Pressure on Pharmaceutical Companies to Reduce Sales-Force Cost

Average drug-development spending has climbed toward USD 2.6 billion per asset, making fixed, multi-therapeutic field forces financially untenable. Outsourcing converts overhead into variable expense, trimming commercial budgets by 15-30% while preserving geographic coverage. CFOs have accelerated this shift ahead of upcoming Inflation Reduction Act pricing negotiations in the United States, widening the adoption window for CSOs capable of rapid deployment and flexible scaling.

APAC Pipeline Expansion Necessitating Multilingual KOL Access & Local Compliance

China has emerged as the preferred outsourcing hub for 17% of biopharma executives, supported by stronger intellectual-property safeguards and upgraded GMP plants. Simultaneously, Japan, India and Korea demand local-language engagement and market-specific pharmacovigilance reporting. CSOs with multilingual staffing and in-country regulatory know-how secure long-term contracts from multinational innovators seeking nimble market entry.

AI-Enabled Territory Optimisation Increasing CSO ROI & Winning Share

Machine-learning platforms now blend prescription data, claims, and demographic feeds to redesign territories in near-real time. Early users posted a 3.5% lift in engagement return, persuading more clients to mandate AI-ready partners. Next-Best-Action engines further personalise calls, raising high-value prescriber reach without head-count expansion. The result is a reinforcing cycle: higher ROI strengthens the case for outsourcing, expanding the pharmaceutical contract sales outsourcing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Framework on Marketing and Selling of Products | ~-0.8% | North America & Europe | Medium term |

| Oncology-Certified Rep Shortage Inflating Labour Costs | ~-0.6% | Global | Short term |

| Source: Mordor Intelligence | |||

Stringent Regulatory Framework on Marketing & Selling of Products

U.S. and EU regulators intensify scrutiny on promotional claims and financial transparency. The Inflation Reduction Act alone is projected to cut USD 288 billion in federal drug outlays, adding indirect commercial risk. CSOs must expand compliance management, driving up operating costs and limiting margin upside, especially for smaller providers.

Oncology-Certified Rep Shortage Inflating Labour Costs

The OECD foresees a shortfall of 1.2 million health professionals across Europe by 2030[2]Source: Organisation for Economic Co-operation and Development, “Health Workforce Projections,” oecd.org . Oncology reps, who require deep clinical training, are in especially short supply. Rising wages compress CSO profitability and dampen the cost advantage relative to an in-house team, creating a structural restraint on the pharmaceutical contract sales outsourcing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hybrid Models Reshape Engagement

Personal promotion dominated revenues with a 45.02% share in 2025, but the personal-promotion hybrid segment is forecast to outpace the overall pharmaceutical contract sales outsourcing market at a 6.78% CAGR to 2031. The hybrid model merges direct detailers with medical-education specialists, delivering scientific depth and promotional agility in a single visit. Oncology, immunology and neurology launches especially benefit because prescribers expect evidence-based conversations alongside commercial logistics. Pharmaceutical companies also employ hybrids to fine-tune engagement frequency, adding virtual touchpoints between in-person calls and thereby extending reach while keeping head-count flat.

Clients cite improved flexibility and risk-sharing as critical advantages. Outsourcing contract duration ranges from tactical vacancy management of six months to multi-year strategic alliances for full product portfolios. CSOs that integrate AI dashboards supply real-time KPIs, allowing sponsors to shift resources among segments without severance liability. These efficiencies help personal-promotion hybrids capture incremental share of the pharmaceutical contract sales outsourcing market despite mature personal-promotion offerings.

By Therapeutic Area: Oncology Leadership and Neurology Momentum

Oncology accounted for a commanding 32.27% of 2025 revenue, underscoring its complexity and physician information demands. The oncology segment captured the largest pharmaceutical contract sales outsourcing market size at USD 3.12 billion in 2025, reflecting widespread CSO deployment for precision medicine launches.

Neurology is projected to grow at 6.12% CAGR, the quickest among tracked specialties, driven by disease-modifying therapies for rare neurological disorders. Breakthrough molecules require representatives versed in biomarker interpretation and specialty distribution, capabilities CSOs can assemble faster than internal teams. Cardiovascular and metabolic franchises remain sizeable but slower growing; nevertheless, GLP-1 agonist success has added fresh momentum, prompting Novo Nordisk to expand outsourced teams via Ashfield Engage to support newly acquired production capacity.

By End User: Biopharmaceutical Companies Outpace Traditional Pharma

Pharmaceutical companies retained 53.55% revenue share in 2025 as they balance global portfolios with lean field operations. Yet biopharmaceutical innovators are forecast to expand sales outsourcing at a 6.38% CAGR, reflecting constrained commercial budgets and the urgency of swift market entry. This shift lifts the pharmaceutical contract sales outsourcing market size for the biopharma end-user segment to an estimated USD 3.41 billion by 2031.

Emerging cell- and gene-therapy developers frequently select CSOs to navigate ultra-small prescriber bases and high-science dialogues. Diagnostic and device firms, though smaller contributors, increasingly bundle instruments with therapeutic regimens, requiring integrated detailing strategies that seasoned CSOs can supply. The transition toward asset-light outsourcing continues to reshape overall spending patterns, solidifying the pharmaceutical contract sales outsourcing industry as a core component of launch planning.

Geography Analysis

North America contributed 40.11% of global revenue in 2025, reflecting its density of headquarters and technology-enabled engagement models. Robust hybrid adoption and AI-centric territory design keep the pharmaceutical contract sales outsourcing market on a steady mid-single-digit growth track through 2031. Companies also pursue advanced analytics to support Inflation Reduction Act compliance, reinforcing the need for sophisticated CSO partners capable of documenting value propositions during payer negotiations.

Asia-Pacific is the fastest-expanding region, advancing at an 8.21% CAGR from 2026-2031. China, India and Japan drive volume gains through accelerated R&D investments and favourable regulatory reforms. China already captures 17% of global outsourcing preference, a share expected to climb as domestic biotech funding rises. The requirement for local-language clinical conversations coupled with intricate pharmacovigilance frameworks renders external partners indispensable, enlarging the pharmaceutical contract sales outsourcing market across the region.

Europe remains strategically critical despite labour shortages and heightened promotional oversight. The OECD’s anticipated 1.2 million healthcare-professional shortfall intensifies talent scarcity, particularly in oncology. Yet anticipated European Medicines Agency approvals for 42 new medicines in 2025 sustain CSO demand. Providers that can marry scientific credibility with rigorous compliance protocols are well placed to capture incremental share even as rising labour costs temper margins.

Competitive Landscape

The pharmaceutical contract sales outsourcing market is moderately concentrated. IQVIA, Syneos Health and Ashfield Engage together steward the broadest global footprints, strengthened by end-to-end service portfolios and continual investment in AI analytics. Syneos Health’s 2025 launch of a Singapore hub exemplifies scale-plus-specialty strategy, providing oncology and rare-disease field teams for multinationals entering Southeast Asia.

Mid-tier competitors such as Amplity Health and EVERSANA carve niches through technology specialisation and therapeutic focus. EVERSANA’s AI-powered territory platform promises a 15% improvement in engagement effectiveness, differentiating its value proposition. Meanwhile, regional specialists like CMIC Group in Japan offer hybrid digital-and-traditional models tailored to cultural expectations, broadening the competitive fabric.

M&A activity remains brisk as providers seek scale to absorb compliance costs and secure scarce therapeutic talent. Accenture’s acquisition of Consus.Health in late 2024 expanded its ability to layer commercial outsourcing atop revenue-cycle optimisation services. The resulting environment rewards both global consolidators and agile niche experts, ensuring competitive intensity across segments of the pharmaceutical contract sales outsourcing market.

Pharmaceutical Contract Sales Outsourcing Industry Leaders

EVERSANA

Granard Pharmaceutical Sales & Marketing

Veeva Systems

The Medical Affairs Company (TMAC)

IQVIA Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce launched a Life Sciences Partner Network to supply CSOs with sector-specific CRM tools

- January 2025: EVERSANA unveiled an AI territory-optimisation engine that raised engagement efficiency in pilot projects.

Global Pharmaceutical Contract Sales Outsourcing Market Report Scope

Pharmaceutical contract sales outsourcing is the process of assigning a part of the company's sales process to a third party or external agency. It is usually done by pharmaceutical and biopharmaceutical companies that lack adequate resources like manpower or time to expand their sales process or decrease their marketing expenditure.

The pharmaceutical contract sales outsourcing market is categorized by service, end-users, and geography. By service, the market is segmented into personal and non-personal services. By personal service, the market is segmented into promotional sales teams, key account management, and vacancy management. By non-personal service, the market is segmented into medical affairs solutions, remote medical science liaisons, nurse/clinical educators, and other non-personal services. By end-users, the market is segmented into pharmaceutical companies and biopharmaceutical companies. For each segment, the market size is provided in terms of value (USD).

| Personal | Promotional Sales Team |

| Key Account Management | |

| Vacancy Management | |

| Non-Personal | Medical Affairs Solutions |

| Remote Medical Science Liaisons | |

| Nurse (clinical) Educators | |

| Other Non-Personal Services | |

| Personal PromotionHybrid (MSL & Medical Education Support) |

| Oncology |

| Cardiovascular Disorders |

| Metabolic Disorders (e.g., Diabetes) |

| Infectious Diseases |

| Neurology |

| Respiratory – Asthma & COPD |

| Orthopedic & Musculoskeletal |

| Rare & Orphan Diseases |

| Pharmaceutical Companies |

| Biopharmaceutical Companies |

| Medical Device & Diagnostics Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Personal | Promotional Sales Team |

| Key Account Management | ||

| Vacancy Management | ||

| Non-Personal | Medical Affairs Solutions | |

| Remote Medical Science Liaisons | ||

| Nurse (clinical) Educators | ||

| Other Non-Personal Services | ||

| Personal PromotionHybrid (MSL & Medical Education Support) | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular Disorders | ||

| Metabolic Disorders (e.g., Diabetes) | ||

| Infectious Diseases | ||

| Neurology | ||

| Respiratory – Asthma & COPD | ||

| Orthopedic & Musculoskeletal | ||

| Rare & Orphan Diseases | ||

| By End User | Pharmaceutical Companies | |

| Biopharmaceutical Companies | ||

| Medical Device & Diagnostics Firms | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the pharmaceutical contract sales outsourcing market?

The pharmaceutical contract sales outsourcing market stands at USD 10.18 billion in 2026 and is projected to reach USD 13.19 billion by 2031.

Which region is growing fastest?

Asia-Pacific is forecast to grow at an 8.21% CAGR during 2026-2031, driven by expanding pipelines and multilingual KOL engagement needs.

Why are hybrid MSL–sales teams gaining traction?

Hybrid teams combine scientific credibility with commercial agility, improving stakeholder trust and accelerating site-cycle times.

How is AI affecting contract sales outsourcing?

AI-enabled territory optimisation and Next-Best-Action analytics have provided early adopters a 3.5% ROI lift and are rapidly becoming standard requirements.

Page last updated on: